India Aviation Market Size, Share, Trends and Forecast by Aircraft Type and Region, 2026-2034

India Aviation Market Size, Share, Trends & Forecast (2026-2034)

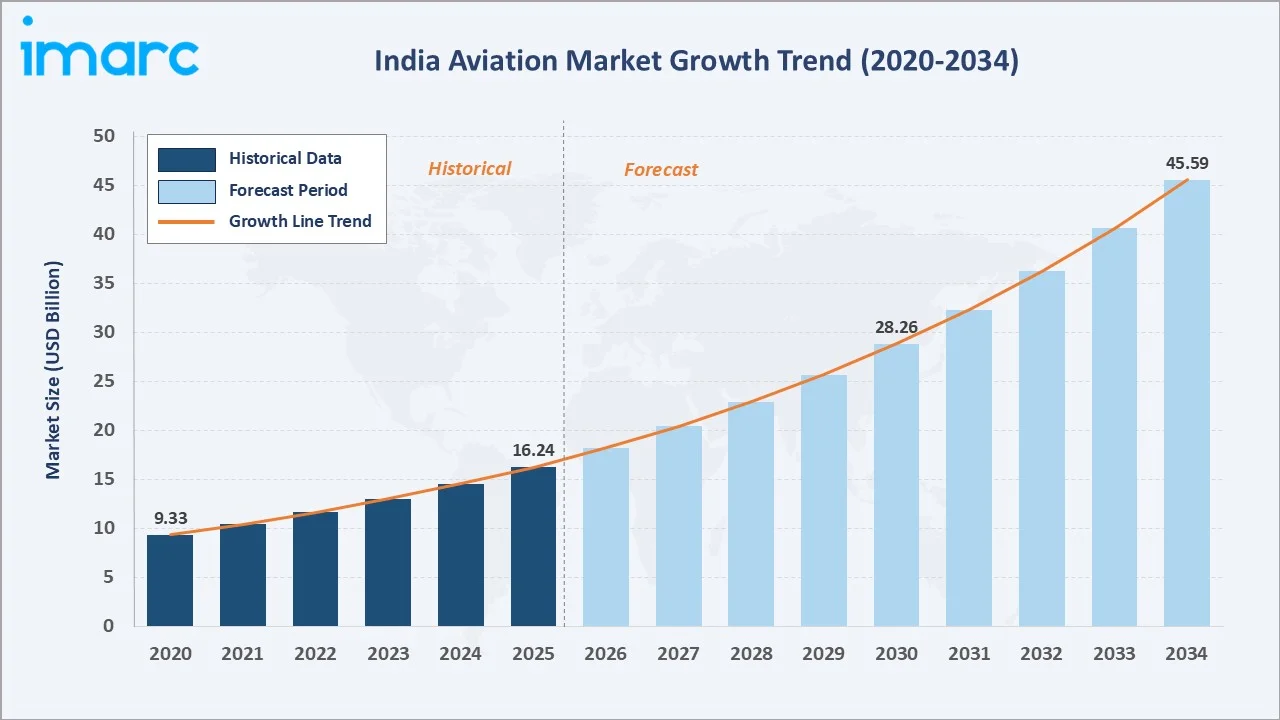

The India aviation market was valued at USD 16.24 Billion in 2025 and is projected to reach USD 45.59 Billion by 2034, expanding at a CAGR of 11.72% during 2026-2034. Growth is anchored by India’s surging aspirational middle class, UDAN regional connectivity scheme with India’s airport network expanded from 74 airports in 2014 to 159 in 2024, government’s Atmanirbhar Bharat defense aviation push, greenfield airport investment under PM Gati Shakti, and India’s journey to become the world’s 3rd-largest aviation market. Commercial aviation leads at 79.4%, military aviation is the fastest growing type, and West India commands 32.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.24 Billion |

|

Forecast Market Size (2034) |

USD 45.59 Billion |

|

CAGR (2026-2034) |

11.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

West India (32.5%, 2025) |

|

Fastest Growing Region |

East India (CAGR ~12.8%, 2026-2034) |

The India aviation market growth expanded from USD 9.33 Billion in 2020 due to COVID-19 travel restrictions before recovering sharply to USD 16.24 Billion in 2025. Anchored at USD 28.26 Billion in 2030, the forecast to USD 45.59 Billion by 2034, validating India’s trajectory as the world’s fastest-growing major aviation economy. India’s 164-170 million domestic passengers confirm structural demand recovery.

To get more information on this market, Request Sample

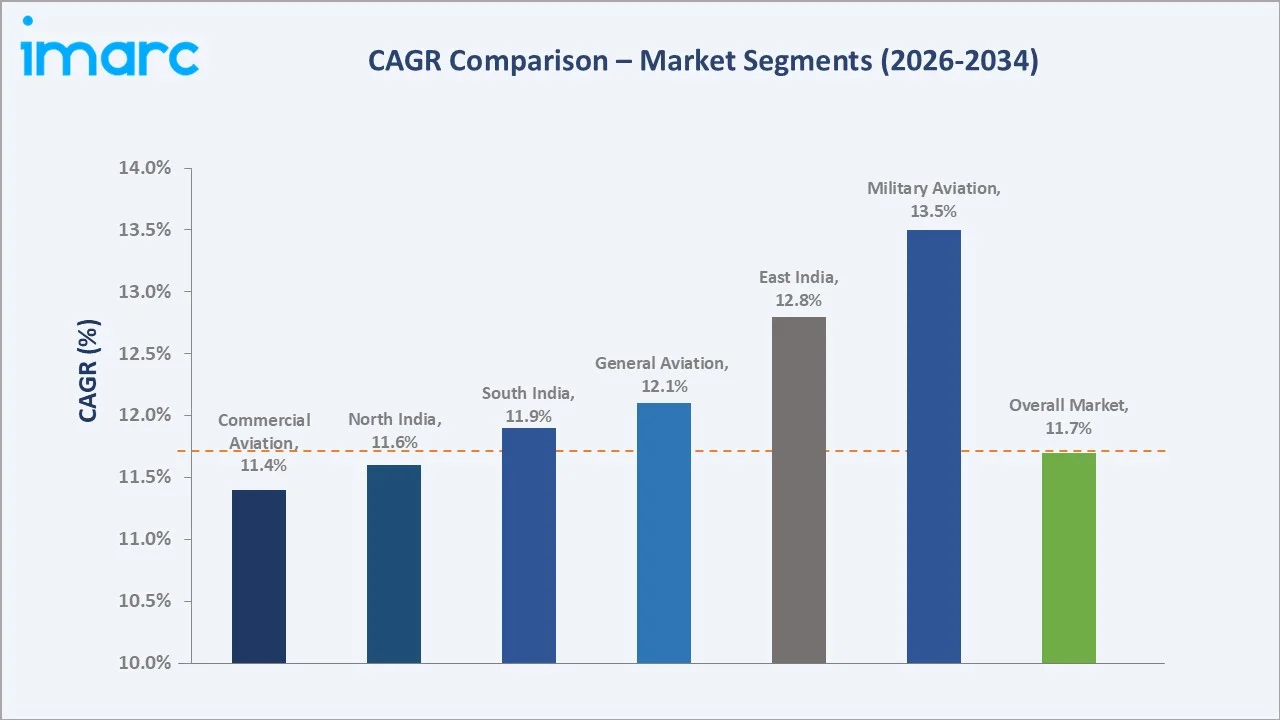

The CAGR across key segments with military aviation at ~13.5% CAGR grows fastest, driven by the September 2025 Ministry of Defence contract with HAL for 97 Tejas Mark-1A combat aircraft valued at INR over ₹62,370 crore, and the Atmanirbhar Bharat defense indigenization mandate targeting domestic procurement. East India at ~12.8% CAGR leads regional growth, reflecting new international connectivity from Kolkata and the North East India greenfield airport pipeline under PM Gati Shakti.

Executive Summary

The India aviation market recovered from USD 9.33 Billion in 2020, to USD 16.24 Billion in 2025, driven by post-pandemic domestic travel explosion, Air India’s historic re-privatization to the Tata Group, Akasa Air’s high-growth market entry, and India’s aviation infrastructure investment entering its most intensive phase. India’s domestic aviation market is structurally unique in global aviation. This structural underpenetration, combined with India’s rising disposable income, expanding airline network coverage, and new airport capacity unlocking previously inaccessible catchments, positions India as the world’s fastest-growing major aviation market through 2034.

Commercial aviation leads at 79.4% encompassing airline ticket revenue, airport charges, cargo revenue, and aviation ancillary services. West India’s 32.5% reflects Mumbai’s primacy as India’s international aviation gateway, with Navi Mumbai International Airport’s 2026 commissioning set to fundamentally rebalance India’s aviation geography.

Key Market Insights

|

Insight |

Data |

|

Dominant Aircraft Type |

Commercial Aviation – 79.4% revenue share (2025) |

|

Dominant Region |

West India – 32.5% revenue share (2025) |

|

Fastest Growing Region |

East India (CAGR ~12.8%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Commercial aviation at 79.4% (2025) is structurally dominant because India’s low-cost carrier model, pioneered by IndiGo’s no-frills high-frequency approach, democratized air travel to price points approaching premium train fares for routes above 500 km, catalyzing a inflation-adjusted decline in domestic airfares.

- West India at 32.5% anchored by Mumbai’s irreplaceable aviation role: Mumbai Chhatrapati Shivaji Maharaj International Airport (CSMIA) 48.88 lakh (4.888 million) people travelled in November 2025, creating chronic congestion that Navi Mumbai International Airport (NMIA) must relieve.

- East India at 17.5% as India’s highest-potential development aviation region: Northeast India’s 45 million population has among India’s lowest aviation penetration rates, representing India’s largest unserved aviation demand pool.

India Aviation Market Overview

India’s aviation market encompasses commercial aviation, military aviation, and general aviation. The ecosystem integrates global aircraft OEMs with India’s domestic aviation sector’s unique characteristics: 1.4 billion population’s first-time flier transition, government’s UDAN regional connectivity mandate, Tata Group’s airline consolidation strategy, and India’s Atmanirbhar Bharat defense indigenization reshaping military aviation procurement.

India’s aviation infrastructure investment represents the world’s largest aviation greenfield program: Navi Mumbai International Airport, Jewar Noida International Airport, Bhogapuram International Airport, Hosur Airport, and UDAN airports under AAI construction, collectively raising the demand in India’s current aviation infrastructure pipeline. This investment pipeline, combined with airline fleet expansion and India’s defense aviation modernization, creates India aviation’s unmatched structural growth case.

Market Dynamics

To evaluate market opportunities, Request Sample

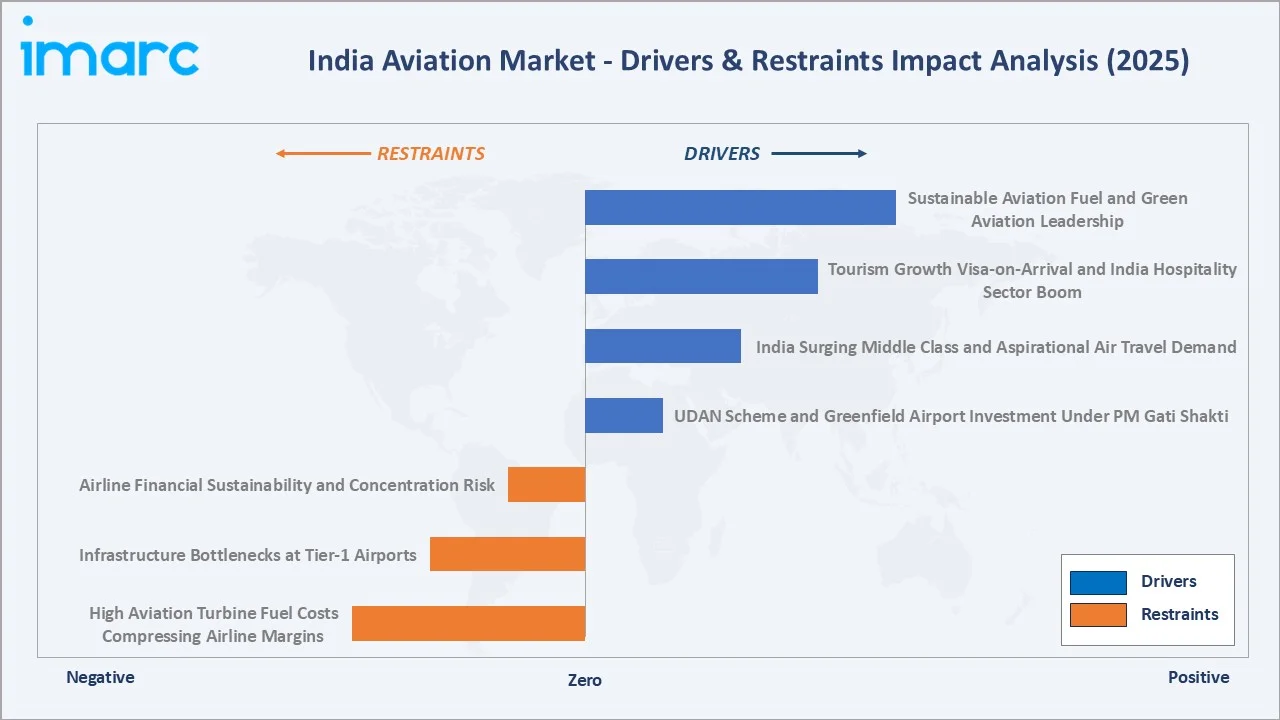

Market Drivers

- UDAN Scheme and Greenfield Airport Investment Under PM Gati Shakti: India’s UDAN Regional Connectivity Scheme, launched in October 2016, connecting 90 airports, 625 UDAN routes, with more than 1.49 crore passengers have benefited from affordable regional air travel.

- India’s Surging Middle Class and Aspirational Air Travel Demand: By 2030, India will add about 75 million middle-class households, with air travel’s sweet spot, representing additional Indians entering air-travel-capable income levels by 2030.

- Tourism Growth, Visa-on-Arrival, and India’s Hospitality Sector Boom: India recorded approximately 56 lakh Foreign Tourist Arrivals, and 303.59 crore Domestic Tourist Visits till August 2025, making tourism the fastest-growing demand segment for Indian carriers.

Market Restraints

- High Aviation Turbine Fuel Costs Compressing Airline Margins: ATF (Aviation Turbine Fuel) represents 35‐45% of Indian airline operating costs, the single largest cost component. India’s state-level ATF pricing system creates artificial cost disparities for airlines operating the same routes in different states.

- Infrastructure Bottlenecks at Tier-1 Airports: India’s top-3 airports, Delhi IGIA, Mumbai CSMIA, and Bengaluru KIA, are all operating at or above declared capacity, creating slot shortages that prevent new route additions and constrain airline growth.

Market Opportunities

- Sustainable Aviation Fuel (SAF) and Green Aviation Leadership: India’s government-mandatory blending of Compressed Bio-Gas in CNG (Transport) & PNG (Domestic) segments of the CGD Sector creates India’s domestic SAF production market opportunity.

- Urban Air Mobility (UAM) and eVTOL Opportunity: India’s cities with population growth and chronic road congestion represent Asia’s most compelling urban air mobility market. Mumbai–Pune–Nashik and Delhi–NCR corridors with a combined high population and inadequate surface transport create the world’s largest potential urban air mobility addressable market outside the US and China.

Market Challenges

- India’s Airport-Airline Bilateral Revenue Share Conflict: India’s Airports Economic Regulatory Authority (AERA)’s aeronautical tariff determination methodology, determining airport charges on a regulated asset base, is contested by Indian airlines, who argue that GMR’s Delhi airport and Mumbai CSMIA’s landing and navigation charges are among the world’s highest relative to traffic volume.

- Airline Financial Sustainability and Concentration Risk: India’s aviation market exhibits extreme fragility, demonstrating that India’s aviation market revenue base cannot sustain financially healthy competing airlines simultaneously at current fuel costs and fare structures.

Emerging Market Trends

1. Air India’s Tata Group Transformation as India’s Full-Service Global Carrier

Air India’s Vihaan.AI transformation program under CEO Campbell Wilson is the most ambitious airline turnaround in Asia’s aviation history. Air India’s merger integration of Air Asia India and Air India Express creates the Tata Aviation Group’s multi-brand strategy, collectively targeting India’s international PAX market and domestic seat share.

2. IndiGo’s 1,000-Aircraft Order and India’s 10th-Year Fleet Transformation

IndiGo’s 2023 announcement of 500 additional Airbus A320 family aircraft, creating a 1,000-aircraft firm order from a single airline for the first time in aviation history, represents a structural commitment to India’s aviation growth trajectory that dwarfs comparable commitments.

3. HAL’s Tejas Mk1A and India’s Military Aviation Industrial Revolution

HAL’s Tejas Light Combat Aircraft (LCA) Mk1A program, 83 aircraft at INR 48,000 crore, the largest domestic Indian defense aviation contract in history, represents India’s definitive transition from import-dependent to domestically manufactured combat aircraft.

4. DigiYatra and India’s Digital Aviation Identity Revolution

DigiYatra, India’s biometric-enabled seamless airport journey platform implemented by the DigiYatra Foundation, is making India’s aviation ecosystem the world’s largest-scale implementation of paperless biometric travel.

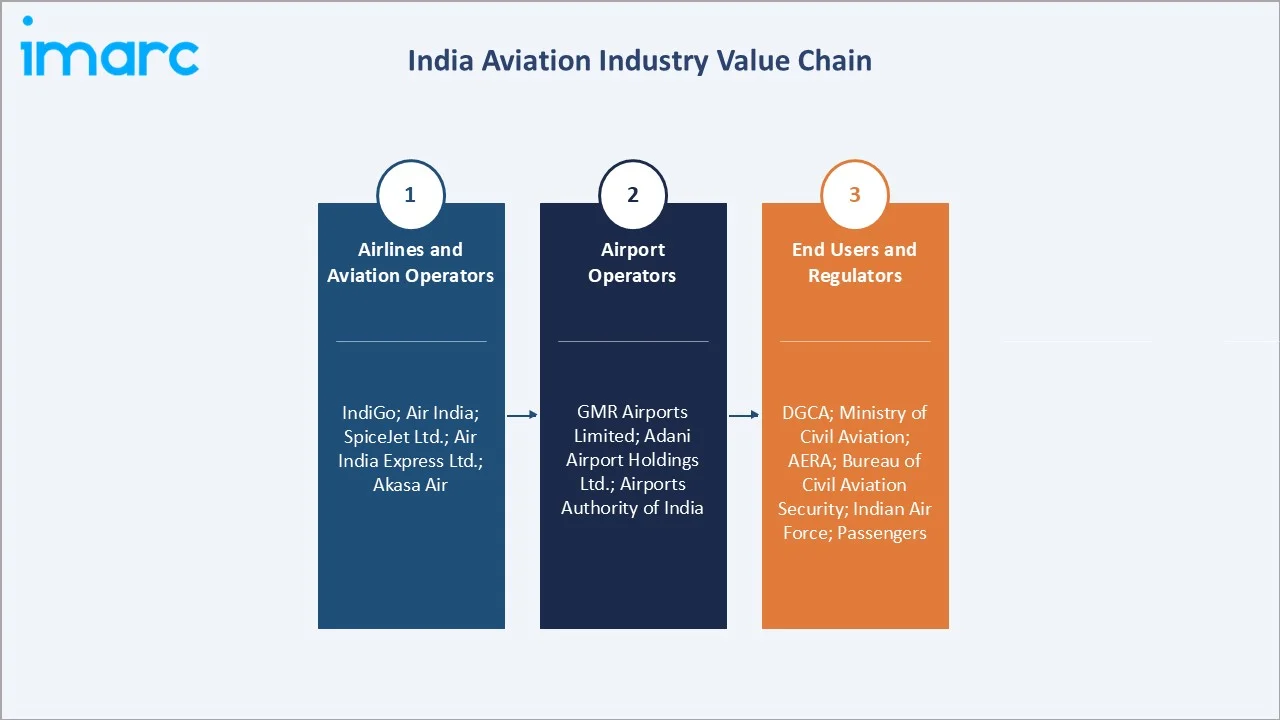

Industry Value Chain Analysis

India’s aviation value chain integrates global aircraft OEMs, domestic manufacturing, airline operations, airport management, MRO services, and end-user travel under regulatory oversight from DGCA, MoCA, AAI, AERA, and BCAS.

|

Stage |

Key Participants |

|

Airlines & Aviation Operators |

IndiGo; Air India; SpiceJet Ltd.; Air India Express Ltd., Akasa Air |

|

Airport Operators |

GMR Airports Limited; Adani Airport Holdings Ltd.; Airports Authority of India |

|

End Users & Regulators |

Directorate General of Civil Aviation; Ministry of Civil Aviation; Airports Economic Regulatory Authority; Bureau of Civil Aviation Security; Indian Air Force; Indian Navy; Passengers |

Airlines capture 45‐55% of total aviation value chain revenue through ticket sales, cargo charges, and ancillary services. Airport operators generate 20‐25% through aeronautical and non-aeronautical revenue.

Technology Landscape in the India Aviation Industry

Next-Generation Narrowbody Aircraft Transforming India’s Fleet

IndiGo and Akasa Air’s new-generation Airbus A320neo family are transforming India’s airline economics at a critical time when ATF costs are the primary P&L lever. Air India’s A350-900 and A321XLR represent India’s next-generation long-haul connectivity that will open new India–Europe and India–Americas non-stop route markets previously economically impossible with widebody jets’ high fixed costs.

Advanced Air Traffic Management and GNSS-Based Approach Systems

AAI’s GAGAN (GPS Aided GEO Augmented Navigation) enhances GPS accuracy, availability, and reliability, enabling its use across all flight phases, including approaches at qualified airports. It also improves position reporting for more efficient air traffic management. Beyond aviation, GAGAN supports better navigation across maritime, road, and rail transport systems.

HAL’s Tejas AESA Radar and Electronic Warfare Systems

LCA Tejas is a 4.5-generation, all-weather, multi-role fighter aircraft, with the Mk1A variant representing its most advanced configuration. It features advanced systems such as AESA radar, an electronic warfare suite with radar warning and self-protection jamming, a digital map generator, smart multi-function displays, a combined interrogator and transponder, and an advanced radio altimeter, among other enhancements.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Aircraft Type | Commercial Aviation | 79.4% | 2025 |

| Region | West India | 32.5% | 2025 |

By Aircraft Type

Commercial aviation leads at 79.4%, encompassing scheduled domestic airlines, scheduled international airlines, charter services, and air cargo. India’s domestic scheduled airline market growth is the segment where India’s aviation growth story plays out most dramatically, with airline profitability recovering from COVID losses as new aircraft economics lower CASK and rising demand volume provides yield leverage.

To access detailed market analysis, Request Sample

Military aviation at 13.8% encompasses HAL production revenue, IAF aircraft import, IN aviation, and Army aviation. General aviation at 6.8% covers business jet operations, helicopter services, flight training organizations, and drone/UAV operations.

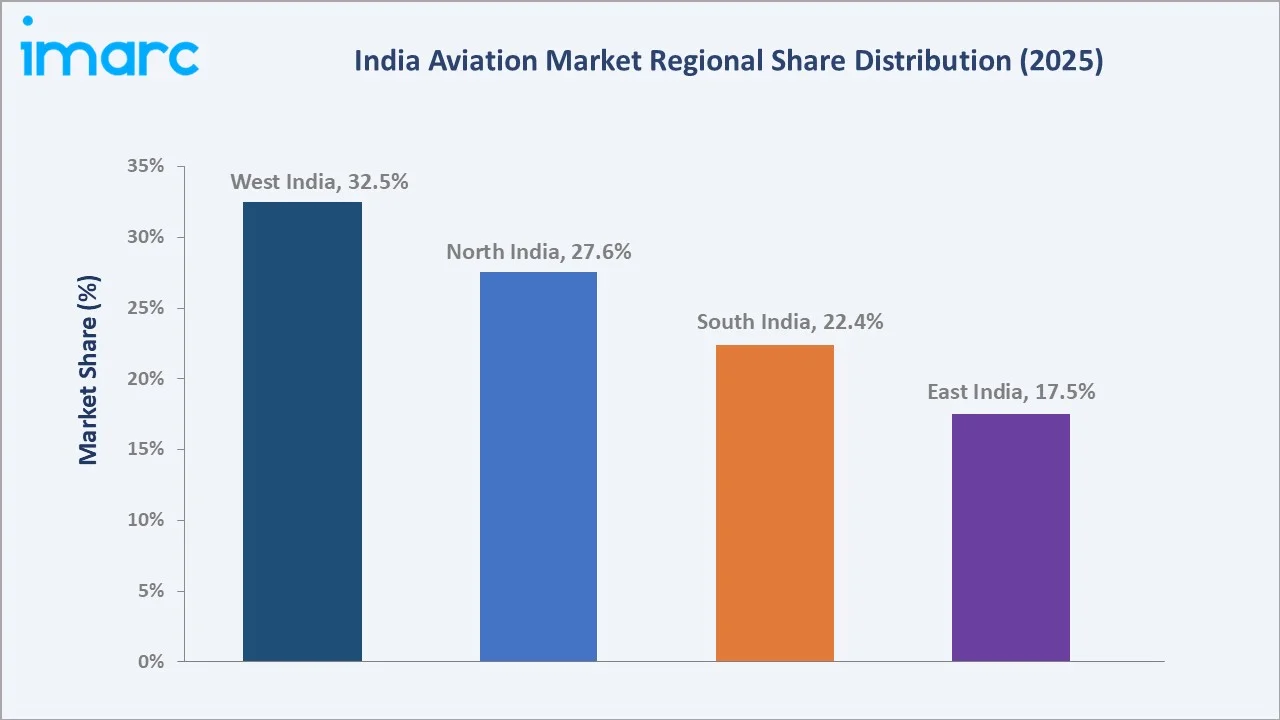

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

32.5% |

Mumbai’s Chhatrapati Shivaji Maharaj International Airport (CSMIA) –one of the India’s busiest airport by international passengers and India’s primary financial hub, generating the highest-value business travel demand nationally |

|

North India |

27.6% |

Indira Gandhi International Airport (IGIA) – India’s busiest airport by total PAX and India’s premier aviation hub, operated by GMR Airports’ DIAL (Delhi International Airport Ltd.) under a 30-year concession |

|

South India |

22.4% |

Bengaluru’s Kempegowda International Airport (KIA) – India’s 3rd-busiest airport operated by BIAL; BIAL Terminal 2 positioning Bengaluru as South India’s premier aviation hub |

|

East India |

17.5% |

Kolkata’s Netaji Subhas Chandra Bose International Airport (NSCBIA) – India’s 6th-busiest airport, AAI-managed, handling Northeast India’s gateway traffic |

West India’s 32.5% dominance reflects Mumbai’s structural aviation primacy, India’s financial capital and top international gateway, which handles high international passengers. Mumbai Airport recorded a peak passenger traffic of 55.5 million in 2025, comprising 39.2 million domestic travelers and 16.3 million international passengers.

South India’s 22.4% reflects IT capital to accommodate corporate aviation demand without the congestion that previously drove business travelers to Mumbai-based alternatives; South India’s Gulf corridor represents India’s densest bilateral aviation market. East India’s 17.5% is India's aviation’s most strategically critical underserved region.

Competitive Landscape

India’s aviation market exhibits high concentration in commercial aviation, moderate concentration in airports, and a monopolistic structure in military aviation.

|

Company Name |

Product / Service Line |

Market Position |

Core Strength |

|

IndiGo |

6E Prime, IndiGo CarGo, IndiGo Stretch |

Market Leader |

Gurugram-headquartered IndiGo achieved and held India’s dominant domestic aviation position with the highest market concentration by a single airline in any large-country aviation market globally. |

|

Air India Ltd. |

A319, A320, A320neo, A321, A321neo, B787-8, B787-9, B777-200LR, B777-300ER, A350-900 |

Market Leader |

Delhi-headquartered Air India is executing India’s most ambitious airline transformation With the recent record-breaking order of 570 new aircraft renews. |

|

Hindustan Aeronautics Limited (HAL) |

LCA Tejas, HTT-40, DORNIER, SU-30 MKI, HAWK, Dhruv ALH, Hindustan -228 |

Market Leader |

Bengaluru-headquartered Hindustan Aeronautics Limited is India’s sovereign aerospace and defense company, central to the Government of India’s Atmanirbhar Bharat (self-reliance) defense aviation mission. |

|

GMR Aviation Pvt Ltd |

Falcon 2000 LX, Embraer Legacy 600 |

Strong Challenger |

Premium private jet charter services for corporate and VIP clients. |

This market structure, commercial aviation’s duopolistic trajectory, airports’ regulated privatization, and military aviation’s strategic public sector anchor – is unique among major aviation markets globally.

Key Company Profiles

IndiGo

IndiGo is India’s undisputed commercial aviation market leader with a high domestic seat share and a 430+ aircraft operational fleet that makes IndiGo the world’s 7th-largest airline by daily departures.

- Portfolio: 6E Prime, IndiGo CarGo, IndiGo Stretch.

- Recent Developments: In April 2025, IndiGo enhanced its premium offering by expanding IndiGoStretch, its tailor-made business product, to the Delhi–Hyderabad route, ensuring a more relaxed and comfortable journey. IndiGo currently offers IndiGoStretch on all flights between Delhi–Mumbai and Delhi–Bengaluru.

- Strategic Focus: Fleet expansion through Airbus delivery acceleration enabling network growth; IndiGo Stretch business class commercialization targeting revenue uplift on premium-demand routes.

Air India Ltd.

Air India is executing India's aviation’s most ambitious transformation under CEO Campbell Wilson’s Vihaan.AI program.

- Portfolio: A319, A320, A320neo, A321, A321neo, B787-8, B787-9, B777-200LR, B777-300ER, A350-900.

- Recent Developments: In October 2025, Air India launched India’s first non-stop flight to the Philippines. The inaugural flight to Manila, Philippines, departed from Delhi’s Indira Gandhi International Airport.

- Strategic Focus: International route network expansion through new A350 long-haul operations; Customer experience transformation; Star Alliance membership enabling global frequent flyer loyalty partnership driving premium traveler share.

Hindustan Aeronautics Limited (HAL)

HAL is India’s only sovereign aerospace manufacturing company and the central pillar of India’s Atmanirbhar Bharat defense aviation program.

- Product Portfolio: LCA Tejas, HTT-40, DORNIER, SU-30 MKI, HAWK, Dhruv ALH, Hindustan -228.

- Recent Developments: In December 2025, Hindustan Aeronautics Limited (HAL) completed the maiden flight of the Dhruv–New Generation (NG) in Bengaluru, signaling its strategic entry into civil and export-focused helicopter markets.

- Strategic Focus: LUH serial production scaling to helicopters establishing HAL’s utility helicopter market position; Civil aircraft MRO expansion to capture India’s airline MRO revenue through HAL’s OBSC.

Market Concentration Analysis

India’s commercial aviation market exhibits very high concentration: IndiGo’s combined domestic commercial aviation concentration creates an effective duopoly. Airport infrastructure has similarly consolidated into a triopoly: GMR, Adani, and AAI (130 airports) handling 95%+ of India’s passenger traffic.

Military aviation concentration is even higher: HAL holds a structural monopoly as India’s sole domestically-manufacturing aerospace company for combat aircraft and helicopters, as a defense electronics sub-system suppliers rather than prime contractors. This public sector dominance while strategically intentional under Atmanirbhar Bharat, creates procurement bottlenecks when HAL’s production capacity cannot meet IAF’s operational readiness requirements.

Investment & Growth Opportunities

Fastest Growing Segments

Military aviation (~13.5% CAGR), East India region (~12.8% CAGR), MRO services (~15‐18% CAGR), eVTOL/urban air mobility (~25‐30% CAGR from very small 2025 base), and air cargo (~18‐22% CAGR from e-commerce expansion) represent India aviation’s highest-growth investment vectors.

Emerging Sector Opportunities

Drone delivery and logistics; drone-based precision agriculture; urban air mobility; defence space and satellite launch aviation.

Investment Themes

India’s aviation investment opportunity spans airline equity, airport infrastructure, MRO, and defense aviation.

- Listed equity investment opportunities: IndiGo, HAL, GMR Airports Infrastructure, Airports Authority of India, Blue Dart Aviation, Adani Enterprises.

- Infrastructure investment: NMIA Navi Mumbai (Adani private infrastructure, USD-denominated infrastructure bond eligibility); Jewar Noida Airport (YEIDA government tenancy + Zurich Airport International concession); Bhogapuram Airport GMR; various UDAN airport PPP models under AAI/MoCA VGF framework.

Future Market Outlook (2026-2034)

The India aviation market is approaching its most transformative and commercially significant decade. From USD 16.24 Billion in 2025, the market will reach USD 45.59 Billion by 2034, at an 11.72% CAGR that makes India the world’s fastest-growing major aviation market by revenue. This growth trajectory is justified by three structural realities unique to India among the world’s major aviation markets.

First, India’s aviation underpenetration is the deepest among billion-population nations: with only 3–5% of India’s 1.4 billion population flying today, India’s addressable market expansion as rising incomes, UDAN accessibility, and competitive fares bring new Indians into air travel, is structurally guaranteed by demographics and economics rather than cyclical demand. Second, India’s aviation infrastructure buildout, the world’s largest aviation greenfield program, is adding PAX capacity through 2030 from Navi Mumbai International Airport, Jewar Noida, Bhogapuram, Purandar Pune, and UDAN airports, creating the physical supply-side capacity for India’s demand growth. Third, India’s military aviation modernization creates a defense aviation demand floor that is independent of commercial aviation’s cyclical dynamics, providing market stability through periods of airline industry turbulence.

Research Methodology

Primary Research

Primary research included structured interviews with 120+ industry stakeholders in 2025, comprising airline commercial directors, airport operators, DGCA airworthiness and air transport officers, HAL business development and programme management executives, MoCA aviation policy officers, IATA India country director, and independent aviation industry analysts.

Secondary Research

Secondary research encompassed DGCA Monthly Traffic Reports, MoCA Annual Reports, Airports Authority of India Traffic Statistics, IATA World Air Transport Statistics 2024, IATA India Country Forecast, Annual Reports, GMR Airports Infrastructure Annual Reports, Adani Enterprises Quarterly Reports, Ministry of Defence Annual Reports, Cabinet Secretariat CCS Defence Procurement disclosures, and IMARC aerospace and aviation industry databases. Over 140 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up aircraft type × region disaggregated model validated against top-down India GDP and air travel propensity models. Key inputs include DGCA domestic PAX growth trajectory, IAF capital acquisition budget, India GDP per capita forecasts, UDAN route activation timeline, new airport capacity addition schedule, airline fleet delivery programmes, and IATA India air travel forecast.

India Aviation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Aircraft Types Covered | Commercial Aviation, General Aviation, Military Aviation |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | IndiGo, Air India Ltd., Hindustan Aeronautics Limited (HAL), GMR Aviation Pvt Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Aviation Market Report

The India aviation market was valued at USD 16.24 Billion in 2025 and is projected to reach USD 45.59 Billion by 2034.

The India aviation market is forecast to grow at a CAGR of 11.72% during 2026-2034, driven by UDAN regional connectivity, India’s middle-class air travel demand, defense aviation self-reliance, and greenfield airport infrastructure investment.

Commercial aviation leads with 79.4% revenue share (2025), with IndiGo’s high domestic seat share and Air India’s international route network driving commercial aviation’s market primacy.

West India leads with 32.5% revenue share (2025), driven by Mumbai CSMIA’s PAX as India’s primary international gateway and the upcoming Navi Mumbai International Airport adding PAX capacity.

Key companies include IndiGo, Air India Ltd., Hindustan Aeronautics Limited (HAL), GMR Aviation Pvt Ltd., and others.

Key drivers include UDAN regional connectivity scheme activating airports, India’s surging aspirational middle class, HAL’s Tejas Mk1A military aviation self-reliance program (INR 48,000 crore), greenfield airport investment, and India’s tourism growth.

Key trends include Air India’s Tata Vihaan.AI transformation, greenfield airport revolution, IndiGo’s 1,000-aircraft order and A321XLR Europe route launch, HAL Tejas production ramp, DigiYatra biometric airport expansion, and India as Asia’s emerging MRO hub under MoCA India MRO Strategy.

Key challenges include high ATF costs, infrastructure bottlenecks at Delhi, Mumbai, and Bengaluru airports, skilled pilot and AME shortage, airline-airport bilateral revenue conflicts, and airline financial sustainability.

Top opportunities include India MRO hub development, Navi Mumbai International Airport and Jewar Noida Airport infrastructure investment, HAL Tejas supply chain MSME investment, Akasa Air growth capital, eVTOL urban air mobility, drone logistics (agricultural + last-mile delivery), and defence FDI in GE-HAL F414 engine JV and Tata Advanced Systems aerospace manufacturing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)