India Carbon Credit Market Size, Share, Trends and Forecast by Type, Project Type, End-Use Industry, and Region, 2026-2034

India Carbon Credit Market Size, Share, Trends & Forecast (2026-2034)

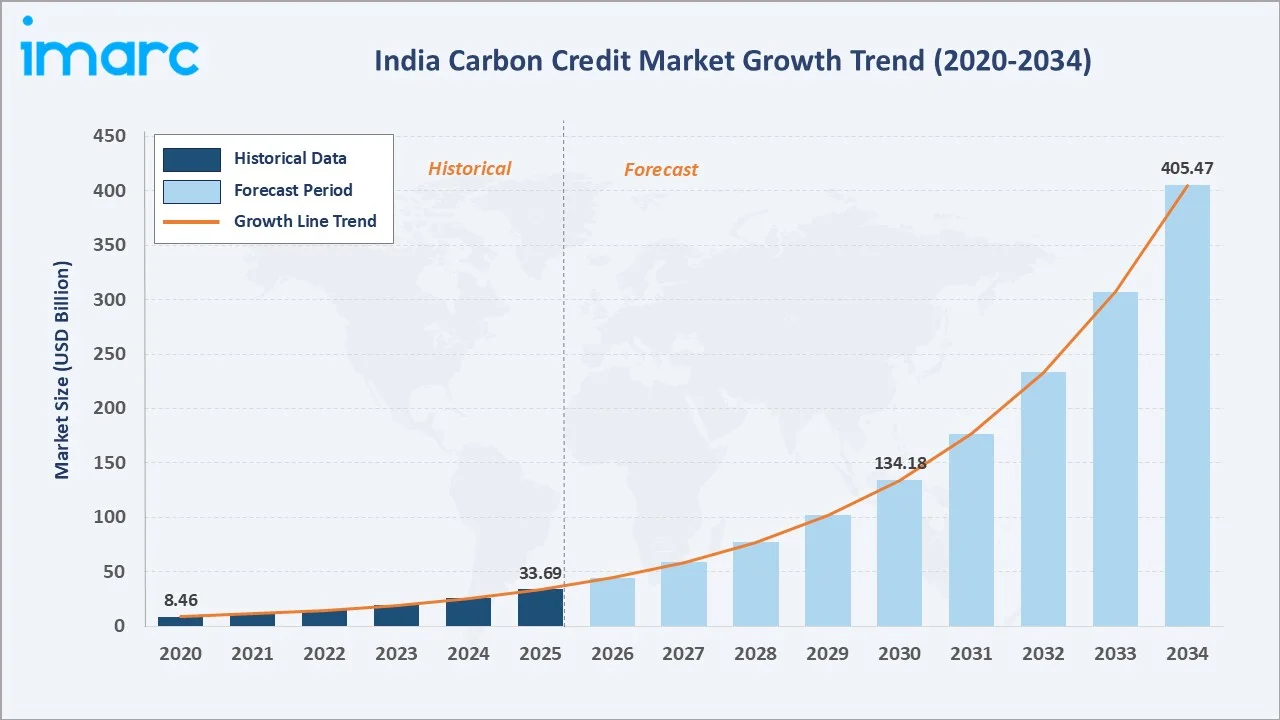

The India carbon credit market reached USD 33.69 Billion in 2025 and is projected to reach USD 405.47 Billion by 2034, growing at a CAGR of 31.84% during 2026-2034. Rapid institutionalization of the Carbon Credit Trading Scheme (CCTS), accelerating corporate Net Zero commitments, and expanding voluntary participation in nature-based and renewable energy projects are the principal forces shaping market trajectory across compliance and voluntary segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 33.69 Billion |

|

Forecast Market Size (2034) |

USD 405.47 Billion |

|

CAGR (2026-2034) |

31.84% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (31.0% share, 2025) |

|

Fastest Growing Region |

West India |

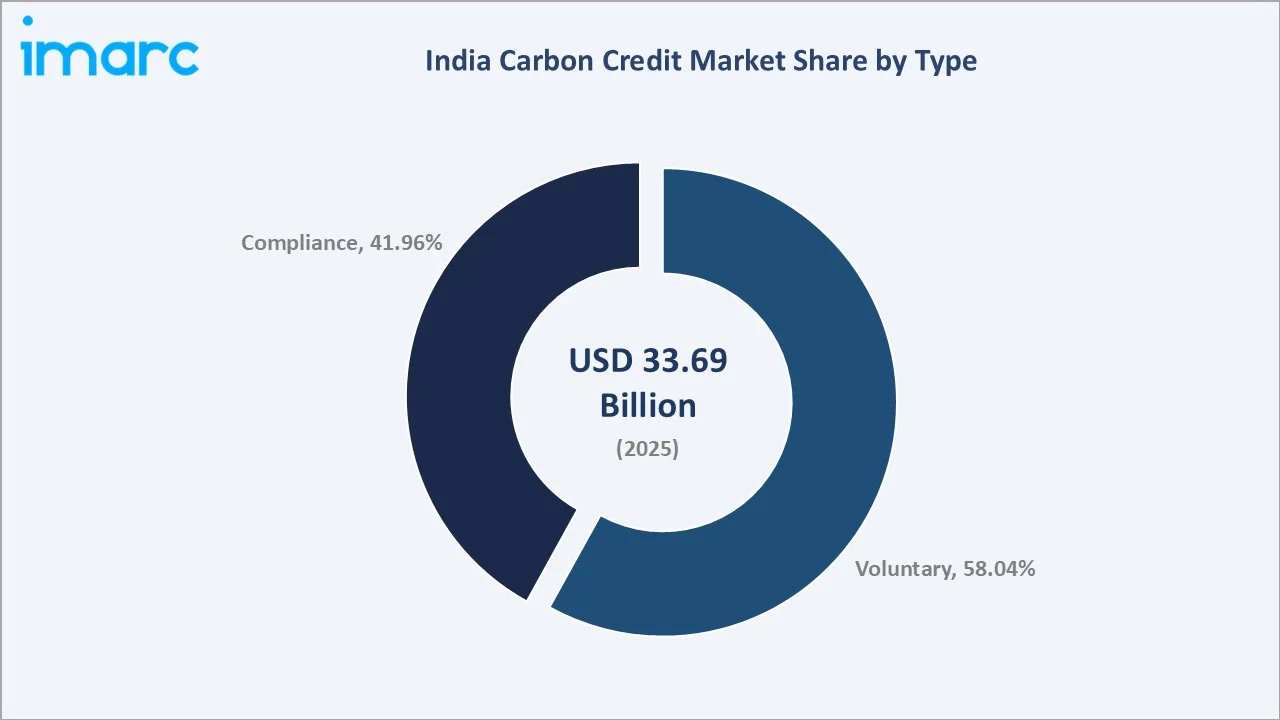

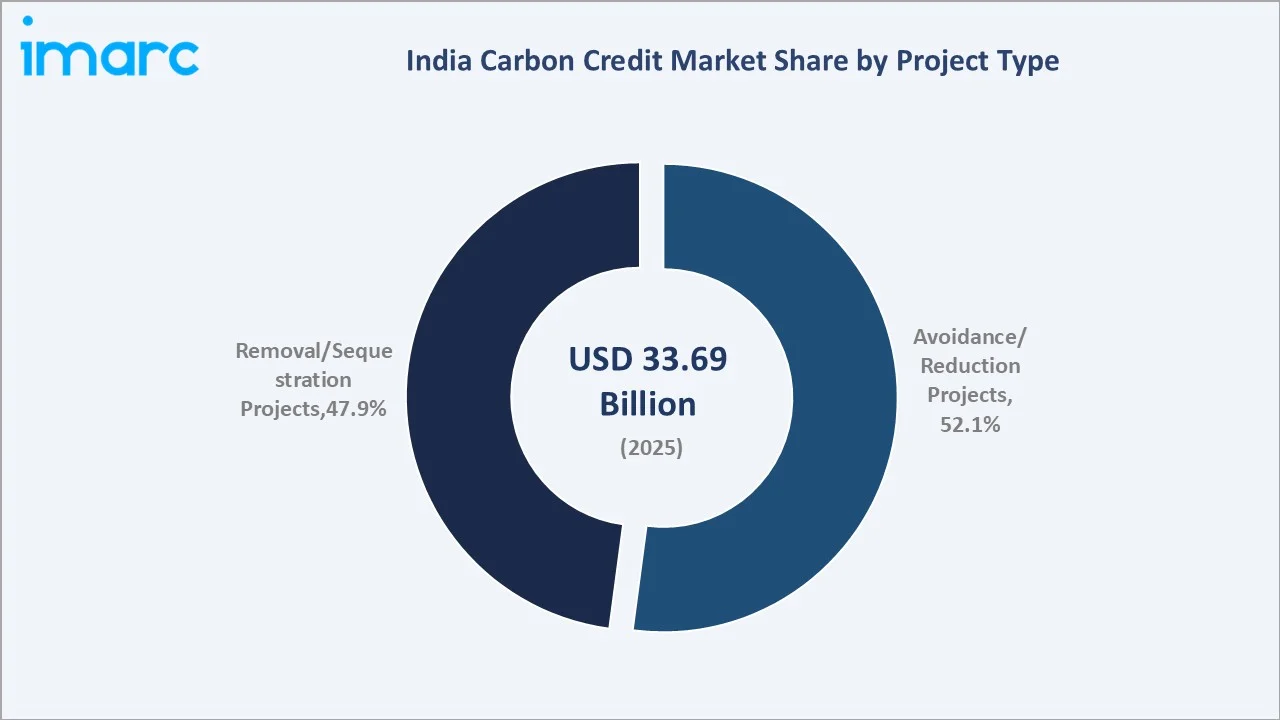

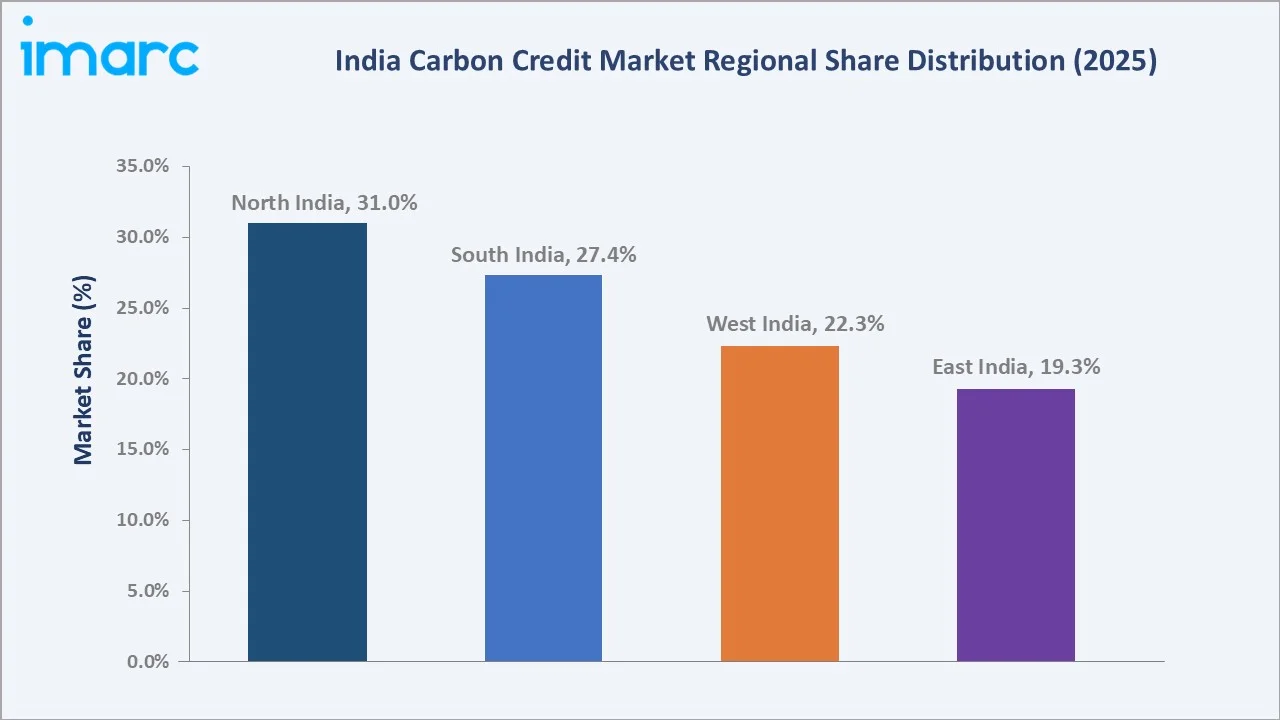

North India dominates with a 31.0% market share in 2025, anchored by energy-intensive industrial clusters across Uttar Pradesh, Haryana, and Punjab. The voluntary segment leads at 58.04%, supported by corporate sustainability commitments and Verra/Gold Standard project registrations. Avoidance/reduction projects account for 52.1% of activity, reflecting renewable energy and industrial efficiency primacy.

To get more information on this market, Request Sample

The market connects compliance obligations under the CCTS with voluntary offset mechanisms, positioning India among the world’s largest emerging carbon trading systems, with the CCTS expected to cover over 700 million tons of CO₂ equivalent at full operationalization.

With Carbon Credit Certificates set to commence trading by mid-2026 and 282 industrial facilities across cement, aluminum, pulp & paper, and chlor-alkali receiving legally binding emission intensity targets, India is transitioning into a structured, financialized carbon market with significant participation from project developers, verification agencies, and end-buyers.

Executive Summary

India’s carbon credit market is on a sustained high-growth path, propelled by the operationalization of the Carbon Credit Trading Scheme, an expanding voluntary offset ecosystem, and aggressive corporate decarbonization commitments. The market reached USD 33.69 Billion in 2025 and is projected to reach USD 405.47 Billion by 2034, with growth supported by both compliance demand from energy-intensive industries and voluntary supply from renewable energy, agriculture, and forestry projects.

North India leads regionally with a 31.0% share in 2025, followed by South India at 27.4%, reflecting concentrations of cement, steel, and thermal power infrastructure. Voluntary credits dominate the type-based segmentation at 58.04%, while avoidance/reduction projects represent 52.1% of project-type activity.

Key activities include the in March 2025, the BEE issued Version 1 of the detailed procedures for the CCTS offset mechanism, while the government approved eight methodologies for the domestic voluntary carbon market. Through collaboration with NDDB and Sustain Plus Energy Foundation’s Manure Management Program, over 1,000 dairy farmers across nine locations in seven states are benefiting financially from sustainable practices, receiving payments that enhance their incomes while supporting India’s transition to net zero.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Voluntary – 58.04% (2025) |

|

Largest Segment (Project Type) |

Avoidance/Reduction Projects – 52.1% (2025) |

|

Leading Region |

North India – 31.0% share (2025) |

|

Fastest Growing Region |

West India |

|

Top Companies |

EKI Energy Services ltd., MITCON Consultancy & Engineering Services Limited, Greenko Group, ReNew, NTPC |

Key Analytical Observations Supporting the Above Data:

- Voluntary credits account for 58.04% of the India carbon credit market in 2025, driven by Net Zero commitments from Indian conglomerates and active project registrations under Verra and Gold Standard.

- Avoidance/reduction projects lead the project-type segmentation at 52.1% (2025), reflecting widespread participation in renewable energy, energy efficiency, and industrial process improvement initiatives.

- North India holds 31.0% of the total market in 2025, anchored by industrial corridors in Uttar Pradesh, Haryana, Punjab, and the Delhi NCR region.

- The CCTS compliance mechanism will cover over 700 million tonnes of CO₂ equivalent at full rollout, ranking among the world’s largest emissions trading systems.

- A report by Down To Earth and the Centre for Science and Environment (DTE-CSE) found that as of June 2023, India had 860 registered projects and a total of 1,451 projects at various stages of consideration under Verra and Gold Standard.

India Carbon Credit Market Overview

A carbon credit represents one tonne of carbon dioxide-equivalent emissions reduced, avoided, or removed from the atmosphere. India’s carbon credit market is structured around two complementary mechanisms: a compliance arm under the CCTS and a parallel voluntary offset framework. Both channels connect emission-intensive sectors and project developers with corporate buyers, sovereign actors, and intermediaries seeking high-integrity credits.

.webp)

Macroeconomic drivers include India’s 2070 Net Zero pledge, an updated Nationally Determined Contribution (NDC) targeting a 47% emissions intensity reduction below 2005 levels by 2035, and parallel rollouts of the Green Hydrogen Mission and the Green Credit Programme. Combined with rapidly improving abatement economics in solar, wind, biomass, and waste-to-energy, these structural forces are converting carbon performance into a tradable financial instrument across India’s industrial backbone.

Market Dynamics

To evaluate market opportunities, Request Sample

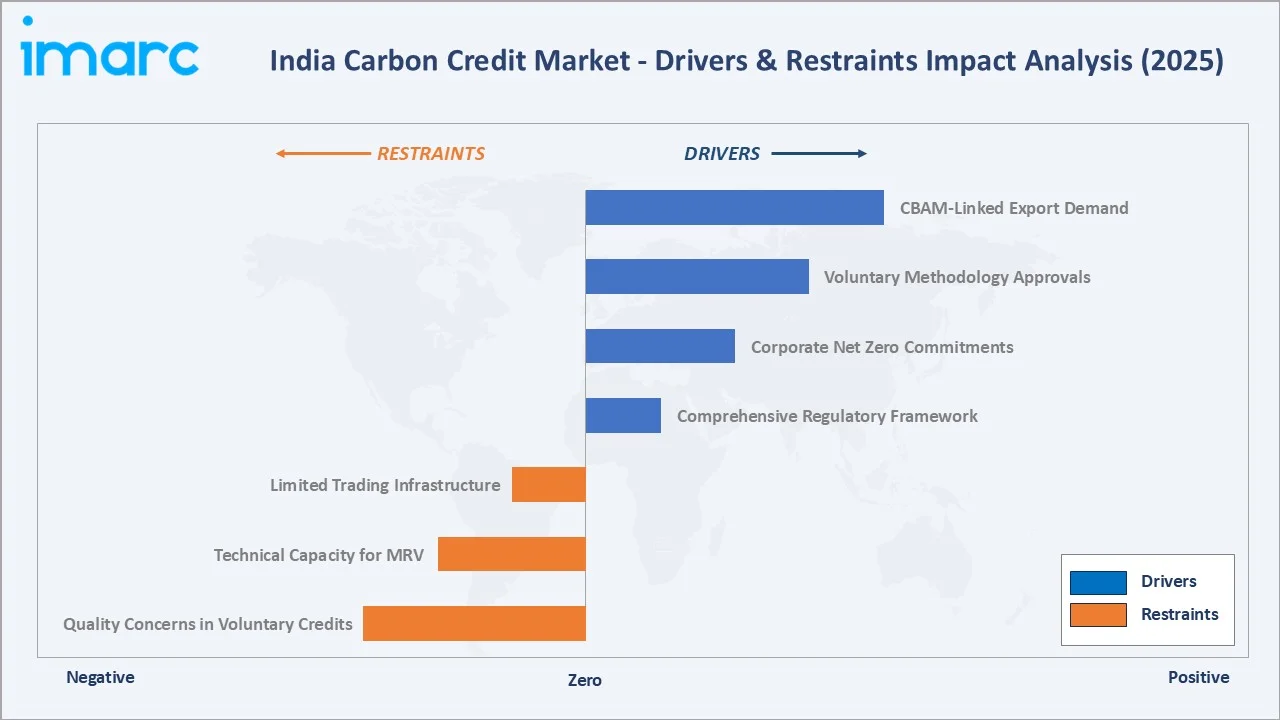

Market Drivers

- Comprehensive Regulatory Framework: The CCTS, notified in June 2023 with detailed compliance regulations issued in July 2024, introduces an intensity-based baseline-and-credit system using FY2024 as the baseline for FY2026–FY2027 compliance years.

- Corporate Net Zero Commitments: Tata Steel, Reliance Industries, Mahindra, Infosys, and NTPC have established aggressive emission reduction timelines, driving captive demand for both compliance certificates and voluntary credits.

- Voluntary Methodology Approvals: In March 2025, the Ministry of Power approved eight voluntary crediting methodologies covering renewable energy with storage, green hydrogen production, mangrove afforestation, landfill methane recovery, and offshore wind.

- CBAM-Linked Export Demand: The European Union’s Carbon Border Adjustment Mechanism, requiring product-level carbon intensity reporting for cement, aluminum, steel, and chemicals from 2026, is creating dual-purpose MRV investment among Indian exporters.

Market Restraints

- Limited Trading Infrastructure: Trading platforms, registry systems, and price discovery mechanisms remain under development, creating short-term volatility and uncertainty in early-stage participation. Initial transactions are restricted to regulated power exchanges with no over-the-counter trading.

- Technical Capacity for MRV: Smaller industrial units lack in-house resources to implement IPCC-aligned monitoring, reporting, and verification systems, posing compliance risks particularly within Tier-2 cement, paper, and chlor-alkali facilities.

- Quality Concerns in Voluntary Credits: Concerns about additionality, permanence, and double-counting in nature-based offsets continue to weigh on premium pricing, forcing developers to invest heavily in third-party verification and Climate, Community and Biodiversity Standards.

Market Opportunities

- Agriculture & Soil Carbon: With over 140 million hectares of cultivable land, regenerative agriculture and biochar projects could generate millions of credits annually. In December 2025, IIT Roorkee and the Uttar Pradesh government launched a farmer carbon credit programme expected to deliver Rs 5,000–Rs 8,000 per hectare in supplementary income.

- Green Hydrogen & Renewable Energy with Storage: India targets 5 MMT of green hydrogen production per annum by 2030, and CCTS methodologies now cover both electrolysis and biomass-based pathways, opening a substantial offset opportunity.

- Biochar and Methane Capture: In January 2025, Google committed to purchasing 100,000 tons of carbon credits from the Indian Biochar Initiative by 2030, signaling international demand for high-integrity Indian removal credits.

Market Challenges

- Implementation Timing: CCC trading is now expected only by mid-2026, three years later than originally envisioned, creating uncertainty for early-mover compliance entities and inhibiting commitment of capital to abatement projects.

- Linkage to International Markets: The CCTS is currently not linked with other systems, and offsets are not yet allowed under the compliance mechanism, limiting cross-border arbitrage and constraining liquidity in initial trading cycles.

Emerging Market Trends

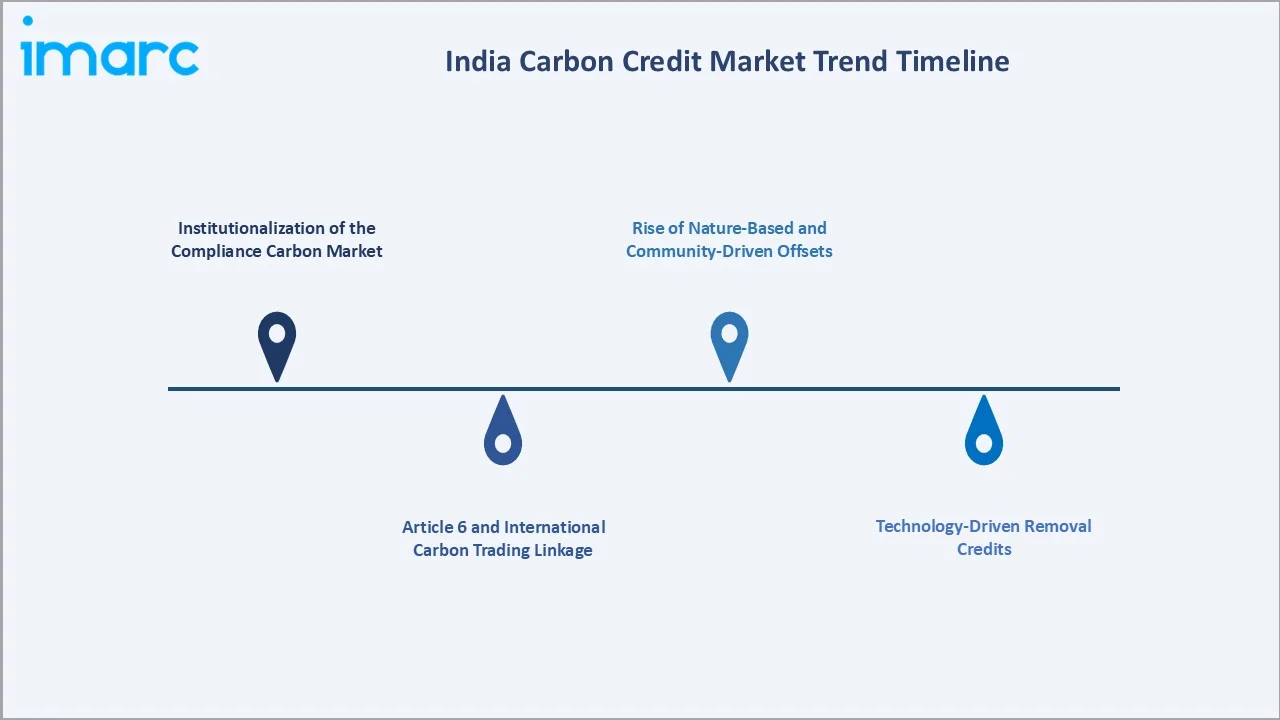

1. Institutionalization of the Compliance Carbon Market

The CCTS transitions the decade-old Perform, Achieve and Trade (PAT) scheme into an emissions-intensity-based credit system, covering nine energy-intensive sectors: aluminum, cement, chlor-alkali, fertilizer, iron & steel, pulp & paper, petrochemicals, petroleum refinery, and textiles. As of FY2025–26, compliance requirements under India’s Carbon Credit Trading Scheme (CCTS) apply to around 490 entities across seven energy-intensive sectors, following the notification of greenhouse gas (GHG) emission intensity targets by the Ministry of Environment, Forest and Climate Change (MoEFCC).

2. Rise of Nature-Based and Community-Driven Offsets

Down To Earth and the Centre for Science and Environment (DTE-CSE) revealed that by June 2023, India had 860 registered projects, with a total of 1,451 projects under different stages of evaluation across the two leading carbon crediting programs, Verra and Gold Standard, which issue carbon credits. Verra’s VM0042, VM0044, and VM0047 methodologies, paired with the Indian Council of Agricultural Research’s pilot programmes, are channelling smallholder participation into agroforestry, improved land management, and biochar projects.

3. Technology-Driven Removal Credits

Emerging removal credit pathways, including direct air capture, biochar, and floating photovoltaic, are diversifying supply. In October 2024, Greenam Energy commissioned a 24.7 MW floating solar photovoltaic plant in Tamil Nadu, the first floating solar project globally accredited under the Verified Carbon Standard, expected to avoid approximately 38,376 tonnes of CO₂ annually.

4. Article 6 and International Carbon Trading Linkage

India submitted its types of activities for international authorization under Article 6.4 of the Paris Agreement to the UNFCCC, including clean cooking using renewable energy at scale. This positions Indian projects, particularly IndianOil's Surya Nutan solar cookers (manufactured by EKI's subsidiary GHG Reduction Technologies) and Oorja Biogas systems, to generate Internationally Transferred Mitigation Outcomes (ITMOs) once the Article 6.4 mechanism becomes operational.

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Project Origination & Development |

Renewable energy IPPs, forestry and agroforestry aggregators, industrial efficiency consultants, and community-based offset originators |

|

Validation & Verification |

Designated Operational Entities (DOEs), accredited third-party auditors, and MRV technology providers |

|

Standards & Registries |

International standards bodies (Verra, Gold Standard), national crediting registries, and central regulators governing baseline setting and issuance |

|

Trading Platforms & Exchanges |

Power exchanges, commodity exchanges, OTC trading desks, and electronic registries facilitating credit transfer |

|

Brokers & Intermediaries |

Carbon credit brokers, advisory firms, climate finance consultants, and ESG advisory houses |

|

End Buyers |

Compliance-obligated industrial entities, corporate Net Zero buyers, sovereign & multilateral funds, and aviation |

Technology Landscape in the India Carbon Credit Industry

Digital MRV and Blockchain Registries

Satellite imagery, IoT sensors, and remote sensing platforms are being deployed for cost-effective, real-time monitoring of land-use carbon. Blockchain-based registries are being piloted to enhance traceability, prevent double-counting, and support automated retirement, with the Grid Controller of India Limited operating the official CCTS registry.

Renewable Energy with Storage

Hybrid solar-storage and offshore wind methodologies approved under the CCTS offset framework are unlocking high-volume credit generation. Greenko Group’s 5,230 MW pumped hydro storage portfolio in Andhra Pradesh represents a flagship technology cluster aligned with the new methodologies.

Biochar and Soil Sequestration

Biochar produced from agricultural residue offers durable carbon storage with co-benefits for soil health. In January 2025, Google signed the world’s largest biochar carbon removal deal with Indian startup Varaha, agreeing to purchase 100,000 tons of CO₂ removal credits by 2030.

Green Hydrogen Crediting

Approved methodologies cover electrolysis and biomass routes for green hydrogen, aligning with India’s 5 MMT/year target by 2030 under the National Green Hydrogen Mission.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Types | Voluntary | 58.04% | 2025 |

| Project Type | Avoidance/Reduction Projects | 52.1% | 2025 |

| End Use Industry | Power | 20.05% | 2025 |

| Region | North India | 31.0% | 2025 |

By Type

Voluntary credits dominate the type segment with a 58.04% share in 2025. Their dominance reflects strong corporate sustainability commitments, growing participation in nature-based offset projects, and rising international demand for high-integrity Indian credits certified under Verra and Gold Standard.

To access detailed market analysis, Request Sample

Compliance credits hold the remaining 41.96%, generated under the CCTS by obligated entities that outperform their assigned greenhouse gas emission intensity targets. Compliance credits are projected to gain share progressively as the CCTS commences active trading in 2026 and additional sectors, steel, fertilizer, and others, are formally onboarded into the compliance perimeter.

By Project Type

Avoidance/reduction projects lead the project-type segment at 52.1% of the Indian carbon credit market in 2025, covering renewable energy generation, energy efficiency improvements, fuel switching, and industrial process upgrades. These projects benefit from established methodologies, predictable issuance timelines, and broad buyer acceptance across both voluntary and compliance channels.

Removal/sequestration projects represent 47.9% and are split between nature-based pathways, afforestation, reforestation, mangrove restoration, soil carbon, and improved agricultural land management, and technology-based pathways, including biochar, direct air capture, and bioenergy with carbon capture.

Regional Market Insights

North India leads with a 31.0% share in 2025, anchored by energy-intensive industrial clusters across Uttar Pradesh, Haryana, Punjab, and the Delhi NCR region. The region hosts a high concentration of cement, iron and steel, fertilizer, and thermal power plants, four of the nine sectors notified under the CCTS compliance framework.

|

Region |

Share (2025) |

Key Drivers & Anchors |

|

North India |

31.0% |

Cement, iron & steel, fertilizer, thermal power; agricultural belt for biogas/biochar/afforestation projects |

|

South India |

27.4% |

Renewable energy hub; technology-based credits, including floating solar PV |

|

West India |

22.3% |

Industrial decarbonization in Dahej, Hazira chemical clusters; Rajasthan solar/wind belts; voluntary nature-based projects |

|

East India |

19.3% |

Coal-linked steel, aluminum, power assets in transition; forestry-rich states supporting REDD+ pipelines |

South India follows at 27.4%, driven by Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana, where renewable energy capacity is concentrated and where landmark projects such as Greenam Energy’s 24.7 MW floating solar plant in Tamil Nadu have set global precedents for technology-based credit issuance.

Competitive Landscape

The India carbon credit market exhibits a fragmented structure spanning project developers, verification agencies, trading platforms, brokers, and industrial conglomerates. Leading developers, EKI Energy Services lid., Greenko Group, ReNew, and NTPC, anchor high-volume renewable energy and clean cooking credit issuance.

|

Company |

Services/Brand |

Market Position |

Core Strength |

|

EKI Energy Services ltd. |

Offsetting to achieve Carbon Neutrality, Carbon Markets Capacity Building Advisory |

Market Leader |

India's largest carbon credit developer; supplied 200M+ offsets across 40+ countries; BSE-listed |

|

MITCON Consultancy & Engineering Services Limited |

MITCON |

Strong Challenger |

Pune-based long-standing technical advisory; 150+ projects with carbon credits valued at USD 9M+; cooperative-led agricultural carbon aggregation expertise |

|

Greenko Group |

Greenko |

Market Leader |

Leading energy transition company; 1,680 MW pumped hydro storage pipeline |

|

ReNew |

Decarbonization Solutions |

Strong Challenger |

Leading IPP focused on wind, solar, storage, green hydrogen pilots, and a carbon credit program tied to a renewable generation portfolio. |

|

NTPC |

NTPC |

Market Leader |

India's largest power producer, renewable subsidiary NTPC Green Energy, generates compliance and voluntary credits at scale; a central PSU with strong policy alignment. |

MITCON Consultancy & Engineering Services Limited provides advisory and intermediation services, while TÜV SÜD South Asia, DNV, and Bureau Veritas dominate validation and verification. Strategic alliances between Indian developers and global standards bodies are accelerating credit quality benchmarking and integration with international voluntary markets.

.webp)

Key Company Profiles

EKI Energy Services ltd.

EKI Energy Services ltd., headquartered in Indore, is one of India’s largest carbon credit developers and suppliers, listed on the Bombay Stock Exchange. The company has supplied over 200 million offsets across 40+ countries.

- Service Portfolio: Carbon credit generation, supply, asset management, sustainability audits, climate-positive consulting.

- Recent Development: In December 2024, the Partnership for Carbon Accounting Financials (PCAF) announced a collaboration with EKI Energy Services ltd., to support financial institutions in measuring, reporting, and managing greenhouse gas emissions tied to financial activities.

- Strategic Focus: Article 6.4 ITMO readiness through Surya Nutan and Oorja Biogas; PCAF-aligned financial sector emissions accounting.

MITCON Consultancy & Engineering Services Limited

MITCON, based in Pune, is a long-standing technical advisory firm with a deep portfolio in carbon credit syndication. To date, MITCON has facilitated carbon credits valued at over USD 9 million from 150+ projects across solar, wind, biomass, and afforestation.

- Service Portfolio: Carbon project development, validation support, GHG inventory, energy auditing, ESG advisory.

- Recent Development: In March 2025, MITCON announced the commissioning of its biochar plant as part of its sustainability and clean energy initiatives. The project supports climate action by reducing emissions and promoting circular economy practices, while creating new opportunities in carbon credit generation and sustainable agriculture.

- Strategic Focus: Mid-cap industrial and renewable energy clients; cooperative-led agricultural carbon aggregation.

Greenko Group

Greenko, headquartered in Hyderabad, is one of India’s leading energy transition companies with operations in pumped hydro storage, solar, and wind, generating substantial volumes of compliance and voluntary carbon credits.

- Service Portfolio: Renewable energy generation, integrated energy storage, hybrid utility-scale projects.

- Recent Development: In May 2024, Yara Clean Ammonia signed a landmark agreement with India’s Greenko ZeroC (AM Green) for the long-term supply of renewable ammonia from its Kakinada facility, with up to 50% of Phase-1 production allocated for global distribution.

- Strategic Focus: Pumped hydro storage at scale; offtake partnerships with Microsoft and other corporate Net Zero buyers.

Market Concentration Analysis

The India carbon credit market is moderately fragmented at the developer level, with the top five players, EKI Energy Services ltd., MITCON Consultancy & Engineering Services Limited, Greenko Group, ReNew, and NTPC, collectively accounting for an estimated 35–40% of voluntary credit issuance and a meaningful share of compliance generation through their operating assets.

A long tail of regional developers, agritech aggregators, and forestry NGOs supplies the remainder, particularly within nature-based pathways. Consolidation is gaining momentum as MRV technology, Verra/Gold Standard certification costs, and CCTS compliance complexity raise entry barriers, encouraging joint ventures and platform plays among brokers, registries, and tier-1 industrials.

Investment & Growth Opportunities

Fastest Growing Segments

Nature-based removals (estimated CAGR ~34%), green hydrogen-linked credits (~36%), and biochar (~33%) are projected to outpace the broader market through 2034, supported by approved CCTS methodologies and binding international offtake from corporate buyers including Google, Microsoft, and Stripe.

Strategic Vectors

- Vertical integration across project development, MRV, and brokerage to capture margin retention through the full credit lifecycle.

- Article 6.4 readiness to access ITMO-grade premium pricing once the bilateral mechanism becomes operational.

- CBAM-linked MRV platforms serving Indian exporters of cement, aluminum, steel, and chemicals subject to EU border carbon pricing.

Future Market Outlook (2026-2034)

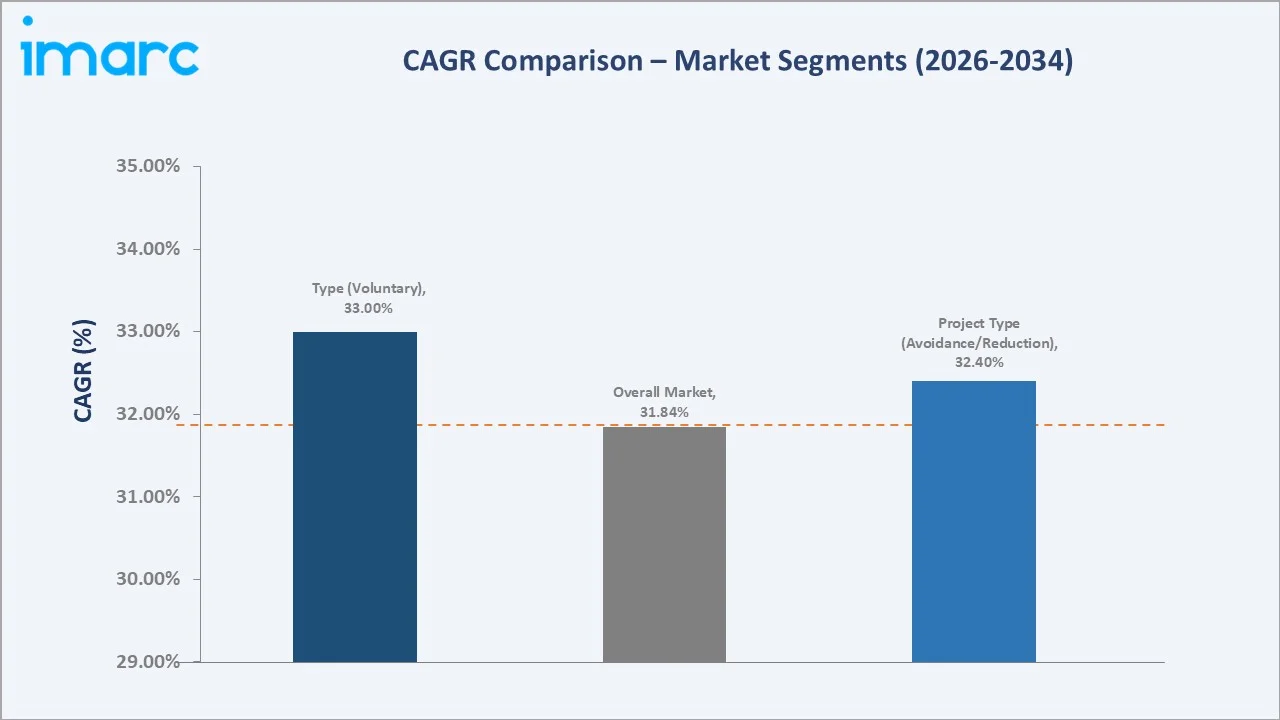

India’s carbon credit market is positioned for sustained, high-magnitude growth. From a base of USD 33.69 Billion in 2025, the market is projected to reach USD 405.47 Billion by 2034, expanding at a CAGR of 31.84%.

Three structural macro-themes will shape the trajectory: full operationalization of the CCTS compliance market with active CCC trading from 2026; deepening voluntary supply through nature-based, agricultural, and removal projects; and India’s integration with international carbon mechanisms under Article 6.4. Manufacturers, utilities, and project developers that build certified-ready, MRV-equipped portfolios early will be best positioned to capture premium pricing and serve both domestic compliance demand and CBAM-linked export markets.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including carbon credit developers, validation/verification bodies, regulatory authorities, energy-intensive industrial buyers, agricultural cooperatives, and technology providers across all four Indian regions.

Secondary Research

Secondary research included Bureau of Energy Efficiency notifications, Ministry of Power and MoEFCC publications, ICAP and IETA briefings, Verra and Gold Standard registry data, company annual reports, and trade publications. Over 200 sources were triangulated for market sizing and segmentation.

Forecasting Models

Market size estimations apply a hybrid top-down and bottom-up approach, combining sectoral abatement cost curves, NDC trajectories, voluntary credit issuance pipelines, and corporate Net Zero demand signals. The base-case CAGR of 31.84% reflects consensus across regulatory milestones, methodology approvals, and observed pricing in compliance and voluntary markets.

India Carbon Credit Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Compliance, Voluntary |

| Project Types Covered |

|

| End Use Industries Covered | Power, Energy, Aviation, Transportation, Buildings, Industrial, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | EKI Energy Services ltd., MITCON Consultancy & Engineering Services Limited, Greenko Group, ReNew, NTPC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Carbon Credit Market Report

The India carbon credit market reached USD 33.69 Billion in 2025 and is projected to reach USD 405.47 Billion by 2034.

The market is expected to grow at a CAGR of 31.84% during the forecast period 2026-2034, supported by CCTS rollout, voluntary methodology approvals, and corporate Net Zero adoption.

North India leads with a 31.0% share in 2025, driven by industrial clusters across Uttar Pradesh, Haryana, and Punjab, and a strong pipeline of agricultural and forestry offset projects.

Voluntary credits dominate the type segment at 58.04% in 2025, supported by corporate sustainability commitments and rapidly growing project registrations under Verra and Gold Standard.

Avoidance/reduction projects lead the project-type segment at 52.1% in 2025, primarily through renewable energy generation, industrial energy efficiency, and process improvement projects.

Key players include EKI Energy Services ltd., MITCON Consultancy & Engineering Services Limited, Greenko Group, ReNew, and NTPC.

The CCTS establishes a compliance carbon market covering nine energy-intensive sectors, with binding emissions intensity targets for FY2026–FY2027 and CCC trading expected from mid-2026, transforming carbon performance into a tradable financial instrument.

Key challenges include limited trading and registry infrastructure, technical capacity gaps for MRV in smaller industrial units, quality assurance concerns in voluntary credits, and the absence of linkages between Indian compliance and international offset markets.

Major opportunities lie in nature-based removals, biochar, green hydrogen-linked credits, agricultural carbon aggregation, and Article 6.4-aligned ITMO projects, with corporate offtake from buyers including Google, Microsoft, and Stripe, enhancing financial viability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)