India Bio Stimulants Market Size, Share, Trends and Forecast by Product Type, Crop Type, Form, Origin, Distribution Channel, Application, End User, and Region, 2026-2034

India Bio Stimulants Market Size, Share, Trends & Forecast (2026-2034)

The India bio stimulants market was valued at USD 120.7 Million in 2025 and is projected to reach USD 319.7 Million by 2034, exhibiting a CAGR of 11.09% during 2026-2034. India's National Mission for Sustainable Agriculture, which allocates over significant investments annually toward organic farming transitions and soil health improvements, directly accelerates bio stimulant adoption at the farm level. Growing demand for high-yield sustainable crop solutions, rising awareness among Indian farmers about soil microbiome health, favorable government initiatives supporting organic inputs, and expanding export-oriented horticulture are the primary drivers shaping the market growth.

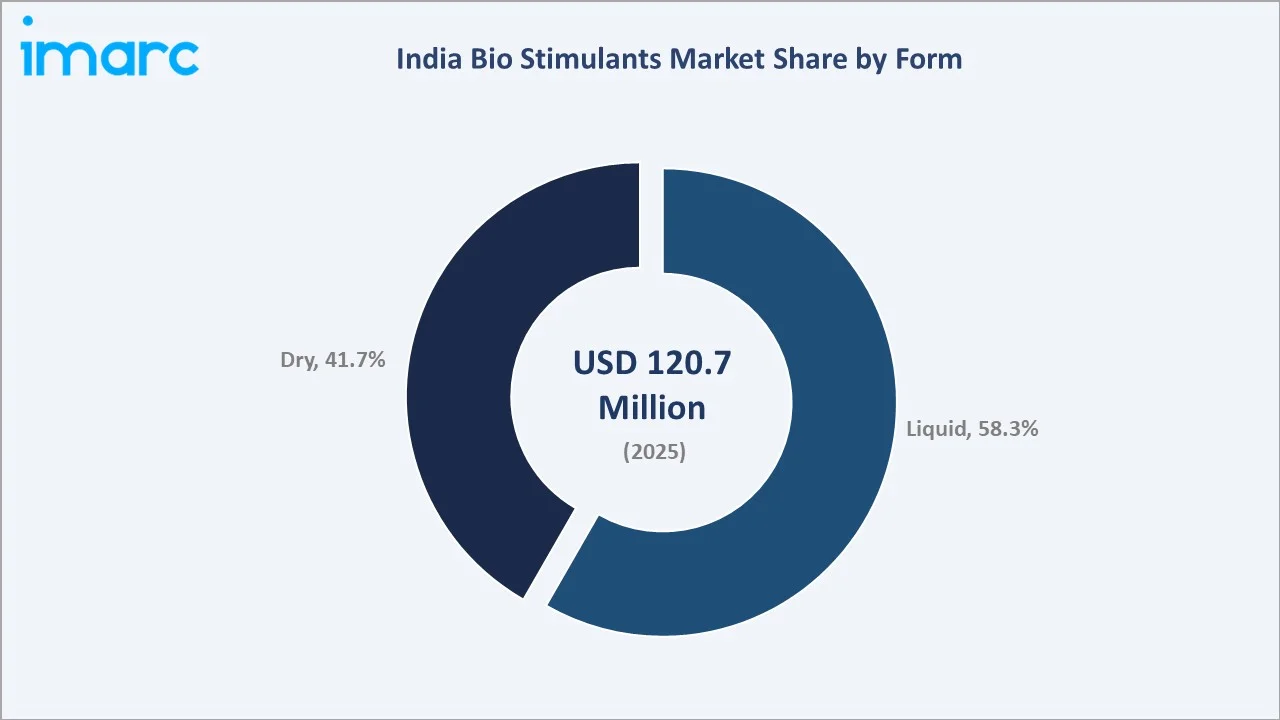

Liquid leads the form segment at 58.3%, natural commands 69.4% of the origin segment, and North India holds 29.7% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 120.7 Million |

|

Forecast Market Size (2034) |

USD 319.7 Million |

|

CAGR (2026-2034) |

11.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29.7%, 2025) |

|

Second Largest Region |

South India (26.4%, 2025) |

|

Leading Form |

Liquid (58.3%, 2025) |

|

Leading Origin |

Natural (69.4%, 2025) |

The India bio stimulants market grew from USD 71.3 Million in 2020 to USD 120.7 Million in 2025, driven by expanding organic farming mandates, government soil health card schemes, and rising input cost pressures nudging farmers toward cost-efficient bio-based solutions. Projected to reach USD 204.2 Million in 2030 and USD 319.7 Million by 2034, the forecast is supported by increasing microbiome research, growth in contract farming for export crops, and deepening penetration in horticulture and cash crop segments.

.webp)

To get more information on this market, Request Sample

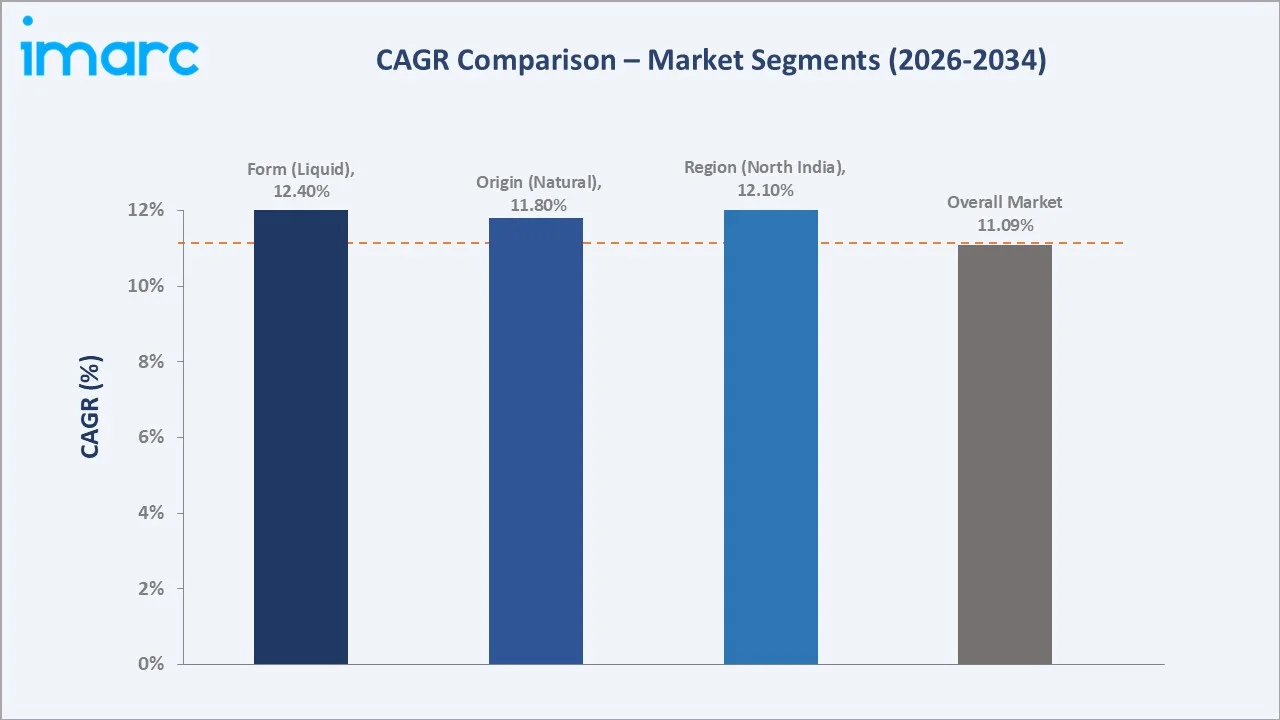

CAGR trajectories across form and origin sub-segments indicate that the liquid and natural categories are growing faster than the overall 11.09% market CAGR, driven by ease of application, faster crop absorption, and growing preference for organic-certified inputs among contract farming operations.

Executive Summary

The India bio stimulants market is on a strong growth trajectory from USD 71.3 Million in 2020 to USD 319.7 Million by 2034. The segment has evolved from limited specialty-crop applications to mainstream adoption across rice, wheat, horticulture, and cash crop cultivation. Soil health deterioration, rising input costs, and regulatory pressure on synthetic agrochemical residues are collectively accelerating the shift toward bio-based inputs. Affordable microbial inoculants, seaweed-derived extracts, and humic acid-based formulations are expanding the addressable farmer base beyond organized agribusinesses to smallholder farming operations.

Liquid leads the form segment at 58.3% in 2025, supported by precision fertigation compatibility and fast uptake in drip-irrigated horticulture. Natural commands 69.4% of the origin segment, anchored by regulatory preference, certification requirements for organic export crops, and farmer familiarity with seaweed and plant-extract formulations. North India holds the largest regional share at 29.7%, supported by extensive wheat and paddy cultivation, strong agri-input distribution networks, and government-backed soil health initiatives. As per the Ministry of Agriculture & Farmers Welfare, 2025-26 Advance Estimates, Punjab boasted the highest wheat output per hectare, around 5.0 Tons per hectare, in contrast to the national average of 3.5 Tons per hectare.

Key Market Insights

|

Insight |

Data |

|

Leading Form |

Liquid – 58.3% share (2025) |

|

Second Largest Form |

Dry – 41.7% share (2025) |

|

Leading Origin |

Natural – 69.4% share (2025) |

|

Second Largest Origin |

Synthetic – 30.6% share (2025) |

|

Leading Region |

North India – 29.7% share (2025) |

|

Second Largest Region |

South India – 26.4% share (2025) |

|

Top Companies |

UPL, Coromandel International Ltd., Biostadt, Acadian Seaplants Limited |

Key Analytical Observations Expanding On The Data Above:

- Liquid at 58.3% dominates the form segment due to compatibility with drip and sprinkler irrigation systems, easier incorporation into fertigation schedules, and faster plant uptake. The format is especially preferred in horticulture, protected cultivation, and precision farming applications across South and West India.

- Dry at 41.7% maintains a strong position in rain-fed and resource-constrained farming systems. It offers longer shelf life, lower logistics costs, and ease of broadcast application over large acreage, supporting adoption among smallholder wheat and paddy farmers.

- Natural at 69.4% leads the origin segment, anchored by regulatory preference for organically certifiable inputs, rising consumer awareness of chemical residue limits in export produce, and growing agronomic awareness of soil microbiome health.

- Synthetic at 30.6% serves growers seeking standardized formulations with predictable dosage and efficacy. This segment is more prevalent in commercial floriculture, contract farming, and polyhouse operations where yield consistency is prioritized.

- North India at 29.7% commands regional share, supported by large-scale wheat and paddy cultivation, strong agri-input distribution networks in Haryana, Punjab, and Uttar Pradesh, and government incentives for soil health restoration. In Haryana, the region allocated for rice farming grew from 15.26 Lakh hectares in 2020 to 18.68 Lakh hectares by 2025.

India Bio Stimulants Market Overview

Bio stimulants are substances and microorganisms applied to seeds, plants, or the rhizosphere to enhance crop nutrition efficiency, tolerance to abiotic stresses, and overall quality traits irrespective of nutrient content. The India bio stimulants market spans a wide ecosystem of microbial inoculants, seaweed extracts, humic and fulvic acids, protein hydrolysates, amino acids, and inorganic compounds, with applications across cereals, pulses, fruits, vegetables, floriculture, and plantation crops.

The Indian ecosystem integrates raw material suppliers including seaweed harvesters and industrial fermentation units, research and development institutions, formulators and manufacturers, agri-input distributors and co-operative networks, regulatory bodies, and end users comprising progressive farmers, contract farming aggregators, and export-oriented growers. Together they form a vertically connected supply chain enabling delivery of bio stimulant solutions from laboratory to field.

Market Dynamics

To evaluate market opportunities, Request Sample

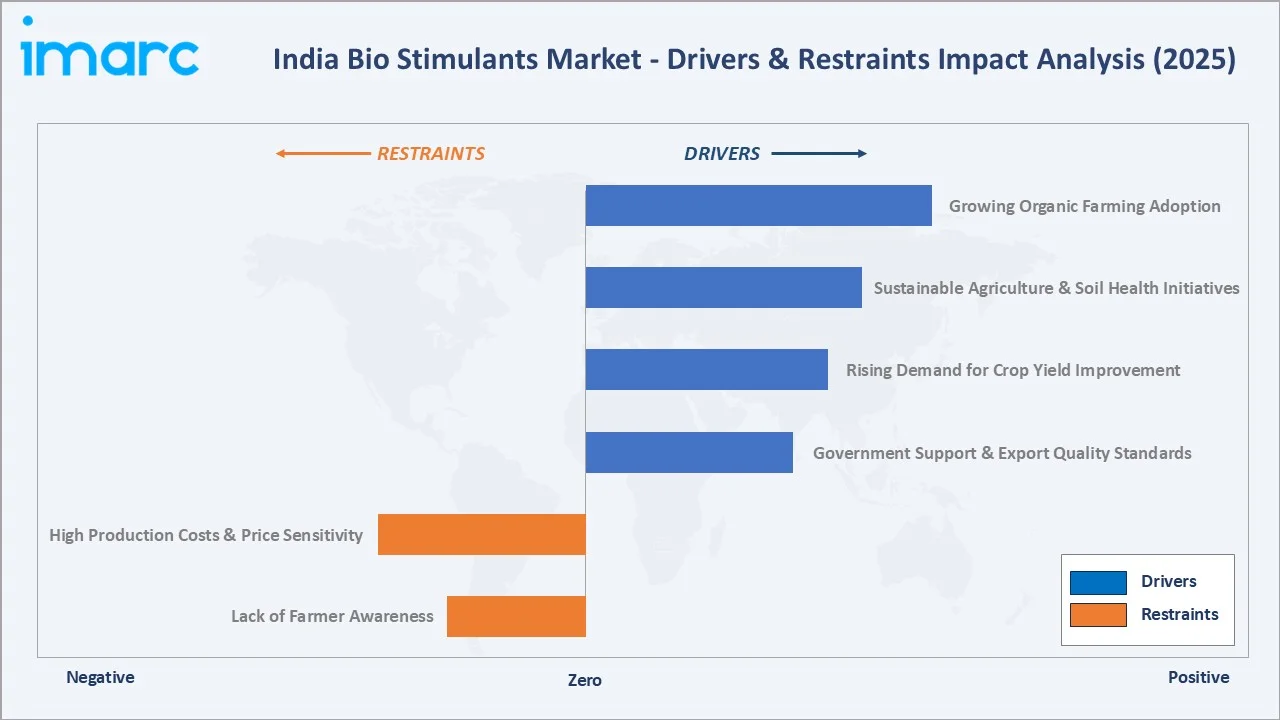

Market Drivers

- Growing Organic Farming Adoption: India's expanding organic cultivation base is driving consistent demand for certifiable bio-based inputs. Organic farming mandates require inputs free of synthetic pesticides and fertilizers, directly expanding the bio stimulant addressable market. As per IMARC Group, the India organic farming market size was valued at USD 6,133.68 Million in 2025.

- Sustainable Agriculture and Soil Health Initiatives: Deteriorating soil organic carbon levels across major cropping belts and Central Government-backed Soil Health Card schemes are incentivizing farmers to adopt microbial inoculants and humic acid-based formulations that restore microbial activity and nutrient cycling capacity.

- Rising Demand for Crop Yield Improvement: Growing food demand from an expanding population, combined with shrinking cultivable land per farmer, is pressuring growers to enhance yield from existing acreage. Bio stimulants addressing nutrient-use efficiency, root development, and abiotic stress tolerance directly support yield optimization without increasing input costs.

- Government Support and Export Quality Standards: Increasing regulatory restrictions on maximum residue levels in horticultural exports to the European Union and the United States are compelling export-oriented growers to substitute synthetic crop protection inputs with bio stimulants, supporting market premiumization and new channel development.

Market Restraints

- High Production Costs and Price Sensitivity: Microbial bio stimulant products have shorter shelf lives, require cold-chain logistics, and involve complex fermentation-based manufacturing processes. These factors increase per-unit costs relative to conventional chemical inputs, limiting adoption among cost-sensitive smallholder farmers who dominate India's agricultural landscape.

- Lack of Farmer Awareness and Technical Knowledge: A significant portion of Indian farmers, particularly in rain-fed and semi-arid regions, lack awareness of bio stimulant mechanisms, recommended dosages, and application timing. Absence of localized extension services and language-specific technical guidance constrains market penetration in tier-2 and tier-3 agricultural districts.

Market Opportunities

- Precision Agriculture and Fertigation Integration: Rapid adoption of drip irrigation and micro-sprinkler systems across Maharashtra, Gujarat, Karnataka, and Andhra Pradesh creates a natural channel for liquid bio stimulants. Integration with soil sensors, crop monitoring platforms, and AI-based advisory tools can enable precision application, improving efficacy and farmer ROI.

- Export-Oriented Horticulture and Organic Certification: India's growing export ambitions in fruits, vegetables, spices, and processed food segments require compliance with importing country pesticide residue norms. Bio stimulants that qualify for use in certified organic production systems represent a premium, low-competition segment with strong margin potential.

Market Challenges

- Efficacy Variability Across Agro-Climatic Zones: Bio stimulant performance is heavily dependent on soil type, ambient temperature, moisture levels, and crop variety. Results achieved in controlled trial conditions may not consistently replicate across India's diverse agro-climatic zones, reducing confidence among first-time adopters and creating hesitancy in repeat purchasing.

- Counterfeit and Substandard Products: Proliferation of adulterated bio stimulant products in unorganized distribution channels undermines category credibility and adversely impacts farmer confidence. Inadequate quality enforcement at state-level markets constrains the growth of premium, science-backed formulations.

Emerging Market Trends

1. Shift Toward Microbiome-Based and Consortia Bio Stimulants

Indian agri-biotech firms and research institutions are moving beyond single-strain microbial formulations toward multi-microorganism consortia products that simultaneously address nitrogen fixation, phosphate solubilization, and hormone-mediated growth promotion. These synergistic combinations deliver broader soil health benefits, reduce application frequency, and command premium pricing in organized retail and institutional channels.

2. Integration with Precision Agriculture and Digital Advisory Platforms

Bio stimulant manufacturers are partnering with agri-tech platforms to embed product recommendations into AI-powered crop advisory tools. Soil testing integration, crop stress mapping via remote sensing, and real-time weather analytics are enabling context-specific bio stimulant prescriptions. This trend is accelerating adoption among progressive farmers in organized horticulture clusters.

3. Seaweed Extract Products Gaining Mainstream Adoption

Seaweed-based bio stimulants containing alginic acid, mannitol, betaines, and natural growth hormones are expanding beyond specialty horticulture into mainstream paddy, cotton, and soybean applications. Coastal proximity to large Kappaphycus alvarezii cultivation zones in Tamil Nadu and Gujarat is supporting domestic raw material availability, reducing import dependence and improving cost competitiveness for Indian manufacturers.

4. Rise of Nano-Formulation and Slow-Release Bio Stimulants

Nano-encapsulation technologies applied to microbial inoculants and plant growth-promoting compounds are extending product shelf life, improving heat and UV stability, and enabling controlled-release application profiles suited to rain-fed farming conditions. These innovations are attracting R&D investment from both domestic agro-chemical companies and start-ups backed by agri-biotech venture funds.

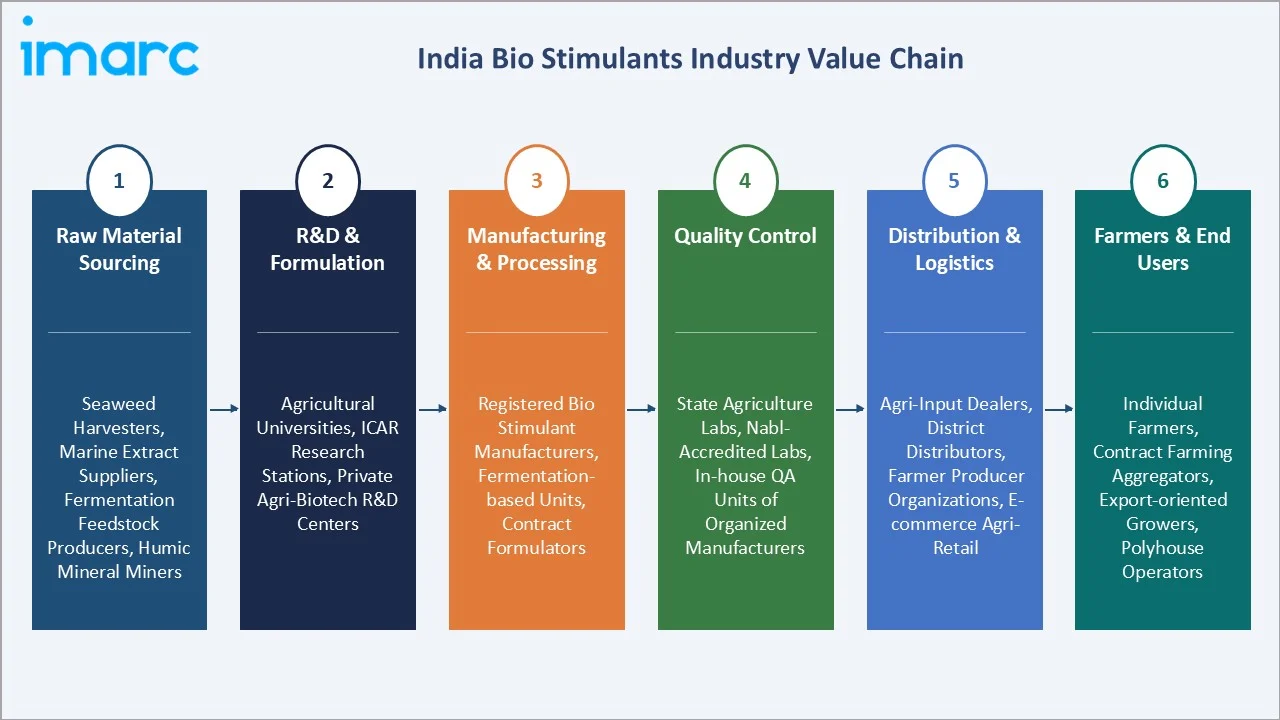

Industry Value Chain Analysis

The India bio stimulants value chain spans six stages from raw material sourcing through end user application and product lifecycle management. Manufacturing, formulation, and distribution capture the highest value-add, while regulatory compliance and farmer advisory increasingly determine sustainable competitive position in this evolving market.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Seaweed harvesters, marine bio-extract suppliers, industrial fermentation units, humic mineral miners, and amino acid feedstock producers |

|

R&D & Formulation |

Agricultural universities, public research institutions, private agri-biotech R&D centers, and ICAR-affiliated research stations developing microbial strains and novel bio stimulant compounds |

|

Manufacturing & Processing |

Registered bio stimulant manufacturers, contract formulators, fermentation-based production units, and granulation and liquid-processing facilities |

|

Quality Control |

State agriculture department testing laboratories, NABL-accredited private labs, and in-house quality assurance units of organized manufacturers |

|

Distribution & Logistics |

Agri-input dealers, district-level distributors, farmer producer organizations, cooperative societies, and e-commerce agri-retail platforms |

|

Farmers & End Users |

Individual farmers, contract farming aggregators, export-oriented growers, polyhouse operators, and crop advisory service providers managing application at farm level |

Vertically integrated companies owning proprietary microbial strains, in-house fermentation, and direct-to-farmer distribution networks are positioned to capture greater value than intermediaries reliant on third-party manufacturing and commodity raw materials.

Technology Landscape in the India Bio Stimulants Industry

Microbial Strain Development and Industrial Fermentation

Advances in high-throughput microbial screening, genomic characterization, and large-scale submerged fermentation are enabling bio stimulant manufacturers to produce consistent, high-viability microbial inoculants at commercially viable costs. Proprietary strain libraries developed under indigenous soil conditions are delivering climate-resilient formulations adapted to India's diverse agro-ecosystems.

Nano-Encapsulation and Controlled-Release Formulation Technology

Nano-encapsulation of bioactive compounds and microbial cells is extending shelf life under ambient storage conditions, enabling distribution to remote markets without unbroken cold-chain infrastructure. Polymer-based slow-release coatings for dry granule formats are improving product performance under variable rainfall and temperature conditions common to Indian dryland farming.

Bioinformatics and Genomic Tools for Product Development

Metagenomics-based soil microbiome analysis and functional gene annotation tools are accelerating identification of novel plant growth-promoting microorganisms. AI-assisted genomic screening is reducing development cycles for next-generation consortia products, enabling manufacturers to address specific crop-soil combination challenges more precisely.

Smart Delivery and Digital Integration

Real-time soil nutrient sensors, IoT-enabled fertigation controllers, and smartphone-based crop advisory apps are creating new touchpoints for bio stimulant recommendation and dosage optimization. Integration of bio stimulant scheduling into precision agriculture platforms is improving product efficacy outcomes and building data-driven evidence for scalable adoption.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Form |

Liquid |

58.3% |

2025 |

|

Origin |

Natural |

69.4% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North India |

29.7% |

2025 |

By Form

Liquid commands 58.3% majority share in 2025, driven by compatibility with drip and micro-sprinkler irrigation systems, rapid foliar and root absorption, ease of dosage adjustment, and seamless incorporation into fertigation schedules in high-value horticulture. The segment benefits from strong adoption in polyhouse vegetables, banana, grapes, and floriculture, where precision water application is standard practice.

To evaluate market opportunities, Request Sample

Dry at 41.7% in 2025 serves rain-fed and dryland cropping systems where liquid application infrastructure is unavailable. Its longer shelf life, lower transportation costs, and suitability for seed treatment and soil application further support adoption across broad-acre crops and traditional farming systems.

By Origin

Natural dominates with 69.4% share in 2025, reflecting strong regulatory preference for organically certifiable inputs, growing export quality requirements limiting synthetic residues, and farmer familiarity with seaweed and plant-extract formulations. The segment is anchored by humic and fulvic acids, seaweed extracts, protein hydrolysates, and microbial inoculants derived from naturally occurring organisms.

Synthetic at 30.6% in 2025 serves commercial operations requiring standardized, reproducible formulations with precisely defined active ingredient concentrations. Synthetic amino acid blends, betaines, and chemically derived plant hormone analogues are preferred in organized commercial floriculture, tissue culture nurseries, and contract farming operations targeting consistent produce quality for processing and export.

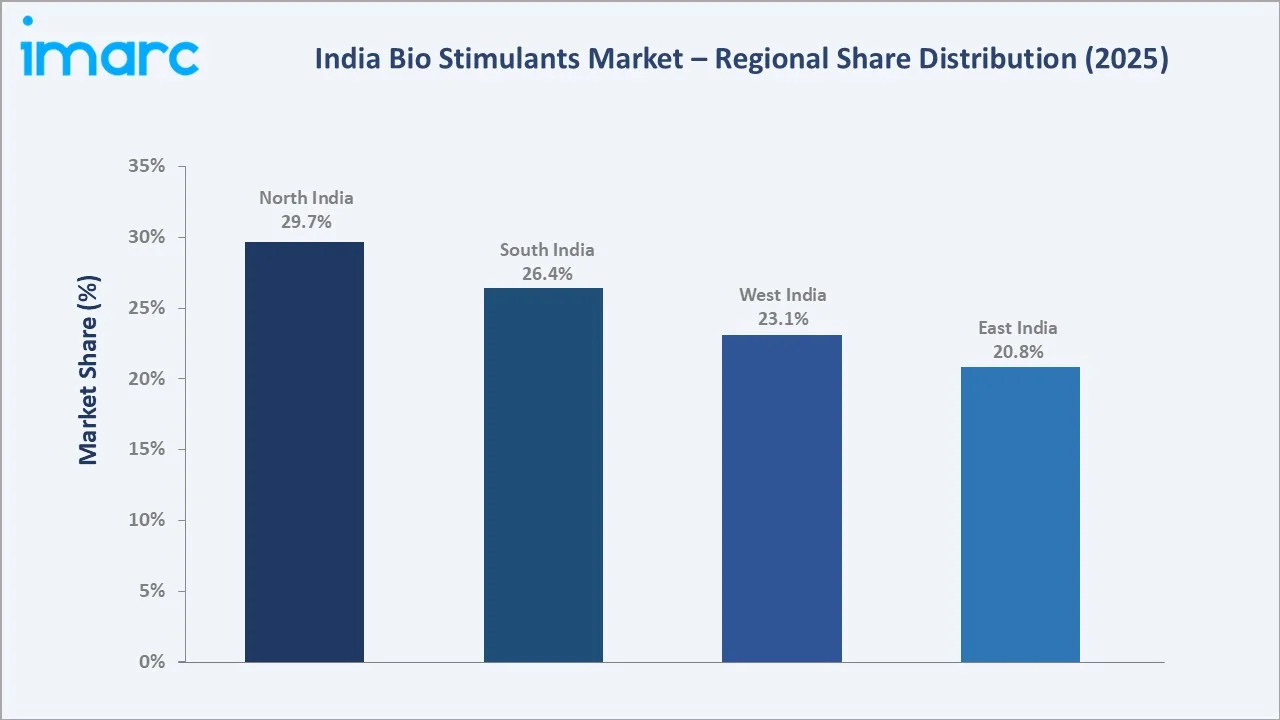

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

29.7% |

Large wheat and paddy cultivation base, strong agri-input distribution networks, government soil health restoration initiatives, and high awareness among organized farming communities |

|

South India |

26.4% |

High-value horticulture and floriculture expansion, export-oriented banana and grape cultivation, strong drip irrigation penetration, and rising bio stimulant adoption in organized contract farming |

|

West India |

23.1% |

Expanding cotton, sugarcane, and onion cultivation, growing organic certification demand, established agri-input retail infrastructure, and increasing polyhouse horticulture investment |

|

East India |

20.8% |

Emerging awareness among rice farming communities, expanding government-sponsored soil health programs, growing demand from tea and jute plantation sectors, and increasing tier-2 agri-input distribution |

North India at 29.7% in 2025 leads the regional landscape, anchored by the Indo-Gangetic Plain's extensive wheat and paddy cultivation, strong presence of organized agri-input distributors in Haryana, Punjab, and Uttar Pradesh, and active implementation of Soil Health Card-driven micronutrient management programs that create awareness and acceptance for bio-based inputs.

South India at 26.4% is the second largest region. Rapid expansion of drip-irrigated horticulture, strong export-compliance requirements for fruits and vegetables, and the presence of well-organized farmer producer organizations in Tamil Nadu, Karnataka, and Andhra Pradesh are accelerating structured bio stimulant adoption through 2034.

Competitive Landscape

The India bio stimulants market is moderately fragmented, with established domestic agri-input conglomerates, dedicated bio stimulant specialists, and multinational crop science firms competing across product, geography, and crop-type dimensions. Product differentiation through proprietary microbial strains, agronomic trial data, regulatory compliance track record, and distribution depth forms the key competitive moat.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

UPL |

Opteine, Bioclassic |

Leader |

Developing and expanding a broad-based biological crop nutrition portfolio to support sustainable yield improvement across diverse cropping systems |

|

Coromandel International Ltd. |

Coromandel, ABDA, CoroShakti |

Leader |

Strengthening farmer reach through an extensive rural retail and distribution network to drive bio stimulant adoption across key agricultural regions |

|

Biostadt |

Biozyme Aaloo+, Biozyme Biocane+ |

Challenger |

Expanding proprietary bio stimulant product range through farmer-centric advisory networks and growing presence in domestic and international markets |

|

Acadian Seaplants Limited |

Stimplex |

Emerging |

Growing local market presence through dedicated manufacturing operations and distribution partnerships to serve farmer demand for seaweed-based bio stimulant solutions |

Key players include UPL, Coromandel International Ltd., Biostadt, and Acadian Seaplants Limited, among others.

Key Company Profiles

UPL

UPL is a global provider of sustainable agricultural products and solutions, headquartered in Mumbai, India. The company offers an integrated portfolio of crop protection, bio stimulants, seed treatments, and post-harvest solutions serving farmers across diverse agro-climatic zones. UPL operates through multiple business platforms and holds one of the largest post-patent agricultural product portfolios worldwide.

- Product Portfolio: Bio stimulant products for foliar and soil application targeting crop nutrition efficiency, abiotic stress tolerance, flowering improvement, and yield enhancement across cereals, horticulture, and cash crop segments in India.

- Recent Development: In May 2026, UPL secured Fertilizer Control Order (FCO) registration in India for Bioclassic, its flagship fermentation-derived biostimulant.

- Strategic Focus: Expanding integrated biological crop nutrition portfolio leveraging pan-India distribution infrastructure across cereal and horticulture segments.

Coromandel International Ltd.

Coromandel International Ltd. is a leading Indian agri-solutions company with diversified operations spanning fertilizers, crop protection, specialty nutrients, organic inputs, and bio products. The company serves farmers across India through an extensive network of retail outlets and dealer channels, offering a broad range of agricultural input solutions for diverse cropping systems.

- Product Portfolio: Proprietary plant-based bio stimulant products developed and patented in-house, targeting soil microflora improvement, nutrient assimilation, and produce quality enhancement for horticultural and field crops across India.

- Recent Development: The company continues to strengthen its bio stimulants portfolio through product innovation, expanded market outreach, and increased farmer engagement initiatives aimed at promoting sustainable crop productivity and improved nutrient-use efficiency across diverse cropping systems.

- Strategic Focus: Leveraging an extensive rural retail network and dedicated bio team capabilities to expand bio stimulant penetration across South and West India through farmer education and integrated crop management advisory.

Biostadt

Biostadt is a diversified agri-inputs company serving the Indian agricultural sector and global markets. With manufacturing facilities across multiple locations in India, the company offers a comprehensive range of products spanning bio stimulants, crop protection chemicals, hybrid seeds, biofertilizers, and aquaculture inputs, with a strategic focus on biological and sustainable solutions for Indian farmers.

- Product Portfolio: Seaweed extract-based bio stimulant products under the Biozyme brand, including crop-specific variants designed for diverse Indian farming conditions, alongside a range of plant growth regulators, microbial products, and specialty crop nutrition inputs.

- Recent Development: The company continues to expand its biological and specialty plant nutrition portfolio through product enhancements, agronomic research initiatives, and broader market penetration efforts aimed at improving crop productivity, stress tolerance, and sustainable farming outcomes across key agricultural regions.

- Strategic Focus: Pioneering the India bio stimulant category with proprietary seaweed-based brands, deepening farmer connect through a dedicated agronomist network, and growing international export presence across multiple countries.

Market Concentration Analysis

The India bio stimulants market is moderately fragmented, with the top five players collectively accounting for an estimated 35-40% of organized market revenue in 2025. The remainder is distributed across a large number of regional and state-level formulators, agri-biotech start-ups, and cooperative-sector producers that serve localized cropping systems and specific agro-climatic niches.

Barriers to entry in the organized segment include the need for regulatory registration across multiple product categories, investment in fermentation or extraction manufacturing capabilities, agronomic field trial data for product efficacy validation, and established distributor relationships in target cropping districts. These factors favor well-capitalized incumbents with diversified portfolios and existing farmer trust.

Consolidation pressures are beginning to emerge as larger agri-input companies acquire niche bio stimulant brands and microbial strain libraries to strengthen their biological inputs portfolio. Strategic investments from domestic agro-chemical multinationals in bio stimulant R&D facilities and start-up acquisitions signal an accelerating shift toward integrated crop nutrition offerings that combine conventional and bio-based inputs under unified brand umbrellas.

Investment & Growth Opportunities

Fastest-Growing Segments

Liquid growing at an estimated 12.4% CAGR through 2034 represents the fastest-growing form segment, driven by drip irrigation expansion, polyhouse horticulture growth, and precision fertigation adoption. South India at an estimated 13.5% CAGR is the fastest growing regional market, anchored by export horticulture and organized contract farming growth.

Emerging Markets

East India at 20.8% share in 2025 represents significant upside potential for bio stimulant market participants. Growing digital agricultural advisory reach, government-supported soil health programs in Odisha, West Bengal, and Jharkhand, and the large rice cultivation base offer addressable entry points for microbial inoculants and seaweed-based products through cooperative and state agri-input channels.

Venture & Investment Trends

Investment is flowing into agri-biotech start-ups focused on proprietary microbial strain discovery, metagenomics-based soil health diagnostics, and digital advisory platforms that bundle bio stimulant recommendations with precision agronomy services. Foreign direct investment in Indian bio stimulant manufacturing has increased through joint ventures and licensing arrangements as multinational crop science companies seek local production capabilities to reduce import costs and meet regulatory indigenization requirements.

Future Market Outlook (2026-2034)

The India bio stimulants market is forecast to expand from USD 120.7 Million in 2025 to USD 319.7 Million by 2034 at a CAGR of 11.09%, adding approximately USD 199 Million in incremental annual market value over the forecast period. By 2030, the market is projected to reach USD 204.2 Million, representing a key milestone in transition from specialty to mainstream agri-input category.

Three structural forces will define the market through 2034: a maturing dedicated regulatory framework creating clarity for new product entry; deepening integration of bio stimulants with precision agriculture, digital advisory, and fertigation ecosystems; and rising export quality standards in Indian agriculture creating non-negotiable demand for residue-compliant bio-based inputs. These dynamics will drive both volume growth and premiumization of bio stimulant product portfolios.

By 2034, the India bio stimulants industry is expected to be defined by science-backed, trial-validated formulations tailored to specific Indian crop-soil combinations, with organized distribution channels, digital farmer advisory integration, and transparent efficacy documentation forming the competitive baseline for all market participants.

Research Methodology

Primary Research

Primary research included structured interviews with bio stimulant manufacturers, agri-input distributors, agronomy experts, export-oriented grower representatives, and regulatory specialists, validating market sizing, regional demand patterns, segment mix evolution, and technology adoption trends across India's diverse agro-climatic zones.

Secondary Research

Secondary sources included publications from the Ministry of Agriculture and Farmers' Welfare, Directorate of Plant Protection Quarantine and Storage, ICAR research journals, state agriculture department reports, Soil Health Card mission documents, export-import data from APEDA, and annual reports, press releases, and investor presentations from listed agri-input companies.

Forecasting Models

Market forecasts used top-down and bottom-up models combining crop acreage data, bio stimulant penetration rates by crop category, product price evolution, segment mix shifts, regulatory transition scenarios, and macroeconomic agricultural investment variables. Scenario analysis addressed regulatory framework pace, organic certification growth, and export demand evolution through 2034.

India Bio Stimulants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Crop Types Covered | Cereals and Grains, Fruits and Vegetables, Turf and Ornamentals, Oilseeds and Pulses, Others |

| Forms Covered | Dry, Liquid |

| Origins Covered | Natural, Synthetic |

| Distribution Channels Covered | Direct, Indirect |

| Applications Covered | Foliar Treatment, Soil Treatment, Seed Treatment |

| End Users Covered | Farmers, Research Organizations, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | UPL, Coromandel International Ltd., Biostadt, Acadian Seaplants Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India bio stimulants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India bio stimulants market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India bio stimulants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Bio Stimulants Market Report

The India bio stimulants market was valued at USD 120.7 Million in 2025, driven by growing organic farming adoption, soil health initiatives, and rising demand for crop yield optimization across diverse Indian agro-climatic zones.

The market is projected to grow at a CAGR of 11.09% from 2026 to 2034, reaching USD 319.7 Million, supported by expanding drip irrigation adoption, rising export quality requirements, and favorable government agri-input policies.

Liquid leads at 58.3% in 2025, driven by fertigation compatibility, faster plant absorption, and widespread adoption in drip-irrigated horticulture.

Natural dominates at 69.4% in 2025, anchored by regulatory preference for organic inputs, export residue compliance requirements, and growing farmer familiarity with seaweed and microbial formulations.

North India commands 29.7% in 2025, led by extensive wheat and paddy cultivation, strong agri-input distribution networks, and active soil health restoration programs in Haryana, Punjab, and Uttar Pradesh.

Leading players include UPL, Coromandel International Ltd., Biostadt, and Acadian Seaplants Limited, among others.

Key drivers include growing organic farming mandates, soil health deterioration, rising crop yield pressures, government subsidy programs for bio inputs, and export quality standards limiting synthetic agrochemical residues in horticultural produce.

High production costs relative to conventional inputs, limited farmer awareness in rain-fed regions, and proliferation of substandard products in unorganized markets are the primary restraints.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)