India Bulk Oxygen Market Size, Share, Trends and Forecast by Delivery Mode, Form, Type, End User, and Region, 2026-2034

India Bulk Oxygen Market Summary:

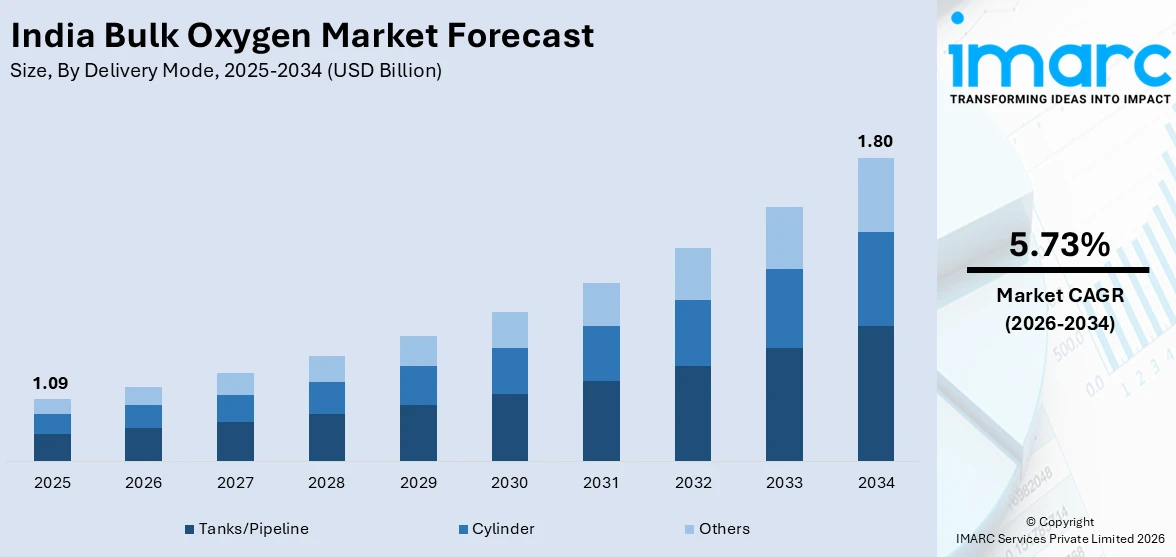

The India bulk oxygen market size was valued at USD 1.09 Billion in 2025 and is projected to reach USD 1.80 Billion by 2034, growing at a compound annual growth rate of 5.73% from 2026-2034.

The India bulk oxygen market is witnessing robust expansion, driven by the country's rapidly growing healthcare infrastructure, large-scale industrialization, and accelerating steel and chemical production sectors. Rising demand for medical-grade oxygen in hospitals and critical care units is significantly bolstering the market, alongside robust consumption in metal fabrication, oil and gas processing, and aerospace applications. Continuous investments in air separation units and cryogenic storage technologies further strengthen the market share.

Key Takeaways and Insights:

- By Delivery Mode: Tanks/pipeline dominate the market with a share of 52% in 2025, owing to their ability to ensure uninterrupted, high-volume oxygen supply to large-scale industrial and healthcare consumers, eliminating frequent cylinder changeovers and reducing per-unit distribution costs.

- By Form: Liquid oxygen leads the market with a share of 60% in 2025, driven by its higher energy density, cost-efficient transportation in cryogenic tankers, and suitability for large hospitals and industrial plants requiring consistent, high-purity oxygen supply at scale.

- By Type: Industrial prevails the market with a share of 55% in 2025, reflecting strong demand from the steel manufacturing, chemical processing, and refining industries that rely heavily on oxygen for combustion enhancement, oxidation reactions, and efficient metal processing.

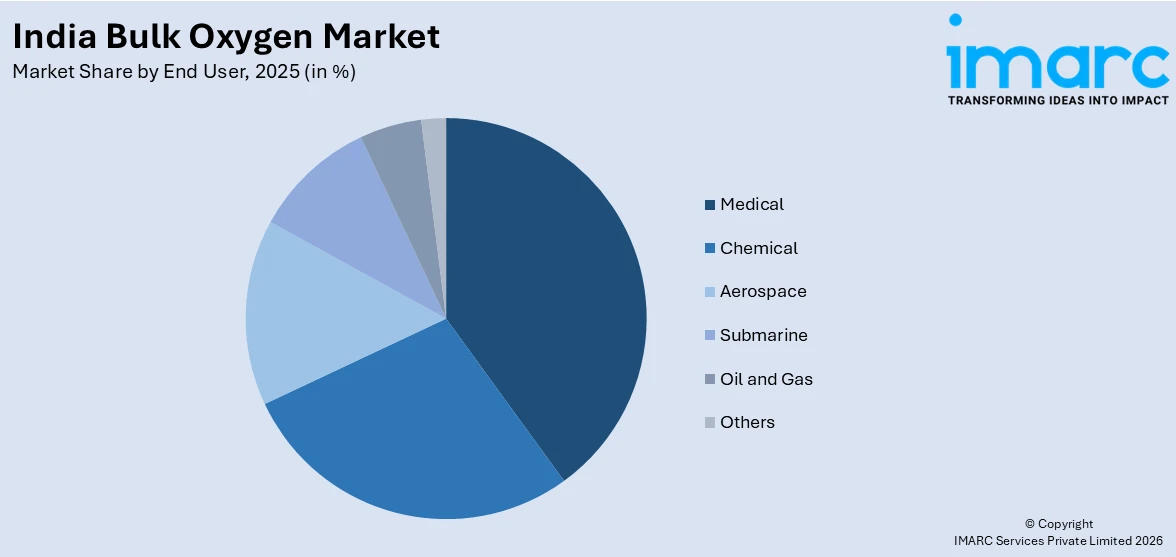

- By End User: Medical represents the largest segment with a market share of 40% in 2025, underpinned by the expanding hospital network, rising prevalence of respiratory diseases, and government initiatives to strengthen healthcare oxygen supply across public and private facilities in India.

- Key Players: Key players drive the India bulk oxygen market through strategic investments in air separation units, expanded cryogenic distribution networks, and long-term supply agreements with major industrial and healthcare clients. Their focus on digital monitoring, sustainable operations, and capacity enhancement ensures supply reliability, accelerates market penetration, and supports India's growing medical and industrial oxygen demand.

To get more information on this market Request Sample

The India bulk oxygen market is underpinned by a convergence of structural growth drivers spanning multiple high-demand sectors. India's healthcare system is rapidly expanding, with private hospitals expected to add over 4,000 new beds in FY26 alone, backed by investments of INR 11,500 Crore. This hospital expansion is directly translating into sustained demand for medical-grade liquid oxygen across intensive care units and surgical departments. Beyond healthcare, strong growth in steel manufacturing, metal fabrication, and chemical processing industries is significantly increasing industrial oxygen consumption for combustion, cutting, and oxidation processes. Infrastructure development and rising investments in manufacturing capacity are also reinforcing oxygen demand across construction-linked sectors. Additionally, the broadening of cryogenic storage and transportation infrastructure is enabling more efficient distribution of bulk oxygen across urban and semi-urban healthcare facilities and industrial clusters.

India Bulk Oxygen Market Trends:

Rise of On-Site Oxygen Generation Systems in Healthcare and Industrial Facilities

Indian hospitals and industrial facilities are increasingly adopting pressure swing adsorption (PSA) and vacuum PSA systems for on-site oxygen generation, reducing dependency on external bulk deliveries. In December 2024, the Indian Government announced the installation of 32 PSA oxygen generation facilities in Jammu and Kashmir as part of a national effort to enhance healthcare infrastructure. These installations cut transportation costs, eliminate supply chain vulnerabilities, and guarantee continuous oxygen availability during peak demand or emergency situations, making on-site generation a preferred long-term strategy for facilities across urban and rural India.

Integration of Digital Monitoring and Smart Supply-Chain Technologies

The India bulk oxygen supply ecosystem is transforming through the adoption of digital tank-monitoring platforms, telemetry systems, and automated refill management tools that enhance supply reliability and operational transparency. Industrial distributors and hospital oxygen suppliers are deploying Internet of Things (IoT)-enabled sensors that track real-time consumption patterns, generate predictive replenishment alerts, and optimize delivery routing across geographically dispersed customers. This digitalization reduces manual intervention, prevents stockouts, and enables proactive quality tracking throughout the distribution network, raising the bar for service standards across both healthcare and industrial end use segments within the market.

Expansion of Cryogenic Storage and Transportation Infrastructure

India is witnessing significant investment in cryogenic logistics infrastructure as bulk oxygen suppliers upgrade tanker fleets, expand regional filling hubs, and install advanced vacuum-insulated storage tanks at customer sites. The expansion is being driven by surging demand from hospitals, steel plants, and chemical facilities that require high-volume, reliable oxygen supply. Improved cryogenic infrastructure reduces delivery disruptions, extends the geographic reach of merchant bulk supply networks, and enhances the safety and efficiency of liquid oxygen handling. This trend is particularly relevant in tier-II and tier-III cities, where healthcare and industrial expansion is outpacing the existing distribution network's capacity.

Market Outlook 2026-2034:

The India bulk oxygen market is positioned for sustained, multi-sector growth over the forecast period, supported by ambitious industrial expansion, continued healthcare infrastructure investment, and the integration of advanced oxygen production and distribution technologies. The market generated a revenue of USD 1.09 Billion in 2025 and is projected to reach a revenue of USD 1.80 Billion by 2034, growing at a compound annual growth rate of 5.73% from 2026-2034. Increasing adoption of digital supply-chain technologies, on-site generation systems, and cryogenic infrastructure modernization will further optimize delivery reliability and cost efficiency across industrial and medical end use segments. Additionally, supportive government initiatives aimed at strengthening healthcare preparedness and domestic manufacturing capabilities are expected to further reinforce long-term demand for bulk oxygen across the country.

India Bulk Oxygen Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Delivery Mode |

Tanks/Pipeline |

52% |

|

Form |

Liquid Oxygen |

60% |

|

Type |

Industrial |

55% |

|

End User |

Medical |

40% |

Delivery Mode Insights:

- Tanks/Pipeline

- Cylinder

- Others

Tanks/pipeline dominate with a market share of 52% of the total India bulk oxygen market in 2025.

The tanks/pipeline delivery mode commands the largest share of the India bulk oxygen market, owing to its unmatched ability to provide continuous, high-volume oxygen supply to large-scale end users without the logistical constraints associated with individual cylinder management. In industrial settings, such as steel plants, refineries, and chemical processing facilities, pipeline networks deliver oxygen directly to production lines, enabling seamless, uninterrupted operations with no interruption risk from cylinder shortages or changeover delays. For major hospital complexes with high daily oxygen consumption, liquid oxygen tanks connected to internal piping systems provide a far more reliable and cost-efficient solution than cylinder-based delivery.

Cryogenic tanker deliveries to bulk liquid oxygen storage tanks installed at customer sites represent another critical component of the tanks/pipeline segment. These storage systems allow facilities to maintain substantial oxygen reserves, ensuring supply continuity during periods of peak demand, transportation delays, or supply disruptions. The Indian government's focus on bolstering oxygen self-sufficiency across public hospitals has further reinforced investments in liquid oxygen storage tanks and piped distribution infrastructure. As India's industrial and healthcare sectors continue to scale, the cost-effectiveness and operational reliability of tanks/pipeline systems ensure their enduring dominance over alternative delivery formats in the market.

Form Insights:

- Liquid Oxygen

- Compressed Oxygen

- Oxygen Gas Mixture

Liquid oxygen leads with a share of 60% of the total India bulk oxygen market in 2025.

Liquid oxygen's commanding position within the India bulk oxygen market is attributable to its superior energy density, ease of large-volume transportation, and versatility across both medical and industrial applications. Hospitals depend on bulk liquid oxygen supplies to maintain continuous pipeline distribution through medical gas manifold systems, which are essential for intensive care units, surgical theatres, and emergency departments. In July 2024, Air Liquide India inaugurated a new air separation unit in Kosi Kalan, Uttar Pradesh, with a daily production capacity exceeding 365 Tons of liquid oxygen and medical oxygen.

In industrial applications, liquid oxygen is the preferred supply format for steel plants, petrochemical refineries, and glass manufacturers that require large, continuous volumes of high-purity oxygen for blast furnace operations, oxidation reactions, and combustion enhancement. The ability to vaporize liquid oxygen on demand and deliver it through pipeline networks makes it ideal for facilities with fluctuating but high average oxygen requirements. Expanding cryogenic logistics infrastructure, including modernized tanker fleets and regional filling stations, is enhancing the geographic coverage of liquid oxygen distribution across India, enabling market penetration into emerging industrial corridors and secondary healthcare hubs beyond major metropolitan centers.

Type Insights:

- Industrial

- Medical

Industrial exhibits a clear dominance with a 55% share of the total India bulk oxygen market in 2025.

Industrial accounts for the majority of bulk oxygen consumption in India, underpinned by the country's rapidly scaling steel production, chemical processing, refining, and metal fabrication sectors. Oxygen is a critical input in blast furnace-basic oxygen furnace steelmaking, where it is injected to accelerate decarburization and improve furnace efficiency. India produced 151.1 Million Tons of crude steel in FY 2024–25, and its National Steel Policy targets 300 Million Tons of capacity by 2030–31, signaling a proportional and sustained increase in industrial oxygen demand.

Beyond steel, industrial oxygen plays an essential role in chemical synthesis, water treatment, glass manufacturing, and oil and gas processing operations across India. The government's Make in India initiative has catalyzed domestic manufacturing investment across multiple industries, driving up aggregate industrial oxygen consumption. The need for oxygen in production facilities is increasing due to the growth of industrial clusters and the construction of new manufacturing parks. Furthermore, the use of high-purity bulk oxygen sources is increasing as improved combustion and oxidation technologies are incorporated into industrial processes.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Chemical

- Aerospace

- Submarine

- Oil and Gas

- Medical

- Others

Medical represents the leading segment with a 40% share of the total India bulk oxygen market in 2025.

The medical end user segment is the largest single consumer of bulk oxygen in India, reflecting the country's vast and expanding healthcare infrastructure and the critical role of oxygen therapy across a wide spectrum of clinical applications. Indian hospitals rely on bulk liquid oxygen and piped distribution systems for intensive care units, surgical procedures, anesthesia delivery, and respiratory disease management. The prevalence of chronic respiratory conditions, such as asthma, combined with rising cardiovascular disease burden, is sustaining baseline medical oxygen demand across public and private healthcare facilities.

Large-scale government initiatives have further bolstered the medical oxygen supply infrastructure. The medical segment also benefits from the integration of digital monitoring technologies that enable predictive oxygen replenishment, reducing the risk of supply shortfalls in critical care environments. As India's hospital network expands into tier-II and tier-III cities, the medical end user segment will continue to be the primary demand anchor for the India bulk oxygen market.

Regional Insights:

- North India

- South India

- East India

- West India

North India is a significant market for bulk oxygen, driven by the high concentration of industrial facilities, major hospital networks, and significant steel and chemical manufacturing activity across states, such as Uttar Pradesh, Delhi-NCR, Rajasthan, and Madhya Pradesh. North India's dense population and expanding private hospital infrastructure further sustain strong demand for medical-grade bulk oxygen.

In South India, the market is supported by a robust industrial base, encompassing steel, pharmaceuticals, chemicals, and aerospace sectors across Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana. The region's advanced healthcare infrastructure and concentration of multi-specialty hospitals, which account for a significant share of national medical tourism revenue, sustain high medical oxygen consumption. Rapidly expanding manufacturing corridors and smart city initiatives across the region are expected to reinforce industrial oxygen demand over the forecast period.

East India is an emerging growth region for bulk oxygen, anchored by the large steel manufacturing complexes of Odisha, Jharkhand, and West Bengal. The presence of integrated steel plants and metal processing facilities is generating strong and consistent industrial oxygen demand across the region. Additionally, expanding infrastructure and manufacturing projects are further strengthening the requirement for bulk oxygen in fabrication, welding, and heavy industrial operations.

West India represents a major hub for bulk oxygen demand, driven by the region’s strong concentration of chemical, petrochemical, pharmaceutical, and metal processing industries across Gujarat and Maharashtra. Large industrial clusters, refineries, and manufacturing facilities rely extensively on oxygen for combustion, oxidation, and process optimization applications. In addition, the presence of advanced healthcare infrastructure and major metropolitan hospital networks in cities, such as Mumbai, Pune, and Ahmedabad, sustains steady demand for medical-grade bulk oxygen.

Market Dynamics:

Growth Drivers:

Why is the India Bulk Oxygen Market Growing?

Expanding Healthcare Infrastructure and Rising Respiratory Disease Burden

India's healthcare system is undergoing a fundamental transformation, with large-scale investments in hospital construction, intensive care unit (ICU) expansion, and emergency care infrastructure creating sustained, long-term demand for bulk medical oxygen. At the same time, the growing incidence of respiratory conditions, such as chronic obstructive pulmonary disease, asthma, pneumonia, and other lung-related illnesses, is leading to higher hospitalization rates and longer treatment durations requiring oxygen support. In 2023, it was estimated that 35 Million individuals were affected by asthma in India. Increasing air pollution levels and heightened health awareness are further contributing to rising need for oxygen therapy. The growing geriatric population, which is more susceptible to respiratory and cardiovascular conditions, further amplifies this demand. Government programs are extending quality healthcare access to tier-II and tier-III cities, where new hospital facilities are being commissioned at an accelerating pace, each requiring bulk oxygen supply infrastructure.

Rapid Industrialization and Expansion of Steel and Chemical Manufacturing

India's industrial sector is a primary engine of bulk oxygen demand, with steel, chemical processing, refining, and metal fabrication industries collectively representing the largest consumption base for industrial-grade oxygen in the country. Oxygen is a fundamental input in blast furnace and basic oxygen furnace steelmaking processes, where it is injected to accelerate carbon removal, improve combustion efficiency, and enhance product quality. The Steel Ministry projects steel demand to grow by 8% annually in 2024 and 2025, driven by the government's National Infrastructure Pipeline, which encompasses planned infrastructure investments across roads, railways, ports, and urban development. Chemical and petrochemical plants rely on oxygen for oxidation reactions, partial combustion, and wastewater treatment, while the glass, cement, and paper industries use oxygen enrichment to improve furnace performance and reduce fuel consumption. The government's Make in India initiative and Production Linked Incentive schemes have attracted significant manufacturing investment across multiple sectors, creating new and growing pockets of industrial oxygen demand across India's expanding industrial corridors and special economic zones.

Technological Advancements in Oxygen Production and Distribution Infrastructure

The India bulk oxygen market is benefiting from sustained technological innovation across the full production and distribution value chain, from air separation unit efficiency improvements to advanced cryogenic logistics and digital monitoring platforms. Modern cryogenic air separation units, incorporating advanced heat exchangers, optimized compressors, and efficient liquefaction modules, are significantly improving oxygen production yields while reducing energy consumption per ton of output. Leading industrial gas companies are investing heavily in new-generation plants in India. On the distribution side, companies are deploying IoT-enabled telemetry systems that monitor oxygen tank levels in real time, optimize delivery routing, and generate predictive replenishment alerts, significantly reducing stockout risks and improving supply chain efficiency. The adoption of vacuum-insulated bulk storage tanks, modular on-site generation units, and upgraded cryogenic tanker fleets is extending the geographic reach of bulk oxygen supply networks into secondary cities and industrial corridors.

Market Restraints:

What Challenges the India Bulk Oxygen Market is Facing?

High Capital Expenditure for Air Separation and Cryogenic Infrastructure

The establishment of large-scale air separation units and cryogenic storage infrastructure requires substantial upfront capital investment, creating entry barriers for new market participants and constraining the pace of supply network expansion in underserved regions. The high cost of specialized cryogenic tankers, vacuum-insulated storage tanks, and air separation equipment limits the ability of smaller regional distributors to scale their operations, potentially creating supply gaps in remote industrial clusters and rural healthcare facilities where oxygen access remains a critical challenge.

Logistical Complexities and Cold Chain Distribution Challenges

Distributing liquid oxygen across India's diverse and often challenging geography presents significant logistical hurdles, including road infrastructure limitations, extreme temperature variations, and the specialized handling requirements of cryogenic materials. Ensuring the integrity of the cold chain from production facility to end user demands advanced logistics coordination, trained personnel, and compliant transportation equipment, which adds complexity and cost to the supply chain. In remote regions and tier-III cities, inadequate road connectivity and limited availability of trained cryogenic logistics operators can disrupt the reliability of bulk oxygen deliveries to hospitals and industrial customers.

Price Regulation and Government Control on Medical Oxygen Pricing

The Government of India classifies medical oxygen as an essential drug, with pricing regulated by the National Pharmaceutical Pricing Authority. While this regulation serves an important public health function by ensuring oxygen affordability for patients, it constrains the revenue realization and profit margins of bulk oxygen suppliers in the medical segment. The regulatory framework limits the ability of suppliers to pass on rising energy, transportation, and raw material costs to medical end users, potentially dampening investment incentives for expanding medical-grade oxygen production and distribution infrastructure in underserved areas.

Competitive Landscape:

The India bulk oxygen market features a moderately consolidated competitive structure, dominated by multinational industrial gas corporations with deep technical expertise, large-scale production assets, and established long-term supply agreements with major industrial and healthcare clients. Market participants compete primarily on production reliability, supply security, pricing structures, geographic distribution reach, and the ability to offer integrated digital supply management services. Differentiation is increasingly driven by technology investments in advanced air separation, cryogenic logistics modernization, and on-site generation capabilities. Leading players are actively expanding their Indian asset bases through new air separation unit construction, strategic acquisitions, and long-term supply partnerships with steel majors, petrochemical companies, and hospital networks, reinforcing barriers to entry for smaller regional competitors.

India Bulk Oxygen Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Delivery Modes Covered | Tanks/Pipeline, Cylinders, Others |

| Forms Covered | Liquid Oxygen, Compressed Oxygen, Oxygen Gas Mixtures |

| Types Covered | Industrial, Medical |

| End Users Covered | Chemical, Aerospace, Submarine, Oil and Gas, Medical, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request |

Frequently Asked Questions About the India Bulk Oxygen Market Research Report and Industry Forecast Report

The India bulk oxygen market size was valued at USD 1.09 Billion in 2025.

The India bulk oxygen market is expected to grow at a compound annual growth rate of 5.73% from 2026-2034 to reach USD 1.80 Billion by 2034.

Tanks/pipeline dominated the market with a share of 52%, driven by its ability to provide continuous, high-volume oxygen supply to large steel plants, chemical facilities, and hospital complexes with centralized piped distribution systems, ensuring operational reliability and cost efficiency.

Key factors driving the India bulk oxygen market include the rapid expansion of healthcare infrastructure, accelerating steel and chemical manufacturing, government medical oxygen self-sufficiency programs, increasing investments in air separation units, and growing adoption of cryogenic storage and digital supply-chain management technologies.

Major challenges include high capital expenditure for air separation and cryogenic infrastructure, logistical complexities in cold-chain distribution across remote and tier-III regions, government price regulation on medical oxygen limiting supplier margin expansion, and dependence on energy-intensive production processes susceptible to input cost volatility.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)