India BOPP Films Market Size, Share, Trends and Forecast by Type, Thickness, Production Process, Application, and Region, 2026-2034

India BOPP Films Market Size, Share, Trends & Forecast (2026-2034)

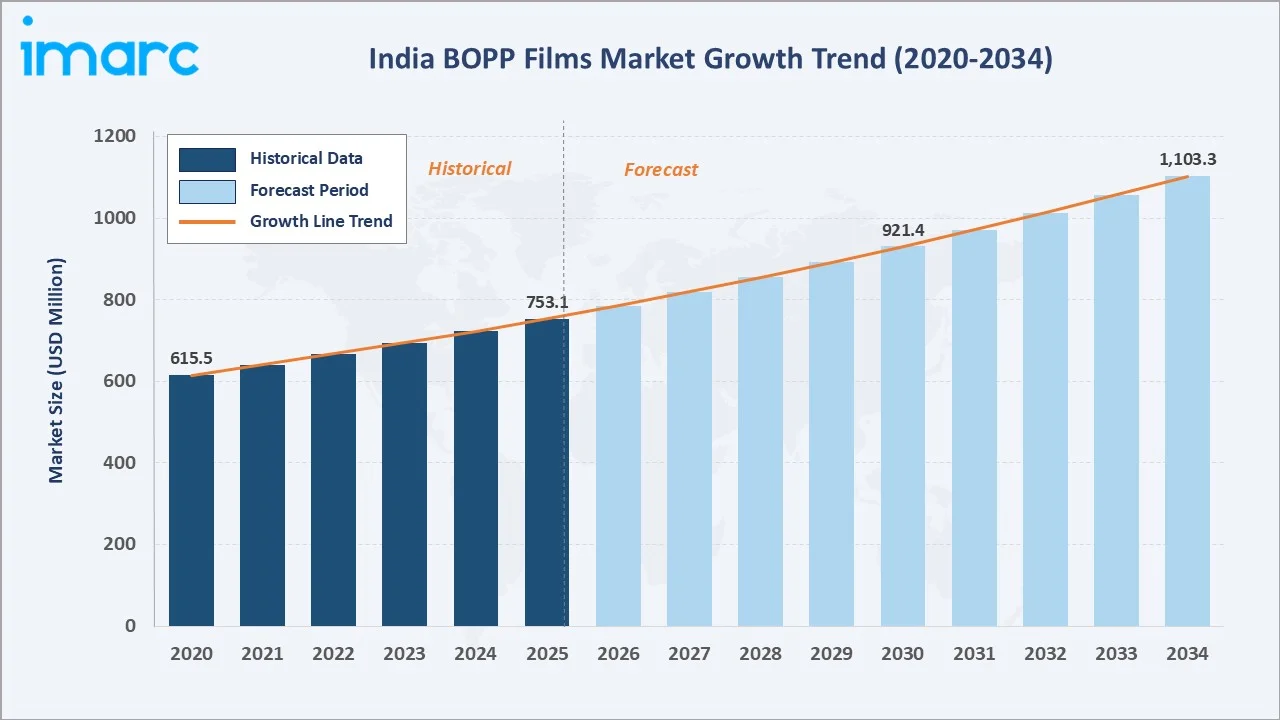

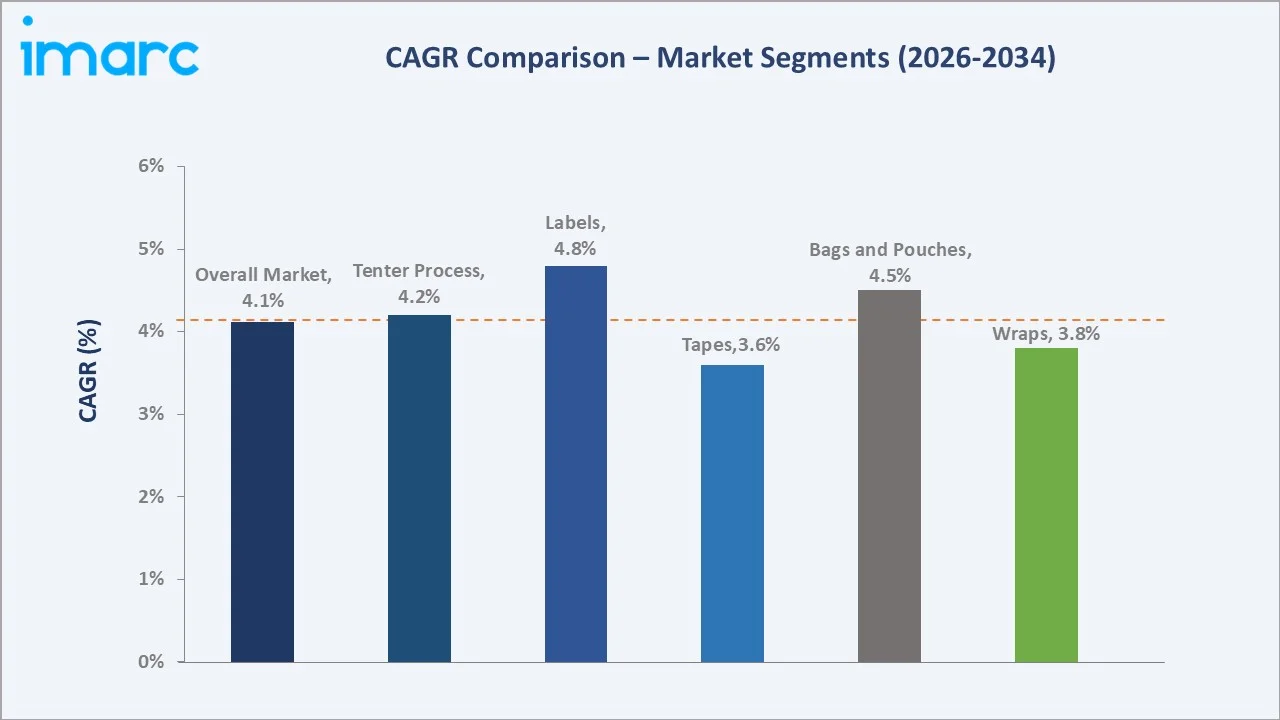

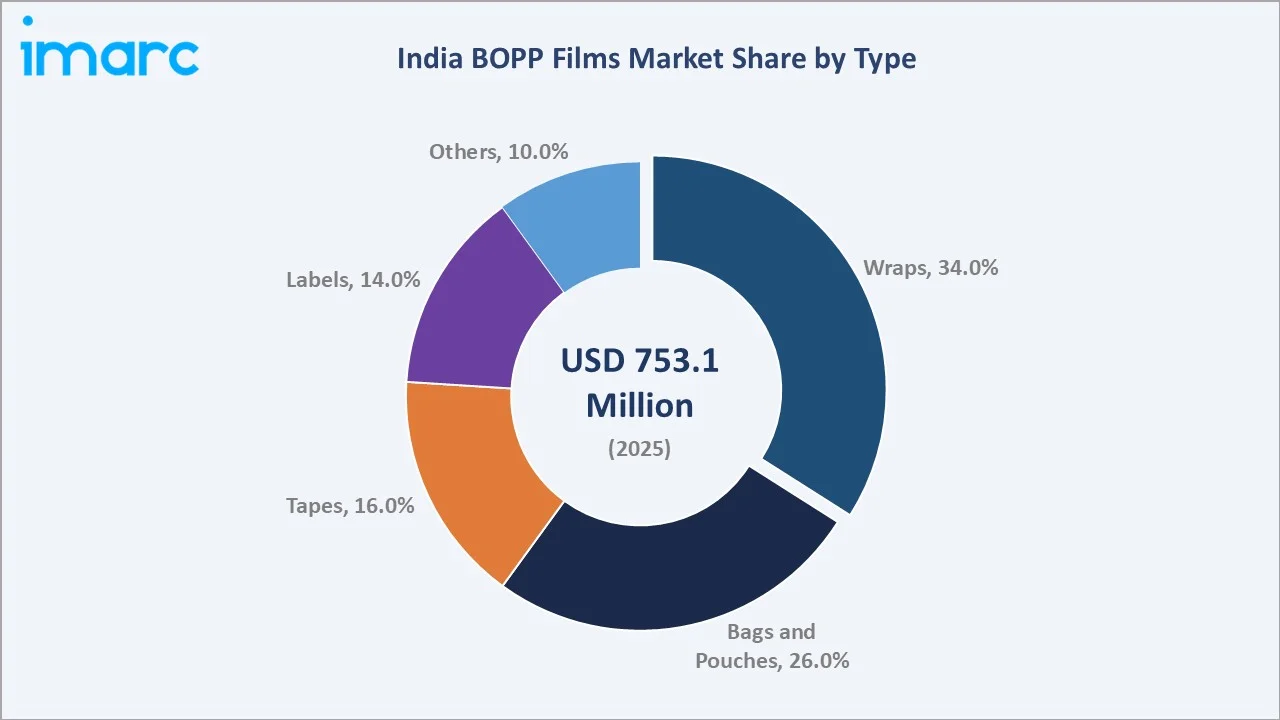

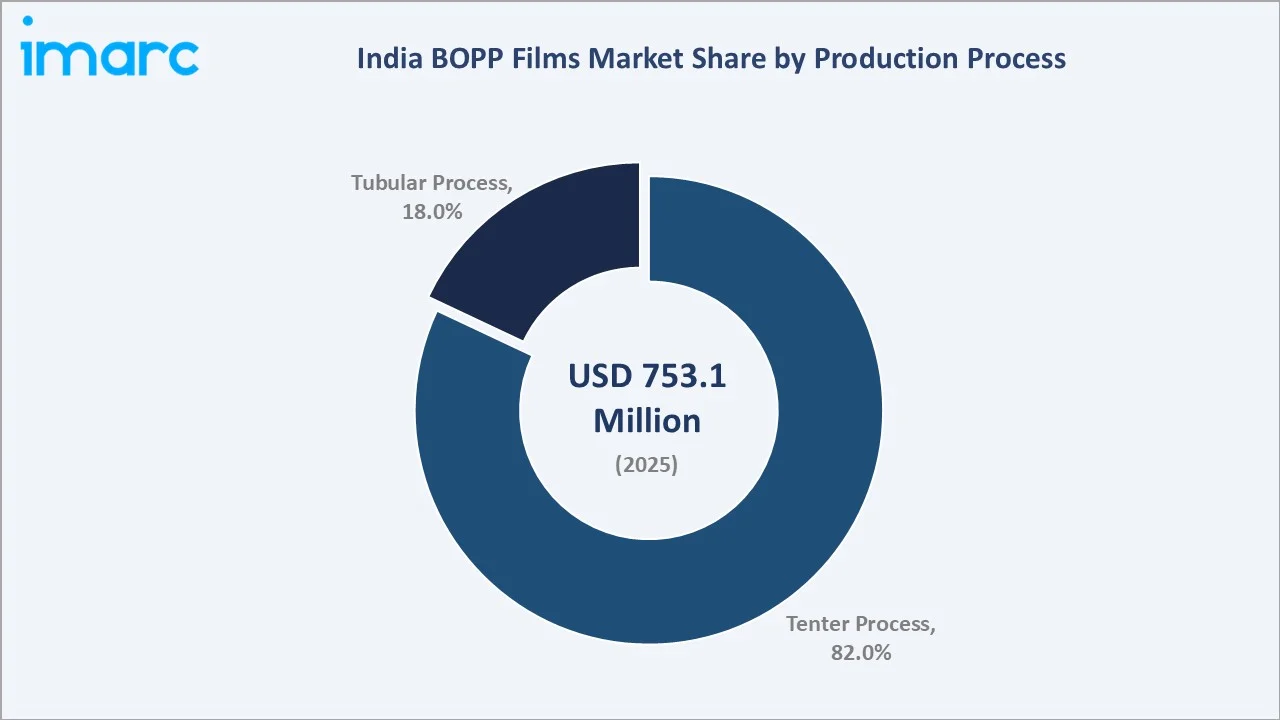

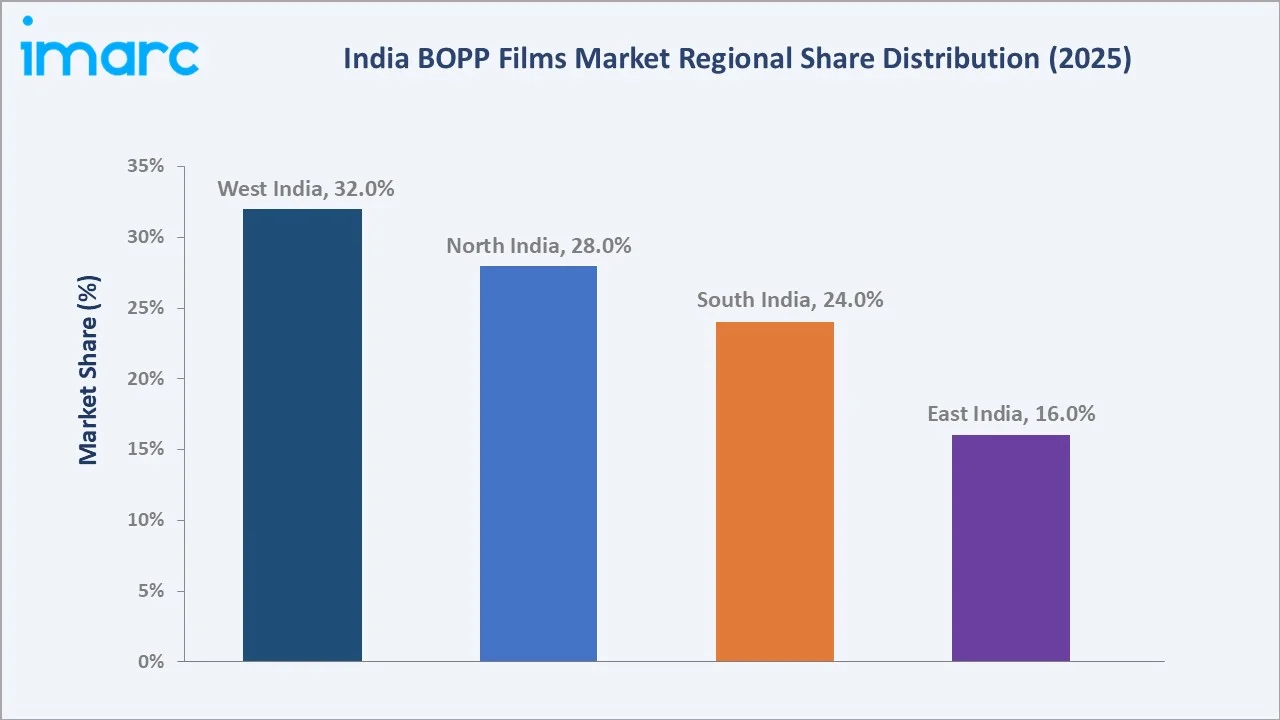

The India BOPP films market reached USD 753.1 Million in 2025 and is projected to reach USD 1,103.3 Million by 2034, growing at a CAGR of 4.12% during 2026-2034. The market is driven by the rapid growth of the packaged food, FMCG, and e-commerce sectors, which are increasing demand for lightweight, durable, and cost-effective packaging solutions. India has a well-established packaging ecosystem, with more than 22,000 packaging units, nearly 85% of which are SMEs. This large packaging and converting base is driving the India BOPP films market by increasing demand for flexible, lightweight, and cost-effective films used in food, FMCG, labels, lamination, and consumer goods packaging. Wraps lead at 34.0%. Tenter process dominates at 82.0%. West India commands 32.0% of the national market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 753.1 Million |

| Forecast Market Size (2034) | USD 1,103.3 Million |

| CAGR (2026-2034) | 4.12% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Type | Wraps (34.0%, 2025) |

| Dominant Production Process | Tenter (82.0%, 2025) |

| Leading Region | West India (32.0%, 2025) |

India BOPP films market expanded from USD 615.5 Million in 2020 to USD 753.1 Million in 2025, anchored at USD 921.4 Million in 2030, and forecast to reach USD 1,103.3 Million by 2034. BOPP (Biaxially Oriented Polypropylene) film is produced by extruding molten PP resin into a thick sheet and simultaneously or sequentially stretching it in both machine direction (MD) and transverse direction (TD) to align polymer chains, creating a film with dramatically superior mechanical strength, optical clarity, barrier properties, and printability versus unoriented polypropylene. India's BOPP film market is structurally positioned at the intersection of India's most commercially dynamic consumer goods trends, FMCG packaged food growth, organized retail expansion, e-commerce packaging demand, and India's progressive shift from rigid packaging toward flexible packaging, creating the commercial foundation for India's 4.12% CAGR forecast.

To get more information on this market, Request Sample

Labels grow fastest at ~4.8% CAGR through India's organized retail QR-code and brand decoration label proliferation, premium PSA label adoption replacing paper labels, and in-mould BOPP label growth in personal care and beverage packaging. Bags and pouches grow at ~4.5% CAGR through India's D2C food brand packaging, e-commerce protective packaging, and direct-food-contact BOPP pouch growth above traditional multi-material laminate pouches.

Executive Summary

India BOPP films market at USD 753.1 Million in 2025 represents one of Asia's most commercially dynamic flexible packaging substrate markets, with India's combination of consumers with rapidly expanding packaged food adoption, a domestic BOPP film manufacturing industry that has achieved competitive cost and quality positions, and India's progressive organized retail and e-commerce growth creating structural demand expansion across all BOPP film application segments. The market is projected to reach USD 1,103.3 Million by 2034.

Wraps at 34.0% lead through India's dominant biscuit and confectionery packaging application. Tenter process dominates at 82.0% through its superior film properties for all major BOPP applications. West India leads regionally at 32.0%.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Type | Wraps – 34.0% share (2025) |

| Dominant Production Process | Tenter – 82.0% market share (2025) |

| Leading Region | West India – 32.0% share (2025) |

| Market Opportunity | Monomaterial recyclable BOPP for circular economy compliance; specialty barrier and high-slip coatings; metallized BOPP for premium packaging; BOPP label expansion through organized retail |

Key Analytical Observations Supporting The Above Data:

- Wraps at 34.0%: The wraps segment dominates due to its extensive use in packaging snacks, confectionery, bakery products, tobacco, and FMCG goods. BOPP wraps offer excellent printability, moisture resistance, product protection, and cost-effectiveness, making them the preferred packaging solution across industries.

- Tenter process at 82.0%: The tenter process enables the production of high-quality films with superior clarity, strength, dimensional stability, and printability. It is widely preferred for large-scale flexible packaging applications due to its efficiency and ability to produce multilayer and specialty BOPP films.

- West India at 32.0%: West India dominates regionally due to the strong presence of packaging, FMCG, food processing, and manufacturing hubs across Maharashtra and Gujarat. The region also benefits from better logistics, port connectivity, and a large base of flexible packaging converters.

India BOPP Films Market Overview

BOPP film is the most commercially versatile flexible packaging substrate, with its combination of optical clarity, mechanical strength, chemical resistance, printability, heat-sealability, and recyclability making BOPP the primary packaging substrate for India's biscuit, snack, candy, confectionery, personal care, and agricultural packaging sectors. India BOPP films market operates within the broader flexible packaging industry as the most commercially significant single flexible packaging substrate by volume.

The BOPP film market ecosystem integrates PP resin supply, BOPP film manufacturing, value-added film processing, flexible packaging conversion, and regulatory compliance. Macroeconomic factors include rapid urbanization, rising disposable incomes, expanding packaged food and FMCG consumption, and growth in organized retail and e-commerce.

Market Dynamics

To evaluate market opportunities, Request Sample

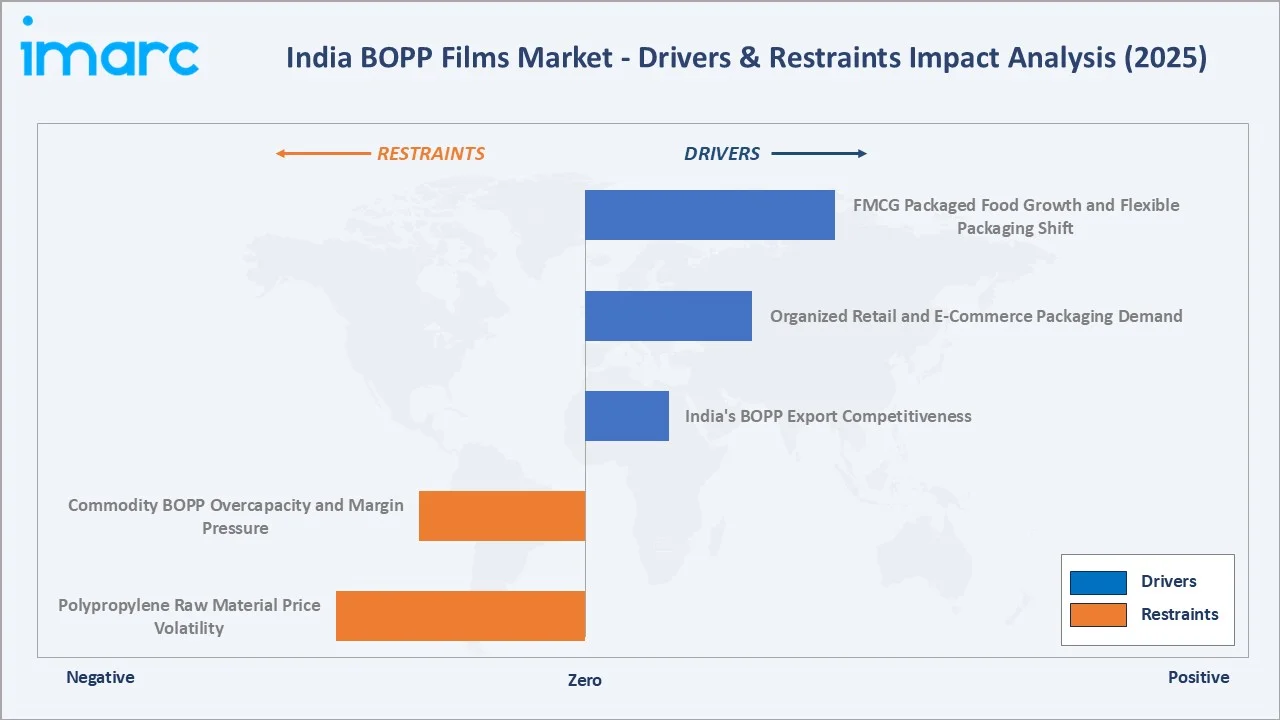

Market Drivers

- FMCG Packaged Food Growth and Flexible Packaging Shift: Rising demand for packaged snacks, confectionery, bakery products, dairy products, and ready-to-eat foods is increasing the need for high-performance packaging materials. BOPP films offer excellent moisture resistance, printability, durability, and cost efficiency, making them ideal for flexible packaging applications. As FMCG companies focus on product shelf life, branding, and lightweight packaging, demand for BOPP films continues to grow.

- Organized Retail and E-Commerce Packaging Demand: Organized retail and e-commerce packaging demand is driving the market as brands require durable, lightweight, and attractive packaging for wider product distribution. BOPP films support high-quality printing, moisture protection, tamper resistance, and shelf appeal, making them suitable for packaged food, personal care, and consumer goods. Rising online deliveries are further increasing demand for reliable flexible packaging that protects products during storage and transit.

- India's BOPP Export Competitiveness: India, China, and Vietnam rank as the top three exporters of BOPP film. India tops with 73,410 shipments. India's BOPP export competitiveness is encouraging capacity expansion, technological upgrades, and higher production volumes among domestic manufacturers. Competitive manufacturing costs, improving product quality, and strong demand from international packaging markets have strengthened India's position as a key exporter of BOPP films. This growth in exports supports economies of scale and boosts investments across the value chain, further accelerating market development.

Market Restraints

- Polypropylene Raw Material Price Volatility: Polypropylene raw material price volatility is creating uncertainty in production costs and profit margins for manufacturers. Since polypropylene is the primary feedstock for BOPP films, fluctuations in crude oil and petrochemical prices directly impact raw material expenses. Frequent price changes make long-term pricing agreements difficult and can increase packaging costs for end users. This volatility also affects investment planning and operational efficiency across the value chain.

- Commodity BOPP Overcapacity and Margin Pressure: Commodity BOPP overcapacity and margin pressure are creating an imbalance between supply and demand. Continuous capacity additions by manufacturers have intensified competition, leading to lower selling prices and reduced profit margins. This makes it difficult for producers of standard commodity-grade films to maintain profitability, especially during periods of weak demand. As a result, companies are increasingly shifting toward specialty and value-added BOPP films to improve margins and differentiate their offerings.

Market Opportunities

- Monomaterial Recyclable BOPP: Monomaterial recyclable BOPP films present a significant opportunity as brand owners and packaging companies increasingly seek sustainable packaging solutions. These films enable easier recycling by replacing multi-material laminates with single-polymer structures, helping companies meet environmental and regulatory requirements. In November 2025, Toppan and its India-based subsidiary Toppan Speciality Films (TSF) launched a hybrid production line in India capable of manufacturing both BOPP and BOPE films on a single machine. The line supports the development of recyclable mono-material packaging, helping brands comply with India’s Plastic Waste Management and EPR norms. As sustainability becomes a key purchasing criterion, demand for recyclable BOPP films is expected to rise substantially.

- Increasing Demand for Transparent, Printable, and Premium Packaging Materials: Brand owners are increasingly seeking packaging that enhances product visibility, shelf appeal, and brand differentiation in competitive retail environments. BOPP films offer excellent clarity, gloss, and printability, making them ideal for high-quality packaging applications. The growing focus on attractive packaging in the FMCG, food, personal care, and consumer goods sectors is expected to drive demand for advanced BOPP film solutions.

Market Challenges

- High Energy and Logistics Costs Impacting Manufacturing Profitability: High energy and logistics costs are increasing overall production and distribution expenses. BOPP film manufacturing is energy-intensive, requiring power for extrusion, stretching, coating, and drying processes. Rising fuel, electricity, transportation, and warehousing costs reduce manufacturers’ margins, especially for commodity-grade films. These cost pressures can also make Indian BOPP products less competitive in price-sensitive domestic and export markets.

- Demand Fluctuations in Key End-Use Sectors Such as FMCG and Consumer Goods: Demand fluctuations in the FMCG and consumer goods sectors are challenging as these industries account for a major share of film consumption. Any slowdown in packaged food, personal care, household goods, or retail sales directly affects packaging demand. Seasonal consumption patterns and changing consumer spending also create uncertainty for manufacturers. This makes production planning, inventory management, and pricing stability more difficult for BOPP film producers.

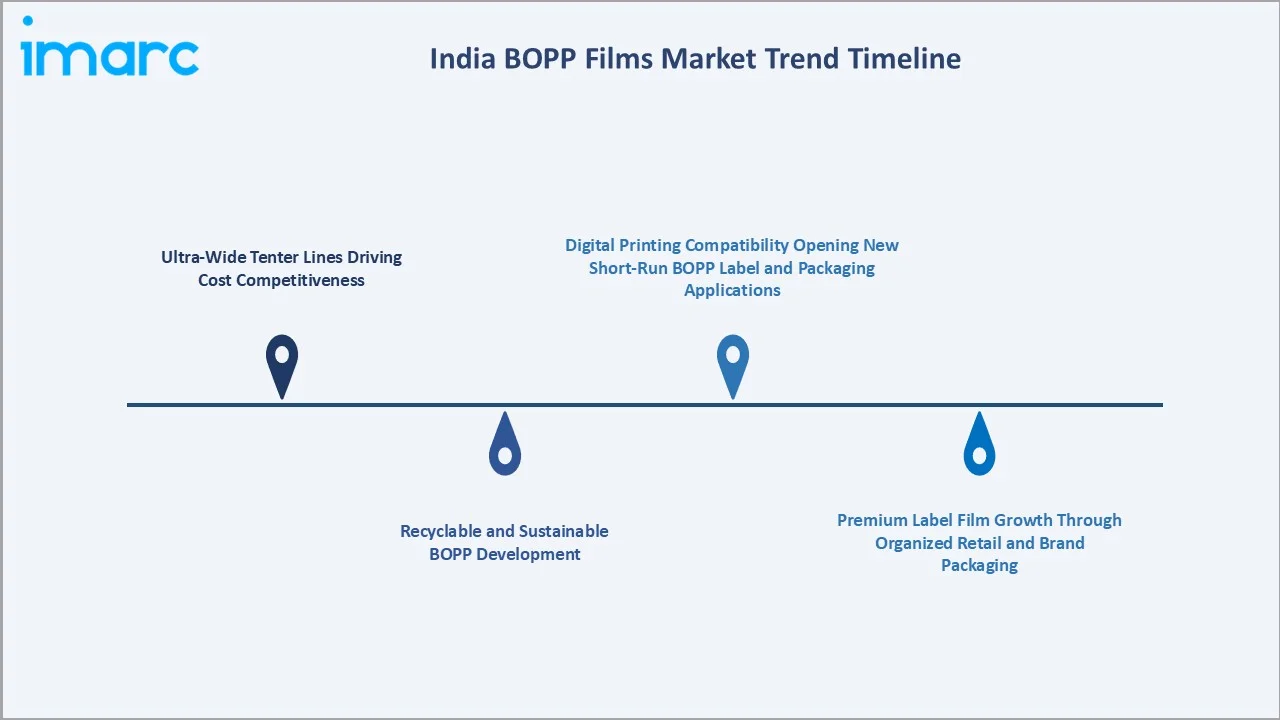

Emerging Market Trends

1. Ultra-Wide Tenter Lines Driving Cost Competitiveness

Ultra-wide tenter lines enable manufacturers to produce higher film volumes with better efficiency. These advanced lines improve economies of scale, reduce per-unit production costs, and support consistent film quality. They also help producers meet rising demand from FMCG, food packaging, labels, and export markets. As competition intensifies, ultra-wide tenter lines are helping Indian manufacturers strengthen cost competitiveness and improve profitability.

2. Recyclable and Sustainable BOPP Development

Recyclable and sustainable BOPP development is emerging as brands shift toward eco-friendly flexible packaging. Manufacturers are developing mono-material, recyclable, and downgauged BOPP films to reduce plastic waste and improve material efficiency. In May 2026, India-based Surya Global Flexifilms (SGF) invested in a BOBST EXPERT K5 3650 mm metallizer with AlOx capability, which is scheduled to be installed at its facility by the end of 2026. As one of India’s leading BOPP producers, SGF will use the new AlOx-enabled system to manufacture sustainable, clear-coated, high-barrier BOPP films using BOBST AlOx GEN II technology. These solutions help FMCG, food, and personal care companies meet sustainability goals while maintaining clarity, strength, and printability. This trend is also supporting innovation in high-barrier recyclable packaging formats.

3. Premium Label Film Growth Through Organized Retail and Brand Packaging

Premium label film growth through organized retail and brand packaging is emerging as companies focus on attractive shelf presentation and stronger brand visibility. BOPP label films offer high clarity, gloss, printability, and durability, making them suitable for beverage bottles, personal care products, food containers, and FMCG packaging. Rising organized retail and premium product launches are increasing demand for high-quality label films. This trend is helping manufacturers move toward value-added BOPP products with better margins.

4. Digital Printing Compatibility Opening New Short-Run BOPP Label and Packaging Applications

Digital printing compatibility enables short-run, customized, and fast-turnaround label and packaging applications. It allows brands to launch limited-edition packs, regional designs, promotional packaging, and SKU-specific labels without the high setup costs of conventional printing. This is especially useful for FMCG, food, personal care, and D2C brands seeking flexible packaging solutions. As demand for personalization and faster product launches grows, digitally printable BOPP films are gaining wider adoption.

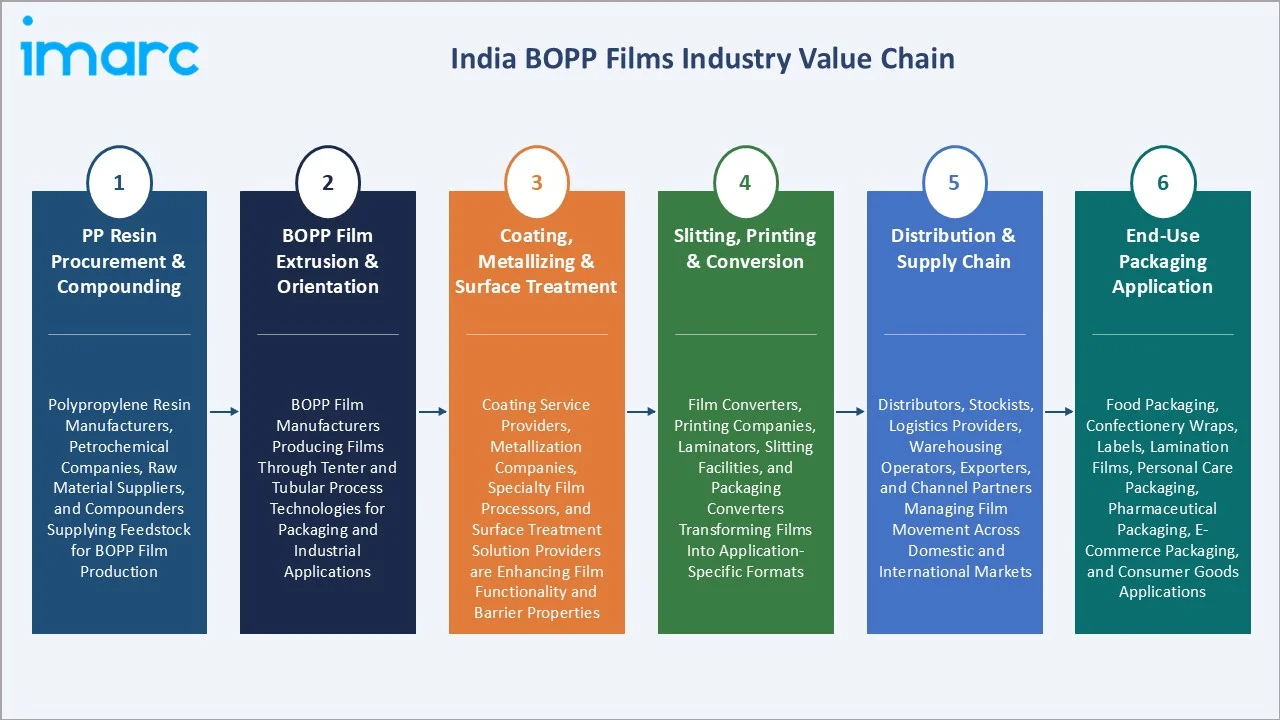

Industry Value Chain Analysis

India BOPP films value chain is one of the most commercially integrated supply chains in India's packaging materials industry. The value chain's commercial structure creates a compressed margin environment in commodity plain BOPP while creating attractive specialty margins in coated, metallized, and high-performance BOPP grades, where product differentiation sustains pricing above commodity plain BOPP benchmarks.

| Stage | Key Participants |

|---|---|

| PP Resin Procurement & Compounding | Polypropylene resin manufacturers, petrochemical companies, raw material suppliers, and compounders supplying feedstock for BOPP film production |

| BOPP Film Extrusion & Orientation | BOPP film manufacturers producing films through tenter and tubular process technologies for packaging and industrial applications |

| Coating, Metallizing & Surface Treatment | Coating service providers, metallization companies, specialty film processors, and surface treatment solution providers enhancing film functionality and barrier properties |

| Slitting, Printing & Conversion | Film converters, printing companies, laminators, slitting facilities, and packaging converters transforming films into application-specific formats |

| Distribution & Supply Chain | Distributors, stockists, logistics providers, warehousing operators, exporters, and channel partners managing film movement across domestic and international markets |

| End-Use Packaging Application | Food packaging, confectionery wraps, labels, lamination films, personal care packaging, pharmaceutical packaging, e-commerce packaging, and consumer goods applications |

The value chain's most commercially significant structural characteristic is the capital intensity of BOPP film tenter manufacturing. The coating and metallizing stage creates the most commercially defensible margin positions in India's BOPP value chain, vacuum metallizing capital and PVDC coating line investment, creating barriers that small-scale converters cannot replicate, sustaining, and specialty margin advantage above plain film commodity competition from smaller domestic and international competitors.

Technology Landscape in the India BOPP Films Industry

Tenter Frame Biaxial Orientation Technology

Tenter frame biaxial orientation technology enables the production of films with superior strength, clarity, stiffness, and dimensional stability. The process stretches polypropylene film in both machine and transverse directions, enhancing its mechanical and barrier properties. It also supports the manufacture of high-quality packaging, labels, and specialty films with improved printability and performance. As demand for premium and value-added BOPP products grows, manufacturers are increasingly investing in advanced tenter line technologies to improve efficiency and competitiveness.

Barrier Coating Technology

Barrier coating technology enhances the oxygen, moisture, aroma, and grease barrier properties of packaging films. Advanced coatings such as AlOx, SiOx, acrylic, and water-based barrier layers help extend product shelf life while reducing the need for multi-layer packaging structures. These technologies support the development of recyclable and sustainable packaging solutions without compromizing performance. In March 2024, TOPPAN Inc and India-based TOPPAN Speciality Films Private Limited (TSF) developed GL-SP, a barrier film that uses biaxially oriented polypropylene (BOPP) as the substrate. As demand for high-barrier food, pharmaceutical, and personal care packaging grows, barrier-coated BOPP films are gaining increasing adoption across the market.

Anti-Fog and Anti-Static Film Technologies

Anti-fog and anti-static film technologies are improving the performance of packaging films in specialized applications. Anti-fog coatings prevent moisture condensation on film surfaces, enhancing product visibility in fresh food and refrigerated packaging. Anti-static technologies reduce dust attraction and electrostatic charge buildup, improving handling, processing efficiency, and product protection. These innovations are helping manufacturers cater to the growing demand for high-performance packaging solutions in food, pharmaceutical, and industrial sectors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Wraps |

34.0% |

2025 |

|

Thickness |

🔒 |

🔒 |

2025 |

|

Production Process |

Tenter |

82.0% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West India |

32.0% |

2025 |

By Type

Wraps lead at 34.0% (2025). The wrap segment encompasses BOPP flow-wrap biscuit packaging, BOPP candy twist wrap, BOPP cigarette overwrap, BOPP fresh produce overwrap, and industrial product shrink wrap, the most commercially diverse BOPP application type by end-use sector breadth above any other BOPP film type.

To access detailed market analysis, Request Sample

Bags and pouches at 26.0% grow at ~4.5% CAGR through D2C food brand and e-commerce packaging. Tapes at 16.0% provide commercial stability through India's logistics and industrial tape market growth. Labels at 14.0% grow fastest at ~4.8% CAGR through organized retail and premium brand packaging adoption. Others at 10.0% include agricultural film, specialty industrial, and emerging bio-BOPP applications.

By Production Process

Tenter process leads at 82.0% (2025). The tenter process dominance reflects its superior film property capability, the independent MD and TD stretch ratio control enabling application-optimized BOPP grades from ultra-clear wraps through high-barrier metallizable film through stiff label facestock through soft sealable pouching film that the tubular process's inherent balanced biaxial orientation cannot match for application-specific performance optimization.

Tubular process at 18.0% serves India's specialty BOPP applications where balanced biaxial orientation is commercially beneficial, heat-shrink BOPP wrap for multipack collation, soft-touch BOPP for premium packaging tactile finish, and specific food contact BOPP grades where tubular processing creates equivalent performance at below-tenter-capital-cost for narrower width specialty applications.

Regional Market Insights

| Region | Share (2025) | Key India BOPP Films Market Drivers & Characteristics |

|---|---|---|

| West India | 32.0% | Driven by the strong presence of packaging converters, FMCG manufacturers, petrochemical facilities, and flexible packaging hubs. |

| North India | 28.0% | Supported by a large consumer base, growing packaged food consumption, and expanding manufacturing activities. |

| South India | 24.0% | Driven by the presence of major food processing, beverage, retail, and consumer goods industries. |

| East India | 16.0% | Driven by increasing urbanization, expanding FMCG distribution networks, and rising adoption of packaged consumer products. |

West India's 32.0% market leadership reflects its dual role as India's largest BOPP manufacturing and consumption geography. North India's 28.0% reflects Uttarakhand's film manufacturing, creating significant production-led market presence alongside Delhi-NCR and UP's FMCG consumption market.

South India's 24.0% reflects Tamil Nadu's food processing industry, Bengaluru's FMCG and pharmaceutical packaging demand, and the region's growing specialty packaging converter ecosystem. East India's 16.0% is the most commercially underdeveloped region with above-national-CAGR growth potential, as Bengal's food processing industry, Odisha's industrial packaging demand, and Northeast India's packaged food adoption create first-generation BOPP demand expansion above the region's historically below-national BOPP market penetration.

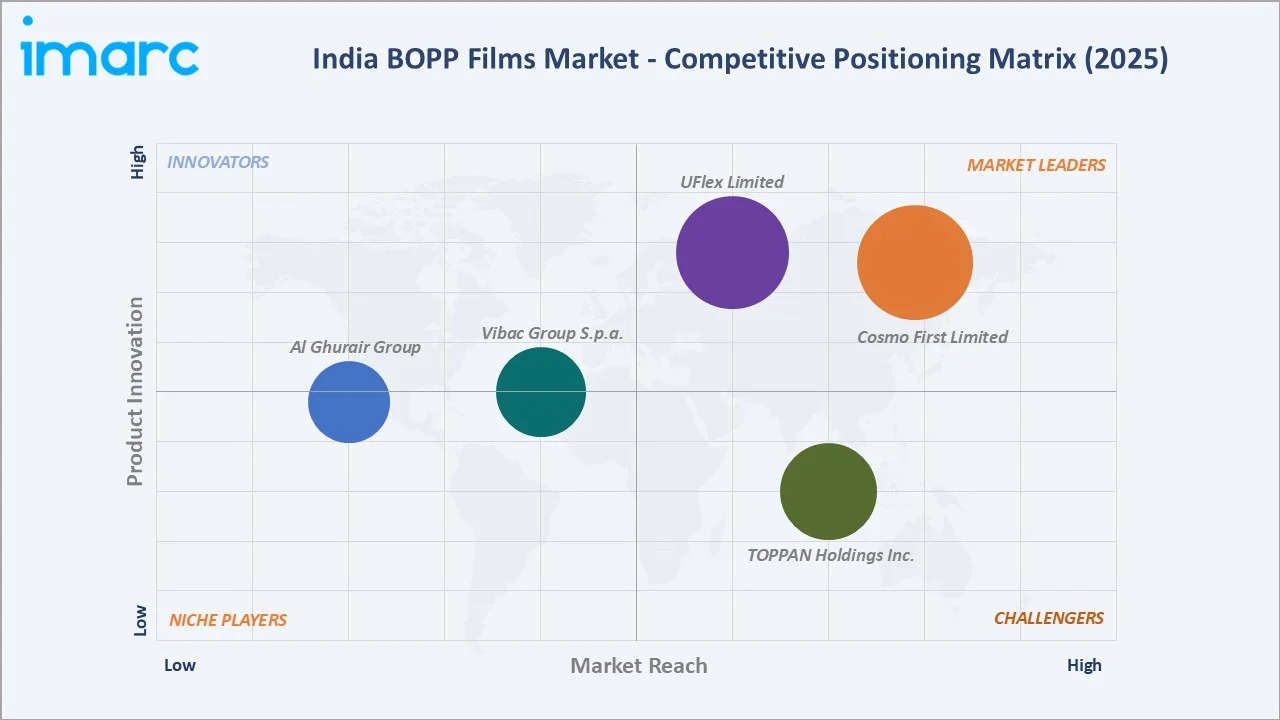

Competitive Landscape

India BOPP films market competitive landscape is a commercial oligopoly at the premium end and a more competitive structure in specialty and niche segments. The competitive landscape's most commercially defining characteristic is India's BOPP industry's capital intensity, creating a natural oligopoly through minimum efficient scale.

| Company | Key Products | Market Position | Core Strength |

|---|---|---|---|

| Cosmo First Limited | BOPP Flexible Packaging Films, BOPP Industrial Films, BOPP Lamination Films | Market Leader | Cosmo First Limited, through Cosmo Films, is a dominant leader in the Indian BOPP film industry. As one of the largest exporters of BOPP films from India, it offers specialized packaging, lamination, and labeling solutions. |

| UFlex Limited | BOPP Packaging Films, BOPP Label Films, BOPP Industrial Films, BOPP Sustainable Films | Market Leader | UFlex Limited is a dominant player in India’s BOPP films market, leveraging a massive integrated manufacturing capacity that includes packaging, label, industrial, and sustainable films. |

| Vibac Group S.p.a. | BOPP Coated and Uncoated Flexible Packaging Films, BOPP Film for Adhesive Tape | Established Player | Vibac Group S.p.a. serves as a high-end European manufacturer and supplier of specialized BOPP films and pressure-sensitive tapes to the Indian market. It supplies advanced specialty films for food packaging and labeling applications across the APAC region. |

| Al Ghurair Group | BOPP Barrier Films, BOPP Heat Resistant Packaging Films | Established Player | Al Ghurair Group plays a significant role in the Indian BOPP film market through its focus on barrier and heat-resistant packaging film solutions. |

| TOPPAN Holdings Inc. | BOPP Packaging Films | Strong Challenger | TOPPAN Holdings Inc., through Toppan Speciality Films Private Limited (TSF), is a major player in the Indian BOPP film market, focusing on high-performance, sustainable, and recyclable flexible packaging solutions. |

The competitive landscape is being reshaped by the specialization imperative, commodity plain BOPP's thin margins creating structural incentive for India's BOPP manufacturers to invest in specialty film grades, coating, and metallizing that create above-commodity commercial returns.

Key Company Profiles

Cosmo First Limited

Cosmo First Limited, through its films business Cosmo Films, is one of the leading players in the India BOPP films market and a manufacturer of specialty films used in packaging, lamination, labeling, and industrial applications.

- Key Products: BOPP Flexible Packaging Films, BOPP Industrial Films, BOPP Lamination Films.

- Recent Developments: In December 2025, Cosmo Films strengthened its flexible packaging portfolio in India by launching advanced packaging films tailored for the fast-growing pet food segment. The company introduced specialized BOPP, CPP, and BOPET films for applications such as dry kibble, wet pet food, treats, and ready-to-eat pet food products.

- Strategic Focus: Strengthening its position in the India BOPP films market through the expansion of its specialty films portfolio, targeting high-growth applications in packaging, labeling, lamination, and industrial sectors.

UFlex Limited

UFlex Limited is one of India’s largest multinational flexible packaging and packaging films companies, with a strong presence across the BOPP films value chain. The company operates an integrated packaging business spanning packaging films, flexible packaging, chemicals, aseptic packaging, holography, engineering, and printing cylinders.

- Key Products: BOPP Packaging Films, BOPP Label Films, BOPP Industrial Films, BOPP Sustainable Films.

- Recent Developments: In November 2025, UFlex Ltd plans to set up a 54,000 tonnes-per-year BOPP film line at its Dharwad complex in Karnataka, India. The company intends to invest over INR 7 billion, or around US$79 million, in the new facility, which is expected to commence operations by the fiscal year ending March 2028.

- Strategic Focus: Expanding its leadership position in the India BOPP films market through capacity expansion, specialty film development, and sustainable packaging innovation.

Market Concentration Analysis

India BOPP films market is moderately concentrated among domestic manufacturers and highly fragmented in terms of converter customers. The market's oligopolistic manufacturing structure reflects BOPP film's capital intensity, creating a minimum efficient scale above most smaller manufacturers' capital capabilities.

Market concentration is increasing through two mechanisms: domestic capacity consolidation and import specialization. Competition is increasingly shifting from commodity-grade BOPP films toward specialty, high-barrier, coated, metallized, label, and sustainable film solutions, where technological capabilities and product innovation provide stronger differentiation. Large players benefit from economies of scale, integrated operations, extensive distribution networks, and export presence, while smaller manufacturers compete primarily on pricing and regional customer relationships.

Investment & Growth Opportunities

Highest Growth Segments

BOPP labels (~4.8% CAGR through organized retail and brand packaging), bags and pouches (~4.5% CAGR through D2C food brands and e-commerce), specialty barrier-coated BOPP (~6-8% CAGR from small base), monomaterial recyclable BOPP (high growth from EPR compliance mandate), BOPP export to Africa and Southeast Asia (~8-10% CAGR through market development), and pharmaceutical BOPP packaging (~7-9% CAGR through pharma packaging modernization) represent India's highest-growth BOPP film investment vectors through 2034.

Emerging Investment Opportunities

India BOPP export expansion to Sub-Saharan Africa and Southeast Asia represents the most commercially scalable export market development opportunity for India's BOPP manufacturers above the already-penetrated Middle East and European export markets.

Investment Themes

- Monomaterial recyclable BOPP product development for India's EPR-compliant packaging market: The transition from non-recyclable multi-material BOPP-BOPET-PE laminates to recyclable monomaterial BOPP-CPP all-PP packaging will be India's most commercially transformative flexible packaging material transition of 2026-2034, driven by EPR mandates, brand owner sustainability commitments, and plastic recycler demand for clean mono-material PP film feed.

- Ultra-wide tenter line investment creating the lowest-cost-per-tonne BOPP film manufacturing to sustain India's export price competitiveness: India's BOPP export competitiveness is sustained through successive ultra-wide tenter line investments that reduce per-tonne production cost through capital amortization over greater film width. Investment in India's next-generation 10.6-metre or 12-metre tenter line creates India's most competitive BOPP plain film cost structure above the current 10.4-metre generation, enabling India's BOPP manufacturers to compete against Chinese BOPP exporters in the Middle East and Africa export markets, where price per kilogram is the primary BOPP supplier selection criterion above product differentiation or origin preference.

Future Market Outlook (2026-2034)

India BOPP films market is projected to grow from USD 753.1 Million in 2025 to USD 1,103.3 Million by 2034, delivering a 4.12% CAGR over the forecast period. The market's anchor value of USD 921.4 Million in 2030 represents India's BOPP film industry at a structural inflection. The market is expected to cross the USD 1 Billion milestone by 2031-2032, as India's FMCG packaged food market expansion, organized retail growth, and e-commerce packaging demand combine with India's BOPP export market development to create above-2020-2025-trend revenue growth for India's major BOPP film manufacturers. The 4.12% CAGR reflects a commercially sustainable growth trajectory underpinned by structural demand drivers above cyclical demand that is susceptible to economic slowdown.

Three structural forces define India's BOPP film market growth through 2034: India's FMCG packaged food market's permanent expansion, creating an incremental BOPP film demand by 2034 above the 2025 baseline, EPR regulation driving monomaterial BOPP transition, creating product transition revenue above simple volume growth as higher-value specialty monomaterial BOPP commands above-plain-BOPP pricing, and India's BOPP export market development growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with India BOPP film industry stakeholders, including Plant Directors; Business Development Managers; Technical Directors; BOPP converter customers; PP resin procurement managers; and regulatory experts. Customer survey from India BOPP film buying companies.

Secondary Research

Secondary research encompassed company annual reports; IBEF India Chemicals and Petrochemicals market data; framework guidelines for plastic packaging; India BOPP film import and export data; India flexible packaging market data; and India packaging industry report. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the downstream FMCG demand linkage model: India's packaged food market volume growth multiplied by BOPP film intensity per tonne of packaged food, creating a BOPP volume demand forecast, multiplied by BOPP price trajectory. Export revenue modelled separately using the addressable market penetration rate for the Middle East and Africa BOPP import growth.

India BOPP Films Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Wraps, Bags and Pouches, Tapes, Labels, Others |

| Thickness Covered | Below 15 Microns, 15-30 Microns, 30-45 Microns, More than 45 Microns |

| Production Process Covered | Tenter, Tubular |

| Applications Covered | Food, Beverage, Tobacco, Personal Care, Pharmaceutical, Electrical and Electronics, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Cosmo First Limited, UFlex Limited, Vibac Group S.p.a., Al Ghurair Group, TOPPAN Holdings Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India BOPP films market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India BOPP films market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India BOPP films industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India BOPP Films Market Report

India BOPP films market reached USD 753.1 Million in 2025, driven by rising demand from packaged food, FMCG, labels, and flexible packaging applications. Growth in organized retail, e-commerce, premium packaging, and recyclable mono-material film solutions is further supporting market expansion.

India BOPP films market grows at 4.12% CAGR during 2026-2034, reaching USD 1,103.3 Million by 2034. Overall growth is sustained by FMCG packaged food expansion, EPR-driven monomaterial BOPP transition creating premium product demand, and India's BOPP export market development.

Wraps lead at 34.0% through India's dominant biscuit and confectionery FMCG packaging application, with India's biscuit market requiring a high amount of BOPP film annually for flow-wrap and family pack biscuit packaging being the single most commercially significant BOPP film end-use in India.

Tenter process leads at 82.0% through its superior film property capability, independent MD and TD stretch ratio control, creating application-optimized BOPP grades for every packaging application above the tubular process's balanced orientation constraint.

West India leads at 32.0% through Gujarat's Cosmo First facility, Gujarat's PP resin supply proximity, and Maharashtra's Pune and Mumbai FMCG cluster, creating the most commercially active BOPP flexible packaging demand in India.

Leading companies include Cosmo First Limited, UFlex Limited, Vibac Group S.p.a., Al Ghurair Group, and TOPPAN Holdings Inc., among others.

India BOPP films market is projected to reach approximately USD 921.4 Million by 2030, driven by FMCG packaged food expansion, EPR-compliant monomaterial BOPP adoption, creating premium specialty BOPP demand, and India BOPP export reaching through Africa and Southeast Asia market development.

Three priority investment opportunities: monomaterial recyclable BOPP product development for India's EPR-compliant packaging transition, ultra-wide 10.4-12 metre tenter line investment creating India's lowest-cost BOPP film supply for export market expansion to Africa and Southeast Asia, and specialty BOPP label film development targeting India's 100,000+ organized retail SKU label proliferation opportunity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)