India ATM Market Size, Share, Trends and Forecast by Solution, Screen Size, Application, ATM Type, and Region, 2026-2034

India ATM Market Summary:

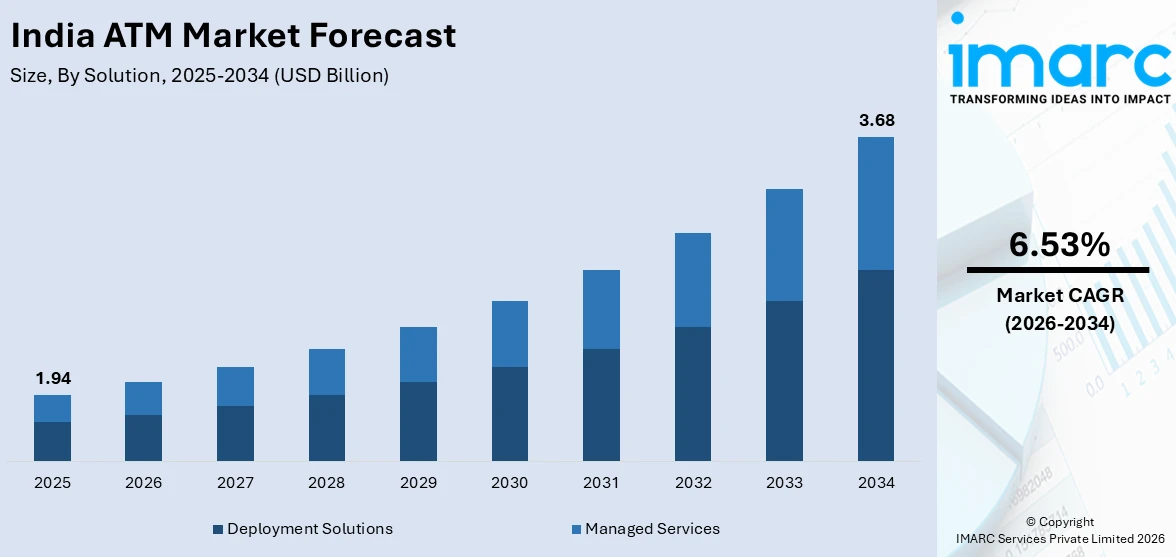

The India ATM market size was valued at USD 1.94 Billion in 2025 and is projected to reach USD 3.68 Billion by 2034, growing at a compound annual growth rate of 6.53% during 2026-2034.

The India ATM market is driven by the country's persistent reliance on cash transactions, strong government-led financial inclusion mandates, and expanding banking infrastructure across semi-urban and rural geographies. Technological advancements such as cash recycling machines, biometric-enabled ATMs, and unified payments interface (UPI)-integrated cardless withdrawal systems are reshaping service delivery and operational efficiency. The convergence of regulatory support, rising debit card penetration, and the growing demand for 24/7 banking services further contribute to the expansion of the India ATM market share.

Key Takeaways and Insights:

- By Solution: Deployment solutions dominate the market with a share of 54.3% in 2025, driven by expanding onsite ATM networks, the growing demand for offsite installations in underserved areas, and adoption of next-generation deployment models including mobile and work-site ATMs to serve diverse banking needs.

- By Screen Size: 15" and below represents the largest segment with a market share of 65.2% in 2025, reflecting the widespread preference for compact, cost-effective ATM terminals that offer reliable performance, ease of installation, and lower operational overhead, particularly across rural and semi-urban banking points.

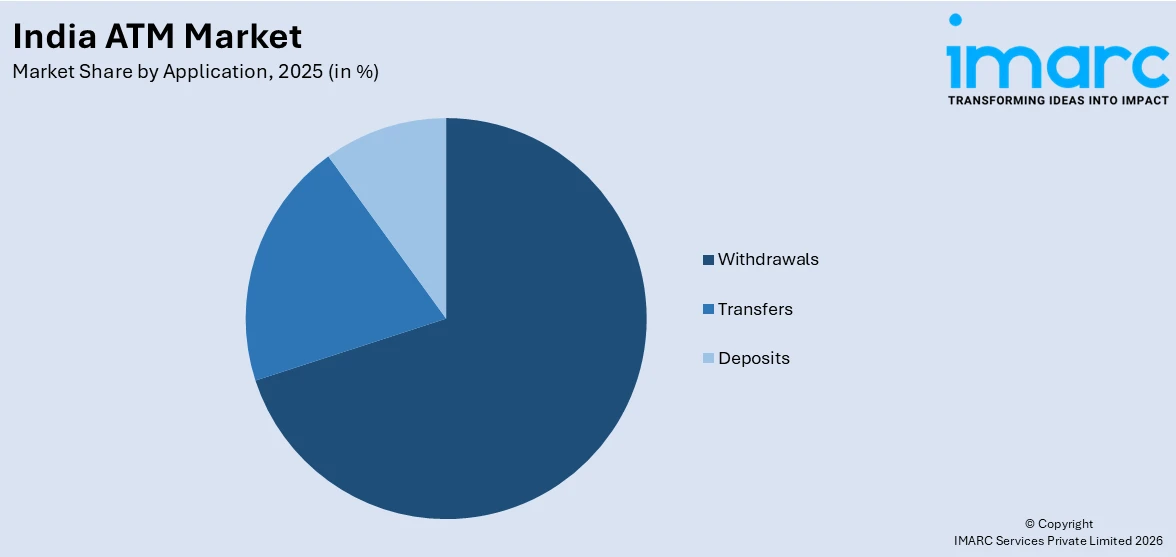

- By Application: Withdrawals lead the market with a share of 69.8% in 2025, underscoring the enduring dominance of cash transactions in India's economy, with ATMs serving as the primary touchpoint for cash access, especially in areas with limited digital payment infrastructure.

- By ATM Type: Conventional/bank ATMs dominate the market with a share of 34.7% in 2025, owing to the extensive networks maintained by public and private sector banks, trust among consumers, and their strategic placement across branches and high-footfall urban and peri-urban locations.

- By Region: North India represents the largest segment with a market share of 28.5% in 2025, benefiting from high population density, dense banking infrastructure, robust government benefit disbursement activity, and significant public sector bank presence across states such as Uttar Pradesh, Punjab, and Delhi NCR.

- Key Players: The India ATM market features a competitive landscape shaped by global technology providers, domestic ATM solution companies, and white-label ATM operators, all competing on the basis of deployment reach, managed service capabilities, hardware innovation, and strategic alignment with financial inclusion mandates. Some of the key players in the market include Euronet Worldwide, Inc., Hitachi Ltd., Diebold Nixdorf, Incorporated, NCR Atleos Corporation, AGS Transact Technologies Ltd., Vortex Engineering Private Limited, ETSOL WATER SOLUTIONS PVT. LTD., Tata Communications Payment Solutions Limited, Brinks India Private Limited, Hyosung India Private Limited, and FIS Solutions Software India Private Limited.

To get more information on this market Request Sample

The ATM market growth in India is driven by sustained demand for cash access alongside increasing technological upgrades that enhance ATM functionality. Cash continues to play an important role in daily transactions across retail markets, small businesses, and rural economies where digital payment adoption remains uneven. Financial institutions are therefore expanding and modernizing ATM infrastructure to maintain reliable cash availability while improving service convenience. At the same time, banks and payment networks are integrating digital technologies with ATM systems to support cardless transactions and improve interoperability with mobile banking platforms. These developments allow ATMs to remain relevant within a rapidly evolving payment ecosystem that combines both cash and digital services. Reflecting this trend, in 2024, the National Payments Corporation of India introduced a UPI-based interoperable cash deposit system that enables customers to deposit cash at ATMs using any UPI-enabled mobile application without requiring a physical debit card.

India ATM Market Trends:

Expansion of White-Label ATM Networks Improving Cash Access

The rise of white-label ATM networks is strengthening cash accessibility and supporting the growth of the India ATM market. White-label ATMs allow non-bank entities to deploy and operate ATM infrastructure that can be used by individuals of any bank, increasing ATM availability without requiring banks to invest directly in new machines. This model helps expand ATM coverage in underserved rural and semi-urban regions where traditional bank branches are limited. Wider deployment of these ATMs improves financial inclusion and ensures continued access to cash despite the rise of digital payments. This trend is evident in 2024, when the Reserve Bank of India granted a white-label ATM license to Electronic Payment and Services, enabling the company to set up and operate ATMs accessible to customers of multiple banks.

Strategic Acquisitions Strengthening ATM Infrastructure Expansion

Strategic acquisitions within the ATM services sector are helping financial service providers expand ATM infrastructure and strengthen operational capabilities. Companies are acquiring existing ATM networks and payment platforms to increase geographic reach, integrate ATM services with digital payment ecosystems, and improve efficiency in managing large ATM networks. These acquisitions enable operators to scale services rapidly while leveraging existing merchant and banking partnerships. Consolidation within the ATM services industry also helps companies optimize network performance and expand service coverage. This trend is evident in 2025, when Tata Communications completed the divestment of Tata Communications Payment Solutions Ltd to Transaction Solutions International, providing the acquiring company access to a white-label ATM platform, payment switch infrastructure, and a network of over 4,600 ATMs.

Integration of Digital Payment Technologies with ATM Infrastructure

The integration of digital payment technologies with ATM infrastructure is enhancing the convenience and accessibility of banking services. ATM systems are incorporating mobile-based authentication and digital payment platforms to enable cardless transactions. These innovations allow users to withdraw or deposit cash without relying on physical debit cards, supporting the growing use of mobile banking applications. Such technological integration improves transaction security and aligns ATM services with evolving digital banking trends. This development is evident in 2024, when Axis Bank introduced a UPI-enabled ATM cash recycler that allowed customers to withdraw and deposit cash using UPI-enabled mobile applications without the need for debit cards.

Market Outlook 2026-2034:

The India ATM market is poised for consistent revenue growth throughout forecast period, underpinned by sustained cash demand, regulatory-driven infrastructure modernization, and ongoing financial inclusion initiatives. The market generated a revenue of USD 1.94 Billion in 2025 and is projected to reach a revenue of USD 3.68 Billion by 2034, growing at a compound annual growth rate of 6.53% from 2026-2034. The shift toward smart ATMs, cash recyclers, and UPI-integrated machines will create compelling upgrade cycles, while white-label operator expansion into Tier III-VI geographies will open new deployment corridors. Managed services adoption will deepen as banks prioritize operational cost efficiency, reinforcing long-term market momentum.

India ATM Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Solution |

Deployment Solutions |

54.3% |

|

Screen Size |

15" and Below |

65.2% |

|

Application |

Withdrawals |

69.8% |

|

ATM Type |

Conventional/Bank ATMs |

34.7% |

|

Region |

North India |

28.5% |

Solution Insights:

- Deployment Solutions

- Onsite ATMs

- Offsite ATMs

- Work Site ATMs

- Mobile ATMs

- Managed Services

Deployment solutions dominate with a market share of 54.3% of the total India ATM market in 2025.

Deployment solutions are emerging as the leading segment driven by the growing preference of banks for outsourced installation, integration and rollout support when expanding ATM networks across urban and semi-urban regions. Financial institutions increasingly rely on specialized vendors to handle site preparation, hardware installation, network configuration and system testing, which reduces operational burden and accelerates deployment timelines. The shift toward white-label ATMs, managed service models and large-scale network expansion programs further strengthens the demand for deployment services. Vendors offering end-to-end rollout capabilities help banks quickly activate new machines while ensuring compliance with regulatory and security standards required for cash dispensing infrastructure across diverse banking environments nationwide today steadily.

Rising ATM penetration targets set by public and private sector banks also support the strong position of deployment solutions within the market. Financial institutions are extending ATM networks in urban and emerging cities to improve cash accessibility and support financial inclusion objectives. Each new installation requires site preparation, system integration, connectivity setup, and ongoing maintenance, encouraging banks to collaborate with specialized service providers. Reflecting this trend, in 2025, fintech company Slice launched India’s first UPI-powered bank branch and ATM in Bengaluru, enabling users to withdraw and deposit cash, open accounts, and access banking services directly through UPI without traditional debit cards. Such innovations demonstrate how ATM expansion and technology integration continue to strengthen self-service banking infrastructure across the country.

Screen Size Insights:

- 15" and Below

- Above 15"

The 15" and below leads with a market share of 65.2% of the total India ATM market in 2025.

15" and below holds the biggest market share attributed to the widespread use of compact ATM models across bank branches, retail locations, and high-traffic public areas. Banks prefer smaller display sizes as they support cost-efficient machine designs while meeting the functional requirements of standard cash withdrawal and balance inquiry transactions. Compact screens also allow ATM manufacturers to produce space-efficient kiosks that can be installed in smaller indoor locations, such as convenience stores, bank lobbies, and transportation hubs. Financial institutions prioritize reliability and lower maintenance costs, and machines with smaller screens generally require less power and simpler hardware configurations, making them suitable for large scale ATM deployment across diverse banking environments in India.

The growing deployment of ATMs in semi urban and rural regions also supports the dominance of 15" and below screen sizes in the market. Banks often install basic cash dispensing machines in these areas where transaction requirements remain straightforward and advanced user interfaces are less necessary. Smaller screens provide clear visibility for essential transaction prompts while keeping machine costs manageable for large network expansion programs. Many public sector banks and white label ATM operators continue to focus on cost-efficient ATM rollout strategies to increase financial inclusion and improve access to banking services. As a result, ATM manufacturers widely supply compact display models that align with banks’ operational priorities and infrastructure conditions across multiple regions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Withdrawals

- Transfers

- Deposits

Withdrawals exhibit a clear dominance with a 69.8% share of the total India ATM market in 2025.

Withdrawals lead the market because of the continued reliance on cash for everyday transactions across many parts of the country. People frequently use ATMs primarily to access cash for retail purchases, transportation payments, small business transactions, and household expenses. Cash remains widely accepted in local markets and informal sectors, sustaining strong demand for withdrawal services. Banks design ATM networks largely around facilitating quick and secure cash dispensing, which remains the most common transaction performed by users. High transaction volumes associated with withdrawals encourage banks to maintain extensive ATM networks to ensure convenient cash availability for customers nationwide.

Continued reliance on cash transactions in semi-urban and rural regions supports the importance of ATM withdrawals in India’s banking ecosystem. Many individuals use ATMs to access salary deposits, remittance transfers, and government benefit payments credited to their bank accounts. This allows account holders to convert digital balances into physical cash conveniently without visiting bank branches. Reflecting this growing role of ATMs in accessing institutional funds, in 2025, the Employees’ Provident Fund Organisation introduced EPFO 3.0 with ATM-based withdrawal facilities for provident fund members. The system enabled users to withdraw funds instantly or transfer money to bank accounts through simplified processes, strengthening the role of ATMs in financial access.

ATM Type Insights:

- Conventional/Bank ATMs

- Brown Label ATMs

- White Label ATMs

- Smart ATMs

- Cash Dispensers

Conventional/bank ATMs dominate with a market share of 34.7% of the total India ATM market in 2025.

Conventional/bank ATMs represent the largest segment owing to the extensive ATM networks operated directly by public and private sector banks across the country. Banks continue to deploy and manage their own machines to provide reliable cash access, account services, and customer support through familiar banking infrastructure. People generally prefer bank-owned ATMs because they are directly linked with their financial institutions and often provide lower or no transaction charges for account holders. These machines are commonly installed at bank branches, commercial areas, and high footfall locations, ensuring strong visibility and accessibility. As a result, conventional bank-operated ATMs continue to account for a significant share of ATM installations nationwide.

Strong trust in bank-operated infrastructure further supports the dominance of conventional ATMs in the market. People often perceive bank ATMs as more secure and dependable for cash withdrawals, balance inquiries, and other basic banking services. Banks also prioritize maintaining their ATM presence to strengthen customer relationships and ensure convenient access to financial services beyond branch operating hours. Continuous investments in machine upgrades, cash management systems, and security features help banks maintain operational efficiency within their ATM networks. While alternative models such as white label and brown label ATMs continue to expand, conventional bank-operated machines remain the primary channel for delivering ATM-based banking services across India.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India leads with a market share of 28.5% of the total India ATM market in 2025.

North India dominates the market due to its large population base, dense urban centers, and strong banking infrastructure across major states. Cities, such as Delhi, Chandigarh, Lucknow, and Jaipur, host extensive ATM networks supported by both public and private sector banks. High population density and active commercial activity generate consistent demand for convenient cash access points. Banks prioritize ATM deployment in these areas to serve a large number of account holders and business establishments that rely on regular cash transactions. The presence of major financial institutions and strong retail networks also contributes to the higher concentration of ATMs across several northern states.

Expanding financial inclusion initiatives and the increasing use of direct benefit transfer programs are strengthening demand for ATMs across several regions in India. As more individuals open bank accounts and receive subsidies, wages, and welfare payments directly through banking channels, accessible cash withdrawal points become essential. ATM networks help convert these digital balances into physical currency, particularly in areas where branch access remains limited. Reflecting this shift toward technology-enabled access to banking services, in 2025, Slice launched a UPI-powered bank branch and ATM in Gurugram that allows customers to deposit or withdraw cash by scanning a QR code through UPI without requiring debit cards. Such innovations improve convenience while supporting the expansion of ATM-based financial access across growing banking populations.

Market Dynamics:

Growth Drivers:

Why is the India ATM Market Growing?

Deployment of Flexible and Upgradeable ATM Systems

The development of flexible ATM infrastructure is enabling banks to modernize their networks while managing operational costs. New ATM models are being designed with upgradeable capabilities, allowing financial institutions to convert existing machines into more advanced systems as customer needs evolve. These systems can be upgraded to support additional services, such as cash recycling, deposits, and digital transaction features, without replacing the entire machine. Such flexibility helps banks improve service offerings while extending the lifespan of ATM hardware. This trend is evident in 2024, when Hitachi Payment Services launched India’s first upgradable ATM that can later be converted into a Cash Recycling Machine, enabling banks to upgrade ATM functionality without replacing existing equipment.

Expansion of ATM Services into New Public Access Locations

The deployment of ATMs in non-traditional public locations is expanding banking accessibility and supporting the continued relevance of ATM networks. Financial institutions and service providers are exploring new environments, such as transportation systems and high-traffic public areas, to provide convenient access to cash. Installing ATMs in these locations helps meet user demand for banking services during travel or daily commuting. This trend is evident in 2025, when Central Railway conducted a trial run of India’s first train with an ATM installed inside the Panchavati Express operating between Nashik and Mumbai. The ATM allowed passengers to withdraw cash while the train is in motion, improving access to banking services during travel.

Mobile and Renewable Energy-Based ATM Solutions

Innovative ATM deployment models are improving banking access in remote and infrastructure-constrained regions. Mobile ATM units and renewable energy-powered systems are being introduced to overcome challenges related to electricity shortages and limited banking infrastructure in rural areas. These solutions allow banks to extend financial services to remote communities without relying on permanent facilities. Mobile and solar-powered ATMs support financial inclusion by enabling basic banking transactions in areas where traditional ATM installation may be difficult. This trend is evident in 2026, when Tripura Gramin Bank launched India’s first solar-powered ATM van, enabling residents in remote regions to perform transactions, such as cash withdrawals and deposits while operating entirely on solar energy.

Market Restraints:

What Challenges the India ATM Market is Facing?

High Operational and Maintenance Costs

Operating an ATM network requires significant recurring expenditure across multiple operational areas. Banks incur costs related to cash replenishment logistics, security staffing, electricity usage, communication networks, regulatory upgrades, and long-term hardware maintenance contracts. Offsite ATMs add further expenses through rental commitments and enhanced security arrangements, leading financial institutions to reassess deployment strategies and gradually reduce locations that deliver limited transaction volumes.

Rising Digital Payment Adoption Reducing Transaction Frequency

Rapid expansion of digital payment systems has steadily reduced the frequency of ATM usage, particularly in urban regions where digital payment infrastructure and consumer familiarity are widespread. As people increasingly rely on mobile payment applications for everyday transactions, the need for physical cash withdrawals declines. Lower transaction volumes weaken the revenue potential of ATMs, prompting financial institutions to slow network expansion and reassess underperforming machines.

Regulatory Complexity and Security Compliance Burdens

The ATM industry in India operates under a strict regulatory framework that requires ongoing compliance with evolving security and operational standards. Banks and service providers must regularly upgrade hardware, strengthen cybersecurity protections, and maintain compatibility with multiple payment networks and authentication protocols. These requirements increase operational complexity and raise long-term technology spending, placing greater pressure on institutions managing large ATM networks.

Competitive Landscape:

The India ATM market exhibits a moderately concentrated competitive structure shaped by the presence of global technology companies, domestic ATM manufacturers, managed service providers, and specialized white-label ATM operators. Global firms supply core hardware, software platforms, and integrated banking technologies, while domestic players focus on manufacturing, deployment, maintenance, and operational support services across the country. White-label ATM operators play an important role in expanding access to banking services in semi-urban and rural locations where banks may not deploy their own machines. Competition in the market revolves around service reliability, network uptime, cost efficiency, technological upgrades, and the ability to manage large ATM networks. Partnerships with banks, payment networks, and financial institutions remain central to sustaining operational scale and long-term service contracts.

Some of the key players in the market include:

- Euronet Worldwide, Inc.

- Hitachi Ltd.

- Diebold Nixdorf, Incorporated

- NCR Atleos Corporation

- AGS Transact Technologies Ltd.

- Vortex Engineering Private Limited

- ETSOL WATER SOLUTIONS PVT. LTD.

- Tata Communications Payment Solutions Limited

- Brinks India Private Limited

- Hyosung India Private Limited

- FIS Solutions Software India Private Limited

Recent Developments:

- March 2025: Findi Ltd raised A$45 million (about ₹243 crore) to expand its fintech operations in India through its subsidiary Transaction Solutions International (India). The funding planned to support technology upgrades, ATM deployment, and expansion of merchant payment solutions across key markets.

- January 2025: Australia-based FINDI acquired fintech firm BANKIT for about A$30 million (around ₹162 crore) through its Indian subsidiary. The deal strengthens FINDI’s merchant network and supports expansion of financial services in rural and semi-urban India. It will also enable wider deployment of ATMs and payment services through BANKIT’s network of over 1.29 lakh outlets across the country.

India ATM Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Covered |

|

| Screen Sizes Covered | 15" and Below, Above 15" |

| Applications Covered | Withdrawals, Transfers, Deposits |

| ATM Types Covered | Conventional/Bank ATMs, Brown Label ATMs, White Label ATMs, Smart ATMs, Cash Dispensers |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Euronet Worldwide, Inc., Hitachi Ltd., Diebold Nixdorf, Incorporated, NCR Atleos Corporation, AGS Transact Technologies Ltd., Vortex Engineering Private Limited, ETSOL WATER SOLUTIONS PVT. LTD., Tata Communications Payment Solutions Limited, Brinks India Private Limited, Hyosung India Private Limited, FIS Solutions Software India Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India ATM Market Report

The India ATM market size was valued at USD 1.94 Billion in 2025.

The India ATM market is expected to grow at a compound annual growth rate of 6.53% during 2026-2034 to reach USD 3.68 Billion by 2034.

Deployment solutions hold the largest revenue share of 54.3% in 2025, driven by expanding onsite ATM networks, the growing offsite and mobile ATM deployments, and increased adoption of cash recycling machines by banks across urban and semi-urban India.

Key factors driving the India ATM market include the integration of digital payment technologies with ATM infrastructure to enable cardless transactions and improve user convenience. UPI-based authentication allows customers to withdraw or deposit cash through mobile apps. In 2024, Axis Bank introduced a UPI-enabled ATM cash recycler supporting such transactions.

Major challenges include high operational and maintenance costs for off-site ATMs, declining per-ATM transaction volumes in urban areas due to rising digital payment adoption, and increasing regulatory compliance burdens related to security hardware upgrades and interoperability mandates from the Reserve Bank of India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)