India Candy Market Size, Share, Trends and Forecast by Type, Flavour, Sugar Content, Nature, Distribution Channel, and Region, 2026-2034

India Candy Market Summary:

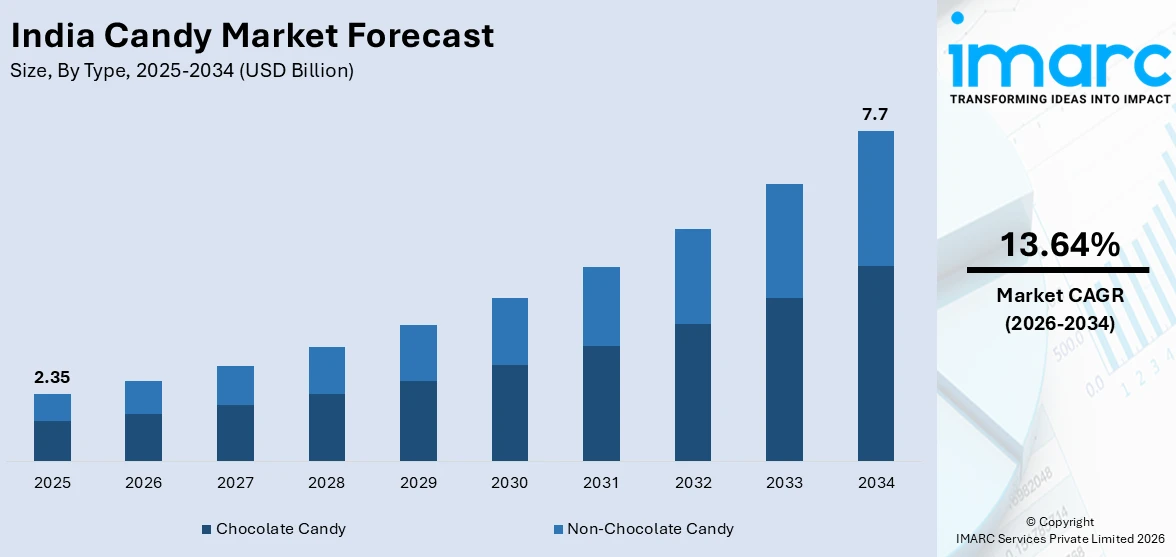

The India candy market size was valued at USD 2.35 Billion in 2025 and is projected to reach USD 7.7 Billion by 2034, growing at a compound annual growth rate of 13.64% from 2026-2034.

The India candy market is witnessing a substantial growth due to the increasing disposable incomes, urbanization, and behavioral changes among the consumers in the country. The increasing demand for quality and unique candies, along with the increasing young population in the country, is driving the market. The development of modern retailing models, increasing penetration of e-commerce, and increasing awareness among the consumers about brands are also adding to the India candy market share.

Key Takeaways and Insights:

-

By Type: Chocolate candy dominates the market with a share of 54.1% in 2025, driven by growing consumer preference for premium chocolate-based confections and the cultural shift toward chocolate gifting during festivals and celebrations.

-

By Flavour: Sweet leads the market with a share of 49.6% in 2025, reflecting the deep-rooted Indian consumer preference for sweet taste profiles across candy categories and age demographics.

-

By Sugar Content: With-added sugar holds the largest share of 78.4% in 2025, underpinned by strong consumer demand for traditional sugar-based confectionery products and their widespread availability across all retail channels.

-

By Nature: Regular dominates the market with a share of 86.3% in 2025, supported by mass-market affordability, broad consumer acceptance, and extensive distribution across urban and rural retail networks.

-

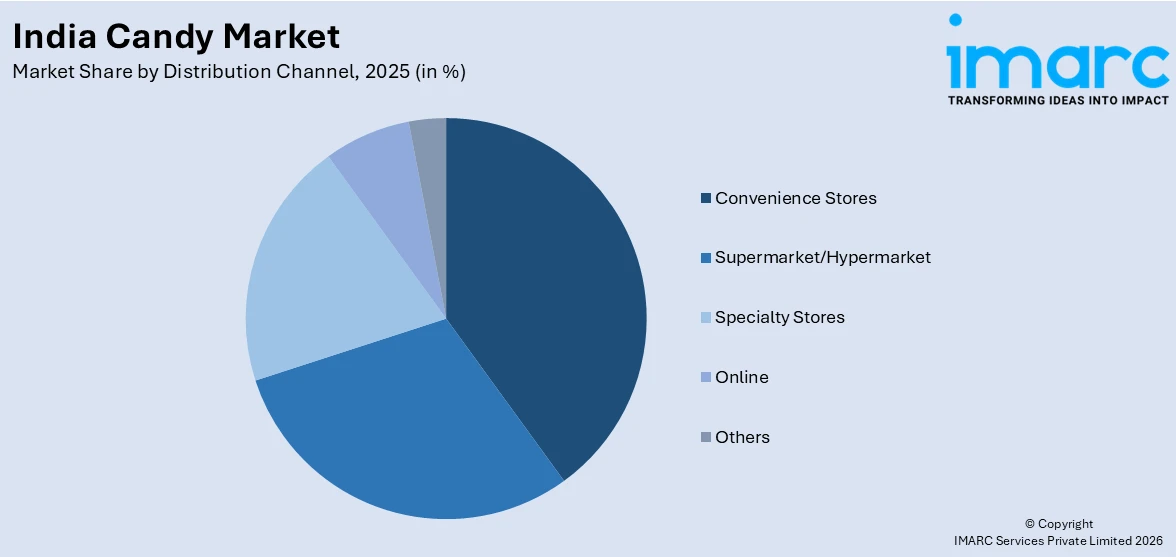

By Distribution Channel: Convenience stores leads the market with a share of 34.2% in 2025, owing to the extensive network of neighborhood retail outlets that facilitate impulse purchasing and everyday candy accessibility.

-

By Region: North India dominates the market with a share of 33.7% share in 2025, driven by high population density, robust urban centers, and a strong tradition of confectionery consumption during festivals and social occasions.

-

Key Players: The India candy market features a competitive landscape with both multinational and domestic manufacturers vying for market share through flavor innovation, product diversification, strategic pricing, and extensive distribution network expansion across urban and rural markets.

To get more information on this market Request Sample

The Indian candy industry is also undergoing a paradigm shift as the manufacturers are blending traditional Indian flavors with modern candy packaging formats. For example, in July 2025, Dharampal Satyapal Group’s Pulse candy, a hard‑boiled Indian candy brand, recorded over INR 750 crore in consumer sales in FY 2024‑25, maintaining its leadership in the segment and highlighting strong consumer demand for localized flavor profiles. The increasing middle-class population with rising purchasing power is also contributing to the demand for both premium and affordable candy products. Innovation in the candy flavor category has emerged as a major differentiator as the manufacturers are blending regional spices, tangy, and fusion concepts to suit the diverse palates of the consumers belonging to different age groups. The increasing organized retail space and the quick commerce business model are also making candy products more accessible to consumers in tier-II and tier-III cities.

India Candy Market Trends:

Growing Premiumization and Indulgence-Driven Consumption

The market for candies in India is observing a significant shift towards the consumption of high-end and indulgent candies. In December 2025, Perfetti Van Melle India, maker of brands like Chupa Chups, Mentos, and Alpenliebe, announced it is strategically pushing higher‑priced ₹5 and ₹10 candy SKUs to balance its portfolio and cater to evolving consumer tastes beyond the traditional Re 1 segment. This is being led by the growing demand for a superior taste experience. As a result, manufacturers are introducing artisanal chocolate candies, high-end gifting lines, and gourmet lines that include exotic ingredients. The growing trend of indulgent gifting of confectionery products during festivals and events is further contributing to the demand for high-end candies. The growing exposure to international standards of confectionery products through travel, digital media, and international retail formats is also impacting consumer preferences.

Integration of Regional and Fusion Flavors

The confectionery industry is also seeing more and more candy manufacturers incorporating traditional Indian ingredients and flavor profiles into their product offerings. In October 2024, ITC’s Candyman brand launched its Candyman Tadka Lollipop featuring green mango and tamarind with a masala‑filled core, reflecting how major players are experimenting with sweet, tangy and spicy fusion flavours rooted in Indian tastes. Fusion flavors that are a mix of tangy, spicy, and sweet are also seeing a lot of success. The company is using indigenous ingredients such as raw mango, tamarind, paan, and local spices to create a culturally relevant candy experience that blends traditional flavors with modern formats. This approach to localization allows the company to create an emotional connect with its consumers while also increasing its appeal across different geographies and demographics.

Expansion of Health-Conscious and Functional Candy Variants

Rising health awareness among Indian consumers is accelerating demand for sugar-free, organic, and functional candy alternatives that offer indulgence without compromising wellness objectives. The India sugar‑free confectionery market size reached USD 72.23 Million in 2024, and IMARC Group projects it could reach USD 120.22 Million by 2033, reflecting the growing popularity of healthier candy options among Indian consumers. Manufacturers are investing in formulations using natural sweeteners, herbal extracts, and fortified ingredients to cater to health-conscious demographics. The growing prevalence of lifestyle-related health concerns, particularly among urban populations, is prompting a shift toward confectionery products with reduced sugar content and added nutritional benefits. This trend is especially prominent among younger consumers and working professionals who seek guilt-free snacking options that align with their broader dietary and wellness priorities.

Market Outlook 2026-2034:

The outlook for the confectionery industry in India is set to remain positive as the factors of urbanization, demographics, and evolving consumption patterns continue to provide favorable conditions for growth. The industry is expected to witness increased focus on innovations in flavors, eco-friendly packaging, and online distribution channels to tap new consumer groups. The growth of tier-II and tier-III cities through modern retail and online channels is expected to tap new demand in the industry. In addition, new investments in health-oriented product development are also expected to diversify the consumer base. The market generated a revenue of USD 2.35 Billion in 2025 and is projected to reach a revenue of USD 7.7 Billion by 2034, growing at a compound annual growth rate of 13.64% from 2026-2034.

India Candy Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Chocolate Candy |

54.1% |

|

Flavour |

Sweet |

49.6% |

|

Sugar Content |

With-Added Sugar |

78.4% |

|

Nature |

Regular |

86.3% |

|

Distribution Channel |

Convenience Stores |

34.2% |

|

Region |

North India |

33.7% |

Type Insights:

- Chocolate Candy

- Non-Chocolate Candy

The chocolate candy dominates with a market share of 54.1% of the total India candy market in 2025.

The chocolate candies market is continuing to maintain its leading market position in the Indian confectionery market due to the rising preference for chocolate-based candies and the popularity of gifting high-quality chocolates during celebrations and festivals. Urbanization and the adoption of international confectionery quality standards have also accelerated the adoption of chocolate candies among the younger generation due to the introduction of a wide range of variants such as filled chocolates, coated candies, and fusion variants that combine traditional Indian flavors with chocolate bases by the confectionery manufacturers. The category's ability to support both impulse and planned purchases has further strengthened its market leadership position.

The category is also supported by robust brand investments in innovation and marketing campaigns that promote chocolate candies as both a daily indulgence and a premium gift option. The leading confectionery manufacturers are also expanding their product offerings with artisanal, dark, and sugar-free chocolate candy variants to target the rising demand from health-conscious and premium-seeking consumers. In addition, the increasing penetration of modern retail and online shopping platforms is also improving product visibility and accessibility, allowing chocolate candy brands to target a wider range of consumers across urban, semi-urban, and emerging rural markets in India.

Flavour Insights:

- Sweet

- Sour

- Mixed Flavor

The sweet leads with a share of 49.6% of the total India candy market in 2025.

The sweet flavor segment retains its dominant position within India's candy market, reflecting the country's deeply ingrained cultural affinity for sweet taste profiles across confectionery products. Traditional preferences rooted in India's rich heritage of sweet consumption during festivals, weddings, and religious celebrations continue to reinforce demand for sweet-flavored candies. Manufacturers leverage this preference by developing diverse sweet candy formats ranging from classic toffees and caramels to modern gummy and chocolate-based offerings that cater to evolving consumer expectations while preserving familiar taste experiences.

The appeal of this product category extends to all age groups and economic classes, with sweet-flavored candies being the indulgences that are within reach in impulse as well as planned purchases. The major players in the confectionery industry have large product portfolios that include sweet-flavored candies, which are available in all retail formats, thus ensuring that the market leadership of this product category is maintained. In addition, the blending of traditional Indian sweets like jaggery, cardamom, and mango with modern candies is helping manufacturers engage with consumers.

Sugar Content Insights:

- Sugar-Free

- With-Added Sugar

The with-added sugar dominates with a market share of 78.4% of the total India candy market in 2025.

The with-added sugar segment commands the overwhelming majority of India's candy market, supported by strong consumer preference for traditional sugar-based confections and their deep integration into everyday consumption habits. Affordability and widespread availability across all retail formats, from neighborhood kirana stores to modern supermarkets, ensure consistent demand for conventional sugar-sweetened candy products. The segment encompasses the broadest range of candy formats, including hard-boiled sweets, toffees, caramels, and chocolate candies, catering to diverse taste preferences across the country.

The price-conscious consumer base in India remains favorably disposed towards sugar-based candies that are value-for-money, especially in the rural and semi-urban sectors, where candies are a treat that is accessible to all sections of society. The massive distribution network that reaches millions of conventional retail stores ensures that sugar-sweetened candies remain visible and accessible in the market at affordable prices. Moreover, the deep-rooted emotional and cultural associations of sugar-based confectionery with celebrations and indulgences ensure that the habitual consumption patterns continue to sustain the commanding market presence of the segment.

Nature Insights:

- Organic

- Regular

The regular leads with a share of 86.3% of the total India candy market in 2025.

The regular candy segment maintains its overwhelming dominance in India's candy market, driven by mass-market affordability, extensive manufacturing infrastructure, and widespread distribution networks that ensure product availability across the country's diverse retail landscape. Conventional candy products cater to the broadest consumer base, with pricing strategies spanning multiple price points that address varied consumption occasions and income levels. The segment's deep penetration across both organized and unorganized retail channels further strengthens its accessibility among urban and rural consumers alike.

The segment benefits from established consumer trust in familiar brands and formats, with both multinational and domestic manufacturers maintaining large-scale production capacities for regular candy products. The extensive reach of India's vast network of kirana stores and neighborhood outlets creates a robust distribution backbone that sustains regular candy accessibility even in remote rural markets. Additionally, strong brand recall built through decades of consistent marketing, wide product assortments, and culturally resonant flavor offerings reinforces habitual purchasing behavior that underpins the segment's commanding market position.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarket/Hypermarket

- Convenience Stores

- Specialty Stores

- Online

- Others

The convenience stores dominates with a market share of 34.2% of the total India candy market in 2025.

Convenience stores continue to hold the top position in the candy distribution market in India, thanks to the extensive network of convenience stores and kirana shops that act as the main point of impulse candy sales. The convenience stores enjoy the advantage of having the closest proximity to the customers, thus facilitating easy and frequent candy sales, even if the value is low. The personalized shopping experience and credit sales provided by the convenience stores ensure a loyal customer base.

The segment's dominance is further sustained by the strategic importance these outlets hold for candy manufacturers' distribution strategies. Major confectionery brands maintain extensive direct distribution networks to service convenience stores, ensuring consistent product availability and shelf visibility across diverse geographic territories. The continued digitization of these stores through B2B ordering platforms and digital payment integration is enhancing operational efficiency while preserving their fundamental role as the primary candy retail channel. This evolving infrastructure enables convenience stores to remain competitive alongside modern retail formats and emerging quick commerce platforms.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 33.7% share of the total India candy market in 2025.

North India maintains its position as the largest regional candy market, underpinned by high population density, robust urban centers including the Delhi NCR metropolitan area, and a deep-rooted tradition of confectionery consumption during festivals, weddings, and religious occasions. The region benefits from well-developed retail infrastructure and strong e-commerce penetration that enhance product accessibility across urban and semi-urban areas. North India's concentration of manufacturing facilities, including major confectionery production plants, supports efficient supply chain operations and rapid market distribution.

The region's diverse consumer base spanning multiple income segments drives demand across both premium and value candy categories. The presence of established domestic and multinational confectionery manufacturers strengthens competitive dynamics and accelerates product innovation tailored to regional taste preferences. Furthermore, the rapid expansion of modern retail formats, quick commerce platforms, and organized distribution networks across North India's tier-II and tier-III cities is unlocking new consumer segments and reinforcing the region's strategic importance as the primary growth engine for India's candy market.

Market Dynamics:

Growth Drivers:

Why is the India Candy Market Growing?

Rising Disposable Incomes and Expanding Middle-Class Population

The growing middle-class population in India and the subsequent rise in their household disposable incomes are creating conducive market conditions for the increased consumption of confectionery products. With rising purchasing power, consumers are showing increased willingness to spend on indulgent treats and high-end confectionery products that provide enhanced taste experiences. For instance, premium and branded confectionery makers have reported notable performance in smaller cities, online gifting platform Winni saw 55% of its chocolate sales coming from tier‑II and tier‑III cities as of 2023, underscoring growing consumer spending power and premiumisation beyond major metros. This is especially true in tier-II and tier-III cities, where the rising affluence is leading to the first-time adoption of branded confectionery products. The growing consumer base is encouraging manufacturers to create a range of products across various price segments, thus increasing market penetration.

Rapid Urbanization and Evolving Consumer Lifestyles

The rapidly growing urbanization trend in India is, in essence, transforming the consumption behavior of confectionery products in the country as the rising urban population is increasingly adopting a snacking pattern that is convenience-driven and, therefore, favors confectionery products. For instance, confectionery major Perfetti Van Melle India reported in 2025 that its products reach nearly 5.5 million retail outlets across the country, highlighting how extensive distribution networks enable easy access to candies and impulse snacks for urban consumers. The rising urban population, especially working professionals, students, and young individuals, are increasingly resorting to candies as a quick and affordable way to indulge in a treat that suits their fast-paced lifestyle. This is, in turn, increasing the potential consumer base for the candy industry while also fueling the growth of modern retailing formats that improve product visibility and impulse buying.

Intensifying Product Innovation and Flavor Diversification

The competitive environment in the Indian candy industry is also pushing manufacturers to innovate constantly through new flavors, textures, and forms that appeal to the changing preferences of consumers. For instance, in September 2024, ITC Foods launched Candyman Sourzzz, marking its entry into the sour candy segment with bold and tangy variants designed to deliver new taste sensations and attract younger consumers seeking unique confectionery experiences. Manufacturers are using a mix of regional Indian ingredients, fusion flavors, and innovative experiences to differentiate their products in the market, which is becoming increasingly saturated. The innovation challenge includes categories such as sour candies, functional confections, caffeinated variants, and traditional spice-infused candies that appeal to different segments of consumers. The focus on innovative taste experiences helps brands to attract consumer attention and build long-term loyalty.

Market Restraints:

What Challenges the India Candy Market is Facing?

Rising Health Consciousness and Sugar Reduction Pressure

Growing consumer awareness about the adverse health effects of excessive sugar consumption, including diabetes and obesity concerns, is creating headwinds for traditional sugar-based candy products. Regulatory initiatives including prominent nutritional labeling requirements by the Food Safety and Standards Authority of India are further intensifying scrutiny on confectionery products, compelling manufacturers to invest in reformulation efforts and healthier alternatives that increase production costs.

Impact of Digital Payments on Low-Value Candy Transactions

The widespread adoption of Unified Payments Interface and digital wallets has inadvertently reduced the historical role of low-cost candies as substitutes for small change in cash transactions. This behavioral shift has diminished a traditional consumption occasion for affordable candy products, particularly in neighborhood retail settings, prompting manufacturers to reassess pricing strategies and develop new value propositions for the entry-level candy segment.

Volatile Raw Material Costs and Supply Chain Pressures

Fluctuations in prices of key raw materials including sugar, cocoa, dairy ingredients, and packaging materials pose significant challenges to candy manufacturers’ profit margins. Supply chain complexities in managing product freshness and quality across India’s diverse geographic and climatic conditions add operational costs, while increasing competition from both organized and unorganized players intensifies pricing pressures throughout the value chain.

Competitive Landscape:

The India candy market has a highly competitive environment with the coexistence of global confectionery majors and established Indian players. Global players have strong market presence due to their strong brands, extensive distribution networks, and substantial investments in marketing and R&D. Indian players compete effectively in the market through their indigenous flavor development, competitive pricing, and strong penetration in the traditional distribution channel, as they are well aware of the consumer preferences in the region. Players in the market are increasingly making investments in product diversification, premiumization, health-oriented alternatives, and digital marketing capabilities to tap the emerging consumer segments. Strategic moves such as new product development, mergers and acquisitions, expansion of manufacturing capacities, and collaborations with modern retail and online shopping platforms are increasingly intensifying the competition and fueling the market growth.

Recent Developments:

-

In November 2025, Pulse Candy, the popular tangy hard candy brand from the Dharampal Satyapal Group, has launched India’s first blow‑controlled digital game, Candy Day The Pulse Way: Surfing Edition, to mark National Candy Day 2025. Developed with MakeAR, the interactive mobile game lets players control a surfing avatar by blowing into their device, targeting digital engagement among Gen‑Z users.

India Candy Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Chocolate Candy, Non-Chocolate Candy |

|

Flavours Covered |

Sweet, Sour, Mixed Flavor |

|

Sugar Contents Covered |

Sugar-Free, With-Added Sugar |

|

Natures Covered |

Organic, Regular |

|

Distribution Channels Covered |

Supermarket/Hypermarket, Convenience Stores, Specialty Stores, Online, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Candy Market Report

The India candy market size was valued at USD 2.35 Billion in 2025.

The India candy market is expected to grow at a compound annual growth rate of 13.64% from 2026-2034 to reach USD 7.7 Billion by 2034.

Chocolate candy, holding the largest share of 54.1%, leads India’s candy market driven by growing consumer preference for premium chocolate-based confections, the cultural shift toward chocolate gifting, and increasing product innovation across diverse chocolate candy formats.

Key factors driving the India candy market include rising disposable incomes, rapid urbanization, expanding modern retail and e-commerce channels, product innovation in flavors and formats, growing youth population, and cultural significance of confectionery consumption.

Major challenges include rising health consciousness about sugar consumption, the impact of digital payments on low-value candy transactions, volatile raw material costs, intense competition across organized and unorganized sectors, and distribution complexities in managing product freshness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)