India Biosimilar Market Size, Share, Trends and Forecast by Molecule, Indication, Manufacturing Type, and Region, 2026-2034

India Biosimilar Market Summary:

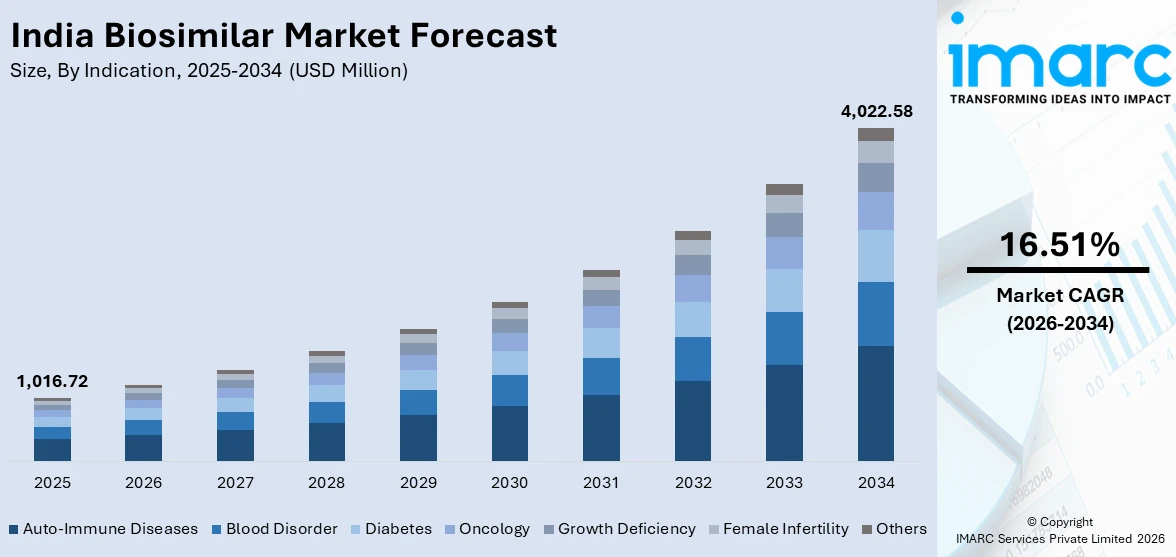

The India biosimilar market size was valued at USD 1,016.72 Million in 2025 and is projected to reach USD 4,022.58 Million by 2034, growing at a compound annual growth rate of 16.51% from 2026-2034.

The India biosimilar market is advancing rapidly as the country strengthens its position as a leading global hub for affordable biologic therapies. Rising prevalence of chronic and autoimmune diseases, supportive government policies, and expanding manufacturing capabilities are accelerating domestic demand. Patent expirations of blockbuster biologics, the growing physician acceptance, and strategic investments in research and development (R&D) are further reshaping the competitive landscape and creating substantial opportunities for market participants.

Key Takeaways and Insights:

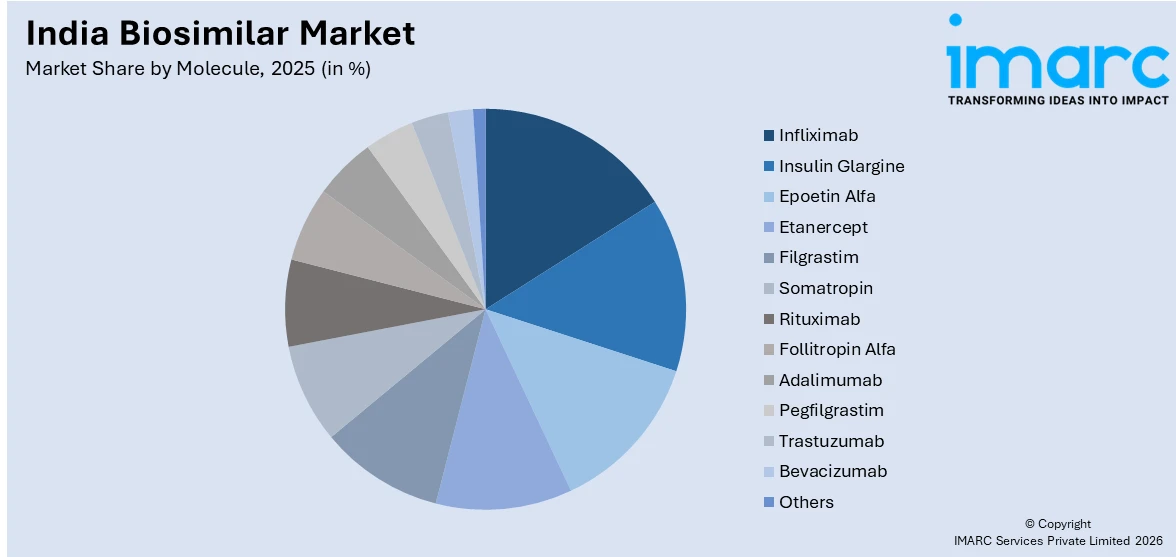

- By Molecule: Infliximab represents the largest segment with a market share of 14% in 2025, driven by widespread adoption in treating autoimmune conditions, such as rheumatoid arthritis, Crohn’s disease, and ulcerative colitis across, India’s expanding patient population.

- By Indication: Auto-immune diseases lead the market with a share of 25% in 2025, owing to the rising burden of conditions like rheumatoid arthritis, psoriasis, and inflammatory bowel disease requiring long-term biologic therapies.

- By Manufacturing Type: In-house manufacturing dominates the market with a share of 63% in 2025, reflecting the vertically integrated capabilities of domestic pharmaceutical companies investing in end-to-end biologics production infrastructure.

- By Region: North India represents the largest segment with a market share of 30% in 2025, supported by concentrated healthcare infrastructure, higher diagnostic rates, and the presence of major pharmaceutical distribution networks across key metropolitan centers.

- Key Players: The India biosimilar market features a dynamic competitive landscape with established domestic biopharmaceutical companies and global players investing in biosimilar development, manufacturing expansion, and strategic partnerships to capture growing market opportunities.

To get more information on this market Request Sample

The India biosimilar market is driven by rising prevalence of chronic and life-threatening diseases, increasing demand for affordable biologic therapies, and strong domestic manufacturing capabilities. The growing incidence of cancer, diabetes, autoimmune disorders, and renal diseases are significantly driving the need for long-term biologic treatment, creating opportunities for lower-cost biosimilar alternatives. Supportive regulatory frameworks and government initiatives promoting biomanufacturing and self-reliance further encourage investment in research, development, and production infrastructure. Expanding healthcare access, improving insurance penetration, and growth of multispecialty hospitals also contribute to higher adoption rates. Strategic collaborations, licensing agreements, and portfolio expansion into oncology, endocrinology, and immunology segments strengthen commercialization and market reach. Additionally, competitive pricing strategies enhance patient affordability and treatment adherence. For instance, in 2025, Zydus Lifesciences launched its Denosumab biosimilar ‘Zyrifa’ in India for preventing skeletal complications in cancer patients, referencing Amgen’s Xgeva, and priced it at Rs 12,495 to enhance affordability.

India Biosimilar Market Trends:

Expansion of Oncology Biosimilars Improving Treatment Access

The growing introduction of oncology-focused biosimilars is significantly influencing the India biosimilar market, as cancer therapies remain among the most expensive biologic treatments. The rising availability of cost-effective alternatives is improving patient access to critical medicines while increasing competition in high-value therapeutic categories. Biosimilars are helping reduce the financial burden associated with advanced oncology care and enabling broader treatment coverage across healthcare settings. In 2025, Alkem Laboratories launched its breast cancer biosimilar ‘Pertuza’ in India as an alternative to Roche’s Perjeta (pertuzumab), developed by Enzene Biosciences for HER2-positive breast cancer. Such developments highlight the growing momentum of biosimilar adoption in India.

Affordable Biosimilars Enhancing Access

The introduction of cost-effective biosimilars for chronic diseases is a crucial factor influencing the India biosimilar market by improving treatment affordability and expanding patient access. For instance, chronic condition like diabetes management requires sustained pharmacological intervention, often creating a significant long-term financial burden for patients. To address this challenge, manufacturers are increasingly developing biosimilar alternatives that reduce therapy costs while maintaining clinical effectiveness. In 2024, Glenmark Pharmaceuticals launched Lirafit™, India’s first biosimilar of liraglutide, approved by the Drug Controller General of India for type 2 diabetes treatment. The product was expected to reduce therapy costs by nearly 70%. Such pricing strategies enhance accessibility, support adherence, and accelerate biosimilar adoption.

Strategic Partnerships Accelerating Biosimilar Commercialization

Collaborations and licensing agreements among leading pharmaceutical companies are bolstering the growth of the India biosimilar market by strengthening commercialization reach and improving access to advanced therapies. Partnerships allow companies to combine development expertise with strong distribution networks, ensuring wider availability of critical biosimilars. In 2025, Zydus Lifesciences and Dr. Reddy’s Laboratories entered a licensing agreement to co-market a pertuzumab biosimilar for HER2-positive breast cancer in India. Developed by Zydus Research Centre, the product will be sold as Sigrima by Zydus and Womab by Dr. Reddy’s under semi-exclusive rights. Such alliances support broader patient access to essential oncology combination treatments.

Market Outlook 2026-2034:

The India biosimilar market shows strong growth potential over the forecast period, driven by the rising burden of chronic diseases, increasing demand for affordable biologic therapies, and a wave of patent expirations for major biologic drugs. Government initiatives promoting domestic biopharmaceutical manufacturing and investment in advanced R&D infrastructure are further supporting market expansion. The market generated a revenue of USD 1,016.72 Million in 2025 and is projected to reach a revenue of USD 4,022.58 Million by 2034, growing at a compound annual growth rate of 16.51% from 2026-2034.

India Biosimilar Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Molecule |

Infliximab |

14% |

|

Indication |

Auto-Immune Diseases |

25% |

|

Manufacturing Type |

In-house Manufacturing |

63% |

|

Region |

North India |

30% |

Molecule Insights:

Access the comprehensive market breakdown Request Sample

- Infliximab

- Insulin Glargine

- Epoetin Alfa

- Etanercept

- Filgrastim

- Somatropin

- Rituximab

- Follitropin Alfa

- Adalimumab

- Pegfilgrastim

- Trastuzumab

- Bevacizumab

- Others

Infliximab dominates with a market share of 14% of the total India biosimilar market in 2025.

Infliximab, a chimeric anti-tumor necrosis factor monoclonal antibody, has established itself as a cornerstone therapy for managing chronic autoimmune and inflammatory conditions in India. The molecule is widely prescribed for treating rheumatoid arthritis, Crohn’s disease, ulcerative colitis, ankylosing spondylitis, psoriatic arthritis, and plaque psoriasis. The growing prevalence of inflammatory bowel disease and related autoimmune conditions across India’s expanding population is catalyzing the demand for infliximab biosimilars, which offer cost-effective alternatives to the originator biologic Remicade.

The segment’s market leadership is further strengthened by the growing acceptance of biosimilar switching among Indian physicians and healthcare providers, reflecting rising confidence in comparable efficacy and safety. Increased clinical experience and supportive regulatory frameworks are encouraging wider adoption in hospital and specialty care settings. Indian manufacturers are simultaneously advancing improved infliximab formulations to address evolving patient needs and enhance treatment convenience. Demand continues to rise due to higher autoimmune disease diagnosis rates and expanding insurance penetration, particularly across tier-two and tier-three cities, where access to affordable biologic therapies is steadily improving.

Indication Insights:

- Auto-Immune Diseases

- Blood Disorder

- Diabetes

- Oncology

- Growth Deficiency

- Female Infertility

- Others

Auto-immune diseases lead with a market share of 25% of the total India biosimilar market in 2025.

Auto-immune diseases represent the largest segment due to the high and rising burden of chronic inflammatory conditions, such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease. These disorders require long-term biologic therapy, making treatment costs a major concern for patients and healthcare providers. Biosimilars offer more affordable alternatives to originator biologics, improving access across both urban and semi-urban populations. Government support for biosimilar adoption and expanding insurance coverage also contribute to stronger demand in this segment.

Another reason auto-immune diseases dominate is the strong clinical acceptance of biosimilars in immunology, supported by increasing physician confidence and regulatory approvals. Many leading biosimilar products in India target tumor necrosis factor inhibitors and other key immune pathways, which are widely prescribed for these conditions. In addition, hospitals and specialty clinics actively promote biosimilars to manage therapy expenses without compromising outcomes. The presence of domestic manufacturers and competitive pricing further accelerates uptake in auto-immune indications nationwide.

Manufacturing Type Insights:

- In-house Manufacturing

- Contract Manufacturing

In-house manufacturing exhibits a clear dominance with a 63% share of the total India biosimilar market in 2025.

In-house manufacturing holds the biggest share in the market owing to the strong capabilities of domestic biopharmaceutical companies and their focus on end-to-end production control. By producing biosimilars internally, firms can ensure consistent quality, regulatory compliance, and cost efficiency across the value chain. This approach also reduces dependence on third-party contractors, helping companies maintain better oversight of complex biologic processes. With the increasing demand for affordable biologics, in-house facilities enable faster scaling and improved supply stability within the country.

Another key driver is the significant investment made by Indian manufacturers in advanced bioprocessing infrastructure, including fermentation, purification, and fill-finish operations. In-house production supports innovation, quicker development timelines, and the ability to customize manufacturing for diverse therapeutic areas. It also strengthens competitiveness in both domestic and export markets by meeting global quality standards. Additionally, government initiatives promoting local production and self-reliance in pharmaceuticals encourage companies to expand internal manufacturing, contributing to the dominance of this segment.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India dominates with a market share of 30% of the total India biosimilar market in 2025.

North India leads the market driven by strong concentration of pharmaceutical manufacturing hubs, research facilities, and major healthcare institutions. States, such as Delhi, Haryana, Punjab, and Uttar Pradesh, have well-developed medical infrastructure and a high presence of specialty hospitals that actively prescribe biosimilars. The region also has a large patient pool suffering from chronic diseases, including cancer and autoimmune disorders, driving the demand for cost-effective biologic therapies. Better access to advanced treatment centers supports faster biosimilar adoption. The data provided by the Indian Council of Medical Research (ICMR), published in The Journal of the American Medical Association (JAMA), which stated India recorded an estimated 1.56 million new cancer cases in 2024, highlighting the rising need for affordable biologic therapies.

Another factor behind North India’s dominance is the strong distribution network and presence of leading domestic biosimilar manufacturers headquartered or operating major facilities in this region. Proximity to regulatory bodies, skilled workforce availability, and established supply chains further support the market growth. In addition, higher awareness among physicians and patients about biosimilar benefits contributes to stronger uptake. Government healthcare programs and private sector investment in tertiary care hospitals across North India also play an important role in boosting biosimilar penetration.

Market Dynamics:

Growth Drivers:

Why is the India Biosimilar Market Growing?

Supportive Regulatory Framework and Policy Initiatives

India’s strengthening regulatory and policy environment continues to bolster the growth of the biosimilar market by fostering innovation, investment, and manufacturing expansion. Clear approval pathways, defined comparability standards, and structured clinical evaluation requirements are enhancing confidence in domestically developed biosimilars while maintaining safety and efficacy benchmarks. In 2024, the Union Cabinet approved the BioE3 Policy to promote high-performance biomanufacturing, emphasizing innovation-led research, entrepreneurship, and the establishment of biomanufacturing and Bio-AI hubs. This initiative supported sustainable bioeconomy models and skilled workforce development, reinforcing India’s biotechnology capabilities. Combined with government support for affordable healthcare and quality compliance aligned with global standards, such measures create a supportive ecosystem for sustained biosimilar growth.

Strong Domestic Manufacturing Capabilities and Cost Advantage

India’s established pharmaceutical manufacturing ecosystem provides a strong competitive edge in biosimilar production through advanced biologics expertise, skilled scientific talent, and cost-efficient large-scale operations. Integrated capabilities across research, development, and manufacturing help companies maintain quality while managing production costs effectively. This strength is reflected in India’s broader pharmaceutical scale, as per IBEF data showing the country holds over 20% of global pharmaceutical export volume and supplies more than 60% of vaccines manufactured worldwide. In FY25, the Indian pharmaceutical industry was valued at INR 4,71,075 Crore (USD 55 Billion), supporting continued investment in bioprocessing infrastructure. Such scale and efficiency reinforce India’s position as a reliable biosimilar manufacturing hub.

Rising Burden of Chronic and Life-Threatening Diseases

The growing prevalence of chronic and life-threatening diseases in India is a primary factor influencing the biosimilar market. Conditions, such as autoimmune disorders, diabetes, and chronic kidney disease, require long-term biologic therapies, which are often expensive and financially burdensome for patients. This prevalence is supported by the data provided by the International Diabetes Federation, which stated that India’s adult population with diabetes reached 89.8 million in 2024. As disease incidence continues to rise due to demographic shifts, urbanization, and lifestyle changes, there is an increase in the demand for cost-effective therapeutic alternatives. Biosimilars provide clinically comparable efficacy to reference biologics at reduced costs, enabling broader patient access to advanced treatments.

Market Restraints:

What Challenges the India Biosimilar Market is Facing?

Complex Development and Manufacturing Requirements Constraining New Market Entrants

Biosimilar development demands sophisticated analytical characterization, extensive clinical evaluation, and specialized biomanufacturing infrastructure that create significant barriers for new market participants. The complexity of producing biologic molecules from living organisms requires substantial capital investment in advanced bioprocessing equipment, quality control systems, and specialized scientific talent, limiting market entry to well-resourced pharmaceutical companies.

Physician Hesitancy and Limited Biosimilar Awareness Impeding Adoption Rates

Despite the growing evidence supporting biosimilar safety and efficacy, physician hesitancy regarding biosimilar switching and limited awareness among healthcare professionals in smaller cities and rural areas continue to constrain market penetration. Inadequate educational initiatives and lingering concerns about immunogenicity differences between biosimilars and reference biologics contribute to slower adoption rates in certain therapeutic segments.

Pricing Pressures and Reimbursement Challenges Affecting Market Profitability

Intense price competition among domestic biosimilar manufacturers combined with limited insurance coverage for biologic therapies in India’s healthcare system creates margin pressures that may discourage continued investment in biosimilar development. The absence of comprehensive reimbursement frameworks for biosimilars across government and private insurance programs constrains patient access and limits revenue potential for manufacturers.

Competitive Landscape:

The India biosimilar market features an increasingly competitive landscape characterized by vertically integrated domestic biopharmaceutical companies competing alongside global manufacturers across diverse therapeutic segments. Market participants are differentiating through comprehensive product portfolios spanning oncology, immunology, diabetology, and ophthalmology, while investing in advanced manufacturing capabilities and international regulatory approvals to strengthen competitive positioning. Strategic partnerships, licensing agreements, and technology collaborations between Indian and global companies are intensifying as manufacturers seek to expand pipeline depth and accelerate market entry across both domestic and international markets, creating a dynamic competitive environment that rewards innovation and operational excellence.

Recent Developments:

- February 2026: The Government of India announced under Union Budget 2026–27 the launch of the Biopharma SHAKTI initiative with an outlay of ₹10,000 crore over five years. The scheme aims to strengthen India’s end-to-end ecosystem for biologics and biosimilars through investments in research, manufacturing, clinical trial infrastructure, and regulatory capacity.

- January 2026: Zydus Lifesciences launched Tishtha, the world’s first biosimilar of nivolumab, in India to improve affordability of cancer treatment. The biosimilar, used for multiple oncology indications, is priced at nearly one-fourth the cost of Bristol Myers Squibb’s innovator drug Opdivo. The launch was enabled after a Delhi High Court verdict cleared Zydus to market the biosimilar ahead of the patent expiry in May 2026.

India Biosimilar Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Molecules Covered | Infliximab, Insulin Glargine, Epoetin Alfa, Etanercept, Filgrastim, Somatropin, Rituximab, Follitropin Alfa, Adalimumab, Pegfilgrastim, Trastuzumab, Bevacizumab, Others |

| Indications Covered | Auto-Immune Diseases, Blood Disorder, Diabetes, Oncology, Growth Deficiency, Female Infertility, Others |

| Manufacturing Types Covered | In-house Manufacturing, Contract Manufacturing |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Biosimilar Market Report

The India biosimilar market size was valued at USD 1,016.72 Million in 2025.

The India biosimilar market is expected to grow at a compound annual growth rate of 16.51% from 2026-2034 to reach USD 4,022.58 Million by 2034.

Infliximab leads the India biosimilar market with 14% revenue share in 2025, driven by widespread adoption in treating autoimmune conditions including rheumatoid arthritis, Crohn’s disease, and ulcerative colitis.

Key factors driving the India biosimilar market include the rising introduction of oncology-focused biosimilars that reduce the cost burden of expensive cancer biologics and improve access to advanced treatments. In 2025, Alkem Laboratories launched the breast cancer biosimilar ‘Pertuza’ as an alternative to Roche’s Perjeta, strengthening affordability and accelerating adoption.

Major challenges include complex development and manufacturing requirements constraining new entrants, physician hesitancy and limited biosimilar awareness in smaller cities, pricing pressures from intense domestic competition, limited insurance reimbursement frameworks, and regulatory complexities associated with demonstrating biosimilarity for complex biologic molecules.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade