India Baby Diapers Market Size, Share, Trends and Forecast by Product Type, Sales Channel, and Region, 2026-2034

India Baby Diapers Market Size, Share, Trends & Forecast (2026-2034)

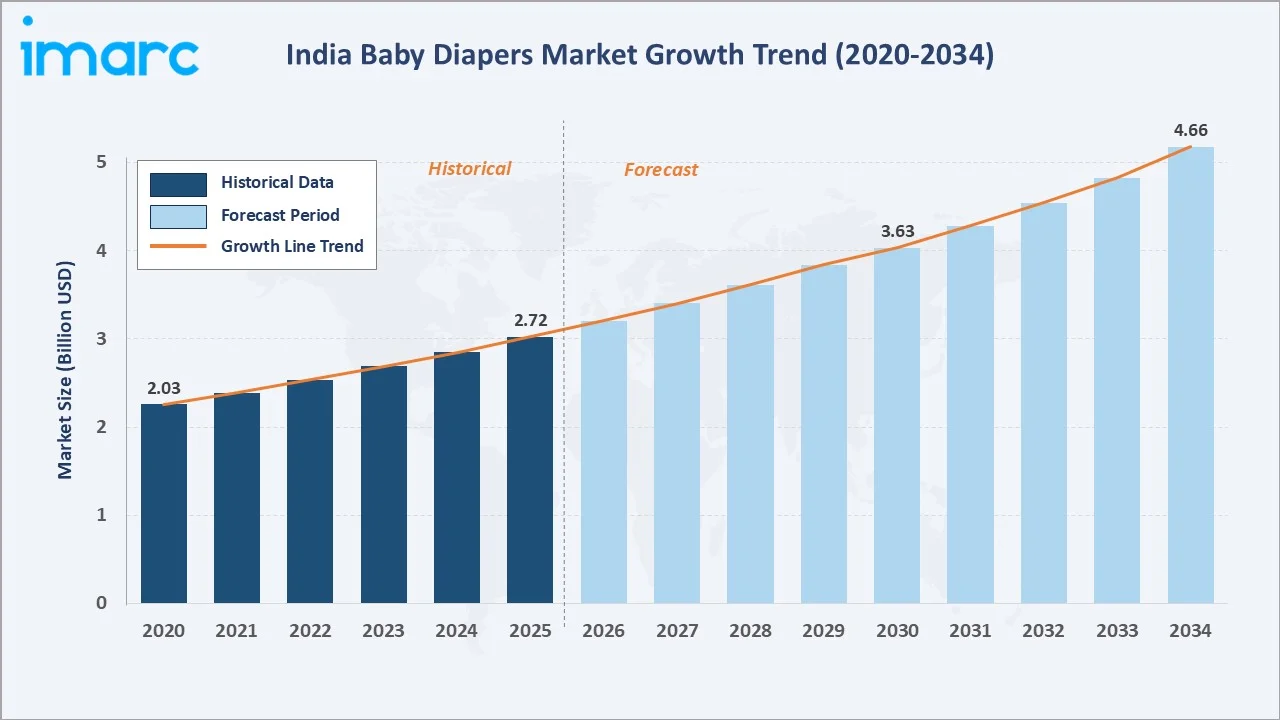

The India baby diapers market reached USD 2.72 Billion in 2025 and is projected to reach USD 4.66 Billion by 2034, growing at a CAGR of 5.99% during 2026-2034. The market is driven by rising birth rates, growing hygiene awareness, increasing disposable incomes, and expanding urban working-parent households. India's birth rate of 16.75 births per 1,000 people in 2024, up 3.74% from 2023, supports a larger infant population and increases the number of babies requiring diaper products. Disposable leads product type at 91.6%. Supermarkets/hypermarkets lead the sales channel at 32.8%. North India leads at 31.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.72 Billion |

|

Forecast Market Size (2034) |

USD 4.66 Billion |

|

CAGR (2026-2034) |

5.99% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Disposable (91.6%, 2025) |

|

Dominant Sales Channel |

Supermarkets/Hypermarkets (32.8%, 2025) |

|

Leading Region |

North India (31.4%, 2025) |

India baby diapers market is showing steady growth, rising from USD 2.03 Billion in 2020 to USD 2.72 Billion in 2025. The market is projected to reach USD 4.66 Billion by 2034, supported by rising hygiene awareness, urbanization, and increasing adoption of disposable baby care products. The USD 3.63 Billion market size in 2030 reflects stronger penetration across both urban and semi-urban households.

To get more information on this market, Request Sample

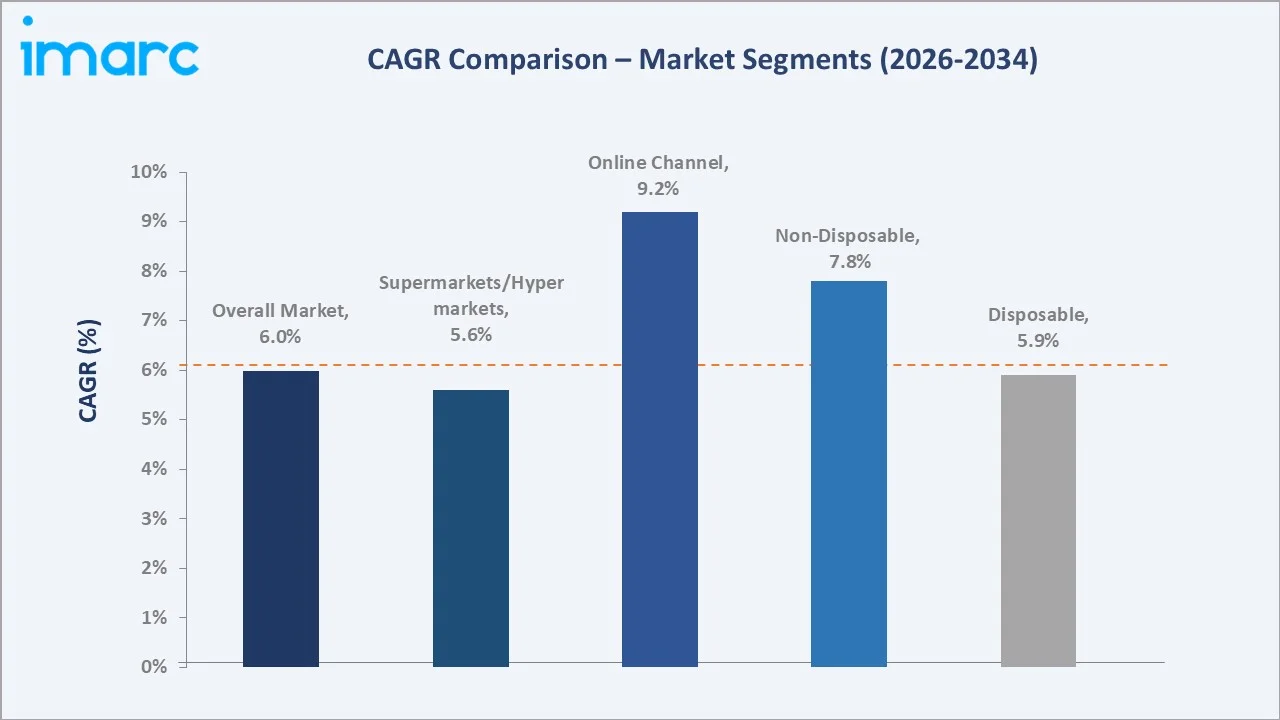

Non-disposable grows fastest at ~7.8% CAGR through D2C cloth and reusable diaper, eco-conscious urban millennial parent adoption. Online channel grows at ~9.2% CAGR through Amazon India, FirstCry, and Meesho subscriptions.

Executive Summary

The India baby diapers market is expanding steadily, driven by rising hygiene awareness, urbanization, and growing adoption of disposable baby care products. The market grew from USD 2.03 Billion in 2020 to USD 2.72 Billion in 2025 and is forecast to reach USD 4.66 Billion by 2034. Rising birth rates, increasing disposable incomes, and working-parent households are supporting demand. E-commerce expansion and wider retail availability are improving product access across urban and semi-urban areas. Premium, skin-friendly, and eco-conscious diapers are expected to shape future growth.

Disposable at 91.6% dominates through Pampers, Huggies, and MamyPoko urban volume. Supermarkets/hypermarkets at 32.8% lead through DMart, Reliance Smart, and Big Bazaar mainstream shelf. North India leads at 31.4% through high birth volume and Delhi NCR premium demand.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Disposable - 91.6% share (2025) |

|

Dominant Sales Channel |

Supermarkets/Hypermarkets - 32.8% market share (2025) |

|

Leading Region |

North India - 31.4% share (2025) |

|

Market Opportunity |

Tier-2 and Tier-3 city disposable penetration; biodegradable bamboo diaper; D2C subscription model; hospital channel newborn diaper |

Key Analytical Observations Supporting The Above Data:

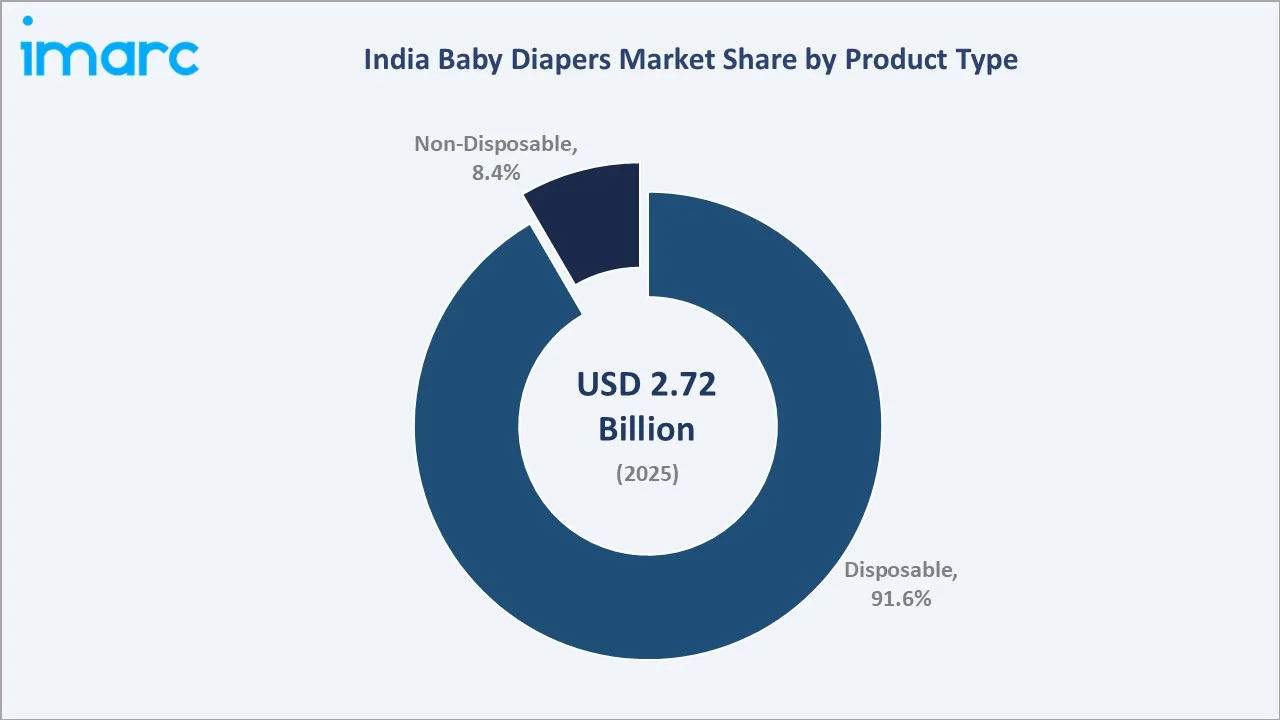

- Disposable at 91.6%: The disposable segment dominates due to its convenience, high absorbency, hygiene benefits, and easy availability across retail and online channels. Rising preference among urban and working parents for ready-to-use baby care products further supports demand.

- Supermarkets/Hypermarkets at 32.8%: Supermarkets and hypermarkets dominate due to wide product availability, brand visibility, bulk-buying options, and consumer trust in organized retail. Parents also prefer these stores for comparing brands, sizes, prices, and promotional offers before purchase.

- North India at 31.4%: North India dominates regionally due to its large child population, rising urbanization, and growing adoption of disposable hygiene products. Higher retail penetration, expanding e-commerce access, and increasing working-parent households further support regional demand.

India Baby Diapers Market Overview

India baby diapers market operates within the broader India baby care market as the highest purchase frequency baby care product. The market is commercially unique due to its combination of high-volume essential demand, recurring purchases, and strong brand loyalty among parents. Growth is supported by hygiene awareness, convenience needs, and premiumization toward softer, skin-friendly, and high-absorbency products. The market also benefits from expanding retail and e-commerce access across urban and semi-urban households.

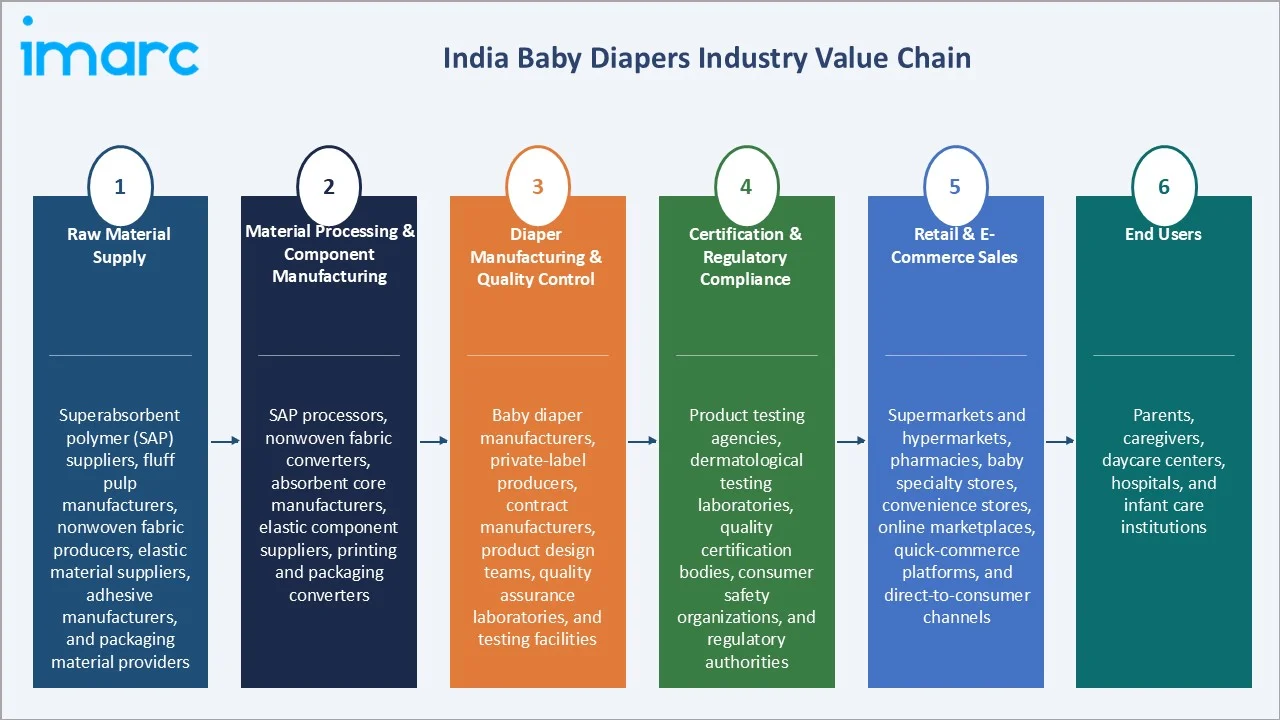

India baby diapers ecosystem integrates superabsorbent polymer (SAP) and fluff pulp raw material supply, diaper manufacturing and quality control, certification and compliance, distributor and C&F agent wholesale, retail and e-commerce channel, and parent and caregiver end user.

Market Dynamics

To evaluate market opportunities, Request Sample

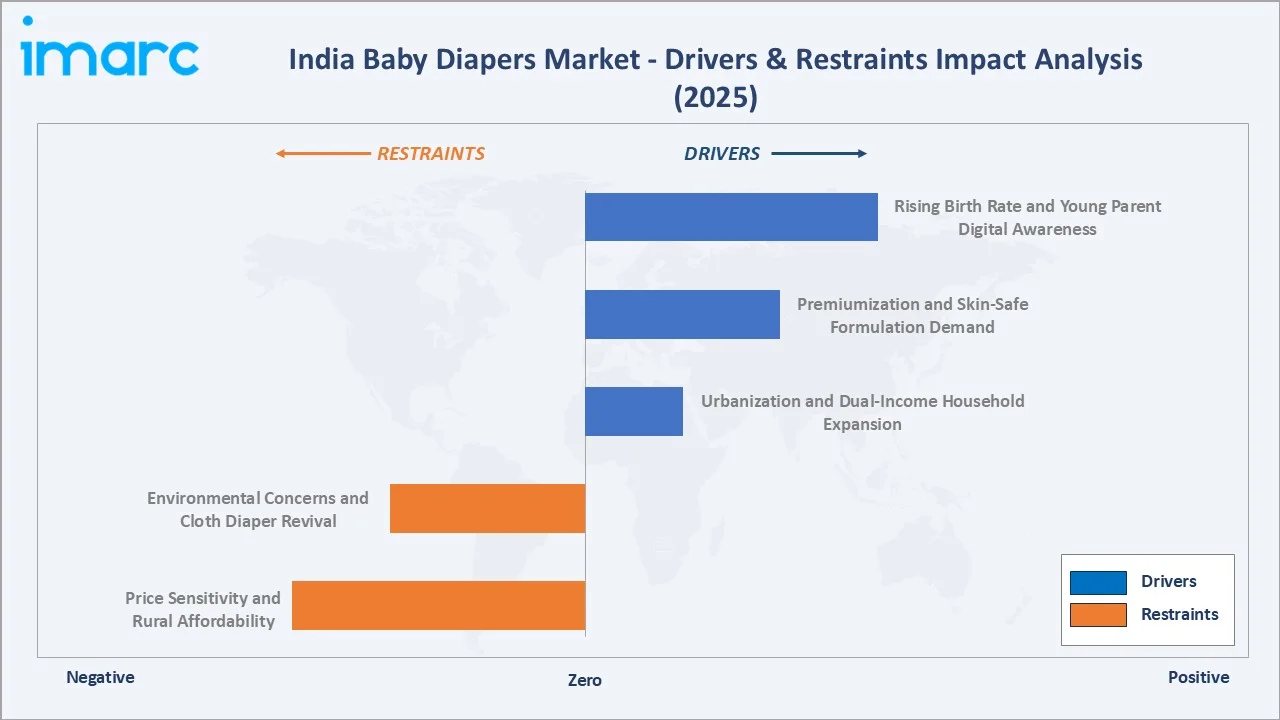

Market Drivers

- Rising Birth Rate and Young Parent Digital Awareness: India's birth rate for 2024 is 16.75 births per 1,000 people, up 3.74% from 2023. These rising birth rates are expanding the infant population, directly increasing the consumer base for baby diapers in India. At the same time, young parents are more digitally aware and exposed to hygiene, baby care, and product comparison content through social media, parenting apps, and e-commerce platforms. This is encouraging faster adoption of disposable, premium, and skin-friendly diapers. Online reviews, influencer recommendations, and subscription buying models are further strengthening repeat purchases.

- Premiumization and Skin-Safe Formulation Demand: Premiumization and skin-safe formulation demand are driving the market as parents increasingly prefer softer, breathable, and dermatologically tested products. Rising awareness about diaper rash, skin irritation, and baby comfort is encouraging demand for high-absorbency and chemical-safe diapers. Brands are responding with aloe vera, hypoallergenic, wetness indicator, and ultra-thin premium variants. This shift supports higher-value sales and strengthens brand differentiation in the market.

- Urbanization and Dual-Income Household Expansion: As stated in the Economic Survey 2023-24, India’s urban population is projected to exceed 40% of the total population by 2030. Urbanization and dual-income household expansion are increasing the demand for convenient and time-saving baby care products. Working parents prefer disposable diapers due to ease of use, hygiene, and reduced laundry burden. Urban households also show a higher willingness to spend on premium, comfortable, and skin-safe diaper products. Expanding modern retail and e-commerce access in cities further supports frequent and bulk purchases.

Market Restraints

- Price Sensitivity and Rural Affordability: Price sensitivity and rural affordability hamper the market because many households still view disposable diapers as a non-essential or occasional-use product. Higher per-unit costs compared to cloth alternatives limit regular usage, especially in rural and low-income segments. Limited purchasing power also restricts the adoption of premium and branded diaper products. As a result, market penetration outside urban and semi-urban areas remains gradual despite rising hygiene awareness.

- Environmental Concerns and Cloth Diaper Revival: Environmental concerns are hampering the market as disposable diapers generate non-biodegradable waste and raise landfill concerns. Growing awareness of sustainability is encouraging some parents to consider reusable cloth diapers and eco-friendly alternatives. Cloth diaper revival is especially appealing to cost-conscious and environmentally aware households. This shift may slow disposable diaper adoption, particularly among urban premium consumers and rural families seeking lower-cost options.

Market Opportunities

- Tier-2 and Tier-3 City Disposable Penetration: Tier-2 and Tier-3 city disposable penetration represent a major opportunity as rising incomes, urbanization, and improved retail access increase awareness of baby hygiene products. Expanding e-commerce platforms and organized retail networks are making diapers more accessible in smaller cities. Tier 2 and Tier 3 cities are gaining strong business attention due to their large untapped e-commerce potential, currently contributing around 35% of India’s e-commerce market and expected to reach 50% by 2026. As e-commerce expands, parents can more easily compare brands, buy affordable packs, and adopt disposable diapers for convenience and hygiene.

- Biodegradable and Bamboo Diapers: Biodegradable and bamboo diapers represent a significant opportunity as parents become more conscious of environmental sustainability and baby skin health. These products offer eco-friendly alternatives to conventional disposable diapers by reducing plastic content and improving biodegradability. Growing awareness of waste management and demand for natural, chemical-free baby care products are encouraging adoption among urban consumers. As sustainability becomes a key purchasing factor, biodegradable diaper innovations can help brands capture premium and environmentally conscious customer segments.

Market Challenges

- Skin Irritation and Diaper Rash Concerns: Skin irritation and diaper rash concerns pose a challenge as parents are highly sensitive to products that may affect infant comfort and health. Concerns regarding prolonged moisture exposure, chemical additives, fragrances, and material quality can discourage regular diaper usage. Negative experiences may also reduce brand loyalty and increase preference for cloth diapers or alternative baby care solutions. As a result, manufacturers must continuously invest in skin-friendly, hypoallergenic, and dermatologically tested products to maintain consumer trust.

- High Dependence on Raw Material Costs: High dependence on raw material costs challenges the market because key inputs such as fluff pulp, superabsorbent polymers, nonwoven fabrics, adhesives, and packaging are price-sensitive. Any increase in crude oil-linked or imported material costs can raise production expenses for manufacturers. This makes it difficult to keep diapers affordable in a price-sensitive market. As a result, brands may face margin pressure or need to pass costs on to consumers, which can slow adoption.

Emerging Market Trends

1. Ultra-Thin Premium and Skin-Safe Material Innovation

Ultra-thin premium and skin-safe material innovation is emerging as parents increasingly prioritize comfort, breathability, and rash prevention. Brands are developing thinner diapers with high absorbency, soft nonwoven layers, hypoallergenic materials, and better moisture-lock technology. These innovations improve baby comfort while reducing bulkiness and leakage concerns. Rising demand for premium baby care products among urban and digitally aware parents is further accelerating this trend.

2. Quick Commerce and Midnight Diaper Delivery

Quick commerce and midnight diaper delivery are emerging trends as parents increasingly need instant access to baby care essentials during emergencies. Platforms offering 10–30 minute delivery make diaper purchases more convenient, especially in urban and dual-income households. This reduces dependency on planned bulk buying and supports impulse or urgent purchases. As quick commerce expands into more cities, it is expected to strengthen diaper accessibility and repeat consumption.

3. Hospital Newborn Diaper Channel

Hospital newborn diaper channels are emerging as brands partner with maternity hospitals, nursing homes, and pediatric care centers to introduce diapers at the first point of use. Sampling and starter packs help build early product familiarity among new parents. This channel can influence long-term brand preference and repeat purchases after discharge. As institutional maternity care expands, hospitals are becoming an important entry point for diaper adoption in India.

4. Biodegradable and Sustainable Diapers

India produces more than 12 billion disposable diapers every year, creating a major waste disposal and landfill burden. Growing waste concerns are encouraging demand for bamboo-based, plant-based, and biodegradable diaper formats in India. Rising demand for chemical-free and eco-friendly baby care products is encouraging brands to launch premium sustainable variants. This trend is especially gaining traction among urban, high-income, and environmentally aware parents.

Industry Value Chain Analysis

India baby diapers value chain integrates raw material supply, material processing & component manufacturing, diaper manufacturing & quality control, certification & regulatory compliance, retail & e-commerce sales, and end users.

|

Stage |

Key Participants |

|

Raw Material Supply |

Superabsorbent polymer (SAP) suppliers, fluff pulp manufacturers, nonwoven fabric producers, elastic material suppliers, adhesive manufacturers, and packaging material providers. |

|

Material Processing & Component Manufacturing |

SAP processors, nonwoven fabric converters, absorbent core manufacturers, elastic component suppliers, printing and packaging converters. |

|

Diaper Manufacturing & Quality Control |

Baby diaper manufacturers, private-label producers, contract manufacturers, product design teams, quality assurance laboratories, and testing facilities. |

|

Certification & Regulatory Compliance |

Product testing agencies, dermatological testing laboratories, quality certification bodies, consumer safety organizations, and regulatory authorities. |

|

Retail & E-Commerce Sales |

Supermarkets and hypermarkets, pharmacies, baby specialty stores, convenience stores, online marketplaces, quick-commerce platforms, and direct-to-consumer channels. |

|

End Users |

Parents, caregivers, daycare centers, hospitals, and infant care institutions. |

The most value-added segment is diaper manufacturing and quality control. This stage captures high value because it converts SAP, fluff pulp, nonwoven fabrics, and elastic components into finished, branded, performance-tested diapers. Product design, absorbency, leakage protection, comfort, and skin-safe features directly determine brand differentiation and consumer loyalty.

Technology Landscape in the India Baby Diapers Industry

Superabsorbent Polymer and Core Design

Superabsorbent polymer (SAP) and core design significantly improve liquid absorption, retention, and leakage protection. Advanced SAP formulations allow diapers to absorb multiple times their weight in liquid while keeping the surface dry for longer periods. Manufacturers are also optimizing core structures to create thinner, lighter, and more comfortable diapers without compromising performance. These innovations enhance baby comfort, reduce diaper rash risk, and support the growing demand for premium, high-performance diaper products.

Sustainable Low-Wood-Pulp Diaper Technology

Sustainable low-wood-pulp diaper technology reducing dependence on conventional tree-based raw materials while maintaining absorbency and performance. Manufacturers are increasingly exploring resource-efficient core designs that lower environmental impact and support sustainability goals. Such innovations help address concerns related to deforestation, raw material availability, and waste generation. In April 2025, Swara Baby Products Pvt. Ltd. introduced an India-first diaper technology focused on sustainability and conscious living. Used in its Baby Hug Pro brand, the technology significantly reduces conventional wood pulp usage from 100% to nearly 7%, helping lower dependence on tree-based materials such as pine and spruce. This innovation supports more eco-friendly diaper manufacturing and contributes to reduced deforestation.

Wetness Indicator Technology

Wetness indicator technology helps parents easily identify when a diaper needs changing. This improves hygiene, reduces prolonged moisture exposure, and lowers the risk of diaper rash. The feature adds convenience for new parents and caregivers, especially during nighttime use and hospital newborn care. As demand for premium and skin-safe diapers rises, wetness indicators are becoming an important product differentiation feature.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Disposable |

91.6% |

2025 |

|

Sales Channel |

Supermarkets/Hypermarkets |

32.8% |

2025 |

|

Region |

North India |

31.4% |

2025 |

By Product Type

Disposable leads at 91.6% (2025), through its convenience, superior hygiene, and time-saving benefits for parents. Rising urbanization, increasing working-parent households, and growing awareness of infant health are encouraging greater adoption of disposable diapers.

To access detailed market analysis, Request Sample

Non-disposable at 8.4% grows fastest at ~7.8% CAGR by appealing to environmentally conscious and cost-sensitive consumers. Reusable cloth diapers offer lower long-term costs and generate less waste compared to disposable alternatives.

By Sales Channel

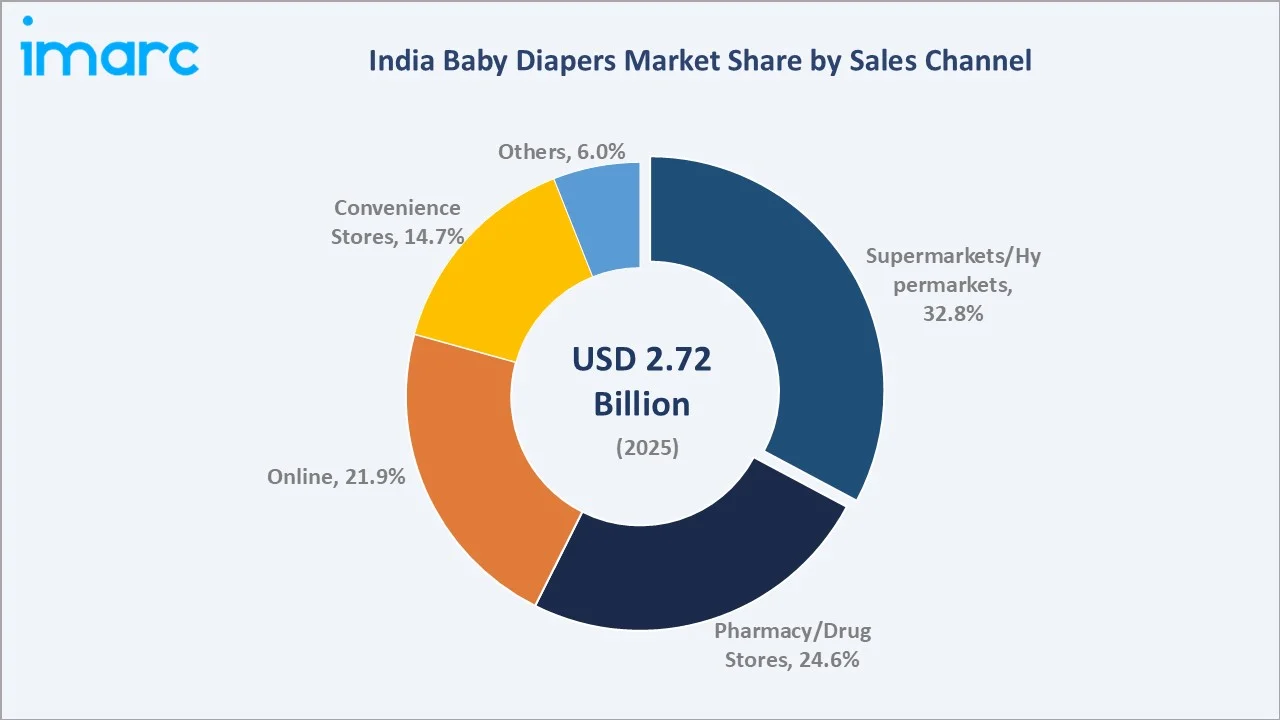

Supermarkets/hypermarkets lead at 32.8% (2025), through DMart, Reliance Smart, and Big Bazaar diaper sales.

Pharmacy/drug stores at 24.6% reflect Apollo Pharmacy, MedPlus, and Netmeds pharmacy chain as India's baby diaper distribution channel. Online at 21.9% grows fastest at ~9.2% CAGR through Amazon India, FirstCry, Flipkart, and Meesho. Convenience stores at 14.7% include kirana, DMart Ready, and Jio Mart. Others at 6.0% include the hospital channel and direct.

Regional Market Insights

|

Region |

Share (2025) |

Key India Baby Diapers Market Drivers & Characteristics |

|

North India |

31.4% |

Driven by a large infant population, rising urbanization, growing disposable incomes, and increasing awareness of baby hygiene products. |

|

West India |

27.6% |

Benefits from high urban household concentration, strong purchasing power, and widespread adoption of premium baby care products. |

|

South India |

24.8% |

Supported by strong healthcare awareness and growing preference for convenient and skin-safe baby care solutions. |

|

East India |

16.2% |

Driven by increasing urbanization, improving retail infrastructure, and rising awareness of infant hygiene. |

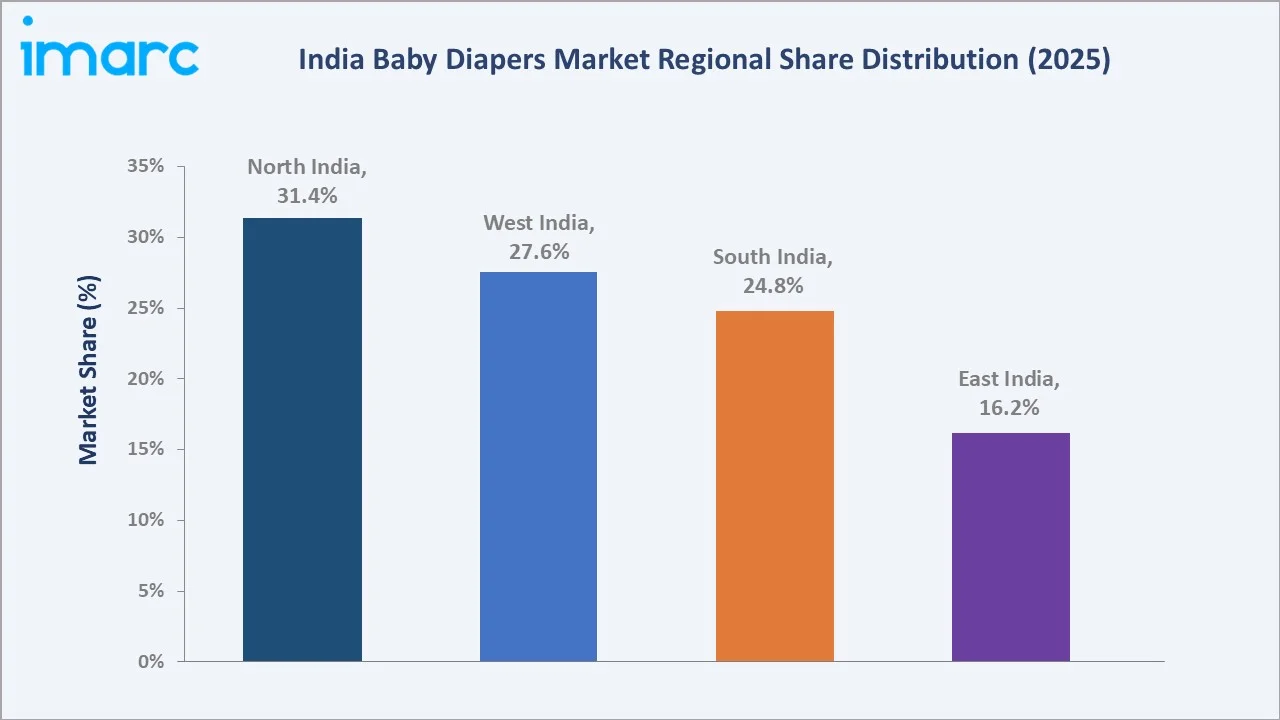

North India leads the India baby diapers market with a 31.4% share, supported by its large infant population, rising urbanization, and growing awareness of baby hygiene products. West India follows with 27.6%, driven by higher disposable incomes, strong retail infrastructure, and demand for premium baby care products.

South India accounts for 24.8%, benefiting from greater healthcare awareness, higher female workforce participation, and increasing adoption of convenient baby care solutions. East India holds 16.2% of the market, supported by improving retail access, urbanization, and growing acceptance of disposable diapers.

Competitive Landscape

The India baby diapers market is moderately concentrated, with competition led by multinational and domestic baby care brands offering a wide range of economy, mid-range, and premium products. Companies compete on absorbency, skin-safe materials, comfort, pricing, distribution reach, and brand trust.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

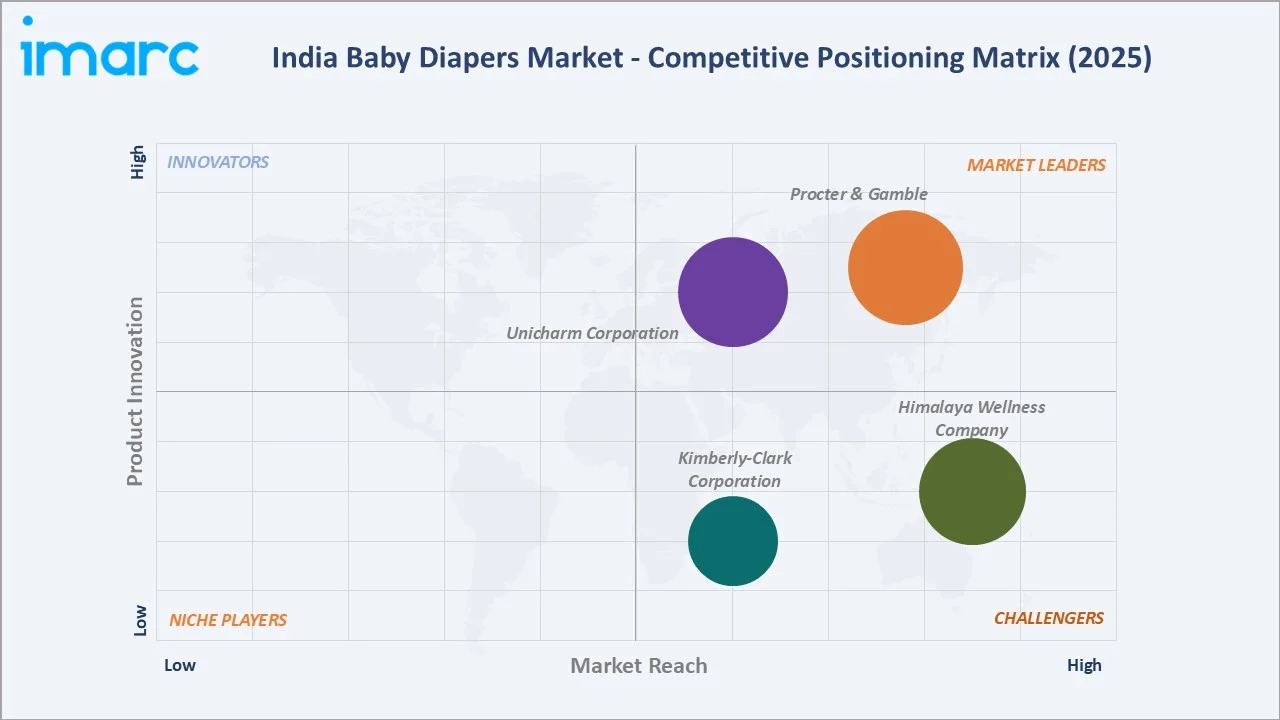

Procter & Gamble |

Pampers |

Market Leader |

Procter & Gamble holds a dominant position in the Indian baby diaper market with its flagship brand, Pampers, often commanding top market share through high-absorbency products, widespread distribution, and premium positioning. |

|

Kimberly-Clark Corporation |

Huggies |

Strong Challenger |

Kimberly-Clark Corporation is a major player in the Indian baby diaper market, driven by its flagship brand, Huggies, which focuses on premium comfort, high absorption, and skin health. |

|

Unicharm Corporation |

MamyPoko |

Market Leader |

Unicharm Corporation is a market leader in India's baby diaper sector, dominating through its MamyPoko brand. |

|

Himalaya Wellness Company |

Himalaya |

Strong Challenger |

Himalaya Wellness Company focuses on providing natural, safe, and clinically tested baby care in India, offering diapers that feature an anti-rash shield and Indian Aloe to prevent diaper rash. |

Product innovation in ultra-thin diapers, wetness indicators, and sustainable materials is becoming a key differentiator. E-commerce, quick-commerce, and hospital channels are increasingly important for customer acquisition and brand visibility. Strategic focus on premiumization, affordability, and rural market expansion is expected to intensify competition over the forecast period.

Key Company Profiles

Procter & Gamble

Procter & Gamble is one of the leading consumer goods companies and a major participant in the India baby diapers market through its flagship Pampers brand. The company offers a broad portfolio of baby care products focused on absorbency, comfort, skin protection, and leakage prevention.

- Key Brands: Pampers

- Recent Developments: In January 2024, Pampers, Procter & Gamble’s baby care brand, introduced its upgraded Premium Care Diapers range. The new diapers feature 360-degree cottony softness for enhanced comfort, along with an anti-rash blanket and aloe vera lotion to help protect babies’ delicate skin from rashes.

- Strategic Focus: Centers on strengthening the Pampers brand through product innovation, premiumization, and wider market penetration.

Kimberly-Clark Corporation

Kimberly-Clark Corporation is a consumer goods company specializing in personal care, baby care, and hygiene products. The company is a prominent participant in the baby diapers industry through its flagship Huggies brand, which offers a range of products focused on comfort, absorbency, leakage protection, and skin care.

- Key Brands: Huggies

- Recent Developments: In November 2025, Huggies, Kimberly-Clark’s baby care brand, launched a new campaign featuring the ‘Geelu Monster’ to highlight the problem of prolonged wetness on babies’ skin. Through a storytelling format, the campaign reinforces Huggies’ positioning as India’s fastest absorbing diaper, supported by consumer insights and product testing.

- Strategic Focus: Strengthening its Huggies portfolio through innovations in absorbency, leakage protection, skin-friendly materials, and baby comfort.

Market Concentration Analysis

The India baby diapers market is moderately concentrated, with multinational brands and established domestic players accounting for a significant share of sales. Leading companies compete through product innovation, premium offerings, brand trust, and extensive distribution networks. The market is characterized by strong competition in absorbency, skin protection, comfort, and affordability. While large brands dominate urban markets, regional and private-label players are expanding their presence through value-priced products. Increasing e-commerce penetration and premiumization trends are expected to intensify competition and encourage continuous product innovation.

Investment & Growth Opportunities

Highest Growth Segments

Online channel (~9.2% CAGR), non-disposable (~7.8% CAGR), pharmacy/drug store (~6.5% CAGR), Tier-2 and Tier-3 city disposable penetration (~8-10% CAGR from lower penetration base), biodegradable diaper (~15-20% CAGR from small base), and hospital newborn channel (~10-12% CAGR) represent India baby diaper highest-growth investment vectors through 2034.

Investment Themes

- Tier-2 and Tier-3 city disposable penetration: Rising incomes, increasing hygiene awareness, growing modern retail presence, and rapid e-commerce expansion are creating a large untapped consumer base. Companies investing in affordable pack sizes, distribution networks, and localized marketing can capture substantial long-term growth opportunities.

- Biodegradable bamboo diaper for eco-parent: Bamboo-based biodegradable diapers offer benefits such as reduced plastic content, improved biodegradability, softness, and natural breathability. As awareness of diaper waste and sustainability increases, premium eco-friendly diaper products are expected to gain traction among urban and high-income consumer segments.

Future Market Outlook (2026-2034)

India's baby diapers market is expected to grow steadily from USD 2.72 Billion in 2025 to USD 4.66 Billion by 2034, registering a 5.99% CAGR. The USD 3.63 Billion market size in 2030 indicates a commercial inflection point, where diaper adoption expands beyond metros into Tier-2 and Tier-3 cities. Growth will be supported by rising hygiene awareness, urbanization, dual-income households, and e-commerce penetration. Premium, skin-safe, and biodegradable diaper formats are also expected to drive higher-value demand. This reflects a shift from occasional usage toward more regular and mainstream diaper consumption across Indian households.

Three structural forces define India’s baby diapers market through 2034: rising hygiene awareness, expanding urban and dual-income households, and wider access through e-commerce and modern retail. Parents are shifting from occasional diaper use to regular consumption due to convenience and infant health concerns. Premiumization is also accelerating demand for skin-safe, ultra-thin, and high-absorbency products. At the same time, Tier-2 and Tier-3 city penetration is creating new volume growth opportunities. Sustainability concerns are further pushing innovation in biodegradable and eco-friendly diaper formats.

Research Methodology

Primary Research

Primary research comprised interviews with baby diaper manufacturers, distributors, retailers, e-commerce platforms, pediatric healthcare professionals, and industry experts. Discussions focused on consumer purchasing behavior, product preferences, pricing trends, distribution strategies, and adoption patterns across urban and rural markets. Insights gathered from these stakeholders were used to validate market size, growth drivers, competitive dynamics, and future opportunities in the India baby diapers market.

Secondary Research

Secondary research encompassed company reports, industry publications, government demographic data, retail studies, e-commerce reports, and baby care market databases. It also included analysis of product launches, pricing trends, distribution channels, and sustainability developments. These sources helped validate market size, competitive positioning, consumer trends, and long-term growth prospects.

Forecasting Models

India baby diapers market revenue forecasts were developed using a penetration and premiumization model: India 0-3 year infant population multiplied by the disposable diaper penetration rate by income tier and geography, multiplied by the average diaper pack price per tier.

India Baby Diapers Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Disposable, Non-Disposable |

| Sales Channels Covered | Supermarkets/Hypermarkets, Convenience Stores, Pharmacy/Drug Stores, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Procter & Gamble, Kimberly-Clark Corporation, Unicharm Corporation, Himalaya Wellness Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India baby diapers market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India baby diapers market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India baby diapers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Baby Diapers Market Report

The India baby diapers market reached USD 2.72 Billion in 2025, driven by rising hygiene awareness, urbanization, and growing demand for convenient baby care products. Increasing disposable incomes, dual-income households, and expanding e-commerce access are supporting regular diaper usage. Premium, skin-safe, and sustainable diaper innovations are further strengthening market growth.

The India baby diapers market grows at 5.99% CAGR during 2026-2034, reaching USD 4.66 Billion by 2034. The CAGR reflects birth volume, urbanization-driven disposable adoption, premiumization trade-up, tier-2 city penetration, and D2C subscription model.

Disposable leads are at 91.6% due to their convenience, hygiene benefits, high absorbency, and easy availability across retail and online channels. Rising urbanization, working-parent households, and preference for time-saving baby care products further support segment dominance.

Supermarkets/hypermarkets lead at 32.8% due to strong product visibility, trusted retail formats, and availability of multiple diaper brands, sizes, and price ranges. Bulk-buying options, discounts, and in-store comparison convenience further support consumer preference for this channel.

North India leads at 31.4% due to its large infant population, rising urbanization, and growing adoption of disposable hygiene products. Strong retail penetration, expanding e-commerce access, and increasing working-parent households further support regional demand.

Leading companies include Procter & Gamble, Kimberly-Clark Corporation, Unicharm Corporation, and Himalaya Wellness Company, among others.

The market reaching approximately USD 3.63 Billion by 2030 indicates steady expansion and wider adoption of baby diapers in India. Growth will be supported by rising hygiene awareness, urbanization, dual-income households, and stronger retail/e-commerce penetration. This milestone reflects the market’s shift from occasional diaper use toward more regular consumption across urban and semi-urban households.

Three priority investment opportunities include Tier-2 and Tier-3 city disposable penetration, biodegradable bamboo diapers for eco-conscious parents, and premium skin-safe diaper innovations. Smaller cities offer significant growth potential due to rising incomes, hygiene awareness, and expanding e-commerce access. Sustainable diaper products are gaining traction as environmental concerns increase among urban consumers. Meanwhile, premium diapers featuring ultra-thin designs, hypoallergenic materials, and enhanced absorbency are attracting parents seeking higher comfort and better infant care solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)