India Anticoagulant Market Size, Share, Trends and Forecast by Drug Class, Route of Administration, Distribution Channel, Application, and Region, 2026-2034

India Anticoagulant Market Summary:

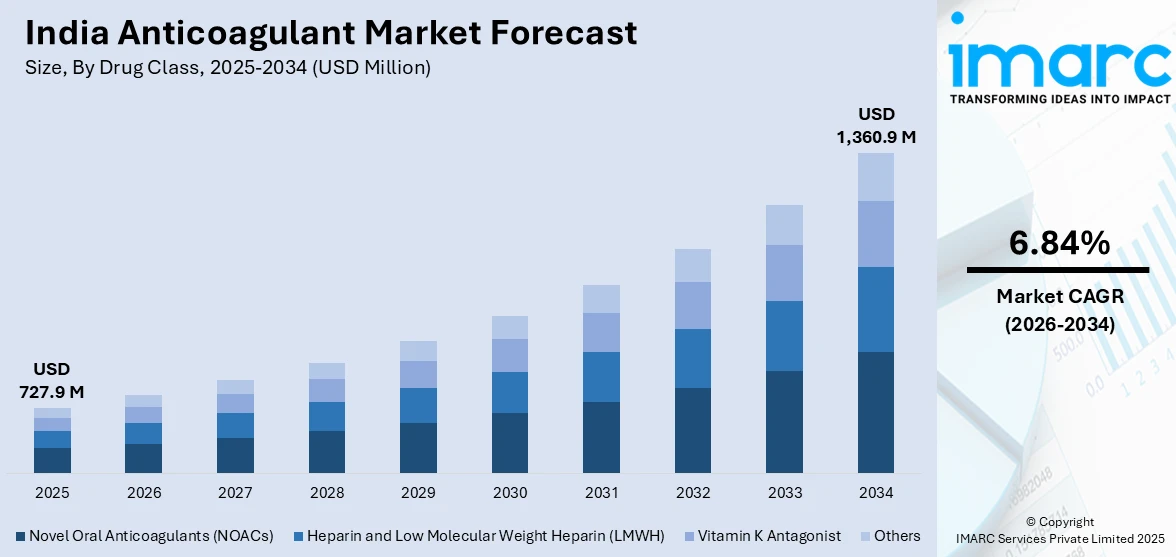

The India anticoagulant market size was valued at USD 727.9 Million in 2025 and is projected to reach USD 1,360.9 Million by 2034, growing at a compound annual growth rate of 6.84% from 2026-2034.

The India anticoagulant market is experiencing strong momentum as the country confronts a growing cardiovascular disease burden and as therapeutic awareness among healthcare providers expands. Rising diagnosis rates for thromboembolic conditions, coupled with increasing adoption of advanced oral anticoagulant therapies, are reshaping treatment protocols across healthcare facilities. Government-led initiatives to strengthen public health infrastructure, expanding health insurance coverage, and a thriving domestic pharmaceutical manufacturing ecosystem are collectively enabling broader patient access to anticoagulant medications, supporting sustained growth in the India anticoagulant market share.

Key Takeaways and Insights:

- By Drug Class: Novel oral anticoagulants (NOACs) dominate the market with a share of 51.9% in 2025, driven by their predictable pharmacokinetics, minimal monitoring requirements, and growing physician preference over traditional vitamin K antagonists.

- By Route of Administration: Oral anticoagulant leads the market with a share of 62.7% in 2025, supported by patient convenience, fixed dosing schedules, and the expanding availability of affordable generic oral formulations.

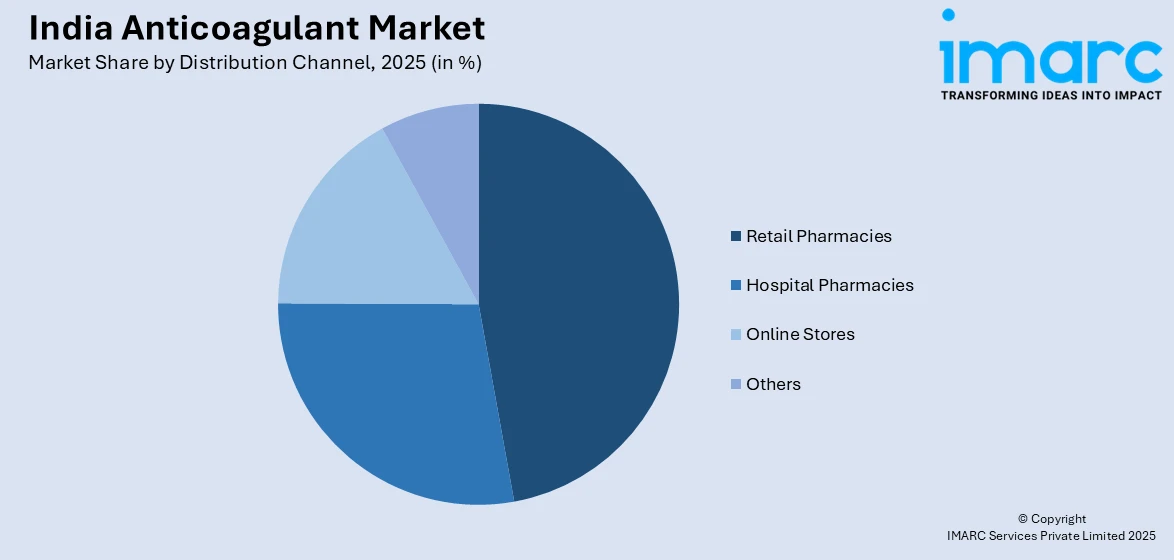

- By Distribution Channel: Retail pharmacies represent the largest segment with a market share of 47.3% in 2025, owing to their extensive nationwide network, accessibility for chronic disease patients, and established trust among consumers.

- By Application: Atrial fibrillation and heart attack leads the market with a share of 39.5% in 2025, reflecting the high burden of cardiac arrhythmias and acute coronary events across India’s adult population.

- By Region: South India dominates the market with a share of 33.9% in 2025, attributed to superior healthcare infrastructure, higher diagnostic awareness, and concentration of tertiary care hospitals.

- Key Players: The India anticoagulant market features a competitive landscape characterized by the presence of both multinational pharmaceutical corporations and prominent domestic generic manufacturers. Companies compete through product portfolio diversification, pricing strategies, and expanding distribution networks to strengthen market positioning.

To get more information on this market Request Sample

The India anticoagulant market is undergoing rapid transformation as clinical practice increasingly emphasizes evidence-based approaches to thromboprophylaxis and stroke prevention. The rising prevalence of cardiovascular disorders is sustaining long-term demand for anticoagulant therapies across hospital and outpatient settings. At the same time, a more supportive regulatory environment is enabling faster access to newer anticoagulant options, broadening treatment choices for clinicians and patients. The introduction of novel oral anticoagulants is improving convenience, safety, and adherence compared with conventional therapies. Together, these factors are strengthening market growth and driving wider adoption of modern anticoagulation regimens across diverse patient populations. The expanding healthcare insurance ecosystem, including Ayushman Bharat, which has issued over 42 crore health cards as of October 2025, is improving access to cardiovascular treatments for economically vulnerable populations. Additionally, the domestic pharmaceutical sector’s capacity to produce affordable generic NOACs is accelerating therapy adoption across tier-two and tier-three cities.

India Anticoagulant Market Trends:

Rising Adoption of Direct Oral Anticoagulants Over Traditional Therapies

Indian healthcare providers are steadily shifting from warfarin-based therapies to direct oral anticoagulants, reflecting a broader move toward treatments with more predictable pharmacological profiles and reduced monitoring needs. Expanding availability of newer anticoagulant options from domestic manufacturers is improving access and affordability. The presence of effective reversal solutions has further enhanced the safety perception of these therapies, increasing clinician confidence in their use. Together, these factors are accelerating the adoption of modern anticoagulant regimens and supporting sustained growth of the anticoagulant market across diverse clinical settings in India.

Digital Health Platforms Transforming Anticoagulant Distribution

The rapid expansion of e-pharmacy platforms is reshaping how patients access anticoagulant medications in India, particularly for chronic disease management requiring consistent refills. Digital health channels are improving medication adherence through automated reminders and home delivery services. The India online pharmacy market size was valued at USD 3.71 Billion in 2025 and is projected to reach USD 14.08 Billion by 2034, growing at a compound annual growth rate of 15.98% from 2026-2034, is enabling patients in semi-urban and rural areas to obtain prescription anticoagulants conveniently, thereby expanding the addressable patient base beyond traditional retail channels.

Personalized Anticoagulation and Point-of-Care Testing Advancements

Advances in point-of-care testing and pharmacogenomics are enabling more personalized anticoagulant therapy in Indian healthcare settings. Clinicians are increasingly using rapid coagulation testing tools and genetic insights to tailor dosing strategies for patients with atrial fibrillation and thromboembolic disorders. The growing integration of digital health platforms and data-driven diagnostic approaches is improving clinical decision-making and treatment outcomes. These developments are enhancing the precision and safety of anticoagulation management, supporting broader adoption of optimized, patient-specific treatment pathways across hospitals and outpatient care facilities.

Market Outlook 2026-2034:

The India anticoagulant market is positioned for sustained expansion, driven by the country’s growing cardiovascular disease prevalence, aging demographics, and expanding healthcare access through government-supported insurance programs. The increasing preference for novel oral anticoagulants over traditional therapies, combined with the entry of affordable generics from domestic manufacturers, is broadening the treatment-eligible patient population. Continued investments in healthcare infrastructure and digital health platforms are expected to further strengthen distribution and therapy adherence. The market generated a revenue of USD 727.9 Million in 2025 and is projected to reach a revenue of USD 1,360.9 Million by 2034, growing at a compound annual growth rate of 6.84% from 2026-2034.

India Anticoagulant Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Drug Class |

Novel Oral Anticoagulants (NOACs) |

51.9% |

|

Route of Administration |

Oral Anticoagulant |

62.7% |

|

Distribution Channel |

Retail Pharmacies |

47.3% |

|

Application |

Atrial Fibrillation and Heart Attack |

39.5% |

|

Region |

South India |

33.9% |

Drug Class Insights:

- Novel Oral Anticoagulants (NOACs)

- Heparin and Low Molecular Weight Heparin (LMWH)

- Vitamin K Antagonist

- Others

Novel oral anticoagulants (NOACs) dominate with a market share of 51.9% of the total of the India anticoagulant market in 2025.

The NOACs segment has established clear market leadership, driven by their superior safety profiles, fixed-dose administration, and reduced need for routine coagulation monitoring compared to traditional vitamin K antagonists. Indian physicians are increasingly prescribing apixaban, rivaroxaban, and dabigatran for stroke prevention in atrial fibrillation and treatment of venous thromboembolism. The availability of generic NOAC formulations from domestic manufacturers has significantly improved affordability, making advanced anticoagulant therapies accessible to a wider patient population in India. Competitive pricing and increased local production have lowered treatment barriers, supporting broader adoption of modern anticoagulants across diverse socioeconomic and healthcare settings.

Clinical evidence demonstrating the effectiveness of novel oral anticoagulants in Asian patient populations has strengthened their acceptance across Indian healthcare facilities. Growing confidence in their safety and efficacy has encouraged clinicians to incorporate these therapies into routine cardiovascular care. At the same time, a supportive regulatory environment is enabling the introduction of additional anticoagulant options, expanding the range of treatments available. The broader availability of multiple formulations and dosing options is improving prescribing flexibility, allowing physicians to better tailor anticoagulant therapy for patients with complex clinical profiles and long-term management needs.

Route of Administration Insights:

- Oral Anticoagulant

- Injectable Anticoagulant

Oral anticoagulant leads the market with a share of 62.7% of the total of the India anticoagulant market in 2025.

Oral anticoagulants command the largest market share, reflecting strong clinical and patient preference for non-invasive drug delivery in chronic thromboprophylaxis. The convenience of tablet-based therapy, combined with the expanding availability of once-daily dosing options through NOACs, supports superior medication adherence compared to injectable alternatives. India’s robust generic pharmaceutical industry has made oral anticoagulants increasingly affordable, facilitating long-term treatment compliance among patients managing atrial fibrillation, deep vein thrombosis, and post-surgical thromboprophylaxis.

The oral anticoagulant segment continues to gain momentum as clinical guidelines increasingly favor direct oral anticoagulants as first-line therapy for a range of thromboembolic conditions. Expanding availability of generic oral formulations is intensifying competition, improving affordability, and supporting wider patient access. At the same time, a rapidly developing retail pharmacy and e-pharmacy ecosystem is enhancing drug availability across urban and rural regions. Improved distribution reach and convenience are reinforcing the dominance of oral anticoagulants and driving sustained growth in this segment of the Indian anticoagulant market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Online Stores

- Others

Retail pharmacies represent the highest revenue with a 47.3% share of the total of the India anticoagulant market in 2025.

Retail pharmacies maintain their dominant position in anticoagulant distribution owing to their extensive geographic reach, established consumer trust, and ability to serve chronic disease patients requiring regular prescription refills. India’s pharmacy network, comprising over eight lakh retail outlets, provides unmatched accessibility for patients on long-term anticoagulant therapy. Retail pharmacies also benefit from healthcare-related trust associations that reduce purchasing discomfort for patients managing sensitive cardiovascular conditions.

The retail channel continues to strengthen through improved supply chain management and integration with digital prescription verification systems. The India retail market size reached USD 1,124.2 Billion in 2025. The market is expected to reach USD 3,505.4 Billion by 2034, exhibiting a growth rate (CAGR) of 12.80% during 2026-2034. The growing emphasis on organized retail pharmacy chains, which offer standardized product quality and trained pharmacist consultations, is enhancing the patient experience. Additionally, government policies supporting generic drug dispensing through retail outlets are ensuring that cost-effective anticoagulant formulations reach a wider patient demographic, particularly in semi-urban and tier-two cities across India.

Application Insights:

- Atrial Fibrillation and Heart Attack

- Stroke

- Deep Vein Thrombosis (DVT)

- Pulmonary Embolism (PE)

- Others

Atrial fibrillation and heart attack lead the market with a share of 39.5% of the total of the India anticoagulant market in 2025.

The atrial fibrillation and heart attack segment represents the largest application area, driven by the growing burden of cardiac rhythm disorders and coronary conditions in India. The increasing incidence of atrial fibrillation and ischemic heart disease is raising the need for long-term anticoagulant therapy to prevent stroke and systemic embolic events. As cardiovascular conditions are being diagnosed more frequently across both urban and semi-urban settings, demand for effective and convenient anticoagulant treatments is expanding. This trend is reinforcing the central role of anticoagulants in cardiac disease management.

Extensive health coverage programs and access to better healthcare in the community are augmenting the provision of cardiovascular treatments to the elderly and high-risk groups. Increased access to cardiac care in hospitals, coupled with increased access to state-of-the-art therapies, is facilitating earlier intervention and overall compliance with treatment. Simultaneously, the better diagnostic facilities and the growing awareness of cardiac arrhythmias are causing the rates to be detected more frequently. Such advancements are expanding the number of patients who need long-term anticoagulation and increasing the demand in all healthcare facilities.

Regional Insights:

- North India

- South India

- East India

- West India

South India represents the largest regional share at 33.9% of the India anticoagulant market in 2025.

South India’s market dominance is underpinned by its well-developed healthcare infrastructure, higher concentration of tertiary care hospitals and specialized cardiac centers, and greater diagnostic awareness among the population. States such as Tamil Nadu, Karnataka, Kerala, and Andhra Pradesh host some of India’s leading cardiology and cardiovascular surgery centers, driving higher detection and treatment rates for thromboembolic conditions. The region’s comparatively higher health literacy and stronger health insurance penetration further support greater anticoagulant utilization.

The South Indian market also benefits from the region’s leadership in pharmaceutical manufacturing and distribution, which ensures efficient availability of anticoagulant medications. The robust presence of organized retail pharmacy chains and the growing adoption of e-pharmacy platforms in cities like Bengaluru, Chennai, and Hyderabad are strengthening distribution networks. Furthermore, South India’s demographic profile, with a relatively higher proportion of elderly citizens, creates sustained demand for chronic cardiovascular therapies, including long-term anticoagulation.

Market Dynamics:

Growth Drivers:

Why is the India Anticoagulant Market Growing?

Escalating Cardiovascular Disease Burden and Aging Population

India is experiencing a significant rise in cardiovascular diseases driven by rapid urbanization, sedentary lifestyles, dietary shifts, and increasing stress levels. The country now accounts for approximately one-fifth of all global CVD-related deaths, with coronary artery disease prevalence in urban areas increasing substantially over recent decades. The United Nations Population Fund’s India Ageing Report 2023 highlights that India is witnessing a sharp rise in its elderly population, with the number of older adults increasing by roughly 41% over each decade. The share of older adults is projected to more than double, exceeding 20% of the total population by 2050. The report further highlights that by 2046, the elderly population is expected to surpass the number of children aged 0–15 years, signaling a major demographic transition toward an ageing society. This demographic shift is creating an expanding patient pool requiring long-term anticoagulation for conditions such as atrial fibrillation, venous thromboembolism, and post-surgical thromboprophylaxis, directly fueling market growth.

Expanding Healthcare Access Through Government Insurance Initiatives

Government-led healthcare programs are dramatically improving access to cardiovascular treatments across India, particularly for economically disadvantaged populations. The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, the world’s largest publicly funded health insurance scheme, has issued over 42 crore health cards as of October 2025, covering cardiothoracic and cardiovascular surgical packages across more than 33,000 empanelled hospitals. For instance, in September 2024, the Union Cabinet extended health coverage to all citizens aged 70 and above, regardless of income, targeting approximately 4.5 crore additional families encompassing six crore senior citizens. This expansion is particularly significant for anticoagulant demand, as the elderly population represents the highest-risk group for atrial fibrillation and thrombotic events requiring long-term anticoagulation therapy.

Growth of Domestic Generic Pharmaceutical Manufacturing

India’s strong generic pharmaceutical manufacturing base is playing a key role in accelerating growth of the anticoagulant market by improving affordability and widening patient access. Domestic producers are increasingly offering cost-effective versions of novel oral anticoagulants, enabling broader adoption of advanced therapies. Supportive industrial policies are strengthening local production of active pharmaceutical ingredients and drug intermediates, enhancing supply reliability. The development of dedicated manufacturing clusters is further reinforcing the domestic API ecosystem, reducing reliance on imports and ensuring consistent availability of anticoagulant medicines across hospital, retail, and online distribution channels throughout the country.

Market Restraints:

What Challenges the India Anticoagulant Market is Facing?

Limited Awareness and Diagnosis in Rural Regions

Despite increasing urbanization, a substantial portion of India’s population residing in rural areas faces limited access to cardiovascular screening and diagnostic services. Atrial fibrillation and venous thromboembolism frequently remain undiagnosed in these communities due to inadequate healthcare infrastructure and low health literacy. This diagnostic gap results in a significant underutilization of anticoagulant therapies, constraining market penetration in rural demographics.

Bleeding Risk Concerns and Physician Hesitancy

The risk of major bleeding complications associated with anticoagulant therapy remains a significant concern among physicians, particularly when treating elderly patients with multiple comorbidities. Limited access to reversal agents and specialized coagulation monitoring in smaller healthcare facilities contributes to physician hesitancy in prescribing anticoagulants. This cautious approach to therapy initiation slows adoption rates, especially in secondary care settings.

Cost Sensitivity and Inconsistent Insurance Coverage

While generic manufacturing has improved affordability, novel oral anticoagulants remain relatively expensive for a significant segment of the Indian population, particularly those without health insurance coverage. Inconsistent reimbursement policies across state-level insurance schemes and limited coverage of newer anticoagulant molecules create financial barriers for patients requiring long-term therapy. Out-of-pocket expenditure continues to influence treatment decisions and medication adherence.

Competitive Landscape:

The India anticoagulant market exhibits a moderately fragmented competitive structure, with multinational pharmaceutical corporations and domestic generic manufacturers operating across multiple price segments and therapeutic categories. Competition is primarily driven by product portfolio breadth, pricing strategies, and distribution network strength. Companies are focusing on expanding their NOAC offerings, introducing affordable generic formulations, and strengthening relationships with healthcare providers to increase prescriber adoption. Strategic investments in clinical education programs, pharmacovigilance initiatives, and partnerships with hospital networks are shaping competitive dynamics, as market participants seek to establish stronger brand recognition and therapeutic credibility across India’s diverse healthcare ecosystem.

Recent Developments:

- In February 2025, the Central Drugs Standard Control Organisation (CDSCO) approved Edoxaban 15, 30, and 60 mg tablets for the prevention of systemic embolism and stroke in adult patients with nonvalvular atrial fibrillation, expanding the range of NOAC therapies available in the Indian market.

- In January 2024, AstraZeneca Pharma India received CDSCO approval for the import and marketing of Andexanet Alfa, a novel reversal agent designed to address life-threatening bleeding associated with Factor Xa inhibitor anticoagulants, marking a significant advancement in anticoagulation safety management in India.

India Anticoagulant Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Drug Classes Covered |

Novel Oral Anticoagulants (NOACs), Heparin and Low Molecular Weight Heparin (LMWH), Vitamin K Antagonist, Others |

|

Routes of Administration Covered |

Oral Anticoagulant, Injectable Anticoagulant |

|

Distribution Channels Covered |

Hospital Pharmacies, Retail Pharmacies, Online Stores, Others |

|

Applications Covered |

Atrial Fibrillation and Heart Attack, Stroke, Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India anticoagulant market size was valued at USD 727.9 Million in 2025.

The India anticoagulant market is expected to grow at a compound annual growth rate of 6.84% from 2026-2034 to reach USD 1,360.9 Million by 2034.

Novel oral anticoagulants (NOACs), representing the largest revenue share of 51.9% in 2025, dominate the India anticoagulant market owing to their predictable pharmacokinetics, fixed dosing schedules, reduced monitoring requirements, and increasing availability of affordable generic formulations from domestic manufacturers.

Key factors driving the India anticoagulant market include the escalating cardiovascular disease burden, aging population demographics, expanding government healthcare insurance coverage through Ayushman Bharat, growing adoption of novel oral anticoagulants, and strengthening domestic pharmaceutical manufacturing capacity.

Major challenges include limited awareness and diagnostic access in rural areas, physician hesitancy due to bleeding risk concerns, cost sensitivity among uninsured populations, inconsistent reimbursement coverage across state insurance schemes, and gaps in specialized coagulation monitoring infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)