India Book Market Size, Share, Trends and Forecast by Type, Format, Distribution Channel, and Region, 2026-2034

India Book Market Size, Share, Trends & Forecast (2026-2034)

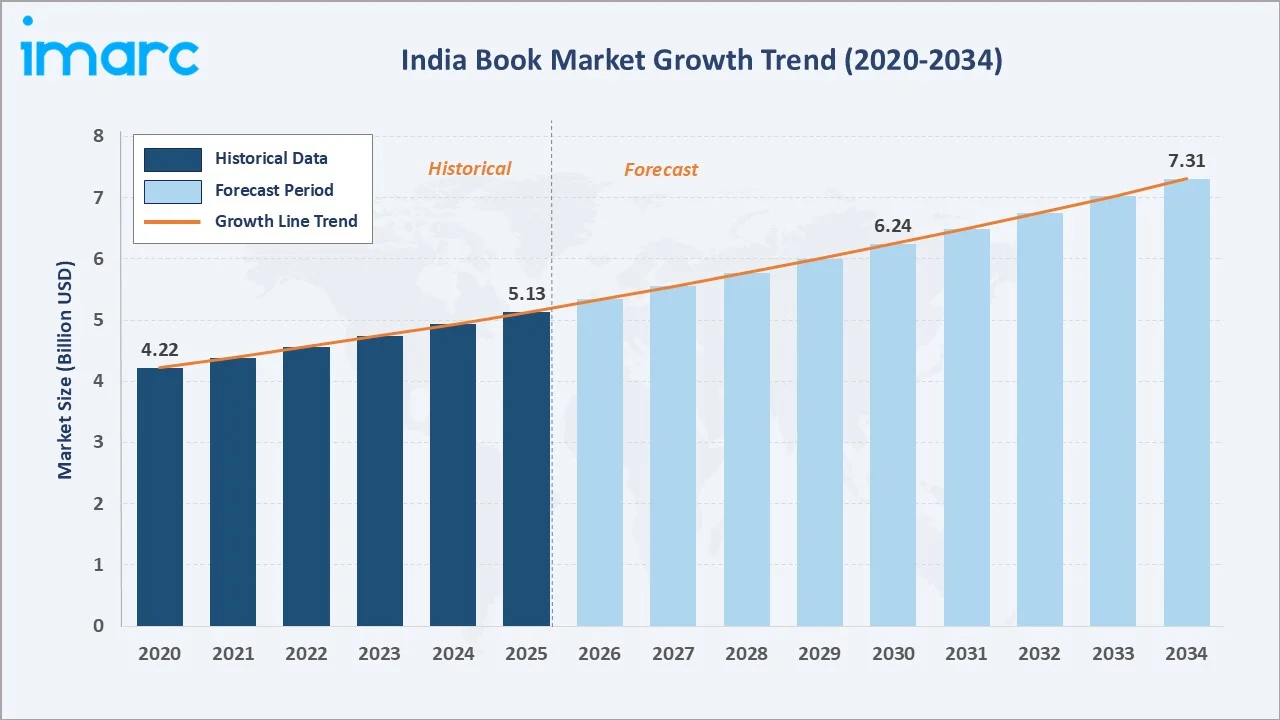

The India book market reached USD 5.13 Billion in 2025 and is projected to reach USD 7.31 Billion by 2034, growing at a CAGR of 4.00% during 2026-2034. India is the world's second-largest publisher of English-language books and one of the fastest-growing reading economies globally, supported by 1.4 billion people, a literacy rate improving toward 80%, 958 million active internet users accelerating digital reading adoption, and the government's transformative National Education Policy (NEP) 2020 mandate reshaping curriculum requirements.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.13 Billion |

|

Forecast Market Size (2034) |

USD 7.31 Billion |

|

CAGR (2026-2034) |

4.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

North India leads regionally with a 31.7% market share in 2025, anchored by Delhi NCR's status as India's publishing capital and the region's dense educational institution concentration. Educational books command 34.8% share of the type segment, while hard copy retains the largest format share at 72.6%.

To get more information on this market, Request Sample

The India book market is structurally supported by three enduring forces: the world's largest school-age population creating non-discretionary educational book demand; India's literary renaissance, with authors like Amish Tripathi, Chetan Bhagat, and Sudha Murthy, building 10 million+ readerships that sustain commercial fiction growth even during economic downturns; and the rapid democratization of reading through Kindle, Storytel, Audible India, and regional language e-book platforms that are creating entirely new readership cohorts among smartphone-enabled younger consumers.

Executive Summary

The India book market is experiencing consistent, broad-based expansion supported by rising literacy, education sector growth, and digital format adoption. The market reached USD 5.13 Billion in 2025 and is forecast to reach USD 7.31 Billion by 2034, growing at a CAGR of 4.00%. India's reading market is characterized by extraordinary diversity, a thriving commercial trade publishing ecosystem, and a rapidly growing digital reading infrastructure encompassing e-books, audiobooks, and serialized fiction apps.

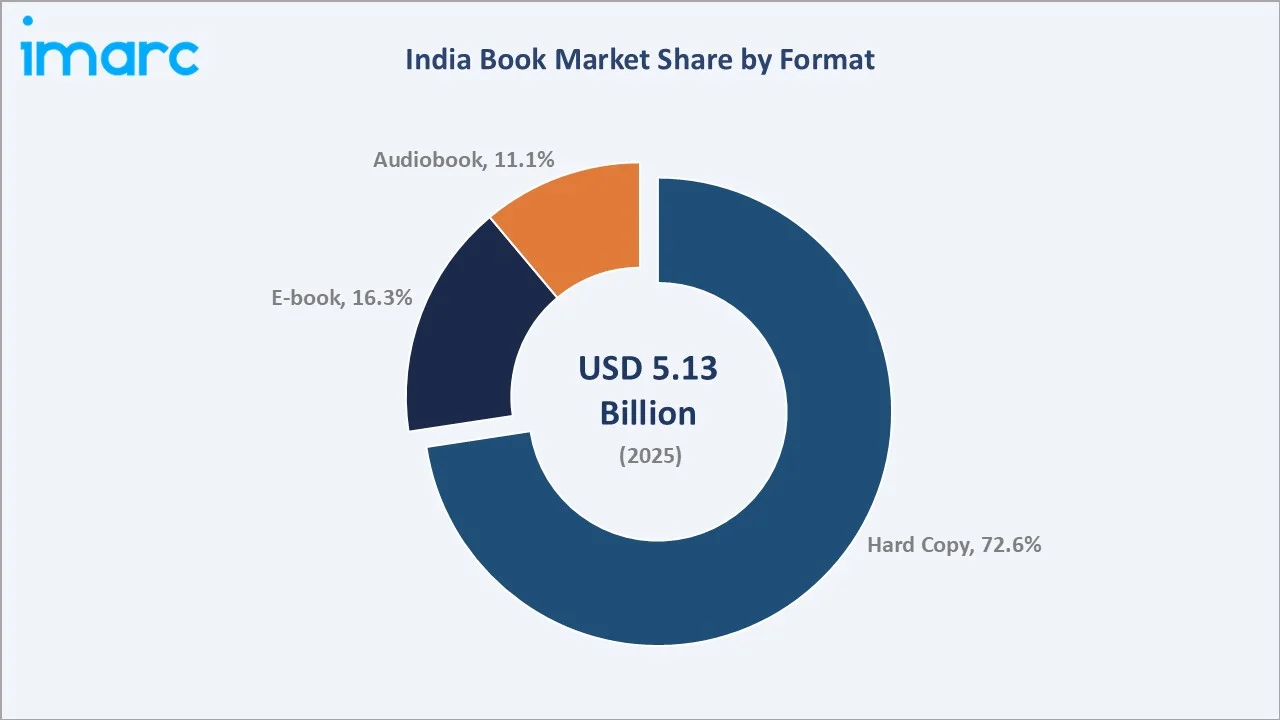

Hard copy books dominate format share at 72.6% in 2025, reflecting India's preference for physical books across educational institutions, competitive exam preparation, gifting occasions, and literary reading. However, digital formats are growing rapidly: e-books at 16.3% and audiobooks at 11.1% are collectively expanding at a 9–12% CAGR as Kindle Unlimited, Storytel, Audible India, and regional language platforms reach first-time digital readers.

Educational books lead the type segment at 34.8%, driven by NEP 2020's curriculum transformation and India's 24.69 crore student population. Leading vendors collectively represent India's most vibrant publishing ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Educational – 34.8% share (2025) |

|

Fastest Growing Type |

Science – ~5.8% CAGR (2026-2034) |

|

Largest Format |

Hard Copy – 72.6% share (2025) |

|

Fastest Growing Format |

Audiobook – ~12.4% CAGR (2026-2034) |

|

Leading Region |

North India – 31.7% share (2025) |

|

Top Companies |

Penguin Random House LLC, HarperCollins Publishers, S Chand And Company Limited, Arihant Publications India Limited |

Key Analytical Observations Supporting the Above Data:

- Educational books at 34.8% (2025) dominate as India's 24.69 crore student population creates non-discretionary book demand that is structurally insulated from consumer spending cycles. NEP 2020's shift from rote learning to competency-based education is driving the replacement of entire textbook inventories across 14.71 lakh schools, creating a multi-year procurement wave that sustains educational publishing growth.

- Hard Copy at 72.6% (2025) leads format share as India's book gifting culture, institutional procurement for libraries and schools, competitive exam preparation requirements, and the reading preferences of 550 million non-smartphone users collectively sustain strong physical book demand.

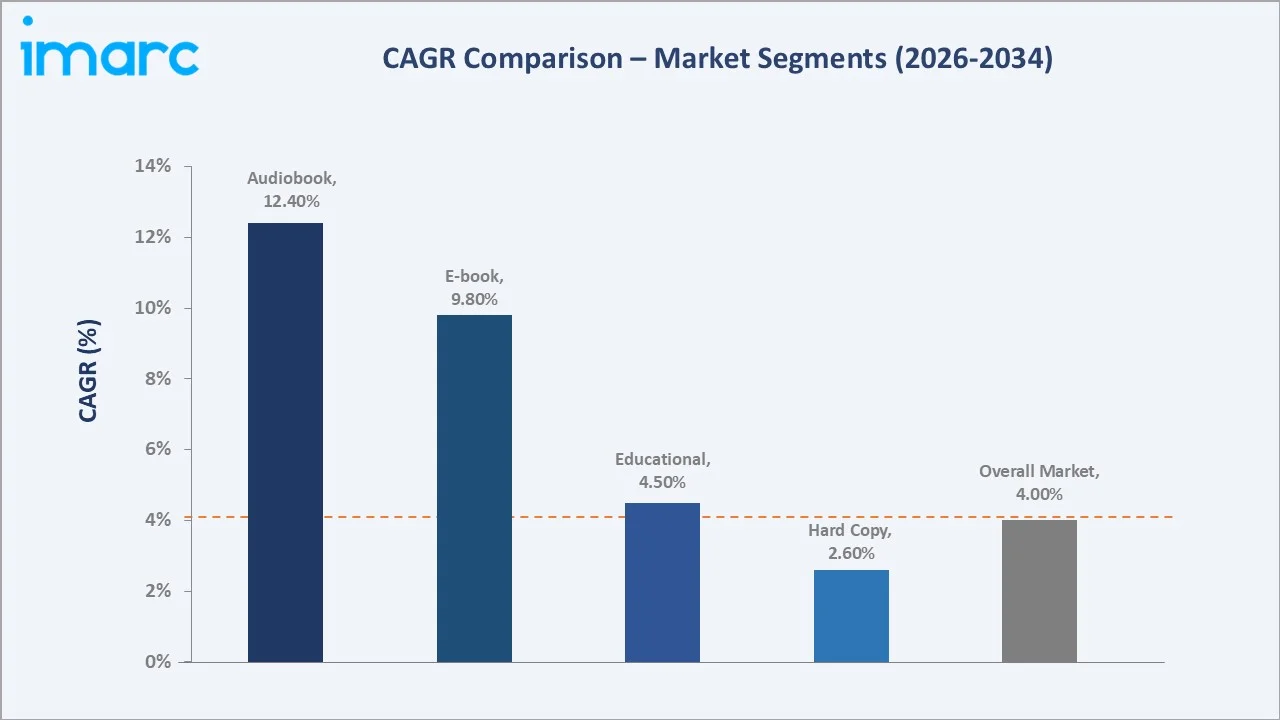

- Audiobooks’ 11.1% share (2025) is expected to grow fastest at ~12.4% CAGR, driven by India's 500 million smartphone users who are adopting audio content consumption during commuting, exercise, and multitasking occasions where visual reading is impractical.

- North India's 31.7% share (2025) reflects Delhi's position as India's publishing capital combined with the region's high educational institution density, competitive exam preparation culture (UPSC, SSC, Banking), and India's largest annual book fair, driving book discovery and sales.

India Book Market Overview

India's book market encompasses the full spectrum of physical and digital reading content: textbooks and academic books for school and university education; competitive exam preparation books for UPSC, JEE, NEET, and banking exams; trade fiction spanning Indian mythology, romance, mystery, fantasy, and literary fiction; non-fiction including business, self-help, biography, and history; children's books; regional language publications; and digital formats including e-books, audiobooks, and serialized fiction apps.

The macroeconomic foundation of India's book market is the government's education investment imperative: the Union Ministry of Education has been allocated INR 1,39,289 crore for 2026-27, marking a 14% increase over the revised estimates for 2025-26. Broadband connections increased from 6.1 crore in March 2014 to 94.92 crore in August 2024, representing a growth of 1,452%, enabling e-book and audiobook adoption at an unprecedented scale.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Literacy Rates and Education Enrolment: The Ministry of Education announced that India’s literacy rate increased to 80.9% in 2023-24, up from 74% in 2011, adding 80+ million new literate consumers to the book market every decade. Gross Enrolment Ratio improvements are increasing school enrolment at all levels, directly expanding the educational book procurement market.

- Digital Publishing and E-book Adoption: Amazon Kindle Unlimited's India subscription has democratized premium English reading access for India's urban middle class. Google Play Books and Apple Books' regional language content expansion is creating first-time digital reading experiences for regional language consumers.

- Growing Youth Reading Culture and Book Clubs: India's 377 million Gen Z and Millennial population is driving a reading renaissance, including bookstagram accounts and WhatsApp book clubs. This is creating peer-driven book discovery that is expanding reading habits among young urban consumers.

- Government NEP 2020 Curriculum Expansion: The National Education Policy 2020's mandate for multidisciplinary education, vocational training integration, mother tongue instruction until Grade 5, and three-language formula implementation requires entirely new textbook content across India's educational system.

Market Restraints

- Piracy and Illegal Content Distribution: Digital book piracy through Telegram channels, illegal PDF sharing platforms, and unauthorized e-book distribution websites represents a significant revenue leakage for India's publishing ecosystem. Major publishers have filed copyright infringement notices against hundreds of piracy operations, but enforcement challenges in digital channels persist.

- Competition from OTT Platforms and Social Media: India's 500-600 million OTT users are competing for the leisure time that could otherwise be spent reading, a competition intensified by social media's infinite scroll consumption model. Publishers must increasingly compete against audiovisual entertainment for discretionary reading time, particularly among the 18–35 demographic.

- Rising Print and Paper Production Costs: Global paper price increases of 25–40% between 2021 and 2023, combined with ink and printing plate cost inflation, have increased physical book production costs by 20–35% over the past three years. Publishers face structural tension between absorbing these cost increases to maintain competitive retail pricing and passing them through in higher cover prices that risk volume loss in India.

Market Opportunities

- Regional Language Publishing Expansion: India's 22 scheduled languages represent 900+ million readers, yet regional language publishing accounts for only 35% of India's total book market value despite representing the majority of the population. Regional language digital reading platforms are creating first-time digital reading behaviors among Hindi, Tamil, Telugu, Marathi, Bengali, and Gujarati readers.

- Subscription Reading Models: Storytel India's monthly subscription, Amazon Kindle Unlimited, and emerging Indian platforms, including Kuku FM, are establishing subscription reading as a growing revenue stream for India's book market. Publishers partnering with subscription platforms secure predictable monthly revenue from a growing subscriber base while reaching consumers who would not purchase individual titles at full price.

Market Challenges

- Author Discoverability and Long-Tail Publishing Economics: India publishes ~90,000 titles annually, creating a discoverability challenge where publishers, retailers, and readers struggle to identify relevant new titles from an overwhelming volume of new releases. The long tail of Indian publishing generates significant content volume but limited commercial visibility, creating a two-tier market where a small number of bestselling titles capture disproportionate revenue.

- Author Compensation and Rights Management: India's traditional publishing royalty structure is facing pressure from self-publishing platforms, creating talent competition for commercially viable authors who can reach audiences independently. Publishers must increasingly invest in author development, marketing support, and rights management services to justify traditional publishing partnerships.

Emerging Market Trends

.webp)

1. New Delhi World Book Fair 2026 and Government Publishing Investment

In January 2026, the Publications Division announced its participation in the New Delhi World Book Fair 2026, showcasing books on art, culture, history, and Gandhian literature, alongside journals including Yojana, Kurukshetra, Aajkal, and Bal Bharati . The New Delhi World Book Fair, hosted at Pragati Maidan with 1,000+ publishers from over 35 countries, serves as India's most significant annual book discovery and rights trading event that brings Indian literature to global publishers.

2. Audiobook Platform Scaling Through Regional Language Content

Kuku FM has emerged as a major audiobook distribution channel by pioneering regional language audiobooks and original audio series in Hindi, Tamil, Telugu, Marathi, and Bengali. The platform's strategy of commissioning original audio content from regional language authors is creating new reading behaviors among the non-English smartphone users who represent India's largest underpenetrated book market.

3. Government Initiatives for Library Development and Book Accessibility

The National Education Policy (NEP) 2020 emphasizes the development of high-quality, engaging learning materials in Indian and local languages to improve educational outcomes. It also promotes wider availability and accessibility of books through schools and public libraries, ensuring inclusive access for all learners, including persons with disabilities.

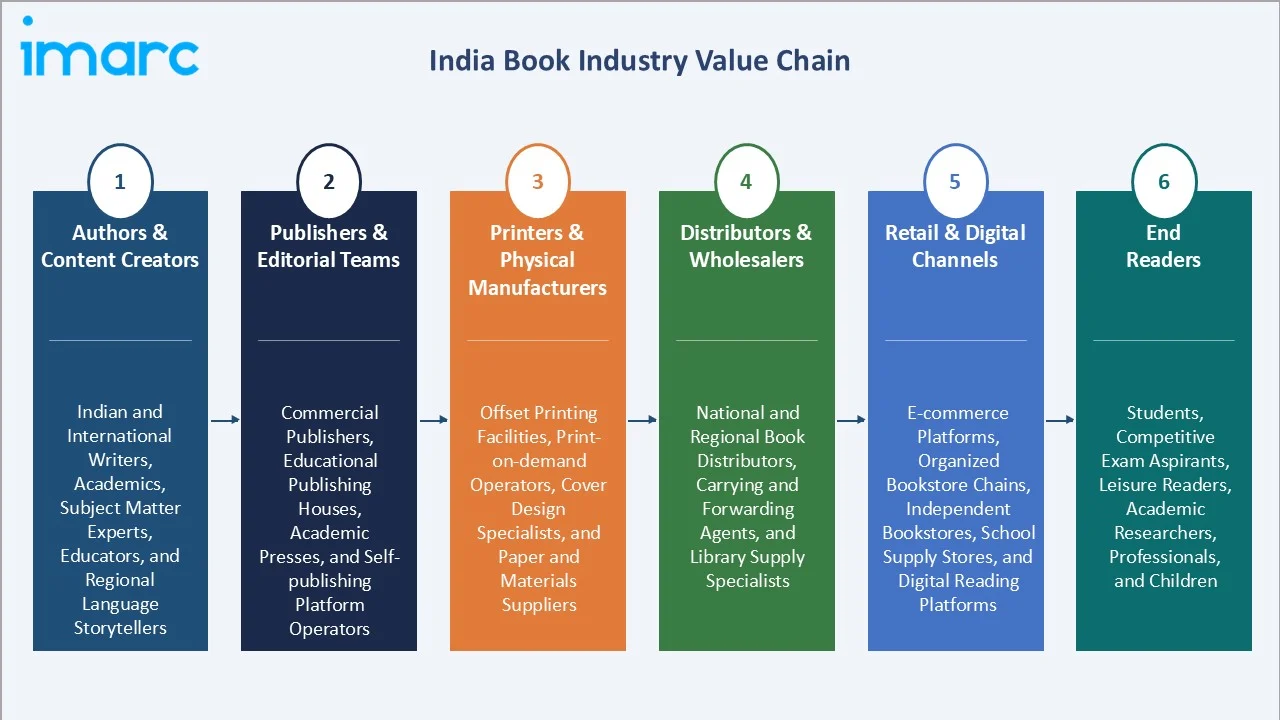

Industry Value Chain Analysis

India's book market value chain spans content creation through reader delivery, with each stage occupied by specialized participants whose collective performance determines the diversity, quality, and accessibility of India's publishing output.

|

Stage |

Key Players / Examples |

|

Authors & Content Creators |

Indian and international writers, academics, subject matter experts, educators, and regional language storytellers |

|

Publishers & Editorial Teams |

Commercial publishers, educational publishing houses, academic presses, and self-publishing platform operators |

|

Printers & Physical Manufacturers |

Offset printing facilities, print-on-demand operators, cover design specialists, and paper and materials suppliers |

|

Distributors & Wholesalers |

National and regional book distributors, carrying and forwarding agents, and library supply specialists |

|

Retail & Digital Channels |

E-commerce platforms, organized bookstore chains, independent bookstores, school supply stores, and digital reading platforms |

|

End Readers |

Students, competitive exam aspirants, leisure readers, academic researchers, professionals, and children |

Technology Landscape in the India Book Industry

E-book Platforms and Digital Reading Infrastructure

India's e-book ecosystem is anchored by Amazon Kindle, supplemented by Google Play Books, Apple Books, and Scribd India. Indian-origin e-book platforms, including Juggernaut Books, Pratilipi, and Notion Press, are serving the mass-market digital reading segment. Total India e-book readership is estimated at 55–65 million active users in 2025, growing at 15%+ annually.

Audiobook and Audio Content Platforms

India's audiobook market is defined by three distinct platform categories: international premium platforms serving English-language urban readers; regional language mass-market platforms serving Hindi and vernacular audio content consumers; and publishing house-owned audio initiatives by Penguin Random House LLC and HarperCollins Publishers that create exclusive audiobook editions of their bestselling titles.

Educational Technology Integration with Physical Publishing

S Chand And Company Limited's digital-physical hybrid books, Arihant Publications' online test series platforms, and Oxford University Press India's digital resource portals are establishing the hybrid book model, where physical textbooks are augmented with QR codes linking to video explanations, online assessments, and supplementary digital content. This hybrid model commands 15–25% price premiums over pure physical books while expanding the addressable market to digital learning tool budgets previously unavailable to traditional publishers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Format |

Hard Copy |

72.6% |

2025 |

|

Type |

Educational |

34.8% |

2025 |

|

Distribution Channel |

Online |

44.3% |

2025 |

|

Region |

North India |

31.7% |

2025 |

By Format

Hard copy dominates with a 72.6% share in 2025. Physical books remain India's primary reading format, reflecting the institutional procurement requirements of 24.69 crore students across 14.71 lakh schools that mandate physical textbooks; the competitive exam preparation culture, where physical books with handwritten annotations are preferred; and India's strong book-gifting tradition during festivals and occasions.

To access detailed market analysis, Request Sample

E-books represent 16.3% of the market and are growing steadily as Kindle Unlimited, Google Play Books, and regional language digital platforms expand their India content catalogs. Audiobooks’ 11.1% share is projected to grow fastest (~12.4% CAGR), driven by smartphone penetration, urban commuting culture, and regional language platform expansion.

By Type

Educational books dominate with a 34.8% share in 2025, encompassing school textbooks, university academic books, competitive exam preparation guides, and professional certification study materials. Educational publishing's dominant share reflects India's structural reality as one of the world's largest education systems, creating a consistently large, non-discretionary procurement market.

Science books at 8.2% and contemporary/realistic fiction at 7.3% are the next largest categories, followed closely by historical at 7.5%, fantasy at 7.0%, romance at 6.5%, mystery at 6.8%, literary at 6.2%, and comic books at 5.9%.

Regional Market Insights

North India's market leadership (31.7%, 2025) reflects Delhi NCR's position as India's publishing capital, combined with the region's extraordinary competitive exam preparation culture that drives India's highest per-capita educational book spending. East India at 24.1% represents India's second-largest book market, driven by West Bengal's tradition of literary reading, and the region's large student population across West Bengal, Bihar, Odisha, and Jharkhand.

.webp)

South India, at 22.6%, is distinguished by India's highest literacy rates, creating the highest reading intensity per capita of any Indian region. South India's strong regional language publishing ecosystem encompasses Tamil, Telugu, Kannada, and Malayalam publishing markets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.7% |

India's publishing capital concentration in Delhi; UPSC and competitive exam culture driving the highest per-capita educational book spend; New Delhi World Book Fair |

|

East India |

24.1% |

West Bengal's strong literary culture and Kolkata's National Book Fair driving reading culture; a large student population in West Bengal, Bihar, Jharkhand, and Odisha; growing regional language digital publishing |

|

South India |

22.6% |

Strong literacy rates driving the highest reading intensity; regional language publishing hubs; IT sector professionals' non-fiction consumption in Bengaluru and Hyderabad |

|

West India |

21.6% |

Mumbai's trade publishing and commercial fiction market; Maharashtra's large educational book procurement; growing Marathi and Gujarati regional language digital publishing adoption. |

Competitive Landscape

India's book market exhibits moderate concentration at the trade publishing level, while the educational publishing segment is more fragmented across educational publishers.

|

Company Name |

Genre/Categories |

Market Position |

Core Strength |

|

Penguin Random House LLC |

Fiction, Non-fiction, Children’s, Penguin Swadesh, Classics, Penguin Audiobooks |

Market Leader |

Extensive trade publishing portfolio; broad national market presence with multi-city editorial and distribution operations |

|

HarperCollins Publishers |

Fiction, Action and Adventure, Anthologies, Classics, Mystery and Thriller, Sci-fi and Fantasy, Graphic Novel, Audiobooks |

Market Leader |

Strong literary and commercial fiction; award-winning author roster; international publishing standards |

|

S Chand And Company Limited |

School Books, Higher Academic Books, Technical & Professional Books, Competitive Exam Books |

Strong Challenger |

Educational publishing leadership; deep CBSE/ICSE alignment; strong Tier 2/3 city distribution |

|

Arihant Publications India Limited |

UPSC & State PSC, Engineering Exam, Medical Exam, School Curriculum, Government Exams, ITI & Polytechnic, Competitive Exam Preparation Books |

Challenger |

Dominant competitive exam preparation publisher; digital test series integration |

The market's linguistic diversity across 22 scheduled languages inherently supports a large number of viable publishers serving distinct language communities that global English-language publishers cannot efficiently reach.

Key Company Profiles

Penguin Random House LLC

Penguin Random House LLC’s subsidiary Penguin Random House India is one of India's largest English-language trade publishers, publishing 250+ new titles annually across literary fiction, commercial fiction, non-fiction, business, children's, and academic categories.

- Key Titles / Series: Fiction, non-fiction, children’s, Penguin Swadesh, classics, and Penguin audiobooks.

- Recent Developments: In April 2026, Penguin Random House India and Kuku FM launched 12 Hindi audiobooks from their exclusive 15-title partnership. The launch marks company’s first professionally produced Hindi audiobook initiative and targets India’s growing regional-language audio audience.

- Strategic Focus: Regional language publishing expansion; digital format co-publication with Kindle and Audible; youth market penetration through campus ambassador programs; audiobook production for Hindi and English bestsellers.

S Chand And Company Limited

S Chand And Company Limited is one of India's largest educational publishers, operating across school textbooks, higher education academic books, competitive exam preparation, and professional reference materials.

- Key Titles / Series: School books, higher academic books, technical & professional books, and competitive exam books.

- Recent Developments: In June 2025, S Chand And Company Limited introduced textbooks integrated with Google Lens-enabled tools to provide students with quick access to explanations and solutions. The initiative aims to make textbook learning more interactive and support easier concept understanding through digital assistance.

- Strategic Focus: NEP 2020 curriculum-aligned textbook series development; digital-physical hybrid book leadership; higher education academic publishing expansion; competitive exam preparation digital platform growth.

Market Concentration Analysis

India's book market exhibits asymmetric concentration: the English-language trade publishing segment is moderately concentrated with Penguin Random House LLC and HarperCollins Publishers, controlling approximately 50–60% of English fiction and non-fiction trade revenue.

The educational publishing segment is more fragmented, with S Chand And Company Limited, Arihant Publications India Limited, and 200+ state-specific educational publishers collectively serving India's diverse school board ecosystem across 28 states. Regional language publishing is highly fragmented, with thousands of small publishers serving distinct language communities that national publishers reach only partially through imprints.

Investment & Growth Opportunities

Fastest Growing Segments

Audiobooks (~12.4% CAGR), e-books (~9.8% CAGR), science books (~5.8% CAGR), competitive exam preparation books (~8% CAGR), and regional language digital reading platforms (~18% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address USD 1.5+ billion in incremental market opportunity within India's book ecosystem by 2030.

Emerging Market Expansion

India's regional language digital reading market represents the largest underpenetrated book market opportunity globally. Current regional language digital reading platforms are only scratching the surface of the potential audience, with the majority of regional language readers having no access to curated digital reading content in their mother tongue.

India's Tier 2 and Tier 3 cities represent an emerging physical and digital book market where rising incomes, expanding educational institution density, and growing aspirational class reading habits are creating consistent book market growth above the national average.

Venture and Institutional Investment Trends

- In October 2025, Kuku FM raised USD 85 million in a Series C funding round led by Granite Asia, with participation from existing investors. The company plans to use the capital to expand its AI-powered audio content ecosystem, strengthen creator monetization, and accelerate growth across regional language markets in India

- Educational technology publishers are attracting the highest valuations in India's education sector. Arihant's online test series platform, Oswaal Books' digital resources, and S. Chand's hybrid content investment are collectively demonstrating that educational publishers who successfully bridge physical and digital content can double their per-student revenue versus traditional textbook-only models.

Future Market Outlook (2026-2034)

The India book market is positioned for steady, sustainable expansion through 2034. From a base of USD 5.13 Billion in 2025, the market is projected to reach USD 7.31 Billion by 2034, representing total incremental value creation of USD 2.18 billion at a CAGR of 4.00%.

The gradual growth reflects the market's structural support from India's rising literacy, expanding education enrollment, growing middle-class reading culture, and the multi-format digital reading expansion that is creating new revenue streams alongside sustained physical book demand.

By 2034, digital formats will collectively represent 35–40% of market value as audiobook adoption reaches 25+ million regular listeners and e-books expand into regional language markets at scale. Educational books will retain 32–35% market share as NEP 2020 implementation completes and India's enrollment expansion sustains demand.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including publishing house executives, literary agents, educational book procurement officers, digital platform managers, bookstore category buyers, and institutional investors across Delhi, Mumbai, Kolkata, Chennai, and Bengaluru.

Secondary Research

Secondary research encompassed company disclosures, Federation of Indian Publishers data, National Book Trust procurement reports, Nielsen BookScan India retail market data, Ministry of Education school enrollment statistics, and industry publications (Publishing Next India, BookBrunch, The Bookseller India).

Forecasting Models

Market size estimations incorporated India GDP and consumer spending growth projections, literacy rate improvement trajectories, education enrollment expansion data, digital platform subscriber growth rates, and publisher revenue disclosures. A base-case CAGR of 4.00% reflects consensus estimates validated against publisher sales data, school enrollment projections, and digital reading platform growth trajectories from FY2020 to FY2025.

India Book Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Science, Historical, Mystery, Fantasy, Literary, Contemporary/Realistic, Romance, Educational, Comic, Others |

|

Formats Covered |

Hard Copy, E-book, Audiobook |

|

Distribution Channel Covered |

Online, Local Book Shops, Mass Merchandisers/Retail Shops, Specialty Bookstores, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Penguin Random House LLC, HarperCollins Publishers, S Chand And Company Limited, Arihant Publications India Limited, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Book Market Report

The India book market reached USD 5.13 Billion in 2025 and is projected to reach USD 7.31 Billion by 2034.

The market is expected to grow at a CAGR of 4.00% during 2026-2034, driven by rising literacy, NEP 2020 curriculum expansion, digital format adoption, and regional language publishing growth.

North India leads with a 31.7% share in 2025, anchored by Delhi NCR's status as India's publishing capital, the region's competitive exam culture, and the New Delhi World Book Fair.

Hard Copy dominates with a 72.6% share in 2025, reflecting institutional educational procurement requirements, India's gifting culture, and physical reading preferences among consumers in areas with limited internet connectivity.

Educational books hold the largest share at 34.8%, driven by India's 24.69 crore student population, NEP 2020 curriculum reform creating textbook replacement demand, and the non-discretionary nature of educational book procurement.

Some of the key players include Penguin Random House LLC, HarperCollins Publishers, S Chand And Company Limited, and Arihant Publications India Limited.

Audiobooks are growing at ~12.4% CAGR owing to India’s growing adoption of audiobooks during commuting and multitasking, regional language platforms’ expanding content availability, and celebrity narrator premium audiobook experiences.

Key challenges include digital book piracy eroding publisher revenues, competition from OTT platforms for leisure time, rising print production costs, limited rural bookstore distribution infrastructure, and author talent competition from high-royalty self-publishing platforms.

Regional language digital reading platforms, audiobook content production, hybrid digital-physical educational books, competitive exam preparation digital platforms, and Tier 2/3 city-organized book retail represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)