India Automotive Market Size, Share, Trends and Forecast by Vehicle Type, Propulsion Type, Application, Ownership Mode, and Region 2026-2034

India Automotive Market Summary:

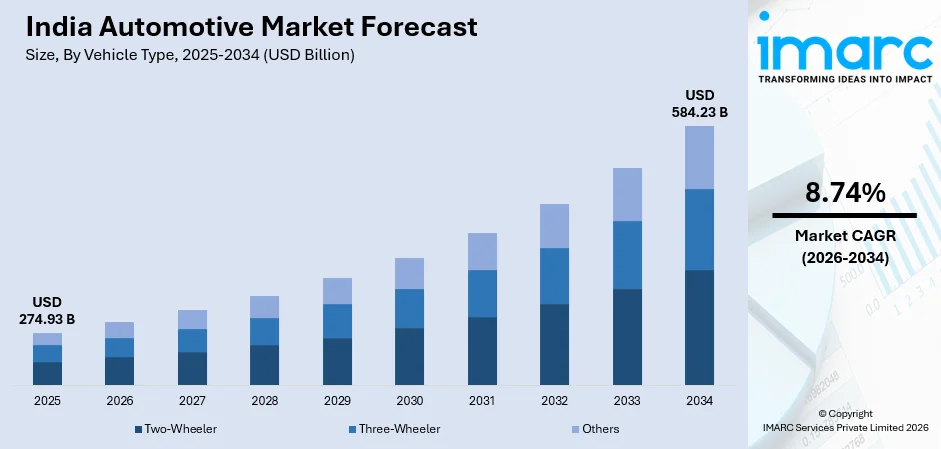

The India automotive market size was valued at USD 274.93 Billion in 2025 and is projected to reach USD 584.23 Billion by 2034, growing at a compound annual growth rate of 8.74% from 2026-2034.

The India automotive market is experiencing robust growth driven by rising consumer demand, government incentives for electric vehicles, expansion of automotive manufacturing infrastructure, and increasing adoption of advanced technologies such as connected and autonomous vehicles, while strong investments in research and development (R&D), supportive policies, and a growing middle-class population continue to propel production, sales, and exports across passenger, commercial, and electric vehicle segments nationwide.

Key Takeaways and Insights:

- By Vehicle Type: Two-wheelers led the market with a 72.6% share in 2025, fueled by affordability, fuel efficiency, easy traffic maneuverability, and rising demand among young consumers for personal mobility in urban and semi-urban areas.

- By Propulsion Type: Internal combustion engines dominated with 86.1% market share, in 2025, driven by fuel availability, established infrastructure, lower costs, and consumer familiarity, maintaining supremacy over electric and alternative propulsion options.

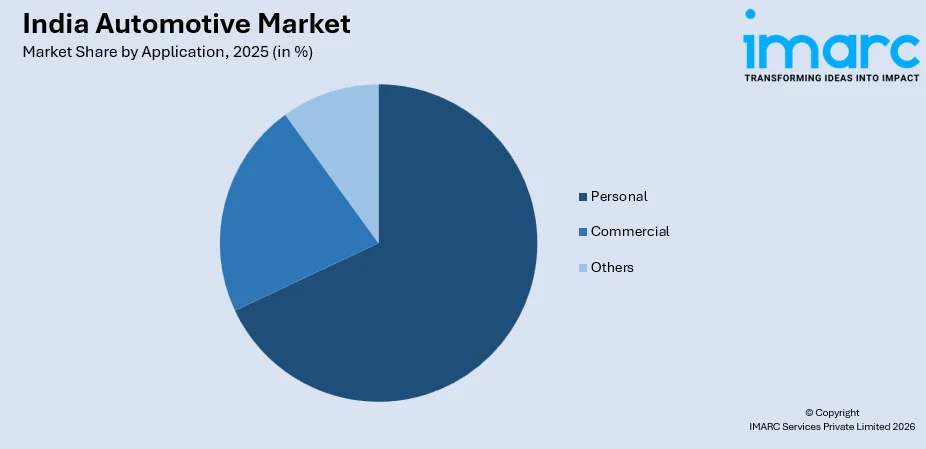

- By Application: Personal dominates the market with a share of 68.4% in 2025, reflecting rising individual mobility needs, growing urbanization, lifestyle preferences, and demand for convenient and independent transportation solutions.

- By Ownership Mode: Individual ownership accounted for the highest market share of 74.2% in 2025, driven by consumer preference for personal convenience, flexibility, and the ability to use vehicles for daily commuting and long-distance travel.

- By Region: West India held the largest market segment, capturing 35.1% share, in 2025, supported by strong industrial growth, urban population density, robust transportation infrastructure, and high vehicle adoption across major states.

- Key Players: The market is highly competitive, with leading manufacturers focusing on product innovation, extensive distribution networks, strategic partnerships, and electrification initiatives to strengthen market position and capture growing consumer demand.

To get more information on this market Request Sample

The India automotive market is experiencing substantial growth, propelled by increasing consumer demand, rising disposable income, and rapid urbanization across major cities. Industry data shows that per capita GNDI at current prices rose from INR 29,894 in 2004–05 to INR 1,00,349 in 2014–15 and further doubled to INR 2,14,951 by 2023–24. Government initiatives promoting electric vehicles, emissions reduction, and Make in India policies are also encouraging domestic manufacturing and technological innovation. The heightened adoption of connected, hybrid, and autonomous vehicle technologies is transforming mobility, while growing awareness of fuel efficiency is influencing vehicle choices. Likewise, significant OEM investments in R&D, digital sales platforms, and dealership network growth are expanding market presence and reach. Growth is further supported by the burgeoning two-wheeler and passenger vehicle segments, as well as expanding commercial vehicle demand for logistics and last-mile delivery. Additionally, rising exports, infrastructure improvements, and greater financial accessibility through easy financing schemes are strengthening the overall market and establishing India as a key automotive hub in Asia.

India Automotive Market Trends:

Rising Adoption of Electric Vehicles (EVs)

The India automotive market is witnessing accelerated adoption of electric vehicles, driven by government incentives, tax benefits, and growing environmental awareness. According to NITI Aayog, India aims to have electric vehicles account for 30% of total vehicle sales by 2030. EV sales in India increased from 50,000 in 2016 to 2.08 million in 2024, while global EV sales rose from 918,000 to 18.78 million over the same period. In parallel, increasing investments in charging infrastructure and battery technology are enhancing the feasibility of EVs for both two-wheelers and passenger vehicles. OEMs are launching cost-effective models with extended range, appealing to urban commuters. Public and private fleet operators are also integrating electric vehicles for last-mile logistics, reflecting a structural shift toward sustainable mobility and reduced reliance on conventional fuels.

Integration of Connected and Smart Vehicle Technologies

Connected car technologies are increasingly integrated into vehicles, offering real-time navigation, telematics, predictive maintenance, and infotainment solutions. For instance, in January 2026, Samsung’s HARMAN India is developing production-ready connected car solutions, including V2V and V2X systems, digital cockpits, telematics control units, and modular platforms, enabling faster OEM timelines, enhanced safety, and seamless 4G/5G/SatCom connectivity, all designed and built in India. Manufacturers are further incorporating IoT-enabled sensors, AI-driven safety features, and mobile connectivity to enhance user experience and operational efficiency. Adoption is driven by urban tech-savvy consumers seeking convenience, safety, and data-driven vehicle management. This trend is transforming vehicle ownership models, enabling fleet operators and individuals to optimize usage, reduce downtime, and enhance predictive decision-making across passenger and commercial segments.

Expansion of Shared Mobility and Micro-Mobility Solutions

Shared mobility and micro-mobility services, including ride-hailing, e-scooters, and bicycle-sharing, are expanding rapidly in urban India. Similarly, rising traffic congestion, parking challenges, and environmental concerns are driving consumer preference for shared solutions. Automotive companies and mobility startups are also collaborating to offer integrated app-based platforms, subscription models, and electric micro-mobility fleets. This trend reduces dependence on personal vehicle ownership, fosters sustainable urban transportation, and provides new revenue streams for OEMs, logistics providers, and technology platforms across metropolitan regions.

Market Outlook 2026-2034:

The India automotive market is poised for sustained growth, driven by increasing rural and semi-urban vehicle adoption, rising demand for premium and compact vehicles, and expansion of organized dealership networks. In parallel, continual technological advancements in electric drivetrains, autonomous features, and lightweight materials are enhancing vehicle efficiency and performance. Government infrastructure development, including expressways and smart city initiatives, further supports market expansion. Apart from this, strategic collaborations, localized manufacturing, and evolving consumer preferences for environmentally friendly and connected vehicles are expected to shape a dynamic, competitive, and innovation-driven automotive landscape. For instance, in November 2025, Japanese automakers Toyota, Suzuki, and Honda invested USD 11 Billion in India, boosting manufacturing, exports, and EV initiatives. Policy support, low costs, and a skilled workforce position India as a new global automotive production and export hub. The market generated a revenue of USD 274.93 Billion in 2025 and is projected to reach a revenue of USD 584.23 Billion by 2034, growing at a compound annual growth rate of 8.74% from 2026-2034.

India Automotive Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Vehicle Type |

Two-Wheeler |

72.6% |

|

Propulsion Type |

Internal Combustion Engine |

86.1% |

|

Application |

Personal |

68.4% |

|

Ownership Mode |

Individual Ownership |

74.2% |

|

Region |

West India |

35.1% |

Vehicle Type Insights:

- Two-Wheeler

- Three-Wheeler

- Others

Two-wheelers dominate with a market share of 72.6% of the total India automotive market in 2025.

They are preferred by students, young professionals, and first-time vehicle owners seeking cost-effective personal mobility solutions. The growing demand for lightweight, low-maintenance vehicles and rising disposable incomes in semi-urban regions further reinforce their dominance, making two-wheelers a crucial segment driving overall market growth.

The segment also benefits from the easy availability of financing options, insurance coverage, and a widespread dealership network. Manufacturers are increasingly introducing advanced features, electric variants, and premium designs to attract a broader consumer base. As such, in February 2026, Yamaha launched its first Indian electric scooter, the EC-06, priced at INR 1.67 Lakh, offering a 169 km range, a 6.7 kW motor, three riding modes, an IP67-rated battery, 24.5L storage, connected features, and an urban-focused design for eco-friendly commuting. Continuous innovation in engine efficiency, safety, and aesthetics ensures that two-wheelers remain a top-performing segment, contributing significantly to sales volumes and shaping market dynamics across India.

Propulsion Type Insights:

- Internal Combustion Engine

- Hybrid Vehicle

- Others

Internal Combustion Engine captured the largest segment, representing 86.1% of the total India automotive market share, in 2025.

The dominance is driven by supported by extensive fuel infrastructure, affordable maintenance, and consumer familiarity. Petrol and diesel engines continue to dominate, particularly in two-wheelers and passenger vehicles, due to their long operational range, cost-effectiveness, and established service networks, making ICE technology the backbone of India’s automotive ecosystem.

Despite growing interest in electric and hybrid propulsion, ICE vehicles maintain a stronghold due to low upfront costs and widespread availability. OEMs continue to optimize ICE efficiency, reducing emissions and improving performance. This segment remains a key revenue driver for manufacturers, sustaining the production and sales of conventional vehicles across both urban and rural regions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Personal

- Commercial

- Others

Personal holds the largest share, accounting for a share of 68.4% in the total India automotive market, in 2025.

Personal vehicles captured the largest market share, reflecting strong consumer demand for individual mobility. In tandem, rising urbanization, growing middle-class income, and the desire for convenience, privacy, and flexible travel patterns have driven the preference for personal vehicle ownership. In 2025, about 36% of the population is estimated to reside in cities, and UN DESA forecasts this share will rise to nearly 50% by 2050. Passenger cars and two-wheelers dominate this segment, catering to daily commuting, leisure, and long-distance travel needs.

The segment is further supported by accessible financing schemes, easy loan approvals, and expanding road infrastructure. Manufacturers are responding with compact, fuel-efficient, and premium models to match evolving consumer expectations. Moreover, personalized features, safety enhancements, and infotainment integration are increasingly influencing purchasing decisions, sustaining the dominance of personal vehicles in India’s automotive market.

Ownership Mode Insights:

- Individual Ownership

- Fleet Ownership

Individual Ownership leads with a share of 74.2% of the total India automotive market in 2025.

The segment’s leadership is reflected in the preference for personal convenience and autonomy. Consumers prioritize the flexibility to travel independently without relying on shared transport or public commuting. Rising income levels, urban mobility demands, and cultural inclination toward personal asset ownership further reinforce this segment’s dominance.

Automotive companies are tailoring offerings for individual buyers, introducing financing options, subscription services, and maintenance packages to enhance ownership experience. The expansion of dealerships, after-sales services, and insurance coverage strengthens customer confidence. Consequently, individual ownership remains a major driver of market sales, particularly for two-wheelers and passenger vehicles, sustaining long-term growth.

Region Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 35.1% share of the total India automotive market in 2025.

West India’s dominance is driven by rapid industrialization, urban population growth, and high consumer purchasing power. Key states such as Maharashtra and Gujarat are major automotive hubs with extensive manufacturing facilities, distribution networks, and strong dealer presence, supporting vehicle sales and market penetration. As such, in August 2025, Suzuki expanded Gujarat’s automotive dominance with a INR 3,200 Crore fourth EV production line, boosting its mega plant. The state, with strong export connectivity, has attracted global automakers, driven investment to INR 29,700 Crore, and fostered job creation and development of the auto ecosystem.

The region benefits from robust infrastructure, including highways, expressways, and logistics networks, facilitating vehicle movement and service access. Likewise, high per-capita income and lifestyle-oriented mobility needs contribute to sustained demand. West India continues to be a critical growth region, shaping market trends, vehicle adoption, and OEM strategic decisions in the Indian automotive market.

.jpeg)

Market Dynamics:

Growth Drivers:

Why is the India Automotive Market Growing?

Growth of Automotive Financing and Subscription Models

Flexible financing options and subscription-based ownership models are reshaping the automotive landscape in India. Consumers increasingly prefer EMI schemes, lease-to-own plans, and short-term vehicle subscriptions to reduce upfront costs and enhance flexibility. For example, in December 2025, Tata Motors launched December EMI schemes for eight models, covering ICE and EVs, with monthly instalments from INR 4,999 (Tiago) to INR 14,555 (Curvv.ev). Offers run until December 31, supporting flexible, long-term financing options. Likewise, banks, NBFCs, and fintech companies are partnering with OEMs to provide tailored financial solutions. These models facilitate vehicle accessibility in tier-2 and tier-3 cities, expand the customer base, and promote the adoption of newer technologies, including electric and connected vehicles, contributing to sustained market expansion.

Rising Demand for Commercial Vehicles and Logistics Expansion

The rapid growth of e-commerce, retail, and logistics sectors is augmenting demand for commercial vehicles, including light and medium-duty trucks, cargo vans, and delivery fleets. Similarly, increasing urbanization, infrastructure development, and last-mile delivery requirements drive fleet expansion. OEMs are introducing fuel-efficient, durable, and technology-enabled commercial vehicles to meet operational efficiency and compliance standards. Furthermore, the growing logistics ecosystem directly supports automotive sales, reinforcing commercial vehicles as a key growth driver in the Indian automotive market. According to IBEF, India’s automobile exports grew 19% in FY25, surpassing 5.3 million units, driven by robust international demand for passenger vehicles, two-wheelers, and commercial vehicles.

Government Policies and Incentives for Vehicle Manufacturing

Supportive government initiatives, such as the Make-in-India campaign, Automotive Mission Plan, and subsidies for electric and hybrid vehicles, are significantly driving market growth. Incentives for domestic production, tax benefits, and reduced import duties encourage OEM investments, local manufacturing, and research and development (R&D). These policies enhance cost competitiveness, foster innovation, and attract foreign players, creating a conducive environment for both passenger and commercial vehicle segments, while simultaneously strengthening India’s position as a regional automotive manufacturing hub.

Market Restraints:

What Challenges the India Automotive Market is Facing?

High Dependence on Fossil Fuels

The India automotive market remains heavily reliant on internal combustion engines, creating vulnerability to fluctuations in crude oil prices and fuel availability. Rising fuel costs directly increase operational expenses for consumers, reducing vehicle affordability and dampening demand. Additionally, heavy reliance on petroleum-based fuels contributes to environmental concerns and regulatory pressures, compelling OEMs to invest in alternative propulsion technologies. Transitioning to sustainable solutions remains gradual due to infrastructure limitations, high costs, and consumer hesitation, constraining market growth.

Infrastructure and Traffic Congestion Challenges

Despite urban expansion, inadequate road infrastructure and traffic congestion in major cities impede efficient vehicle operation and logistics. Poorly maintained roads, limited parking spaces, and lack of organized public transport networks affect vehicle utilization and increase maintenance costs. These issues discourage potential buyers, particularly in urban areas, from investing in larger or premium vehicles. Moreover, infrastructure constraints limit the adoption of electric and connected vehicles, as charging stations and smart mobility frameworks are still in early stages of development.

High Cost of Electric and Advanced Vehicles

Although electric and technologically advanced vehicles are gaining attention, their high upfront costs remain a significant barrier for mass adoption. Limited consumer awareness, insufficient subsidies, and expensive battery technology discourage price-sensitive buyers. Additionally, operating and maintenance costs, coupled with concerns over charging infrastructure and resale value, reduce market penetration. OEMs face challenges in achieving cost efficiency while integrating safety, connectivity, and autonomous features, slowing the transition from conventional vehicles and constraining growth in advanced segments.

Competitive Landscape:

The India automotive market is highly competitive, dominated by leading domestic and international OEMs operating across passenger, two-wheeler, and commercial vehicle segments. Key players are focusing on product diversification, technological innovation, and cost optimization to capture a growing and price-sensitive consumer base. Strategic initiatives include electric vehicle development, connected car solutions, and expansion of dealership and service networks. Collaborations with financial institutions, technology partners, and component suppliers strengthen market presence. Intense competition, coupled with evolving consumer preferences and government policies, drives continuous investment in R&D, marketing, and after-sales services, ensuring dynamic and innovation-driven market growth.

Recent Developments:

- In January 2026, India's automotive industry together with Maruti Suzuki Tata Mahindra and VinFast scheduled to introduce 31 new vehicles in 2026 through their upcoming models which will mainly consist of electric vehicles. The current year will record its highest number of vehicle launches since five years because of increased electric vehicle adoption and growing market demand.

- In June 2025, The Ministry of Heavy Industries launched the SPMEPCI portal which invites international electric vehicle manufacturers to establish operations in India through a minimum investment of ₹4,150 crore while supporting domestic electric vehicle manufacturing and the Make in India initiative and job creation and the Net Zero 2070 objectives.

India Automotive Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Vehicle Types Covered |

Two-Wheeler, Three-Wheeler, Others |

|

Propulsion Types Covered |

Internal Combustion Engine, Hybrid Vehicle, Others |

|

Applications Covered |

Personal, Commercial, Others |

|

Ownership Modes Covered |

Individual Ownership, Fleet Ownership |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Automotive Market Report

The India automotive market size was valued at USD 274.93 Billion in 2025.

The India automotive market is expected to grow at a compound annual growth rate of 8.74% from 2026-2034 to reach USD 584.23 Billion by 2034.

Two-Wheeler dominated the market with 72.6% share in 2025, driven by affordability, fuel efficiency, and widespread adoption in urban, semi-urban, and rural regions.

Key factors driving the India automotive market include rising rural and urban vehicle adoption, demand for electric and premium vehicles, government infrastructure development, technological innovations in drivetrains and safety, and expanding organized dealership networks.

Major challenges in the India automotive market include rising input costs, regulatory compliance pressures, fluctuating fuel prices, limited EV charging infrastructure, intense competition, and changing consumer preferences, which together create hurdles for manufacturers and market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)