India Car Loan Market Size, Share, Trends and Forecast by Type, Car Type, Provider Type, Tenure, and Region, 2026-2034

India Car Loan Market Size, Share, Trends & Forecast (2026-2034)

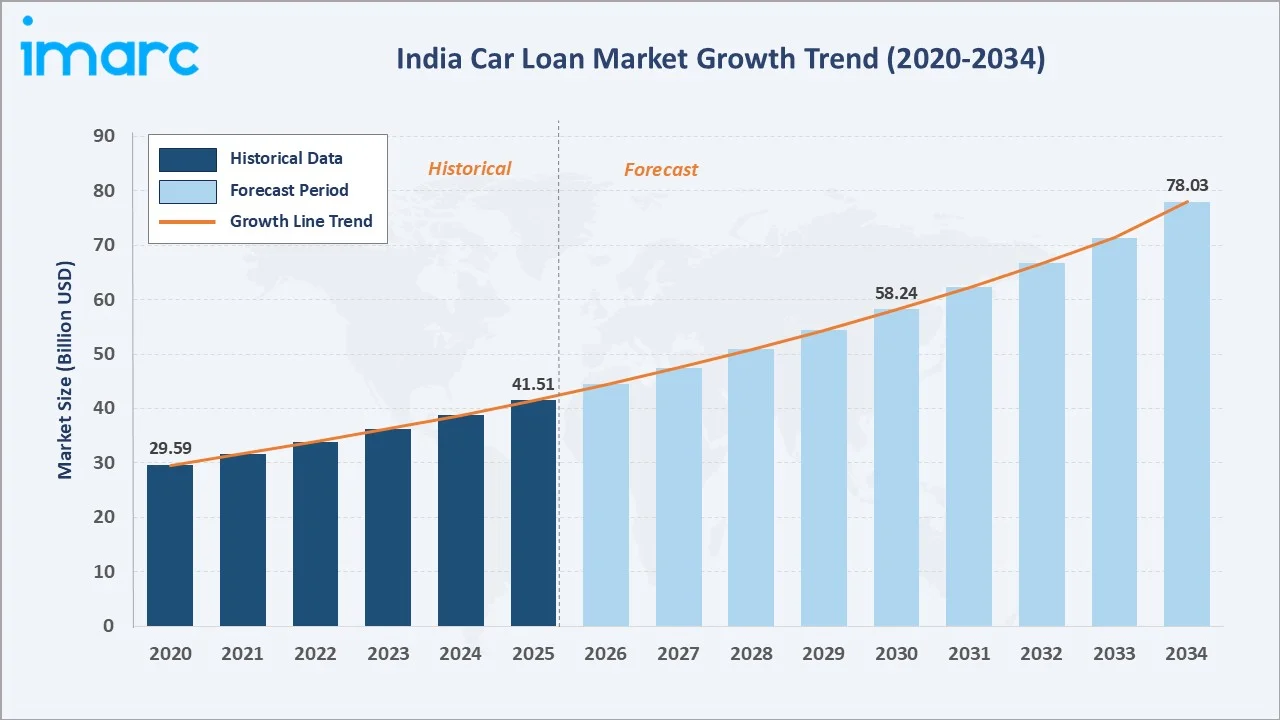

The India car loan market reached USD 41.51 Billion in 2025 and is projected to reach USD 78.03 Billion by 2034, growing at a CAGR of 7.01% during 2026-2034. Growth is driven by rising vehicle ownership aspirations, expanding middle-class incomes, digital lending adoption, and competitive bank and NBFC offerings.

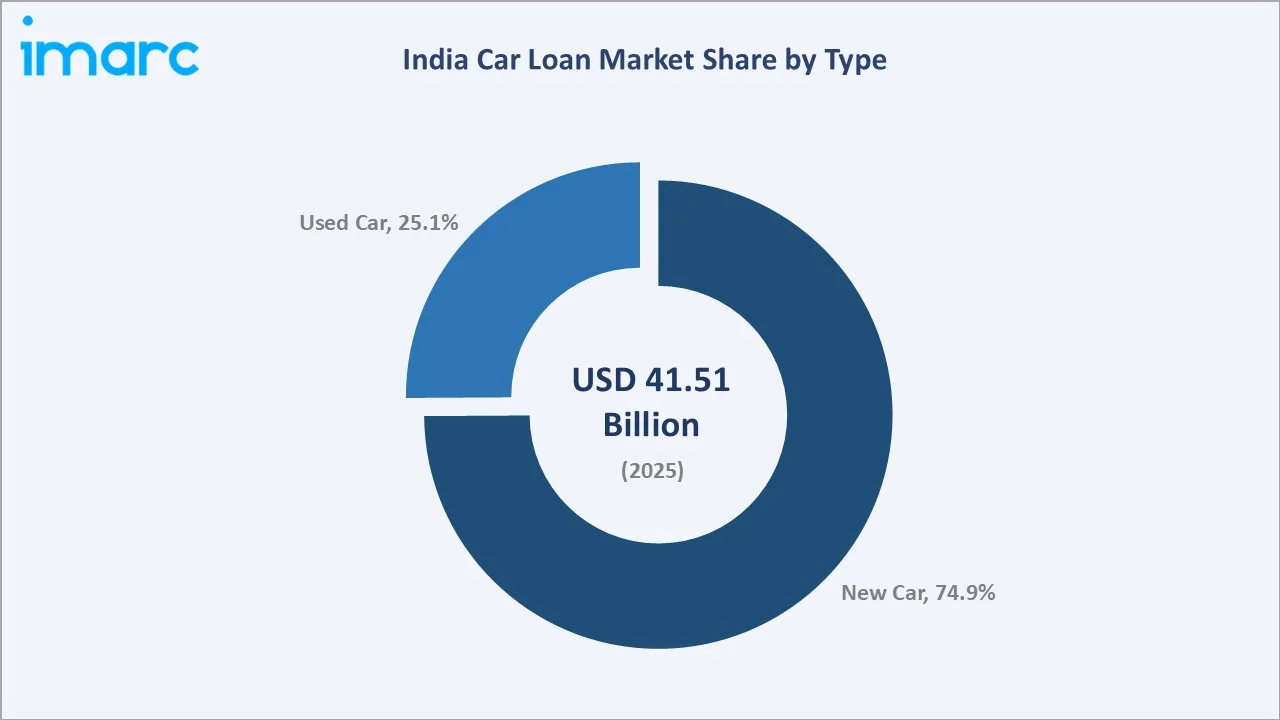

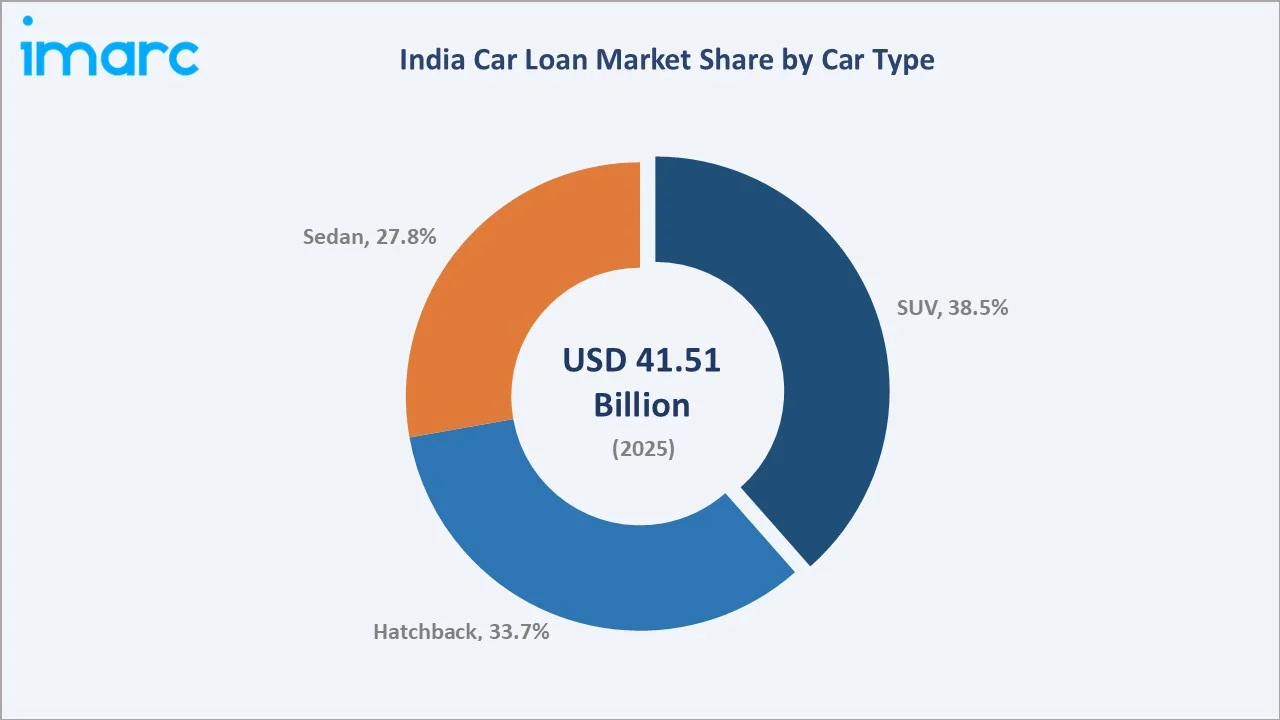

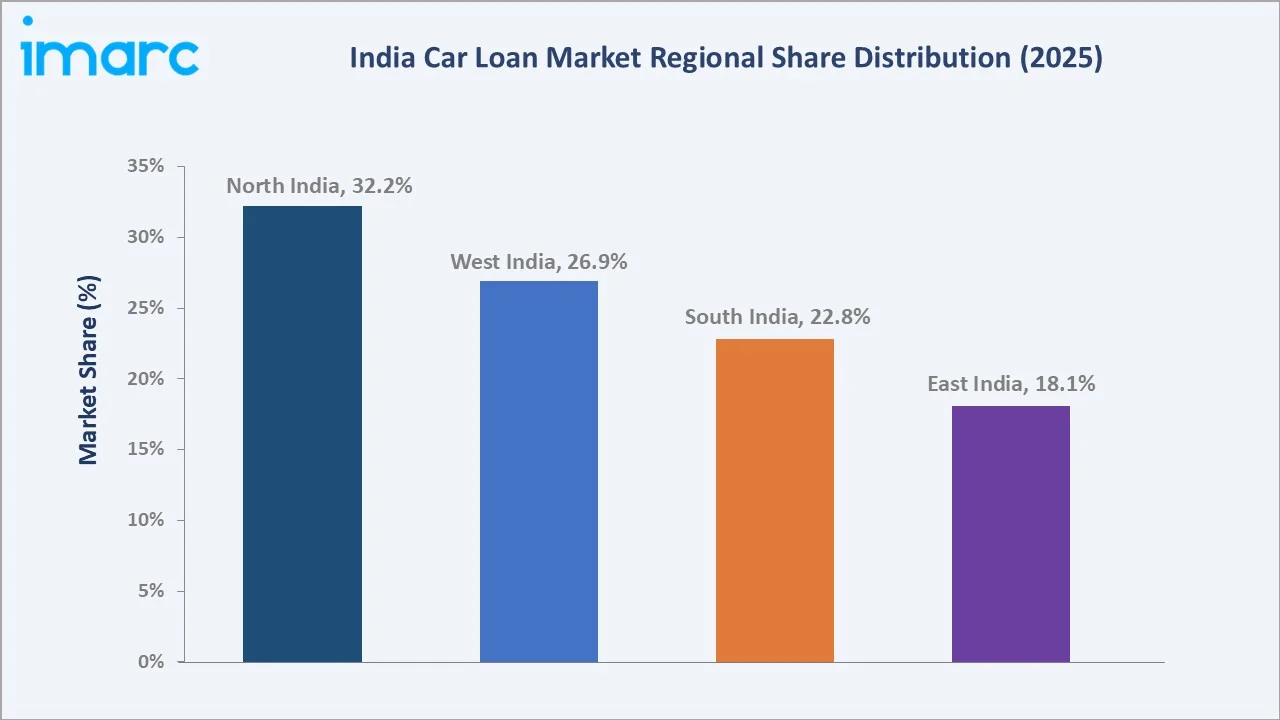

New Car loans dominate at 74.9% while SUVs lead the Car Type segment at 38.5%, reflecting India's structural shift toward premium utility vehicles. North India commands 32.2% regional share through strong urban vehicle ownership in Delhi NCR.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 41.51 Billion |

|

Forecast Market Size (2034) |

USD 78.03 Billion |

|

CAGR (2026-2034) |

7.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

New Car (74.9%, 2025) |

|

Dominant Car Type |

SUV (38.5%, 2025) |

|

Leading Region |

North India (32.2%, 2025) |

The market expanded from USD 29.59 Billion in 2020 to USD 41.51 Billion in 2025, growing steadily through COVID-19 recovery and digital lending expansion. The market is anchored at USD 58.24 Billion in 2030 and projected to reach USD 78.03 Billion by 2034.

To get more information on this market, Request Sample

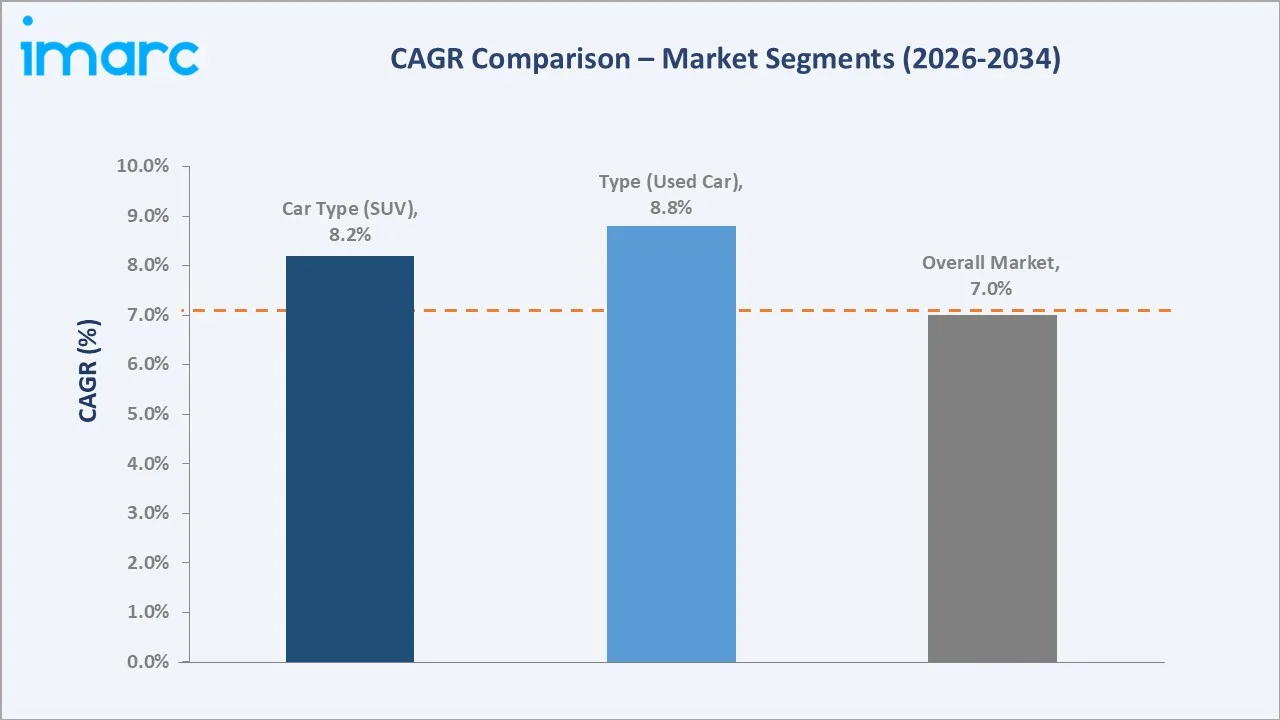

Used Car loans grow at approximately 8.8% CAGR, the fastest among segments, while SUVs lead Car Type growth at approximately 8.2% CAGR. The overall market CAGR of 7.01% reflects sustained demand from India's expanding middle class and digital lending adoption.

Executive Summary

The India car loan market reached USD 41.51 Billion in 2025, representing one of India's largest retail credit segments, driven by rising vehicle ownership aspirations, competitive interest rate offerings, and accelerating digital lending platform adoption among urban and semi-urban borrowers.

New Car loans dominate at 74.9% reflecting sustained preference for new vehicle ownership. SUVs lead the Car Type segment at 38.5%, driven by India's lifestyle aspiration shift toward utility-format premium vehicles among the growing middle class.

North India leads at 32.2%, anchored by high vehicle ownership in Delhi NCR, while West India at 26.9% reflects Maharashtra's large automotive market in Mumbai and Pune.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

New Car – 74.9% share (2025) |

|

Fastest Growing Type |

Used Car – ~8.8% CAGR (2026-2034) |

|

Dominant Car Type |

SUV – 38.5% market share (2025) |

|

Fastest Growing Car Type |

SUV – ~8.2% CAGR (2026-2034) |

|

Leading Region |

North India – 32.2% share (2025) |

|

Market Opportunity |

Used car financing; EV loan products; tier-2/3 city penetration |

Key Analytical Observations Supporting The Above Data:

- New Car at 74.9%: Sustained structural preference for new vehicle ownership among India's urban middle class, reinforced by competitive zero-processing-fee festive season EMI schemes from banks and NBFCs.

- Used Car at 25.1%: Growing formalisation of certified pre-owned vehicle platforms and rising first-time buyer adoption of affordable used vehicles, expanding NBFC product offerings for semi-urban markets.

- SUV at 38.5%: India's structural shift toward utility-format vehicles driven by lifestyle aspiration, expanding road infrastructure, and higher disposable incomes among urban borrowers.

India Car Loan Market Overview

The India car loan market encompasses secured vehicle financing products offered by commercial banks, non-banking financial companies, OEM captive finance arms, and digital lending platforms for the purchase of new and used passenger vehicles across SUV, Hatchback, and Sedan segments.

The ecosystem integrates vehicle manufacturers, dealership networks, credit bureaus, lenders, insurance providers, digital aggregators, and the RBI regulatory framework, collectively enabling India's rapidly growing personal vehicle financing ecosystem.

Market Dynamics

To evaluate market opportunities, Request Sample

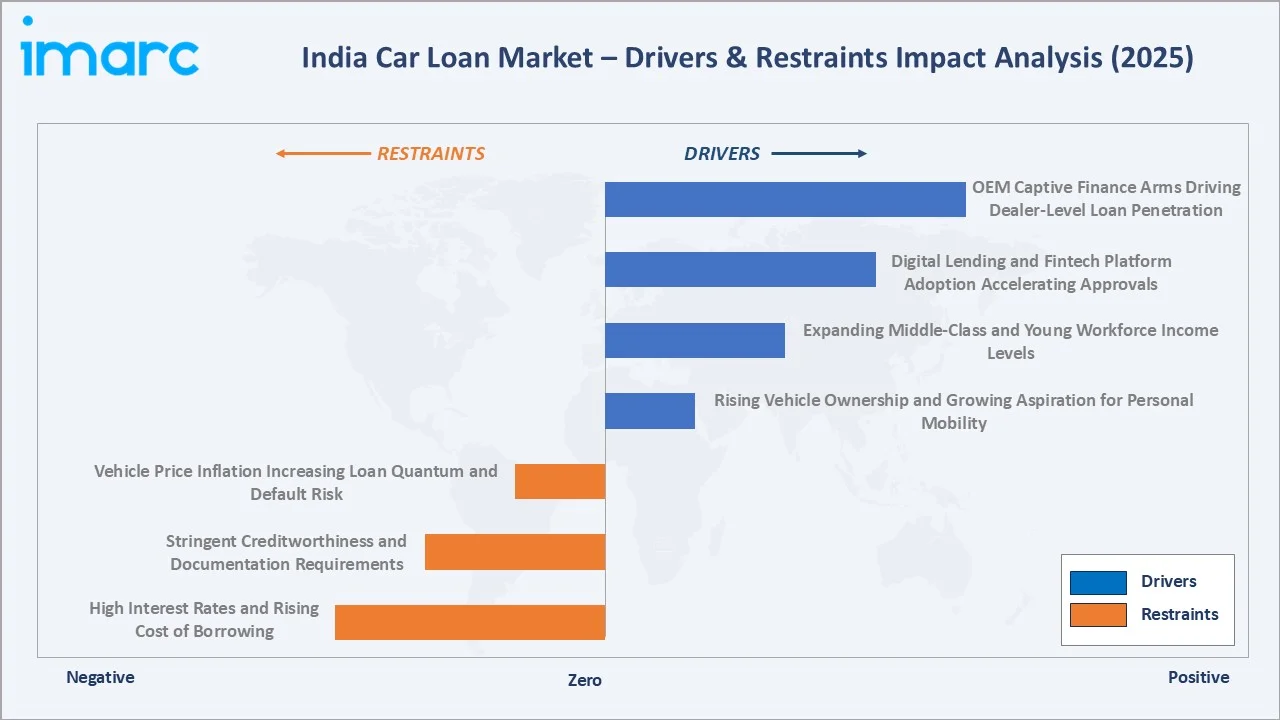

Market Drivers

- Rising Vehicle Ownership and Growing Aspiration for Personal Mobility: India's expanding urban population and aspirational middle class are driving structurally higher demand for personal vehicle ownership, directly expanding the car loan market across new and used segments nationwide.

- Expanding Middle-Class and Young Workforce Income Levels: Rising per-capita incomes, increasing salaried workforce participation, and demographic growth of the 25-40 age cohort are expanding the pool of creditworthy car loan borrowers, sustaining disbursement volume growth.

- Digital Lending and Fintech Platform Adoption Accelerating Approvals: AI-powered credit scoring, instant approval platforms, and digital aggregators like BankBazaar are reducing loan turnaround times from days to hours, expanding car loan accessibility for first-time and repeat borrowers.

- OEM Captive Finance Arms Driving Dealer-Level Loan Penetration: OEM captive finance subsidiaries from Maruti Suzuki, Hyundai, and Tata are embedding loan approval workflows inside dealer CRM systems, lifting loan-attachment rates at the point of vehicle booking.

Market Restraints

- High Interest Rates and Rising Cost of Borrowing: Elevated repo-rate-linked car loan interest rates ranging from 8.5-12% are constraining demand among price-sensitive first-time buyers, limiting volume growth in entry-level hatchback and used car segments.

- Stringent Creditworthiness and Documentation Requirements: Mandatory CIBIL score requirements and documentation standards create access barriers for self-employed borrowers and rural consumers with limited formal credit history, restricting market expansion.

- Vehicle Price Inflation Increasing Loan Quantum and Default Risk: Rising vehicle ex-showroom prices, particularly in the premium SUV segment, are increasing average loan quantum per disbursement, elevating default risk for lenders and constraining affordable financing for lower-income borrowers.

Market Opportunities

- Used Car Financing Market Expansion: The growth in the used car segment represents a significant under-penetrated opportunity. Certified pre-owned vehicle platforms and organised used car networks are enabling systematic credit underwriting for a previously fragmented market.

- EV Car Loan Product Development: India's growing EV adoption is creating demand for specialised EV financing products, including battery-as-a-service financing and lower-interest green car loans, offering lenders a high-margin product differentiation opportunity.

Market Challenges

- Rising Gross NPA Ratios in Vehicle Finance: Increasing gross non-performing asset ratios in the vehicle financing segment, driven by post-pandemic income volatility among self-employed borrowers, are constraining lender risk appetite and tightening underwriting standards across NBFCs.

- Intense Competition Compressing Interest Margins: Growing competition among banks, NBFCs, and fintech lenders is compressing net interest margins on car loan products, making volume growth the primary profitability lever and increasing pressure on operational efficiency.

Emerging Market Trends

1. Digital-First and Instant Car Loan Approval Platforms

Digital lending platforms and fintech aggregators are transforming car loan origination through instant pre-approvals, paperless documentation, and digital disbursements. HDFC Bank's INR 90.6 billion auto loan securitizations reflects the depth of digital innovation in vehicle financing.

2. SUV Loan Segment Premiumisation

India's structural shift toward SUV purchases at 38.5% of car loan disbursements is driving average loan ticket size upward, expanding total market value. Premium SUV financing is becoming a key competitive battleground for both banks and NBFCs across metro India.

3. Used Car Market Formalisation Enabling Loan Growth

Organised used car platforms including Cars24 and CarDekho Rupyy are standardising vehicle valuations and documentation, enabling systematic credit underwriting.

4. EV Financing as an Emerging Product Category

OEM captive finance arms and NBFCs are developing dedicated EV loan products, including Kotak Mahindra Prime's Battery-as-a-Service financing partnership with JSW MG Motor India, embedding EV adoption into the car loan ecosystem.

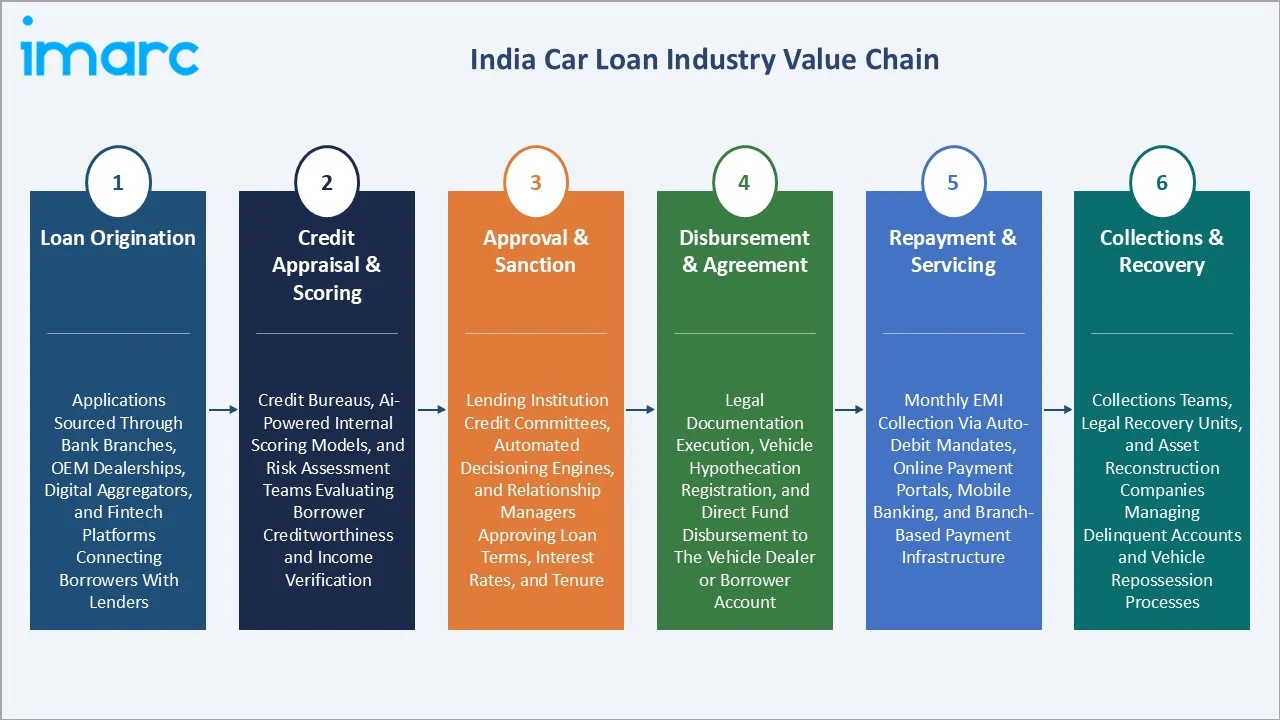

Industry Value Chain Analysis

The India car loan value chain integrates loan origination, credit appraisal and scoring, approval and sanction, disbursement, borrower repayment and servicing, collections and recovery management, and final loan closure across bank branches, OEM dealerships, and digital platforms.

|

Stage |

Key Participants |

|

Loan Origination |

Applications sourced through bank branches, OEM dealerships, digital aggregators, and fintech platforms connecting borrowers with lenders |

|

Credit Appraisal & Scoring |

Credit bureaus, AI-powered internal scoring models, and risk assessment teams evaluating borrower creditworthiness and income verification |

|

Approval & Sanction |

Lending institution credit committees, automated decisioning engines, and relationship managers approving loan terms, interest rates, and tenure |

|

Disbursement & Agreement |

Legal documentation execution, vehicle hypothecation registration, and direct fund disbursement to the vehicle dealer or borrower account |

|

Repayment & Servicing |

Monthly EMI collection via auto-debit mandates, online payment portals, mobile banking, and branch-based payment infrastructure |

|

Collections & Recovery |

Collections teams, legal recovery units, and asset reconstruction companies managing delinquent accounts and vehicle repossession processes |

The credit appraisal and scoring stage represents the highest strategic value tier. AI-powered models and bureau integration determine loan approval speed, risk-adjusted pricing, and competitive differentiation among lenders competing for the same borrower pool in India.

Technology Landscape in the India Car Loan Industry

AI-Powered Credit Scoring and Underwriting Technology

AI and machine learning-based credit scoring models are enabling lenders to process alternative data sources including GST filings, utility payments, and bank transaction history, expanding loan accessibility beyond traditional CIBIL score-dependent underwriting models.

Digital Loan Origination and E-Mandate Platforms

End-to-end digital loan origination with e-KYC, digital signing, and NACH-based e-mandate setup are compressing loan turnaround times to under 24 hours for salaried borrowers, significantly enhancing dealer-level loan attachment rates and customer experience.

Telematics-Based Risk Monitoring and Collections

NBFCs including Shriram Finance are deploying telematics-based repayment tracking for vehicle loans, using real-time location and usage data to enhance early-warning signals, reduce gross NPA ratios, and improve collections efficiency across portfolios.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

New Car |

74.9% |

2025 |

|

Car Type |

SUV |

38.5% |

2025 |

|

Provider Type |

Banks |

52.4% |

2025 |

|

Tenure |

3-5 Years |

52.8% |

2025 |

|

Region |

North India |

32.2% |

2025 |

By Type

New Car loans dominate at 74.9% in 2025, reflecting the sustained structural preference for new vehicle ownership among India's urban middle class. Competitive zero-processing-fee offers and festive season EMI schemes from banks and NBFCs reinforce new car loan dominance.

To access detailed market analysis, Request Sample

The Used Car segment at 25.1% is growing at approximately 8.8% CAGR, driven by formalisation of certified pre-owned vehicle platforms, rising first-time buyer adoption of affordable used vehicles, and expanding NBFC product offerings for the semi-urban and rural market.

By Car Type

SUVs lead at 38.5% in 2025, reflecting India's structural shift toward utility-format vehicles driven by lifestyle aspiration and higher disposable income among urban borrowers. The SUV loan ticket size is typically 30-50% higher than hatchback equivalents, expanding market value.

Hatchbacks at 33.7% serve the mass-market segment, particularly first-time buyers in tier-2 and tier-3 cities. Sedans at 27.8% face competitive pressure from compact SUV formats offering comparable passenger space at similar price points across the Indian market.

Regional Market Insights

|

Region |

Share (2025) |

Key India Car Loan Market Drivers & Characteristics |

|

North India |

32.2% |

Largest share; driven by high vehicle ownership in Delhi NCR; strong dealer network density; premium segment demand in Punjab and Haryana |

|

West India |

26.9% |

Driven by Mumbai and Pune's large automotive market; strong NBFC presence; Maharashtra's high per-capita vehicle financing penetration |

|

South India |

22.8% |

Driven by Bengaluru and Chennai's IT-sector salaried workforce; high digital loan adoption; growing SUV demand among tech-sector professionals |

|

East India |

18.1% |

Emerging market with growing vehicle aspirations; lower penetration; expanding bank and NBFC branch networks in Kolkata and tier-2 cities |

North India, at 32.2%, leads through high vehicle ownership penetration in Delhi NCR, supported by a dense dealer network and strong festive season disbursement activity. West India at 26.9% reflects Maharashtra's large organised automotive market and active NBFC competitive presence.

South India, at 22.8%, is anchored by Bengaluru and Chennai's large salaried IT workforce with high digital lending adoption. East India, at 18.1%, represents the highest untapped growth opportunity as formal lending infrastructure expands through tier-2 city network buildout.

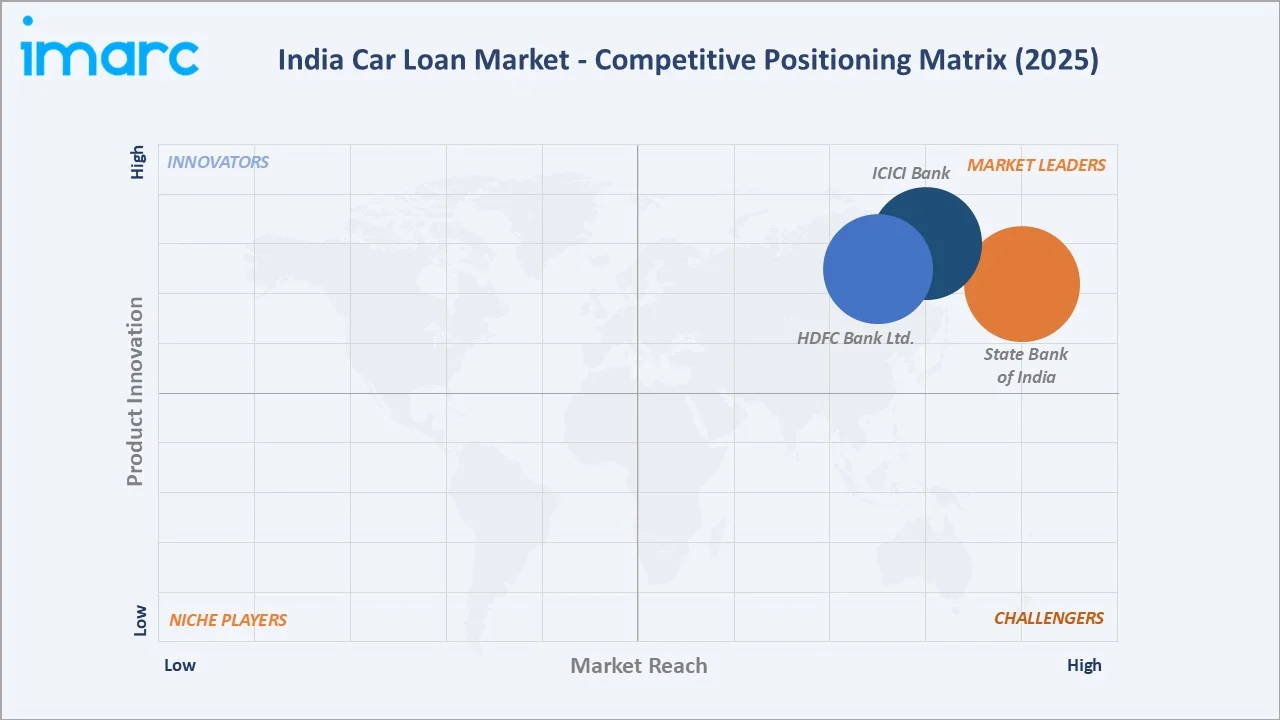

Competitive Landscape

The India car loan market features moderate concentration, with the top five lenders owning slightly above half of the outstanding balances.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

State Bank of India |

Car Loan, Certified Pre-Owned Car Loan, SBI Loyalty Car Loan Scheme, SBI Assured Car Loan Scheme, Green Car Loan: For Electric Cars |

Market Leader |

Largest public sector bank; widest branch network across India; high trust among first-time and rural borrowers |

|

HDFC Bank Ltd. |

HDFC Car Loan, Pre-approved Auto Loans |

Market Leader |

Leading private sector car loan provider, strong digital lending platform, and dealer tie-ups |

|

ICICI Bank |

ICICI Car Loan, Insta Auto Loan |

Market Leader |

AI-driven credit assessments; extensive fintech collaboration across digital lending channels, enabling faster approvals |

Key players include State Bank of India, HDFC Bank Ltd., ICICI Bank, and others.

Key Company Profiles

State Bank of India

State Bank of India is India's largest public sector bank, headquartered in Mumbai, with operations across all Indian states. SBI is the market leader in car loans, offering competitive interest rates and a nationwide branch network across India.

- Key Products: SBI Car Loan, Certified Pre-Owned Car Loan, SBI Loyalty Car Loan Scheme, SBI Assured Car Loan Scheme, Green Car Loan: For Electric Cars

- Strategic Focus: Deepening digital car loan application capabilities through YONO platform integration, expanding EV loan product portfolio, and strengthening tier-2 and tier-3 city penetration through its branch and correspondent banking network.

HDFC Bank Ltd.

HDFC Bank is India's largest private sector bank by total assets, headquartered in Mumbai. In the car loan segment, HDFC Bank co-leads through its extensive dealer finance network, digital lending capabilities, and pre-approved loan product innovations for existing customers.

- Key Products: HDFC Car Loan, Pre-approved Auto Loans

- Strategic Focus: Expanding digital pre-approved loan reach through mobile and internet banking platforms, deepening OEM dealer integration for seamless in-showroom loan origination, and scaling the auto loan portfolio through securitization and co-lending models.

Market Concentration Analysis

The India car loan market features moderate concentration, with the top five lenders holding approximately 55-60% of total outstanding car loan balances, reflecting a competitive but not fully consolidated lending landscape across banks and NBFCs.

NBFCs are collectively gaining share through risk-tiered product innovation, festival season offers, and targeted outreach to borrowers underserved by traditional bank scoring models in semi-urban India.

Investment & Growth Opportunities

Highest Growth Segments

Used Car Financing (~8.8% CAGR), SUV Loan Segment (~8.2% CAGR), and EV-Specific Loan Products represent the three highest-growth opportunity areas within the India car loan market through 2034, each driven by structural demand shifts and new product category development.

Emerging Investment Opportunities

Tier-2 and tier-3 city market expansion represents the highest untapped growth opportunity, as current car loan penetration in smaller cities remains well below metro levels. Lenders investing in digital loan origination, local dealer partnerships, and vernacular loan platforms will capture the next growth wave.

Investment Themes

- Digital Loan Origination Infrastructure: Investing in AI-powered credit scoring, instant pre-approval APIs, and dealer-embedded loan origination technology enables lenders to reduce customer acquisition cost while improving approval speed and loan attachment rates at vehicle purchase.

- Securitization and Co-Lending Models: Car loan securitization and co-lending partnerships between banks and NBFCs create capital-efficient growth models, allowing NBFCs to scale disbursements without proportional balance sheet risk.

Future Market Outlook (2026-2034)

The India car loan market is projected to grow from USD 41.51 Billion in 2025 to USD 78.03 Billion by 2034, delivering a 7.01% CAGR. Growth will be anchored by rising vehicle aspirations, expanding middle-class incomes, digital lending maturation, and structural shift toward premium SUV formats.

The Used Car segment will continue outpacing overall market growth as formalisation accelerates. The SUV car type will expand its dominance as India's vehicle mix premiumises, driving average loan ticket size upward and supporting sustained absolute value disbursement growth.

By 2030, the market is projected to reach approximately USD 58.24 Billion, with digital-native lenders capturing a growing share as embedded finance at OEM dealerships becomes the primary loan origination channel across India's major automotive markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders including bank vehicle finance heads, NBFC senior executives, OEM captive finance officers, automotive dealership principals, credit bureau analysts, and fintech lending platform founders across India.

Secondary Research

Secondary research encompassed RBI auto loan disbursement data, SIAM vehicle sales statistics, company annual reports, CIBIL vehicle finance trend reports, IMARC proprietary BFSI databases, and fintech industry publications. Over 55 secondary sources were reviewed.

Forecasting Models

Market forecasts developed using bottom-up models: (i) vehicle unit sales volumes by car type; (ii) loan attachment rates by channel and borrower segment; (iii) average loan ticket size by type; (iv) regional disbursement growth adjustment factors aligned to RBI monetary policy.

India Car Loan Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | New Car, Used Car |

| Car Types Covered | SUV, Hatchback, Sedan |

| Provider Types Covered | OEM (Original Equipment Manufacturers), Banks, NBFCs (Non Banking Financials Companies) |

| Tenures Covered | Less Than 3 Years, 3-5 Years, More Than 5 Years |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | State Bank of India, HDFC Bank Ltd., ICICI Bank, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Car Loan Market Report

The India car loan market reached USD 41.51 Billion in 2025, driven by New Car type at 74.9%, SUV car type leading at 38.5%, and North India commanding 32.2% regional share through high vehicle ownership in Delhi NCR.

The market grows at 7.01% CAGR during 2026-2034, reaching USD 78.03 Billion by 2034, reflecting rising vehicle ownership aspirations, digital lending adoption, SUV premiumisation, and expanding used car financing infrastructure.

New Car loans dominate at 74.9% in 2025, driven by competitive interest rate offerings, festive season EMI schemes, and strong structural preference for new vehicle ownership among India's urban and semi-urban middle-class consumers.

SUVs lead at 38.5% in 2025, reflecting India's structural shift toward utility-format vehicles. Used Car is the fastest-growing type at approximately 8.8% CAGR through 2034 driven by platform formalisation.

North India leads at 32.2% through high vehicle ownership penetration in Delhi NCR, supported by a dense dealer network and strong festive season disbursement activity from major banks and NBFCs.

Leading companies include State Bank of India, HDFC Bank Ltd., ICICI Bank, and others.

The market is projected to reach approximately USD 58.24 Billion by 2030, driven by digital lending platform maturation, SUV segment expansion, used car financing formalisation, and growing EV-specific loan product adoption.

Three priority opportunities: used car financing platform development, EV-specific loan product innovation including battery-as-a-service financing, and digital loan origination infrastructure for tier-2 and tier-3 city expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)