India Autonomous Vehicle Market Size, Share, Trends and Forecast by Component, Level of Automation, Application, and Region, 2026-2034

India Autonomous Vehicle Market Summary:

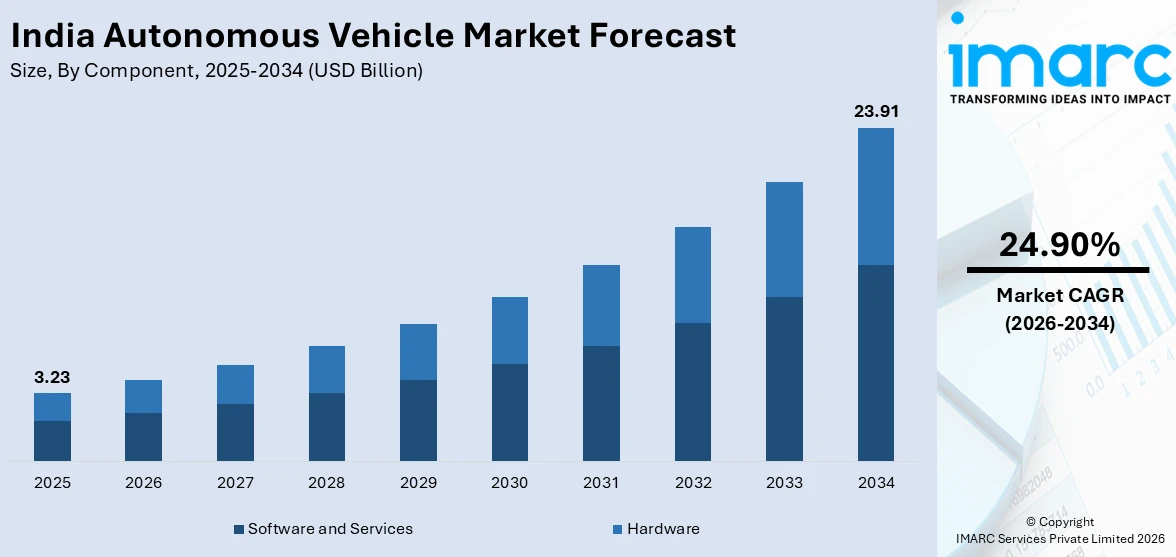

The India autonomous vehicle market size was valued at USD 3.23 Billion in 2025 and is projected to reach USD 23.91 Billion by 2034, growing at a compound annual growth rate of 24.90% from 2026-2034.

The autonomous vehicle market in India is gaining significant momentum as the country enhances its smart mobility ecosystem through forward-thinking policy frameworks, swift digitalization, and increasing technology investments. The growing urbanization, expanding highway systems, and heightened demand for safer travel options are transforming the mobility landscape. The intersection of artificial intelligence (AI), sophisticated sensor technologies, and connected vehicle infrastructure is fostering a conducive environment for autonomous driving functions. Moreover, the increasing focus on minimizing traffic deaths and enhancing logistics efficiency is fostering innovation, establishing India as an upcoming center for autonomous transportation.

Key Takeaways and Insights:

- By Component: Software and services represent the largest segment with a market share of 55% in 2025, establishing themselves as the leading driver of autonomous intelligence and decision-making capabilities in India's rapidly expanding autonomous vehicle ecosystem.

- By Level of Automation: Level 4 leads the market with a share of 45% in 2025, reflecting India's strategic focus on deploying high-automation solutions within controlled operational domains such as industrial campuses, logistics corridors, and smart city environments.

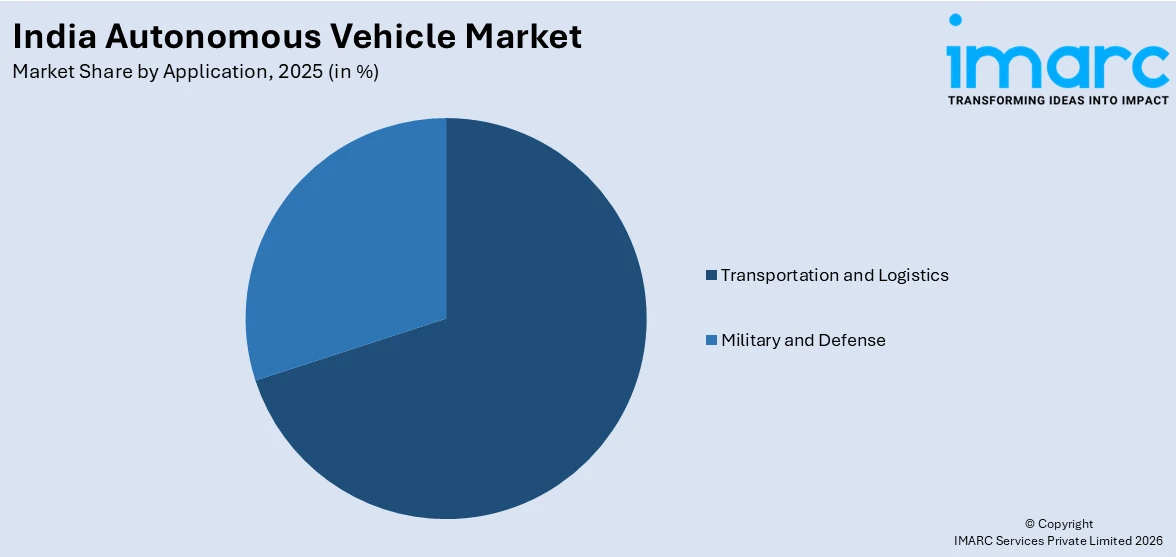

- By Application: Transportation and logistics dominate the market with a share of 70% in 2025, underscoring the sector's rapid adoption of autonomous technologies for freight management, last-mile delivery, and supply chain optimization across India.

- Key Players: The India autonomous vehicle market features a dynamic competitive environment, with established automotive manufacturers, global technology providers, and homegrown startups competing through strategic partnerships, research investments, and innovative product development to capture emerging market opportunities.

To get more information on this market Request Sample

The Indian market for autonomous vehicles is progressing consistently as government-supported smart mobility initiatives, investments from the private sector, and scholarly research increasingly converge to foster the development of autonomous driving. The emphasis on intelligent transport systems, digital infrastructure, and advanced manufacturing is supported by increasing corporate spending on software-defined vehicles, AI, and sensor integration. The increasing adoption of electric vehicles (EVs), the expansion of 5G networks, and the need for safer mobility options are contributing to the supportive environment. Industry platforms are similarly acting as a catalyst for promoting collaboration and the exchange of technology. As an example, the CAEV EXPO 2026, planned at the KTPO Trade Centre in Bengaluru, will bring together automakers, OEMs, tech companies, semiconductor firms, policymakers, and mobility service providers to discuss connected, autonomous, shared, and electric mobility solutions, promoting unified advancement throughout the ecosystem.

India Autonomous Vehicle Market Trends:

Growing Urban Congestion and Demand for Efficient Mobility

Rapid urbanization across India is intensifying transportation challenges, including persistent congestion, extended commute durations, and rising fuel usage. Autonomous vehicle technologies are increasingly regarded as viable solutions to enhance traffic management, minimize human error, and improve route optimization through connected mobility systems. This need is reinforced by demographic trends, as World Bank data indicates that approximately 36.87% of India’s total population resided in urban areas in 2024, reflecting sustained migration toward cities and mounting pressure on existing infrastructure. Fleet-based autonomous mobility in controlled environments can improve asset utilization and reduce idle time, prompting transport authorities and planners to prioritize intelligent mobility systems for passenger and freight movement.

Rising Domestic Innovation

Strengthening in-house design expertise and faster product development cycles among Indian automotive manufacturers are contributing to the advancement of autonomous vehicle technologies. Companies are increasingly investing in dedicated design centers, digital simulation tools, and integrated engineering teams to accelerate concept validation and intellectual property creation. This shift toward rapid prototyping supports quicker commercialization timelines and enhances competitiveness in emerging mobility segments, such as autonomous logistics and compact urban transport. This momentum is reflected in 2025, when Tata Motors patented the fully autonomous Tata YU concept, a compact self-driving vehicle designed to transport both cargo and up to two passengers. Developed in six months at Strate School of Design, Bengaluru, the concept featured hub-mounted electric motors, an automated cargo sorting system for e-commerce, and app-based ride booking for passenger use.

Growing Emphasis on Road Safety and Accident Reduction

India continues to record a significant number of road accidents, largely attributed to human error, fatigue, and distracted driving, strengthening the case for advanced safety technologies. Autonomous and semi-autonomous systems, including advanced driver assistance, collision avoidance, and automated braking, are being positioned as critical tools to enhance road safety outcomes. This priority was reinforced in 2025 at the ETAutoTech Summit in Bengaluru, where industry leaders called for autonomous vehicle technologies to be developed in India for Indian road conditions, with simpler ADAS systems, indigenous R&D, and stronger V2X and V2V integration.

Market Outlook 2026-2034:

The India autonomous vehicle market demonstrates exceptional growth potential throughout the forecast period, underpinned by transformative technological advancements and evolving regulatory frameworks. The market generated a revenue of USD 3.23 Billion in 2025 and is projected to reach a revenue of USD 23.91 Billion by 2034, growing at a compound annual growth rate of 24.90% from 2026-2034. Continued investments in AI research, connected infrastructure development, and strategic partnerships between automotive OEMs and technology providers are expected to accelerate commercialization timelines for higher-level autonomous systems across transportation and defense applications.

India Autonomous Vehicle Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Component | Software and Services | 55% |

| Level of Automation | Level 4 | 45% |

| Application | Transportation and Logistics | 70% |

Component Insights:

- Hardware

- Software and Services

Software and services dominate with a market share of 55% of the total India autonomous vehicle market in 2025.

Software and services lead the market due to their critical role in enabling perception, decision-making, and vehicle control functions. Advanced software platforms integrate AI, ML, sensor fusion, and real-time data analytics to interpret complex road environments and ensure safe navigation. Compared to hardware components, such as sensors and processors, software provides continuous upgrades, customization, and performance optimization through over-the-air updates. Services, including system integration, simulation, mapping, and maintenance further enhance operational efficiency and reliability. This ability to deliver intelligence, adaptability, and lifecycle support positions software and services as the foundational component of autonomous vehicle development in India.

The leadership of software and services is reinforced by India’s strong IT ecosystem, the growing startup landscape, and government initiatives supporting smart mobility and digital infrastructure. Automotive manufacturers increasingly collaborate with technology firms to develop ADAS, high-definition mapping solutions, and cloud-based fleet management platforms. Continuous software improvements enable vehicles to adapt to diverse traffic conditions and regulatory requirements across Indian cities. Additionally, demand for data security, remote diagnostics, and predictive maintenance services further accelerates adoption. By combining innovation, scalability, and technical expertise, software and services drive the evolution of autonomous mobility, sustaining their dominance within the market.

Level of Automation Insights:

- Level 3

- Level 4

- Level 5

Level 4 exhibits a clear dominance with a 45% share of the total India autonomous vehicle market in 2025.

Level 4 holds the biggest market share owing to its ability to deliver high autonomy within defined operational domains while maintaining safety and reliability. Unlike lower levels that require constant human supervision, Level 4 system can independently manage steering, acceleration, braking, and environmental monitoring under specific conditions. This capability makes it suitable for controlled environments, such as urban mobility corridors, logistics hubs, and industrial campuses. Advanced sensor suites, high-definition mapping, and AI algorithms enable precise navigation and obstacle detection. The balance between full autonomy and operational control strengthens Level 4 adoption across pilot projects and commercial deployments.

The leadership of Level 4 is reinforced by increasing investments in smart mobility initiatives, intelligent transport systems, and EV integration across India. Automotive manufacturers and technology companies are prioritizing Level 4 development to address traffic congestion, enhance road safety, and improve fleet efficiency. Regulatory authorities are also exploring controlled testing frameworks that favor semi-structured autonomous deployments before full autonomy becomes mainstream. Additionally, Level 4 reduces driver dependency while retaining operational oversight, making it commercially viable for ride-hailing, last-mile delivery, and public transport pilots. By combining advanced automation, safety assurance, and scalable deployment potential, Level 4 continues to dominate India’s evolving autonomous vehicle landscape.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Transportation and Logistics

- Military and Defense

Transportation and logistics lead with a market share of 70% of the total India autonomous vehicle market in 2025.

Transportation and logistics represent the largest segment driven by the sector’s strong need for operational efficiency, cost reduction, and enhanced safety. Autonomous technologies enable optimized route planning, real-time fleet monitoring, and reduced fuel uage, which are critical for large-scale logistics operations. Compared to passenger mobility segments, transportation and logistics offer structured environments such as highways, ports, and warehouses that facilitate smoother deployment of autonomous systems. The integration of artificial intelligence, advanced sensors, and telematics improves delivery timelines while minimizing human error. This combination of productivity gains, scalability, and reliability positions transportation and logistics as the dominant application segment.

The leadership of transportation and logistics is reinforced by rapid growth in e-commerce, third-party logistics services, and industrial supply chains across India. Companies are increasingly investing in autonomous trucks, last-mile delivery vehicles, and smart warehouse solutions to meet rising demand and manage labor shortages. Government initiatives supporting digital infrastructure, smart highways, and dedicated freight corridors further accelerate adoption. Additionally, predictive maintenance, remote diagnostics, and data-driven fleet optimization services enhance vehicle uptime and operational transparency. By improving efficiency, reducing operational risks, and supporting high-volume movement of goods, autonomous solutions continue to strengthen transportation and logistics as the leading application area.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India plays a significant role in the autonomous vehicle market due to strong government presence, smart city initiatives, and expanding urban mobility projects across Delhi NCR, Chandigarh, and Jaipur. Pilot testing of advanced driver-assistance and autonomous systems is increasing, supported by infrastructure upgrades, research institutions, and growing demand for intelligent transport and logistics solutions.

West and Central India, led by Maharashtra, Gujarat, and Madhya Pradesh, demonstrate strong potential driven by automotive manufacturing hubs and logistics corridors. Mumbai and Pune support innovation through technology partnerships and startup ecosystems, while industrial freight movement across central regions accelerates adoption of autonomous trucks and fleet management solutions.

South India remains a technology-driven hub for autonomous vehicle development, with Bengaluru, Hyderabad, and Chennai leading in research, software engineering, and automotive manufacturing. Strong IT capabilities, electric mobility initiatives, and smart infrastructure projects foster innovation in autonomous systems, making the region a key contributor to India’s intelligent mobility ecosystem.

East India is gradually emerging in the autonomous vehicle market, supported by infrastructure development, port-based logistics, and smart city programs in Kolkata and Bhubaneswar. The growing focus on industrial automation and digital transport solutions encourages pilot deployments, positioning the region for steady advancement in autonomous mobility adoption.

Market Dynamics:

Growth Drivers:

Why is the India Autonomous Vehicle Market Growing?

Expansion of Electric Vehicle Ecosystems

The Indian autonomous vehicle market is significantly propelled by the strategic convergence of electrification and automation, allowing manufacturers to optimize software-defined architectures within simplified mechanical frameworks. Electric drivetrains serve as the ideal foundation for self-driving systems due to their precise digital control and efficient energy management. This synergy is clearly reflected in the domestic landscape, where IBEF data indicates that India’s EV sales reached 1.97 million units in FY25, a 16.9% increase, including over 100,000 electric passenger vehicles. As this electric fleet expands, it provides a robust, data-rich testing ground for Level 2 and Level 3 autonomous features. By aligning electric mobility targets with automated controls, India is rapidly developing a scalable ecosystem that lowers the technical barriers to full-scale autonomous commercialization.

Growth of Logistics, E-commerce, and Last-Mile Delivery

The rapid expansion of e-commerce and organized retail is generating demand for efficient logistics and last-mile delivery solutions. As per the IBEF, India’s e-commerce industry was valued at INR 10,82,875 crore (USD 125 billion) in 2024 and will reach INR 29,88,735 crore (USD 345 billion) by 2030, growing at a CAGR of 15%. This sustained growth is increasing shipment volumes and operational complexity across supply chains. Autonomous vehicle technologies deployed in warehouses, ports, and industrial corridors enhance productivity and reduce costs. Fleet operators are adopting automation to manage driver shortages, improve route predictability, and reduce turnaround times, thereby accelerating pilot deployments across logistics ecosystems nationwide.

Rapid Advancements in AI and Sensor Technologies

Progress in machine learning (ML), computer vision, LiDAR, radar, and edge computing is accelerating the technical feasibility of autonomous vehicles in India. Improvements in object detection, path planning, and real-time decision-making systems are enabling vehicles to operate with greater precision in dense and unpredictable traffic conditions. Cost reductions in sensors and onboard computing hardware are also making advanced driver assistance systems more accessible. Domestic research institutions and automotive engineering firms are strengthening capabilities in embedded systems and automotive software, contributing to localized innovation. This technological maturation is reducing entry barriers and encouraging pilot deployments across commercial and passenger mobility segments.

Market Restraints:

What Challenges the India Autonomous Vehicle Market is Facing?

Inadequate Road Infrastructure and Inconsistent Traffic Management Systems

India's road infrastructure presents fundamental challenges for autonomous vehicle deployment, including limited lane markings, inconsistent signage, unpredictable mixed-traffic patterns, and diverse road surface conditions. Unlike structured driving environments in developed markets, Indian roads feature complex interactions between various vehicle types, pedestrians, animals, and informal road usage that challenge current autonomous perception and decision-making systems.

Fragmented Regulatory Framework and Liability Uncertainties

The absence of a comprehensive unified regulatory framework for autonomous vehicle testing, certification, and commercial deployment across Indian states creates uncertainty for manufacturers and technology developers. Liability assignment in autonomous driving scenarios remains unresolved, while inconsistent state-level policies on testing permits and operational boundaries complicate nationwide scaling strategies for autonomous vehicle companies.

High Technology Costs and Limited User Affordability

The substantial costs associated with autonomous driving hardware, including advanced sensors, processing units, and redundant safety systems present significant affordability barriers in India's price-sensitive automotive market. Research and development (R&D) expenditures for developing autonomous technologies adapted to Indian conditions further escalate costs, limiting near-term accessibility for mass-market user adoption and constraining deployment to premium and commercial segments.

Competitive Landscape:

The India autonomous vehicle market exhibits a dynamic competitive landscape characterized by the convergence of established automotive manufacturers, global technology corporations, and innovative domestic startups. Competition is intensifying as participants pursue differentiated strategies, including full-stack autonomous software development, sensor hardware manufacturing, fleet management platforms, and application-specific deployment solutions. Strategic partnerships between traditional vehicle manufacturers and technology firms are accelerating product development timelines, while dedicated innovation hubs and testing environments are enabling rapid prototyping and validation. The market structure reflects a growing emphasis on India-specific autonomous solutions designed for complex traffic environments, with companies leveraging the nation's deep technology talent pool to develop globally competitive autonomous driving capabilities.

Recent Developments:

- October 2025: India unveiled its first indigenous driverless car, WIRIN, developed through a collaboration between Wipro, Indian Institute of Science, and RV College of Engineering in Bengaluru. Built over six years, the AI-powered vehicle integrates robotics, computer vision, and 5G-based V2X communication to navigate complex Indian road conditions autonomously. The innovation marks a major step toward self-reliant intelligent mobility, with large-scale testing planned before its official rollout.

- September 2025: Omega Seiki Mobility launched Swayamgati, India’s first autonomous electric three-wheeler, marking a major step in driverless mobility for last-mile transport. Equipped with LiDAR, smart sensors, cameras, GPS, and drive-by-wire technology, the vehicle was designed for controlled environments like airports, campuses, and industrial hubs, with a top speed of 12 kmph and a 120 km range.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Hardware, Software and Services |

| Level of Automations Covered | Level 3, Level 4, Level 5 |

| Applications Covered | Transportation and Logistics, Military and Defense |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Autonomous Vehicle Market Report

The India autonomous vehicle market size was valued at USD 3.23 Billion in 2025.

The India autonomous vehicle market is expected to grow at a compound annual growth rate of 24.90% from 2026-2034 to reach USD 23.91 Billion by 2034.

Software and services hold the largest revenue share of 55% in 2025, driven by the growing centrality of AI algorithms, perception software, and cloud-based analytics platforms in enabling autonomous driving capabilities across transportation and defense applications.

Key factors driving the India autonomous vehicle market include strengthening in-house design capabilities and accelerated prototyping by domestic manufacturers, illustrated in 2025 when Tata Motors patented the fully autonomous Tata YU concept, developed within six months in Bengaluru for cargo and passenger mobility applications.

Major challenges include inadequate road infrastructure with inconsistent lane markings and signage, fragmented regulatory frameworks without unified autonomous driving legislation, high technology costs limiting mass-market accessibility, cybersecurity vulnerabilities in connected vehicles, and limited public awareness and consumer trust in autonomous systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade