India Battery Swapping Market Size, Share, Trends and Forecast by Vehicle Type, Operation Type, Service Type, Application, and Region, 2026-2034

India Battery Swapping Market Size, Share, Trends & Forecast (2026-2034)

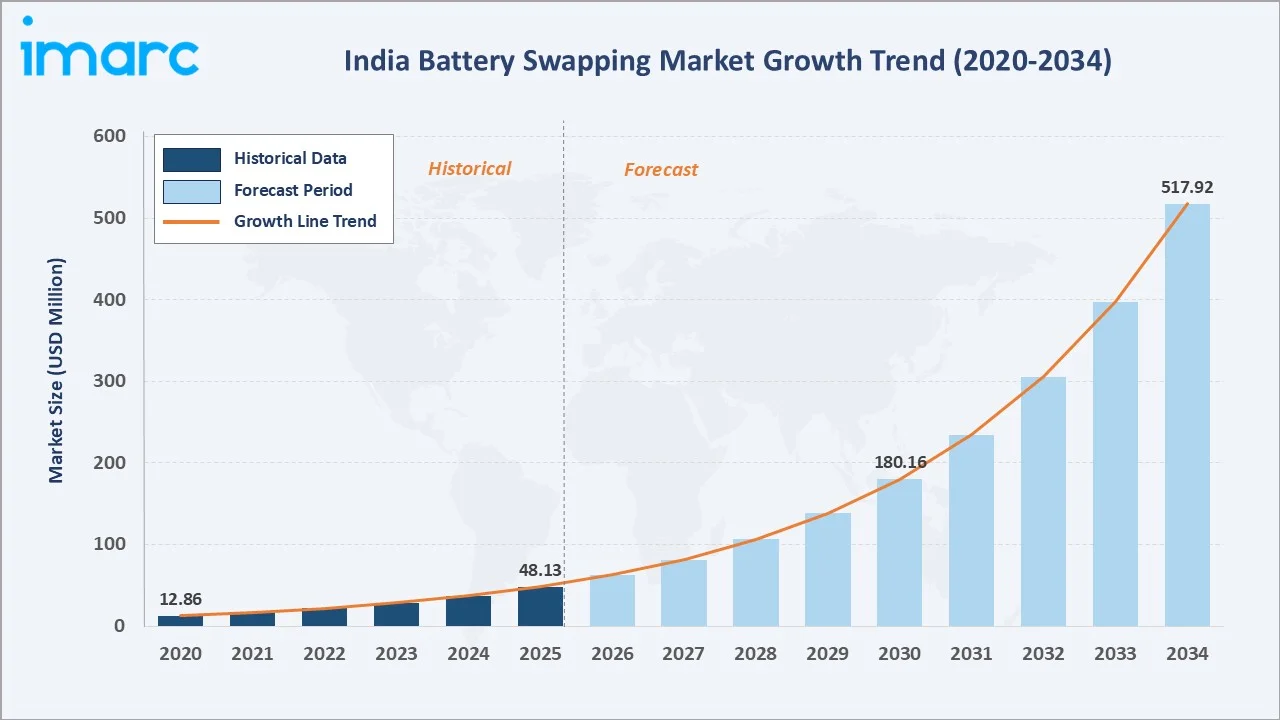

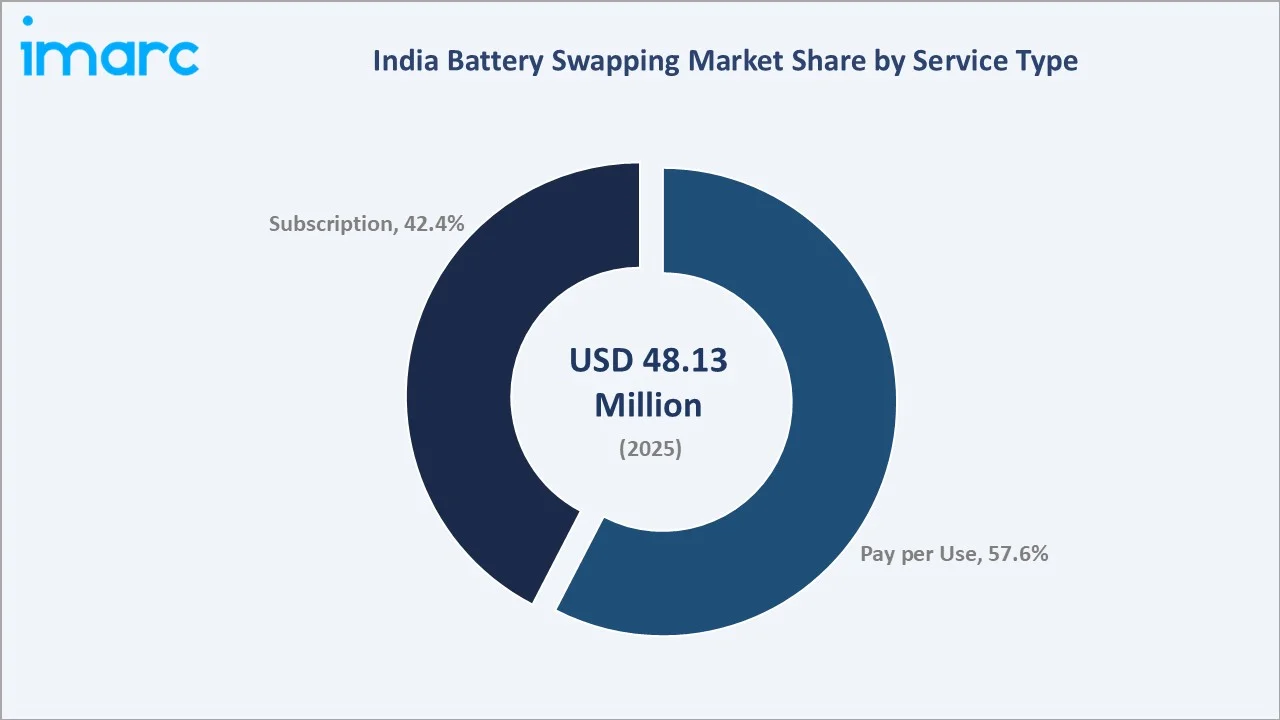

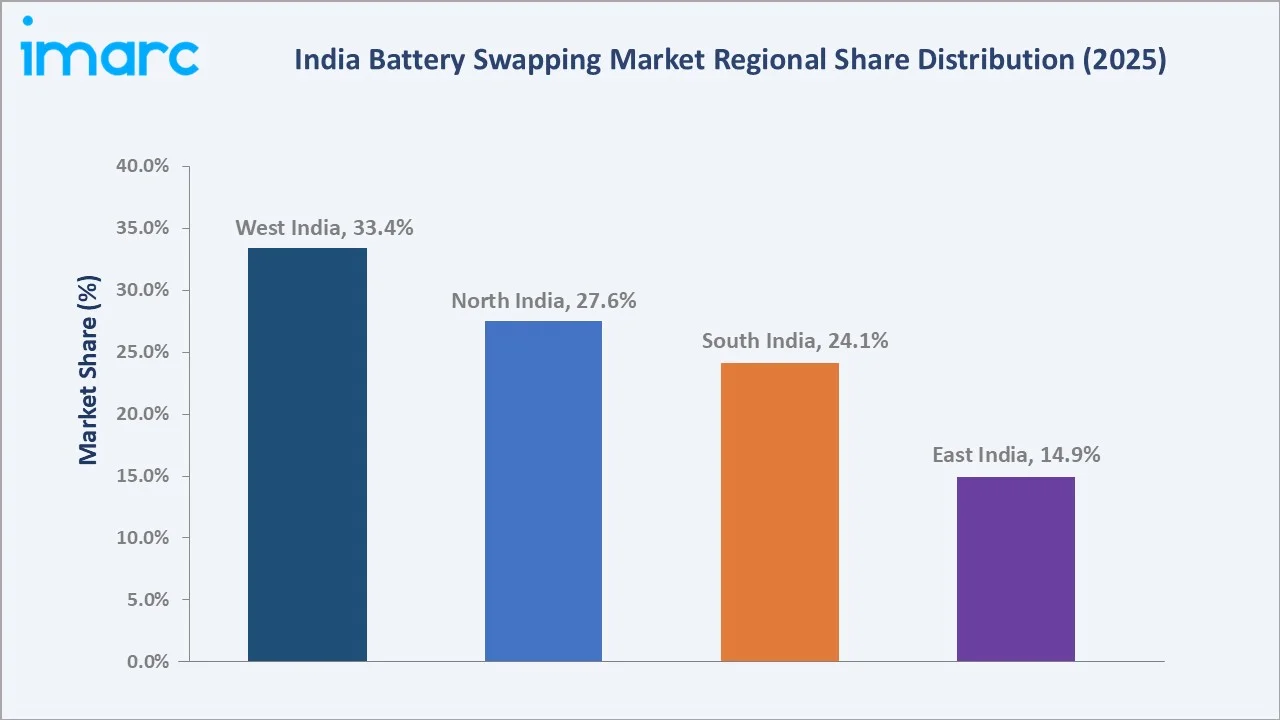

The India battery swapping market reached USD 48.13 Million in 2025 and is projected to reach USD 517.92 Million by 2034, growing at a CAGR of 30.21% during 2026-2034. The market is driven by rising electric vehicle adoption with the Government of India's ambitious target of 30% EV penetration by 2030, demand for faster refueling alternatives, and the need to reduce EV upfront costs by separating battery ownership from vehicle ownership. Manual operation dominates at 63.8%. Pay per use leads service type at 57.6%. West India commands 33.4% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 48.13 Million |

|

Forecast Market Size (2034) |

USD 517.92 Million |

|

CAGR (2026-2034) |

30.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Operation Type |

Manual (63.8%, 2025) |

|

Dominant Service Type |

Pay per Use (57.6%, 2025) |

|

Leading Region |

West India (33.4%, 2025) |

The market expanded from USD 12.86 Million in 2020 to USD 48.13 Million in 2025, anchored at USD 180.16 Million in 2030, and forecast to reach USD 517.92 Million by 2034. NITI Aayog's Battery Swapping Policy framework and national regulatory standards provide the interoperability, safety, and financial framework that converted battery swapping from a niche demonstration technology into a fundable, scalable commercial ecosystem.

To get more information on this market, Request Sample

Automated operation grows fastest at ~34.8% CAGR (2026-2034) as next-generation AI-dispatched battery systems eliminate human attendant dependency, enabling 24/7 unmanned swap station operations with sub-60-second battery exchange. Subscription service type grows at ~31.2% CAGR as fleet operators adopt a monthly battery subscription that eliminates per-swap payment friction and reduces daily operational cost predictability uncertainty.

.webp)

Executive Summary

The India battery swapping market reached USD 48.13 Million in 2025, representing one of the world's most dynamic emerging EV infrastructure markets and the most strategically consequential EV enabling technology in India's specific vehicular and economic context. Battery swapping solves India's three most acute EV adoption barriers simultaneously: range anxiety, upfront cost, and home charging inaccessibility. The market is projected to reach USD 517.92 Million by 2034 at 30.21% CAGR.

Manual operation type at 63.8% dominates as India's battery swapping market matures, manually attended stations operated by station attendants serve 2W and 3W vehicle users with battery packs weighing 8-25 kg that require human handling for safe physical exchange. Pay per use at 57.6% serves retail and occasional EV users. West India at 33.4% leads through Mumbai's deployment scale, Pune's EV ecosystem, and Gujarat's progressive EV policy.

Key Market Insights

|

Insight |

Data |

|

Dominant Operation Type |

Manual - 63.8% share (2025) |

|

Dominant Service Type |

Pay per Use - 57.6% market share (2025) |

|

Leading Region |

West India - 33.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Manual at 63.8% reflecting India's current EV battery form factor and station economics at the early market stage: India's most common swappable batteries require physical handling within the weight range manageable by a single station attendant without mechanical assistance.

- Pay per use at 57.6% serving retail and occasional EV users with no commitment requirement: Pay per use battery swapping serves retail consumers, occasional EV users, tourist e-rental vehicle users, and early adopters who prefer transaction-level flexibility over subscription commitment. Pay per use enables market trial without financial commitment, critical for new EV adopters, uncertain about swapping convenience and network reliability.

- West India at 33.4% anchored by Mumbai-Pune EV ecosystem and Gujarat's progressive policy environment: Mumbai's battery swapping adoption is structurally enabled by the city's flat coastal terrain, extreme apartment density creating residential charging access barriers, and the concentration of India's most active battery swapping operators.

India Battery Swapping Market Overview

India's battery swapping market encompasses all commercial services enabling electric vehicle users to exchange a depleted battery for a fully charged one at a dedicated swap station network, eliminating the fixed-battery EV's long charging time constraint. The market covers swap stations serving two-wheelers, three-wheelers, and emerging commercial vehicle applications. Battery swapping services operate on Battery-as-a-Service (BaaS) commercial models where battery ownership is separated from vehicle ownership. Operators own, manage, charge, and maintain battery inventory while vehicle users pay per swap or subscription.

.webp)

The ecosystem integrates battery manufacturers, swap station hardware providers, Battery Management System (BMS) software developers, network operators, EV OEM partners, fleet operators, ride-hailing platforms, charging energy providers, and battery lifecycle managers. Macroeconomic factors include rapid urbanization, rising fuel costs, growing EV adoption, expanding last-mile delivery fleets, and increasing demand for affordable mobility solutions.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Government Policy Framework: During Budget 2022-2023, the national government announced plans to introduce a Battery Swapping Policy and interoperability standards, with the intent of building and improving the efficiency of the battery swapping ecosystem, thereby driving EV adoption, driving the market by encouraging standardization, reducing range anxiety, lowering EV ownership costs, and supporting faster infrastructure deployment.

- E-2W and E-3W Delivery Fleet Boom Creating Structural Swap Demand: India's EV 2W sales reached 1.14 Million units in FY2025 with fixed-battery and swappable configurations, while cumulative 11-month sales crossed 700,000 units in FY2025. Battery swapping's 90-second swap time enables commercial vehicles to operate 18-20 hours daily versus 12-14 hours with fixed-battery charging, which is the decisive operational advantage driving professional fleet adoption.

- Solving India's Unique EV Adoption Barriers Through Battery Separation Economics: India's specific residential infrastructure context makes home charging unavailable to the majority of India's most price-sensitive EV target market. Battery swapping eliminates home charging dependency.

Market Restraints

- Battery Interoperability Gap Across Proprietary Network Standards: Despite BIS IS 17017 standards, India's battery swapping market remains fragmented across incompatible proprietary battery ecosystems. This creates a 'which network' decision at vehicle purchase that mirrors early mobile carrier lock-in dynamics; consumers hesitate to commit to an EV without certainty that their swapping network will maintain adequate station density in their city.

- Grid Power Reliability Creating Operational Uncertainty in Tier-2/3 Deployment: Battery swapping stations require uninterrupted 3-phase power supply to maintain simultaneous fast charging of depleted batteries while dispensing fully charged batteries to users. Power outages, voltage fluctuations, and load-shedding in India's Tier-2/3 city grid infrastructure create operational disruptions that reduce station availability and damage battery health through incomplete charge cycles.

Market Opportunities

- E-3W Autorickshaw Swapping as India's Highest-Volume Near-Term Opportunity: India recorded over 6 lakh electric three-wheeler registrations in 2024 alone, representing the largest single addressable fleet for battery swapping. Each commercial e-3W performs 3-6 battery cycles daily across 12-16 operating hours, requiring swap infrastructure rather than charging infrastructure.

- V2G (Vehicle-to-Grid) Integration Creating Battery Swapping as Grid Balancing Asset: India's renewable energy capacity target creates significant grid balancing challenges as solar and wind generation intermittency requires large-scale storage. Battery swapping networks' distributed battery inventory collectively constitutes a distributed storage asset that, with V2G-capable charging systems, can discharge stored energy to the grid during peak demand periods and charge during off-peak/renewable surplus periods.

Market Challenges

- OEM Design Lock-In and Retrofit Market Fragmentation Creating Ecosystem Complexity: The majority of India's 2W EV market consists of fixed-battery vehicles where the battery is integrated into the vehicle chassis and cannot be swapped. Retrofitting these vehicles for swappable batteries requires certified modification that voids the manufacturer's warranty, creating a structural division between the OEM-integrated swapping ecosystem and the retrofit market.

- Battery Second Life and Recycling Infrastructure Gaps Creating End-of-Life Risk: Swapped batteries in commercial fleet use reach end-of-life state of health within 2-3 years of intensive commercial operation, creating a battery disposal wave that India's nascent recycling infrastructure is not yet equipped to handle at scale.

Emerging Market Trends

.webp)

1. AI-Powered Dynamic Battery Inventory Management Optimizing Station Uptime

AI-powered dynamic battery inventory management helps operators predict demand, track battery availability, and optimize charging cycles across stations. This improves station uptime, reduces battery shortages during peak hours, supports faster swaps, and enables better fleet servicing for two-wheelers, three-wheelers, and last-mile delivery vehicles.

2. Solar-Integrated Smart Swap Stations Enabling Green and Resilient Operations

Solar-integrated smart swap stations are emerging in India’s battery swapping market as operators look to reduce grid dependence, lower energy costs, and support cleaner EV charging infrastructure. By combining solar power, smart energy management, and battery storage, these stations can improve operational resilience, reduce emissions, and ensure more reliable swapping services in urban and last-mile mobility networks.

3. Multi-Network Interoperability Apps Aggregating Battery Swapping Access

Multi-network interoperability apps are allowing EV users and fleet operators to locate, access, and pay for swaps across multiple station networks through a single platform. This improves convenience, reduces dependence on one operator, supports higher station utilization, and encourages broader adoption of battery swapping among two-wheelers, three-wheelers, and last-mile delivery fleets.

4. Fleet Management Integration Transforming Battery Swapping into a Total EV Operations Platform

Fleet management integration is transforming the market by linking swap stations with vehicle tracking, route planning, battery health monitoring, and driver performance systems. This shifts battery swapping from a standalone refueling service into a broader EV operations platform, helping delivery, logistics, and ride-hailing fleets reduce downtime, optimize utilization, and control operating costs.

Industry Value Chain Analysis

India's battery swapping value chain integrates battery manufacturing and procurement through station infrastructure, IoT software platforms, network operations, fleet service delivery, and battery second-life management. Network operators capture 30-50% gross margins on swap transactions at commercial scale, with battery ownership partially offset by subscription revenue predictability and battery lifecycle asset value.

|

Stage |

Key Participants |

|

Battery Manufacturing & Procurement |

Battery cell suppliers, battery pack manufacturers, battery management system providers, EV component suppliers, testing agencies, and procurement teams. |

|

Swap Station Setup & Installation |

Station equipment manufacturers, charging cabinet providers, energy infrastructure companies, real estate partners, electrical contractors, and installation teams. |

|

IoT & BMS Software Platform |

IoT solution providers, battery management software developers, cloud platform operators, data analytics teams, and mobile app providers. |

|

Swap Network Operation & Maintenance |

Battery swapping operators, station attendants, maintenance teams, energy managers, logistics partners, and service technicians. |

|

Fleet & Rider App Service Delivery |

EV fleet operators, delivery platforms, ride-hailing partners, two-wheeler and three-wheeler users, mobile app providers, and subscription service teams. |

|

Battery Recycling & Second Life Use |

Battery recyclers, second-life energy storage providers, waste management firms, compliance agencies, and sustainability partners. |

The IoT and BMS software platform tier is the battery swapping value chain's most strategically differentiated element. Operators with proprietary real-time battery monitoring, predictive degradation algorithms, and cross-network dispatch optimization create operational advantages that hardware-equivalent competitors cannot replicate.

Technology Landscape in the India Battery Swapping Industry

Lithium-Ion Battery Technology and Pack Design

Lithium-ion battery technology and pack design enabling lighter, higher-density, faster-charging, and more durable battery packs for electric two-wheelers and three-wheelers. Standardized, modular, and smart battery pack designs with BMS integration improve safety, interoperability, battery health tracking, and faster swap turnaround at stations.

Battery Management System (BMS) and IoT Connectivity

Battery management system and IoT connectivity enabling real-time monitoring of battery charge, health, temperature, usage cycles, and location across swap networks. This improves safety, predictive maintenance, inventory planning, theft prevention, and station uptime, while helping operators deliver faster and more reliable swapping services for EV fleets and riders.

Automated Robotic Swap Station Technology

India has about 1,200 active battery swapping stations as of 2025, with ~300,000 swaps conducted daily. Automated robotic swap station technology helps to enable faster, safer, and more standardized battery replacement with minimal manual handling. These systems reduce turnaround time, improve operational efficiency, support high-volume fleet use, and enhance safety by automating battery alignment, removal, insertion, and charging workflows.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | 🔒 | 🔒 | 2025 |

| Operation Type | Manual | 63.8% | 2025 |

| Service Type | Pay per Use | 57.6% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | West India | 33.4% | 2025 |

By Operation Type

Manual operation leads at 63.8% market share (2025). Manually attended battery swapping stations serve the majority of India's commercial e-3W and e-2W swap transactions. Manual stations are typically operated by the network operator or by authorized franchise partners who receive INR 2-5 per swap transaction commission. Manual stations serve the full diversity of vehicle formats and battery sizes currently in India's market.

To access detailed market analysis, Request Sample

Automated operation at 36.2% grows fastest at ~34.8% CAGR. Automated stations achieve 24/7 unmanned operation, sub-60-second swap times without attendant dependency, and higher station utilization rates, enabling placement in high-visibility but unattended locations. The premium user experience of automated swapping commands, premium pricing versus manual swap transactions.

By Service Type

Pay per use leads at 57.6% market share (2025). Pay-per-use battery swapping charges users INR 50-120 per swap transaction based on battery capacity (kWh swapped) and operator pricing. Pay per use serves retail consumers, ride-sharing EV drivers using multiple networks based on availability, and occasional commercial users without fixed-route fleet operations. The pay-per-use model requires no upfront commitment and allows price comparison between networks, making it the dominant commercial model at India's market development stage.

Subscription at 42.4% grows at ~31.2% CAGR as fleet operators and professional riders adopt monthly battery subscription plans. Subscription revenue's predictability enables network operators to secure debt financing against recurring cash flows, critical for capital-intensive station expansion programs requiring long-term financial planning.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West India |

33.4% |

Strong EV fleet adoption, dense urban mobility demand, growing last-mile delivery activity, and higher concentration of commercial two-wheeler and three-wheeler users support battery swapping deployment across major cities and industrial corridors. |

|

North India |

27.6% |

Policy support, expanding EV registrations, high use of electric rickshaws, logistics fleet electrification, and dense urban transport networks are driving demand for accessible and fast battery swapping infrastructure. |

|

South India |

24.1% |

Strong technology ecosystem, rising start-up activity, growing EV manufacturing base, and adoption by delivery, ride-hailing, and urban mobility fleets are supporting the expansion of smart and connected battery swapping networks. |

|

East India |

14.9% |

Growing electric rickshaw adoption, rising urban mobility needs, emerging logistics demand, and gradual EV policy support are creating opportunities for battery swapping stations in developing city clusters and semi-urban markets. |

West India's 33.4% leadership is structurally enabled by Mumbai's unique EV adoption context, the city's residential density creating the world's highest concentration of apartment-dwelling EV users unable to charge at home, flat coastal topography maximizing battery range, and concentration of India's best-funded battery swapping operators.

North India's 27.6% is growing fastest by absolute swap transaction volume as Delhi's mandatory e-3W conversion program and NCR's delivery fleet electrification create the country's highest-volume e-3W swap market. South India's 24.1% is growing fastest by percentage CAGR as Bengaluru's tech-forward EV adoption, Hyderabad's Telangana EV policy, and Tamil Nadu's e-3W mandate create three simultaneous state-level policy tailwinds. East India's 14.9% represents the market's most underserved geographic opportunity as Kolkata's e-rickshaw ecosystem transitions from lead-acid to lithium-ion batteries requiring swap infrastructure.

Competitive Landscape

India's battery swapping market is moderately concentrated with two clear leaders (Gogoro and BatterySmart) by total station count, followed by a cluster of segment-specialized operators and emerging technology-differentiated players. The market's concentration is relatively higher than India's conventional EV charging market due to battery swapping's network effect dynamics; each new station on a network increases value for all existing vehicles compatible with that network, creating winner-take-most dynamics within each proprietary battery ecosystem.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Gogoro |

Gogoro Network |

Strong Challenger |

From breakthrough technology to uncompromising design, safety and service. Every aspect of Gogoro Network is built to make swapping better. |

|

BatterySmart |

BatterySmart |

Strong Challenger |

1,600+ battery swapping stations across 50+ cities |

|

Ampup Energy Private Limited |

VoltUp |

Niche Player |

VoltUp is a meticulously built ecosystem, a one-stop battery swapping platform that promises a future where all 2 and 3-wheeler vehicles can run with zero downtime. |

The competitive landscape is being reshaped by three forces: OEM partnerships aligning vehicle manufacturers with swapping networks to create OEM-validated swap ecosystems with guaranteed vehicle supply; VC consolidation as the market's largest funded operators achieve capital advantages that enable faster network expansion and technology investment relative to under-funded regional operators; and the potential emergence of a NITI Aayog-endorsed interoperability consortium that could create a multi-operator battery sharing network analogous to UPI in payments.

.webp)

Key Company Profiles

Gogoro

Gogoro is the world's most experienced battery swapping company. From breakthrough technology to uncompromising design, safety and service. Every aspect of Gogoro Network is built to make swapping better.

- Platform: Gogoro Network

- Recent Developments: In December 2023, Gogoro announced plans to expand in India. The firm, which already has battery swapping stations in New Delhi and Goa, planned to establish new centers in Mumbai and Pune in Maharashtra.

- Strategic Focus: Gogoro Network interoperability, inviting other Indian OEMs to adopt the Gogoro battery platform, enabling cross-brand swap.

BatterySmart

BatterySmart is one of India's leading two- and three-wheelers dedicated battery swapping company, specializing in the commercial fleet swapping segment that represents India's highest-volume daily swap transaction use case.

- Platform: BatterySmart

- Recent Developments: Battery Smart became India’s first company to complete 100 million battery swaps across its electric two- and three-wheeler network, underscoring the scale of its tech-driven swapping model. To mark the milestone, the company launched a ₹10 crore Driver Welfare Fund 2026 to support nearly 1 lakh drivers with insurance, financial protection, referral rewards, free swaps, and skill-building programs.

- Strategic Focus: Scale its tech-driven battery swapping network for electric two- and three-wheelers while improving rider access, fleet uptime, and driver support services.

Market Concentration Analysis

India's battery swapping market is moderately concentrated, with the top 3 operators commanding approximately 70-75% of organized sector swap transaction revenues. This relatively high concentration reflects battery swapping's network effect economics; operators who achieve critical station density in a city create switching costs for EV users and fleet operators that reinforce market position advantage over time. However, the market's extreme growth rate means absolute revenue opportunities for smaller operators are growing rapidly, even as their market share percentages decline.

Segment-level concentration shows BatterySmart commanding 40-50% of India's organized e-3W autorickshaw swapping market in its operating geographies. These segment-level positions are more defensible than overall market share suggests driver subscription renewal rate demonstrates the stickiness of the e-3W fleet swapping segment once captured. Geographic concentration is significant, reflecting both fleet concentration and consumer EV adoption geography. As Bengaluru, Hyderabad, Chennai, Pune, and Ahmedabad develop their e-3W fleet swapping ecosystems, geographic concentration will reduce through 2030, creating new market entry opportunities for operators not currently competing in metro markets.

Investment & Growth Opportunities

Fastest Growing Segments

Automated operation type (~34.8% CAGR), subscription service model (~31.2% CAGR), e-3W commercial fleet swapping (~35%+ CAGR within vehicle type segment), South India regional market (~32% CAGR from policy tailwinds), and V2G-integrated swap station services (~25%+ from 2027) represent India's highest-growth battery swapping investment vectors through 2034.

Emerging Market Opportunities

East India's Kolkata e-3W ecosystem represents the most significant underserved battery swapping market in India. Kolkata operates high e-rickshaws nationally concentrated in West Bengal, Odisha, and Bihar, the vast majority using lead-acid batteries for which no swap infrastructure exists. As lithium-ion conversion incentives through state government subsidy programs accelerate. First-mover battery swapping operators establishing East India e-3W networks in 2026-2028 will capture subscriber lock-in economics in a market with minimal current organized competition.

Investment Themes

- Solar-integrated automated swap station for highway and fuel plaza deployment: The National Highway Authority of India (NHAI) is actively seeking EV energy infrastructure partners for its highway network. Solar-integrated automated swap stations at highway dhabas, toll plazas, and fuel stations would serve India's growing inter-city e-2W and e-3W highway travel market, currently unserved by any swap network.

- Battery second-life stationary storage business complementing swap operations: Swap station operators accumulating retired batteries are uniquely positioned to deploy these batteries in stationary storage applications at near-zero incremental material cost.

Future Market Outlook (2026-2034)

The India battery swapping market is projected to grow from USD 48.13 Million in 2025 to USD 517.92 Million by 2034, delivering a 30.21% CAGR over the forecast period. The market's anchor value of USD 180.16 Million in 2030 represents a battery swapping ecosystem that has crossed the inflection point from early-adopter commercial fleet deployment to mass-market urban EV infrastructure, where battery swapping stations at petrol pumps, metro exits, and e-commerce fulfillment center parking lots are as ubiquitous as ATMs, serving India's EV 2W and EV 3W fleet with daily energy replenishment at 90-second speed.

Three structural forces define the India battery swapping market's exceptional growth trajectory through 2034: India's e-2W and e-3W adoption reaching tipping point as total cost of ownership parity with petrol vehicles accelerates new vehicle sales, each commercial vehicle converting to battery swapping as the energy access model that enables economically viable daily operation; the NITI Aayog Battery Swapping Policy's second phase establishing mandatory interoperability standards that unlock cross-network battery usage, dramatically increasing effective station density for each EV user and accelerating network growth beyond current proprietary ecosystem constraints; and the gig economy's structural dependency on last-mile EV delivery creating professional EV riders by 2030 who require battery swapping's operational continuity rather than charging's 4-8 hour downtime to maintain their daily earnings.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including CEO and CTO executives; NITI Aayog EV and Battery Swapping Policy officials; BIS technical committee members for IS 17017 battery swapping standards; EV OEM product heads; NBFC financing officers from Northern Arc Capital and Ecozen's rural swap program team; and 50+ e-3W autorickshaw drivers using Battery Smart and Chargeup subscription services in Delhi NCR and Lucknow.

Secondary Research

Secondary research encompassed NITI Aayog Battery Swapping Policy 2022 and draft BIS IS 17017 standards, MHI FAME II and FAME III scheme allocation documents, Vahan vehicle registration database, CEEW India EV Charging Infrastructure report 2025, RMI India Battery Swapping market assessment 2024, FICCI EV report 2025, Bloomberg NEF India EV Outlook 2025, company press releases and investor communications, and SEBI-filed documents for listed entities with EV divisions. Over 90 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up operation type x service type models calibrated against Vahan EV 2W/3W registration data, swap transaction per registered vehicle per day assumptions by vehicle type, average revenue per swap by model (pay per use vs subscription), and operator-disclosed transaction volumes. Key inputs include India EV 2W penetration projections (NITI Aayog 70% EV 2W share by 2030 scenario), e-3W fleet electrification state-by-state mandate timeline, FAME III subsidy impact coefficient on new EV adoption, average swap revenue per kWh of electricity delivered, and station throughput scaling assumptions from Gogoro's Taiwan operational data applied to India's projected utilization curves.

India Battery Swapping Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Two-wheeler, Three-wheeler, Passenger Car, Commercial Vehicle |

| Operation Types Covered | Automated, Manual |

| Service Types Covered | Pay per Use, Subscription |

| Applications Covered | Passenger, Commercial |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Gogoro, BatterySmart, Ampup Energy Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India battery swapping market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India battery swapping market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India battery swapping industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Battery Swapping Market Report

The India battery swapping market reached USD 48.13 Million in 2025, driven by NITI Aayog's Battery Swapping Policy framework, e-2W and e-3W delivery fleet electrification boom, FAME III infrastructure subsidies, and Battery Smart's e-3W registered vehicles generating high daily swap transactions.

The market grows at 30.21% CAGR during 2026-2034, reaching USD 517.92 Million by 2034, driven by EV 2W and EV 3W fleet adoption by 2030, automated station technology maturation, subscription model commercial fleet lock-in, and V2G grid services revenue emerging by 2030.

Manual leads at 63.8% through human-attended stations serving commercial e-3W and e-2W fleets.

Pay per use leads at 57.6% at INR 50-120/swap for retail and occasional users.

West India leads at 33.4%, anchored by Mumbai's swapping station network, Gujarat's progressive e-3W policy, and Pune's EV startup ecosystem creating India's most concentrated urban battery swapping demand.

Leading companies include Gogoro, BatterySmart, and Ampup Energy Private Limited, among others.

The market is projected to reach approximately USD 180.16 Million by 2030, with automated stations comprising 50%+ of new deployments, subscription surpassing pay-per-use in revenue, high e-3W vehicles registered on swap networks, South India overtaking North India in transaction volume, and V2G grid balancing pilots generating ancillary station revenue.

NITI Aayog's 2022 Battery Swapping Policy established a BaaS commercial framework, GST rationalization, BIS IS 17017 interoperability standards, swap infrastructure subsidies, and NBFC financing enablement for battery leasing.

Battery swapping specifically addresses India's three unique EV adoption barriers: 65%+ urban EV users in apartments without home charging access (swapping eliminates charging location dependency), 40-50% battery cost in EV purchase price, and commercial fleet operators' 4-8 hour charging downtime cost (swapping delivers 90-second energy replenishment, enabling 20-hour daily operations).

Three priority opportunities: e-3W subscription swapping in Tier-2 UP and Bihar cities; solar-automated highway swap stations on the NHAI network for inter-city EV travel; and battery second-life stationary storage businesses built on retired commercial fleet swap batteries, achieving near-zero material cost storage deployment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)