India Cardiovascular Devices Market Size, Share, Trends and Forecast by Device Type, Application, End User, and Region, 2026-2034

India Cardiovascular Devices Market Summary:

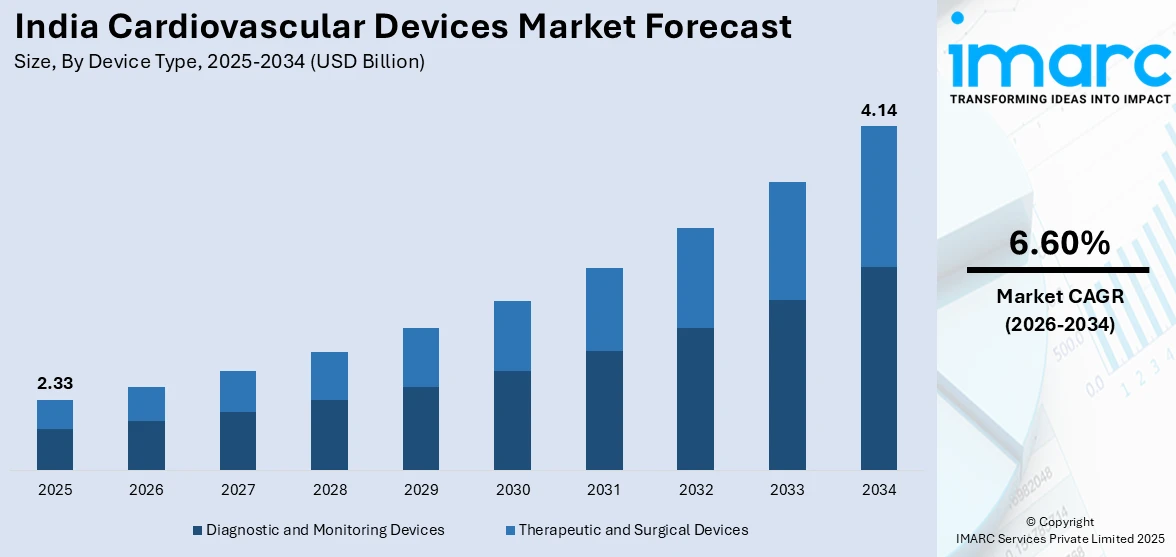

The India cardiovascular devices market size was valued at USD 2.33 Billion in 2025 and is projected to reach USD 4.14 Billion by 2034, growing at a compound annual growth rate of 6.60% from 2026-2034.

The India cardiovascular devices market is growing steadily, driven by the increasing incidence of cardiovascular diseases, the fast development of the healthcare infrastructure, and the increasing adoption of advanced diagnostic and therapeutic solutions. The increasing penetration of health insurance, the increasing awareness about preventive cardiac care, and the strong government initiatives for the development of domestic medical device manufacturing are all contributing to the growing demand in various product segments, thus boosting the India cardiovascular devices market share.

Key Takeaways and Insights:

- By Device Type: Diagnostic and monitoring devices dominate the market with a share of 55% in 2025, driven by the widespread integration of electrocardiogram systems and remote cardiac monitoring solutions across healthcare facilities throughout India.

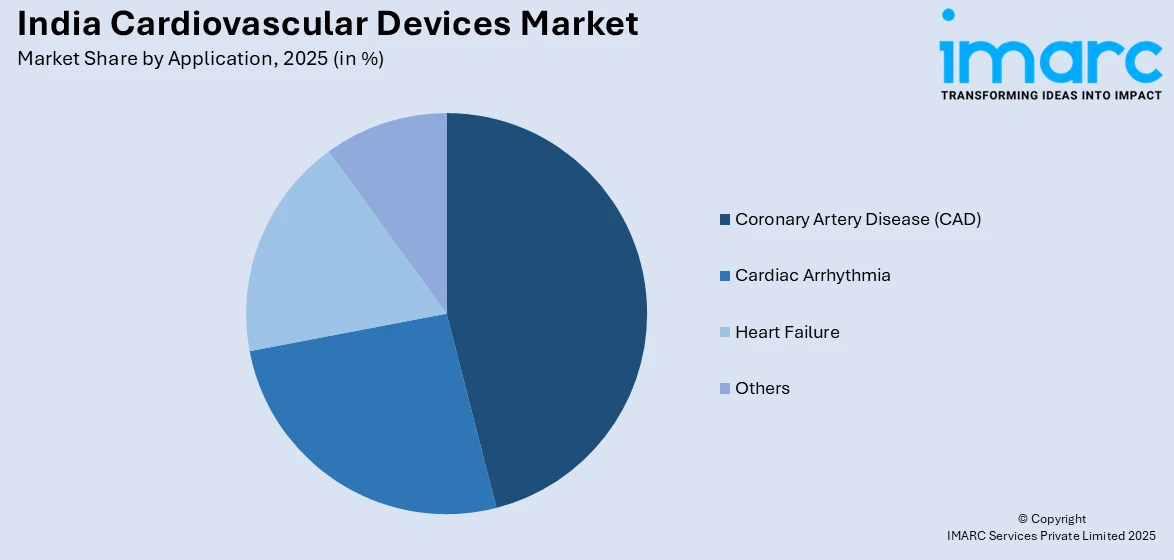

- By Application: Coronary Artery Disease (CAD) leads the market with a share of 43% in 2025, reflecting the high incidence of ischemic heart conditions and strong demand for dedicated coronary diagnostic and interventional devices.

- By End User: Hospitals represent the largest segment with a market share of 70% in 2025, supported by their advanced cardiovascular infrastructure, including catheterization laboratories and hybrid operating rooms enabling complex cardiac procedures.

- Key Players: The India cardiovascular devices market features a mix of established multinational medical device corporations and emerging domestic manufacturers, competing across diagnostic, monitoring, and interventional segments through technology-driven product portfolios and strategic distribution networks.

To get more information on this market Request Sample

India's cardiovascular devices market is shaped by a rapidly evolving healthcare landscape, driven by demographic shifts and escalating lifestyle-related health conditions. The country's large and diverse population presents a wide spectrum of cardiovascular health needs, ranging from preventive diagnostics to complex interventional therapies. In September 2025, Medtronic introduced its Evolut™ FX+ transcatheter aortic valve system in India following approval from the Central Drugs Standard Control Organization (CDSCO), enhancing treatment options for patients with severe aortic stenosis and underscoring increased access to advanced interventional cardiology devices. Public and private healthcare institutions are steadily expanding their cardiac care capabilities, creating sustained demand for both diagnostic and surgical devices. The integration of digital health platforms and remote monitoring technologies is transforming patient care pathways, enabling early detection and continuous management of cardiac conditions. Favorable government policies supporting domestic medical device production are reducing import dependency while improving affordability, broadening access to cardiovascular devices across diverse healthcare settings nationwide.

India Cardiovascular Devices Market Trends:

Rising Adoption of Remote Cardiac Monitoring Solutions

The increasing demand for continuous cardiac surveillance is driving rapid integration of remote monitoring technologies across India's healthcare landscape. Wearable and connected devices enable uninterrupted tracking of heart rhythm, electrical activity, and vital cardiovascular parameters for patients managing chronic heart conditions. In December 2025, Indian health‑tech firm vTitan launched its AI‑enabled vCardio wearable cardiac monitor, a locally developed solution designed to provide continuous ECG tracking and real‑time anomaly detection, facilitating remote patient monitoring both in clinical settings and at home. These solutions facilitate prompt clinical intervention by transmitting real-time physiological data to care teams, significantly enhancing early detection capabilities and supporting more proactive, outcomes-focused cardiac management throughout diverse healthcare settings across the country.

Expansion of Minimally Invasive Cardiovascular Interventions

Minimally invasive cardiovascular procedures are redefining treatment standards across India, with healthcare providers increasingly prioritizing approaches that minimize surgical trauma and accelerate patient recovery. Advanced catheter-based technologies and imaging-guided interventional techniques empower clinicians to address complex cardiac conditions with enhanced procedural precision and reduced complication risk. For example, in May 2025, S.L. Raheja Hospital in Mumbai completed 50 successful Transcatheter Aortic Valve Replacement (TAVR) procedures, underscoring the growing adoption and clinical success of minimally invasive structural heart interventions in the country. This clinical shift is driving consistent adoption of specialized interventional instruments across tertiary hospitals and dedicated cardiac centers, reshaping how cardiovascular diseases are managed throughout the country.

Integration of Artificial Intelligence in Cardiac Diagnostics

Artificial intelligence is progressively embedded within cardiovascular diagnostic platforms, fundamentally improving the speed and accuracy of cardiac assessment across clinical environments in India. Intelligent algorithms analyze electrocardiogram outputs, echocardiographic imaging, and patient health histories to identify abnormalities with greater consistency than conventional methods alone. In September 2025, AliveCor launched its AI‑powered Kardia 12L handheld 12‑lead ECG system in India, the first of its kind cleared by the Central Drugs Standard Control Organisation (CDSCO), enabling clinicians to rapidly detect a wide range of cardiac conditions, including arrhythmias and ischemia, with real‑time AI analysis at the point of care. This capability enables clinicians to detect conditions at earlier stages and develop individualized treatment strategies aligned with specific patient risk profiles, enhancing diagnostic confidence and supporting more precise, personalized cardiovascular care delivery.

Market Outlook 2026-2034:

The India cardiovascular devices market is expected to witness steady growth during the forecast period, driven by the increasing burden of cardiovascular diseases, government investments in the healthcare infrastructure, and the growing need for advanced technology-based diagnostic and therapeutic solutions. The rising adoption of remote monitoring and AI-based diagnostic solutions is also expected to fuel growth in this market, across tier-one and tier-two cities. Increasing public-private partnerships in the field of cardiac care and favorable government policies for manufacturing are also expected to improve the accessibility and affordability of products. The market generated a revenue of USD 2.33 Billion in 2025 and is projected to reach a revenue of USD 4.14 Billion by 2034, growing at a compound annual growth rate of 6.60% from 2026-2034.

India Cardiovascular Devices Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Device Type | Diagnostic and Monitoring Devices | 55% |

| Application | Coronary Artery Disease (CAD) | 43% |

| End User | Hospitals | 70% |

Device Type Insights:

- Diagnostic and Monitoring Devices

- Electrocardiogram (ECG)

- Remote Cardiac Monitoring

- Others

- Therapeutic and Surgical Devices

- Cardiac Rhythm Management (CRM) Devices

- Catheter

- Stents

- Heart Valves

- Others

The diagnostic and monitoring devices dominate with a market share of 55% of the total India cardiovascular devices market in 2025.

Diagnostic and monitoring devices lead the way in the India cardiovascular devices market, supported by the need for precise and constant cardiac monitoring. Electrocardiogram systems continue to play a pivotal role in the routine cardiac assessment of patients in a hospital or clinic setting, providing critical information regarding heart rate, rhythm, and electrical conduction abnormalities. The widespread use of electrocardiogram systems in primary and secondary care facilities cements their primary role in the cardiovascular diagnostic landscape of India.

Remote cardiac monitoring is one of the most rapidly developing sub-segments of the device type, driven by the increasing adoption of wearable technology and digital health platforms that enable the continuous monitoring of physiological functions outside of the traditional healthcare setting. These solutions offer significant clinical benefit to patients with arrhythmias and other chronic cardiovascular diseases, enabling the remote transmission of physiological data to healthcare providers for timely intervention. The convergence of advanced connectivity capabilities with smaller sensor technologies is steadily expanding the accessibility and utility of remote cardiac monitoring solutions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Coronary Artery Disease (CAD)

- Cardiac Arrhythmia

- Heart Failure

- Others

Coronary Artery Disease (CAD) leads with a share of 43% of the total India cardiovascular devices market in 2025.

Coronary artery disease continues to be the most common form of cardiovascular disease in the Indian subcontinent, thereby creating a constant demand for advanced diagnostic and interventional equipment. The high prevalence of Ischemic Heart Disease, which is largely driven by lifestyle factors such as a sedentary lifestyle, changing eating habits, and stress, requires effective diagnostic and therapeutic strategies. Diagnostic Imaging Equipment, Coronary Catheterization Systems, and Drug Eluting Stents are the three main tools used in the management of CAD.

The treatment of coronary artery disease is increasingly being covered by integrated care pathways that integrate accurate diagnostic skills with minimally invasive treatment approaches. The latest advances in coronary stenting and catheter-based revascularization are providing better clinical results with reduced procedural complexity and shorter recovery times. The rising focus on early risk assessment and preventive cardiology is also driving the adoption of monitoring and imaging solutions. These factors, taken together, continue to make CAD the leading application segment that influences the demand for cardiovascular devices in India.

End User Insights:

- Hospitals

- Specialty Clinics

- Others

The hospitals dominate with a market share of 70% of the total India cardiovascular devices market in 2025.

Hospitals serve as the primary channel for cardiovascular device adoption across India, supported by their comprehensive cardiac care infrastructure and capacity to conduct complex diagnostic and interventional procedures. Tertiary care and multi-specialty hospitals operate advanced catheterization laboratories, electrophysiology suites, and sophisticated imaging platforms that collectively require an extensive range of cardiovascular devices. The dense concentration of trained cardiologists and cardiac surgeons within these institutional settings further reinforces hospitals' central and indispensable role in device utilization.

The hospital segment continues attracting substantial investment in cardiovascular technology upgrades, driven by expanding patient volumes and growing institutional focus on superior clinical outcomes. Public tertiary care facilities and private multi-specialty hospitals alike are progressively enlarging their cardiac departments, integrating advanced interventional instruments and continuous monitoring technologies into established clinical workflows. Additionally, government-sponsored cardiac care programs are systematically directing patients toward accredited hospital networks, generating consistent device procurement demand and firmly reinforcing the hospital segment's dominant standing within India's cardiovascular devices end-user landscape.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents a significant cardiovascular devices market, anchored by major tertiary care hospitals and specialized cardiac centers concentrated in key metropolitan areas. High population density, rising lifestyle-associated cardiovascular risk factors, and rapid expansion of private healthcare facilities collectively sustain strong and consistent demand for both diagnostic and therapeutic cardiovascular devices throughout the region.

West and Central India demonstrate robust cardiovascular device demand, underpinned by a well-established private healthcare ecosystem and high urbanization levels across key metropolitan centers. The region's expanding network of specialty cardiac hospitals, multi-specialty facilities, and advanced diagnostic centers continues to accelerate device adoption and broaden access to comprehensive cardiovascular care services.

South India exhibits substantial cardiovascular device uptake, driven by a high concentration of internationally accredited hospitals and advanced cardiac care facilities offering specialized interventional and diagnostic services. The region's prominence as a medical tourism destination and consistently high cardiac procedure volumes sustain strong and diversified demand for cardiovascular diagnostic and therapeutic devices.

East and Northeast India constitute an emerging cardiovascular devices market, characterized by progressively expanding healthcare infrastructure and growing population awareness of cardiac health conditions. Government-led healthcare initiatives and increasing private sector investment are steadily improving access to cardiovascular diagnostics and therapeutic solutions, creating meaningful growth opportunities across underserved communities throughout the region.

Market Dynamics:

Growth Drivers:

Why is the India Cardiovascular Devices Market Growing?

Rising Burden of Cardiovascular Diseases

The increasing prevalence of cardiovascular diseases across India's diverse population is a fundamental driver propelling market growth. Rapid urbanization, sedentary lifestyles, high-calorie dietary patterns, and elevated stress levels have significantly increased the incidence of conditions including coronary artery disease, hypertension, and cardiac arrhythmia. According to the 2021‑2023 Cause of Death Report by the Sample Registration System (SRS) under the Registrar General of India, cardiovascular diseases now account for nearly one‑third of all deaths in the country, making CVD the leading cause of mortality. This expanding disease burden translates directly into heightened demand for cardiovascular devices across both diagnostic and therapeutic categories. Healthcare providers are progressively scaling their cardiac care capabilities to address rising patient volumes, necessitating broader deployment of advanced monitoring systems, interventional instruments, and imaging technologies. Furthermore, growing awareness of cardiovascular risk factors is encouraging early medical consultation and routine cardiac screenings, sustaining continuous demand for cardiovascular devices throughout the country.

Government Initiatives and Healthcare Policy Support

Supportive government policies and healthcare programs are significantly contributing to the growth of the cardiovascular devices market in India. National health coverage schemes designed to extend cardiac care access to economically vulnerable populations are driving patient volumes at public and private healthcare institutions equipped with cardiovascular technology. Production-linked incentive programs encouraging domestic manufacturing of medical devices are reducing dependency on imports and improving the affordability of cardiovascular equipment across healthcare settings. As of 2025, under the PLI Scheme for Medical Devices, 22 greenfield projects have started production of over 55 products, including critical imaging and cardio‑respiratory devices formerly reliant on imports. These policy frameworks are creating a conducive environment for both established manufacturers and emerging domestic players to expand their market presence, enhancing the availability and adoption of cardiovascular diagnostic and therapeutic devices at a national scale.

Technological Advancements in Cardiovascular Devices

Continuous innovation in cardiovascular device technology is accelerating market expansion by improving the clinical effectiveness and usability of diagnostic and therapeutic tools. The development of next-generation electrocardiographic systems, advanced catheter-based interventional devices, and smart cardiac monitoring wearables is transforming how cardiovascular conditions are detected and managed. In November 2025, Indian medtech firm Meril Life Sciences presented one-year results from its LANDMARK trial for the indigenous Myval transcatheter heart valve at PCR London Valves 2025, the first global study comparing an India-developed THV with leading international platforms. Integration of digital connectivity and data analytics capabilities into modern cardiovascular platforms enables seamless information sharing between patients and clinicians, supporting proactive disease management. The growing adoption of artificial intelligence-assisted diagnostic tools further enhances detection accuracy, enabling earlier intervention and better patient outcomes, collectively expanding the addressable market for cardiovascular devices throughout India.

Market Restraints:

What Challenges the India Cardiovascular Devices Market is Facing?

Regulatory Complexities and Approval Timelines

The regulatory framework governing medical device approval in India is evolving, and compliance with updated standards can be time-consuming and resource-intensive for manufacturers. Extended approval timelines for new cardiovascular device introductions may delay market entry, limiting the availability of innovative technologies. Navigating multi-stage regulatory requirements across different device categories adds operational complexity for manufacturers seeking to launch advanced cardiovascular solutions.

High Cost of Advanced Cardiovascular Devices

The significant cost associated with advanced cardiovascular devices presents affordability challenges for a substantial portion of the patient population in India. Premium diagnostic systems, implantable therapeutic devices, and specialized interventional instruments remain financially inaccessible to patients outside major urban centers or without comprehensive health insurance coverage, limiting market penetration across lower-income demographics and rural healthcare settings.

Infrastructure Disparities Across Healthcare Settings

Significant disparities in healthcare infrastructure between metropolitan and rural regions of India constrain the equitable adoption of cardiovascular devices. Tier-two and tier-three healthcare facilities often lack the physical infrastructure, trained clinical personnel, and technical support systems required to operate advanced cardiac diagnostic and monitoring technologies, limiting market reach and slowing the broader diffusion of cardiovascular solutions beyond well-equipped urban healthcare centers.

Competitive Landscape:

The India cardiovascular devices market is characterized by a dynamic and evolving competitive landscape, comprising a blend of established multinational medical device corporations and a growing cohort of domestic manufacturers. Multinational players leverage their extensive research and development capabilities, global manufacturing excellence, and established clinical credibility to maintain strong market positions across premium diagnostic and therapeutic device segments. Domestic manufacturers are increasingly competitive, differentiating through cost-effective product offerings and localized manufacturing capabilities that align with government procurement preferences and affordability requirements across public healthcare settings. Strategic partnerships between international device companies and Indian healthcare institutions are facilitating technology transfer and accelerating the localization of advanced cardiovascular solutions. Competition is intensifying across diagnostic imaging, remote monitoring, interventional cardiology, and cardiac rhythm management segments, with players focusing on product innovation, digital integration, and distribution network expansion to capture share across both urban and emerging tier-two markets.

Recent Developments:

- In January 2026, Cardio Diagnostics Holdings, in partnership with Aimil Ltd. and Dr. Lal PathLabs, launched the PrecisionCHD™ test in India. This AI‑powered blood test detects drivers of coronary heart disease, including non‑obstructive CHD, enabling personalized management. The launch marks Cardio Diagnostics’ first expansion outside the USA.

India Cardiovascular Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Device Types Covered |

|

| Applications Covered | Coronary Artery Disease (CAD), Cardiac Arrhythmia, Heart Failure, Others |

| End Users Covered | Hospitals, Specialty Clinics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Cardiovascular Devices Market Research Report and Industry Forecast Report

The India cardiovascular devices market size was valued at USD 2.33 Billion in 2025.

The India cardiovascular devices market is expected to grow at a compound annual growth rate of 6.60% from 2026-2034 to reach USD 4.14 Billion by 2034.

Diagnostic and monitoring devices dominated the market, capturing 55% share, driven by the high utilization of electrocardiogram systems and remote monitoring solutions across India's healthcare facilities.

Key factors driving the India cardiovascular devices market include the rising prevalence of cardiovascular diseases, expanding healthcare infrastructure, favorable government policies, technological innovation in diagnostic and therapeutic devices, and growing health insurance penetration across diverse population segments.

Major challenges include regulatory compliance complexities, high cost of advanced cardiovascular devices limiting affordability, and infrastructure disparities between metropolitan and rural healthcare settings constraining equitable market penetration across the country.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)