India Automotive Glass Market Size, Share, Trends and Forecast by Glass Type, Material Type, Vehicle Type, Application, End User, Technology, and Region, 2026-2034

India Automotive Glass Market Summary:

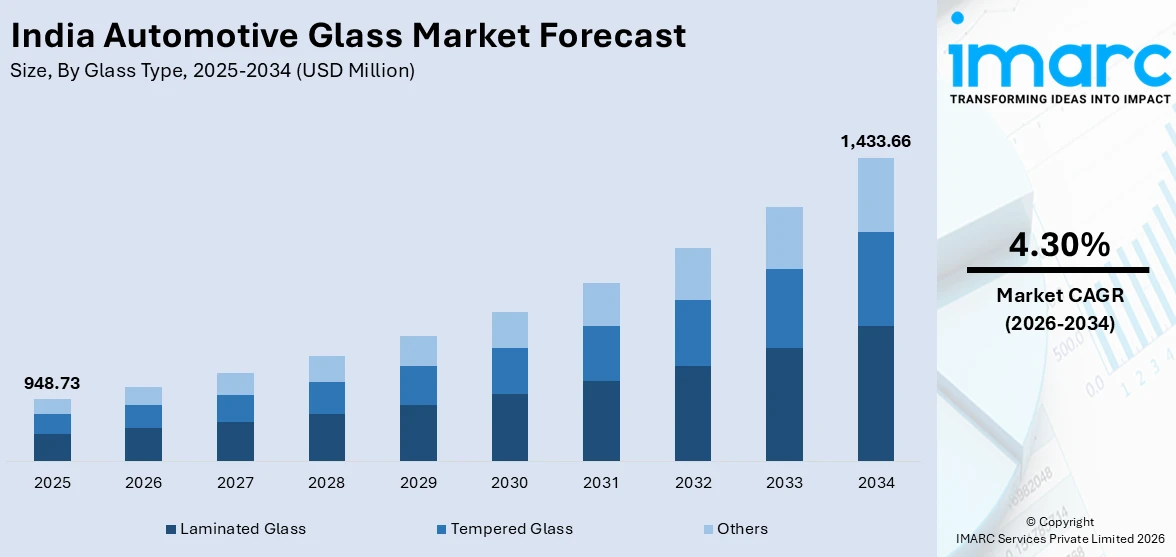

The India automotive glass market size was valued at USD 948.73 Million in 2025 and is projected to reach USD 1,433.66 Million by 2034, growing at a compound annual growth rate of 4.30% from 2026-2034.

The market is driven by surging domestic vehicle production, mandatory safety regulations promoting laminated glass adoption, and rising consumer preference for thermally efficient and acoustically superior glazing solutions. Expanding urbanization, growing middle-class purchasing power, and accelerating electric vehicle penetration further stimulate demand for advanced glass technologies across passenger and commercial vehicle segments. Increasing integration of infrared-rejecting and solar-control glass solutions continues to redefine the India automotive glass market share.

Key Takeaways and Insights:

- By Glass Type: Laminated glass dominates the market with a share of 66.0% in 2025, driven by mandatory windshield safety regulations, superior shatterproof properties, and widespread OEM adoption.

- By Material Type: IR PVB leads the market with a share of 34.0% in 2025, owing to exceptional infrared heat rejection, ultraviolet protection, and growing electric vehicle OEM preference.

- By Vehicle Type: Passenger cars represent the largest segment with a market share of 74.0% in 2025, driven by surging domestic demand, rising incomes, and advanced safety glazing adoption.

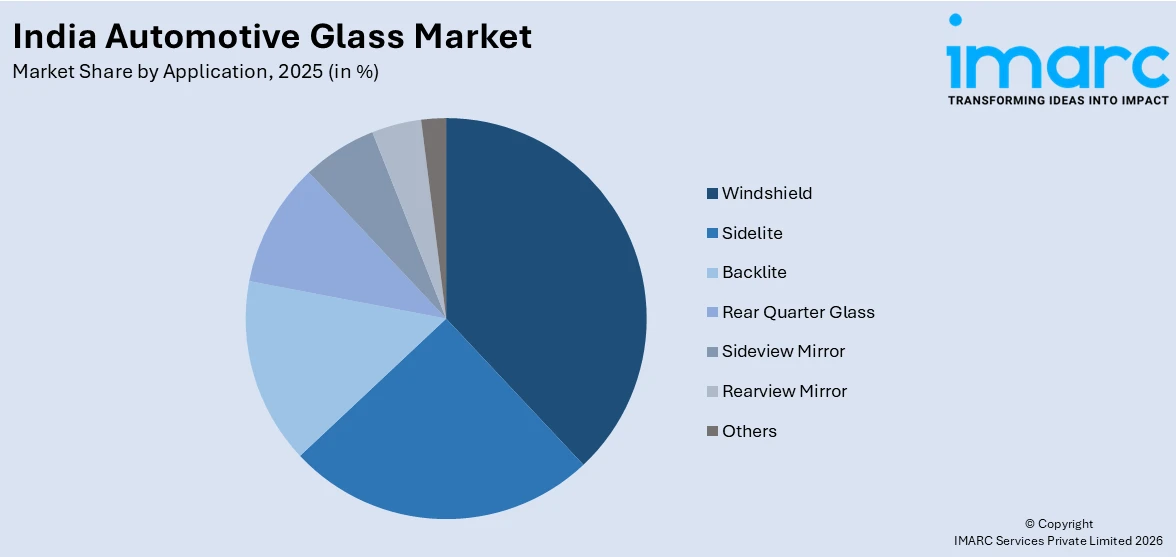

- By Application: Windshield dominates the market with a share of 38.0% in 2025, owing to mandatory laminated glass compliance, ADAS sensor integration, and multifunctional glazing technology requirements.

- By End User: OEMs lead the market with a share of 81.0% in 2025, owing to deeply integrated supply chain partnerships, high-volume procurement contracts, and stringent quality compliance requirements.

- By Technology: Passive glass represents the largest segment with a market share of 85.0% in 2025, driven by cost-competitiveness, technical maturity, and entrenched mass-market manufacturing adoption.

- By Region: North India leads the market with a share of 32.0% in 2025, driven by concentrated automotive manufacturing hubs, established OEM supply chains, and strong vehicle assembly presence.

- Key Players: The India automotive glass market features a moderately competitive landscape, with established domestic manufacturers and global glass suppliers competing across OEM and aftermarket channels through product innovation, advanced manufacturing capabilities, and long-term supply partnerships.

To get more information on this market Request Sample

The India automotive glass market is underpinned by a convergence of structural and technological growth forces that are steadily reshaping demand across all vehicle categories. The country's rapidly expanding automotive manufacturing base, supported by favourable government policies, growing infrastructure investment, and rising household incomes, generates sustained demand for both OEM and aftermarket glass components. In November 2025, India’s Directorate General of Trade Remedies recommended extending anti‑dumping duties on Malaysian glass imports for five years to protect domestic producers such as Asahi India Glass and Saint‑Gobain India. Consumer expectations for vehicles with enhanced safety, thermal comfort, and aesthetic sophistication have elevated the role of advanced glazing technologies within vehicle design. Regulatory mandates requiring certified safety glass in windshields have transformed laminated glass from a premium option into a baseline compliance imperative. The accelerating adoption of electric vehicles further amplifies demand for lightweight, energy-efficient glass solutions engineered to reduce cabin thermal load, extend battery range, and support next-generation driver assistance technologies.

India Automotive Glass Market Trends:

Rising Integration of Advanced Driver Assistance Technologies into Automotive Glazing

The widespread deployment of advanced driver assistance systems across new vehicle categories is fundamentally transforming automotive glass design in India. Windshields are increasingly engineered to accommodate embedded camera zones, sensor arrays, and radar-transparent sections supporting collision avoidance, lane-keeping, and adaptive cruise functionalities. In 2025, Asahi India Glass expanded its automotive portfolio with ADAS-ready windshields, integrating heads-up displays, rain sensors, and radar-transparent sections to meet rising OEM demand. This integration demands precision manufacturing and optically uniform laminated glass substrates that maintain unimpaired sensor performance under all operating conditions.

Growing Preference for Thermally Efficient and Solar-Control Glazing Solutions

India's demanding climatic conditions, characterized by prolonged high solar radiation and elevated ambient temperatures, are accelerating the shift toward thermally efficient automotive glass. Infrared-rejecting interlayers and solar-control coatings are increasingly specified by vehicle manufacturers to reduce cabin heat accumulation, enhance occupant comfort, and lower the energy burden on air conditioning systems. In August 2025, Asahi India Glass began leveraging locally sourced float and solar control glass at its Patan facility, boosting thermal performance capabilities for windshields and sunroofs to better suit India’s high‑temperature conditions. This preference is particularly pronounced within the electric vehicle segment, where minimizing thermal load through advanced glazing directly improves battery efficiency and extends driving range, further supporting adoption across premium and mid-range vehicle categories.

Broadening Application Scope of Laminated Glass Across Vehicle Glazing Positions

Historically concentrated in front windshields, laminated glass is progressively being adopted across a wider range of vehicle glazing positions in India, including side windows, rear screens, and panoramic roof panels. Rising consumer expectations for acoustic insulation, enhanced occupant protection, and refined vehicle aesthetics are encouraging OEMs to extend laminated glass specifications beyond regulatory minimums. In 2024, Asahi India Glass (AIS) projected supplying over 1.5 million sunroof glasses and expanding laminated side-window glass with solar and acoustic insulation, reflecting rising premium automotive demand. This broadening adoption is especially prominent within premium passenger vehicles and utility vehicle segments, where acoustic laminated glass and curved panoramic roofing systems are increasingly positioned as key value-differentiating features.

Market Outlook 2026-2034:

The India automotive glass market is poised for consistent and well-supported growth over the forecast period, anchored by sustained vehicle production expansion, progressively stringent safety regulations, and the accelerating shift toward electric and connected vehicle platforms. Revenue expansion is expected to be reinforced by growing OEM demand for advanced glazing technologies, including IR PVB laminated glass, ADAS-integrated windshields, and panoramic solar-control roofing systems. Expanding vehicle penetration in smaller cities and rising aftermarket replacement demand are anticipated to contribute meaningfully to overall market progression through the forecast horizon. The market generated a revenue of USD 948.73 Million in 2025 and is projected to reach a revenue of USD 1,433.66 Million by 2034, growing at a compound annual growth rate of 4.30% from 2026-2034.

India Automotive Glass Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Glass Type |

Laminated Glass |

66.0% |

|

Material Type |

IR PVB |

34.0% |

|

Vehicle Type |

Passenger Cars |

74.0% |

|

Application |

Windshield |

38.0% |

|

End User |

OEMs |

81.0% |

|

Technology |

Passive Glass |

85.0% |

|

Region |

North India |

32.0% |

Glass Type Insights:

- Laminated Glass

- Tempered Glass

- Others

Laminated glass dominates with a market share of 66.0% of the total India automotive glass market in 2025.

Laminated leads the India automotive glass market, reflecting its essential role in windshield safety compliance and its structural superiority over conventional alternatives. Its bonded interlayer construction prevents glass from shattering upon impact, retaining fragments and protecting occupants from injury while maintaining structural integrity during collision events. Beyond safety, laminated glass delivers meaningful acoustic damping, ultraviolet filtration, and improved weathering resistance, making it the preferred glazing specification for OEM procurement across passenger cars, utility vehicles, and premium vehicle platforms throughout India.

Laminated adoption continues to expand as vehicle manufacturers progressively integrate advanced functionalities directly into the glazing substrate. ADAS sensor compatibility, head-up display projection zones, and infrared-rejecting interlayers are increasingly specified within laminated windshield constructions, elevating both technical complexity and per-unit commercial value. Growing consumer expectations for cabin quietness, thermal comfort, and enhanced occupant protection further reinforce OEM preference for laminated glass across a broadening range of glazing positions beyond the windshield, including side windows, rear screens, and panoramic roof panels.

Material Type Insights:

- IR PVB

- Metal Coated Glass

- Tinted Glass

- Others

IR PVB leads with a share of 34.0% of the total India automotive glass market in 2025.

IR PVB dominates the material type segment, reflecting its critical advantage in filtering infrared radiation and significantly reducing solar heat transmission into vehicle interiors. The interlayer is laminated between glass panels to create windshields and panoramic roofs that maintain lower cabin temperatures, reducing dependence on air conditioning and improving overall vehicle energy efficiency. This functional superiority is increasingly recognized by OEMs developing both conventional and electric vehicle architectures, where effective cabin thermal management directly influences occupant comfort, system efficiency, and overall vehicle performance across diverse operating conditions.

Growing awareness of in-cabin climate quality among Indian consumers is further strengthening the demand for IR PVB as a premium yet increasingly accessible material specification. As electric vehicle adoption accelerates across the country, the strategic advantage of IR PVB in reducing thermal load and extending battery range positions it as a preferred glazing interlayer for next-generation vehicle platforms. OEMs are increasingly standardizing IR PVB specifications across mid-range and premium vehicle lines, reinforcing its dominant position within the material type segment throughout the forecast period.

Vehicle Type Insights:

- Passenger Cars

- Light Commercial Vehicles

- Trucks

- Buses

- Others

Passenger cars exhibit a clear dominance with a 74.0% share of the total India automotive glass market in 2025.

Passenger cars represent the largest vehicle type segment, driven by the sustained expansion of domestic vehicle ownership, India's growing middle-class population, and increasing consumer preference for safety-certified and thermally comfortable vehicles. The diversity of the passenger car segment, spanning entry-level hatchbacks through premium sedans and utility vehicles, generates broad and consistent demand for automotive glass across multiple specifications and price points. In June 2024, Asahi India Glass noted rising OEM demand for UV‑cut side window glasses and rear‑defogger‑equipped windshields in passenger cars, driven by premium feature adoption nationwide.

The ongoing transition toward passenger cars within this segment is creating incremental demand for lightweight, solar-rejecting, and multifunctional glazing technologies tailored to electric drive-train requirements. IR PVB laminated windshields, panoramic solar-control roofs, and ADAS-compatible glass are increasingly specified across new electric passenger car platforms, adding both technical complexity and commercial value to OEM glass procurement. Rising vehicle penetration in smaller cities and Tier-2 markets further sustain structural volume growth within the passenger car segment, extending consistent automotive glass demand across a widening geographic base.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Windshield

- Sidelite

- Backlite

- Rear Quarter Glass

- Sideview Mirror

- Rearview Mirror

- Others

Windshield leads with a market share of 38.0% of the total India automotive glass market in 2025.

Windshields hold the largest application segment, driven by mandatory laminated glass regulations governing front glazing across all new vehicle categories. Their role as a primary occupant safety structure, responsible for maintaining cabin integrity during collisions and retaining airbag deployment forces, makes them non-negotiable components within every vehicle assembly. The critical nature of windshield performance has elevated supplier quality standards and deepened OEM procurement relationships, ensuring windshields remain the highest-value and most technically demanding glazing application within India's automotive glass market across all vehicle segments.

The integration of advanced technologies directly into windshield substrates is further strengthening this segment's commercial importance. ADAS camera zones, rain and light sensors, head-up display projection areas, and solar-control coatings are increasingly standard specifications within new vehicle windshields, transforming them from passive safety components into active multifunctional surfaces. Growing consumer demand for connected and intelligent vehicle experiences, combined with tightening safety regulations requiring more sophisticated glazing solutions, ensures that windshield technology investment by OEMs will continue to expand consistently throughout the forecast period.

End User Insights:

- OEMs

- Aftermarket Suppliers

OEMs dominate with a market share of 81.0% of the total India automotive glass market in 2025.

OEMs account for the dominant end user segment, reflecting the deeply integrated nature of automotive glass supply within India's vehicle assembly ecosystem. Glass manufacturers develop bespoke glazing solutions aligned with precise OEM technical specifications, safety certifications, and production schedule requirements. Long-term supply agreements, just-in-time logistics, and co-development of advanced glass technologies cement these partnerships as the primary revenue engine for leading glass producers. The growing complexity of OEM glass requirements, spanning ADAS compatibility, thermal management, and acoustic performance, further reinforces supplier focus on this channel.

As India's automotive industry evolves toward electric, connected, and safety-advanced vehicle platforms, OEM glass procurement is becoming progressively more technically demanding and commercially significant. Vehicle manufacturers are engaging glass suppliers earlier in the product development cycle, collaborating on integrated glazing solutions that serve multiple functional roles simultaneously. This deepening co-development relationship strengthens the structural stability of OEM revenue streams while creating meaningful barriers for new entrants seeking to penetrate established OEM supply chains. The OEM segment is therefore expected to maintain its commanding market position throughout the forecast period.

Technology Insights:

- Active Smart Glass

- Suspended Particle Glass

- Electrochromic Glass

- Liquid Crystal Glass

- Passive Glass

- Thermochromic Glass

- Photochromic Glass

Passive glass leads with a share of 85.0% of the total India automotive glass market in 2025.

Passive glass holds the dominant technology segment position, reflecting its established status as a cost-effective, reliable, and technically proven solution across India's mass-market automotive landscape. Passive glass variants deliver functional temperature and light-management characteristics without requiring electrical actuation or embedded control systems, making them inherently compatible with conventional vehicle architectures across all price segments. Their affordability and broad manufacturing scalability make them the default glazing technology specification for passenger cars, commercial vehicles, and two-wheelers produced across India's highly price-competitive automotive manufacturing base.

The entrenched position of passive glass within OEM supply chains is reinforced by its consistent performance across India's diverse climatic and operational environments. Thermochromic and photochromic variants within this category respond passively to temperature and light stimuli, delivering meaningful solar management benefits without additional vehicle system complexity or cost. As vehicle manufacturers seek to balance advanced glazing performance with cost-efficiency targets across mass-market platforms, passive glass remains the pragmatic and commercially viable technology of choice, sustaining its dominant market position throughout the forecast period across all major vehicle categories.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India dominates with a market share of 32.0% of the total India automotive glass market in 2025.

North India leads the regional segment, driven by the dense concentration of vehicle manufacturing and component supply activities across Delhi NCR, Haryana, and adjacent industrial corridors. The region benefits from mature automotive infrastructure, established logistics networks, and a deep OEM supplier ecosystem that positions it as a primary consumption hub for automotive glass. Strong industrial policy support, skilled workforce availability, and proximity to key supply chain networks further consolidate North India's leadership position within the domestic automotive glass market across all major glazing categories and vehicle types.

Continued investment in vehicle manufacturing capacity and the progressive expansion of automotive supplier parks within North India are expected to sustain this region's dominant market positioning throughout the forecast period. The concentration of passenger car assembly plants, commercial vehicle manufacturers, and component suppliers within this region ensures consistently high-volume demand for laminated windshields, sidelites, and advanced glazing solutions. Rising vehicle ownership among urban and semi-urban consumers within northern states also contributes to growing aftermarket replacement demand, adding a secondary demand layer that reinforces North India's overall automotive glass market leadership.

Market Dynamics:

Growth Drivers:

Why is the India Automotive Glass Market Growing?

Expanding Domestic Vehicle Production and Rising Automobile Ownership

India's automotive industry has established itself as one of the world's largest vehicle manufacturing bases, with domestic production continuing to scale in response to rising consumer demand across passenger cars, utility vehicles, commercial vehicles, and two-wheelers. Increasing urbanization, progressive improvement in road infrastructure, expanding access to vehicle financing, and growing middle-class incomes are collectively elevating automobile ownership levels across the country. In January 2026, Maruti Suzuki announced a new Gujarat plant to add one million vehicles annually, supporting rising domestic demand and strengthening India’s position as a global automotive hub. This structural growth in vehicle production directly amplifies demand for automotive glass at the OEM level, as every newly assembled vehicle requires windshields, sidelites, backlites, and mirror components sourced from certified glass suppliers.

Stringent Safety Regulations Mandating Adoption of Certified Safety Glass

Progressive tightening of automotive safety standards by Indian regulatory authorities has made the use of certified laminated glass in vehicle windshields a compliance requirement across all new vehicle types. According to reports, in March 2025, the Government of India notified 187 Quality Control Orders covering 769 products under compulsory BIS certification, reinforcing mandatory compliance for safety-critical automotive components including laminated glass. These regulations have fundamentally altered procurement practices within the automotive industry, elevating laminated glass from a premium specification to an essential manufacturing input. Alignment of Indian safety norms with global standards drives OEMs to adopt advanced, compliant glass, boosting demand for safety components.

Growing Consumer Preference for Premium Comfort and Aesthetic Glazing Features

Rising disposable incomes and evolving consumer aspirations are reshaping vehicle purchasing behaviour across India, with buyers increasingly prioritising in-cabin comfort, noise insulation, and aesthetic refinement in their vehicle selection decisions. In April 2025, over 53% of new Hyundai cars sold in India were purchased with sunroof variants, reflecting rising consumer demand for premium comfort and cabin features. This shift is encouraging automakers to offer advanced glazing specifications, including acoustic laminated glass, tinted sidelights, and panoramic roof panels, as either standard or optional features across mid-range and premium vehicle platforms. As buyers demand higher quality and enhanced driving comfort, automotive glass evolves from safety necessity to a key differentiator, boosting premiumization in India.

Market Restraints:

What Challenges the India Automotive Glass Market is Facing?

High Volatility in Raw Material Input Costs

Automotive glass manufacturing relies on key raw materials including soda ash, silica sand, and polyvinyl butyral interlayers, all of which are subject to recurring price fluctuations tied to global commodity markets and energy costs. These input cost variations create significant margin pressure for glass producers, particularly those operating under fixed-price OEM supply contracts, limiting their ability to sustain profitability while maintaining competitive pricing.

Significant Capital Requirements for Manufacturing Infrastructure

Establishing and sustaining automotive glass manufacturing operations demands substantial capital investment across float glass furnaces, tempering lines, lamination facilities, and precision quality control systems. These elevated entry barriers and ongoing capital expenditure requirements limit the ability of smaller domestic manufacturers to expand production capacity in alignment with rising vehicle output, potentially creating supply constraints and increasing dependency on imported glass for specialized product categories.

Competitive Pressure from Low-Cost Imported Glass Products

India's automotive glass market faces sustained competitive pressure from imported products manufactured in lower-cost regions and priced below domestically produced equivalents. The aftermarket segment is particularly vulnerable, as price sensitivity among end consumers enables lower-cost imports to capture meaningful replacement demand. This dynamic constrains domestic manufacturers' pricing power and limits their revenue realization potential within the replacement glass distribution channel.

Competitive Landscape:

The India automotive glass market is characterized by a moderately concentrated competitive landscape, with established domestic producers and international glass suppliers competing across OEM and aftermarket channels. Leading participants leverage vertically integrated manufacturing operations, robust product development capabilities, and long-standing OEM supply agreements to sustain their market positions. Differentiation is achieved through advanced product development encompassing IR PVB laminated glass, acoustic windshields, ADAS-compatible glazing, and thermally efficient solar-control glass. Regional distribution strength, quality certification, and the ability to co-develop tailored glazing solutions with vehicle manufacturers represent critical competitive capabilities shaping market dynamics and supplier positioning in India.

India Automotive Glass Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Glass Types Covered | Laminated Glass, Tempered Glass, Others |

| Material Types Covered | IR PVB, Metal Coated Glass, Tinted Glass, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Trucks, Buses, Others |

| Applications Covered | Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, Rearview Mirror, Others |

| End Users Covered | OEMs, Aftermarket Suppliers |

| Technologies Covered |

|

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Automotive Glass Market Research Report and Industry Forecast Report

The India automotive glass market size was valued at USD 948.73 Million in 2025.

The India automotive glass market is expected to grow at a compound annual growth rate of 4.30% from 2026-2034 to reach USD 1,433.66 Million by 2034.

Laminated glass held the largest share, driven by mandatory windshield safety regulations, superior shatterproof and occupant protection properties, strong acoustic and ultraviolet filtration performance, and widespread adoption across OEM supply chains serving passenger and commercial vehicle manufacturers throughout India.

Key factors driving the India automotive glass market include expanding domestic vehicle production, mandatory safety regulations promoting laminated glass adoption, accelerating electric vehicle transition, rising demand for thermally efficient IR PVB glass, and increasing ADAS technology integration within automotive windshields and glazing systems.

Major challenges include raw material input cost volatility affecting producer margins, high capital investment requirements for glass manufacturing infrastructure, competitive pressure from lower cost imported products in the aftermarket segment, and the technical complexity of scaling advanced smart glass production for mass-market vehicle platforms in India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)