India Caustic Potash Market Size, Share, Trends and Forecast by Form, Grade, End Use, and Region, 2026-2034

India Caustic Potash Market Summary:

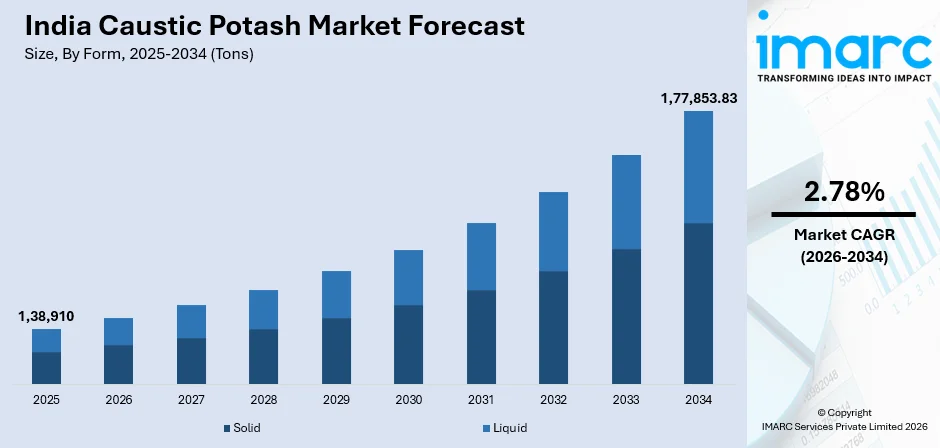

The India caustic potash market size reached 1,38,910 Tons in 2025 and is projected to reach 1,77,853.83 Tons by 2034, growing at a compound annual growth rate of 2.78% from 2026-2034.

The market is experiencing steady growth driven by expanding applications in agriculture and chemical manufacturing. Rising demand for potassium-based fertilizers to enhance crop yields and increasing industrial use in soap, glass and textile production are key growth factors. Supply chain optimization and investments in local production capacity are improving market stability. However, price volatility in feedstock and regulatory shifts may influence future market dynamics.

Key Takeaways and Insights:

- By Form: Solid dominates the market with a share of 60% in 2025, driven by its versatile applications across agriculture, pharmaceutical, and food processing industries.

- By Grade: Industrial leads the market with a share of 55% in 2025, owing to its widespread use in chemical synthesis, soap manufacturing, and water treatment processes.

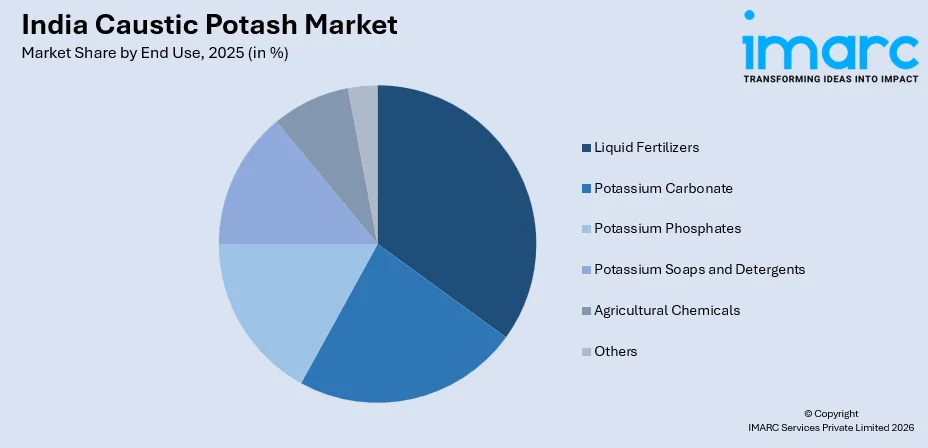

- By End Use: Liquid fertilizers represent the largest segment with a market share of 26% in 2025, supported by India’s expanding micro-irrigation infrastructure and growing emphasis on balanced crop nutrition.

- Key Players: The India caustic potash market features a moderately concentrated competitive landscape, with leading domestic manufacturers investing in capacity expansions and downstream integration to strengthen market positioning, improve cost efficiency, and secure long term demand from fertilizer and industrial end use segments.

To get more information on this market Request Sample

The India caustic potash market plays a strategic role within the country’s broader chlor alkali and specialty chemicals ecosystem, supported strongly by fertilizer demand. Its significance is reinforced by the scale of the Indian fertilizer market, which was valued at INR 1,021 billion in 2025 and is projected to reach INR 1,433.6 billion by 2034, highlighting sustained nutrient consumption growth. Caustic potash is extensively used in producing potassium-based fertilizers that enhance soil quality and crop productivity. Beyond agriculture, the market benefits from steady demand across soaps and detergents, pharmaceuticals, agrochemicals, food processing, and select industrial applications requiring high purity alkaline inputs. Domestic manufacturers are focusing on capacity optimization, process efficiency, and cost control to manage input price fluctuations and energy intensity. Import dependence for raw materials and exposure to global pricing cycles continue to influence overall market dynamics.

India Caustic Potash Market Trends:

Expanding Industrial Application Base

Industrial diversification is positively influencing caustic potash consumption beyond traditional fertilizer use. This trend is reinforced by the expanding agrochemicals sector, with the India agrochemicals market valued at USD 15.5 Billion in 2024 and projected to reach USD 23.3 Billion by 2033, supporting sustained demand growth. Rising activity across pharmaceuticals, food processing, agrochemicals, and specialty chemicals is broadening application requirements. Manufacturers rely on caustic potash for dependable pH control, synthesis efficiency, and formulation stability. As downstream industries expand capacity and enhance quality standards, the need for consistent, high purity alkaline inputs continues to strengthen.

Focus on Operational Efficiency Improvements

Capacity optimization and operational efficiency improvements are emerging as a positive trend in the India caustic potash market. Producers are focusing on process control, energy management, and yield optimization to improve cost competitiveness. These measures help mitigate input price volatility and enhance supply reliability for downstream buyers. Improved logistics planning and inventory discipline further support consistent market availability. As efficiency driven strategies mature, manufacturers can protect margins while maintaining stable pricing, strengthening overall market confidence and long-term industry sustainability under evolving regulatory and sustainability expectations across India over time.

Strengthening Agricultural Demand Fundamentals

Rising agricultural intensity is strengthening demand for caustic potash across India. Indian fertiliser companies plan to sign a joint venture with Uralchem to establish a Russia based urea plant, strengthening long term fertiliser and potash security. The deal, expected during Vladimir Putin’s India visit, aims to reduce import risks, nationwide supply. Increasing focus on crop yield optimization, soil nutrient balancing, and horticulture expansion is driving consistent consumption of potassium-based inputs. Farmers are gradually adopting higher value fertilizers to improve productivity and resilience against climatic variability. This shift supports stable offtake from fertilizer manufacturers and encourages long term procurement planning. As agricultural practices become more input efficient and commercially oriented, caustic potash demand benefits from predictable seasonal cycles and structurally improving end user awareness across domestic agricultural value chains nationwide.

Market Outlook 2026-2034:

The India caustic potash market outlook remains stable, supported by steady agricultural demand and gradual expansion across industrial end use sectors. Consumption is expected to follow predictable seasonal patterns linked to crop cycles, while industrial offtake provides baseline stability. Producers are likely to prioritize cost control and supply reliability amid input volatility. Overall, market growth is anticipated to be moderate, with demand resilience outweighing near term operational and regulatory challenges. The market size reached 1,38,910 Tons in 2025 and is projected to reach 1,77,853.83 Tons by 2034, growing at a compound annual growth rate of 2.78% from 2026-2034.

India Caustic Potash Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Form |

Solid |

60% |

|

Grade |

Industrial |

55% |

|

End Use |

Liquid Fertilizers |

26% |

Form Insights:

- Solid

- Liquid

The solid dominates with a market share of 60% of the total India caustic potash market in 2025.

The solid form represents the largest segment in the India caustic potash market due to its superior handling, storage stability, and suitability for bulk transportation. Solid caustic potash is preferred by fertilizer manufacturers and industrial users as it offers longer shelf life and lower risk of spillage or leakage compared to liquid variants. Its compatibility with large scale manufacturing operations supports consistent dosing and controlled application across diverse end use industries.

Demand for solid caustic potash is further supported by its widespread use in agrochemicals, pharmaceuticals, and specialty chemical formulations requiring precise alkalinity control. End users favor solid grades for ease of inventory management and flexibility in downstream processing. Additionally, solid caustic potash enables cost efficient procurement and logistics planning, particularly for users operating in inland or multi location facilities, reinforcing its dominant position within the domestic market structure.

Grade Insights:

- Industrial

- Reagent

- Pharma

The industrial leads with a share of 55% of the total India caustic potash market in 2025.

The industrial segment leads the India caustic potash market, driven by its critical role across a wide range of chemical and manufacturing applications. Caustic potash is extensively used across pharmaceuticals, agrochemicals, food processing, soaps and detergents, and specialty chemical production, where consistent alkalinity and process reliability are essential. This demand is reinforced by the scale of the India pharmaceutical market, valued at USD 68.38 Billion in 2025 and projected to reach USD 174.67 Billion by 2034, supporting sustained industrial consumption. Stable industrial demand provides year-round offtake, reducing seasonality compared to agriculture led applications and ensuring steady volume utilization across manufacturing cycles.

Growth in domestic manufacturing and capacity expansion across downstream industries continues to reinforce the dominance of the industrial segment. Producers value caustic potash for applications such as pH regulation, synthesis reactions, and formulation stability. As industrial users focus on quality compliance and process efficiency, demand for high purity caustic potash remains strong, positioning the industrial segment as the primary contributor to overall market consumption.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Potassium Carbonate

- Potassium Phosphates

- Potassium Soaps and Detergents

- Liquid Fertilizers

- Agricultural Chemicals

- Others

The liquid fertilizers exhibit a clear dominance with a 26% share of the total India caustic potash market in 2025.

Liquid fertilizers exhibit clear dominance in the India caustic potash market due to their ease of application, faster nutrient absorption, and compatibility with modern farming practices. Liquid formulations enable uniform nutrient distribution through fertigation and foliar application, improving potassium uptake efficiency. Farmers increasingly prefer liquid fertilizers for high-value crops, horticulture, and precision agriculture systems, supporting consistent demand for liquid caustic potash-based inputs across key agricultural regions.

The dominance of liquid fertilizers is further reinforced by the rapid adoption of drip irrigation and controlled nutrient delivery systems. This trend aligns with the growth of the India drip irrigation market, which reached USD 284.13 million in 2024 and is projected by IMARC Group to reach USD 662.30 million by 2033. Such systems require highly soluble potassium sources, positioning liquid caustic potash formulations as a practical solution. Improved storage and handling infrastructure, along with lower application losses, enhances cost effectiveness for farmers, strengthening the segment’s leadership within the overall India caustic potash market structure.

Regional Insights:

- North India

- West and Central India

- South India

- East India

Demand in North India is supported by intensive agriculture and diversified cropping patterns. Potassium based inputs are used to improve yield quality in cereals, fruits, and vegetables. Strong fertilizer distribution networks and seasonal procurement cycles sustain steady caustic potash consumption, while expanding agro processing activity adds incremental industrial demand across key northern states.

West and Central India benefit from a strong industrial base and well-developed chemical manufacturing clusters. Caustic potash consumption is supported by agrochemicals, pharmaceuticals, and specialty chemicals, alongside fertilizer usage. Proximity to ports and large manufacturing hubs improves supply efficiency, supporting stable offtake and encouraging long term sourcing arrangements.

South India shows consistent demand driven by horticulture, plantation crops, and food processing industries. Liquid fertilizer adoption and precision farming practices support potassium based nutrient usage. Industrial consumption from pharmaceuticals and specialty chemicals adds demand stability. Favorable infrastructure and organized agriculture contribute to predictable caustic potash consumption patterns across the region.

East India is witnessing gradual growth in caustic potash demand supported by expanding agricultural activity and improving input penetration. Increased focus on crop productivity, soil health, and fertilizer access is strengthening consumption. Developing industrial activity and logistics improvements are further supporting steady market expansion across eastern states.

Market Dynamics:

Growth Drivers:

Why is the India Caustic Potash Market Growing?

Policy Support for Potash Usage

Supportive government policies aimed at improving nutrient balance in Indian agriculture are a key growth driver for the India caustic potash market. The Government of India is promoting balanced fertilization through soil testing, nutrient based subsidies, customised and nano fertilizers, and regenerative agriculture practices, improving nutrient efficiency, reducing losses, and supporting long term soil health and sustainable agricultural productivity nationwide. Programs promoting balanced fertilization, soil health management, and improved nutrient efficiency are indirectly increasing potash consumption. Inclusion of potassium focused inputs in agronomic advisory frameworks is strengthening long term demand visibility.

Rising Food Security Requirements

India’s growing population and rising food consumption requirements are driving sustained demand for higher agricultural output. India’s population reached 1,420.6 million in March 2026, up from 1,408.0 million in March 2025, marking a record high. To meet food security goals, farmers are increasingly required to improve yield quality and consistency, which supports the use of potassium-based inputs. Caustic potash benefits from this structural need to enhance crop resilience and productivity. As food supply pressures intensify, fertilizer consumption becomes less discretionary, positioning caustic potash as a critical input supporting long term agricultural output growth nationwide.

Increasing Contract and Commercial Farming

The expansion of contract farming and commercial crop cultivation is emerging as a distinct growth driver for the India caustic potash market. India’s agri and processed food exports rose 7.1% YoY to INR 51,071 Crore in Q1 FY26, supported by 110.5 Million hectares Kharif sowing, strong rice exports, and rising FDI inflows. Organized farming models prioritize yield optimization, input precision, and consistent output quality, leading to structured fertilizer usage patterns. These operations rely on scientifically balanced nutrient programs, supporting steady potash demand. As agribusiness participation increases and farming becomes more commercially driven, caustic potash demand benefits from planned procurement cycles and predictable consumption volumes across regions

Market Restraints:

What Challenges the India Caustic Potash Market is Facing?

High Energy and Production Costs

High energy and production costs constrain the India caustic potash market significantly. Manufacturing processes are energy intensive, making producers vulnerable to electricity and fuel price fluctuations. Rising operating expenses pressure margins and limit pricing flexibility. Smaller manufacturers struggle to absorb cost shocks, leading to capacity underutilization and cautious expansion decisions across the domestic industry over near to medium term outlook.

Dependence on Imported Raw Materials

Dependence on imported raw materials remains a key restraint for the India caustic potash market. Exposure to global supply conditions, currency movements, and international pricing cycles increases cost uncertainty. Import reliance also heightens logistics risks and lead time variability. These factors complicate procurement planning for manufacturers and restrict consistent pricing strategies across domestic end use sectors over longer planning horizons.

Regulatory and Environmental Compliance Pressure

Environmental compliance and safety regulations act as a restraint on market expansion. Handling, storage, and disposal requirements for caustic potash increase compliance costs and operational complexity. Stricter monitoring standards require continuous investment in safety systems and training. For some producers, regulatory burden slows capacity additions and delays project execution timelines across multiple manufacturing locations, affecting competitiveness and investment appetite nationally.

Competitive Landscape:

The competitive landscape of the India caustic potash market is moderately consolidated, with a mix of established domestic chemical producers and regional suppliers competing on cost efficiency and supply reliability. Larger players benefit from integrated operations, long term customer relationships, and stronger distribution networks. Smaller manufacturers compete through regional proximity and flexible supply arrangements. Competition is primarily driven by pricing discipline, consistent product quality, and the ability to manage raw material volatility, rather than aggressive capacity expansion or differentiation.

Recent Developments:

- In February 2026, Gujarat Alkalies and Chemicals Limited approved over INR 1,000 Crore capex to install biofuel and coal fired boilers, set up a 33,870 TPA phosphoric acid facility at Dahej, and expand caustic potash capacity at Vadodara to reduce costs and boost revenues.

India Caustic Potash Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | ‘000 Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Forms Covered | Solid, Liquid |

| Grades Covered | Industrial, Reagent, Pharma |

| End Uses Covered | Potassium Carbonate, Potassium Phosphates, Potassium Soaps and Detergents, Liquid Fertilizers, Agricultural Chemicals, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Caustic Potash Market Research Report and Industry Forecast Report

The India caustic potash market size reached 1,38,910 Tons in 2025.

The India caustic potash market is expected to grow at a compound annual growth rate of 2.78% from 2026-2034 to reach 1,77,853.83 Tons by 2034.

Liquid fertilizers, holding the largest end-use share at 26%, lead the India caustic potash market, driven by expanding micro-irrigation infrastructure, government emphasis on balanced nutrient management, and growing adoption of water-soluble potassium fertilizer formulations.

Key factors driving the India caustic potash market include government agricultural subsidies promoting potassium-based fertilizers, domestic capacity expansions by leading manufacturers, rising demand from soap and personal care industries, and expanding pharmaceutical and food processing applications.

Major challenges include high import dependency exposing the market to global price volatility, elevated energy costs in chlor-alkali production, competitive pricing pressure from cheaper sodium hydroxide substitutes, and supply chain vulnerabilities linked to geopolitical uncertainties.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)