India Carbonated Soft Drinks Market Size, Share, Trends and Forecast by Flavor, Distribution Channel, and Region, 2026-2034

India Carbonated Soft Drinks Market Summary:

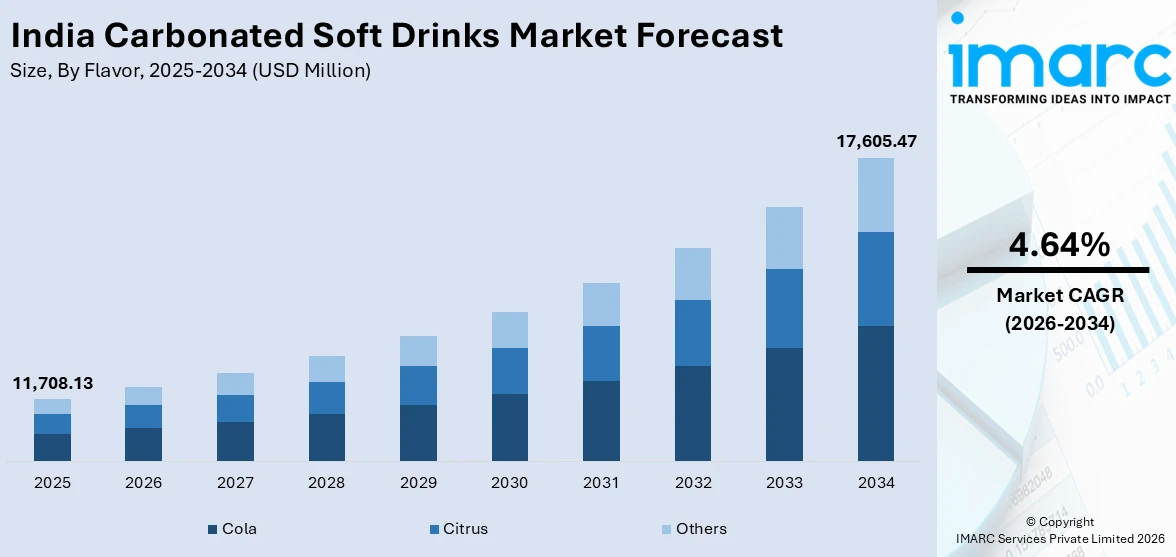

The India carbonated soft drinks market size reached USD 11,708.13 Million in 2025. The market is projected to reach USD 17,605.47 Million by 2034, growing at a CAGR of 4.64% during 2026-2034. The market is driven by the accelerating shift towards health-conscious beverage variants, including low-calorie and sugar-free options, and the rapid expansion of organized retail infrastructure penetrating Tier 2 and Tier 3 cities. Besides this, surging impact of social media platforms is fueling the India carbonated soft drinks market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 11,708.13 Million |

| Market Forecast in 2034 | USD 17,605.47 Million |

| Market Growth Rate (2026-2034) | 4.64% |

| Key Segments | Flavor (Cola, Citrus, Others), Distribution Channel (Hypermarkets, Supermarkets and General Merchandisers, Convenience Stores and Gas Stations, Food Service Outlets, Online and D2C, Others) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Carbonated Soft Drinks Market Outlook (2026-2034):

The India carbonated soft drinks market is positioned for sustained expansion throughout the forecast period, underpinned by escalating urbanization rates, rising disposable incomes across middle-class households, and evolving consumer preferences favoring packaged convenience beverages. The strategic penetration into emerging Tier 2 and Tier 3 cities represents significant untapped potential, while manufacturers' proactive introduction of healthier low-calorie and sugar-free formulations addresses the growing wellness consciousness. Additionally, government mandates aimed at promoting sustainable packaging practices are propelling the market expansion.

To get more information on this market Request Sample

Impact of AI:

AI is progressively transforming the carbonated soft drinks market in India through sophisticated applications in consumer behavior analytics, supply chain optimization, and production efficiency enhancement. AI-powered platforms enable manufacturers to analyze massive datasets from social media, e-commerce platforms, and retail channels to identify emerging flavor preferences and consumption patterns, facilitating rapid product innovations and personalized marketing campaigns. In manufacturing facilities, AI-based quality control systems and predictive maintenance algorithms are improving operational efficiency, reducing wastage, and ensuring consistent product quality.

Market Dynamics:

Key Market Trends & Growth Drivers:

Rising Health Consciousness

Indian consumers are demonstrating a decisive shift towards healthier carbonated beverage alternatives, with particular emphasis on sugar-free and low-calorie variants that align with the growing wellness awareness and lifestyle modifications. This transformation is fundamentally reshaping product portfolios across the industry, as major beverage manufacturers are responding to evolving consumer preferences by introducing diet and light offerings across multiple flagship brands. The health-conscious movement is gaining substantial momentum in urban markets where consumers are increasingly scrutinizing nutritional labels and making informed choices about sugar intake to mitigate risks associated with obesity and diabetes. Metropolitan consumers, particularly millennials and Gen-Z demographics, are actively seeking beverages that deliver refreshment without compromising their health objectives. In March 2025, both Coca-Cola and PepsiCo released zero-sugar and no-sugar variants priced at INR 10 across multiple brands, including Thums Up X Force, Coke Zero, Sprite Zero, and Pepsi No-Sugar, marking the first time their Indian operations introduced diet and light beverages at this competitive price point.

Expansion of Organized Retail Channels

The proliferation of modern retail infrastructure, encompassing supermarket chains, hypermarkets, and convenience stores, is impelling the India carbonated soft drinks market growth, substantially improving product accessibility and consumer convenience across urban and semi-urban geographies. As per the IMARC Group, the India retail market size reached USD 993.1 Billion in 2024. This retail modernization trend is creating unprecedented opportunities for beverage brands to establish stronger market presence and implement sophisticated merchandising strategies that enhance brand visibility and drive impulse purchases. Organized retail formats offer consumers the advantage of extensive product variety, competitive pricing through promotional offers, and pleasant shopping environments that encourage exploration of new beverage options. The strategic expansion into Tier 2 and Tier 3 cities, where organized retail presence is experiencing rapid growth, represents a critical avenue for market penetration, as these regions are demonstrating increasing purchasing power and evolving consumption patterns.

Sustainability Initiatives and Adoption of Recycled Packaging Materials

Environmental consciousness and regulatory imperatives are driving transformative changes in packaging practices across the market in India, with manufacturers increasingly prioritizing sustainable materials and circular economy principles in their operations. Government mandates, particularly the Plastic Waste Management Rules amendments introduced in June 2025, require beverage manufacturers to ensure at least 30% of their plastic packaging is recyclable by 2025-2026, with progressive escalation targets in subsequent years to promote comprehensive plastic waste management. This regulatory framework, combined with the growing consumer expectations for environmentally responsible brands, is encouraging companies to invest substantially in recycled packaging technologies and establish robust collection-recycling infrastructure. Major beverage corporations are demonstrating leadership by transitioning towards fully recycled PET (rPET) bottles, which significantly reduce dependence on virgin plastic while maintaining food-grade safety standards approved by international regulatory authorities.

Key Market Challenges:

Increasing Regulatory Pressure and Taxation on Sugary Beverages

Regulatory scrutiny and taxation pose a significant challenge for the carbonated soft drinks market in India. The government has been actively considering stricter norms on high-sugar consumables, including potential sugar taxes, advertising restrictions, and mandatory front-of-pack nutritional labelling. Carbonated soft drinks are taxed at a higher goods and services tax (GST) rate, placing them in the premium pricing category relative to local beverage alternatives. If additional sugar taxes are implemented, retail prices may increase further, impacting demand among price-sensitive consumers. Additionally, restrictions on marketing to children, school-zone sales limitations, and health-warning mandates could affect brand visibility and promotional strategies. Compliance with evolving food safety and labelling regulations also increases operational complexity and costs for manufacturers.

Competition from Regional Players and Low-Priced Local Beverages

The carbonated soft drinks market in India is facing intense competition from both regional bottled beverage brands and traditional low-cost local drinks, such as nimbu soda, jaljeera, aam panna, cane juice, buttermilk, and regional fruit beverages. These alternatives are often seen as more refreshing, affordable, and suited to local tastes, particularly in rural and semi-urban markets. Smaller local soda manufacturers offer products at significantly lower prices, making it difficult for large brands to maintain volume growth in price-sensitive areas. Moreover, the rapid expansion of value-based beverage categories like flavored sparkling water, masala sodas, and ethnic drinks is creating additional competition. Strong cultural attachment to regional beverages further restricts carbonated soft drink penetration beyond metros.

Seasonality of Demand and Limited Year-Round Consumption Occasions

Carbonated soft drink sales in India are heavily seasonal, with a major spike during summer months and significantly lower demand during monsoons and winter. This seasonal dependency creates volatility in production planning, inventory management, and revenue cycles. Unlike tea, coffee, or packaged water, carbonated soft drinks are not deeply embedded in daily consumption habits throughout the year. Cultural and climatic factors play a significant role, with many households avoiding cold fizzy drinks in winter or during illness, reducing recurring consumption. Limited meal-pairing acceptance also restricts year-round usage, unlike Western markets where sodas often accompany food. Events and celebrations fuel occasional demand, but regular at-home consumption remains low. Brands have attempted to position carbonated soft drinks for festivals, parties, and youth hangouts, but the category still lacks universal daily relevance.

India Carbonated Soft Drinks Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India carbonated soft drinks market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on flavor and distribution channel.

Analysis by Flavor:

- Cola

- Citrus

- Others

The report has provided a detailed breakup and analysis of the market based on the flavor. This includes cola, citrus, and others.

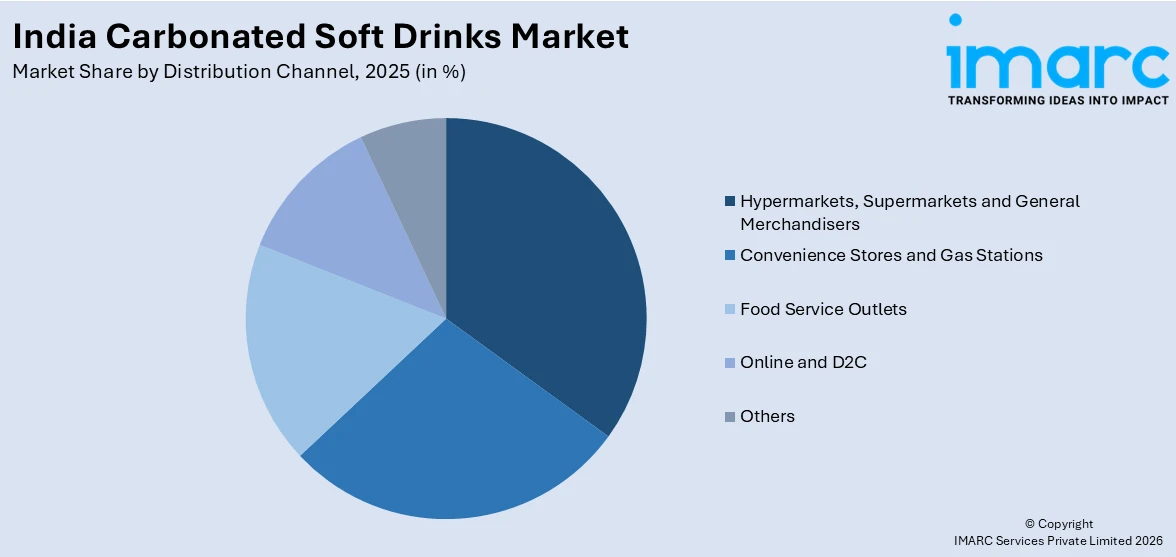

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Hypermarkets, Supermarkets and General Merchandisers

- Convenience Stores and Gas Stations

- Food Service Outlets

- Online and D2C

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes hypermarkets, supermarkets and general merchandisers, convenience stores and gas stations, food service outlets, online and D2C, and others.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India carbonated soft drinks market exhibits a highly competitive landscape dominated by multinational beverage giants with extensive distribution networks, complemented by emerging domestic brands. Competition primarily centers on brand loyalty cultivated through decades of consistent marketing, product quality maintained through sophisticated manufacturing processes, and distribution excellence, ensuring ubiquitous availability across urban and rural markets. Established international players maintain competitive advantages through substantial marketing budgets enabling high-visibility campaigns, celebrity endorsements, and sports sponsorships that reinforce brand positioning. The market is witnessing strategic responses from major players, including portfolio diversification towards healthier variants, volume expansion initiatives, and sustainability commitments addressing environmental consciousness. Innovations in flavors, packaging formats, and value propositions continue to drive competitive differentiation, as companies are seeking to capture evolving consumer preferences across diverse demographic segments throughout India's heterogeneous market landscape.

India Carbonated Soft Drinks Industry Latest Developments:

- October 2025: Nakoda Group of Industries Limited, a firm based in India, proudly revealed its strategic entry into the rapidly expanding beverages sector with the introduction of its new brand ‘NO CTRL (NO CONTROL),’ which featured a selection of energy drinks and flavored carbonated soft drinks. The release highlighted Nakoda’s commitment to penetrate high-demand consumer markets with innovative products aimed at the youth.

India Carbonated Soft Drinks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Flavors Covered | Cola, Citrus, Others |

| Distribution Channels Covered | Hypermarkets, Supermarkets and General Merchandisers, Convenience Stores and Gas Stations, Food Service Outlets, Online and D2C, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Carbonated Soft Drinks Market Report

The India carbonated soft drinks market reached a value of USD 11,708.13 Million in 2025

The market is projected to grow at a CAGR of 4.64% during 2026-2034, reaching USD 17,605.47 Million by 2034.

Key growth drivers include rising health consciousness, tier 2 and tier 3 retail penetration, social media influence on consumer choices, and increasing disposable income among urban households.

The report covers segmentation by flavor, distribution channel, and region. Each segment includes detailed market size and forecast analysis.

Key trends include low-calorie and sugar-free variant launches, sustainable rPET packaging adoption, AI-driven flavor innovation, and regional market diversification targeting health-oriented youth demographics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)