India Carotenoids Market Size, Share, Trends and Forecast by Product Type, Source, Formulation, Application, and Region, 2026-2034

India Carotenoids Market Summary:

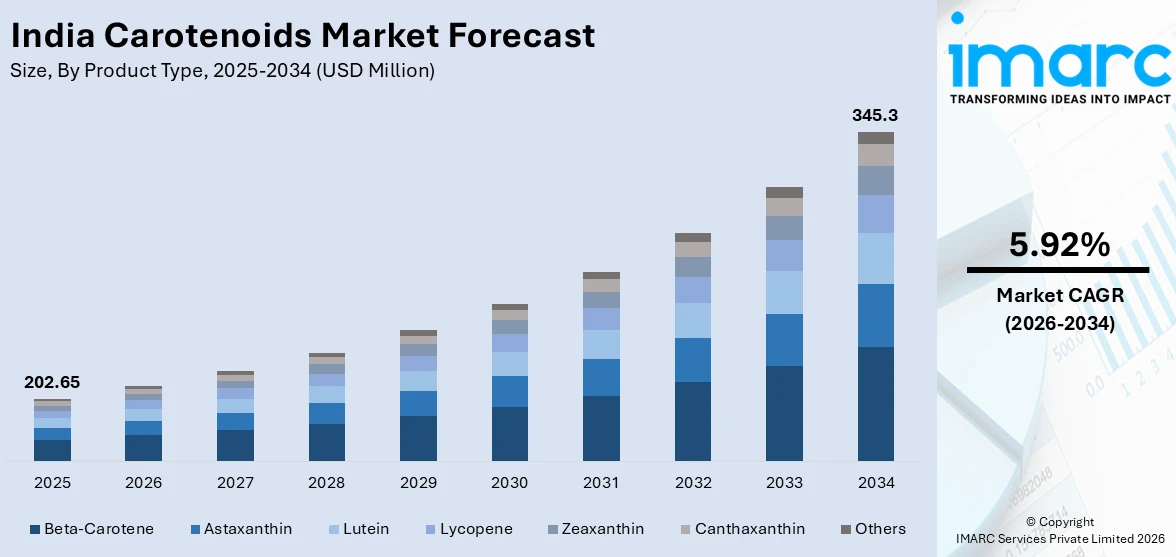

The India carotenoids market size was valued at USD 202.65 Million in 2025 and is projected to reach USD 345.3 Million by 2034, growing at a compound annual growth rate of 5.92% from 2026-2034.

The India carotenoids market is experiencing robust expansion, propelled by the country’s rising demand for natural colorants, functional food ingredients, and health-oriented nutraceutical products. Growing consumer preference for clean-label formulations, increased adoption of carotenoid-enriched dietary supplements, and an evolving regulatory environment favoring natural additives are collectively reshaping India’s carotenoids landscape. Expanding applications across food processing, animal nutrition, and personal care sectors continue to strengthen India carotenoids market share.

Key Takeaways and Insights:

- By Product Type: Beta-carotene dominates the market with a share of 31.8% in 2025, owing to its widespread adoption as a provitamin A source in food fortification, dietary supplements, and animal feed applications. Regulatory endorsement of beta-carotene as a safe natural colorant further reinforces its market leadership.

- By Source: Synthetic leads the market with a share of 58.7% in 2025. This dominance is driven by cost-effectiveness, consistent quality, and scalability of synthetic carotenoid production that meets the high-volume requirements of India’s food processing and animal nutrition industries.

- By Formulation: Powder exhibits a clear dominance in the market with 36.9% share in 2025, reflecting strong manufacturer preference for versatile, shelf-stable, and easily blendable formulations suited to diverse food, supplement, and feed production processes.

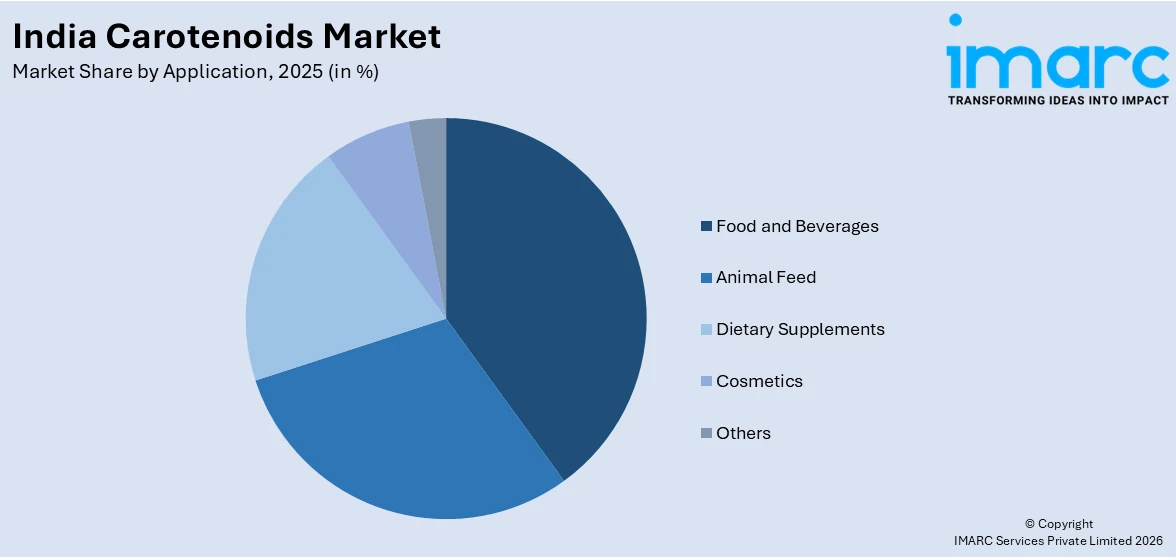

- By Application: Food and beverages hold the largest segment with a market share of 34.6% in 2025, reflecting the core demand for natural colorants and nutritional enhancers across India’s expansive processed food and functional beverage sectors.

- By Region: North India represents the leading region with 33.4% share in 2025, driven by the concentration of major food processing hubs, pharmaceutical manufacturing clusters, and a large consumer base with rising health awareness across Delhi-NCR, Uttar Pradesh, and Punjab.

- Key Players: Key players drive the India carotenoids market by expanding production capacities, investing in advanced encapsulation and formulation technologies, and strengthening distribution networks. Their focus on backward integration, quality certifications, and partnerships with food and supplement manufacturers accelerates product innovation and ensures consistent supply across diverse industry segments.

To get more information on this market Request Sample

The India carotenoids market is progressing as the Indian food processing, nutraceutical, and animal feed industries continue to grow. Increasing health awareness among the growing Indian middle class is driving the demand for functional ingredients that provide antioxidant, immunological, and nutritional benefits. The Indian regulatory framework, as governed by the Food Safety and Standards Authority of India, is supportive of carotenoid adoption and allows the use of beta-carotene, canthaxanthin, and other carotenoid compounds as approved natural food color additives. With India being the most populous nation in the world and the country undergoing rapid urbanization and dietary changes, there is a huge market demand for carotenoid-supplemented products, including fortified drinks and foods, eye health supplements, and poultry feed additives. For example, Improvements in microalgae fermentation and microencapsulation technologies are making it easier for manufacturers to develop cost-effective and highly bioavailable carotenoid formulations specifically suited to the India market.

India Carotenoids Market Trends:

Rising Demand for Clean-Label and Natural Ingredients

Indian consumers are increasingly gravitating toward food and beverage products formulated with natural, recognizable ingredients, driving demand for plant-derived and microalgae-sourced carotenoids as alternatives to synthetic colorants. Manufacturers are reformulating product lines to incorporate natural beta-carotene and lycopene to meet clean-label expectations. For instance, the Food Safety and Standards Authority of India has listed beta-carotene among its approved natural food colorants under the Food Safety and Standards Regulations, reinforcing consumer confidence and enabling broader commercial adoption of carotenoid-based colorants across processed food categories.

Expansion of Functional Food and Nutraceutical Applications

India’s nutraceutical sector is witnessing rapid growth, creating new demand channels for carotenoids in dietary supplements, functional beverages, and wellness products. Carotenoids such as lutein for eye health and astaxanthin for anti-aging are gaining popularity among health-conscious urban consumers. For instance, according to the IMARC Group, India’s nutraceutical market size was valued at USD 8.93 Billion in 2025 and is projected to reach USD 23.09 Billion by 2034, growing at a compound annual growth rate of 11.14% from 2026-2034, indicating a substantial addressable market for carotenoid-based supplement formulations, supporting India carotenoids market growth.

Technological Advances in Carotenoid Production and Formulation

Indian manufacturers are investing in advanced production methods including microbial fermentation, supercritical extraction, and microencapsulation technologies to enhance carotenoid bioavailability, stability, and cost efficiency. These innovations enable manufacturers to develop novel formulations suited for diverse applications in food fortification, cosmetics, and pharmaceutical preparations. For instance, in May 2025, a leading Indian carotenoid manufacturer presented its MiniBeads micro-encapsulated carotenoid and vitamin solutions at Vitafoods Europe, demonstrating India’s growing capabilities in developing advanced, application-specific carotenoid ingredient technologies for global markets.

Market Outlook 2026-2034:

The India carotenoids market is set for growth, with the increasing number of food processing operations, the rising use of dietary supplements, and the modernization of animal feed practices. The government's efforts to promote the use of natural food additives, the growing awareness of preventive nutrition, and the development of aquaculture and poultry sectors are expected to fuel the revenue growth of the India carotenoids market. The development of manufacturing capabilities and the standardization of products will further enhance the India carotenoids market. The market generated a revenue of USD 202.65 Million in 2025 and is projected to reach a revenue of USD 345.3 Million by 2034, growing at a compound annual growth rate of 5.92% from 2026-2034.

India Carotenoids Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Beta-Carotene |

31.8% |

|

Source |

Synthetic |

58.7% |

|

Formulation |

Powder |

36.9% |

|

Application |

Food and Beverages |

34.6% |

|

Region |

North India |

33.4% |

Product Type Insights:

- Beta-Carotene

- Astaxanthin

- Lutein

- Lycopene

- Zeaxanthin

- Canthaxanthin

- Others

Beta-carotene dominates with a market share of 31.8% of the total India carotenoids market in 2025.

Beta-carotene is the most widely consumed carotenoid in India, valued for its dual function as a natural colorant and provitamin A source. Its extensive use spans food fortification programs, dietary supplement formulations, and poultry feed production, where it enhances egg yolk pigmentation and supports animal health. Regulatory acceptance by the Food Safety and Standards Authority of India as a permitted natural food color under the Food Safety and Standards Regulations has facilitated its widespread integration across India’s processed food industry, from bakery products to dairy beverages.

The segment benefits from India’s growing food processing sector and rising demand for vitamin A-enriched products driven by government nutrition initiatives. Manufacturers are developing advanced formulations including water-dispersible powders, oil suspensions, and micro-encapsulated beadlets to meet diverse application requirements. India’s strong pharmaceutical manufacturing base, particularly among companies with integrated carotenoid production capabilities in Hyderabad and Visakhapatnam, supports cost-competitive supply chains that serve both domestic consumption and export markets across Asia, Europe, and the Americas.

Source Insights:

- Synthetic

- Natural

Synthetic leads with a share of 58.7% of the total India carotenoids market in 2025.

Synthetic carotenoids maintain strong market leadership in India owing to their cost advantages, consistent quality parameters, and ability to meet large-scale production requirements across the food, feed, and pharmaceutical industries. Chemical synthesis processes deliver standardized product specifications essential for industrial applications where precise color intensity and nutritional content are required. India's expanding animal feed sector relies heavily on synthetic carotenoids for cost-effective supplementation across poultry, aquaculture, and dairy operations, reinforcing sustained demand throughout the value chain.

Indian manufacturers have developed robust synthetic production capabilities supported by backward integration and pharmaceutical-grade quality management systems. The ability to produce multiple carotenoid types including beta-carotene, canthaxanthin, and astaxanthin from integrated chemical synthesis platforms enables competitive pricing and supply reliability. However, the natural carotenoids segment is gaining momentum as clean-label preferences expand, prompting manufacturers to invest in microalgae-based and fermentation-derived production technologies to complement their synthetic portfolios and address evolving consumer preferences.

Formulation Insights:

- Oil Suspension

- Powder

- Emulsion

- Others

Powder exhibits a clear dominance with a 36.9% share of the total India carotenoids market in 2025.

Powder formulations lead the India carotenoids market due to their versatility, extended shelf life, and compatibility with diverse manufacturing processes across food, dietary supplements, and animal feed sectors. Powdered carotenoids offer advantages in blending uniformity, controlled dosing, and ease of incorporation into dry mixes, capsules, and tablet formulations. The growing nutritional supplements industry in India demonstrates strong alignment between carotenoid powder demand and broader consumption patterns, further reinforcing the dominance of this formulation type.

Manufacturers are advancing powder formulations through spray-drying and microencapsulation techniques that improve color stability, bioavailability, and resistance to oxidation during storage and processing. These innovations are particularly relevant for India’s tropical climate, where ingredient degradation from heat and humidity presents formulation challenges. The growing popularity of protein powders, functional drink mixes, and fortified food products among India’s young, health-conscious demographic is creating sustained demand for high-performance carotenoid powder ingredients tailored for modern product development requirements.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Animal Feed

- Dietary Supplements

- Food and Beverages

- Cosmetics

- Others

Food and beverages hold the largest share at 34.6% of the total India carotenoids market in 2025.

The food and beverages segment commands the largest share of India's carotenoids market, driven by the country's rapidly expanding processed food industry and consumer demand for naturally colored, nutritionally fortified products. Beta-carotene, lycopene, and lutein are widely utilized as coloring and functional ingredients in bakery products, dairy beverages, confectioneries, and ready-to-eat meals. Significant government support through modernization and value addition initiatives under the Ministry of Food Processing Industries continues to strengthen demand for carotenoid-based ingredients across the sector.

Growing urbanization and evolving dietary patterns among India’s young population are accelerating demand for functional food and beverage products enriched with health-promoting ingredients. Manufacturers are incorporating carotenoids into fortified juices, plant-based dairy alternatives, snack foods, and instant noodle products to address nutritional deficiencies and appeal to wellness-oriented consumers. The convergence of clean-label trends, rising disposable incomes, and increasing awareness about the health benefits of antioxidant-rich diets positions the food and beverages segment for continued growth across urban and semi-urban markets.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents the leading region with a 33.4% share of the total India carotenoids market in 2025.

North India leads in terms of the overall market share in the India carotenoids market, driven by the presence of food processing firms, pharmaceutical manufacturing units, and a large consumer base in the states of Uttar Pradesh, Delhi-NCR, Punjab, and Haryana. The region's established distribution network and proximity to large consumption centers facilitate smooth supply chain management for carotenoid manufacturers. North India's poultry sector, one of the largest in the country, also supports substantial demand for feed-grade carotenoids to improve egg yolk color and poultry health.

The increasing urban population and health awareness in the region are fueling the demand for dietary supplements and functional foods containing carotenoids. Large cities in North India are emerging as prominent markets for nutraceutical brands that use beta-carotene, lutein, and astaxanthin in wellness products for eye health, immunity, and anti-aging purposes. The presence of organized retail stores, growing e-commerce penetration, and rising consumer expenditure on preventive healthcare products together contribute to sustained demand for carotenoids in North India.

Market Dynamics:

Growth Drivers:

Why is the India Carotenoids Market Growing?

Expanding Food Processing and Fortification Initiatives

India’s food processing industry is undergoing rapid modernization, creating substantial demand for carotenoid-based colorants and nutritional additives. The government’s focus on reducing post-harvest losses and promoting value-added food manufacturing through initiatives such as the Production-Linked Incentive scheme for food processing is encouraging manufacturers to adopt natural ingredients including carotenoids. Rising production of packaged foods, dairy products, bakery items, and functional beverages requires reliable supplies of beta-carotene and lycopene for coloring and fortification applications. The food processing sector contributes to India’s manufacturing gross value added and has attracted growing foreign direct investment, reflecting robust industry expansion that directly benefits carotenoid suppliers. India’s National Food Security Act and micronutrient fortification programs further stimulate demand by promoting vitamin A enrichment in staple foods distributed through public distribution systems, creating institutional-level consumption channels for provitamin A carotenoids.

Rising Consumer Health Consciousness and Dietary Supplement Demand

India’s expanding middle class and increasing health awareness are fueling unprecedented demand for dietary supplements and nutraceutical products that incorporate carotenoids as active ingredients. Growing prevalence of lifestyle diseases including diabetes, cardiovascular conditions, and vision-related disorders is motivating consumers to adopt preventive healthcare measures through supplementation. Carotenoids such as lutein and zeaxanthin for macular health, astaxanthin for anti-inflammatory benefits, and beta-carotene for immune support are gaining traction among urban consumers. India’s dietary supplements market size was valued at INR 201.46 Billion in 2025 and is projected to reach INR 572.62 Billion by 2034, growing at a compound annual growth rate of 12.31% from 2026-2034, creating expanding demand channels for carotenoid-based formulations. The convergence of rising disposable incomes, urbanization, and digital health awareness campaigns is transforming consumer purchasing behavior, with increasing adoption of daily supplement regimens that incorporate carotenoid ingredients for holistic wellness and preventive nutrition.

Growth of Animal Nutrition and Aquaculture Sectors

India’s animal feed industry represents a significant and growing demand channel for carotenoids, driven by the expansion of commercial poultry, dairy, and aquaculture operations across the country. Carotenoids play essential roles in enhancing egg yolk pigmentation, improving poultry skin coloration, and supporting fish health and fillet appearance in aquaculture systems. The Indian government’s commitment to fisheries development, demonstrated through the Pradhan Mantri Matsya Kisan Samridhi Sah-Yojana sanctioned INR 11.84 Crores for four years from 2023-24 to 2026-27, is driving formalization and modernization of aquaculture practices that incorporate carotenoid supplementation. Rising per capita consumption of poultry, eggs, and seafood in India, coupled with growing export-oriented aquaculture production, is sustaining demand for both synthetic and natural carotenoids in feed formulations. Investments in scientific farming practices, improved feed conversion efficiency, and premium animal product quality standards continue to expand the addressable market for feed-grade carotenoid products across India.

Market Restraints:

What Challenges the India Carotenoids Market is Facing?

High Production Costs of Natural Carotenoids

Natural carotenoid extraction from plant sources and microalgae involves complex cultivation, harvesting, and purification processes that result in significantly higher production costs compared to synthetic alternatives. This cost disparity limits adoption among price-sensitive food manufacturers and small-scale producers in India’s fragmented food processing landscape. The capital-intensive nature of microalgae cultivation infrastructure and specialized extraction equipment creates barriers for new entrants seeking to expand natural carotenoid production capacity.

Stability and Shelf-Life Challenges

Carotenoids are inherently susceptible to degradation from exposure to light, heat, and oxygen, posing formulation and storage challenges particularly relevant to India’s tropical and subtropical climate conditions. Maintaining product potency throughout supply chains that often lack temperature-controlled logistics requires additional investment in advanced encapsulation and packaging technologies. These stability constraints can increase end-product costs and complicate quality assurance for manufacturers targeting mass-market consumer segments.

Limited Consumer Awareness in Rural Markets

Despite growing health consciousness in urban India, awareness of carotenoid-specific health benefits remains limited among rural populations, which constitute a substantial portion of the country’s consumer base. The absence of widespread nutritional literacy regarding the roles of lutein, astaxanthin, and other specialized carotenoids constrains demand expansion beyond metropolitan markets. Educational outreach and consumer communication efforts require significant investment, which can be challenging for manufacturers operating within competitive pricing environments.

Competitive Landscape:

The India carotenoids market is represented by a combination of established global players and niche local producers competing on the basis of quality, price, and new formulation developments. The companies that have in-house processing capabilities ranging from chemical synthesis to fermentation-based production and advanced formulation development continue to enjoy a competitive edge in terms of economies of scale and reliability of supply. The market is marked by steady investments in R&D, with a focus on enhancing the bioavailability of carotenoids, new formulation developments for specific applications, and diversification of product lines to meet the growing requirements of the food, dietary supplement, animal feed, and cosmetic industries.

India Carotenoids Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Beta-Carotene, Astaxanthin, Lutein, Lycopene, Zeaxanthin, Canthaxanthin, Others |

|

Sources Covered |

Synthetic, Natural |

|

Formulations Covered |

Oil Suspension, Powder, Emulsion, Others |

|

Applications Covered |

Animal Feed, Dietary Supplements, Food and Beverages, Cosmetics, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Carotenoids Market Report

The India carotenoids market size was valued at USD 202.65 Million in 2025.

The India carotenoids market is expected to grow at a compound annual growth rate of 5.92% from 2026-2034 to reach USD 345.3 Million by 2034.

Beta-carotene dominated the market with a share of 31.8%, driven by its widespread adoption as a provitamin A source in food fortification, dietary supplements, and animal feed applications across India.

Key factors driving the India carotenoids market include expanding food processing activities, rising dietary supplement consumption, growing animal nutrition demand, regulatory support for natural food additives, and increasing consumer health awareness.

Major challenges include high production costs of natural carotenoids, stability and shelf-life constraints in tropical climates, limited consumer awareness in rural markets, price sensitivity among small-scale manufacturers, and complex regulatory compliance requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade