India Automobile Market Size, Share, Trends and Forecast by Fuel Type, Vehicle Type, Channel, and Region, 2026-2034

India Automobile Market Size, Share, Trends & Forecast (2026-2034)

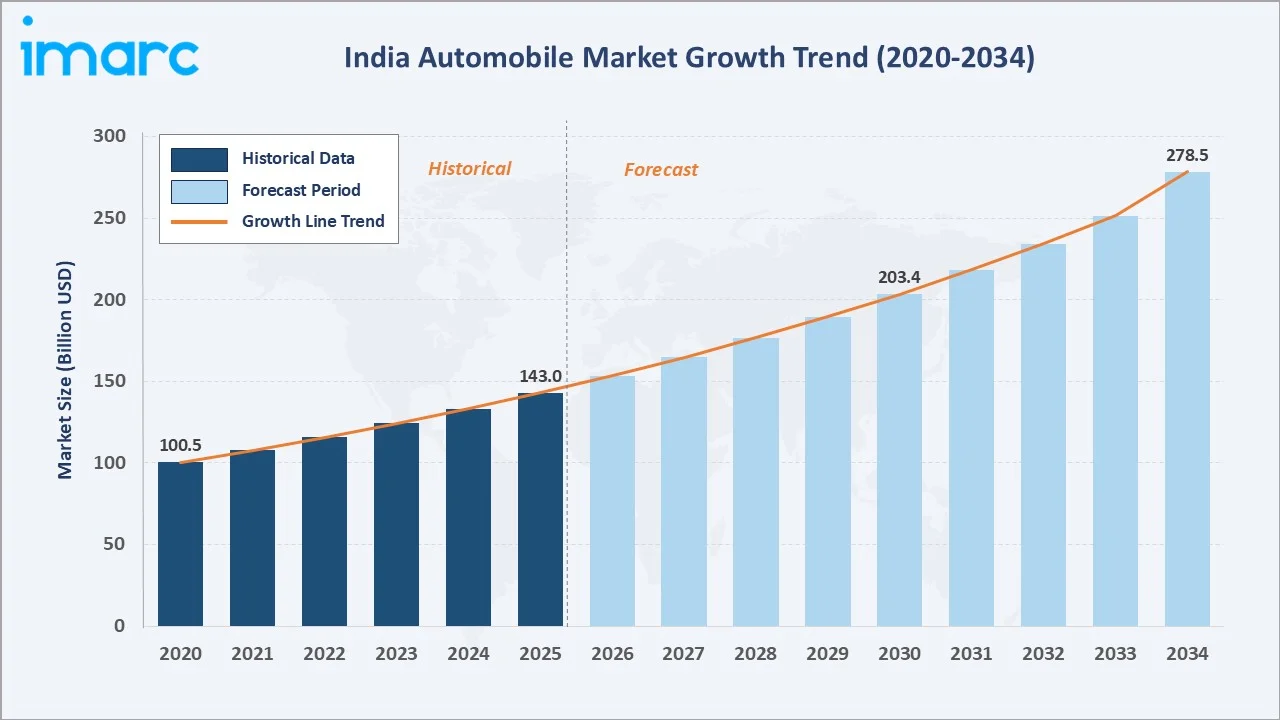

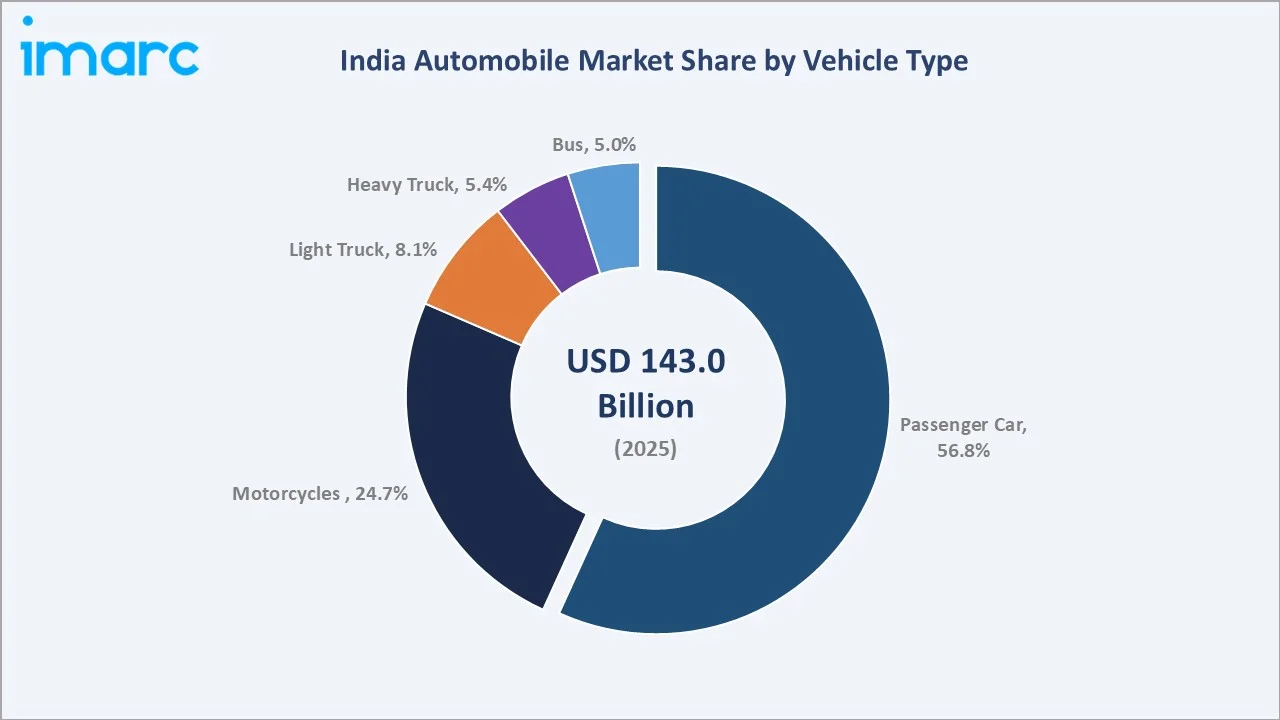

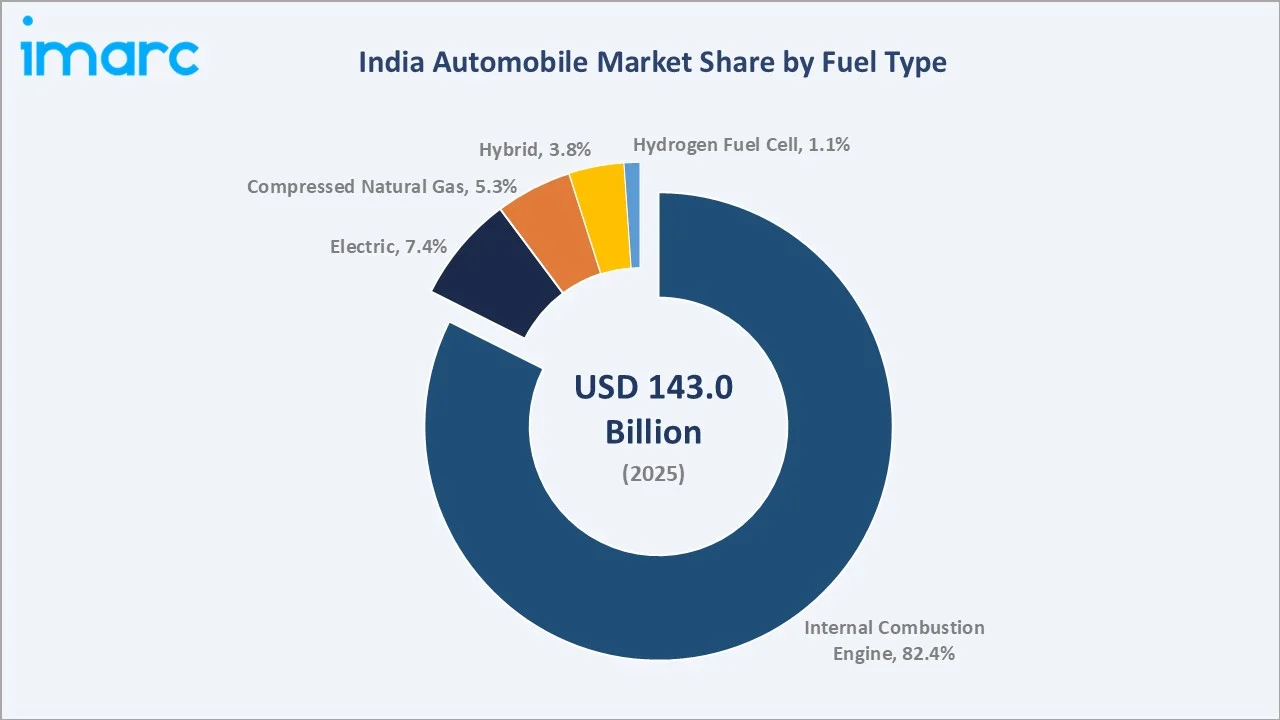

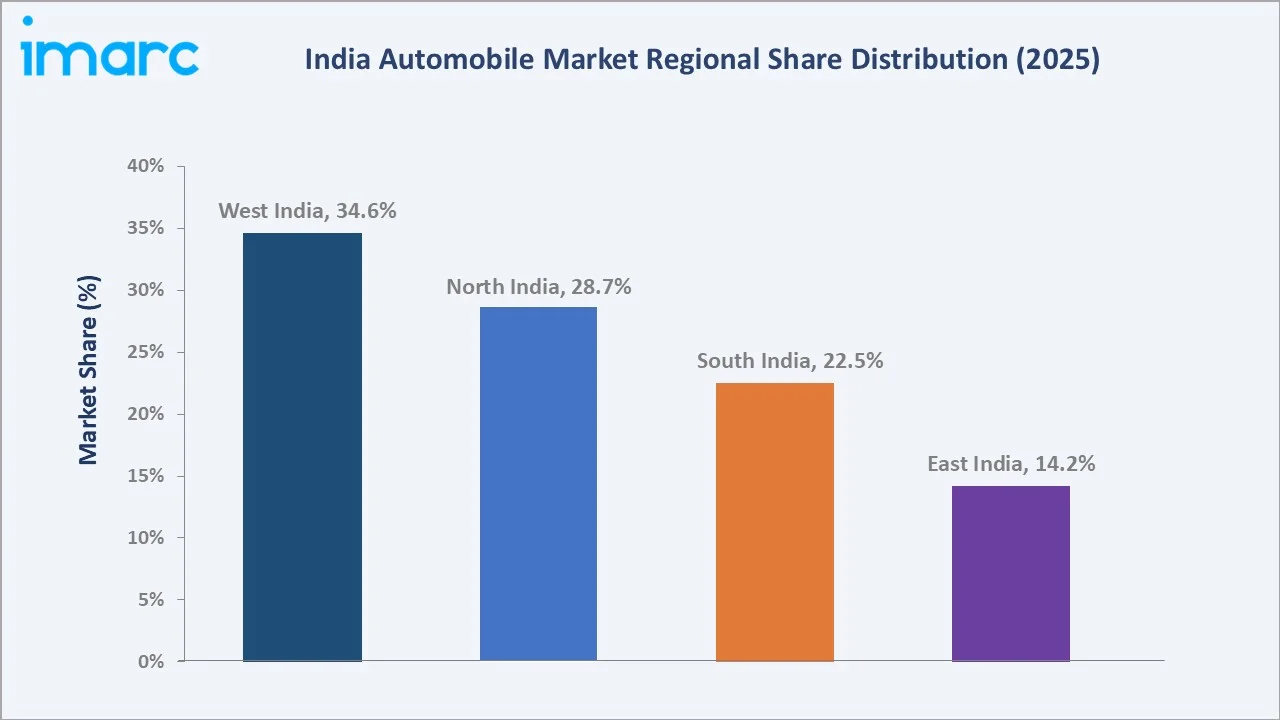

The India automobile market reached USD 143.0 Billion in 2025 and is projected to reach USD 278.5 Billion by 2034, growing at a CAGR of 7.31% during 2026-2034. The market is driven by rising disposable incomes, rapid urbanization, and increasing demand for personal mobility across urban and semi-urban areas. Government initiatives supporting vehicle manufacturing, infrastructure development, and electric vehicle adoption further contribute to market growth. The PLI scheme for automobiles and auto components was allocated Rs. 2,818.9 crore, equivalent to about USD 325.6 million, in FY26. Passenger car leads vehicle type at 56.8%. Internal combustion engine leads fuel type at 82.4%. West India leads regionally at 34.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 143.0 Billion |

|

Forecast Market Size (2034) |

USD 278.5 Billion |

|

CAGR (2026-2034) |

7.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Vehicle Type |

Passenger Car (56.8%, 2025) |

|

Dominant Fuel Type |

Internal Combustion Engine (82.4%, 2025) |

|

Leading Region |

West India (34.6%, 2025) |

The India automobile market is showing strong expansion, rising from USD 100.5 billion in 2020 to USD 143.0 billion in 2025. It is projected to reach USD 203.4 billion by 2030 and further grow to USD 278.5 billion by 2034. Growth is supported by rising disposable incomes, urbanization, improved road infrastructure, and increasing demand for personal mobility. Government support for domestic manufacturing and electric vehicle adoption is also strengthening the long-term market outlook.

To get more information on this market, Request Sample

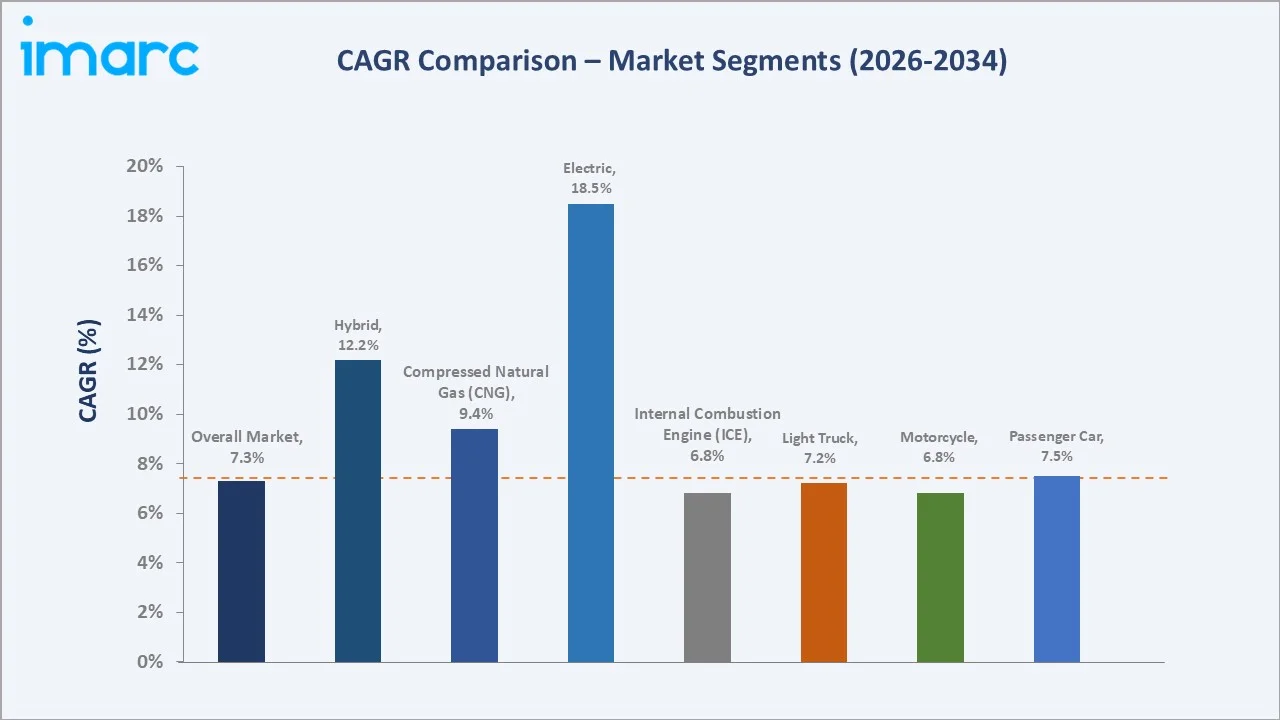

Electric vehicles grow fastest at ~18.5% CAGR through government initiatives. Hybrid grows at ~12.2% CAGR. CNG grows at ~9.4% CAGR through Delhi-Mumbai CNG bus and auto fleet expansion.

Executive Summary

The India automobile market is growing steadily, supported by rising disposable incomes, urbanization, and increasing demand for personal mobility. Market value expanded from USD 100.5 billion in 2020 to USD 143.0 billion in 2025 and is projected to reach USD 278.5 billion by 2034. Government initiatives such as the PLI scheme are strengthening domestic manufacturing and auto component production. EV adoption, infrastructure expansion, and technology localization are further reshaping the industry. Strong demand across passenger vehicles, two-wheelers, commercial vehicles, and electric mobility segments supports a positive long-term outlook. Passenger cars at 56.8% leads the market. Internal combustion engine at 82.4% leads through mass-market affordability. West India leads regionally at 34.6%.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Passenger Car - 56.8% share (2025) |

|

Dominant Fuel Type |

Internal Combustion Engine - 82.4% market share (2025) |

|

Leading Region |

West India - 34.6% share (2025) |

|

Market Opportunity |

EV two-wheeler mass market; premium SUV segment; CNG alternative fuel fleet; connected and ADAS-equipped vehicles; rural market penetration; India EV export hub through PLI scheme |

Key Analytical Observations Supporting the Above Data:

- Passenger Car at 56.8%: The passenger cars dominate due to rising demand for personal mobility, urban commuting, and family transportation. Growing disposable incomes, financing availability, and new model launches further support higher passenger car sales.

- Internal Combustion Engine at 82.4%: The internal combustion engine dominates due to its established fuel infrastructure, wide model availability, and lower upfront cost compared to electric vehicles. Strong demand in passenger cars, two-wheelers, and commercial vehicles continues to support ICE vehicle sales.

- West India at 34.6%: The West India region dominates due to its strong automotive manufacturing base, supplier ecosystem, and major industrial hubs in Maharashtra and Gujarat. Higher urbanization, strong consumer demand, port connectivity, and investment in EV and auto component production further support regional leadership.

India Automobile Market Overview

The India automobile market is one of the largest automobile markets globally, supported by its vast population, expanding middle class, and growing urbanization. The country is a major producer and consumer of passenger vehicles, two-wheelers, and commercial vehicles, with a well-established manufacturing ecosystem. Strong government support through initiatives such as Make in India and the PLI scheme continues to attract domestic and foreign investments. Rising vehicle ownership, infrastructure development, and increasing adoption of advanced and electric vehicles are further strengthening India's position in the global automotive industry. Macroeconomic factors include rising GDP growth, increasing disposable incomes, and rapid urbanization, which support higher vehicle ownership.

Market Dynamics

To evaluate market opportunities, Request Sample

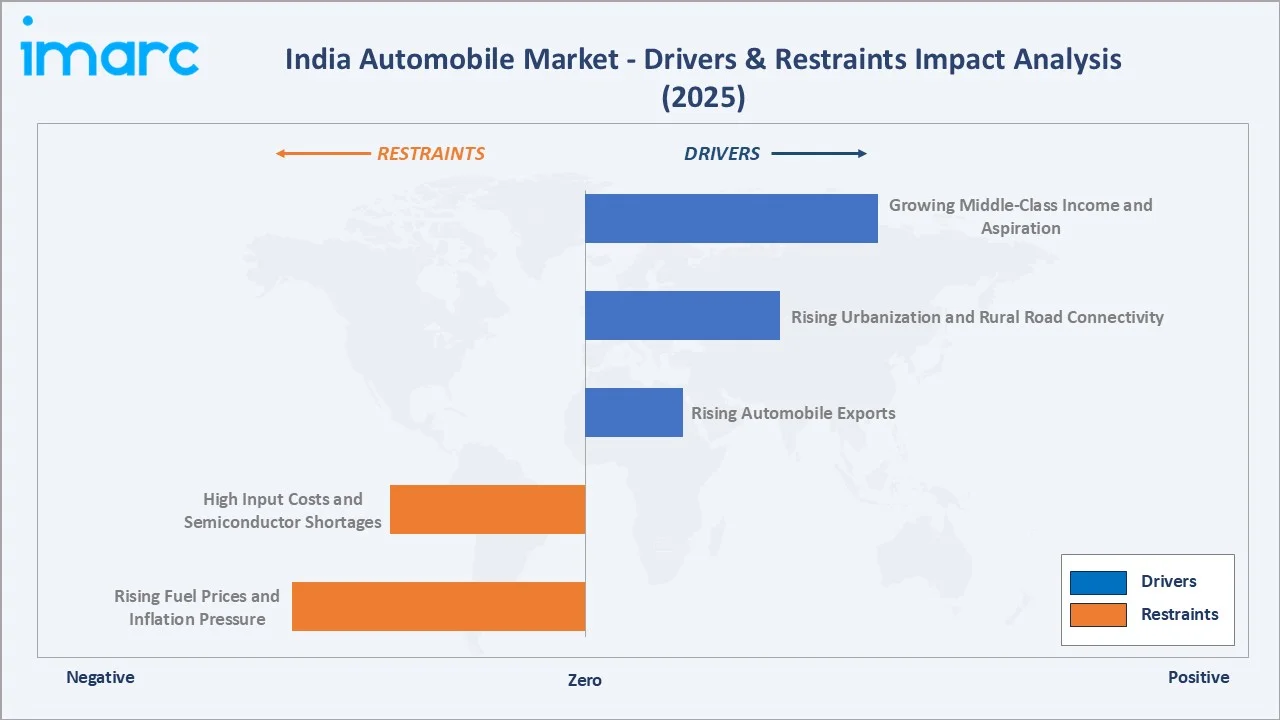

Market Drivers

- Growing Middle-Class Income and Aspiration: In FY26, households with annual income above ₹8 lakh represented 34.38% of total Indian households. This share is expected to increase to 42.74% by FY31, indicating that nearly four in ten households may earn over ₹8 lakh annually within the next five years. This growing middle-class income and aspiration are major drivers, as rising household earnings are improving affordability and enabling consumers to upgrade from two-wheelers to passenger cars. Increasing aspirations for comfort, convenience, safety, and social status are encouraging purchases of premium and feature-rich vehicles. Easy access to vehicle financing and a wider range of models across price segments further support demand. As urbanization and lifestyle changes continue, automobile ownership is increasingly viewed as both a necessity and a symbol of upward mobility.

- Rising Urbanization and Rural Road Connectivity: Rising urbanization and rural road connectivity are expanding access to transportation across both metropolitan and underserved regions. Rapid urban growth is increasing demand for personal vehicles for daily commuting, while improved rural roads under government infrastructure programs are making vehicle ownership more practical in smaller towns and villages. Better connectivity enhances mobility, supports economic activity, and increases demand for passenger and commercial vehicles. As a result, automakers are witnessing stronger sales penetration beyond major urban centers.

- Rising Automobile Exports: India’s automobile exports increased by 19% in FY25, surpassing 5.3 million units, supported by strong overseas demand for passenger vehicles, two-wheelers, and commercial vehicles. Rising automobile exports are strengthening production volumes, improving manufacturing efficiency, and attracting investments from global automakers. India has emerged as a key export hub for small cars, two-wheelers, and auto components due to its cost-competitive manufacturing base and skilled workforce. Growing exports enable manufacturers to achieve economies of scale, increase capacity utilization, and expand supplier networks.

Market Restraints

- High Input Costs and Semiconductor Shortages: High input costs and semiconductor shortages are increasing production costs for automakers and component suppliers. Rising prices of steel, aluminum, rubber, plastics, batteries, and electronic components can reduce margins or push vehicle prices higher. Semiconductor shortages also disrupt production schedules, especially for feature-rich vehicles, EVs, and connected models. These challenges can delay deliveries, reduce affordability, and weaken consumer demand in price-sensitive segments.

- Rising Fuel Prices and Inflation Pressure: Rising fuel prices and inflation pressure are increasing the overall cost of vehicle ownership and reducing consumer purchasing power. Higher fuel expenses make buyers more cautious about purchasing new vehicles, particularly in price-sensitive segments. Inflation also raises the cost of raw materials, manufacturing, logistics, and financing, leading to higher vehicle prices. These factors can delay purchase decisions and moderate demand growth across passenger and commercial vehicle categories.

Market Opportunities

- Electric Vehicle Adoption: India registered 56.75 lakh electric vehicles by February 2025. This rising electric vehicle adoption is a major opportunity as government incentives, fuel-cost savings, and stricter emission norms are accelerating demand for EVs. Rising investments in battery manufacturing, charging infrastructure, and localized EV components are strengthening the ecosystem. Automakers can capture growth through electric two-wheelers, passenger EVs, commercial EVs, and fleet electrification. This shift also opens opportunities in software, connected mobility, battery recycling, and charging services.

- Premium and Luxury Vehicle Segment Growth: Premium and luxury vehicle segment growth is an opportunity as rising incomes and aspirational lifestyles are increasing demand for feature-rich, high-end vehicles. Consumers are upgrading toward SUVs, luxury sedans, connected cars, and advanced safety-equipped models. This creates higher-margin opportunities for automakers, dealers, and component suppliers. Expansion of financing options and luxury brand networks in Tier-1 and Tier-2 cities further supports premium vehicle adoption.

Market Challenges

- Charging Infrastructure Gaps for Electric Vehicles: Charging infrastructure gaps for electric vehicles may slow the EV adoption, especially in smaller cities, on highways, and in rural areas. Limited public charging availability creates range anxiety and reduces buyer confidence. Uneven charger distribution, long charging times, and grid-capacity constraints also affect fleet and commercial EV deployment. These gaps can delay the transition from ICE vehicles to EVs despite policy support and rising consumer interest.

- Supply Chain Disruptions and Raw Material Price Volatility: Supply chain disruptions and raw material price volatility are increasing uncertainty in production planning and vehicle pricing. Fluctuations in steel, aluminum, rubber, lithium, nickel, and semiconductor costs can raise manufacturing expenses and compress margins. Delays in imported components or logistics bottlenecks may disrupt assembly schedules and extend vehicle delivery timelines. These risks make localization, supplier diversification, and inventory planning critical for automakers and component manufacturers.

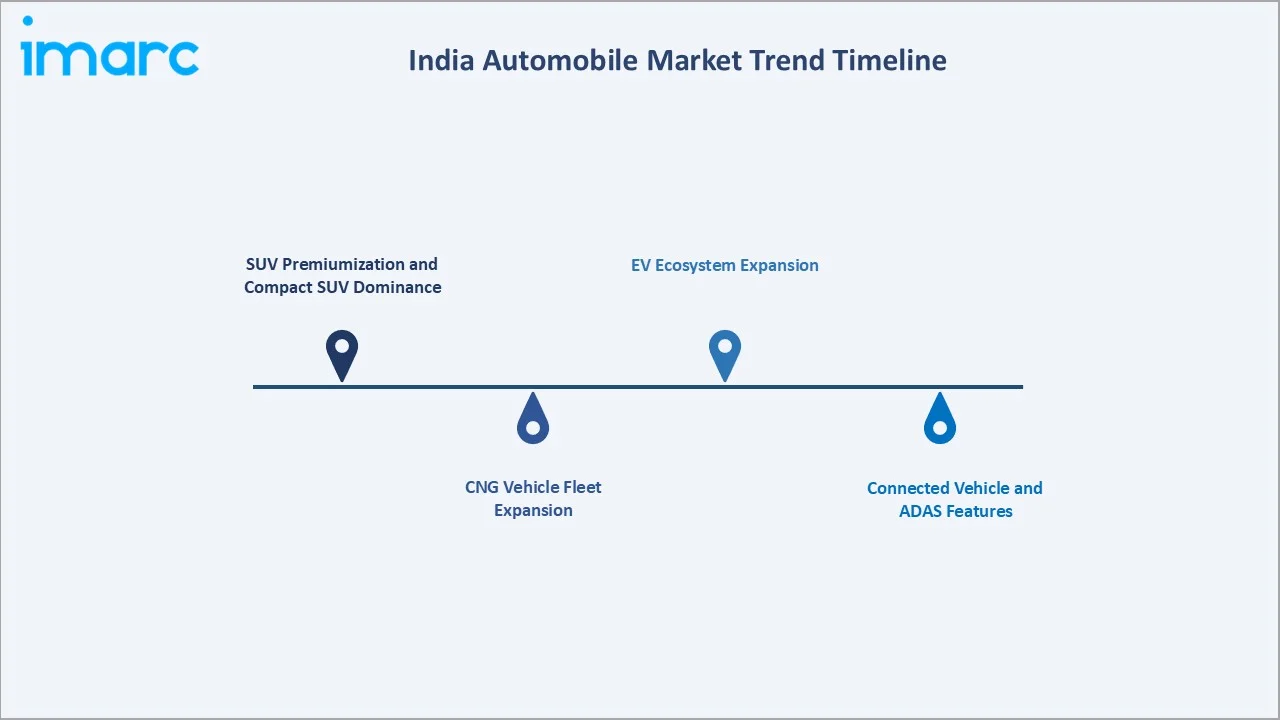

Emerging Market Trends

1. SUV Premiumization and Compact SUV Dominance

SUV premiumization and compact SUV dominance are emerging as consumers increasingly prefer vehicles with higher ground clearance, bold styling, advanced features, and better road presence. Compact SUVs are gaining strong traction because they offer SUV-like appeal at relatively accessible price points. Automakers are responding with feature-rich models, connected technologies, sunroofs, ADAS, and multiple powertrain options. This trend is shifting demand away from traditional hatchbacks and sedans while creating higher-value opportunities for OEMs.

2. EV Ecosystem Expansion

EV ecosystem expansion is emerging as growth is shifting beyond vehicle sales to charging networks, battery manufacturing, software, financing, and after-sales services. India aims for electric vehicles to account for 30% of total vehicle sales by 2030. EV sales in the country increased sharply from 50,000 units in 2016 to 2.08 million units in 2024. Government incentives and OEM investments are accelerating EV model launches across two-wheelers, passenger cars, buses, and commercial fleets. Expansion of public and private charging infrastructure is reducing range anxiety and improving consumer confidence. This trend is creating new opportunities for automakers, battery suppliers, charging operators, and mobility service providers.

3. CNG Vehicle Fleet Expansion

CNG vehicle fleet expansion is emerging due to lower running costs and relatively cleaner emissions compared to conventional petrol and diesel vehicles. The rapid expansion of CNG refueling infrastructure and supportive government policies are encouraging adoption across passenger cars, taxis, and commercial fleets. Automakers are increasing the availability of factory-fitted CNG models to meet growing demand. This trend is particularly strong among cost-conscious consumers and fleet operators seeking fuel-efficient mobility solutions.

4. Connected Vehicle and ADAS Features

Connected vehicle and ADAS features are emerging as consumers increasingly demand safer, smarter, and more technology-enabled vehicles. OEMs are integrating features such as telematics, infotainment connectivity, lane assistance, adaptive cruise control, parking assist, and collision warnings. Rising premiumization, growth in SUVs, and demand for convenience are accelerating adoption beyond luxury models into mid-segment vehicles. This trend is creating opportunities for automakers, sensor suppliers, software developers, and connected mobility platforms.

Industry Value Chain Analysis

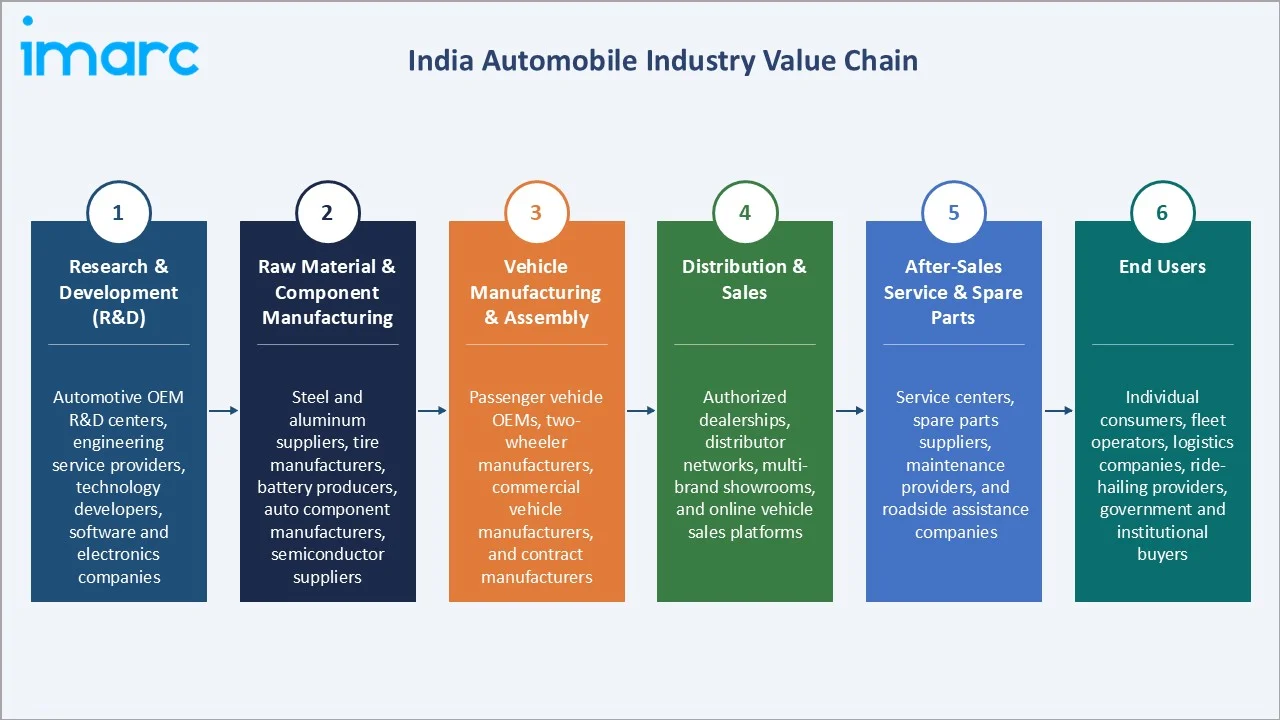

India automobile value chain integrates research & development (R&D), raw material & component manufacturing, vehicle manufacturing & assembly, distribution & sales, after-sales service & spare parts, and end users.

|

Stage |

Key Participants |

|

Research & Development (R&D) |

Automotive OEM R&D centers, engineering service providers, technology developers, software and electronics companies |

|

Raw Material & Component Manufacturing |

Steel and aluminum suppliers, tire manufacturers, battery producers, auto component manufacturers, semiconductor suppliers |

|

Vehicle Manufacturing & Assembly |

Passenger vehicle OEMs, two-wheeler manufacturers, commercial vehicle manufacturers, and contract manufacturers |

|

Distribution & Sales |

Authorized dealerships, distributor networks, multi-brand showrooms, and online vehicle sales platforms |

|

After-Sales Service & Spare Parts |

Service centers, spare parts suppliers, maintenance providers, and roadside assistance companies |

|

End Users |

Individual consumers, fleet operators, logistics companies, ride-hailing providers, government and institutional buyers |

The vehicle manufacturing and assembly stage is the most value-added segment in the India automobile value chain. This stage combines engineering, technology integration, powertrain development, electronics, safety systems, and branding to convert components into finished vehicles, generating the highest share of value creation and profitability.

Technology Landscape in the India Automobile Industry

Autonomous and Assisted Driving Technologies

Autonomous and assisted driving technologies are enhancing vehicle safety, driver convenience, and overall driving efficiency. Automakers are increasingly integrating features such as adaptive cruise control, lane departure warning, automatic emergency braking, blind-spot detection, and parking assistance into new models. Growing consumer awareness of vehicle safety, along with evolving regulatory standards, is accelerating the adoption of ADAS technologies. These advancements are laying the foundation for higher levels of vehicle automation and smarter mobility solutions in the future.

Hydrogen Fuel Cell and Green Mobility Technologies

Automakers and energy companies are investing in hydrogen fuel cell vehicles, green hydrogen production, and supporting infrastructure for commercial transport applications. India is advancing cleaner transportation through five pilot projects launched under the National Green Hydrogen Mission. These projects will introduce 37 hydrogen-powered buses and trucks across key routes, including 15 fuel-cell vehicles and 22 hydrogen internal combustion engine vehicles. These technologies offer the potential for zero tailpipe emissions, fast refueling, and extended driving ranges compared to conventional battery-electric vehicles. Growing policy support, pilot projects, and investments in clean energy are accelerating research and development in hydrogen-based mobility solutions.

Advanced Safety and Crash-Avoidance Technologies

Advanced safety and crash-avoidance technologies are improving vehicle safety and reducing accident risks. Automakers are increasingly integrating features such as automatic emergency braking, electronic stability control, blind-spot monitoring, collision warnings, and lane-keeping assistance across vehicle segments. Rising consumer awareness, stricter safety regulations, and higher Global NCAP safety expectations are accelerating adoption. These technologies are driving innovation in sensors, cameras, radar systems, and vehicle intelligence, making safety a key differentiator in the market.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fuel Type |

Internal Combustion Engine |

82.4% |

2025 |

|

Vehicle Type |

Passenger Car |

56.8% |

2025 |

|

Channel |

Dealerships |

48.5% |

2025 |

|

Region |

West India |

34.6% |

2025 |

By Vehicle Type

Passenger car leads at 56.8% (2025), due to rising demand for personal mobility, urban commuting, and family transportation. Growing incomes, easy financing, compact SUV demand, and frequent new model launches continue to support strong sales in this segment.

To access detailed market analysis, Request Sample

Motorcycles at 24.7% reflect India's strong preference for affordable and fuel-efficient personal transportation, particularly in urban and rural areas. Light trucks at 8.1% reflect growing demand for last-mile delivery, e-commerce logistics, and intra-city goods transportation. Heavy trucks at 5.4% reflect the country's increasing freight movement requirements driven by industrial production, mining, construction, and long-distance logistics activities. Bus at 5.0% reflect sustained demand for public transportation, employee commuting, school transportation, and intercity travel.

By Fuel Type

Internal combustion engine leads at 82.4% (2025), through petrol and diesel engines across mass-market passenger cars, motorcycles, and commercial vehicles.

Electric at 7.4% grows fastest at ~18.5% CAGR. Compressed natural gas at 5.3% reflects the CNG fleet. Hybrid at 3.8% reflects strong hybrid and mild hybrid vehicles. The hydrogen fuel cell at 1.1%.

Regional Market Insights

|

Region |

Share (2025) |

Key India Automobile Market Drivers & Characteristics |

|

West India |

34.6% |

Reflecting its strong automotive manufacturing ecosystem, major OEM production facilities, extensive supplier network, high vehicle ownership, and export-oriented infrastructure. |

|

North India |

28.7% |

Reflects strong consumer demand, large urban population centers, expanding middle-class incomes, and significant commercial vehicle and passenger car sales. |

|

South India |

22.5% |

Reflects the presence of major automotive manufacturing hubs, growing EV investments, strong auto-component production, and rising vehicle demand. |

|

East India |

14.2% |

Reflects increasing vehicle penetration, infrastructure development, improving road connectivity, and growing demand for passenger and commercial vehicles. |

West India's 34.6% dominance is supported by strong OEM manufacturing hubs, auto-component clusters, port access, and high vehicle demand in Maharashtra and Gujarat. North India's 28.7% due to large consumer markets, strong commercial vehicle usage, and expanding urban mobility needs.

South India's 22.5% benefits from established auto manufacturing, EV investments, and technology-driven component production. East India's 14.2% gradually growing with improving road connectivity, infrastructure development, and rising vehicle penetration.

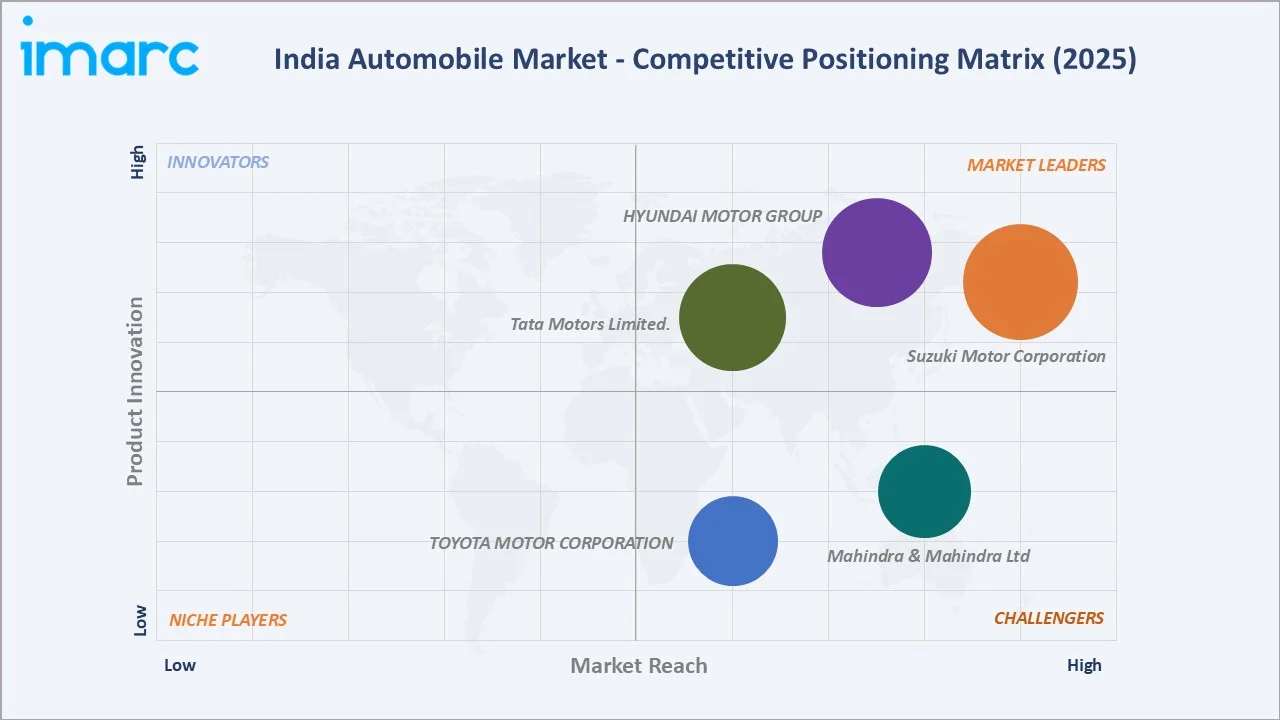

Competitive Landscape

The India automobile market is moderately concentrated, with leading players accounting for a significant share of vehicle sales. Competition is driven by product innovation, pricing strategies, fuel efficiency, safety features, and expanding EV portfolios. Automakers are investing heavily in SUVs, electric vehicles, connected technologies, and localization of components to strengthen market positions.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Suzuki Motor Corporation |

Maruti Suzuki Arena, NEXA, True Value |

Market Leader |

Suzuki Motor Corporation is the foundational architect of personal mobility in India. Through its subsidiary Maruti Suzuki India Limited, it commands the passenger vehicle market. |

|

HYUNDAI MOTOR GROUP |

Hyundai |

Market Leader |

Hyundai Motor Group operates as one of the largest passenger vehicle manufacturers in India. Through Hyundai Motor India, it drives major domestic sales and serves as a vital global export hub. |

|

Tata Motors Limited. |

Tata Motors |

Market Leader |

Tata Motors Limited is a leading Indian multinational automotive manufacturing company. It plays a foundational role in the nation's economy as the dominant manufacturer of commercial vehicles and a top-tier producer of passenger cars. |

|

Mahindra & Mahindra Ltd |

Mahindra |

Strong Challenger |

Mahindra & Mahindra Ltd pioneered utility vehicles in India by assembling the Willys Jeep. The Mahindra Automotive flagship is a dominant SUV manufacturer and one of the largest tractor producers by volume, driving widespread domestic mobility and commercial transport. |

|

TOYOTA MOTOR CORPORATION |

Toyota |

Strong Challenger |

Operating primarily through Toyota Kirloskar Motor, the Toyota Motor Corporation has shaped the Indian automotive industry by introducing iconic, highly durable utility vehicles and pioneering locally manufactured self-charging strong hybrid electric vehicles. |

Global OEMs continue to expand manufacturing and R&D operations in India, attracted by strong domestic demand and export opportunities. The market remains highly competitive across passenger vehicles, two-wheelers, commercial vehicles, and emerging electric mobility segments.

Key Company Profiles

Suzuki Motor Corporation

Suzuki Motor Corporation is a leading player in the India automobile market through its subsidiary Maruti Suzuki India Limited, which holds a strong position in the passenger vehicle segment. The company is known for affordable, fuel-efficient, and reliable cars across hatchbacks, sedans, MPVs, and compact SUVs.

- Key Brands: Maruti Suzuki Arena, NEXA, True Value.

- Recent Developments: In June 2026, Maruti Suzuki began deliveries of the WagonR Bio-Flex, India’s first passenger car designed to operate on ethanol blends ranging from E20 to E100. Priced at Rs 7.24 lakh ex-showroom, the model includes ethanol-compatible injectors, modified fuel lines, an upgraded fuel pump, and a recalibrated ECU, marking a shift of flex-fuel technology from pilot trials to mainstream consumer use.

- Strategic Focus: Maintaining its leadership in the India automobile market through its subsidiary, Maruti Suzuki India Limited, by strengthening its presence in the mass-market passenger vehicle segment.

HYUNDAI MOTOR GROUP

Hyundai Motor Group is a major participant in the India automobile market through its subsidiary, Hyundai Motor India Limited. The company has established a strong presence across hatchback, sedan, SUV, and electric vehicle segments, making it one of the leading passenger vehicle manufacturers in the country.

- Key Brands: Hyundai

- Recent Developments: In April 2026, Hyundai Motor India Limited launched the new Hyundai IONIQ 5 with upgrades in performance, technology, safety, and everyday usability. Built on Hyundai’s Electric Global Modular Platform, the IONIQ 5 reflects the company’s focus on smart, sustainable, and customer-centric electric mobility.

- Strategic Focus: Focused on strengthening its position in India through expansion of its SUV, premium vehicle, and electric vehicle portfolios.

Market Concentration Analysis

The India automobile market is moderately concentrated, with a handful of large manufacturers accounting for a substantial share of vehicle sales, particularly in the passenger vehicle segment. Companies such as Suzuki Motor Corporation, HYUNDAI MOTOR GROUP, Tata Motors Limited, Mahindra & Mahindra Ltd, and TOYOTA MOTOR CORPORATION dominate the market through extensive dealer networks, strong brand recognition, and diversified product portfolios. However, competition remains intense due to the presence of global OEMs, emerging EV manufacturers, and strong regional players. Market concentration is higher in passenger vehicles, while two-wheelers and commercial vehicles exhibit a more diversified competitive landscape. Continuous investment in EVs, SUVs, connected technologies, and localization strategies is shaping competitive positioning across the industry.

Investment & Growth Opportunities

Highest Growth Segments

Electric vehicles (~18.5% CAGR), hybrid (~12.2% CAGR), CNG (~9.4% CAGR through fleet mandate), passenger car (~7.5% CAGR), SUV premium, and EV two-wheeler mass market (Ola Electric ~25% CAGR from high base) represent India's automobile industry's highest-growth investment vectors through 2034.

Investment Themes

- EV ecosystem investment: Investment in the EV ecosystem offers strong growth potential through battery manufacturing, charging infrastructure, software platforms, and localized component production. Rising EV adoption and government incentives are creating opportunities across the entire electric mobility value chain.

- SUV premiumization platform: SUV premiumization presents an attractive investment theme as consumers increasingly prefer feature-rich, higher-margin SUVs with advanced safety, connectivity, and comfort features. This trend is enabling automakers to improve profitability while expanding their premium vehicle portfolios.

Future Market Outlook (2026-2034)

India automobile market is projected to grow from USD 143.0 Billion in 2025 to USD 278.5 Billion by 2034, delivering a 7.31% CAGR over the forecast period through rising middle-class automobile aspiration, PM e-DRIVE EV acceleration, SUV premiumization structural shift, EV ecosystem expansion, and India's favorable young demography. The market's anchor value of USD 203.4 Billion in 2030 represents India's automobile industry at EV mainstream inflection.

Three structural forces define India's automobile market growth through 2034. First, rising middle-class incomes and urbanization are expanding demand for passenger vehicles, SUVs, and premium mobility solutions. Second, government support through manufacturing incentives, infrastructure development, and export promotion is strengthening domestic production and global competitiveness. Third, the transition toward electric, connected, and safer vehicles is accelerating technological innovation and creating new growth opportunities across the automotive value chain.

Research Methodology

Primary Research

Primary research comprised interviews with automobile manufacturers, component suppliers, dealerships, fleet operators, industry experts, and policy stakeholders across India. Discussions focused on vehicle demand trends, production outlook, technology adoption, EV penetration, pricing dynamics, and consumer preferences. These insights were used to validate market estimates, competitive positioning, and future growth assumptions across vehicle segments and regions.

Secondary Research

Secondary research encompassed the review of company annual reports, investor presentations, industry publications, government databases, SIAM reports, automotive trade statistics, and policy documents. It also included analysis of vehicle registration data, export-import trends, EV adoption metrics, and infrastructure developments. These sources were used to assess market size, competitive dynamics, technology trends, and long-term industry growth prospects.

Forecasting Models

Forecasting models combined historical vehicle sales, production volumes, export performance, GDP growth, disposable income trends, and urbanization indicators to project market demand. A hybrid methodology incorporating time-series analysis, econometric modeling, and vehicle segment-specific adoption trends was used to estimate future growth. Scenario-based forecasting also evaluated the impact of EV penetration, infrastructure development, regulatory changes, and technology adoption through 2034.

India Automobile Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Fuel Types Covered |

Internal Combustion Engine, Electric, Hybrid, Hydrogen Fuel Cell, Compressed Natural Gas |

|

Vehicle Types Covered |

Passenger Car, Light Truck, Heavy Truck, Bus, Motorcycle |

|

Channels Covered |

Direct Sales, Dealerships, Online Sales, Fleet Sales, Export |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Suzuki Motor Corporation, HYUNDAI MOTOR GROUP, Tata Motors Limited., Mahindra & Mahindra Ltd, TOYOTA MOTOR CORPORATION, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Automobile Market Report

The India automobile market reached USD 143.0 Billion in 2025, driven by rising disposable incomes, urbanization, improved road infrastructure, and growing demand for personal and commercial mobility. Government support for domestic manufacturing, EV adoption, exports, and advanced auto components further strengthens long-term market growth.

The India automobile market grows at 7.31% CAGR during 2026-2034, reaching USD 278.5 Billion by 2034. The CAGR reflects middle-class income growth, PM e-DRIVE EV policy, SUV premiumization, favorable young demography, and the PLI automobile export scheme.

Passenger car leads at 56.8% due to increasing personal mobility needs, rising household incomes, and strong demand for compact cars, sedans, and SUVs. Easy financing options and continuous new model launches further support segment dominance.

Internal combustion engine leads at 82.4% due to its extensive fuel distribution network, lower upfront vehicle costs, and wide availability across passenger, two-wheeler, and commercial vehicle categories. Established consumer familiarity and supporting service infrastructure further reinforce its dominance.

West India leads at 34.6% due to strong OEM manufacturing hubs, auto-component clusters, port connectivity, and export infrastructure in Maharashtra and Gujarat. High urbanization, industrial activity, and consumer purchasing power further support regional dominance.

Leading companies include Suzuki Motor Corporation, HYUNDAI MOTOR GROUP, Tata Motors Limited., Mahindra & Mahindra Ltd, and TOYOTA MOTOR CORPORATION, among others.

The market is projected to reach approximately USD 203.4 Billion by 2030, supported by rising vehicle ownership, urbanization, and income growth. Expansion in EVs, SUVs, exports, and domestic manufacturing is expected to further strengthen market growth.

Three priority investment opportunities in the India automobile market include electric vehicle ecosystem development, encompassing batteries, charging infrastructure, and localized EV components. SUV premiumization platforms offer attractive growth potential as consumers increasingly favor feature-rich and higher-margin SUV models. Additionally, connected and software-defined vehicle technologies, including ADAS, telematics, and digital mobility solutions, present significant opportunities as demand for smarter, safer, and technology-enabled vehicles continues to rise.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)