India Alkaline Battery Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Alkaline Battery Market Size, Share, Trends & Forecast (2026-2034)

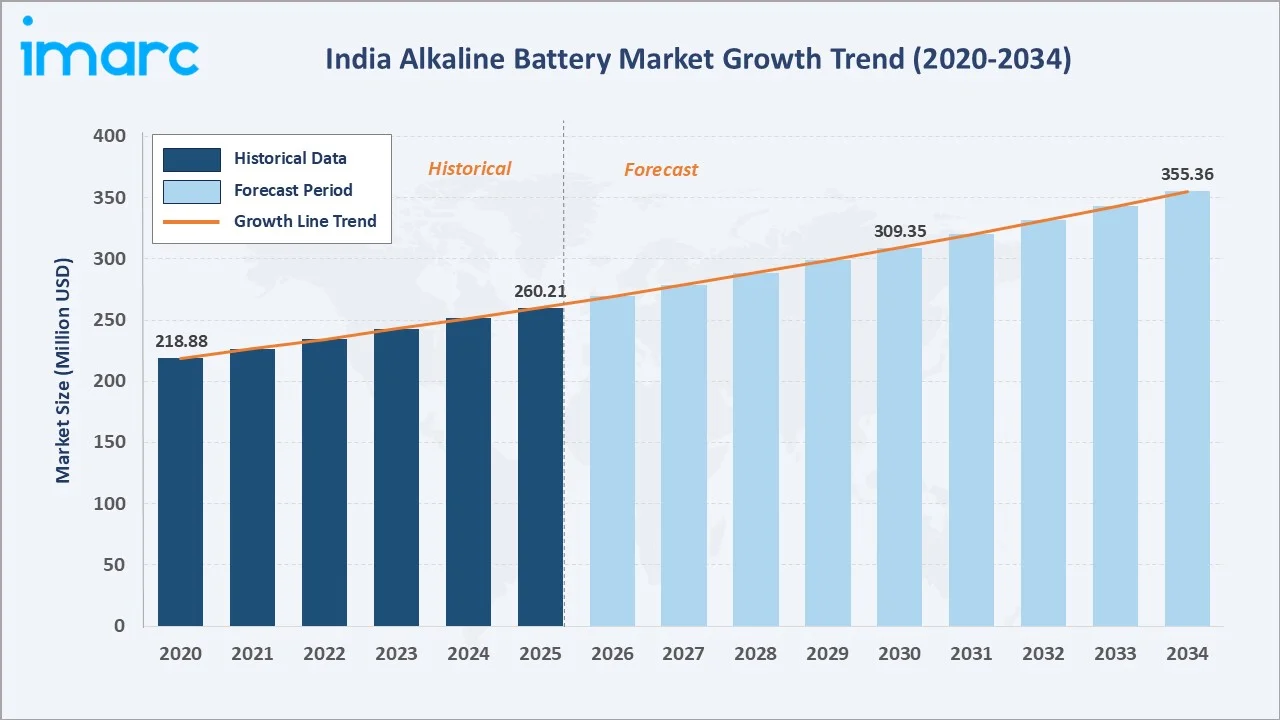

The India alkaline battery market reached USD 260.21 Million in 2025 and is projected to reach USD 355.36 Million by 2034, growing at a CAGR of 3.52% during 2026-2034. India's alkaline battery market is driven by the country's rapidly expanding consumer electronics ecosystem, with a large rural and semi-urban population still reliant on portable power solutions for torches, radios, remote controls, and wall clocks.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 260.21 Million |

|

Forecast Market Size (2034) |

USD 355.36 Million |

|

CAGR (2026-2034) |

3.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

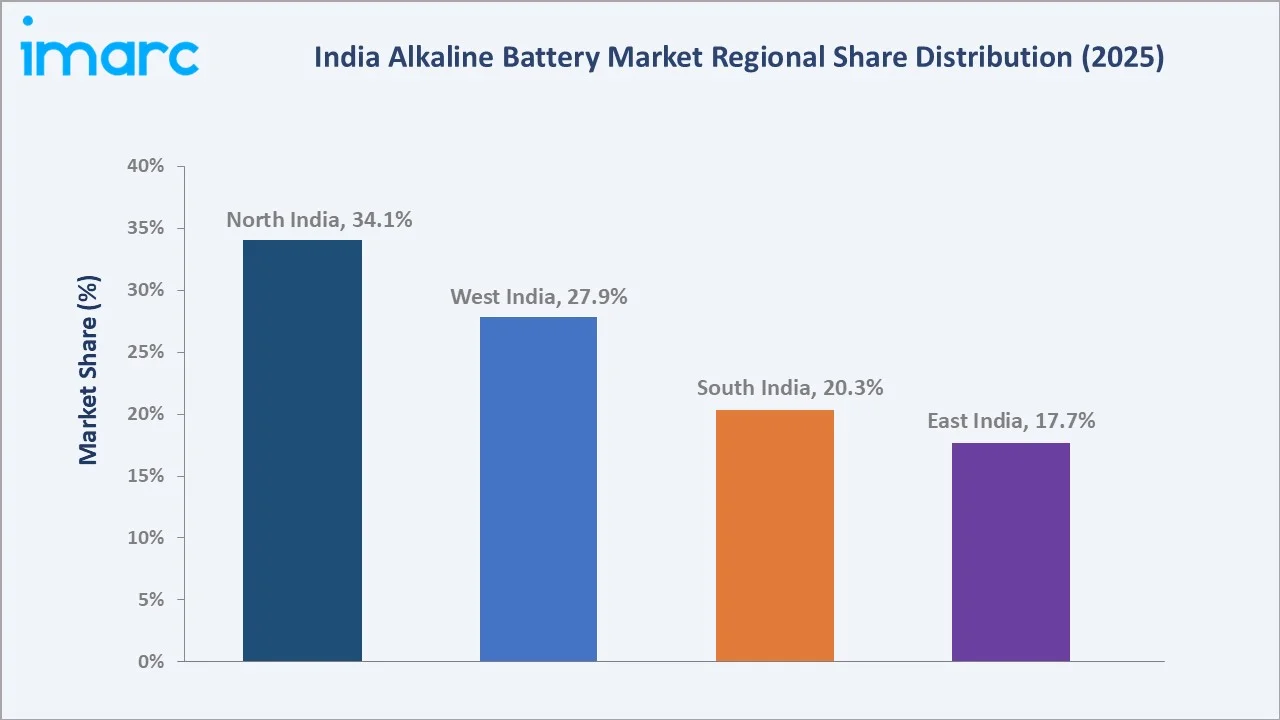

North India leads regionally with a 34.1% market share in 2025, driven by Delhi NCR's dense retail network and the region's large household consumption base. Primary batteries command a 62.3% share of the type breakdown, while consumer electronics retain the largest application share at 55.4%.

To get more information on this market, Request Sample

The India alkaline battery market is underpinned by three structural forces: the sustained transition from zinc-carbon to alkaline chemistry across India's mass-market battery segments; the growth of India's consumer electronics market projected to reach USD 300 billion by 2026, creating sustained demand for long-lasting portable power; and government policies including the Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell (ACC) battery storage, which is attracting manufacturing investment that will improve domestic alkaline battery supply chain efficiency and cost competitiveness.

Executive Summary

The India alkaline battery market is experiencing steady expansion, driven by rising consumer electronics penetration, rural electrification broadening the portable power market, and the systematic replacement of zinc-carbon batteries by alkaline chemistry across India's organized retail channels. The market reached USD 260.21 Million in 2025 and is forecast to reach USD 355.36 Million by 2034, growing at a CAGR of 3.52%.

Primary batteries dominate with a 62.3% share in 2025, encompassing standard AA, AAA, C, D, and 9V alkaline cells used in consumer electronics, toys, remote controls, torches, and wall clocks. Secondary alkaline batteries represent 37.7% and are growing fastest at approximately 5.8% CAGR, driven by the environmental sustainability imperative and cost optimization needs of commercial users deploying batteries at scale in retail point-of-sale systems, security devices, and industrial sensor applications.

Consumer electronics at 55.4% leads the application segment, followed by commercial at 29.8%. North India at 34.1% leads regionally. Leading vendors compete across the premium, mid-range, and value alkaline battery segments through brand investment, distribution expansion, and product innovation.

Key Market Insights

|

Insight |

Data |

|

Largest Battery Type |

Primary – 62.3% share (2025) |

|

Fastest Growing Type |

Secondary – ~5.8% CAGR (2026-2034) |

|

Largest Application |

Consumer Electronics – 55.4% share (2025) |

|

Fastest Growing Application |

Consumer Electronics – ~4.6% CAGR (2026-2034) |

|

Leading Region |

North India – 34.1% share (2025) |

|

Top Companies |

Eveready Industries India Limited, Panasonic Holdings Corporation, Duracell Inc., Indo National Limited, Geep Industries Pvt. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Primary batteries at 62.3% (2025) dominate as India's household battery consumption is overwhelmingly driven by disposable AA and AAA alkaline cells for remote controls, wall clocks, torches, and toys. Eveready Industries India Limited is equipped with five production lines and can manufacture 800 million AA and AAA batteries annually, which ensures primary alkaline availability across every tier of India's retail ecosystem.

- Secondary batteries at 37.7% (2025) share are expected to grow fastest over the forecast period as India's corporate and commercial users deploy rechargeable alkaline systems in security cameras, wireless keyboards, POS terminals, and IoT sensors. Growing environmental awareness among urban consumers is also driving household adoption of rechargeable alkaline alternatives to reduce battery waste.

- Consumer Electronics at 55.4% (2025) leads applications owing to India's consumer electronics market, a primary demand driver for alkaline batteries. The proliferation of smart home devices, gaming peripherals, Bluetooth speakers, and digital cameras requiring alkaline power is expanding consumption beyond traditional remote control and torch applications toward a broader device ecosystem.

- North India's 34.1% (2025) share reflects Delhi NCR's position as India's largest metropolitan consumer market, the region's dense modern retail penetration, and the significant industrial and institutional battery consumption from Uttar Pradesh's manufacturing belt and Punjab's agricultural equipment operations requiring portable power for irrigation control systems.

India Alkaline Battery Market Overview

Alkaline batteries utilize zinc powder as the anode, manganese dioxide (MnO₂) as the cathode, and potassium hydroxide (KOH) as the electrolyte, a chemistry that delivers 50–400% more energy density than zinc-carbon cells while maintaining stable voltage output throughout the discharge cycle. The India alkaline battery market encompasses standard cylindrical cells, prismatic cells, button cells, and specialty alkaline formats for medical devices, industrial sensors, and military applications.

India's battery market macroeconomic context is defined by the government's National Battery Recycling Framework under the Battery Waste Management Rules (2022), which mandates Extended Producer Responsibility for battery manufacturers and sets collection and recycling targets that are progressively tightening through 2026–2030. These regulatory requirements are creating a compliance moat for organized alkaline battery manufacturers with established collection programs while pressuring unorganized importers that lack recycling infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

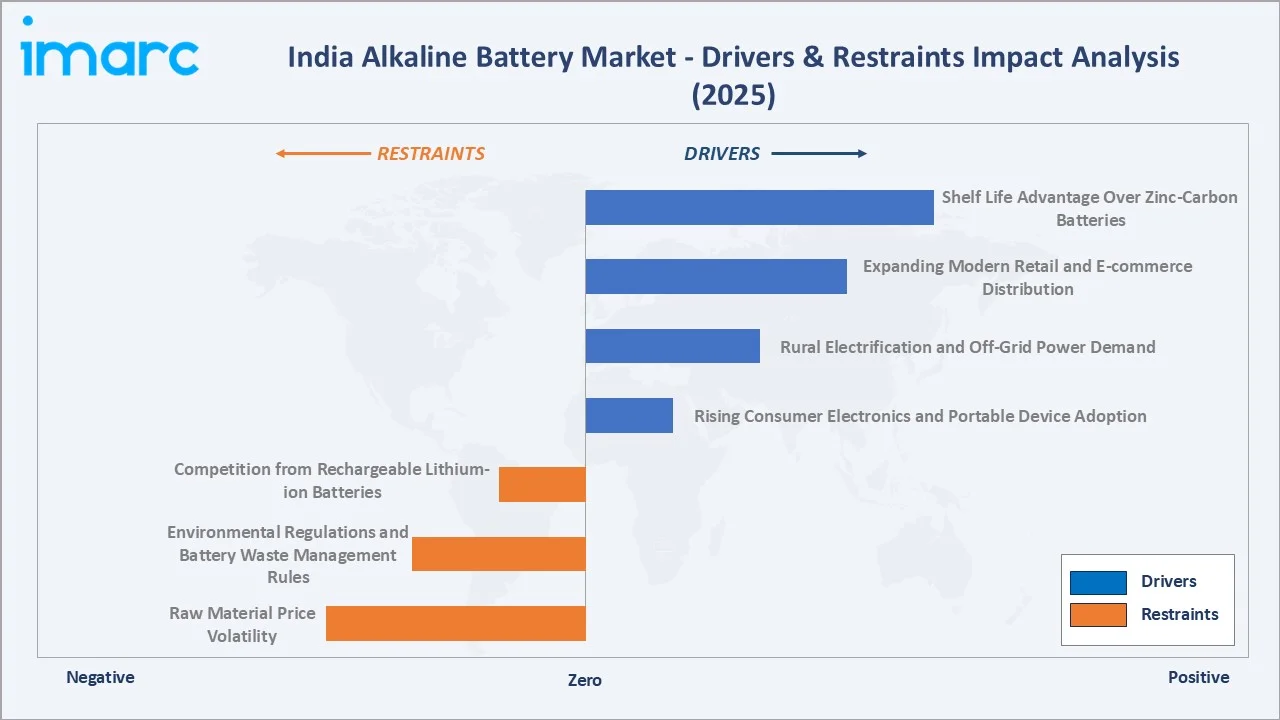

Market Drivers

- Rising Consumer Electronics and Portable Device Adoption: India's consumer electronics market is projected to reach USD 300 billion by 2026, with smartphones, smart TVs, digital cameras, gaming controllers, and smart home devices collectively driving demand for alkaline batteries.

- Rural Electrification and Off-Grid Power Demand: Despite 100% village electrification under the Saubhagya scheme, rural households, particularly in northern and eastern states, face unplanned supply interruptions lasting six hours or more per day, sustaining demand for torch batteries, transistor radio power, and lantern cells where alkaline batteries' superior performance in low-drain applications makes them the rural household's preferred choice.

- Expanding Modern Retail and E-commerce Distribution: India's organized retail penetration has grown from 15% to 25% of battery sales between 2020 and 2025, with D-Mart, Reliance Retail, and BigBasket creating high-visibility shelf placement for premium alkaline brands. E-commerce battery sales through Amazon, Flipkart, and JioMart have grown ~35% annually, democratizing access to international premium brands like Duracell and Panasonic across Tier 2 and Tier 3 cities.

- Shelf Life Advantage Over Zinc-Carbon Batteries: Premium alkaline batteries offer 5–10 year shelf lives versus 2–3 years for zinc-carbon alternatives, delivering compelling value to India's kirana store and wholesale distribution channel, where inventory management and battery returns for expired stock represent significant cost items.

Market Restraints

- Competition from Rechargeable Lithium-ion Batteries: USB-rechargeable lithium-ion AA battery alternatives at INR 300–500 per cell are increasingly competing with rechargeable alkaline systems at INR 150–200 per cell for smartphone accessories, portable speakers, and handheld gaming devices, where USB charging convenience aligns with consumer behavior.

- Environmental Regulations and Battery Waste Management Rules: Under the Battery Waste Management Rules, 2022, alkaline batteries are covered under EPR obligations, requiring producers to ensure proper collection, recycling, or refurbishment. Recyclers must demonstrate technical capability to process alkaline batteries safely and generate EPR certificates based on actual waste processed and recovered materials.

- Raw Material Price Volatility: Zinc price increase, along with MnO₂ supply constraints from China, creates input cost pressures that squeezed battery manufacturer margins by 3–5 percentage points. India's dependence on zinc imports and MnO₂ sourcing from Chinese suppliers creates structural raw material vulnerability that limits margin stability in competitive retail pricing environments.

Market Opportunities

- Smart Home and IoT Device Proliferation: India's smart home market is creating new demand for alkaline batteries in smart locks, doorbells, wireless sensors, remote controls, and baby monitors that require reliable, long-lasting power between charge cycles.

- Defense and Government Battery Procurement: India's defense modernization program creates dedicated demand for high-performance alkaline batteries in surveillance equipment, night-vision devices, communication gear, and field equipment deployed across extreme temperature environments from Himalayan glaciers to Rajasthan's desert terrain.

Market Challenges

- Consumer Price Sensitivity in Mass Market: India's mass-market battery consumer is highly price-sensitive. Alkaline AA batteries retail at INR 35–80 per cell versus INR 10–20 for zinc-carbon equivalents, creating a 3–4x price premium that constrains alkaline adoption among the low-income households in India's rural and semi-urban markets.

- Counterfeit Battery Problem: India's battery market suffers from significant counterfeiting, with counterfeit batteries estimated to represent 8–12% of branded alkaline battery volumes in unorganized retail channels. Counterfeit batteries deliver inferior performance that damages brand trust, creates safety risks from battery leakage and occasional swelling, and generates warranty returns that impose after-sales costs on genuine brand owners without corresponding revenue.

Emerging Market Trends

1. Eveready Industries' Jammu Manufacturing Expansion and Ultima Campaign

In April 2026, Eveready commissioned its INR 200 crore alkaline battery plant in Jammu, with an installed annual capacity of 456 million units. The facility will support domestic manufacturing, reduce import dependence, and serve both the Indian and export markets. Eveready's Ultima Alkaline Battery campaign was strengthened in April 2024 with a new brand ambassador and nationwide TV commercial campaign, creating the largest alkaline battery marketing push in India's history.

2. Battery Waste Management Rules Compliance Driving Industry Consolidation

The Battery Waste Management Rules (2022) mandate is creating compliance-driven market consolidation as smaller battery importers and unorganized manufacturers lacking EPR infrastructure exit the organized retail market. BIS mandatory certification requirements for alkaline batteries under IS 1653 are similarly eliminating sub-standard imports, creating a regulatory moat that benefits established organized players with existing compliance infrastructure.

3. E-commerce Democratizing Premium Alkaline Battery Access

Amazon India, Flipkart, and Blinkit are transforming alkaline battery distribution by making premium international brands accessible to consumers in 2,000+ Tier 2 and Tier 3 cities that previously had no physical retail access to premium alkaline products. E-commerce alkaline battery sales grew at approximately 35% CAGR between 2022 and 2025, with multipacks gaining adoption as price-conscious Indian consumers discover the per-cell cost economics of multipack purchasing that reduces the perceived premium versus zinc-carbon singles.

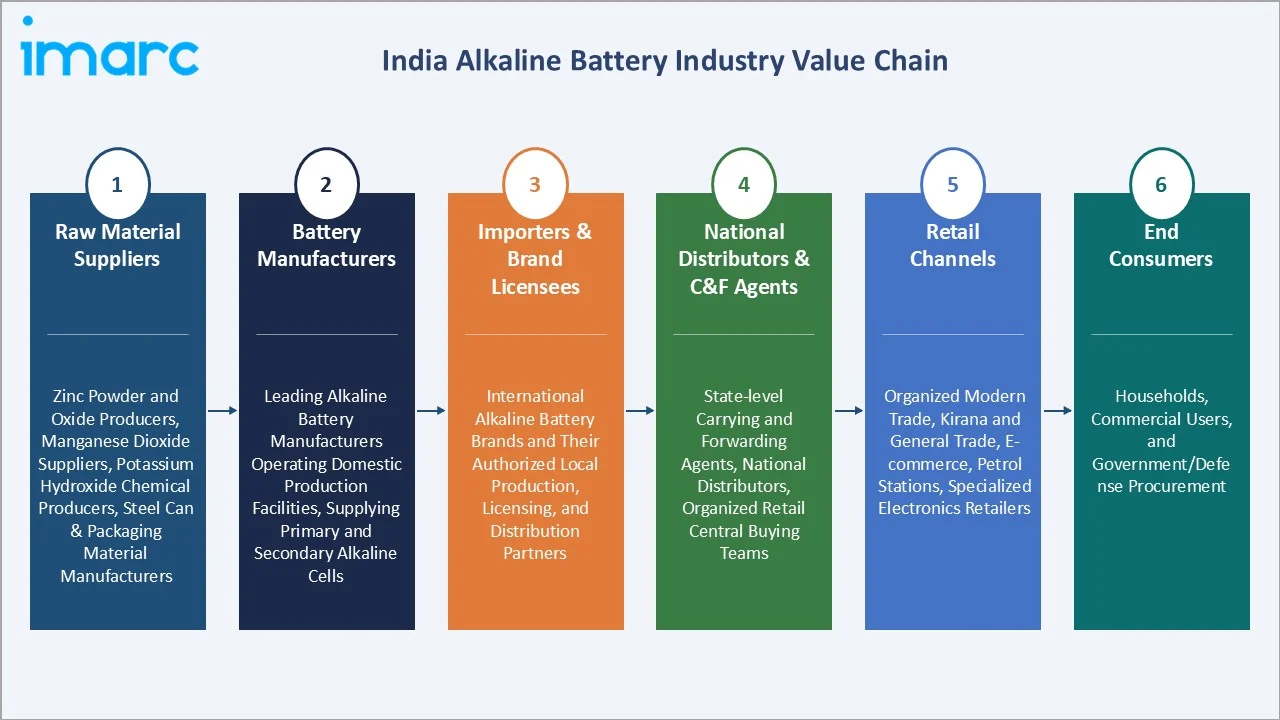

Industry Value Chain Analysis

India's alkaline battery value chain spans raw material supply through end consumer purchase, with each stage occupied by specialized suppliers, manufacturers, distributors, and retailers whose collective efficiency determines battery availability, product quality, and consumer price points.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Zinc powder and oxide producers, manganese dioxide suppliers, potassium hydroxide chemical producers, steel can & packaging material manufacturers |

|

Battery Manufacturers |

Leading alkaline battery manufacturers operating domestic production facilities, supplying primary and secondary alkaline cells |

|

Importers & Brand Licensees |

International alkaline battery brands and their authorized local production, licensing, and distribution partners |

|

National Distributors & C&F Agents |

State-level carrying and forwarding agents, national distributors, organized retail central buying teams |

|

Retail Channels |

Organized modern trade, kirana and general trade, e-commerce, petrol stations, specialized electronics retailers |

|

End Consumers |

Households, commercial users, and government/defense procurement |

Technology Landscape in the India Alkaline Battery Industry

Primary Alkaline Battery Technology

Primary alkaline batteries deliver 1.5V nominal voltage with superior energy density versus zinc-carbon, enabling 50–400% longer device runtimes depending on application drain rate. Eveready's Ultima series uses high-purity electrolytic grade MnO₂ to deliver 10-year shelf life and guaranteed leak-proof construction, key performance advantages in India's retail environment where slow inventory turnover can leave batteries on shelves for 2–3 years before purchase.

Rechargeable Alkaline Manganese (RAM) Battery Technology

Rechargeable alkaline manganese batteries serve India's commercial and institutional alkaline battery market, where lifecycle cost economics justify the 3–4x premium over disposable alkaline cells. They are mainly used in applications requiring frequent replacement cycles, such as meters, remotes, flashlights, medical devices, and industrial equipment, where reusability helps reduce long-term battery procurement and waste disposal costs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Primary |

62.3% |

2025 |

|

Application |

Consumer Electronics |

55.4% |

2025 |

|

Region |

North India |

34.1% |

2025 |

By Type

The primary battery segment dominates with a 62.3% share in 2025, reflecting India's consumer battery market structure, where household purchases of AA and AAA alkaline cells for remote controls, toys, clocks, and torches represent the vast majority of battery consumption by unit volume.

To access detailed market analysis, Request Sample

Secondary batteries represent 37.7% of the market share (2025) and are projected to grow fastest at approximately 5.8% CAGR, driven by commercial users' lifecycle cost optimization and growing urban consumer environmental consciousness. The rechargeable alkaline segment benefits from India's expanding smart device ecosystem, where wireless keyboards, gaming controllers, smart remote controls, and portable speakers require frequent battery replacement.

By Application

Consumer Electronics commands a 55.4% share in 2025, as approximately 85.5% of households owned at least one smartphone along with multiple battery-powered consumer electronics accessories, creating household battery consumption that drives 300+ million AA/AAA alkaline cell purchases annually in organized retail alone.

Commercial applications represent 29.8% of the market share (2025) and are expected to grow steadily as India's organized retail expansion drives consistent large-scale battery procurement by retail chains. The others segment at 14.8% encompasses government, defense, agriculture, and industrial applications that require specialized alkaline formats or ruggedized battery performance for extreme environment deployments.

Regional Market Insights

North India's market leadership (34.1%, 2025) reflects the region's combination of India's largest metropolitan consumer market, a dense organized retail network with high alkaline battery shelf visibility, and the significant institutional battery consumption from UP's manufacturing belt, Punjab's agricultural equipment sector, and Rajasthan and J&K's defense establishment procurement.

West India at 27.9% share (2025) is India's second-largest alkaline battery market, driven by Maharashtra's projected 12.93 crore population as of March 2026 and Gujarat's rapidly expanding manufacturing sector, where industrial and institutional battery consumption is growing at above-market rates.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

34.1% |

Delhi NCR's large consumer market and organized retail density; UP's manufacturing and industrial battery consumption; defense procurement from J&K and Uttarakhand establishments |

|

West India |

27.9% |

Maharashtra's large urban consumer base; Gujarat's growing manufacturing sector battery demand; expanding modern retail penetration in Tier 2 cities; strong e-commerce battery adoption |

|

South India |

20.3% |

Karnataka and Tamil Nadu's electronics manufacturing cluster; growing smart home adoption in Bengaluru and Hyderabad; strong organized retail penetration in Chennai, Bengaluru, and Hyderabad metro areas |

|

East India |

17.7% |

West Bengal's large consumer market; growing modern retail in Kolkata and Bhubaneswar; northeast India's reliance on torch batteries due to power supply gaps |

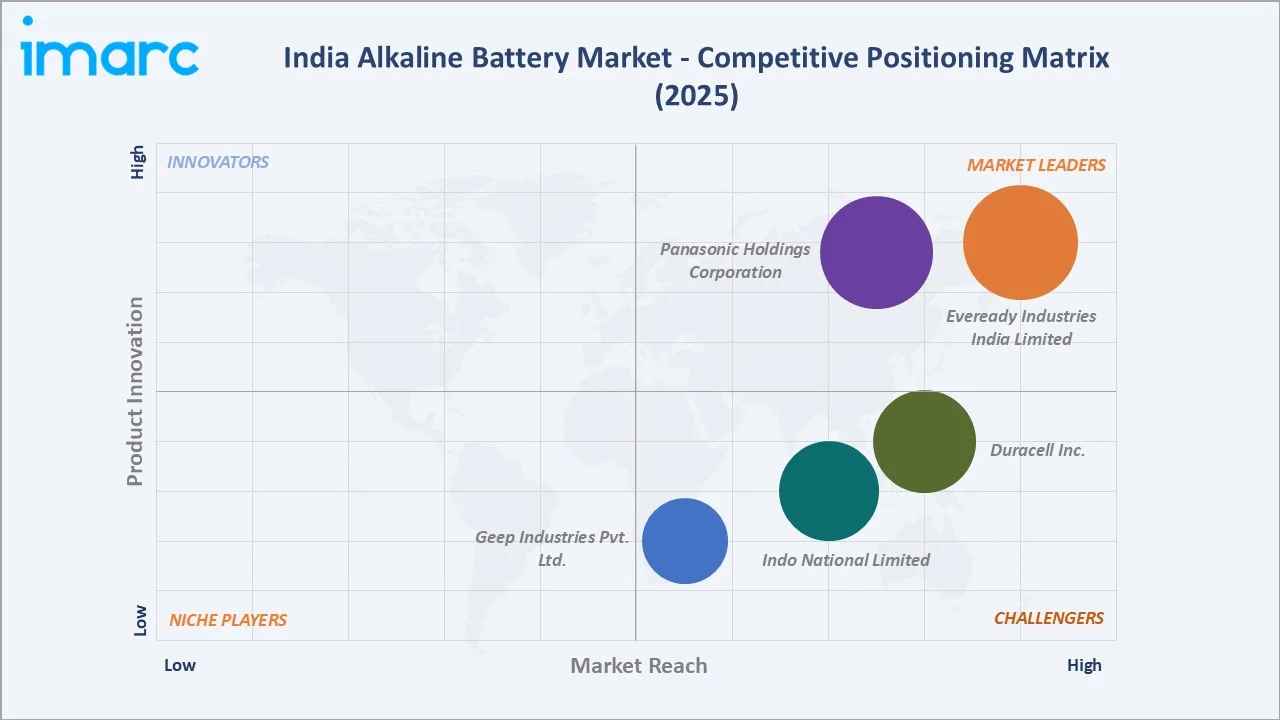

Competitive Landscape

The India alkaline battery market is moderately concentrated, with Eveready Industries India Limited leading the overall dry-cell segment with ~52% share. Market participants are expanding domestic manufacturing capacities and strengthening retail and e-commerce networks to capture growing demand.

|

Company Name |

Key Brands / Products |

Market Position |

Core Strength |

|

Eveready Industries India Limited |

Eveready Ultima Alkaline, Eveready Ultima Pro |

Market Leader |

Extensive domestic distribution network and strong retail channel penetration; broad alkaline battery portfolio spanning premium and mass-market segments |

|

Panasonic Holdings Corporation |

EVOLTA, Panasonic Alkaline |

Market Leader |

Strong presence across organized modern trade and institutional procurement channels; established domestic manufacturing base |

|

Duracell Inc. |

Duracell Ultra, Duracell |

Strong Challenger |

Growing domestic production capabilities; one of the leading premium alkaline brand positioning in the organized retail segment |

|

Indo National Limited |

Nippo Thor, Nippo Digi |

Strong Challenger |

Strong regional distribution network across South and West India; cost-efficient manufacturing supporting accessible price-point positioning |

|

Geep Industries Pvt. Ltd. |

Geep |

Challenger |

Established value-segment alkaline battery range; strong distribution reach in North India; institutional and commercial battery supply capabilities |

International brands continue to leverage technological advancements and premium positioning, while domestic manufacturers focus on affordability and deeper penetration into tier-II and rural markets. Product innovation, sustainability initiatives, and recycling compliance are emerging as important competitive differentiators in the industry.

Key Company Profiles

Eveready Industries India Limited

Eveready Industries India Limited is one of India's largest dry-cell battery manufacturers and the dominant force in India's alkaline battery market. The company’s brand portfolio serves the full spectrum of India's battery market from ultra-premium to value segments.

- Product Portfolio: Eveready Ultima Alkaline (AA, AAA, C, D, 9V) and Eveready Ultima Pro.

- Recent Developments: In April 2026, Eveready commissioned its ₹200 crore alkaline battery plant in Jammu, with an annual installed capacity of 456 million units. The facility will support India’s shift toward high-performance batteries, reduce import dependence, and serve export markets.

- Strategic Focus: Jammu facility scale-up for cost-competitive premium alkaline production; rural distribution deepening for Ultima alkaline penetration; Battery Waste Management Rules compliance program expansion.

Panasonic Holdings Corporation

Panasonic Holdings Corporation’s subsidiary Panasonic Energy India Co. Ltd. operates one of India's largest domestic alkaline battery manufacturing facilities and serves the premium end of India's consumer battery market.

- Product Portfolio: Panasonic EVOLTA Premium Alkaline (AA, AAA, C, D, 9V), and Panasonic Alkaline.

- Recent Developments: For FY2026 (ended March 31, 2026), Panasonic Holdings Corporation reported consolidated revenue of JPY 8,048.7 billion (~JPY 8.05 trillion) and net profit attributable to shareholders of about JPY 189.5 billion.

- Strategic Focus: Smart home IoT battery demand capture; e-commerce channel expansion; premium segment share growth; EPR compliance leadership as a brand differentiator in organized retail.

Indo National Limited

Indo National Limited operates under the 'Nippo' brand. Indo National's strategic focus on the value-premium alkaline segment has made Nippo Alkaline the preferred choice for price-conscious premium battery buyers in South India and the growing Maharashtra market.

- Product Portfolio: Nippo Thor Alkaline (AA, AAA) and Nippo Digi Alkaline.

- Recent Developments: In May 2026, Indo National Limited launched Nippo THOR Max, entering the premium alkaline battery category in India. The launch strengthens Nippo’s portfolio beyond conventional dry-cell batteries and targets demand from high-drain devices such as toys, remotes, clocks, flashlights, and electronic gadgets.

- Strategic Focus: Nippo Thor premium-value alkaline market share capture; North and West India distribution expansion; modern trade and e-commerce channel investment; alkaline battery innovation for smart home and IoT applications.

Market Concentration Analysis

The India alkaline battery market is moderately concentrated, with established players such as Eveready Industries India Limited, Duracell Inc., and Indo National Limited competing on brand strength, distribution reach, and product performance.

Established manufacturers are increasingly focusing on premiumization, higher-performance alkaline offerings, and e-commerce penetration to capture growing demand from smartphone accessories, gaming devices, smart home products, and other high-drain electronic applications. While a few major brands dominate organized retail channels, emerging domestic manufacturers and private-label offerings are gradually increasing competitive pressure in value-oriented market segments.

Investment & Growth Opportunities

Fastest Growing Segments

Secondary rechargeable alkaline batteries (~5.8% CAGR), consumer electronics applications (~4.6% CAGR), e-commerce battery distribution (~35% CAGR), and smart home IoT alkaline applications (~20% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address INR 1,500+ crore (~USD 180 million) in incremental market opportunity within India's alkaline battery ecosystem by 2030.

Emerging Market Expansion

India's semi-urban and rural markets represent the most significant underpenetrated alkaline battery growth opportunity. Alkaline penetration in rural India is estimated at just 12–18% of total dry-cell battery consumption versus 55–65% in metro markets, with the remaining rural consumption dominated by low-cost zinc-carbon cells.

The rural alkaline market development opportunity is estimated at USD 40–55 million annually by 2030, as rising rural incomes, expanding mobile and consumer electronics device penetration, and organized retail deepening progressively convert rural zinc-carbon buyers to alkaline chemistry.

Northeast India and Jammu & Kashmir represent high-potential emerging sub-markets with structurally elevated alkaline battery demand driven by persistent power supply gaps, defense sector procurement, and tourism-driven consumer electronics device usage. States including Assam, Meghalaya, Manipur, and Tripura are experiencing rapid mobile phone and consumer electronics penetration that is driving first-time alkaline battery demand among households previously relying on zinc-carbon cells.

Government and Policy Investment Trends

- The Battery Waste Management Rules (2022) and the Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell storage are creating favorable conditions for domestic alkaline battery manufacturers to invest in capacity expansion and technology upgrades.

- India's electronics manufacturing PLI is creating downstream demand for alkaline batteries in assembled consumer electronics products. India-made phones, tablets, and IoT devices incorporated into the domestic supply chain will generate device-bundled alkaline starter battery demand, creating a new high-volume, low-acquisition-cost battery placement channel for organized manufacturers.

Future Market Outlook (2026-2034)

The India alkaline battery market is positioned for steady, sustained expansion through 2034. From a base of USD 260.21 Million in 2025, the market is projected to reach USD 355.36 Million by 2034, representing total incremental value creation of USD 95.15 million at a CAGR of 3.52%.

This moderate growth reflects the market's maturity in urban India, where alkaline penetration is already high, offset by the significant growth opportunity in rural India's zinc-carbon to alkaline conversion, the expanding commercial application segment, and the emergence of rechargeable alkaline as a mainstream urban consumer product.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including battery manufacturers, national distributors, modern trade category managers, e-commerce marketplace sellers, retail chemists, and kirana battery suppliers, and government battery waste management officials across North, West, South, and East India.

Secondary Research

Secondary research encompassed company annual reports, BIS battery certification databases, Ministry of Environment Battery Waste Management Rules compliance reports, India Retail Report battery category data, and industry publications (Battery India, Electronics For You, IBEF Electronics Sector Report).

Forecasting Models

Market size estimations incorporated India consumer electronics market growth projections, per-capita battery consumption trajectories, alkaline penetration rate modeling versus zinc-carbon, and vendor revenue and capacity disclosures. A base-case CAGR of 3.52% reflects consensus estimates validated against vendor capacity expansion plans, retail battery category buyer forecasts, and India's consumer electronics market growth trajectories from FY2020 to FY2025.

India Alkaline Battery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Primary, Secondary |

| Applications Covered | Consumer Electronics, Commercial, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Eveready Industries India Limited, Panasonic Holdings Corporation, Duracell Inc., Indo National Limited, Geep Industries Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India alkaline battery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India alkaline battery market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India alkaline battery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Alkaline Battery Market Report

The India alkaline battery market reached USD 260.21 Million in 2025 and is projected to reach USD 355.36 Million by 2034.

The market is expected to grow at a CAGR of 3.52% during 2026-2034, driven by consumer electronics adoption, rural alkaline penetration, and expanding commercial applications.

North India leads with a 34.1% share in 2025, driven by Delhi NCR's large consumer market, UP's industrial consumption, and defense procurement from the northern establishment.

Primary batteries dominate with a 62.3% share in 2025, reflecting household consumption of disposable AA and AAA alkaline cells for consumer electronics, torches, toys, and remote controls.

Consumer electronics hold the largest share at 55.4%, encompassing TV/AC remote controls, gaming controllers, digital cameras, wireless peripherals, and smart home sensors across India's expanding consumer electronics market.

Some of the key players include Eveready Industries India Limited, Panasonic Holdings Corporation, Duracell Inc., Indo National Limited, and Geep Industries Pvt. Ltd.

Secondary batteries are growing at ~5.8% CAGR because commercial users' lifecycle cost optimization, urban consumers' environmental consciousness, and the proliferation of smart home devices requiring frequent battery replacement are driving adoption of rechargeable alkaline alternatives.

Key challenges include competition from rechargeable lithium-ion batteries, Battery Waste Management Rules compliance costs, raw material price volatility (zinc, MnO₂), low-cost Chinese import pressure, and consumer price sensitivity in the mass-market battery segment.

Smart home IoT device alkaline demand, rural zinc-carbon to alkaline conversion, defense battery procurement, premium alkaline e-commerce distribution, and EPR-compliant battery recycling infrastructure represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)