India Bearings Market Size, Share, Trends and Forecast by Product, Product Type, End User, and Region, 2026-2034

India Bearings Market Size, Share, Trends & Forecast (2026-2034)

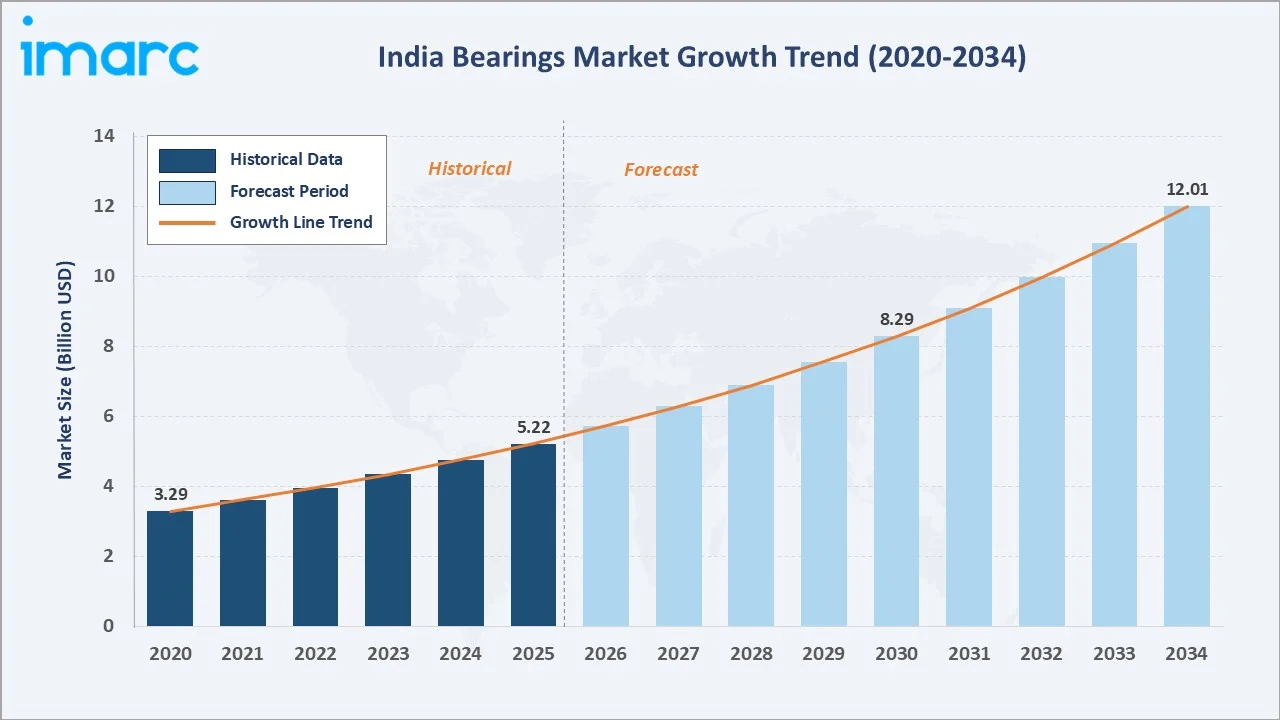

The India bearings market size reached USD 5.22 Billion in 2025 and is projected to reach USD 12.01 Billion by 2034, exhibiting a CAGR of 9.69% during 2026-2034. Expanding automotive production, rising industrial automation, and accelerating infrastructure investment are the primary forces driving market growth.

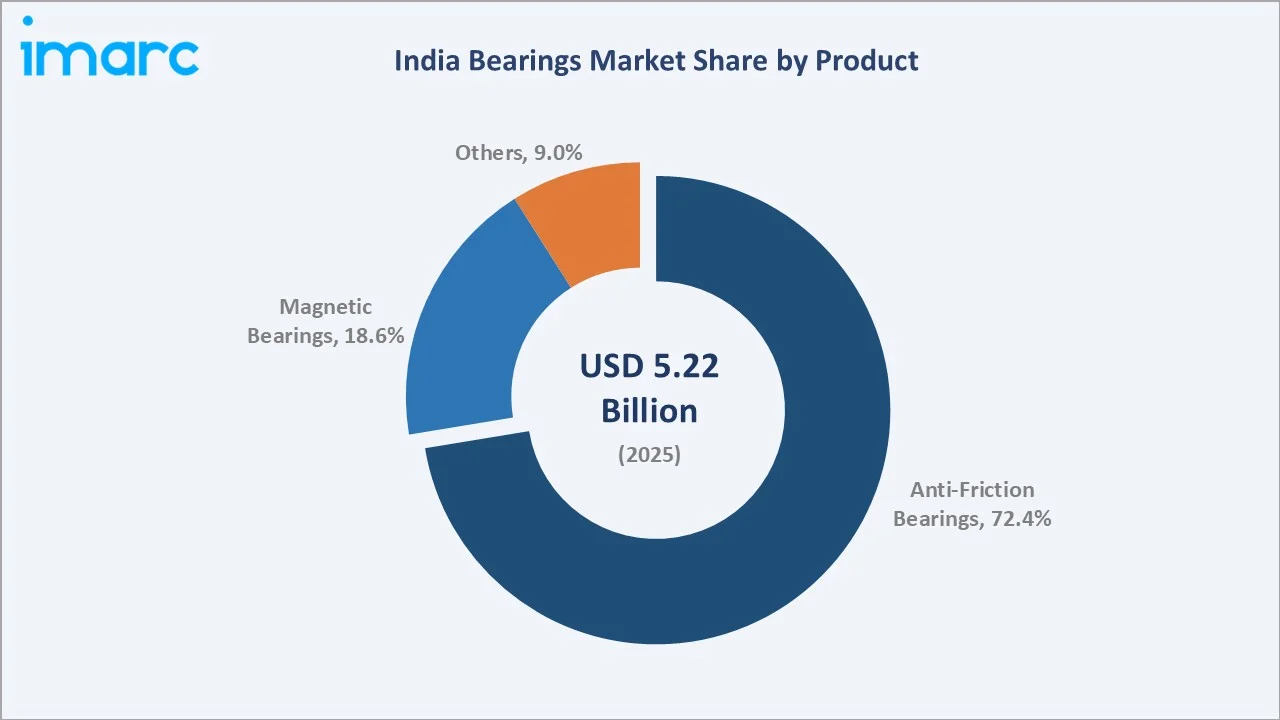

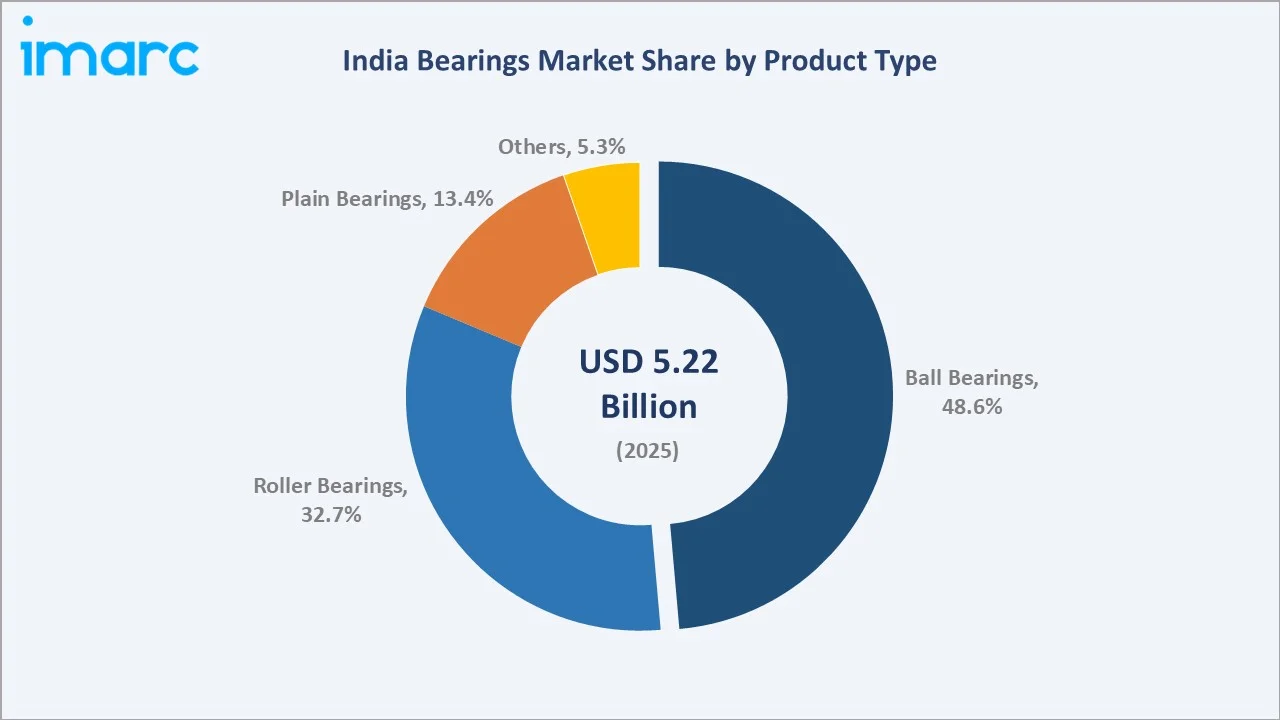

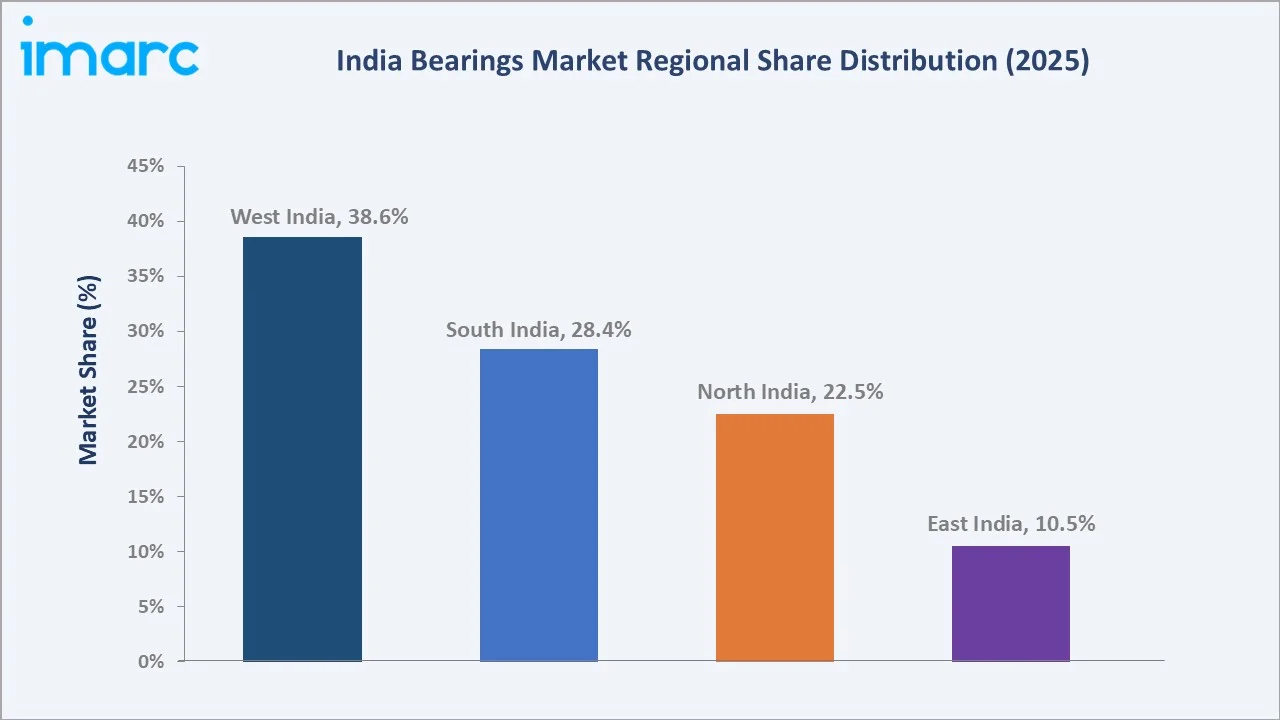

Anti-friction bearings dominate the product mix at 72.4% in 2025, while ball bearings lead the product type segment at 48.6%. West India commands a 38.6% regional share in 2025, reflecting the region's industrial and automotive manufacturing concentration.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.22 Billion |

|

Forecast Market Size (2034) |

USD 12.01 Billion |

|

CAGR (2026-2034) |

9.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (38.6% share, 2025) |

|

Second Largest Region |

South India (28.4% share, 2025) |

|

Leading Product |

Anti-Friction Bearings (72.4%, 2025) |

|

Leading Product Type |

Ball Bearings (48.6%, 2025) |

The India bearings market growth trajectory from 2020 through 2034, with historical expansion to USD 5.22 Billion in 2025, reflects consistent industrial-driven demand. The forecast to USD 12.01 Billion captures accelerating EV adoption, renewable energy investment, and manufacturing-sector automation.

To get more information on this market, Request Sample

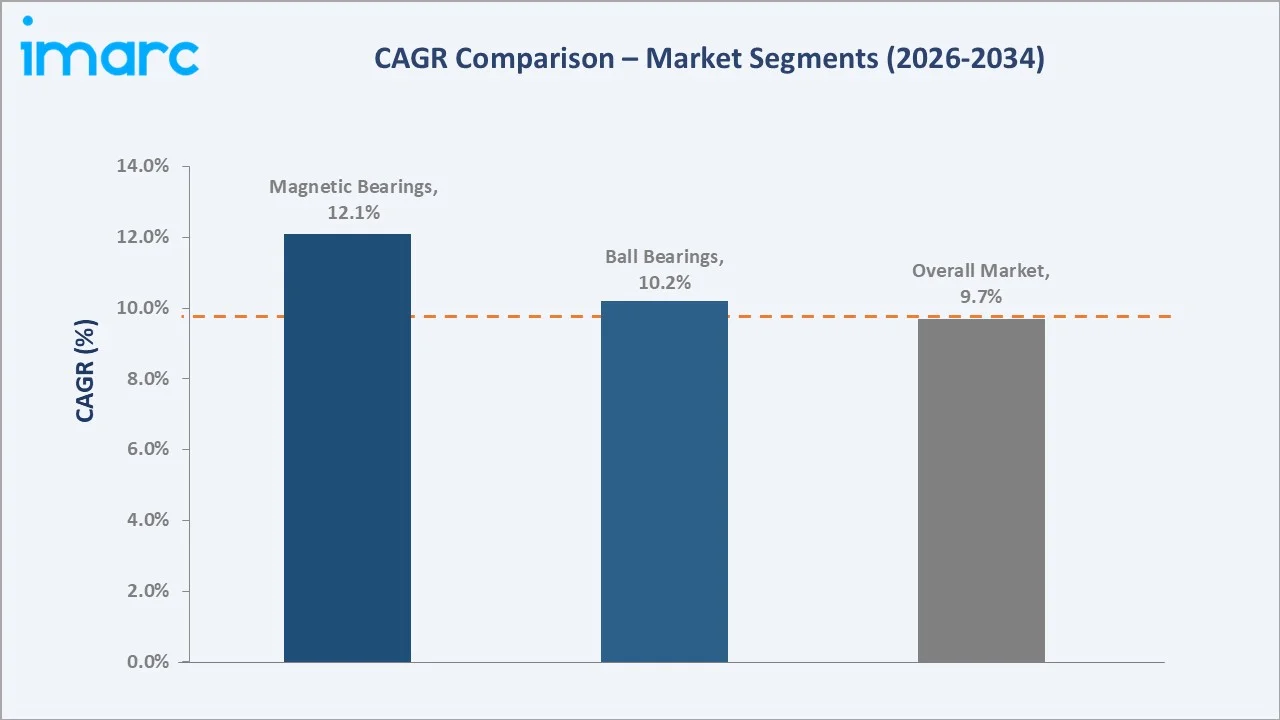

The CAGR trajectories across key product and regional sub-segments, with magnetic bearings at ~12.1% CAGR and anti-friction bearings at ~10.8% CAGR, represent the fastest-growing categories within the India bearings industry analysis through 2034.

Executive Summary

The India bearings market is on a sustained growth trajectory from USD 5.22 Billion in 2025 to USD 12.01 Billion by 2034. Bearings are critical components deployed across automotive drivetrains, industrial machinery, railways, and renewable energy systems, benefiting from non-discretionary demand characteristics.

Anti-friction bearings dominate the product mix at 72.4% in 2025, owing to their superior load-handling and friction-reduction profile across automotive and industrial applications. Magnetic bearings at 18.6% command premium pricing in high-speed precision machinery, growing at the fastest product CAGR of ~12.1% through 2034.

Ball bearings lead the product type segment at 48.6% in 2025, reflecting widespread specification in automotive wheel hubs, electric motors, and general machinery. Roller bearings at 32.7% dominate heavy-duty industrial, railway, and mining applications requiring higher radial load capacity versus ball bearings.

West India dominates at 38.6% in 2025, reflecting the concentration of automotive OEM clusters in Pune and Gujarat. South India at 28.4% and North India at 22.5% follow, driven by Chennai's automotive hub and the NCR industrial manufacturing expansion respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Anti-Friction Bearings – 72.4% share (2025) |

|

Fastest Growing Product |

Magnetic Bearings – ~12.1% CAGR (2026-2034) |

|

Leading Product Type |

Ball Bearings – 48.6% share (2025) |

|

Largest Region |

West India – 38.6% share (2025) |

|

Key Companies |

Schaeffler India Limited, The Timken Company, NEI Ltd., JTEKT India Limited, NSK Ltd. |

Key Analytical Observations Expanding on the Above Data:

- Anti-friction bearings, at 72.4% in 2025, dominate because they address the broadest range of mechanical applications across automotive, industrial, and railway sectors, offering significantly lower friction coefficients and energy losses versus plain bearing alternatives across all load and speed conditions.

- Ball bearings, at 48.6% in 2025, lead the product type segment because they deliver the optimal balance of radial and axial load capacity, low friction, and cost efficiency for the largest application categories including two-wheelers, passenger cars, and electric motors in India.

- West India's 38.6% dominance in 2025 reflects structural manufacturing advantages: Pune's position as India's automotive capital hosting Tata Motors, Bajaj Auto, and numerous Tier-1 suppliers, alongside Gujarat's DMIC corridor industrial investment generating sustained bearing procurement.

- Magnetic bearings at 18.6% and a projected 12.1% CAGR benefit from surging adoption in high-speed turbines, EV motors, aerospace, and precision machine tools where contactless operation eliminates mechanical wear and lubrication requirements entirely.

India Bearings Market Overview

Bearings are mechanical components enabling constrained relative motion between two parts. They are classified by load direction, contact type, and configuration. The India bearings ecosystem integrates steel mills, precision machining facilities, heat treatment providers, surface finishing companies, authorised distributors, and diverse end-use industries across automotive, industrial, railway, and energy sectors.

India produced 25.93 million vehicles in FY 2023, with the automotive sector accounting for approximately 60% of national bearing demand. Industrial automation, railway modernisation under Vande Bharat programmes, and expanding renewable energy infrastructure collectively drive the remaining 40% of market demand.

Market Dynamics

To evaluate market opportunities, Request Sample

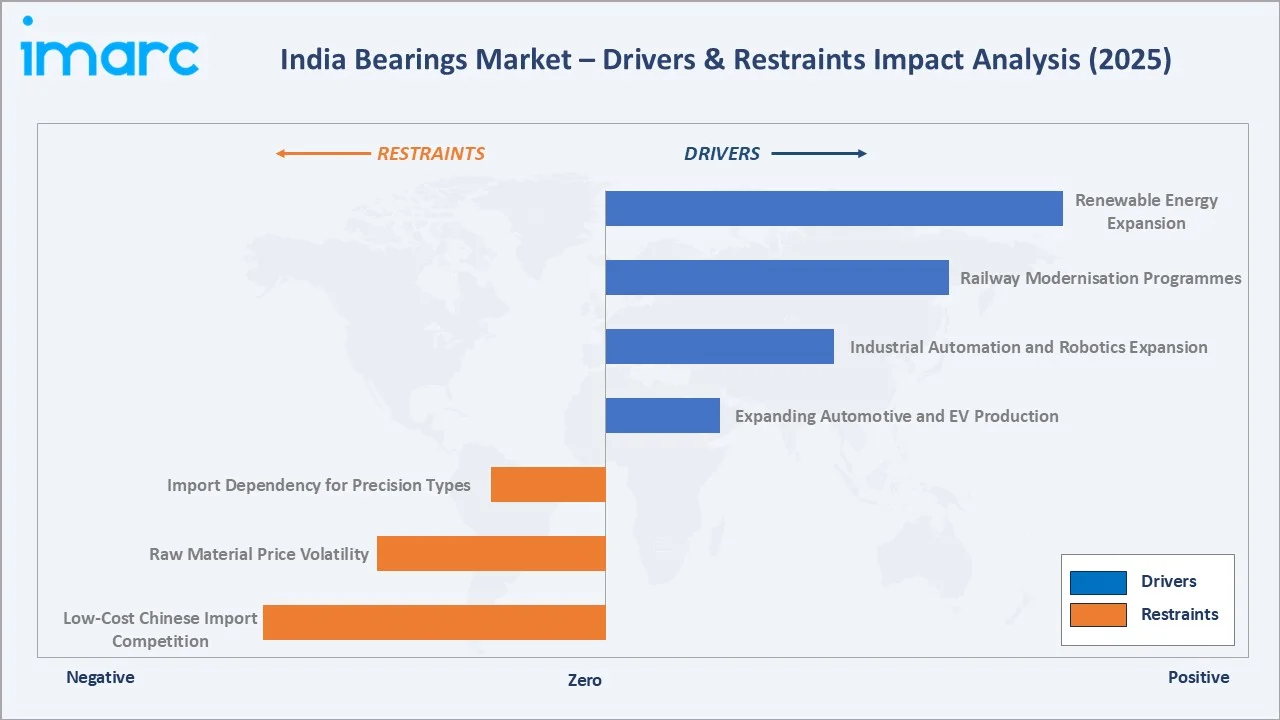

Market Drivers

- Expanding Automotive and EV Production: India's vehicle fleet exceeding 340 million registered vehicles including 227 million two-wheelers generates structurally high bearing demand. The EV transition is accelerating adoption of high-speed, low-friction bearings for motor systems, requiring configurations tolerating up to 25,000 RPM beyond standard ICE applications.

- Industrial Automation and Robotics Expansion: The National Infrastructure Pipeline investment of USD 1.4 Trillion through 2025 and the PLI scheme covering 14 sectors are driving factory automation upgrades that intensify precision bearing demand in conveyor systems, CNC machinery, and robotic arms across manufacturing plants.

- Railway Modernisation Programmes: Indian Railways' annual capital expenditure exceeding INR 2.93 Lakh Crore, with the Vande Bharat Express fleet expansion targeting 475 trains by 2025, generates large-scale tapered roller and spherical bearing procurement for traction motors, axle boxes, and bogie suspension systems.

Market Restraints

- Low-Cost Chinese Import Competition: The availability of significantly cheaper imported alternatives has intensified competition in the market, leading to increased penetration in certain segments and forcing domestic manufacturers to lower prices; this dynamic has resulted in margin compression, particularly in price-sensitive and aftermarket segments.

- Raw Material Price Volatility: Prices of key inputs are closely linked to global commodity cycles, leading to frequent cost variations; such volatility creates unpredictability in production expenses and can adversely impact profitability, especially under long-term or fixed-price supply agreements.

Market Opportunities

- Electric Vehicle Drivetrain Bearing Demand: India's EV penetration target of 30% two-wheelers and 70% commercial vehicles by 2030 under FAME-III will generate large-scale demand for specialised traction motor bearings, requiring low-noise deep groove ball bearings and ceramic hybrid bearings capable of handling elevated RPM and electrical insulation.

- Wind Energy and Renewable Infrastructure: India's 500 GW renewable energy target by 2030 requires construction of large-format wind turbine installations across new projects, each containing multiple spherical roller and slewing ring bearings for main shaft, gearbox, and generator applications, creating a high-value specialist bearing sub-segment.

Market Challenges

- Counterfeit Bearing Proliferation: The widespread presence of substandard and counterfeit alternatives in the replacement segment poses safety and reliability concerns, undermines the brand value of established manufacturers, and creates unfair price competition; this, in turn, puts pressure on margins for authorized players who are unable to match the low prices of such products distributed through unorganized channels.

- Quality Workforce and Precision Manufacturing Gap: Achieving ISO Grade 3 and Grade 4 precision bearing production required for EVs, aerospace, and precision machinery demands skilled operators and tightly controlled manufacturing environments that remain limited across Indian second-tier cities and industrial clusters.

Emerging Market Trends

1. Smart Bearings and IoT-Enabled Predictive Maintenance

Smart bearing adoption is accelerating across automotive and industrial sectors. Sensors embedded in bearing units enable real-time monitoring of temperature, vibration, and rotational speed. Leading manufacturers have launched condition monitoring platforms that integrate with plant-level SCADA systems, reducing unplanned downtime by up to 40–60% for industrial operators.

2. Electric Vehicle Bearing Specialisation

India's EV industry is driving development of specialised bearings tolerating higher rotational speeds up to 25,000 RPM, electrical insulation properties preventing stray current passage, and reduced acoustic emissions meeting the EV's lower overall noise environment. Ceramic hybrid and insulated bearing variants are becoming standard specifications for domestic EV motor OEM programmes.

3. Localisation Under Make in India and PLI Scheme

PLI scheme benefits and import substitution policy are incentivising international bearing majors to expand Indian manufacturing capacity. Investment programmes by leading manufacturers are targeting new precision bearing production lines, progressively reducing dependence on European and Japanese parent-company imports and positioning India as a bearing export hub.

4. Green and Lightweight Bearing Material Innovation

Sustainability requirements are driving adoption of ceramic, polymer, and composite bearing materials offering lower weight, higher corrosion resistance, and longer lubrication intervals. Self-lubricating plain bearings for food processing and pharmaceutical applications, and PEEK polymer bearings for chemical equipment, represent growing specialised Indian market sub-segments with premium pricing.

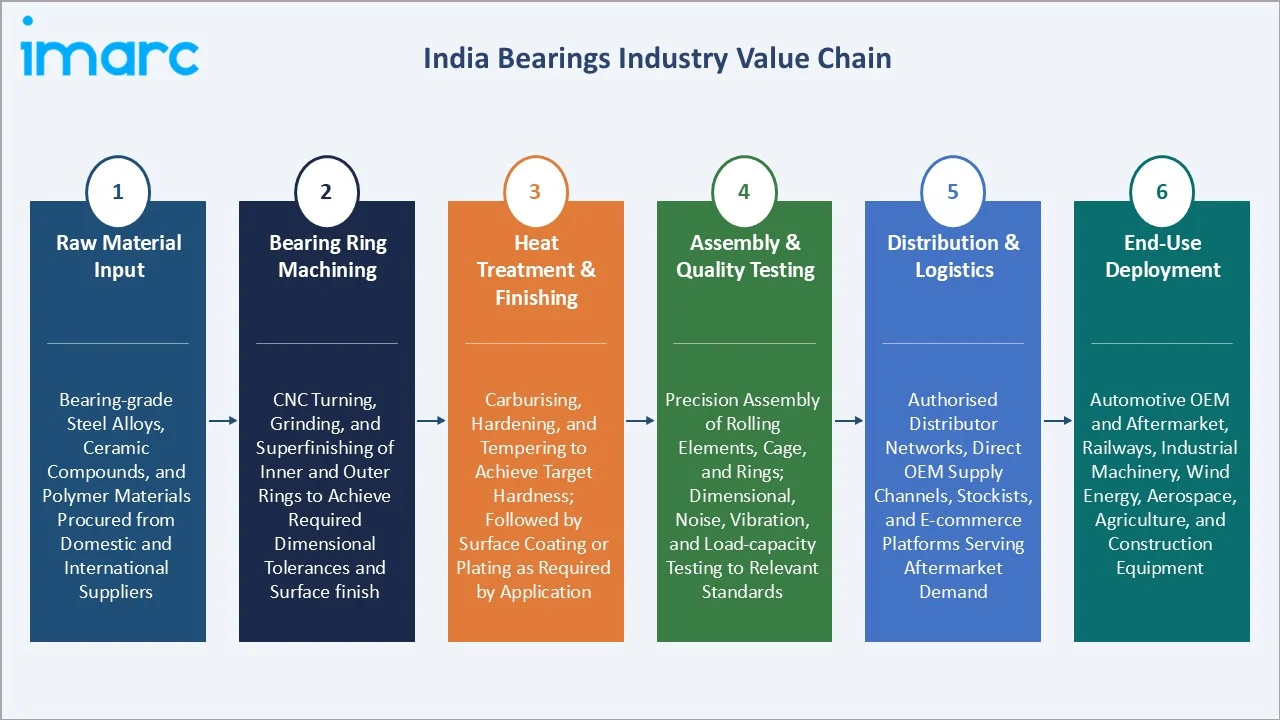

Industry Value Chain Analysis

The bearings value chain spans six stages from raw material input through end-use deployment. Precision machining and heat treatment capture the highest value-add margins, while distribution logistics and OEM qualification processes generate significant barriers to entry that favour established, well-capitalised manufacturers with proven quality management systems.

|

Stage |

Description |

|

Raw Material Input |

Bearing-grade steel alloys, ceramic compounds, and polymer materials procured from domestic and international suppliers |

|

Bearing Ring Machining |

CNC turning, grinding, and superfinishing of inner and outer rings to achieve required dimensional tolerances and surface finish |

|

Heat Treatment & Finishing |

Carburising, hardening, and tempering to achieve target hardness; followed by surface coating or plating as required by application |

|

Assembly & Quality Testing |

Precision assembly of rolling elements, cage, and rings; dimensional, noise, vibration, and load-capacity testing to relevant standards |

|

Distribution & Logistics |

Authorised distributor networks, direct OEM supply channels, stockists, and e-commerce platforms serving aftermarket demand |

|

End-Use Deployment |

Automotive OEM and aftermarket, railways, industrial machinery, wind energy, aerospace, agriculture, and construction equipment |

The value chain is characterised by high barriers at the machining, heat treatment, and quality testing stages, where capital investment and technical expertise requirements are most demanding. Manufacturers controlling these steps internally maintain structural cost advantages over those relying on external processing.

Technology Landscape in the India Bearings Industry

Precision Machining and Grinding Technology

Modern bearing manufacturing in India employs CNC turning centres achieving inner ring bore tolerances within ±1–3 microns for precision-grade bearings. Centreless grinding and superfinishing operations achieve raceway roughness values of Ra 0.1–0.3 μm, critical for low-noise and vibration-free performance in EV and precision machinery applications requiring ABEC 5 to ABEC 9 grade specifications.

Material Innovation: Ceramic Hybrid and High-Performance Steel

High-carbon chromium bearing steel remains the dominant material, providing hardness of 58–65 HRC after heat treatment. Ceramic hybrid bearings using silicon nitride balls offer 40% lower density, 30–50% higher stiffness, and electrical insulation properties. High-strength low-alloy steels are progressively replacing conventional grades in heavy-duty applications demanding improved fatigue life.

Digital Twin and Simulation-Based Design

Leading manufacturers are deploying digital twin platforms for bearing performance simulation, fatigue life prediction, and lubrication optimisation under application-specific load cycles. FEA-based load distribution analysis enables custom bearing design for railway axle boxes, wind turbine main shafts, and EV motor applications with optimised contact geometry and cage configurations.

Surface Engineering and Coating Technologies

Advanced surface engineering is extending bearing service life in demanding environments. Physical vapour deposition coatings such as TiN and DLC applied to rolling elements reduce friction coefficients by 30–40% in dry or marginal lubrication conditions. Ceramic oxide coatings for electrical insulation, and chromate-free zinc-nickel platings for corrosion protection, are gaining traction across automotive and industrial bearing specifications in India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Anti-Friction Bearings |

72.4% |

2025 |

|

Product Type |

Ball Bearings |

48.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

West India |

38.6% |

2025 |

By Product

Anti-friction bearings command a 72.4% majority share in 2025 owing to their fundamental applicability across all major mechanical systems where rolling element contact minimises friction and energy loss. Their broad performance profile makes them the default specification across automotive, industrial, and railway applications in India, covering everything from bicycle hubs to high-speed turbines.

To access detailed market analysis, Request Sample

Magnetic bearings at 18.6% in 2025, growing fastest, are increasingly specified in high-speed turbines, compressors, flywheel energy storage, and EV motor applications where contactless levitation eliminates mechanical wear entirely. Their substantial price premium generates revenue significance disproportionate to volume share.

By Product Type

Ball bearings dominate the product type segment at 48.6% in 2025, representing the most versatile and cost-efficient rolling element configuration for standard automotive and industrial applications. Deep groove ball bearings serve the high-volume two-wheeler and passenger car segments that constitute the majority of India's vehicle production output of over 28 million units in 2023-24.

Roller bearings at 32.7% in 2025 dominate heavy-duty applications including commercial vehicle axles, railway axle boxes, rolling mills, and construction equipment where higher radial load capacity is required. Tapered roller bearings are standard specifications for wheel hub assemblies of commercial vehicles and tractors across India's diverse agricultural and logistics sectors.

Regional Market Insights

|

Region |

Share (2025) |

Key Characteristics |

|

West India |

38.6% |

Largest automotive OEM concentration; industrial corridors; DMIC investment |

|

South India |

28.4% |

Automotive manufacturing hub; aerospace & defence; wind energy expansion |

|

North India |

22.5% |

Diversified manufacturing base; defence corridor; railway manufacturing |

|

East India |

10.5% |

Mining & heavy industry; steel sector; emerging manufacturing investment |

West India's 38.6% market dominance in 2025 is driven by the most structurally concentrated automotive manufacturing base in India. The region's industrial and automotive clusters generate the highest sustained bearing procurement volumes, supplemented by Gujarat's rapidly expanding industrial corridor investments and petrochemical complex bearing requirements.

South India, with 28.4% in 2025, is experiencing strong growth from Chennai's automotive manufacturing cluster hosting major two-wheeler, passenger car, and commercial vehicle OEMs, alongside Bengaluru's expanding aerospace and defence manufacturing base. Tamil Nadu's large wind energy pipeline generates specialised large format bearing procurement supplementing automotive demand.

Competitive Landscape

The India bearings market is moderately consolidated, with international majors holding dominant market positions and domestic players serving specific product niches. The top five players collectively command approximately 60–68% of market revenue, reflecting OEM qualification barriers and the high capital investment required for precision bearing manufacturing at scale.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Schaeffler India Limited |

Rolling bearings and plain bearings |

Leader |

Automotive + industrial dual brand; precision bearing expansion |

|

The Timken Company |

Cylindrical Bearings, Plain Bearings, Spherical Roller Bearings, Tapered Roller Bearings, Thrust Bearings, Precision Bearings, Ball Bearings |

Leader |

Heavy industry, railways, wind energy; premium positioning |

|

NEI Ltd. |

Ball Bearings, Roller Bearings, Cylindrical Roller Bearings, Spherical Roller Bearings, Needle Roller Bearings, Tapered Roller Bearings, Railway Bearings |

Challenger |

Railway OEM; domestic network; capacity expansion |

|

JTEKT India Limited |

Single Ball bearings, Tapered Roller Bearings |

Challenger |

Automotive OEM focus; Toyota group ecosystem |

|

NSK Ltd. |

Ball Bearings, Roller Bearings, Super Precision Bearings |

Challenger |

Precision machinery; EV bearings; machine tool segment |

Key players include Schaeffler India Limited, The Timken Company, NEI Ltd., JTEKT India Limited, NSK Ltd., and others.

Key Company Profiles

Schaeffler India Limited

Schaeffler India Limited, is a leading bearing manufacturer serving both automotive and industrial segments with an extensive product portfolio. The company operates manufacturing facilities in Gujarat, serving domestic OEMs and export markets with precision bearings across the full product range demanded by Indian industries.

- Product Portfolio: Rolling bearings and plain bearings.

- Recent Developments: In August 2025, Schaeffler India announced the expansion of its industrial product portfolio by introducing locally manufactured large-size spherical roller bearings, along with cast steel housings and related accessories, reinforcing its focus on localization and domestic manufacturing. Produced at its Savli facility in Gujarat, these solutions are designed for heavy-duty applications across key sectors such as steel, cement, mining, and power, offering improved performance, durability, and reliability while supporting the company’s broader “Make in India” commitment and enhancing its ability to deliver comprehensive, end-to-end motion solutions.

- Strategic Focus: Schaeffler India's dual-brand strategy differentiates FAG's industrial and heavy-duty automotive positioning from INA's precision motion and needle bearing specialisation, enabling segment-specific competitive advantage across the broadest product range available from any single supplier in India.

The Timken Company

The Timken Company, specialises in tapered roller bearings and premium large-bore industrial bearings for railways, mining, and heavy machinery. Manufacturing facilities are strategically positioned near India's steel and heavy industry clusters, supporting both OEM supply and aftermarket distribution.

- Product Portfolio: Cylindrical Bearings, Plain Bearings, Spherical Roller Bearings, Tapered Roller Bearings, Thrust Bearings, Precision Bearings, Ball Bearings.

- Recent Developments: In April 2025, Timken India inaugurated an expansion of its bearing manufacturing facility in Bharuch, Gujarat, aimed at enhancing production capacity and supporting growing demand from industrial and automotive sectors. The expansion reflects the company’s continued investment in strengthening local manufacturing capabilities, improving operational efficiency, and reinforcing its presence in the Indian market, while aligning with its broader strategy of delivering advanced bearing solutions and supporting regional growth.

- Strategic Focus: Timken India focuses on premium positioning in heavy-duty segments where total lifecycle cost justifies price premiums over commodity alternatives, targeting railways, wind energy, and metals industry applications where bearing performance directly impacts operational safety and efficiency.

NEI Ltd.

NEI is India's leading domestically owned bearing manufacturer and exporter. NEI is the only bearing manufacturer in the world to win the prestigious Deming Grand Prize (2015), producing over 200 million bearings annually across 3,100+ variants from five manufacturing plants in Rajasthan and Gujarat.

- Product Portfolio: Ball Bearings, Roller Bearings, Cylindrical Roller Bearings, Spherical Roller Bearings, Needle Roller Bearings, Tapered Roller Bearings, Railway Bearings.

- Strategic Focus: NEI's strategy centres on maintaining its dominant position as India's largest domestic bearing manufacturer by deepening OEM relationships across automotive, railway, and aerospace segments, while accelerating international growth through the NBC Global platform. Its Deming Grand Prize-certified quality infrastructure and ongoing investment in Industry 4.0 manufacturing technologies position NEI as a preferred partner for both Indian and global OEMs seeking quality-certified, cost-competitive bearing supply.

Market Concentration Analysis

The India bearings market is moderately concentrated at the national level, with the top five players commanding 60–68% of total market revenue. This concentration reflects OEM supply qualification requirements and the high capital and precision manufacturing investment required to compete at scale. Market concentration is higher in the automotive OEM segment than in the industrial or aftermarket segments.

Consolidation is driven by OEM qualification requirements favouring established suppliers with proven quality systems and local technical support. International groups benefit from global technology transfer, enabling product range breadth that domestic manufacturers cannot cost-effectively replicate independently, creating sustained market share advantages for incumbents.

Investment & Growth Opportunities

Fastest-Growing Segments

Magnetic bearings at ~12.1% CAGR through 2034 represent the highest-growth product segment, driven by EV motor applications, high-speed industrial turbines, and precision equipment where contactless operation justifies premium pricing. Ball bearings at ~10.2% CAGR reflect broad-based automotive and industrial demand expansion driven by India's vehicle production growth and factory automation.

Emerging Markets

East India at ~9.5% CAGR represents the fastest-growing region for bearings through 2034, supported by steel and mining sector expansion, proposed industrial complex investments, and the emerging manufacturing cluster development that will progressively narrow the bearing consumption gap with western and southern Indian markets over the forecast period.

Venture & Investment Trends

PLI scheme incentives for precision engineering components are attracting greenfield bearing manufacturing investments from international players seeking to reduce import dependence and serve domestic market growth. Private equity interest in bearing distribution network consolidation is growing, targeting aggregation of regional aftermarket distributors serving the high-margin replacement segment with national reach.

Future Market Outlook (2026-2034)

The India bearings market is forecast to expand from USD 5.22 Billion in 2025 to USD 12.01 Billion by 2034 at a CAGR of 9.69%, adding approximately USD 6.79 Billion in incremental annual market value over the forecast period. This robust growth reflects India's structural industrial expansion, manufacturing sector upgrade, and consumption upgrade across automotive and industrial end-markets.

Three technological forces will significantly shape the bearings landscape through 2034. First, EV penetration will require bearing manufacturers to develop entirely new product lines tolerating higher RPM, electrical insulation, and reduced acoustic emissions. Second, Industry 4.0 will drive smart bearing integration into connected factory environments. Third, renewable energy expansion targeting 500 GW by 2030 will sustain demand for specialised wind turbine and solar tracker bearing applications.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024–2025 with India bearings industry stakeholders, including senior commercial managers at bearing manufacturers, automotive OEM procurement heads, EPC project managers in renewable energy, and authorised bearing distributors. Primary data validated market sizing, product and regional segment shares, and technology adoption timelines across end-use sectors.

Secondary Research

Key secondary sources include SIAM Vehicle Production Statistics (2020–2024), Ministry of Heavy Industries PLI Scheme data, Indian Railways Annual Report (2024), CEA Renewable Energy Installation Data, EEPC India Bearing Export Statistics, IEA World Energy Investment Report (2024), and trade publications including Bearing News, Power Transmission World, and Automotive Manufacturing Solutions India.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating India GDP growth rates, vehicle production indices, industrial output data, and historical market evolution patterns. Scenario analysis encompassing base, optimistic, and conservative cases was performed to reflect policy and macroeconomic uncertainty through 2034.

India Bearings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Anti-Friction Bearings, Magnetic Bearings, Others |

| Product Types Covered | Ball Bearings, Roller Bearings, Plain Bearings, Others |

| End Users Covered | Automotive Industry, Heavy Industry, ARS Industry, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Schaeffler India Limited, The Timken Company, NEI Ltd., JTEKT India Limited, NSK Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India bearings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India bearings market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India bearings industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Bearings Market Report

The India bearings market reached USD 5.22 Billion in 2025, reflecting consistent demand from automotive production, industrial automation, and railway modernisation investment across all four regions of India.

The market is projected to reach USD 12.01 Billion by 2034, growing at a CAGR of 9.69% during 2026-2034, driven by EV adoption, renewable energy infrastructure, and industrial automation expansion across India's manufacturing sectors.

Anti-friction bearings lead with a 72.4% product share in 2025, valued for their superior friction reduction and broad compatibility across automotive drivetrains, industrial machinery, railway systems, and energy applications throughout India.

Ball bearings lead the product type segment at 48.6% in 2025, representing the most versatile and cost-efficient rolling element configuration across two-wheelers, passenger cars, electric motors, and general industrial machinery applications.

West India commands a 38.6% market share in 2025, driven by Pune's automotive OEM concentration, Gujarat's industrial corridor investment, and the Delhi-Mumbai Industrial Corridor's manufacturing expansion driving the highest bearing procurement volumes.

Magnetic bearings are the fastest-growing product segment at ~12.1% CAGR through 2034, driven by electric vehicle motor applications, high-speed industrial turbines, and precision machinery demanding contactless, maintenance-free bearing solutions.

Leading companies include Schaeffler India Limited, The Timken Company, NEI Ltd., JTEKT India Limited, NSK Ltd., and others.

West India hosts India's largest automotive OEM cluster in Pune, Gujarat's DMIC industrial corridor investments, and Maharashtra's diversified manufacturing base, creating the highest concentration of bearing demand from automotive, engineering, and infrastructure sectors nationally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)