India Antibiotic Market Size, Share, Trends and Forecast by Action Mechanism, Drug Class, Spectrum of Activity, Route of Administration, End User, and Region, 2026-2034

India Antibiotic Market Summary:

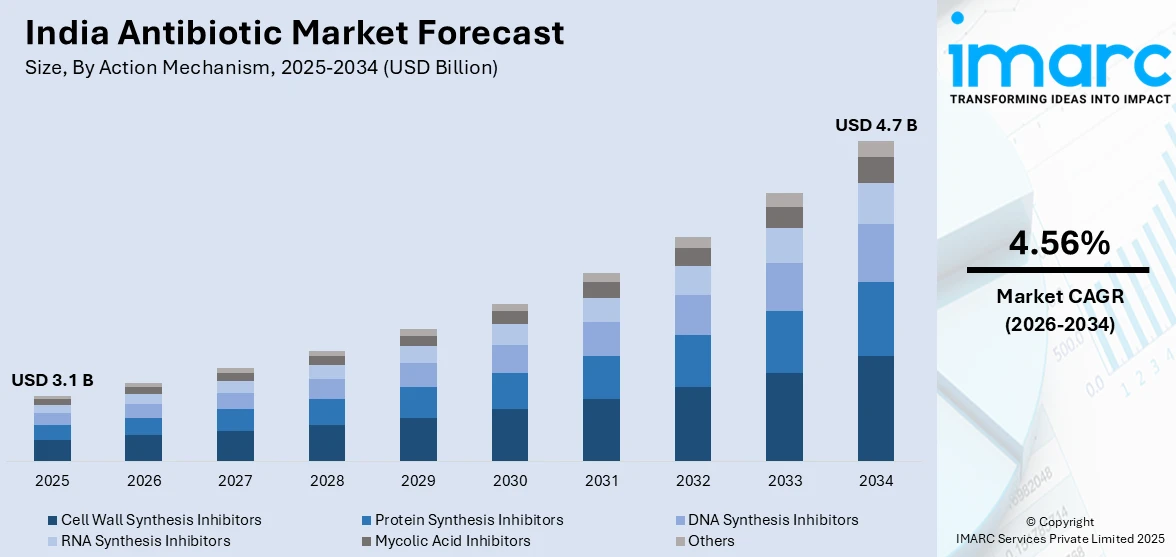

The India antibiotic market size was valued at USD 3.1 Billion in 2025 and is projected to reach USD 4.7 Billion by 2034, growing at a compound annual growth rate of 4.56% from 2026-2034.

The market's expansion is primarily driven by India's substantial burden of infectious diseases, with the country accounting for a large number of community pneumonia cases and acute respiratory infection cases annually. Rapid healthcare infrastructure development, and bed capacity expansion, is creating greater antibiotic accessibility across urban and rural populations. Government initiatives focusing on antimicrobial stewardship are shaping responsible antibiotic consumption patterns while expanding the India antibiotic market share.

Key Takeaways and Insights:

- By Action Mechanism: Cell wall synthesis inhibitors dominate the market with 42.8% share in 2025, driven by well-established beta-lactam antibiotics including penicillins and cephalosporins offering proven efficacy against diverse pathogens with favorable safety profiles enabling widespread clinical adoption across hospital and community settings.

- By Drug Class: Cephalosporin holds 37.9% market share in 2025, benefiting from multi-generational therapeutic options spanning first to fifth-generation molecules, availability in oral and parenteral formulations, and physician confidence in treating respiratory, urinary tract, and severe infections despite emerging resistance concerns.

- By Spectrum of Activity: Broad-spectrum antibiotics account for 55.3% market share in 2025, reflecting physician preference for all-rounder pathogen coverage addressing polymicrobial infections and diagnostic uncertainty in resource-constrained settings.

- By Route of Administration: Oral represents the largest segment with a market share of 48.1% in 2025, dominating through convenience enabling outpatient treatment, patient compliance advantages, cost-effectiveness compared to parenteral alternatives, and suitability for community-acquired infections managed in primary care settings without requiring hospitalization or sterile administration infrastructure.

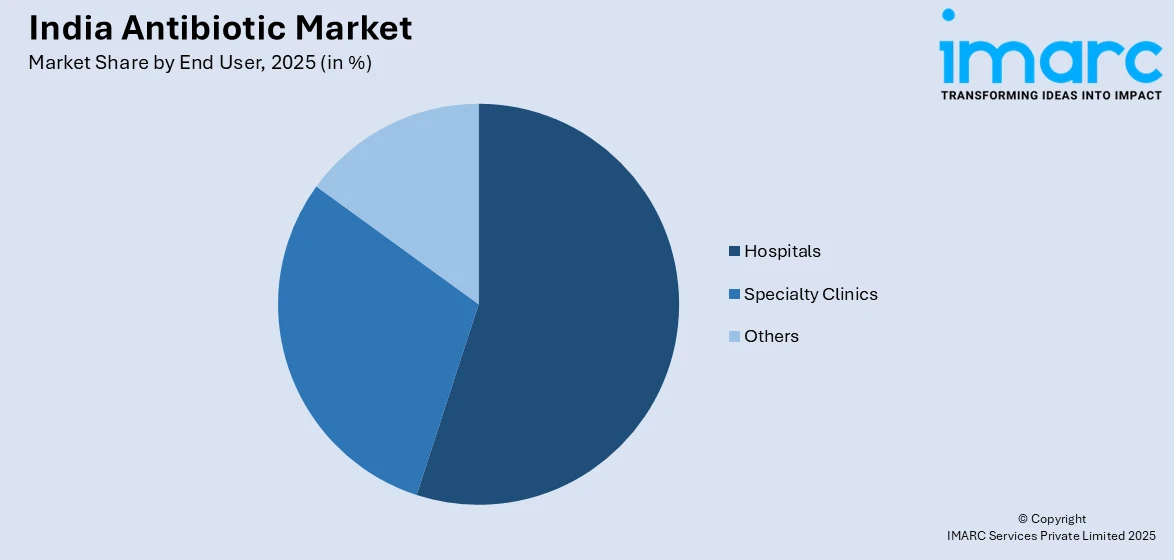

- By End User: Hospitals constitute the largest segment with 43.7% share in 2025, driven by management of severe infections needing parenteral administration and intensive monitoring.

- By Region: West India leads with 34.8% of the market in 2025, anchored by pharmaceutical manufacturing hubs in Maharashtra and Gujarat, advanced healthcare infrastructure in Mumbai and Pune, higher per capita healthcare expenditure, and concentrated presence of tertiary care facilities driving sophisticated antibiotic prescribing patterns.

- Key Players: Key players in India’s antibiotic market are expanding production capacity, investing in R&D for new formulations, strengthening export networks, improving compliance with global quality standards, and adopting cost-efficient manufacturing. Many are also focusing on antimicrobial resistance programs and strategic partnerships.

To get more information on this market Request Sample

The India antibiotic market is experiencing a paradigm shift due to the rising challenges of antimicrobial resistance and innovation in the country. The launch of Nafithromycin in November 2024 is a milestone in the country as it is the first indigenously developed macrolide antibiotic in the past three decades by Wockhardt with support from the government through BIRAC funding. The new antibiotic has shown 10 times more efficacy than azithromycin and fills an important gap in the treatment of drug-resistant community-acquired bacterial pneumonia. The market is challenged by the need to address the healthcare needs of the population while fighting antimicrobial resistance, with 300,000 deaths annually due to antimicrobial resistance. Third-generation cephalosporins account for a large share of the overall consumption of antibiotics. Government regulatory measures including the ban on 156 fixed-dose combinations and stricter Schedule H1 prescription requirements are reshaping market dynamics. Hospital sector expansion supports growing hospital-based antibiotic utilization. The oral segment's dominance with numerous private sector consumption highlights community healthcare's critical role, while West India's leadership reflects concentrated pharmaceutical manufacturing and advanced healthcare infrastructure in Maharashtra and Gujarat.

India Antibiotic Market Trends:

Rising Antimicrobial Resistance Driving Novel Drug Development

Antimicrobial resistance has emerged as the most pressing challenge confronting India's antibiotic market, with the country reporting approximately 300,000 deaths annually from resistant infections. This crisis has catalyzed unprecedented innovation in indigenous antibiotic development. The NDA was submitted on September 30, 2025, and its approval signifies a groundbreaking moment, not just for Wockhardt, but also for the broader Indian pharmaceutical sector, the Mumbai-based drug manufacturer stated. The company stated that submitting an NDA to the US FDA signifies one of the toughest scientific and regulatory barriers in international drug development. Zaynich has received fast-track designation from the USFDA, acknowledging its ability to meet urgent and unmet medical needs.

Government Regulatory Framework Strengthening

The Indian government has intensified regulatory oversight to combat irrational antibiotic use and contain resistance. In August 2024, authorities banned 156 fixed-dose combination formulations, including multiple antibiotic cocktails lacking scientific justification that fueled resistance development. The National Action Plan on AMR 2.0, launched for 2025-2029, emphasizes One Health surveillance integrating human, animal, and environmental health sectors with strengthened antimicrobial stewardship programs. The Red Line Campaign requiring antibiotics to display vertical red lines on packaging signals prescription-only status, while Schedule H1 enforcement mandates that doctors write exact indications when prescribing antimicrobials, fundamentally reshaping prescribing practices across India's healthcare ecosystem.

Digital Health Integration Transforming Antibiotic Prescribing

Digital transformation is revolutionizing antibiotic management and distribution across India's healthcare landscape. The country's digital health market, valued at 16,114.2 Million in 2024, is projected to reach USD 76,012.7 Million by 2033 at a 18.81% compound annual growth rate as per the predictions of IMARC Group. Hospital chains including Apollo and Fortis are implementing sophisticated telemedicine platforms linking smaller facilities to city-based infectious disease specialists, enabling expert consultation for complex antibiotic decisions. E-prescription systems integrated with antimicrobial stewardship software are reducing inappropriate prescribing through automated decision support, drug-drug interaction alerts, and resistance pattern tracking. Apollo 24/7 has conducted over 1 million teleconsultations annually, demonstrating digital health's scale in reaching patients across tier-2 and tier-3 cities where specialist access remains limited.

Market Outlook 2026-2034:

The India antibiotic market is poised for sustained expansion through 2030, driven by persistent infectious disease burden, healthcare infrastructure modernization, and pharmaceutical innovation addressing antimicrobial resistance. The market generated a revenue of USD 3.1 Billion in 2025 and is projected to reach a revenue of USD 4.7 Billion by 2034, growing at a compound annual growth rate of 4.56% from 2026-2034. Indigenous antibiotic development initiatives following Nafithromycin's successful launch position India as an emerging innovation hub, with Wockhardt's Zaynich filing in March 2025 demonstrating superior efficacy over meropenem for drug-resistant infections. Government focus on universal health coverage through Ayushman Bharat's expansion covering Innumerable beneficiaries and regulatory emphasis on rational prescribing will shape consumption patterns while supporting sustainable market development anchored in clinical need rather than irrational use.

India Antibiotic Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Action Mechanism |

Cell Wall Synthesis Inhibitors |

42.8% |

|

Drug Class |

Cephalosporin |

37.9% |

|

Spectrum of Activity |

Broad-Spectrum Antibiotics |

55.3% |

|

Route of Administration |

Oral |

48.1% |

|

End User |

Hospitals |

43.7% |

|

Region |

West India |

34.8% |

Action Mechanism Insights:

- Cell Wall Synthesis Inhibitors

- Protein Synthesis Inhibitors

- DNA Synthesis Inhibitors

- RNA Synthesis Inhibitors

- Mycolic Acid Inhibitors

- Others

Cell wall synthesis inhibitors dominate with a market share of 42.8% of the total India antibiotic market in 2025.

Cell wall synthesis inhibitors represent the cornerstone of India's antibiotic market, leveraging well-established efficacy against diverse bacterial pathogens through disruption of peptidoglycan synthesis. Beta-lactam antibiotics including penicillins, cephalosporins, and carbapenems constitute this category's primary components. Third-generation cephalosporins alone account for a majority of antibiotic consumption in India, with drugs like ceftriaxone and cefixime widely prescribed for respiratory tract infections, pneumonia, urinary tract infections, and suspected sepsis cases across hospital and community settings. These antibiotics' broad acceptance stems from decades of clinical experience, favorable safety profiles, and oral formulation availability enabling outpatient treatment compliance.

The segment benefits from continuous pharmaceutical innovation addressing resistance challenges, exemplified by beta-lactamase inhibitor combinations extending efficacy against resistant strains. Market dynamics reflect escalating resistance concerns, with over 50% of E. coli and Klebsiella pneumoniae isolates demonstrating resistance to third-generation cephalosporins in surveillance data. This resistance pressure drives demand for novel combinations and fourth-generation cephalosporins, while healthcare providers' familiarity with cell wall synthesis inhibitors' prescribing patterns ensures sustained market dominance despite emerging resistance challenges requiring judicious use and stewardship program implementation across India's diverse healthcare landscape.

Drug Class Insights:

- Cephalosporin

- Penicillin

- Fluoroquinolone

- Macrolide

- Carbapenem

- Aminoglycoside

- Others

Cephalosporin leads with a share of 37.9% of the total India antibiotic market in 2025.

Cephalosporins dominate India's antibiotic landscape through multi-generational therapeutic options addressing diverse bacterial infections with varying resistance profiles. The market encompasses first-generation agents for skin and soft tissue infections, second-generation drugs for respiratory and urinary tract conditions, third-generation cephalosporins providing enhanced gram-negative coverage for severe infections, and advanced fourth and fifth-generation molecules targeting multidrug-resistant pathogens. These antibiotics' widespread adoption reflects physicians' confidence in established efficacy, availability across oral and parenteral formulations, and generally favorable tolerability profiles enabling broad population use including pediatric and geriatric patients requiring dose adjustments.

Cephalosporin market dynamics face pressure from escalating antimicrobial resistance and regulatory scrutiny promoting rational use. Third-generation cephalosporins experienced prescribing increases in hospital settings despite resistance concerns, while government initiatives including Schedule H1 enforcement and antimicrobial stewardship programs aim to curb inappropriate empirical use. Pharmaceutical innovation continues with novel beta-lactamase inhibitor combinations like cefepime-enmetazobactam addressing extended-spectrum beta-lactamase producing organisms. The segment's trajectory balances sustained clinical utility against resistance mitigation imperatives, with market growth supported by hospital expansion, infectious disease burden, and continued physician preference for cephalosporins' versatility across infection types, despite emerging alternatives from carbapenem and fluoroquinolone classes in specific resistant infection scenarios.

Spectrum of Activity Insights:

- Broad-Spectrum Antibiotics

- Narrow-Spectrum Antibiotics

Broad-spectrum antibiotics exhibit a clear dominance with a 55.3% share of the total India antibiotic market in 2025.

Broad-spectrum antibiotics command majority market share in India through their ability to target multiple bacterial species simultaneously, addressing the clinical reality of polymicrobial infections and diagnostic uncertainty in resource-constrained settings. These agents including third-generation cephalosporins, fluoroquinolones, broad-spectrum penicillins, and macrolides enable empirical treatment initiation before definitive pathogen identification, critical in time-sensitive conditions like sepsis, pneumonia, and complicated urinary tract infections. The broad-spectrum segment's dominance reflects systemic healthcare challenges including limited diagnostic infrastructure particularly in rural and semi-urban areas where rapid bacterial identification remains unavailable, driving physicians toward comprehensive coverage ensuring therapeutic success across diverse pathogens.

Urban primary care pharmacies reported carrying at least three distinct broad-spectrum generic brands to prevent stockouts. However, this preference accelerates antimicrobial resistance development, with surveillance revealing Salmonella Typhi isolates in Gujarat state showing resistance to frontline broad-spectrum agents including ceftriaxone and ciprofloxacin. Antimicrobial stewardship initiatives and diagnostic advancement including point-of-care testing expansion aim to shift prescribing toward narrow-spectrum agents where appropriate, though broad-spectrum antibiotics will maintain market leadership given India's infectious disease complexity, diagnostic limitations, and clinical practice patterns prioritizing immediate comprehensive coverage over delayed targeted therapy in critical infection scenarios.

Route of Administration Insights:

- Oral

- Parenteral

- Topical

- Others

Oral leads with a share of 48.1% of the total India antibiotic market in 2025.

Oral antibiotics constitute the predominant route of administration in India's antibiotic market, with a major portion of antibiotics consumed in the private sector delivered orally according to consumption studies spanning multiple years. This overwhelming preference reflects oral formulations' convenience enabling outpatient treatment, patient compliance advantages through familiar tablet, capsule, and syrup formats, and cost-effectiveness compared to parenteral alternatives requiring sterile administration and healthcare personnel involvement. Oral preparations demonstrated relative increase, with oral liquid formulations showing particularly strong growth indicating substantial pediatric antibiotic use expansion.

Market dynamics favor oral antibiotic expansion through rural healthcare infrastructure development, telemedicine platforms enabling remote prescribing for community-acquired infections, and Ayushman Bharat scheme's outpatient coverage extension increasing access to oral antibiotics for previously underserved populations. Generic manufacturers have introduced over 150 new oral antibiotic SKUs including fast-dissolving tablets, dispersible formulations, and flavored pediatric syrups improving palatability and compliance. Digital health integration through e-prescription systems and community pharmacist training initiatives aim to rationalize oral antibiotic dispensing, while pharmaceutical innovation focuses on bioavailability enhancement and resistance-breaking combinations maintaining oral route's therapeutic utility against evolving bacterial resistance patterns in India's diverse epidemiological landscape.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Specialty Clinics

- Others

Hospitals exhibit a clear dominance with a 43.7% share of the total India antibiotic market in 2025.

Hospitals represent one of the largest end users in India’s antibiotic market, driven by the high volume of inpatient and outpatient treatments for bacterial infections. Public and private hospitals rely heavily on antibiotics for surgical prophylaxis, intensive care, respiratory infections, urinary tract infections, and treatment of hospital-acquired infections. Rising patient admissions, expanding hospital infrastructure, and increasing availability of advanced diagnostic facilities are supporting antibiotic demand across tertiary care centers. At the same time, hospitals are facing strong pressure to ensure responsible antibiotic use due to the growing threat of antimicrobial resistance. Hospitals are also increasingly investing in infection control practices, including improved sanitation, isolation protocols, and staff training, to reduce infection rates and minimize antibiotic dependency.

In addition, hospitals are becoming key channels for the adoption of newer-generation antibiotics, especially in critical care units where resistant infections are more common. Private multi-specialty hospitals in metro cities are often early adopters of advanced therapies, while government hospitals continue to drive bulk antibiotic consumption due to large patient inflows and budget-based procurement. Hospitals also influence market dynamics through tender-based purchasing, supplier contracts, and preference for trusted domestic manufacturers with strong regulatory compliance.

Regional Insights:

- North India

- South India

- East India

- West India

West India leads with a share of 34.8% of the total India antibiotic market in 2025.

West India leads the regional antibiotic market through concentration of pharmaceutical manufacturing capabilities, advanced healthcare infrastructure in major metros, and higher per capita healthcare expenditure supporting premium antibiotic adoption. The region encompasses Maharashtra and Gujarat, housing pharmaceutical industry clusters in cities including Mumbai, Pune, Ahmedabad, and Vadodara where major antibiotic manufacturers maintain production facilities, research centers, and corporate headquarters. This industrial concentration ensures superior supply chain efficiency, faster new product launches, and enhanced market penetration across hospital and retail channels. Mumbai and Pune's healthcare ecosystems include numerous tertiary care hospitals, specialized infectious disease centers, and medical colleges driving sophisticated antibiotic prescribing patterns for complex infections including drug-resistant tuberculosis, hospital-acquired infections, and immunocompromised patient populations requiring reserve antibiotics and novel combinations.

Regional dynamics reflect Maharashtra's position as India's leading state for healthcare investment with hospital chains including Apollo, Fortis, and Jupiter planning significant expansion projects. Gujarat's pharmaceutical sector contributes substantially to antibiotic production with strong API manufacturing infrastructure supplying domestic formulation units. West India benefits from higher insurance penetration compared to national average, supporting hospital antibiotic utilization through cashless treatment programs under Ayushman Bharat and private insurance schemes. Urban healthcare delivery models incorporating telemedicine, chain pharmacies, and corporate hospital networks are most advanced in West India, enabling efficient antibiotic distribution and stewardship program implementation. Regional market leadership positions West India as bellwether for national antibiotic consumption trends, pharmaceutical innovation adoption, and resistance mitigation strategies.

Market Dynamics:

Growth Drivers:

Why is the India Antibiotic Market Growing?

High Burden of Infectious Diseases Driving Sustained Demand

India's antibiotic market experiences robust demand growth driven by the country's substantial infectious disease burden affecting diverse population segments across urban and rural geographies. According to data from the National Centre for Disease Control (NCDC), India has experienced a significant increase in seasonal influenza A (H1N1) cases this year, while fatalities have fallen to their lowest level in four years. By September 30, 2025, the nation documented 3,320 cases and merely 14 deaths, a remarkable difference from earlier years when lower infection rates led to far greater fatalities. This persistent infectious disease burden across age groups, infection types, and geographic regions ensures sustained baseline antibiotic demand supporting market growth despite antimicrobial stewardship initiatives promoting judicious prescribing, with clinical necessity driving continued antibiotic utilization for managing India's substantial infection-related morbidity and mortality affecting millions annually.

Rapid Healthcare Infrastructure Expansion and Hospital Network Growth

Healthcare infrastructure modernization represents a pivotal growth driver transforming antibiotic accessibility and consumption patterns across India's evolving medical landscape. The Central Govt Health Scheme (CGHS) has experienced significant growth over five years, with 468 hospitals added to the panel across the country in 2025, greatly surpassing the 42 hospitals that left the scheme during that time. Official figures presented in Parliament indicated that although there has been an increase in exits this year, the overall network has significantly expanded, enhancing treatment choices for lakhs of government employees and pensioners nationwid. The expansion encompasses not merely bed additions but comprehensive capability development including intensive care units, neonatal intensive care facilities, operating theaters, and infection control infrastructure necessitating parenteral antibiotic availability and antimicrobial stewardship program implementation. Hospital expansion coincides with digital health integration through telemedicine platforms linking smaller facilities to urban specialists, electronic health records enabling prescription tracking, and supply chain management systems ensuring antibiotic availability across distributed facility networks.

Government Healthcare Coverage Initiatives Expanding Access

Government healthcare initiatives particularly the Ayushman Bharat scheme are revolutionizing antibiotic accessibility for previously underserved populations through comprehensive health coverage expansion and infrastructure development programs. Ayushman Bharat, launched as the world's largest government-funded healthcare initiative, has empaneled 31,466 hospitals nationwide including 14,194 private facilities, authorizing over 9.84 crore hospital admissions worth over Rs. 1.40 lakh crore as of July 2025. This massive coverage expansion enables economically disadvantaged populations to access hospital-based antibiotic therapy for serious infections including pneumonia, sepsis, complicated urinary tract infections, and surgical site infections that previously remained untreated or managed inadequately through out-of-pocket expenditure constraints. The scheme's cashless treatment framework eliminates financial barriers to antibiotic access, allowing hospitals to prescribe appropriate antibiotic regimens including parenteral formulations and newer agents without cost considerations limiting clinical decision-making for covered beneficiaries.

Market Restraints:

What Challenges the India Antibiotic Market is Facing?

Escalating Antimicrobial Resistance Undermining Treatment Efficacy

Antimicrobial resistance represents the most formidable challenge confronting India's antibiotic market, progressively eroding treatment effectiveness and driving mortality through resistant infections. India reports nearly a million deaths annually from antibiotic-resistant infections, with surveillance data revealing alarming resistance patterns including over 90% of Salmonella Typhi isolates in Gujarat state showing resistance to ceftriaxone and ciprofloxacin, while more than 50% of E. coli and Klebsiella pneumoniae isolates demonstrate resistance to third-generation cephalosporins nationally. This resistance crisis stems from multiple factors including over-the-counter antibiotic availability despite regulatory restrictions, irrational prescribing patterns with broad-spectrum agents constituting 55% of consumption against WHO recommendations, and incomplete treatment courses contributing to selection pressure. This resistance escalation constrains antibiotic market growth by reducing demand for older molecules rendered ineffective, necessitating expensive reserve antibiotics increasing treatment costs, and dampening pharmaceutical investment in antibiotic development given limited commercial returns and rapid resistance emergence post-launch eroding market exclusivity value propositions.

Stringent Regulatory Restrictions and Prescription Enforcement Limiting Accessibility

Regulatory tightening aimed at combating antimicrobial resistance and promoting rational use imposes significant market constraints through prescribing restrictions and sales limitations. The Central Government's January 2024 directive requiring doctors to write exact indications when prescribing antimicrobial drugs increases prescription scrutiny and documentation burden potentially reducing casual antibiotic prescribing. Schedule H1 classification mandates that antibiotics display red vertical lines on packaging and require valid prescriptions for dispensing, with enforcement gradually improving particularly in urban pharmacy chains though rural compliance remains inconsistent. These regulatory measures, while clinically justified for resistance containment, constrain market dynamics through reduced over-the-counter sales, prescription requirement enforcement limiting impulse purchases, and physician hesitation from regulatory scrutiny regarding antibiotic prescribing patterns potentially leading to under-prescribing in borderline clinical scenarios where antibiotic intervention might benefit patients.

Intense Price Competition from Generic Proliferation Compressing Margins

Market saturation with generic antibiotics creates intense price competition eroding profit margins and limiting innovation investment. Price erosion particularly affects newer antibiotics where generic competition emerges post-patent expiry, reducing commercial incentives for pharmaceutical companies to invest in antibiotic research and development given limited market exclusivity periods before generic entry. This pricing pressure constrains market value growth despite volume expansion, reduces resources available for antimicrobial stewardship program implementation, and discourages pharmaceutical innovation in antibiotic class development where development costs exceed revenue potential given resistance-driven limited commercial lifespan and pricing constraints from generic competition dominating India's cost-sensitive antibiotic market dynamics.

Competitive Landscape:

Key market players in India’s antibiotic market are taking several steps to strengthen their business growth and competitiveness. Many companies are expanding manufacturing capacity to meet rising domestic demand and export opportunities, especially in regulated markets like the US and Europe. Firms are investing in research and development to introduce newer formulations, combination therapies, and differentiated products targeting resistant infections. Improving compliance with global quality and regulatory standards has become a major priority, helping Indian manufacturers build trust and secure international approvals. Players are also strengthening distribution networks across tier-2 and tier-3 cities to improve access and market penetration. Strategic partnerships, licensing deals, and acquisitions are being used to broaden product portfolios and enter new therapeutic segments. Additionally, companies are focusing on antimicrobial stewardship efforts and sustainable production practices to address rising concerns around antibiotic resistance and environmental impact.

India Antibiotic Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Action Mechanisms Covered |

Cell Wall Synthesis Inhibitors, Protein Synthesis Inhibitors, DNA Synthesis Inhibitors, RNA Synthesis Inhibitors, Mycolic Acid Inhibitors, Others |

|

Drug Classes Covered |

Cephalosporin, Penicillin, Fluoroquinolone, Macrolide, Carbapenem, Aminoglycoside, Others |

|

Spectrum of Activities Covered |

Broad-Spectrum Antibiotics, Narrow-Spectrum Antibiotics |

|

Routes of Administration Covered |

Oral, Parenteral, Topical, Others |

|

End Users Covered |

Hospitals, Specialty Clinics, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Antibiotic Market Report

The India antibiotic market size was valued at USD 3.1 Billion in 2025.

The India antibiotic market is expected to grow at a compound annual growth rate of 4.56% from 2026-2034 to reach USD 4.7 Billion by 2034.

Cell wall synthesis inhibitors held the largest share at 42.8% in 2025, dominated by beta-lactam antibiotics including penicillins and cephalosporins. Third-generation cephalosporins alone constitute a major portion of total consumption, with ceftriaxone and cefixime widely prescribed for respiratory, urinary tract, and severe bacterial infections.

Key factors driving the India antibiotic market include the high burden of infectious diseases with acute respiratory infection cases annually, rapid healthcare infrastructure expansion with hospitals growing facilities, and government coverage initiatives including Ayushman Bharat authorizing hospital admissions providing enhanced antibiotic access across socioeconomic segments.

Major challenges include escalating antimicrobial resistance with approximately a million annual deaths from resistant infections and E. coli and Klebsiella isolates showing third-generation cephalosporin resistance, stringent regulatory restrictions including Schedule H1 prescription requirements and ban on 156 fixed-dose combinations, and intense generic competition with 700+ cefixime formulations driving prices down.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)