India Car Insurance Market Size, Share, Trends and Forecast by Coverage, Application, Distribution Channel, and Region, 2026-2034

India Car Insurance Market Size, Share, Trends & Forecast (2026-2034)

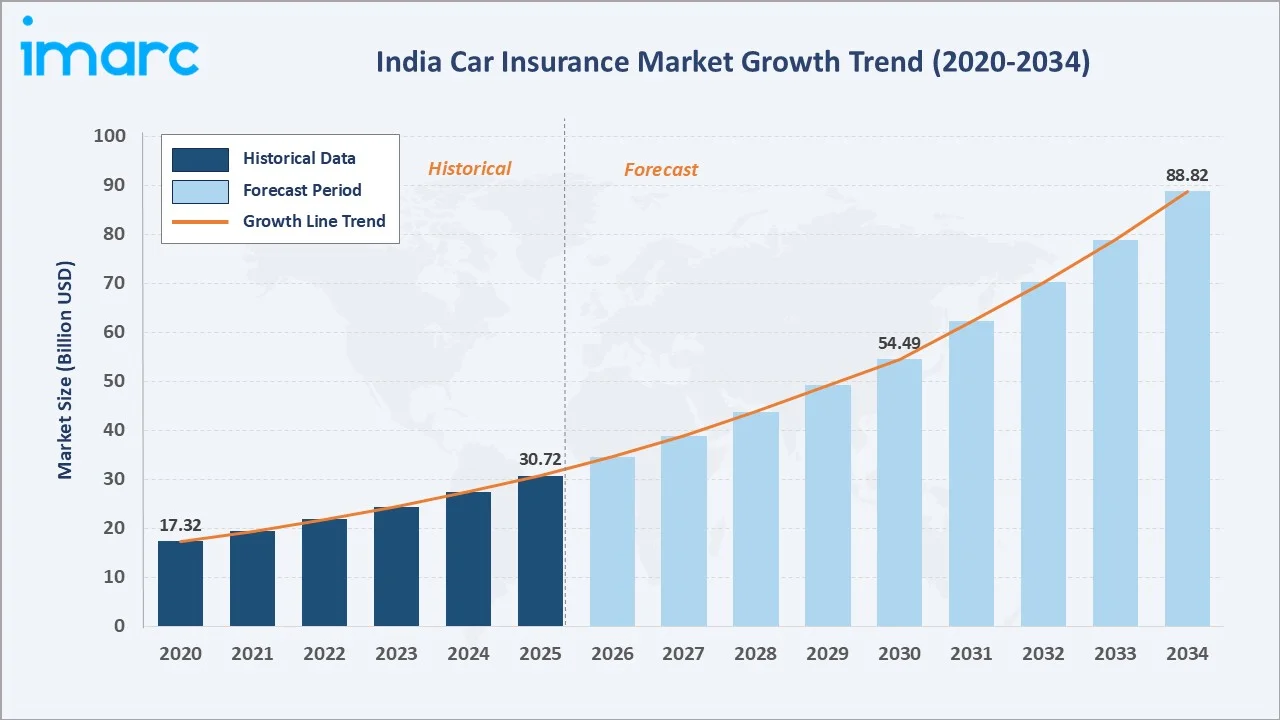

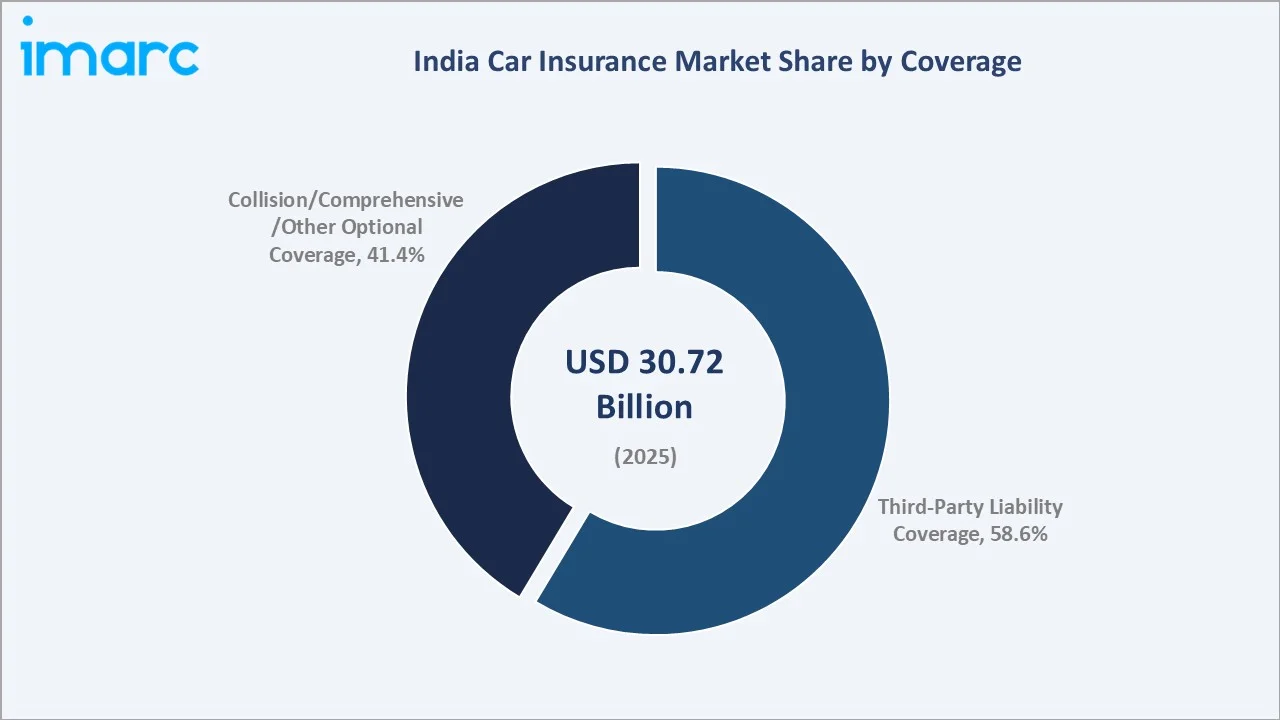

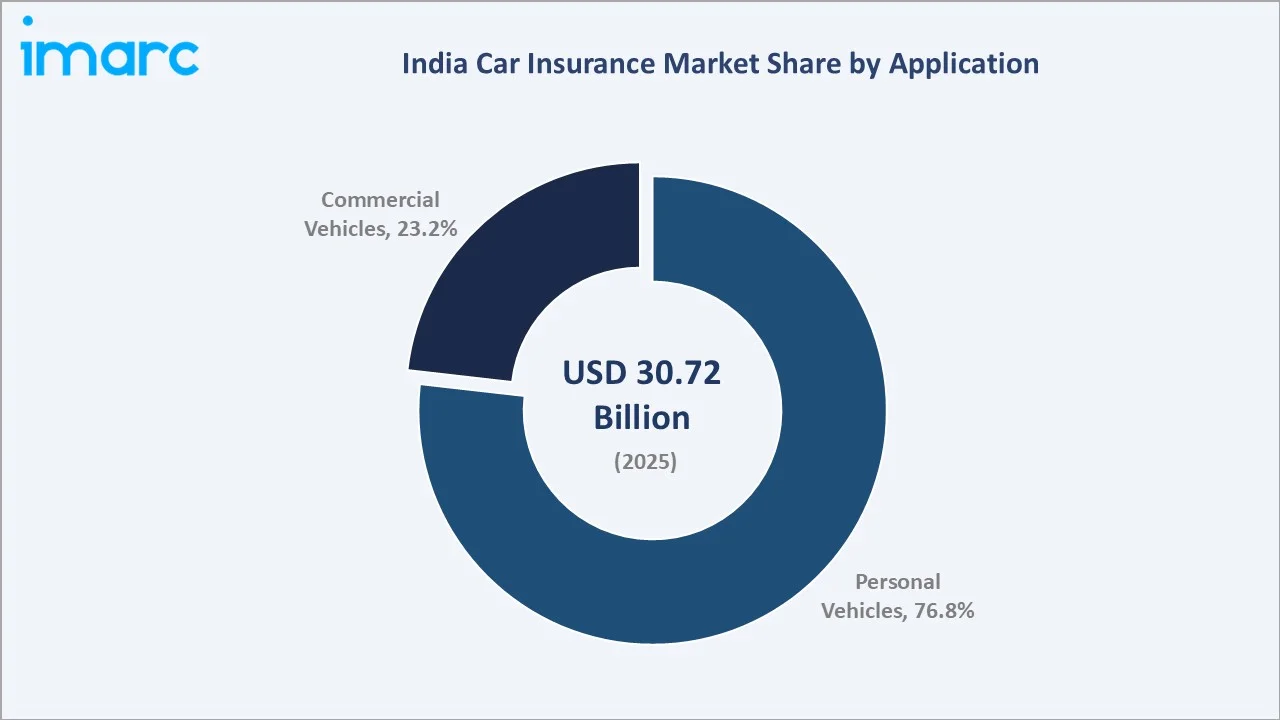

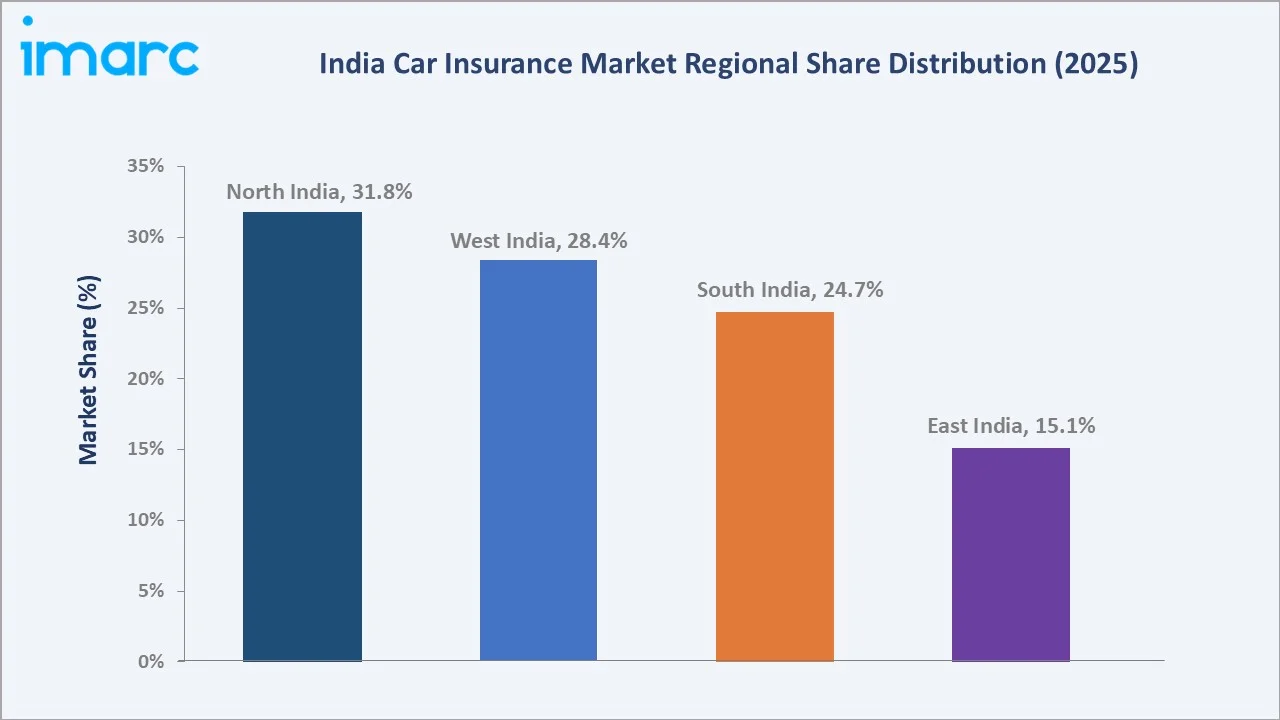

The India car insurance market reached USD 30.72 Billion in 2025 and is projected to reach USD 88.82 Billion by 2034, growing at a CAGR of 12.15% during 2026-2034. The market is driven by rising vehicle ownership, mandatory third-party motor insurance regulations, and increasing awareness of financial protection against accidents, theft, and natural disasters. India’s on-road vehicle base is expected to more than double from 226 million in 2023 to around 494 million by 2050, creating a larger insurable vehicle pool. There is a higher car ownership preference in wealthier markets like Chandigarh, Goa, and Haryana, which is driving demand for motor insurance across both mass and premium vehicle segments. Third-party liability leads coverage at 58.6%. Personal vehicles lead the application at 76.8%. North India leads regionally at 31.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 30.72 Billion |

|

Forecast Market Size (2034) |

USD 88.82 Billion |

|

CAGR (2026-2034) |

12.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Coverage |

Third-Party Liability Coverage (58.6%, 2025) |

|

Dominant Application |

Personal Vehicles (76.8%, 2025) |

|

Leading Region |

North India (31.8%, 2025) |

India car insurance market shows strong growth, rising from USD 17.32 Billion in 2020 to USD 30.72 Billion in 2025. It is expected to reach USD 54.49 Billion by 2030, supported by rising vehicle ownership and mandatory insurance requirements. By 2034, the market is forecast to reach USD 88.82 Billion, reflecting sustained demand for comprehensive and third-party coverage. Digital policy issuance, online renewals, and higher awareness of accident-related financial protection are further strengthening market expansion.

To get more information on this market, Request Sample

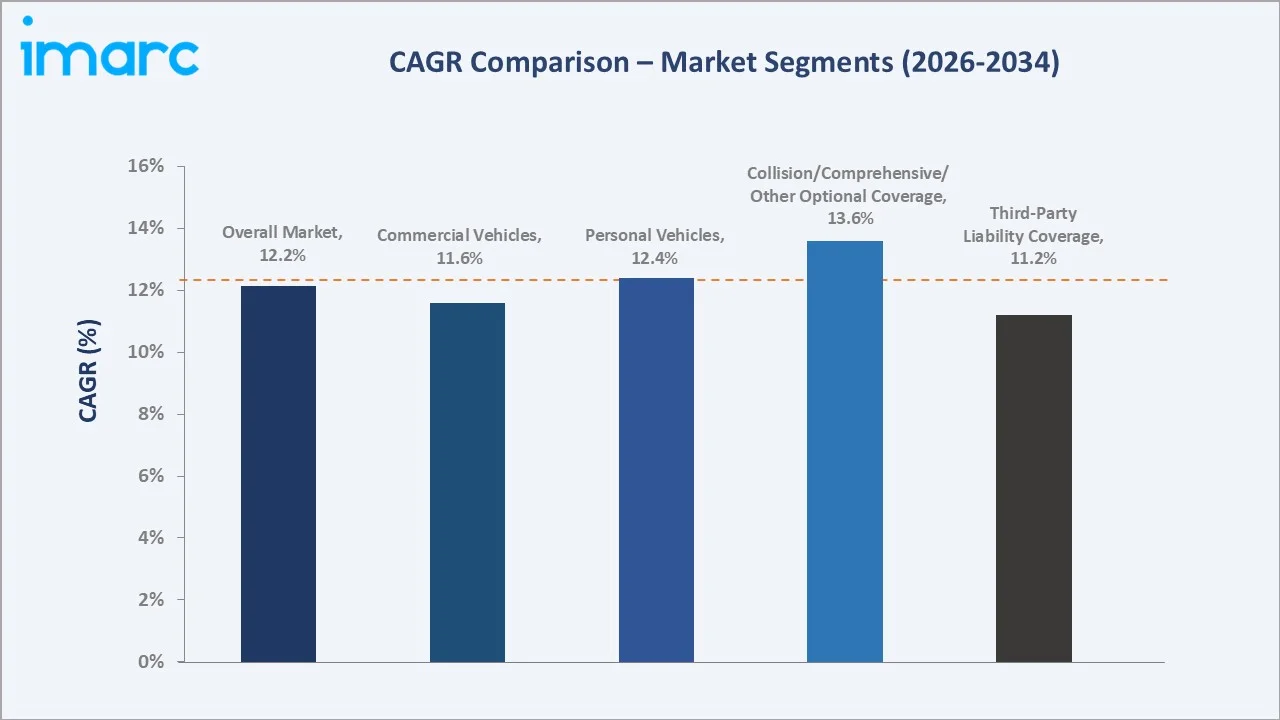

Collision/comprehensive/other optional coverage grows fastest at ~13.6% CAGR through zero-depreciation add-on, return-to-invoice, roadside assistance, and engine protection rider adoption. Personal vehicles grow at ~12.4% CAGR through new car sales, OEM bundled at-showroom insurance, and insurtech digital direct policy growth.

Executive Summary

India car insurance market is expanding steadily, driven by rising vehicle ownership, mandatory third-party insurance, and growing awareness of financial protection. The market increased from USD 17.32 Billion in 2020 to USD 30.72 Billion in 2025 and is projected to reach USD 88.82 Billion by 2034. Rapid growth in passenger car ownership is widening the insurable vehicle base across urban and semi-urban regions. Digital insurance platforms, online renewals, and app-based claim services are improving accessibility and customer convenience. Increasing accident risks, repair costs, theft concerns, and preference for comprehensive coverage are further supporting premium growth. Third-party liability leads the coverage segment at 58.6%. Personal vehicles lead at 76.8%. North India leads regionally at 31.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Coverage |

Third-Party Liability Coverage - 58.6% share (2025) |

|

Dominant Application |

Personal Vehicles - 76.8% market share (2025) |

|

Leading Region |

North India - 31.8% share (2025) |

|

Market Opportunity |

EV car insurance product development; UBI pay-as-you-drive telematics; commercial fleet AI underwriting; digital insurance |

Key Analytical Observations Supporting the Above Data:

- Third-Party Liability at 58.6%: Third-party liability dominates as it is legally mandatory for all vehicle owners under motor insurance regulations. Its lower premium cost compared to comprehensive policies also makes it the most widely purchased coverage, especially among price-sensitive consumers.

- Personal Vehicles at 76.8%: The personal vehicles segment dominates due to the large and growing population of privately owned cars across the country. Rising disposable incomes, increasing vehicle purchases, and mandatory motor insurance requirements continue to drive demand from personal vehicle owners.

- North India at 31.8%: North India dominates due to its large personal vehicle base, rising urbanization, and strong car ownership across states such as Delhi, Haryana, Punjab, and Uttar Pradesh. Higher policy renewals, road traffic density, and expanding digital insurance adoption further support regional growth.

India Car Insurance Market Overview

India car insurance market operates within the broader India non-life insurance market as the largest non-life premium segment. India car insurance market is unique due to its large mix of mandatory third-party policies and fast-growing comprehensive coverage demand. The market is also highly price-sensitive, with digital insurers, aggregators, and app-based claim services making policy purchase and renewal easier across metro, tier-2, and tier-3 cities.

India car insurance ecosystem integrates reinsurers and risk capital, insurance companies and underwriters, agents, brokers, insurtech and digital aggregators, regulatory bodies, and personal and commercial vehicle policyholders. Macroeconomic factors include rising disposable incomes, sustained economic growth, and increasing vehicle ownership across urban and semi-urban areas.

Market Dynamics

To evaluate market opportunities, Request Sample

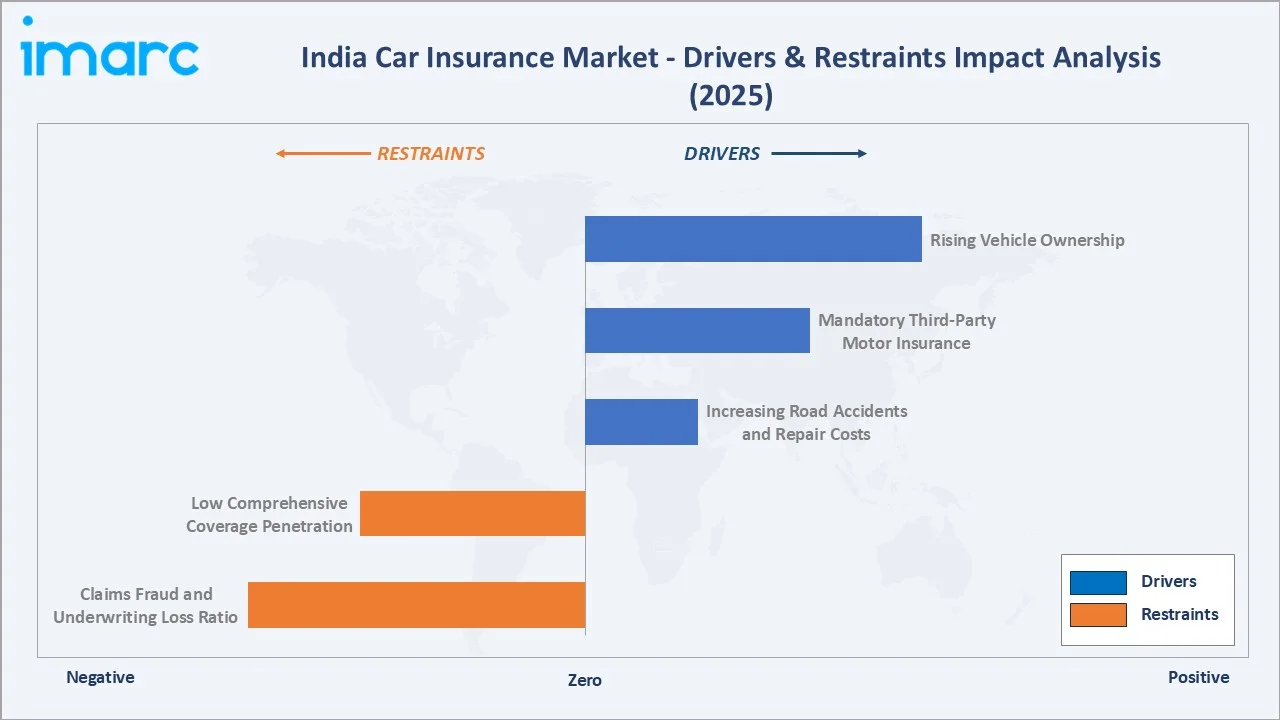

Market Drivers

- Rising Vehicle Ownership: Rising vehicle ownership is driving the market as every new vehicle added to the road increases the potential customer base for insurers. Growing disposable incomes, easier access to vehicle financing, and improving road infrastructure are encouraging passenger car purchases across urban and semi-urban regions. India’s on-road vehicle base is projected to more than double from 226 million in 2023 to nearly 494 million by 2050. Vehicle ownership intensity is also expected to rise sharply, from 163 registered vehicles per 1,000 people in 2023 to 309 per 1,000 people by 2050. Wealthier states and union territories such as Chandigarh, Goa, and Haryana are likely to show a stronger preference for car ownership, creating sustained demand for both third-party and comprehensive insurance policies. Additionally, higher vehicle density increases accident and damage risks, further reinforcing the need for insurance coverage and policy renewals.

- Mandatory Third-Party Motor Insurance: Mandatory third-party motor insurance drives the market as every vehicle owner is legally required to maintain at least third-party liability coverage. This creates a steady baseline demand for motor insurance across both new and existing vehicles. As vehicle registrations increase, the compulsory nature of this policy directly expands the insured customer base. It also encourages insurers to cross-sell own-damage, comprehensive, and add-on covers, supporting higher premium growth.

- Increasing Road Accidents and Repair Costs: In India, a total number of 4,80,583 road accidents were reported by Police Departments of States and Union Territories (UTs) in 2023. These increasing road accidents raise awareness of the financial risks associated with vehicle ownership. Higher traffic density and accident frequency are encouraging vehicle owners to purchase and renew insurance policies for protection against damages and liabilities. At the same time, the rising cost of spare parts, advanced vehicle technologies, and repair services has increased claim values, making comprehensive coverage more attractive. This trend is supporting premium growth and strengthening demand for broader insurance protection.

Market Restraints

- Low Comprehensive Coverage Penetration: Low comprehensive coverage penetration hampers the market, as many vehicle owners purchase only mandatory third-party insurance to meet legal requirements. This limits premium growth because third-party policies are generally lower-priced than comprehensive plans. Price sensitivity, low awareness, and weak renewal discipline further restrict uptake of own-damage and add-on covers. As a result, insurers face limited opportunities to increase policy value, improve customer retention, and expand higher-margin coverage products.

- Claims Fraud and Underwriting Loss Ratio: Claims fraud and high underwriting loss ratios increase insurers’ claim payouts and reduce profitability. Fraudulent claims, inflated repair bills, staged accidents, and false damage reporting raise operational costs and force insurers to tighten underwriting standards. Higher loss ratios can also lead to increased premiums, making comprehensive policies less affordable for customers. This weakens policy uptake, limits insurer margins, and slows sustainable market expansion.

Market Opportunities

- Commercial Fleet AI Underwriting: Commercial fleet AI underwriting enables insurers to assess fleet risks more accurately using telematics, driving behavior, route patterns, and vehicle usage data. AI-driven underwriting can improve pricing precision, reduce fraud, and lower claim costs for commercial vehicle operators. As logistics, e-commerce, and ride-hailing fleets expand across India, demand for customized fleet insurance solutions is increasing. This creates opportunities for insurers to offer usage-based policies, enhance profitability, and improve customer retention through data-driven risk management.

- Growing Adoption of App-Based Motor Insurance Services: Growing adoption of app-based motor insurance services is making policy purchase, renewal, and claims management faster and more convenient. Mobile platforms allow insurers to reach a broader customer base, particularly in Tier-2 and Tier-3 cities, while reducing distribution costs. In March 2025, PhonePe introduced a new vehicle insurance offering for two-wheelers and four-wheelers, providing buyers with affordable online alternatives to dealership-based insurance plans. Through the PhonePe app, users can compare policies from multiple insurers and purchase coverage digitally. The launch addresses common issues such as high premiums, restricted choices, and biased dealership recommendations, while offering a more transparent and competitive insurance experience. As smartphone and internet penetration continue to rise, app-based insurance services are expected to drive higher policy adoption and renewal rates.

Market Challenges

- High Customer Sensitivity to Premium Increases: High customer sensitivity to premium increases is a key challenge, as many consumers prioritize affordability when purchasing or renewing policies. Even modest premium hikes can lead customers to switch insurers, opt for only mandatory third-party coverage, or delay renewals. This limits insurers' ability to pass on rising claim and repair costs, putting pressure on profitability. The challenge is particularly pronounced in price-sensitive segments and smaller cities, where insurance is often viewed as a regulatory requirement rather than a risk-management tool.

- Delayed Claim Settlements and Customer Dissatisfaction: Delayed claim settlements and customer dissatisfaction weaken customer trust in insurers. Slow claim approvals, lengthy documentation, and disputes over repair estimates can discourage policy renewals. Poor claim experience may also push customers toward low-cost policies instead of comprehensive coverage. This affects insurer retention rates, brand loyalty, and long-term market growth.

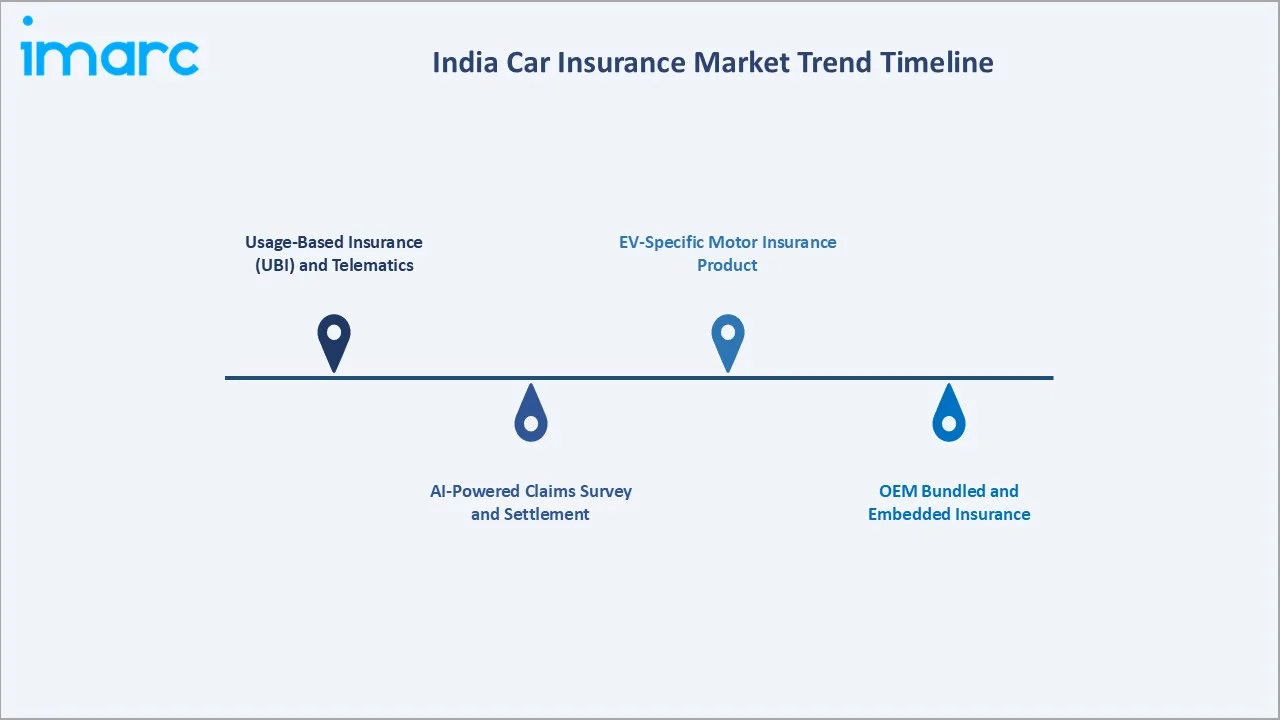

Emerging Market Trends

1. Usage-Based Insurance (UBI) and Telematics

Usage-Based Insurance (UBI) and telematics are emerging as insurers increasingly leverage vehicle data to assess risk and personalize premiums. Telematics devices and mobile applications monitor factors such as driving behavior, mileage, speed, and braking patterns, enabling pay-how-you-drive and pay-as-you-drive models. In August 2024, Zuno, formerly Edelweiss, launched a new motor insurance add-on called Pay How You Drive (PHYD). The feature evaluates users’ driving behaviour and generates a point-based Zuno Driving Quotient (ZDQ) score for each trip. Based on this driving score, customers can receive discounts of up to 30% on their motor insurance premiums during annual renewal. These solutions promote safer driving habits while offering cost savings to low-risk drivers. As digital adoption and connected vehicle technologies expand, UBI is expected to enhance underwriting accuracy, customer engagement, and product innovation in the motor insurance sector.

2. AI-Powered Claims Survey and Settlement

AI-powered claims survey and settlement is emerging as insurers use image analytics, automation, and digital inspection tools to assess vehicle damage faster. Customers can upload photos or videos through mobile apps, reducing the need for physical surveys. This helps shorten claim turnaround time, improve transparency, and lower operational costs. AI-based fraud detection also supports more accurate claim validation, enhancing insurer profitability and customer satisfaction.

3. OEM Bundled and Embedded Insurance

OEM bundled and embedded insurance is emerging as automakers integrate insurance offerings directly at the point of vehicle purchase. This allows customers to receive insurance quotes, financing, registration, and add-on covers as part of a seamless buying journey. OEM partnerships with insurers also support customized plans based on vehicle model, usage, and service network access. As digital vehicle sales and connected car ecosystems grow, embedded insurance is expected to improve policy penetration, renewal rates, and customer convenience.

4. EV-Specific Motor Insurance Product

EV insurance policies surged 670% between 2025 and 2026. These EV-specific motor insurance policies are emerging as electric vehicles require coverage for unique components such as batteries, motors, chargers, and charging cables. Higher battery replacement costs and specialized repair needs are encouraging insurers to design tailored add-ons and protection plans. These products also address risks linked to charging damage, roadside assistance, and software-related issues. As EV adoption rises, EV-focused insurance will become an important growth area for insurers.

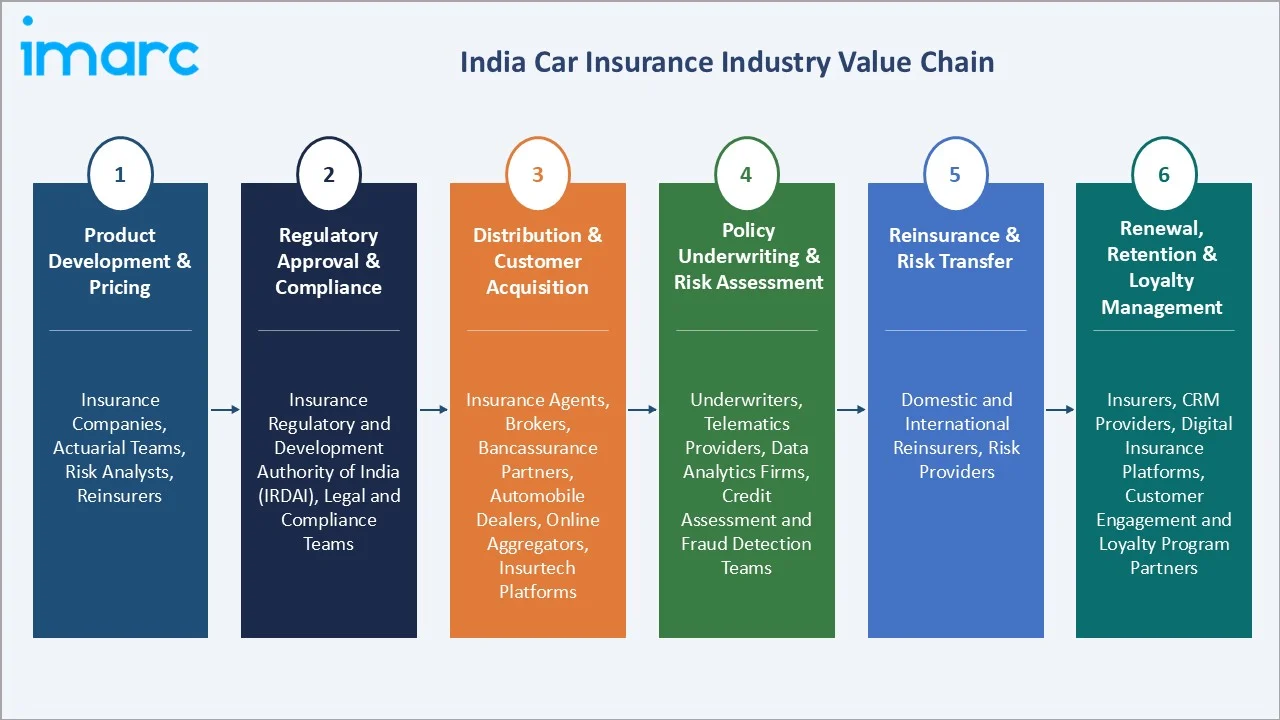

Industry Value Chain Analysis

India car insurance value chain integrates product development & pricing, regulatory approval & compliance, distribution & customer acquisition, policy underwriting & risk assessment, reinsurance & risk transfer, and renewal, retention & loyalty management.

|

Stage |

Key Participants |

|

Product Development & Pricing |

Insurance companies, actuarial teams, risk analysts, reinsurers |

|

Regulatory Approval & Compliance |

Insurance Regulatory and Development Authority of India (IRDAI), legal and compliance teams |

|

Distribution & Customer Acquisition |

Insurance agents, brokers, bancassurance partners, automobile dealers, online aggregators, InsurTech platforms |

|

Policy Underwriting & Risk Assessment |

Underwriters, telematics providers, data analytics firms, credit assessment and fraud detection teams |

|

Reinsurance & Risk Transfer |

Domestic and international reinsurers, risk providers |

|

Renewal, Retention & Loyalty Management |

Insurers, CRM providers, digital insurance platforms, customer engagement and loyalty program partners |

Policy underwriting & risk assessment is the most value-added stage in the India car insurance value chain because it directly determines risk selection, premium pricing, and insurer profitability. Insurers leverage actuarial models, telematics, AI, and customer data to accurately assess driver and vehicle risk profiles. Effective underwriting helps reduce claim losses, improve customer segmentation, and enable personalized products such as usage-based insurance. As the market becomes more digital and data-driven, this stage increasingly serves as a key competitive differentiator for insurers.

Technology Landscape in the India Car Insurance Industry

Digital Payment and Premium Collection Platforms

Digital payment and premium collection platforms enable faster and paperless premium payments. UPI, wallets, cards, and net banking allow customers to buy or renew policies instantly through apps and insurer websites. These platforms reduce collection delays, improve policy issuance efficiency, and support automated reminders for renewals. They also help insurers expand digital reach, lower distribution costs, and improve customer convenience.

Digital Claims Technology

Digital claims technology enables faster, paperless, and more efficient claims processing. Insurers are increasingly using AI-powered image recognition, mobile-based damage assessment, and automated claim workflows to reduce settlement times and operational costs. In June 2026, Kiwi General Insurance commenced operations in India, entering the private motor insurance segment with a product powered by its proprietary technology platform. The company follows a hybrid distribution model, combining digital channels with agent networks. Kiwi states that partners can be onboarded digitally within one day and provided access to tools such as performance dashboards and claims trackers. This reflects the broader industry shift toward seamless digital payments, quicker policy processing, and enhanced customer experience.

Automated Underwriting and Risk Scoring

Automated underwriting and risk scoring enable faster and more accurate policy pricing. Insurers use AI, data analytics, vehicle history, claim records, and driver profiles to assess risk in real time. This reduces manual underwriting, improves operational efficiency, and supports personalized premium pricing. It also helps insurers control fraud, lower loss ratios, and offer customized products such as usage-based insurance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Coverage |

Third-Party Liability Coverage |

58.6% |

2025 |

|

Application |

Personal Vehicles |

76.8% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North India |

31.8% |

2025 |

By Coverage

Third-party liability coverage leads at 58.6% (2025), as it is legally mandatory for every vehicle owner. Its lower premium cost makes it widely adopted, especially among price-sensitive customers. Rising vehicle registrations continuously expand the customer base for this segment.

To access detailed market analysis, Request Sample

Collision/comprehensive/other optional coverage at 41.4% grows fastest at ~13.6% CAGR through zero-depreciation add-on, return-to-invoice, engine protection, and OEM-showroom-bundled comprehensive, creating comprehensive-premiumization India motor insurance.

By Application

Personal vehicles lead at 76.8% (2025), due to the country’s large and expanding base of privately owned cars. Rising disposable incomes, urbanization, and easier vehicle financing are increasing personal car purchases. Mandatory motor insurance and growing preference for comprehensive coverage further support this segment’s dominance.

Commercial vehicles at 23.2% due to their higher insurance requirements and continuous operation across logistics, transportation, e-commerce, and passenger mobility sectors. Fleet owners typically maintain comprehensive coverage to protect against accidents, cargo losses, and third-party liabilities.

Regional Market Insights

|

Region |

Share (2025) |

Key India Car Insurance Market Drivers & Characteristics |

|

North India |

31.8% |

Supported by high vehicle ownership, dense urban populations, and strong insurance penetration. |

|

West India |

28.4% |

Driven by strong economic activity, high disposable incomes, and large vehicle populations. |

|

South India |

24.7% |

Driven by rapid urbanization, growing middle-class incomes, and strong automobile sales. |

|

East India |

15.1% |

Witnessing steady growth due to expanding vehicle ownership, improving road infrastructure, and rising insurance awareness. |

North India's 31.8% market leadership is supported by a large vehicle population, higher car ownership rates, and strong insurance penetration across major states such as Delhi, Uttar Pradesh, Haryana, and Punjab. West India's 28.4% driven by strong economic activity, rising disposable incomes, and substantial vehicle sales in Maharashtra and Gujarat.

South India's 24.7% benefits from rapid urbanization, growing middle-class purchasing power, and high digital adoption, encouraging online policy purchases and renewals. East India's 15.1% driven by increasing vehicle ownership, improving road infrastructure, and expanding insurance awareness.

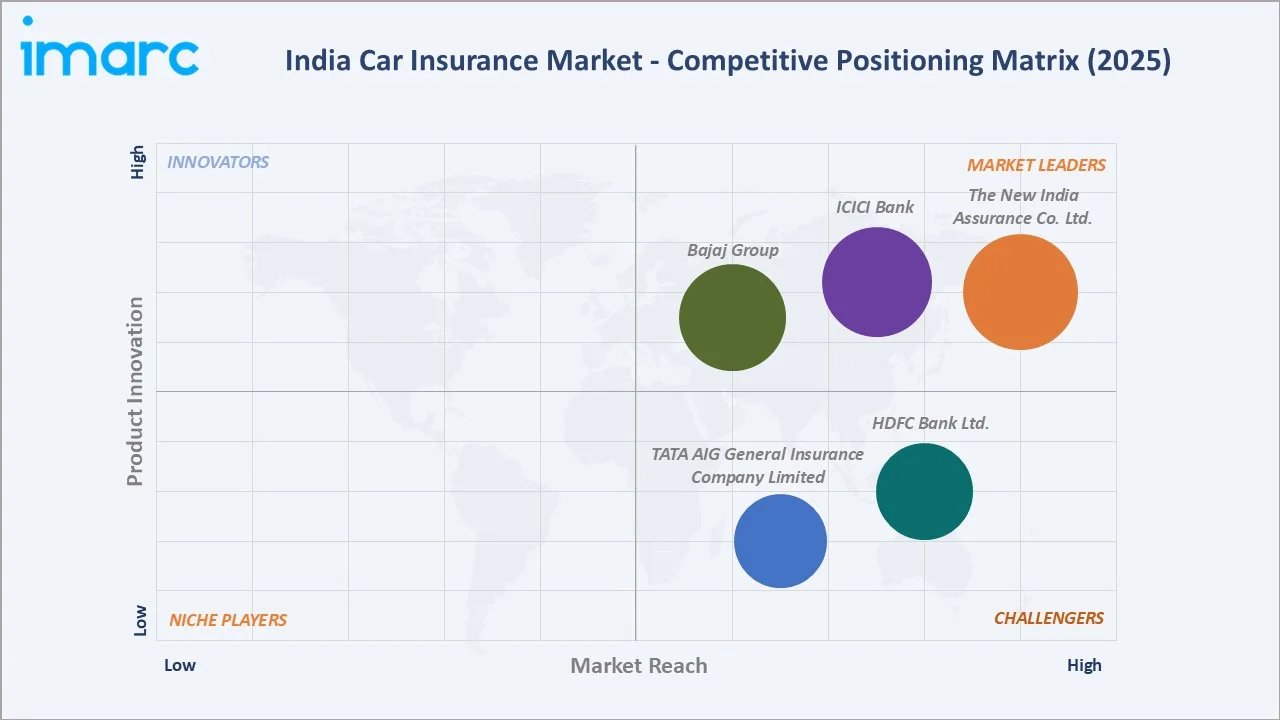

Competitive Landscape

The India car insurance market is highly competitive, with a mix of public-sector insurers, private insurance companies, and emerging InsurTech players competing on pricing, coverage, and customer experience. Market participants are increasingly investing in digital platforms, AI-driven underwriting, and automated claims processing to enhance operational efficiency and customer engagement.

|

Company |

Key Offerings |

Market Position |

Core Strength |

|

The New India Assurance Co. Ltd. |

Liability Only Policy, Package Policy |

Market Leader |

The New India Assurance Co. Ltd. is a premier, government-owned general insurance company in India. It acts as a major market leader in car insurance by providing statutory third-party liability and comprehensive coverage to protect vehicle owners against accidents, natural disasters, and theft. |

|

ICICI Bank |

ICICI Lombard car insurance |

Market Leader |

ICICI Bank operates as a key distributor and facilitator of motor insurance in India. The bank, with its subsidiary, ICICI Lombard General Insurance, provides comprehensive vehicle protection and financial solutions to retail and corporate customers. |

|

Bajaj Group |

Bajaj Car Insurance |

Market Leader |

The Bajaj Group’s role in Indian car insurance is operating Bajaj General Insurance. They are one of the dominant market leaders, known for extensive cashless networks, tech-driven policy management, and pioneering telematics to provide comprehensive financial protection to vehicle owners. |

|

HDFC Bank Ltd. |

HDFC ERGO Car Insurance |

Strong Challenger |

HDFC Bank Ltd. acts as a corporate insurance agent, distributor, and financial facilitator rather than directly underwriting car insurance policies. The actual coverage, policies, and claims are handled by its joint-venture subsidiary, HDFC ERGO General Insurance Company. |

|

TATA AIG General Insurance Company Limited |

TATA AIG Motor Insurance |

Strong Challenger |

Tata AIG General Insurance Company Limited plays a prominent role in the Indian car insurance market by providing comprehensive coverage plans. It facilitates mandatory third-party liability, own-damage, and comprehensive motor policies with wide-ranging add-ons to protect against accidents, theft, and natural disasters. |

Strategic partnerships with automobile manufacturers, dealerships, banks, and online aggregators are expanding distribution reach. Innovation in usage-based insurance, telematics, and app-based policy management is further intensifying competition, while strong brand reputation and extensive service networks remain key differentiators.

Key Company Profiles

The New India Assurance Co. Ltd.

The New India Assurance Co. Ltd. is India's largest public-sector general insurance company and one of the leading players in the country's car insurance market. It serves a broad customer base through an extensive network of branches, agents, brokers, bancassurance partners, and digital platforms. The company maintains a strong presence across urban and rural markets, benefiting from its long-standing brand reputation, large customer base, and nationwide service infrastructure.

- Key Offerings: Liability Only Policy, Package Policy.

- Strategic Focus: Strengthening its leadership in the India car insurance market through digital transformation, customer-centric product innovation, and operational efficiency.

ICICI Bank

ICICI Bank is one of India's largest private-sector banks and plays an important role in the car insurance market through its bancassurance partnerships and digital financial services ecosystem. The bank distributes motor insurance products to retail customers through collaborations with leading insurers, including comprehensive, own-damage, and third-party car insurance policies.

- Key Offerings: ICICI Lombard car insurance.

- Recent Developments: In May 2026, ICICI Lombard General Insurance launched Service Assure under its IL Smart Assist roadside assistance offering. The service promises to reach private car customers within 30 minutes across eight metro cities in case of vehicle breakdowns or accidents. Introduced during the company’s 25-year milestone, the launch reflects ICICI Lombard’s shift from traditional claims support toward a stronger service-assurance model in motor insurance.

- Strategic Focus: Strengthening its presence in the India car insurance market through its bancassurance model, digital distribution channels, and vehicle financing ecosystem. It emphasizes cross-selling insurance products alongside car loans and other financial services to enhance customer lifetime value.

Market Concentration Analysis

The India car insurance market exhibits moderate market concentration, with a mix of large public-sector insurers, established private insurers, and emerging InsurTech players competing for market share. Public-sector companies such as The New India Assurance Co. Ltd. maintain a strong presence due to their extensive branch networks and long-standing customer relationships, while private insurers compete through digital capabilities, product innovation, and superior customer service. The market is witnessing increasing competition from technology-driven entrants offering app-based policy issuance, AI-enabled claims processing, and usage-based insurance products. Strategic partnerships with automobile manufacturers, dealerships, banks, and online aggregators are becoming critical for customer acquisition.

Investment & Growth Opportunities

Highest Growth Segments

Collision/comprehensive/optional coverage (~13.6% CAGR through add-on and comprehensive premiumization), online channel (~15-18% CAGR), EV car insurance (~30-40% CAGR from smaller base), UBI telematics (~20-25% CAGR), commercial fleet AI underwriting (~12-15% CAGR), and digital-direct Insurtech (~18-20% CAGR) represent India car insurance highest-growth investment vectors through 2034.

Investment Themes

- EV-specific car insurance: The rapid adoption of electric vehicles in India is creating demand for specialized insurance products covering batteries, charging equipment, software systems, and EV-specific repair costs. Insurers that develop tailored EV protection plans, battery warranties, and charging-related coverage can capitalize on a fast-growing vehicle segment and generate higher-value premiums.

- Commercial fleet AI underwriting and telematics for India logistics expansion: The expansion of e-commerce, logistics, and last-mile delivery fleets is driving demand for AI-powered underwriting and telematics-based insurance solutions. By analyzing real-time driving behavior, route patterns, and vehicle utilization, insurers can offer usage-based pricing, reduce claims costs, and improve risk assessment for commercial fleet operators.

Future Market Outlook (2026-2034)

India’s car insurance market is projected to expand strongly from USD 30.72 Billion in 2025 to USD 88.82 Billion by 2034, registering a 12.15% CAGR. This growth reflects rising vehicle ownership, mandatory third-party insurance, and increasing demand for comprehensive coverage. The 2030 market value of USD 54.49 Billion signals a digital inflection point, where online policy issuance, app-based renewals, and AI-enabled claims become mainstream. InsurTech entrants, aggregator platforms, and embedded insurance models are expected to improve accessibility and pricing transparency. Rising repair costs, EV adoption, and telematics-based products will further support premium growth over the forecast period.

Three structural forces define India car insurance market through 2034: rapid vehicle ownership growth, regulatory-led mandatory insurance adoption, and digital transformation of policy distribution and claims. Rising car sales and higher road density are expanding the insurable base, while third-party liability rules ensure baseline coverage. At the same time, InsurTech platforms, app-based renewals, AI claims, and telematics are shifting the market toward faster, more personalized insurance solutions. Increasing repair costs and EV adoption are further supporting demand for comprehensive and specialized coverage.

Research Methodology

Primary Research

Primary research comprised in-depth interviews and discussions with insurance company executives, underwriting managers, claims specialists, motor insurance distributors, brokers, automobile dealers, and InsurTech providers across India. Insights were gathered on policy demand, pricing trends, claims experience, digital adoption, customer preferences, and emerging opportunities in comprehensive, telematics-based, and EV insurance segments.

Secondary Research

Secondary research encompassed industry reports, IRDAI publications, insurer annual reports, government vehicle registration data, company press releases, and automotive sector databases. It also included analysis of digital insurance trends, regulatory updates, claims data, and competitive developments. These sources helped validate market trends, segmentation, growth drivers, and future opportunities in India’s car insurance market.

Forecasting Models

Forecasting models utilized a combination of bottom-up and top-down market estimation approaches, supported by historical premium growth, vehicle registration trends, insurance penetration rates, and macroeconomic indicators. Market projections were validated through CAGR analysis, scenario-based forecasting, and triangulation with industry expert insights.

India Car Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Coverages Covered | Third-Party Liability Coverage, Collision/Comprehensive/Other Optional Coverage |

| Applications Covered | Personal Vehicles, Commercial Vehicles |

| Distribution Channels Covered | Direct Sales, Individual Agents, Brokers, Banks, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | The New India Assurance Co. Ltd., ICICI Bank, Bajaj Group, HDFC Bank Ltd., TATA AIG General Insurance Company Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India car insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India car insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India car insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Car Insurance Market Report

The India car insurance market reached USD 30.72 Billion in 2025, driven by rising vehicle ownership, mandatory third-party liability coverage, and increasing demand for comprehensive protection. Higher road accidents, rising repair costs, and growing awareness of financial security are encouraging policy adoption. Digital insurers, app-based renewals, online comparison platforms, and AI-enabled claims services are further accelerating market growth.

The India car insurance market grows at 12.15% CAGR during 2026-2034, reaching USD 88.82 Billion by 2034. The CAGR reflects mandatory TP renewal base, new vehicle sales first-policy, comprehensive premiumization trade-up, insurtech digital disruption, and EV insurance product.

Third-party liability coverage leads at 58.6% as it is legally mandatory for all vehicle owners under the Motor Vehicles Act. Its affordability and compulsory nature ensure widespread adoption, making it the largest policy segment across both private and commercial vehicles.

Personal vehicles lead at 76.8% due to the large and growing base of privately owned cars across urban and semi-urban areas. Rising incomes, easier auto financing, and mandatory insurance requirements continue to support policy demand from individual vehicle owners.

North India leads at 31.8% due to its large vehicle base, higher car ownership, and strong urban demand across Delhi, Haryana, Punjab, and Uttar Pradesh. Rising traffic density, mandatory insurance compliance, and growing digital policy adoption further support regional dominance.

Leading companies include The New India Assurance Co. Ltd., ICICI Bank, Bajaj Group, HDFC Bank Ltd., and TATA AIG General Insurance Company Limited, among others.

The India car insurance market is projected to reach USD 54.49 Billion by 2030, reflecting strong growth driven by rising vehicle ownership, expanding insurance penetration, and increasing demand for comprehensive coverage. The 2030 milestone also represents a digital inflection point, with online policy distribution, AI-enabled claims processing, and InsurTech innovation becoming mainstream across the industry.

Three priority investment opportunities stand out in India’s car insurance market. First, EV-specific car insurance products offer significant potential as electric vehicle adoption accelerates. Second, commercial fleet AI underwriting and telematics solutions can capitalize on the rapid expansion of logistics, e-commerce, and mobility fleets. Third, digital insurance distribution platforms and app-based policy services present strong growth prospects by improving customer acquisition, policy management, and claims efficiency across urban and emerging markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade