India API Market Size, Share, Trends and Forecast by Type, Functionality and Purpose, Industry Vertical, and Region, 2026-2034

India API Market Size, Share, Trends & Forecast (2026-2034)

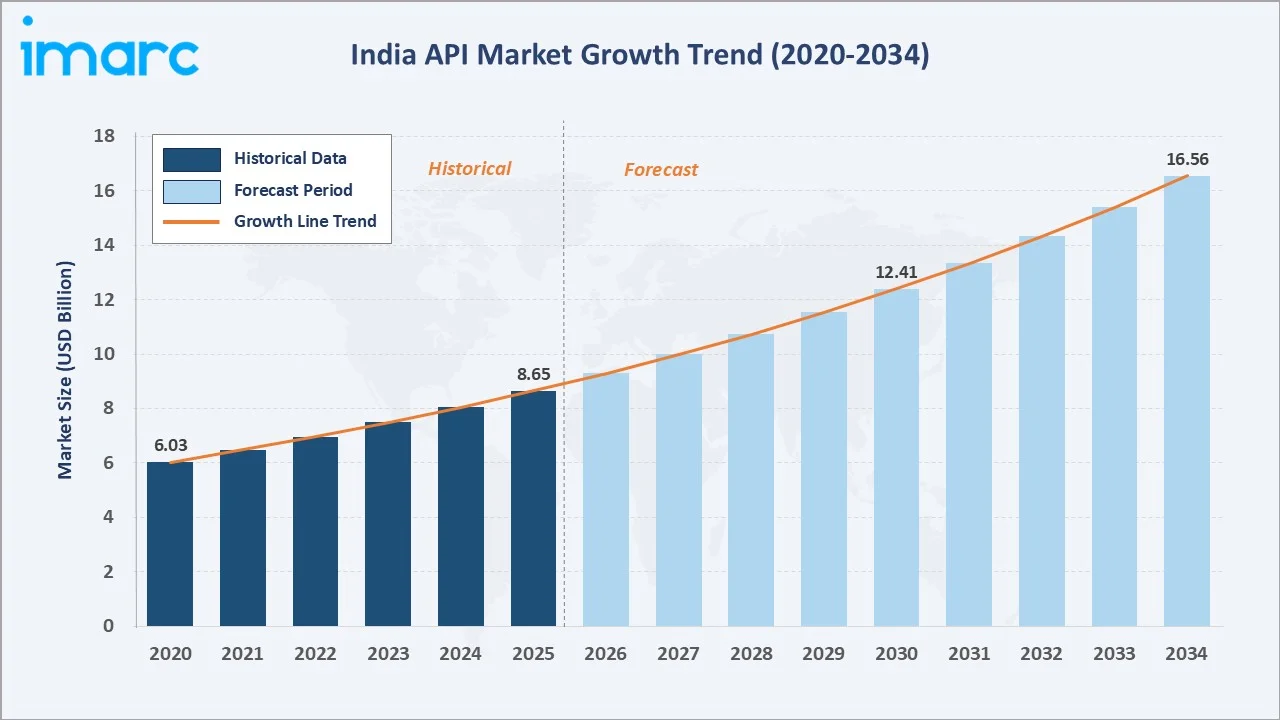

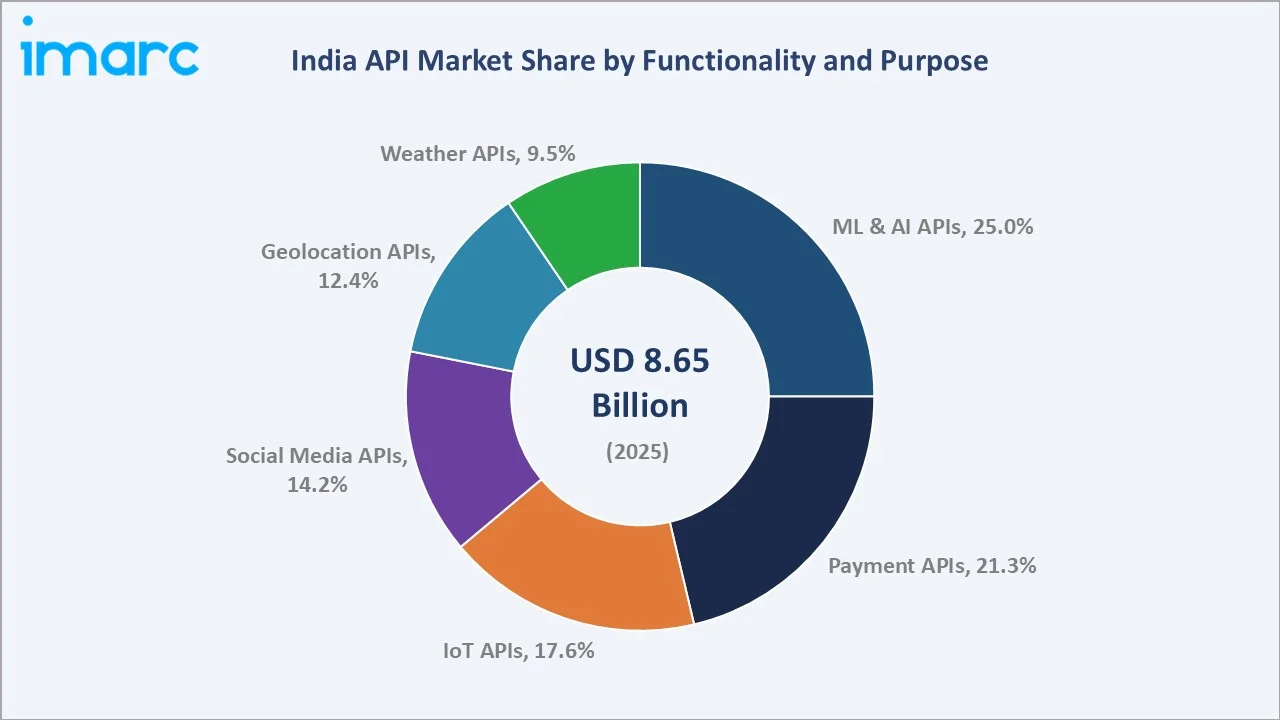

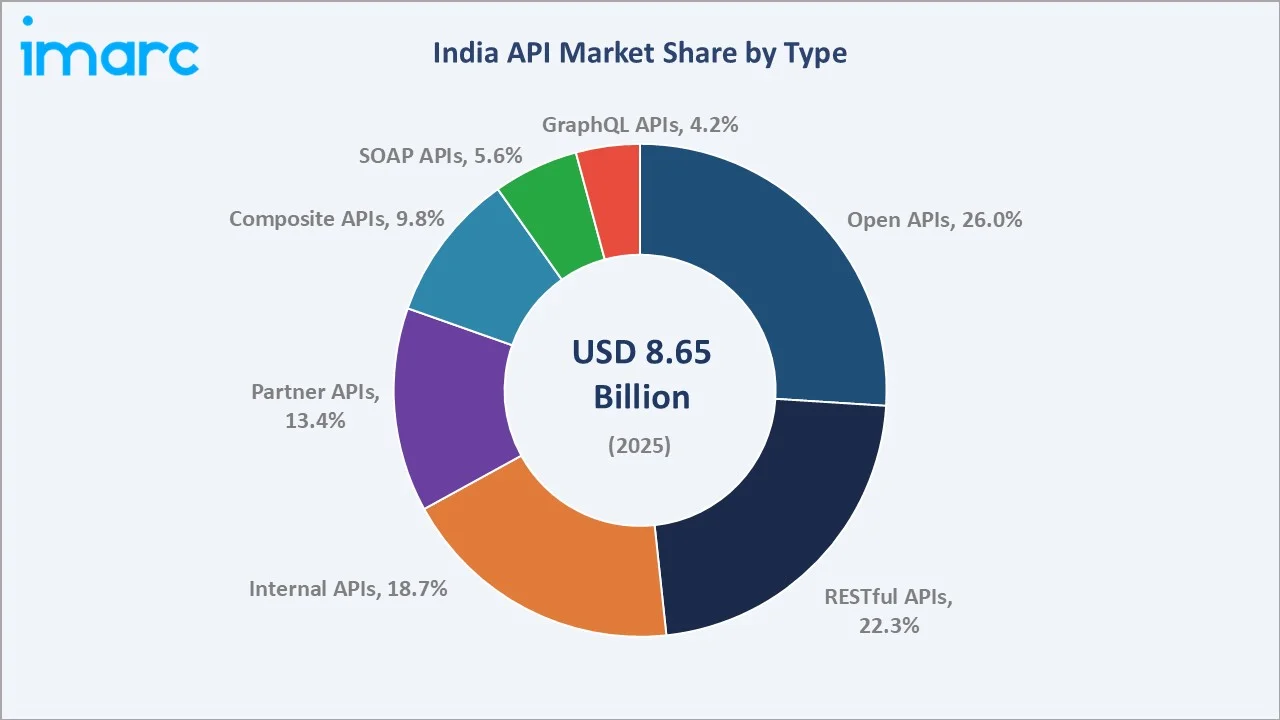

The India API market size was valued at USD 8.65 Billion in 2025 and is projected to reach USD 16.56 Billion by 2034, exhibiting a CAGR of 7.48% during the forecast period 2026-2034. The Digital India initiative, rapid fintech expansion, and surging demand for AI-driven software integration are powering India API market growth. Machine Learning and AI APIs dominate with a 25.0% share in 2025, while Open APIs command 26.0% by type. North India leads regionally at 30.0%, underpinned by Delhi NCR's government digital infrastructure and Gurugram's thriving startup ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.65 Billion |

|

Forecast Market Size (2034) |

USD 16.56 Billion |

|

CAGR (2026-2034) |

7.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (30.0% share, 2025) |

|

Fastest Growing Region |

South India (Rapid Digital Growth) |

|

Leading Segment (by Functionality) |

Machine Learning & AI APIs (25.0%, 2025) |

|

Leading Segment (by Type) |

Open APIs / Public APIs (26.0%, 2025) |

To get more information on this market, Request Sample

The India API market growth trajectory from 2020 through 2034 contrasts a robust historical CAGR of approximately 7.5% against a sustained forecast curve powered by cloud adoption, UPI-led fintech APIs, and enterprise AI integration demands across all industry verticals.

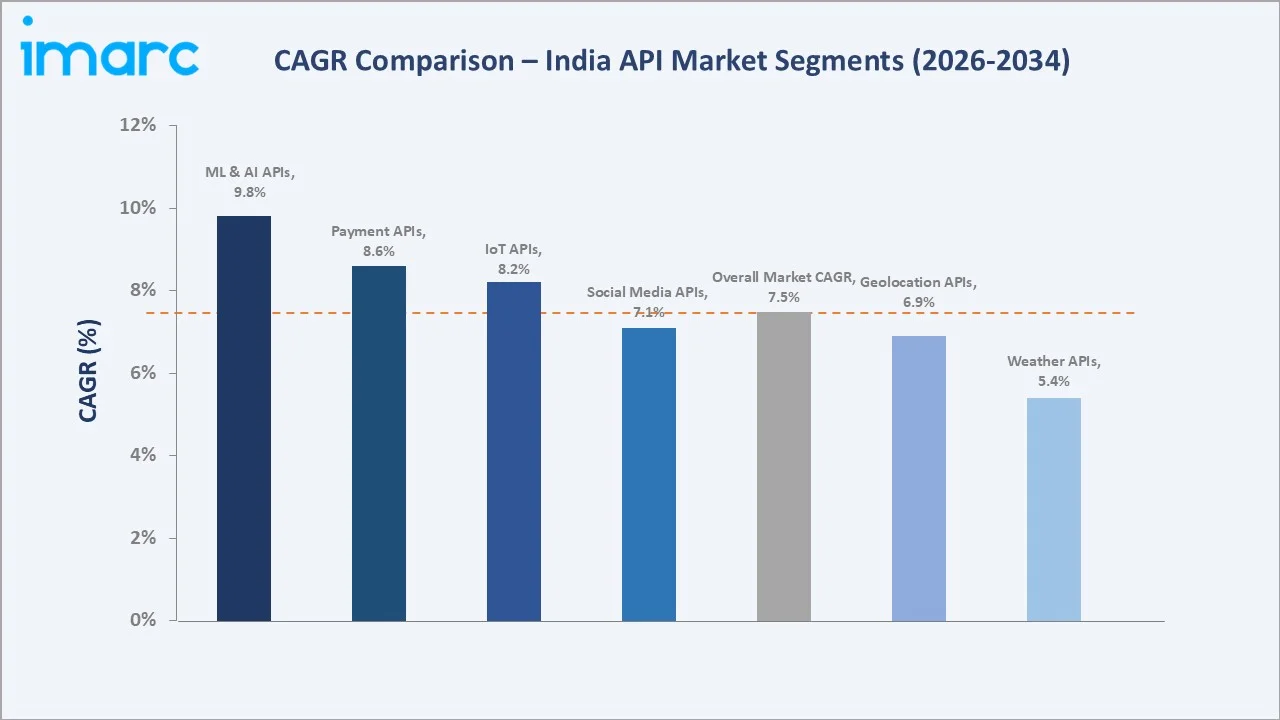

Segment-level CAGR comparisons highlight ML & AI API adoption and IoT API ecosystem expansion as the fastest-growing sub-categories within the India API market forecast through 2034.

Executive Summary

The India API market is undergoing a structural transformation, driven by government-led digitization mandates, rapid fintech proliferation, and the deepening penetration of cloud-native architecture across enterprises. Valued at USD 8.65 Billion in 2025, the market is forecast to more than double to USD 16.56 Billion by 2034 at a CAGR of 7.48%. The Unified Payments Interface (UPI) processed over 13,000 crore transactions in FY 2024-25, creating a massive payment API consumption layer that spans banks, fintechs, and e-commerce platforms.

Machine Learning and AI APIs hold the largest share at 25.0% in 2025, fueled by enterprise demand for intelligent automation, NLP-based chatbots, and recommendation engines. Payment APIs represent the second-largest segment at 21.3%, propelled by the Reserve Bank of India's (RBI) open banking framework and account aggregator regulations. Among API types, Open (Public) APIs lead at 26.0%, reflecting India's rapidly expanding developer ecosystem of over 5 million registered API developers in 2025.

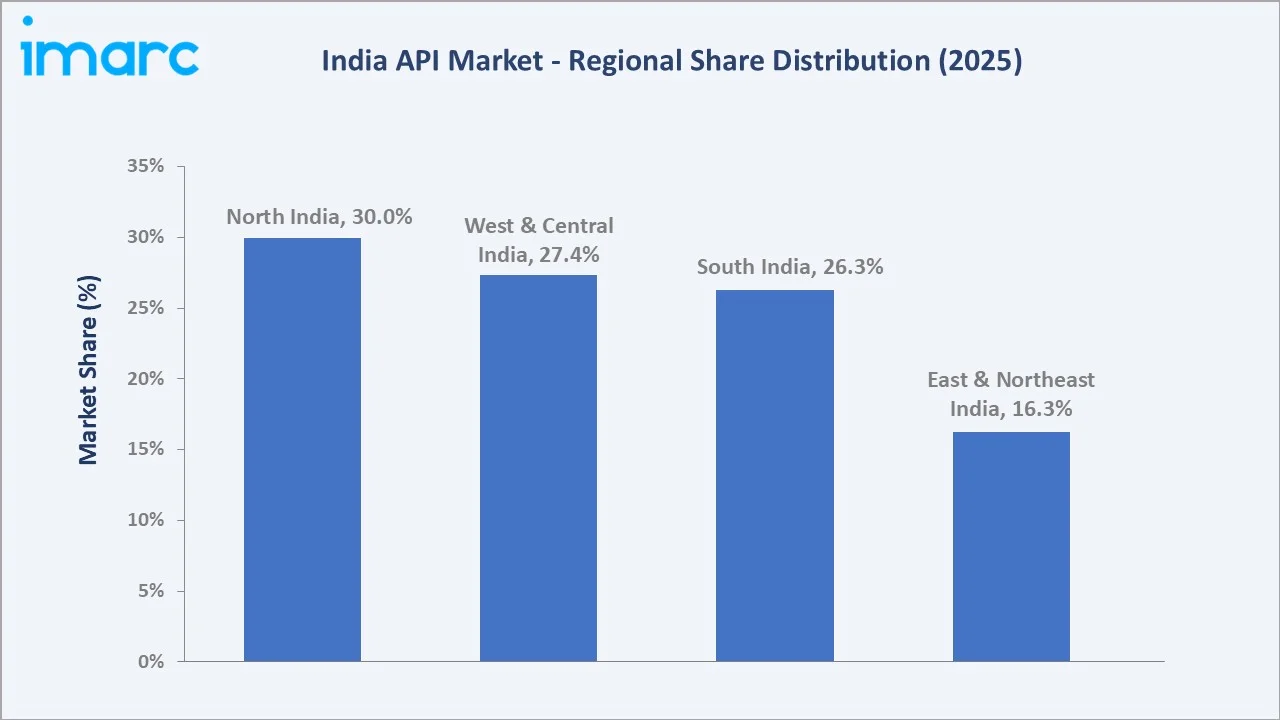

North India commands 30.0% of the market, anchored by Delhi NCR's concentration of government digital hubs and corporate headquarters. South India, led by Bangalore's world-class technology clusters, holds 26.3% and is the fastest-growing region. The India API market outlook remains highly positive as open banking, IoT-connected smart cities, and AI-led enterprise transformation collectively intensify API demand across all sectors through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Functionality) |

Machine Learning & AI APIs – 25.0% share (2025) |

|

Second Segment (Functionality) |

Payment APIs – 21.3% share (2025) |

|

Largest Segment (Type) |

Open APIs (Public APIs) – 26.0% share (2025) |

|

Fastest Growing Type |

GraphQL APIs – ~10.2% CAGR (2026-2034) |

|

Leading Region |

North India – 30.0% revenue share (2025) |

|

Fastest Growing Region |

South India – Accelerating at ~8.5% CAGR |

|

Top Companies |

Infosys, TCS, Wipro, Google (Apigee), Razorpay, AWS India |

|

Market Opportunity |

Fintech & AI/ML API convergence driven by RBI Open Banking mandates |

Key Analytical Observations Supporting the Above Data:

- ML & AI APIs' 25.0% dominance in 2025 reflects the rapid enterprise adoption of generative AI tools, natural language processing APIs, and machine vision services - areas in which Indian enterprises collectively raised an estimated USD 560 Million in AI infrastructure in FY 2024-25.

- Payment APIs' 21.3% share is directly correlated with India's fintech boom. UPI's 21.6 Billion transactions in FY 2025, combined with RBI's Account Aggregator framework enabling 50+ active entities, have created an unprecedented demand layer for standardized, compliance-ready payment APIs.

- Open APIs' 26.0% lead among types reflects India's developer-first ecosystem philosophy, with platforms such as the Government of India's Open Government Data (OGD) platform publishing over 4,500 APIs across ministries in 2025.

- GraphQL APIs are the fastest-growing type at an estimated 10.2% CAGR through 2034, gaining traction among product-led tech companies seeking flexible data querying capabilities for mobile-first applications.

- North India's 30.0% regional leadership is anchored by Delhi NCR's convergence of government digital transformation projects, a dense financial sector API consumer base, and the Gurugram-Noida startup corridor housing 4,200+ funded startups.

- South India is the fastest-growing region, underpinned by Bangalore's over 10,000 technology companies, Hyderabad's HITEC City housing 1,500+ IT firms, and deepening cloud-API adoption among both global multinationals and emerging startups.

India API Market Overview

Application Programming Interfaces (APIs) are the foundational connective tissue of modern digital ecosystems, enabling seamless communication between disparate software applications, platforms, and devices. The India API industry spans a diverse landscape including Payment APIs, Machine Learning APIs, IoT integration interfaces, Social Media connectors, Geolocation services, and Weather data APIs - each serving distinct enterprise and government use cases.

The market operates at the intersection of India's ambitious Digital India programme, the expanding startup economy, and surging demand for cloud-native software development practices. Macroeconomic enablers such as India's USD 3.7 Trillion GDP projection for 2027, a developer base exceeding 5 million, and one of the world's highest rates of mobile internet penetration at 86.3% in 2025 collectively position India as a high-velocity API consumption market. Regulatory frameworks including the RBI's Account Aggregator system and the Ministry of Electronics and Information Technology's (MeitY) National Open Digital Ecosystems (NODE) strategy are directly shaping the India API market trends and growth architecture.

Market Dynamics

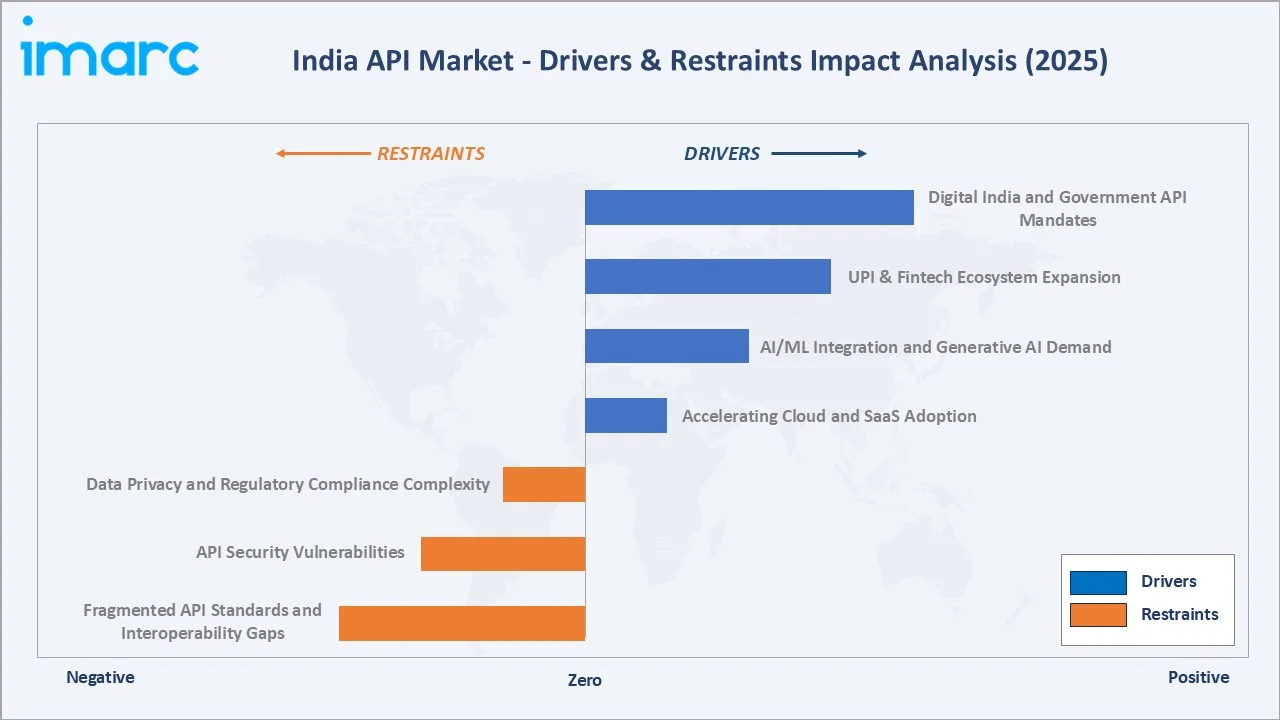

Market Drivers

- Digital India and Government API Mandates: The Indian government's Digital India programme, backed by a cumulative investment of over USD 18 Billion through 2025, has institutionalized API-first thinking across central and state governments. The Government of India's Open Government Data (OGD) platform hosts 4,500+ APIs, and MeitY's National Open Digital Ecosystem (NODE) strategy mandates interoperability standards, directly stimulating API adoption across 50+ government departments and allied private enterprises.

- UPI & Fintech Ecosystem Expansion: India's Unified Payments Interface processed 228.5 Billion transactions worth INR 299.75 Trillion in FY 2025, creating a massive, standardized payment API consumption layer. The RBI's Account Aggregator framework, with 50+ operational entities by mid-2025, has further institutionalized secure financial data APIs, unlocking embedded finance and BNPL use cases for 300+ fintech companies.

- Accelerating Cloud and SaaS Adoption: India's cloud services market reached USD 8.3 Billion in 2023, growing at 23% year-over-year. Cloud-native development paradigms - including microservices, serverless architecture, and containerized applications - inherently require API-based communication, directly driving demand for RESTful, GraphQL, and composite API solutions across enterprise IT, e-commerce, and logistics sectors.

- AI/ML Integration and Generative AI Demand: Indian enterprises raised an estimated USD 560 Million in AI infrastructure in FY 2024-25. The rapid commercialization of large language models (LLMs), computer vision APIs, and predictive analytics services is accelerating ML & AI API consumption, particularly in BFSI, healthcare, retail, and edtech verticals.

Market Restraints

- Data Privacy and Regulatory Compliance Complexity: India's Digital Personal Data Protection (DPDP) Act 2023, effective 2025, introduces stringent data localization and consent management requirements. API providers must invest in compliance infrastructure, adding development cost and deployment complexity, which particularly constrains smaller API developers and startups operating on limited budgets.

- API Security Vulnerabilities: India's Computer Emergency Response Team (CERT-In) reported a 30% year-on-year increase in API-related cybersecurity incidents in 2024. Insecure API endpoints, broken object-level authorization, and lack of rate limiting remain critical vulnerabilities, raising enterprise risk concerns and slowing adoption in sensitive sectors such as healthcare and government banking.

- Fragmented API Standards and Interoperability Gaps: The absence of unified API governance frameworks across India's heterogeneous enterprise landscape - spanning legacy mainframe systems, mid-tier ERP platforms, and modern SaaS stacks - creates significant integration friction, increasing API management costs and limiting seamless multi-cloud API orchestration.

Market Opportunities

- Open Banking and Account Aggregator Ecosystem: The RBI's Account Aggregator framework and proposed Open Banking regulations present APIs opportunity through 2030, enabling consented financial data sharing across banks, NBFCs, and fintechs. Over 2.2 Billion financial data-sharing requests were processed by the AA network in FY 2024-25, signalling exponential growth potential for standardized financial APIs.

- Smart Cities and IoT API Integration: India's Smart Cities Mission, covering 100 cities with a cumulative budget of INR ₹1,64,678 Crore through 2025, is creating substantial demand for IoT-connected APIs spanning urban mobility, smart utilities, surveillance, and citizen services.

- 5G-Enabled API Services: India's telecom operators - Reliance Jio, Airtel, and BSNL - are deploying 5G network APIs that enable ultra-low latency, network slicing, and edge computing capabilities. The GSMA estimates that 5G API-driven services could generate USD 300 Billion in global revenues by 2030, with India expected to represent a 12-15% share.

Market Challenges

- Developer Skill Gaps in Advanced API Technologies: Despite India's large developer pool of 5+ million, a significant skill gap persists in advanced API security protocols, GraphQL schema design, API lifecycle management, and AI/ML API integration. This constrains the pace of high-complexity API development and deployment, particularly in tier-2 and tier-3 city technology hubs.

- Monetization Models and API Commercialization: A majority of Indian API providers still operate on freemium or cost-centre models rather than revenue-generating API monetization strategies. The transition to mature API product management, developer experience investment, and usage-based pricing models remains a significant operational challenge for both startups and large IT services firms.

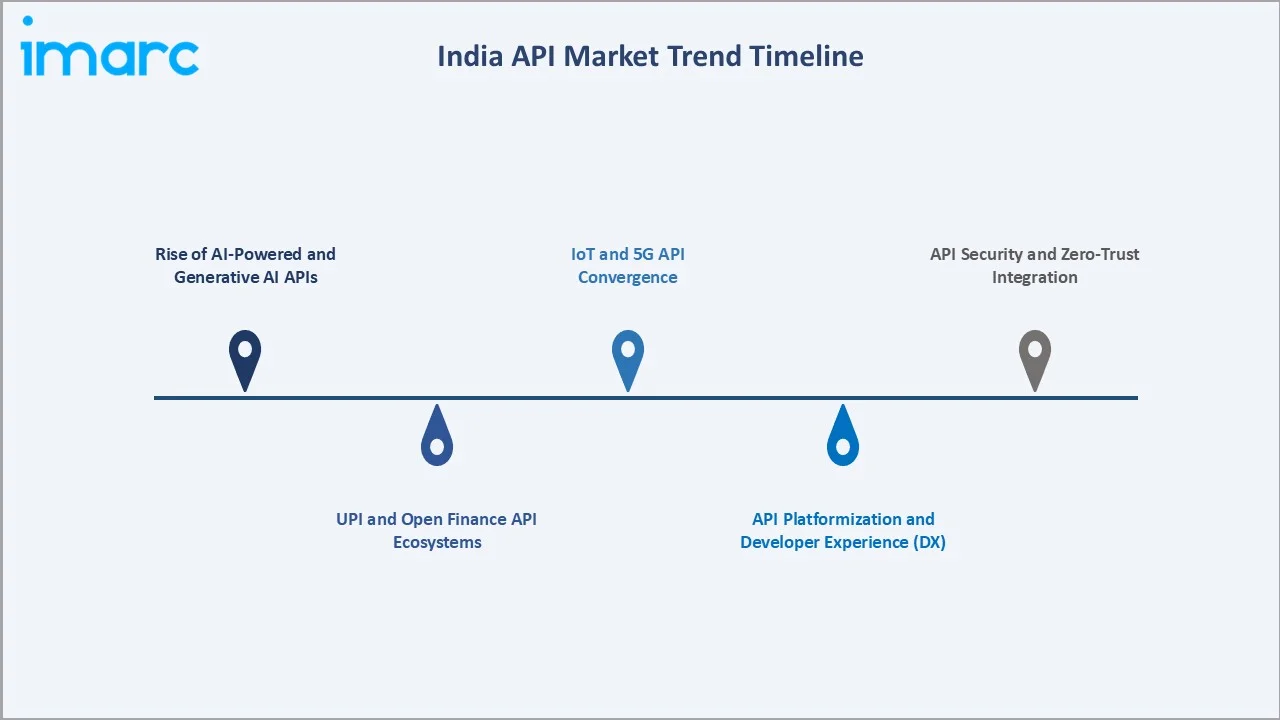

Emerging Market Trends

1. Rise of AI-Powered and Generative AI APIs

Generative AI APIs, led by OpenAI's GPT models and Google's Gemini, are being rapidly integrated into Indian enterprise software stacks. Indian SaaS companies registered a 59% share in AI API consumption between 2023 and 2025. This trend is fundamentally reshaping enterprise workflows in BFSI, healthcare, legal tech, and edtech, where AI APIs drive conversational interfaces, document processing, and predictive decisioning at scale.

2. UPI and Open Finance API Ecosystems

India's Account Aggregator network processed 2.2 Billion consent-based data requests in FY 2024-25, reflecting the explosive growth of open finance API ecosystems. RBI's proposed Open Banking Guidelines, expected to be finalized by 2026, will formalize standardized API specifications for financial data sharing, directly unlocking credit assessment APIs, embedded lending, and insurance distribution use cases for 300+ fintech operators.

3. API Platformization and Developer Experience (DX)

Indian enterprises are shifting from point-to-point integration toward API platform strategies, creating centralized API gateways, internal developer portals, and self-service API marketplaces. Platforms such as MuleSoft and Apigee are gaining rapid traction. Developer experience (DX) investment - encompassing comprehensive API documentation, sandbox environments, and SDKs - has emerged as a key competitive differentiator for API providers targeting India's strong developer community.

4. IoT and 5G API Convergence

India's 5G subscriber base surpassed 250 Million in 2025, enabling telecom operators to offer network-as-a-service (NaaS) APIs for enterprise IoT deployments. IoT API usage in smart manufacturing, precision agriculture, connected logistics, and urban infrastructure is expanding at 8.2% CAGR. The convergence of 5G connectivity APIs with IoT device management APIs is creating new revenue streams for both telecom operators and API middleware providers.

5. API Security and Zero-Trust Integration

Following a 30% rise in API-related cybersecurity incidents in 2024, Indian enterprises are significantly increasing API security investments. Zero-trust API security frameworks, OAuth 2.0 and OpenID Connect implementations, and AI-powered anomaly detection for API traffic are becoming standard. MeitY's Cyber Surakshit Bharat initiative and CERT-In's expanded API security guidelines are further institutionalizing security-first API development practices across government and enterprise ecosystems.

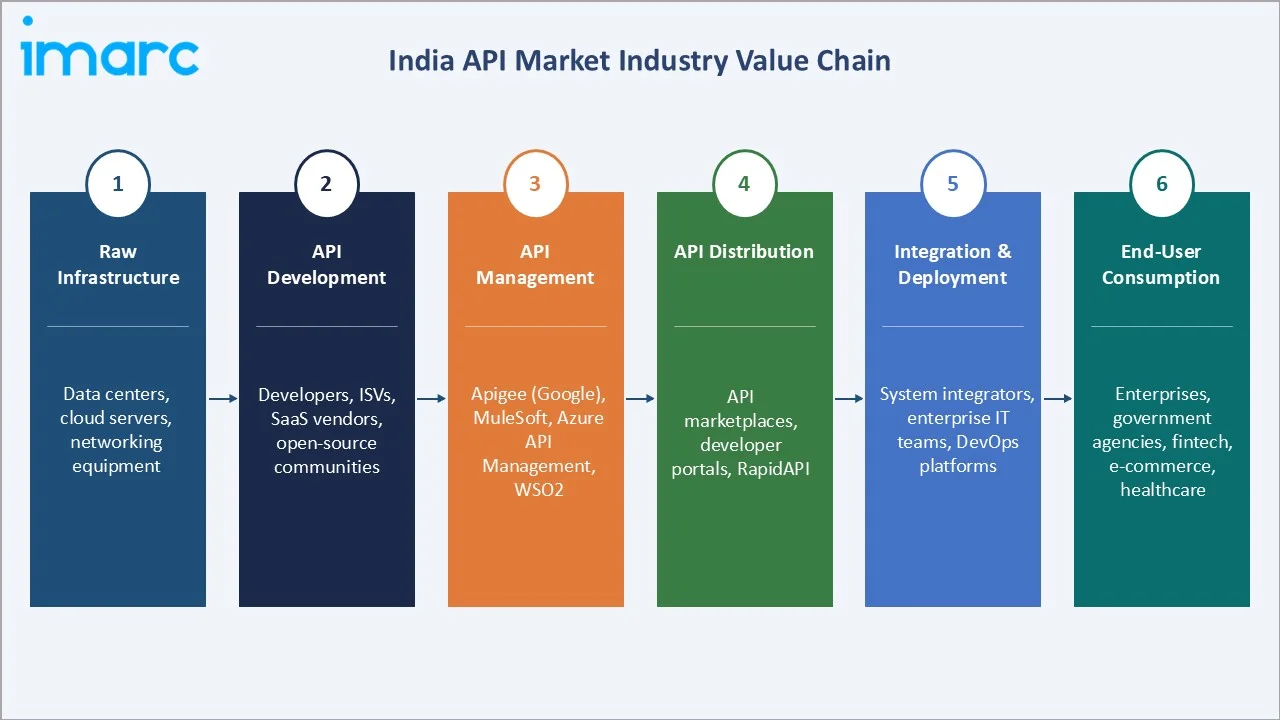

Industry Value Chain Analysis

The India API industry value chain spans six integrated stages from raw infrastructure provisioning through end-consumer API consumption. Each stage presents distinct competitive dynamics, investment requirements, and strategic opportunity relevant to the overall India API market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Infrastructure |

Data centers, cloud servers, networking equipment |

|

API Development |

Developers, ISVs, SaaS vendors, open-source communities (Node.js, Python, Java) |

|

API Management |

Apigee (Google), MuleSoft (Salesforce), Azure API Management, WSO2 |

|

API Distribution |

API marketplaces, developer portals, RapidAPI |

|

Integration & Deployment |

System integrators, enterprise IT teams, DevOps platforms, CI/CD pipelines |

|

End-User Consumption |

Enterprises, government agencies, fintech, e-commerce, healthcare, SMBs |

API management platforms hold the highest strategic value in the chain by consolidating governance, security, analytics, and lifecycle management into a single control plane. Meanwhile, API marketplaces and developer portals are reshaping distribution, allowing API providers to reach enterprise clients directly while building monetizable developer communities. Integrators and system integrators continue to play a critical bridging role, particularly in connecting legacy enterprise systems with modern cloud-native API architectures.

Technology Landscape in the India API Industry

RESTful and GraphQL API Architecture

REST remains the dominant API architectural style in India, commanding 22.3% of the API type market in 2025, favoured for its simplicity, statelessness, and compatibility with web and mobile applications. GraphQL is the fastest-growing protocol at an estimated 10.2% CAGR through 2034, increasingly adopted by product-led technology companies for its superior flexibility in querying nested data structures - a critical capability for India's complex, microservices-based e-commerce and fintech platforms.

AI/ML Integration and Intelligent API Capabilities

Machine Learning and AI APIs constitute 25.0% of the India API market in 2025 and represent the highest-growth functionality tier. Large language model (LLM) APIs from providers such as OpenAI, Google Gemini, and Anthropic are increasingly embedded into Indian SaaS products. Domestic AI API providers including Sarvam AI and Krutrim are building India-specific LLM APIs optimized for 22 scheduled Indian languages, creating a localized AI API layer with significant enterprise and government demand potential.

API Security and Zero-Trust Technologies

API security technologies including OAuth 2.0, OpenID Connect, mTLS, and API gateway-based rate limiting are becoming mandatory components of enterprise API stacks in India. AI-powered API threat detection platforms, which analyze API traffic patterns to identify anomalies and injection attacks in real time, are emerging as a fast-growing technology sub-segment. India's CERT-In expanded its API security advisories in 2024, accelerating enterprise investment in runtime API protection solutions.

API Management Platforms and DevOps Integration

Cloud-native API management platforms - including Google Apigee, MuleSoft Anypoint, and Azure API Management, - are experiencing rapid adoption growth in India. The integration of API lifecycle management with CI/CD pipelines, Infrastructure-as-Code (IaC) frameworks, and GitOps workflows is enabling Indian enterprises to deploy and scale APIs at significantly higher velocity, reducing average API time-to-market from weeks to hours.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India API market, along with forecasts at the regional and national level from 2026 to 2034. The market has been analyzed based on Functionality and Purpose and Type.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Open APIs (Public APIs) |

26.0% |

2025 |

|

Functionality and Purpose |

Machine Learning and AI APIs |

25.0% |

2025 |

|

Industry Vertical |

Financial API |

29.0% |

2025 |

|

Region |

North India |

30.0% |

2025 |

By Functionality and Purpose

To access detailed market analysis, Request Sample

Machine Learning and AI APIs lead the functionality segment with a 25.0% market share in 2025. India's enterprise AI adoption has surged 68% between 2022 and 2025, with BFSI, e-commerce, and healthcare sectors driving the highest API consumption. Domestic AI platforms from companies such as Sarvam AI and Krutrim are supplementing global LLM API providers, creating a vibrant multi-vendor AI API ecosystem. This segment is forecast to grow at approximately 9.8% CAGR through 2034, underpinned by India's National AI Mission with a dedicated budget of INR 10,372 Crore (approximately USD 1.3 Billion) announced in 2024.

Payment APIs hold a 21.3% share in 2025, the second-largest segment. UPI's 13,116 crore transactions in FY 2024-25 have created a massive, standardized payment API layer consumed by 300+ licensed payment system operators. The RBI's Payments Vision 2025 framework and account aggregator regulations are further expanding payment API use cases into embedded lending, BNPL, and cross-border remittance corridors.

IoT APIs represent 17.6% of the functionality market. India's Smart Cities Mission and IIOT adoption in manufacturing, agriculture, and logistics are driving IoT API demand. The Indian IoT market is projected to exceed USD 15 Billion by 2027, with every connected device requiring API-based data exchange.

Social Media APIs account for 14.2%, driven by India's 462 Million social media users in 2025. Geolocation APIs hold 12.4%, propelled by Zomato, Ola, and Flipkart's logistics intelligence platforms. Weather APIs, at 9.5%, serve agriculture, logistics, and insurance sectors.

By Type

Open APIs (Public APIs) command the largest share at 26.0% in 2025. The Government of India's OGD platform, RBI's open banking APIs, and tech giants' public API programs (Google Maps, Twitter/X API, Meta Graph API) collectively drive this segment. Open APIs are the primary vehicle for India's thriving third-party developer ecosystem, estimated at 5 Million+ registered API developers in 2025.

RESTful APIs hold 22.3% and remain the dominant technical standard across web, mobile, and cloud-native applications. Internal (Private) APIs represent 18.7%, widely used within large Indian conglomerates and IT services firms for internal system integration. Partner APIs at 13.4% are critical for B2B ecosystems, particularly in supply chain, logistics, and insurance distribution.

Composite APIs at 9.8% are gaining traction in complex enterprise workflows requiring orchestrated multi-service calls. SOAP APIs at 5.6% serve legacy BFSI and government applications. GraphQL APIs at 4.2% are the fastest-growing type at ~10.2% CAGR, driven by product-led SaaS companies requiring flexible, client-specified data fetching.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.0% |

Government Digital India hubs (Delhi NCR), major IT parks, BFSI sector API demand, startup ecosystem in Gurugram and Noida |

|

West & Central India |

27.4% |

Fintech capital Mumbai, Pune IT corridor, Maharashtra ITPOL, strong e-commerce and payment API consumption |

|

South India |

26.3% |

Bangalore tech hub (Silicon Valley of India), Chennai IT exports, Hyderabad HITEC City, strong cloud and AI API adoption |

|

East & Northeast India |

16.3% |

Kolkata emerging BPO sector, Bhubaneswar IT parks, government digitization API consumption, growing startup activity |

North India commands 30.0% of the India API market in 2025. Delhi NCR serves as India's government digital hub, with MeitY, UIDAI, NPCI, and major public-sector banks headquartered in the region. The Gurugram-Noida corridor hosts 4,200+ funded startups and the Indian operations of leading MNCs, creating a concentrated enterprise API consumption cluster. The National Capital Region's fintech density - including Paytm, PolicyBazaar, and IndiaMart - further amplifies payment, insurance, and commerce API demand.

West and Central India holds 27.4%, with Mumbai serving as India's financial capital. The BFSI sector's concentration in Mumbai drives substantial consumption of payment APIs, compliance APIs, and financial data APIs. Pune's IT corridor, home to 1,500+ IT companies, supplements API development demand. Maharashtra's ITPOL industrial parks are attracting API management platform investments, while e-commerce giants operating from Gujarat and Maharashtra generate high-volume logistics and payment API traffic.

South India represents 26.3% and is the fastest-growing region at an estimated 8.5% CAGR. Bangalore's ecosystem of 10,000+ technology companies, 400+ global capability centers (GCCs), and 10,000+ active startups makes it the epicenter of India's API innovation. Hyderabad's HITEC City houses 1,500+ IT companies and is a key hub for cloud API services from Microsoft, Amazon, and Google. Chennai's IT export strength and emerging deep-tech startup scene further reinforce South India's API market momentum.

East and Northeast India accounts for 16.3%, the smallest but increasingly relevant regional share. Kolkata's emerging BPO sector and Bhubaneswar's Infovalley IT park are driving gradual API adoption. Government digitization programs under the Digital North East initiative, focusing on e-governance, digital payments, and healthcare digitization, are creating structured API demand in the region. The government's USD 1.2 Billion Digital North East vision 2022-2030 is gradually unlocking API infrastructure investment across these states.

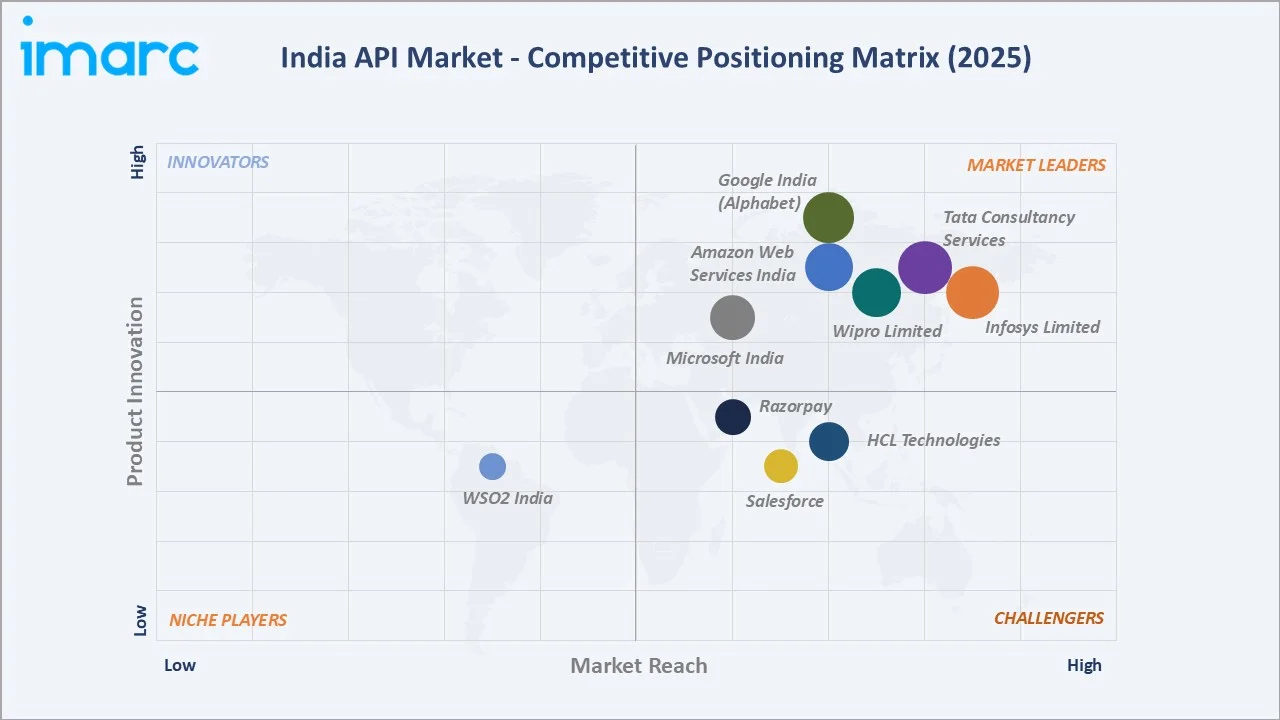

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Infosys Limited |

Finacle API Connect |

Leader |

Enterprise banking APIs, global delivery, deep domain expertise |

|

Tata Consultancy Services |

TCS API Management Solution on Google Cloud |

Leader |

Scale, IT services, government digitization APIs |

|

Wipro Limited |

Wipro API |

Leader |

Cloud-native API development, AI/ML integration |

|

Google India (Alphabet) |

Apigee |

Leader |

Best-in-class API management platform, GCP ecosystem |

|

Amazon Web Services India |

AWS API Gateway |

Leader |

Serverless API management, massive developer base |

|

Microsoft India |

Azure API Management |

Leader |

Enterprise cloud APIs, hybrid integration strength |

|

Razorpay |

Razorpay Payment API |

Challenger |

Dominant fintech payment APIs, SMB-focused, RBI-compliant |

|

Salesforce |

Mulesoft API |

Challenger |

Enterprise integration, iPaaS leadership |

|

HCL Technologies |

HCL Digital Experience (DX) |

Challenger |

API management, telecom and manufacturing APIs |

|

WSO2 India |

WSO2 API Manager |

Emerging |

Open-source API management, growing enterprise traction |

The India API market's competitive landscape is moderately fragmented, with global technology platforms, Indian IT services majors, and specialized fintech API providers competing across different segments. Leading players differentiate through platform capabilities, regulatory compliance depth, and developer ecosystem strength. Indian IT services giants such as Infosys and TCS compete through domain-specific API solutions for banking, insurance, and government sectors, while global platforms (Google Apigee, AWS API Gateway, Azure APIM) compete on the breadth of managed API infrastructure services.

Strategic acquisitions and partnerships are reshaping the landscape. In December 2024, Infosys deepened its partnership with Apigee (Google Cloud) to co-sell API management solutions to Indian banking clients. In 2025, Razorpay launched its RazorpayX Business Banking API suite, targeting India's MSME segment with embedded financial service APIs. The domestic API economy is also witnessing the rise of Indian-origin API management challengers such as WSO2's India operations, which expanded its Bangalore development center.

Key Company Profiles

Infosys Limited

Infosys Limited is one of India's largest IT services and consulting companies, headquartered in Bangalore, Karnataka. Founded in 1981, Infosys serves 1,800+ clients across 56 countries, generating revenues of USD 18.6 Billion in FY 2024-25. Its Finacle core banking platform is deployed in 100+ countries, making Infosys a dominant provider of domain-specific financial APIs globally.

- Platform & API Portfolio: Infosys offers the Finacle API Suite for open banking, the Infosys Cobalt cloud API platform for enterprise integration, and the Live Enterprise Suite featuring over 100 pre-built APIs across HR, finance, and supply chain domains. Its AI API offerings through Infosys Topaz cover generative AI, NLP, and analytics capabilities.

- Recent Developments: In March 2025, Infosys announced a strategic alliance with Google Cloud to jointly deliver Apigee-powered API management solutions to Indian banking clients. In Q3 FY25, Infosys launched its open banking API accelerator for Indian cooperative banks, enabling compliance with RBI Account Aggregator specifications within 8 weeks.

- Strategic Focus: Infosys's strategy centers on scaling its open banking API platform globally while deepening AI API capabilities through the Infosys Topaz programme, targeting USD 2 Billion in AI-related revenues by FY 2026.

Tata Consultancy Services (TCS)

TCS is India's largest IT services company by revenue, headquartered in Mumbai, with FY 2024-25 revenues of USD 30 Billion. TCS serves 600+ clients across BFSI, retail, manufacturing, and government sectors globally, with a significant presence in India's digital transformation programmes.

- Platform & API Portfolio: TCS offers the TCS API Gateway for enterprise middleware integration, TCS BaNCS open banking APIs serving 500+ financial institutions globally, and TCS iON APIs for education and government digital services. Its TCS Cognix AI platform exposes ML and analytics APIs for enterprise consumption.

- Recent Developments: In January 2025, TCS launched API-first modernization frameworks for Indian public sector banks, enabling core banking API migration aligned with RBI's open banking roadmap. TCS also expanded its digital services to MeitY's DigiLocker platform, integrating document verification APIs for 500+ government use cases.

- Strategic Focus: TCS focuses on scaling its API-led digital transformation offerings for the Indian government and BFSI sector while expanding its global API services footprint through TCS BaNCS's open banking platform.

Google India (Apigee - Alphabet Inc.)

Google India operates as the Indian subsidiary of Alphabet Inc., providing cloud services, AI platforms, and API management solutions through Google Cloud and its Apigee API Management platform. Apigee is globally recognized as one of the most comprehensive API management suites, covering design, security, analytics, and monetization.

- Platform & API Portfolio: Google India offers Apigee API Management (full lifecycle management), Google Maps Platform APIs (used by Ola, Zomato, Swiggy), Google Cloud AI APIs (Vision, NLP, Translation, Vertex AI), and Firebase APIs for mobile-first Indian app developers. Gemini AI APIs are rapidly gaining adoption among Indian generative AI startups.

- Recent Developments: In 2024-25, Google India expanded its Apigee for open banking program in partnership with NPCI, supporting UPI API standardization. In March 2025, Google India announced a USD 15 Billion investment in Indian AI and cloud infrastructure over the next two years, directly expanding the capacity for API platform services.

- Strategic Focus: Google India's strategy centers on making Apigee the de facto API management platform for Indian enterprises, government, and fintechs, while leveraging Gemini's generative AI APIs to capture the rapidly growing AI API market.

Market Concentration Analysis

The India API market exhibits moderate fragmentation. The top five players - Infosys, TCS, Google (Apigee), AWS India, and Microsoft Azure - collectively account for an estimated 32-38% of India API market revenue in 2025. The remaining market share is distributed across Wipro, HCL Technologies, Razorpay, MuleSoft, WSO2, and a large number of niche API providers and domestic startups.

The market is experiencing a bifurcated dynamic. At the enterprise API platform tier, consolidation is occurring around platform breadth, AI API capabilities, and regulatory compliance (particularly for RBI open banking and DPDP Act alignment). Simultaneously, the Indian fintech and SaaS startup ecosystem is generating a second tier of specialized, domain-specific API providers in areas such as insurance aggregation APIs, agricultural data APIs, healthcare records APIs, and legal document APIs.

This dual dynamic - consolidation at the platform tier and proliferation at the domain-specific API tier - is creating an increasingly layered competitive environment through 2034. Large IT services firms are evolving toward API platform businesses while simultaneously acquiring domain-specific API startups to build vertical API portfolios. This consolidation trend is expected to intensify between 2026 and 2030 as open banking regulations and AI mandates create winner-take-most dynamics in high-regulation API segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Machine Learning and AI APIs are the highest-growth functionality sub-segment at approximately 9.8% CAGR through 2034. GraphQL APIs are the fastest-growing type at ~10.2% CAGR, reflecting the shift toward flexible, client-driven data querying by India's product-led software companies. Open Banking and Account Aggregator APIs represent the most structurally significant payment API growth opportunity, underpinned by RBI regulatory mandates and 2.2 Billion AA network data requests in FY 2024-25.

Emerging Market Expansion

Tier-2 and tier-3 Indian cities represent significant untapped API market potential. Government schemes including PM GatiShakti (digital infrastructure) and BharatNet (rural broadband) are extending high-speed internet to 600,000+ villages, creating new API consumption endpoints in agriculture, healthcare, and rural fintech. The INR 10,372 Crore National AI Mission (2024) is catalyzing AI API development across academic, government, and commercial sectors simultaneously.

Venture and Strategic Investment Trends

Indian API economy startups, with fintech API, health-tech API, and AI API verticals commanding the highest deal values. Notable investments include Sarvam AI's USD 41 Million Series A (2024) for India-specific language model APIs, and Perfios's USD 229 Million funding round (2023) for financial data APIs. Strategic investments by AWS, Google, and Microsoft in Indian data center infrastructure - exceeding USD 10 Billion combined through 2025 - are directly expanding the managed API infrastructure capacity in the country.

Future Market Outlook (2026-2034)

The India API market forecast projects steady value expansion from USD 8.65 Billion in 2025 to USD 16.56 Billion by 2034 at a CAGR of 7.48%. An intermediate milestone of USD 12.41 Billion by 2030 reflects the market's strong mid-period acceleration driven by open banking regulation finalization, 5G API service commercialization, and India's increasing role as a global technology export hub.

Technological disruptions that will shape the market through 2034 include: the proliferation of Agentic AI - autonomous AI agents consuming and orchestrating multiple APIs simultaneously - which could expand AI API consumption by 3-5x beyond current projections; quantum-safe API encryption standards mandated by MeitY post-2028 as quantum computing capabilities mature; and the emergence of Intent-Based APIs driven by large language models where natural language requests are automatically translated into API calls without developer coding.

India's growing role as a global API talent and innovation hub - supplying a disproportionate share of global API developer talent and increasingly originating global API platform companies - positions the country for compounding structural advantages in the API economy through 2034. The convergence of Digital India's infrastructure investments, RBI's progressive open banking framework, India's National AI Mission, and the 5G network buildout collectively support a positive long-term India API market outlook.

Research Methodology

Primary Research

Primary research forms the qualitative and validation backbone of this report. IMARC Group's analysts conducted structured interviews and expert consultations with API product managers, Chief Technology Officers at Indian enterprises, fintech API developers, regulatory compliance officers at RBI-licensed entities, and API platform sales executives. Primary research inputs were used to validate market size estimates, segment growth projections, competitive positioning assessments, and emerging trend identification.

Secondary Research

Secondary research drew upon an extensive range of authoritative sources including: Reserve Bank of India (RBI) regulatory publications and Account Aggregator framework updates; Ministry of Electronics and Information Technology (MeitY) policy documents and Digital India mission reports; National Payments Corporation of India (NPCI) UPI transaction data; NASSCOM industry reports on Indian IT and API economy; IDC India, Gartner, and Forrester research on cloud and API management markets; and company annual reports, investor presentations, and press releases for profiled competitors.

Forecasting Models

Market size forecasts were developed using a combination of bottom-up and top-down estimation approaches. Bottom-up modeling aggregated revenue data across API type segments, functionality categories, and regional markets. Top-down validation cross-referenced India GDP growth projections, enterprise IT spending indices, and cloud market expansion rates. A Compound Annual Growth Rate (CAGR) of 7.48% was derived through triangulation of multiple data sources and scenario analysis covering optimistic, base, and conservative growth trajectories through 2034.

India API Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Open APIs (Public APIs), Partner APIs, Internal APIs (Private APIs), Composite APIs, RESTful APIs, SOAP APIs, GraphQL APIs |

| Functionality and Purposes Covered | Payment APIs, Geolocation APIs, Social Media APIs, Weather APIs, Machine Learning and AI APIs, IoT APIs |

| Industry Verticals Covered | Healthcare API, Financial API, Retail and E-commerce API, Travel and Hospitality API, Telecommunications API, Automotive API, Government and Public Sector API |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Infosys Limited, Tata Consultancy Services, Wipro Limited, Google India (Alphabet), Amazon Web Services India, Microsoft India, Razorpay, Salesforce, HCL Technologies, WSO2 India, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India API Market Report

The India API market was valued at USD 8.65 Billion in 2025 and is projected to reach USD 16.56 Billion by 2034, growing at a CAGR of 7.48% during 2026-2034.

The market is projected to expand at a CAGR of 7.48% from 2026 to 2034, driven by digital India mandates, fintech growth, and accelerating AI/ML API adoption across industries.

Machine Learning and AI APIs lead with 25.0% market share in 2025, followed by Payment APIs at 21.3% and IoT APIs at 17.6%, reflecting enterprise AI and fintech API consumption growth.

Open APIs (Public APIs) lead with 26.0% share in 2025, followed by RESTful APIs at 22.3% and Internal (Private) APIs at 18.7%, underpinned by India's developer-first API philosophy.

North India leads with 30.0% market share in 2025, anchored by Delhi NCR's government digital hubs, BFSI API demand, and the Gurugram-Noida startup ecosystem.

South India is the fastest-growing region, driven by Bangalore's 10,000+ tech companies, Hyderabad's HITEC City, and accelerating cloud and AI API adoption at an estimated 8.5% CAGR.

Key drivers include the Digital India initiative, UPI-led fintech expansion processing 13,000+ crore transactions in FY25, accelerating cloud adoption, AI/ML demand, and RBI's open banking framework.

Key players include Infosys, TCS, Wipro, Google India (Apigee), Amazon Web Services India, Microsoft Azure, Razorpay, Salesforce (MuleSoft), HCL Technologies, and WSO2 India.

The India API market is forecast to reach USD 12.41 Billion by 2030, representing a key intermediate milestone supported by 5G commercialization, open banking regulations, and AI API proliferation.

The AA framework processed 1.8 Billion data-sharing requests in FY 2024-25, creating significant demand for standardized financial APIs across 50+ licensed entities in banking, insurance, and wealth management.

Digital India's USD 18 Billion cumulative investment through 2025 and MeitY's NODE strategy directly mandate API-first interoperability across government systems, driving structured API demand from 50+ central ministries.

Key opportunities include open banking API ecosystems, 5G network APIs, AI/ML API platforms targeting India's National AI Mission, IoT Smart Cities APIs, and GraphQL adoption by India's fast-growing SaaS product companies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)