India Battery Market Size, Share, Trends and Forecast by Type, Product, Application, and Region, 2026-2034

India Battery Market Summary:

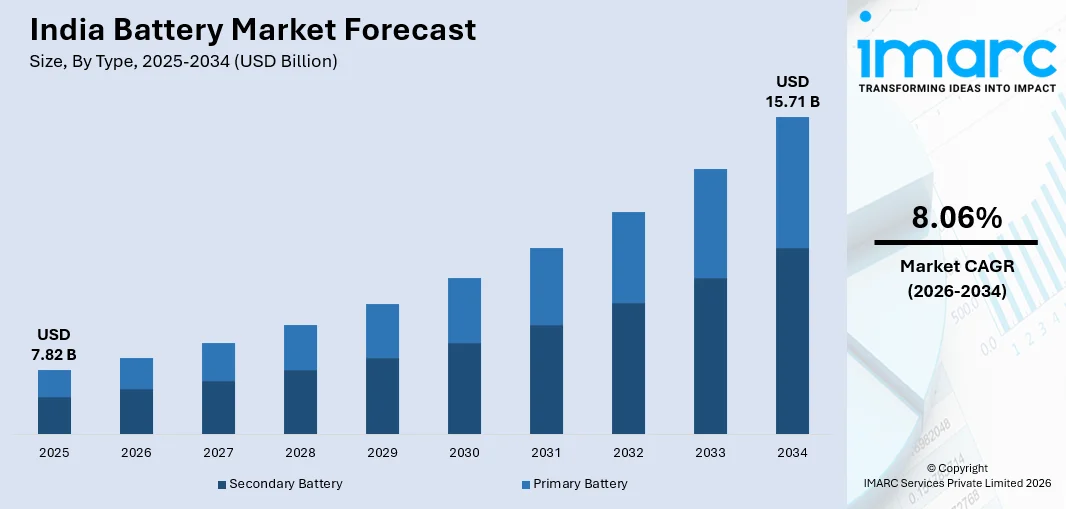

The India battery market size was valued at USD 7.82 Billion in 2025 and is projected to reach USD 15.71 Billion by 2034, growing at a compound annual growth rate of 8.06% from 2026-2034.

The market is driven by the rapid expansion of electric vehicle (EV) adoption, growing renewable energy storage requirements, and increasing consumer electronics penetration across urban and rural areas. Government initiatives promoting clean energy transition and domestic manufacturing capabilities are accelerating sectoral growth. Rising industrialization, telecommunications infrastructure development, and the shift toward sustainable power solutions are further propelling demand, contributing to the expansion of India battery market share.

Key Takeaways and Insights:

-

By Type: Secondary battery dominates the market with a share of 65% in 2025, driven by high demand for rechargeable energy storage across automotive, industrial, and consumer electronics, offering superior lifecycle and cost benefits.

-

By Product: Lithium-ion leads the market with a share of 58% in 2025, owing to high energy density, lightweight design, fast charging, long lifespan, and growing adoption in EVs, portable devices, and grid storage.

-

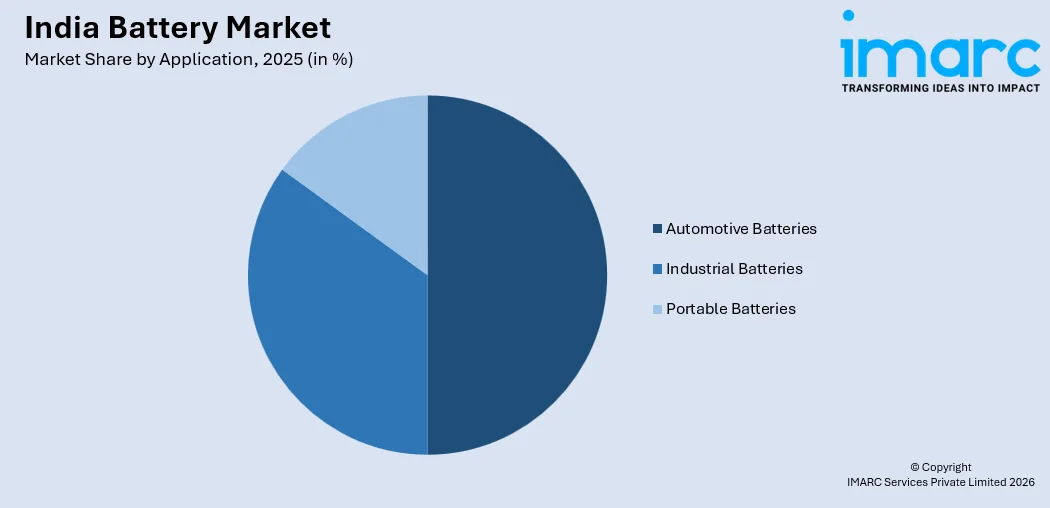

By Application: Automotive batteries represent the largest segment with a market share of 46% in 2025, driven by rising EV adoption, expanding vehicle production, government incentives, and demand for reliable start-stop systems in conventional vehicles.

-

By Region: West & Central India dominates the market with a share of 34% in 2025, owing to automotive hubs, strong industrial infrastructure in Maharashtra and Gujarat, higher urbanization, and significant electronics and renewable energy installations.

-

Key Players: The India battery market is moderately consolidated, with domestic and international players competing through innovation, capacity expansion, and partnerships, focusing on technological advancement and strategic positioning across products and applications.

To get more information on this market Request Sample

The India battery market is witnessing strong growth, driven by the nation’s shift toward sustainable energy and electrified transportation. Supportive government policies, including production-linked incentive schemes, are attracting substantial investments in domestic battery manufacturing. According to sources, in February 2025, the Ministry of Heavy Industries signed a PLI ACC Programme Agreement with Reliance New Energy Battery Limited, awarding 10 GWh capacity, contributing to a cumulative 40 GWh allocated under India’s ACC scheme. Moreover, expanding telecommunications networks require dependable backup power, while the renewable energy sector demands efficient storage solutions for solar and wind generation. Rising disposable incomes are boosting adoption of consumer electronics, increasing the need for portable power sources. Simultaneously, the automotive industry’s transition to EVs, reinforced by favorable regulations and consumer incentives, is fueling demand for advanced battery technologies across passenger and commercial vehicles. Combined, these factors are creating a dynamic market environment, encouraging technological innovation, capacity expansion, and strategic collaborations among domestic and international battery manufacturers.

India Battery Market Trends:

Advancement in Solid-State Battery Technologies

The India battery market is witnessing increasing research and development focus on solid-state battery technologies as manufacturers seek alternatives to conventional liquid electrolyte systems. These advanced batteries offer improved safety profiles by eliminating flammable components while delivering higher energy densities suitable for next-generation EVs. Research institutions and private enterprises are collaborating to accelerate commercialization timelines, with pilot production facilities being established across major industrial corridors. In March 2025, Vikram Solar announced plans to establish a 1 GWh solid-state battery facility, initially scalable to 5 GWh, supporting India’s energy storage ambitions and advancing domestic renewable technology development. The technology promises enhanced thermal stability, faster charging capabilities, and extended operational lifespans, making it attractive for premium automotive and aerospace applications requiring superior performance characteristics.

Integration of Battery Energy Storage with Renewable Infrastructure

Growing renewable energy installations across India are driving demand for grid-scale battery energy storage systems to address intermittency challenges associated with solar and wind generation. Utilities and independent power producers are increasingly deploying large-capacity battery installations to stabilize grid operations, manage peak demand periods, and enhance overall system reliability. In July 2025, IFC and IndiGrid partnered to develop a 180 MW/360 MWh standalone battery energy storage system in Gujarat, enhancing grid stability and supporting India’s renewable energy integration goals. Moreover, this trend is supported by regulatory frameworks encouraging energy storage adoption and declining technology costs improving project economics. The integration enables better utilization of renewable assets while reducing dependence on conventional peaking power plants, contributing to decarbonization objectives across the electricity sector.

Emergence of Battery Swapping Ecosystem

The proliferation of electric two-wheelers and three-wheelers in India is catalyzing the development of battery swapping infrastructure as an alternative to conventional charging. This model addresses range anxiety concerns while reducing vehicle acquisition costs by decoupling battery ownership from vehicle purchase. Urban areas are witnessing rapid deployment of swapping stations, supported by partnerships between vehicle manufacturers and energy service providers. As per sources. in January 2025, Jitendra EV partnered with Battery Smart to integrate batteryswapping technology, providing access to over 1,400 swap stations across 40 cities, reducing charging downtime and promoting EV adoption in India. Moreover, the ecosystem enables fleet operators to maximize vehicle utilization through instant battery exchanges, while standardization efforts are progressing to enhance interoperability across different vehicle platforms and service networks.

Market Outlook 2026-2034:

The India battery market is projected to witness substantial revenue expansion throughout the forecast period, supported by accelerating EV adoption rates, expanding renewable energy storage deployments, and growing consumer electronics demand. Government initiatives promoting domestic manufacturing and reducing import dependence are expected to attract significant capital investments in production capacity expansion. Technological advancements improving energy density, charging speeds, and lifecycle performance will enhance product appeal across application segments. The market revenue trajectory indicates sustained double-digit growth as electrification trends across transportation, industrial, and residential sectors continue strengthening. The market generated a revenue of USD 7.82 Billion in 2025 and is projected to reach a revenue of USD 15.71 Billion by 2034, growing at a compound annual growth rate of 8.06% from 2026-2034.

India Battery Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Secondary Battery |

65% |

|

Product |

Lithium-Ion |

58% |

|

Application |

Automotive Batteries |

46% |

|

Region |

West & Central India |

34% |

Type Insights:

- Primary Battery

- Secondary Battery

Secondary battery dominates with a market share of 65% of the total India battery market in 2025.

Secondary batteries represent the dominant segment within the India battery market, commanding substantial revenue contribution through their application across diverse end-use industries. The rechargeable nature of these batteries makes them economically viable for applications requiring frequent charge-discharge cycles, including automotive starter systems, EVs, industrial backup power, and portable electronics. Their superior total cost of ownership compared to primary alternatives drives preference among commercial and industrial users seeking sustainable power solutions.

The growing emphasis on environmental sustainability and circular economy principles further supports secondary battery adoption as manufacturers implement recycling programs to recover valuable materials. In October 2025, NavPrakriti launched India’s first lithiumion battery recycling plant in Eastern India near Kolkata, supporting circular economy goals and recovering critical minerals for sustainable energy storage applications. Furthermore, technological improvements in battery management systems optimize performance while extending operational lifespans, enhancing value propositions for end-users. The expanding electric mobility sector represents a significant growth catalyst as vehicle electrification accelerates across passenger cars, two-wheelers, and commercial fleets requiring high-performance rechargeable energy storage solutions.

Product Insights:

- Lithium-Ion

- Lead Acid

- Nickel Metal Hydride

- Nickel Cadmium

- Others

Lithium-ion leads with a share of 58% of the total India battery market in 2025.

Lithium-ion dominates the India battery market product landscape, driven by superior performance characteristics meeting evolving energy storage requirements across transportation and stationary applications. These batteries deliver higher energy density per unit weight and volume compared to alternative chemistries, enabling compact designs suitable for space-constrained applications. Their ability to support fast charging protocols addresses convenience requirements for EV users while high cycle life reduces replacement frequency and associated ownership costs.

The establishment of lithium-ion manufacturing facilities is enhancing supply chain resilience while reducing import dependence for this critical technology. As per sources, in 2025, Union Minister inaugurated TDK’s ₹3,000 Crore lithium-ion battery plant in Sohna, Haryana, producing 20 Crore battery packs annually for mobile, laptop, and wearable devices. Moreover, ongoing innovations in cathode and anode materials are improving energy densities and reducing costs, expanding addressable market opportunities. Grid-scale energy storage applications increasingly specify lithium-ion technology for renewable integration projects, while consumer electronics manufacturers continue preferring these batteries for smartphones, laptops, and wearable devices requiring lightweight, high-capacity power sources.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Automotive Batteries

- Industrial Batteries

- Portable Batteries

Automotive batteries exhibit a clear dominance with a 46% share of the total India battery market in 2025.

Automotive batteries lead application-wise market distribution, reflecting the substantial battery requirements across India's expanding vehicle fleet. Conventional internal combustion vehicles require reliable starting, lighting, and ignition batteries, while the growing EV segment demands high-capacity traction batteries enabling adequate driving ranges. Commercial vehicle electrification initiatives targeting urban logistics and public transportation are generating substantial demand for heavy-duty battery systems capable of sustained operation under demanding duty cycles.

Government policies promoting electric mobility through purchase incentives, charging infrastructure development, and manufacturing subsidies are accelerating automotive battery demand growth. Original equipment manufacturers are localizing battery pack assembly operations to meet domestic content requirements while reducing costs. As per sources, in January 2025, Hyundai Motor India began local assembly of EV battery packs at its Chennai facility, achieving 92% localization and supporting the launch of the Hyundai Creta Electric in the domestic market. Furthermore, the aftermarket segment contributes meaningfully as vehicle parc expansion drives replacement demand, with consumers increasingly preferring advanced battery technologies offering improved performance and extended warranty coverage for their vehicles.

Regional Insights:

- South India

- North India

- West & Central India

- East India

West & Central India dominates with a market share of 34% of the total India battery market in 2025.

West and Central India represents the leading regional market, supported by concentrated industrial activity across Maharashtra, Gujarat, and Madhya Pradesh. The presence of major automotive manufacturing hubs drives strong demand for both original equipment and aftermarket batteries. Well-developed industrial infrastructure supports factories requiring reliable backup power solutions, while accelerating urbanization fuels consumer electronics adoption. Metropolitan centers such as Mumbai, Pune, and Ahmedabad contribute significantly to battery demand through dense populations, higher income levels, and expanding commercial and residential energy needs.

The region’s favorable business environment continues to attract investments in battery manufacturing capacity, supported by efficient logistics networks that enable seamless distribution across domestic markets. Large-scale renewable energy installations, particularly solar parks and wind corridors in Gujarat, are increasing demand for grid-scale battery energy storage systems. Expanding EV charging infrastructure across urban centers supports higher EV adoption, while progressive state-level clean mobility policies reinforce the region’s sustained leadership in the India battery market.

Market Dynamics:

Growth Drivers:

Why is the India Battery Market Growing?

Accelerating Electric Vehicle Adoption Across Transportation Segments

The India battery market is experiencing significant growth momentum from the rapid electrification occurring across passenger vehicles, two-wheelers, three-wheelers, and commercial fleets. In February 2025, India’s EV registrations reached 56.75 Lakh vehicles, supported by government initiatives like PM E-DRIVE and FAME India, reflecting strong growth across two-wheelers, three-wheelers, and passenger EV segments. Further, government policy frameworks establishing ambitious electrification targets are supported by substantial purchase incentives reducing acquisition costs for consumers. Automakers are expanding EV portfolios with models addressing diverse price points and use cases, from entry-level commuter vehicles to premium passenger cars. The total cost of ownership advantages over conventional vehicles, including lower fuel and maintenance expenses, are enhancing consumer value propositions and accelerating adoption rates particularly in urban environments.

Expanding Renewable Energy Storage Requirements

India's aggressive renewable energy capacity addition targets are generating substantial demand for battery energy storage systems enabling grid integration of intermittent solar and wind generation. Utility-scale storage installations help manage supply-demand mismatches, provide ancillary services supporting grid stability, and enable time-shifting of renewable generation to higher-value periods. Distributed storage deployments at commercial and industrial facilities reduce peak demand charges while providing backup power capabilities. Policy mechanisms including storage purchase obligations and favorable tariff structures are improving project economics, attracting investments in battery storage capacity across transmission and distribution networks.

Government Manufacturing Incentives Stimulating Domestic Production

Production-linked incentive schemes targeting advanced battery cell manufacturing are catalyzing significant investments in domestic production capacity. According to sources, in 2025, under the Azadi Ka Amrit Mahotsav, the Ministry of Heavy Industries reported that Ola Cell Technologies installed 1 GWh capacity under the PLI ACC scheme, supporting domestic advanced battery manufacturing. Further, these policy frameworks provide financial support for establishing gigafactory-scale facilities capable of meeting growing domestic demand while reducing import dependence for critical energy storage technologies. The incentives attract both domestic enterprises and international battery manufacturers seeking to participate in India's expanding market opportunity. Localized production enhances supply chain resilience, reduces logistics costs, and supports downstream industries including EV manufacturing requiring reliable battery component supply.

Market Restraints:

What Challenges the India Battery Market is Facing?

Limited Raw Material Availability and Supply Chain Dependencies

The India battery market faces constraints from limited domestic availability of critical raw materials including lithium, cobalt, and nickel required for advanced battery chemistries. Dependence on imports exposes manufacturers to supply disruptions, price volatility, and geopolitical risks affecting material availability. Developing domestic mining operations and establishing strategic material reserves require substantial time and investment, creating near-term supply uncertainties for expanding production facilities.

Inadequate Charging and Swapping Infrastructure

Insufficient charging infrastructure availability, particularly in semi-urban and rural areas, constrains EV adoption rates and associated battery demand growth. Range anxiety concerns persist among potential purchasers uncertain about charging accessibility during longer journeys. Infrastructure development requires coordinated investments across public and private entities, with standardization challenges and grid capacity constraints adding complexity to deployment timelines.

Technology Transition Uncertainties and Investment Risks

Rapid technological evolution in battery chemistries creates investment uncertainties for manufacturers establishing production facilities based on current technologies. The potential emergence of superior alternatives could strand capital deployed in existing manufacturing capacity before achieving adequate returns. Market participants must balance competitive positioning requirements against technology transition risks while managing significant capital expenditure decisions.

Competitive Landscape:

The India battery market competitive landscape features a diverse mix of established domestic manufacturers, international energy storage providers, and emerging technology specialists competing across product segments and application verticals. Market participants differentiate through technological capabilities, manufacturing scale, distribution networks, and customer service excellence. Domestic players leverage local market understanding and established channel relationships, while international entrants contribute advanced technologies and global best practices. Strategic partnerships between vehicle manufacturers and battery suppliers are reshaping competitive dynamics, with integrated offerings becoming increasingly important for automotive applications. Investment in research and development capabilities enables participants to advance product performance while reducing costs, with intellectual property portfolios providing competitive advantages.

Recent Developments:

-

In December 2025, Singareni Collieries Company (SCCL) and Altmin signed an MoU to set up India’s first large-scale battery-grade lithium refinery in Telangana, investing Rs 2,250 crore, targeting 2027 operations. The project aims to support India’s EV and energy storage ecosystem while reducing import dependence on refined lithium.

India Battery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Primary Battery, Secondary Battery |

| Products Covered | Lithium-Ion, Lead Acid, Nickel Metal Hydride, Nickel Cadmium, Others |

| Applications Covered | Automotive Batteries, Industrial Batteries, Portable Batteries |

| Regions Covered | South India, North India, West & Central India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Battery Market Research Report and Industry Forecast Report

The India battery market size was valued at USD 7.82 Billion in 2025.

The India battery market is expected to grow at a compound annual growth rate of 8.06% from 2026-2034 to reach USD 15.71 Billion by 2034.

Secondary battery held the largest market share, fueled by widespread adoption across automotive, industrial, and consumer electronics sectors, where rechargeable energy storage solutions offer superior lifecycle performance, cost-efficiency, and reliability compared to single-use alternatives.

Key factors driving the India battery market include accelerating EV adoption, expanding renewable energy storage requirements, government manufacturing incentives, growing consumer electronics penetration, and increasing industrialization demanding reliable power solutions.

Major challenges include high initial vehicle costs, inadequate charging infrastructure in remote regions, variable government incentives, lengthy battery replacement cycles, supply chain limitations, and limited consumer awareness of electric mobility advantages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)