India CCTV Market Size, Share, Trends and Forecast by Type, End User Vertical, and Region, 2026-2034

India CCTV Market Summary:

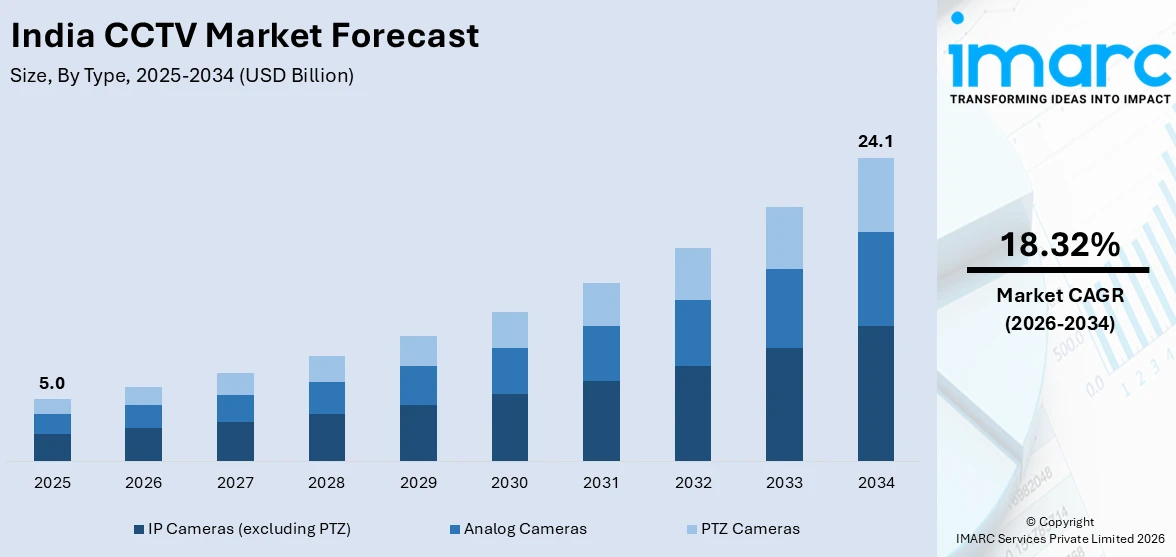

The India CCTV market size was valued at USD 5.0 Billion in 2025 and is projected to reach USD 24.1 Billion by 2034, growing at a compound annual growth rate of 18.32% from 2026-2034.

The India CCTV market is witnessing robust expansion, fueled by escalating public safety concerns, rapid urbanization, and the government's ambitious smart city and safe city initiatives. Growing demand across the government, industrial, and commercial sectors is increasingly driving adoption of advanced surveillance solutions. Favorable regulatory frameworks and the integration of artificial intelligence (AI) into surveillance systems are further enhancing the market share.

Key Takeaways and Insights:

- By Type: IP cameras (excluding PTZ) dominate the market with a share of 58.4% in 2025, owing to their superior image resolution, scalability, and compatibility with AI-driven video analytics platforms. The accelerating shift from analog to digital network infrastructure is reinforcing adoption across government and enterprise deployments.

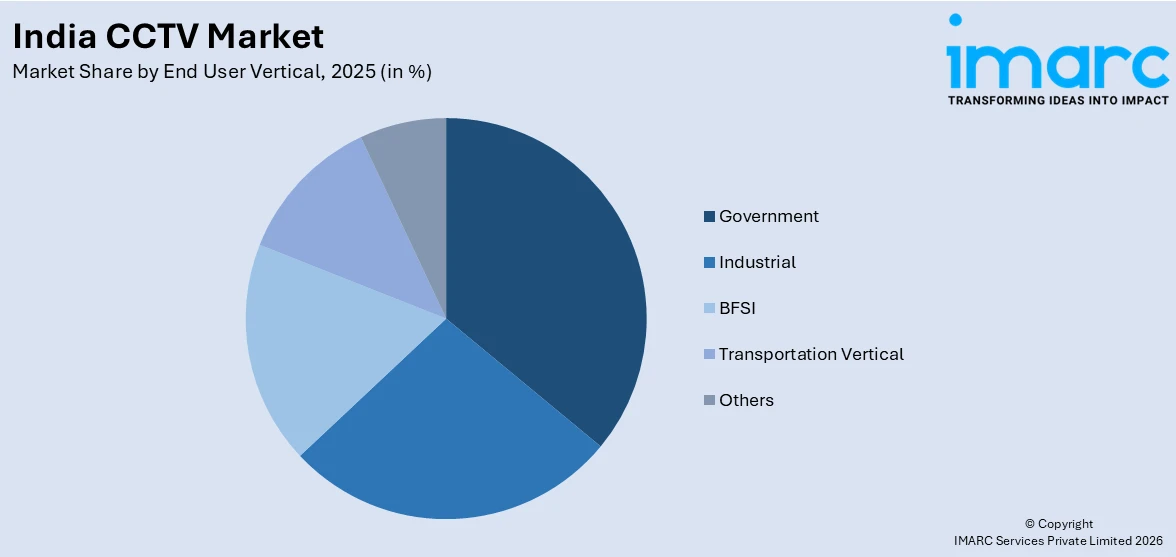

- By End User Vertical: Government leads the market with a share of 35.2% in 2025. This dominance is driven by large-scale public safety deployments, smart city surveillance mandates, and safe city project investments across major metropolitan regions nationwide.

- By Region: North India comprises the largest region with 32.6% share in 2025, driven by extensive surveillance deployments across Delhi-NCR, Uttar Pradesh, and Haryana, including flagship safe city programs and AI-enabled traffic monitoring systems in key urban centers.

- Key Players: Key players drive the India CCTV market by advancing AI-based video analytics, expanding domestic manufacturing capacities under Make in India guidelines, and strengthening relationships with government agencies and system integrators. Their investments in cybersecurity compliance, edge computing capabilities, and next-generation camera technologies ensure comprehensive surveillance solutions across diverse verticals.

To get more information on this market Request Sample

The India CCTV market is undergoing a significant transformation, driven by the convergence of technological innovation, regulatory reform, and growing public sector investment in surveillance infrastructure. The proliferation of IP-based cameras has displaced legacy analog systems, as end users increasingly demand scalable platforms capable of integrating with command-and-control centers and advanced analytics software. Government-led initiatives, such as the Smart Cities Mission and Safe City Projects, have catalyzed the installation of sophisticated surveillance networks across urban centers. According to the World Bank Group, by 2036, India’s cities and towns will house 600 Million individuals, which is 40% of the population, underscoring the urgency of expanding surveillance infrastructure. From industrial facilities and transportation hubs to banking institutions and residential complexes, demand for connected, AI-ready CCTV systems is intensifying across all end user verticals.

India CCTV Market Trends:

Integration of AI in Surveillance Systems

The India CCTV market is witnessing a rapid shift towards AI-enhanced surveillance, as governments, enterprises, and law enforcement agencies increasingly adopt cameras capable of facial recognition, behavioral analysis, and real-time anomaly detection. These intelligent systems extend surveillance beyond passive recording, enabling predictive security responses, automated traffic enforcement, and dynamic crowd management in high-density public areas. During the Maha Kumbh Mela 2025 in Prayagraj, 2,700 AI-enabled cameras monitored over 400 Million visitors, illustrating the growing effectiveness of smart surveillance at scale.

Adoption of Cloud-Based and IP-Networked Surveillance Platforms

India's surveillance landscape is experiencing a decisive migration from analog to IP-networked and cloud-integrated platforms, driven by the cost-efficiency, scalability, and remote management advantages these architectures offer. Enterprises and government agencies are increasingly deploying IP cameras with embedded analytics that allow on-device processing, minimizing bandwidth consumption while enabling real-time incident response. Cloud-based video management platforms are gaining traction among mid-market buyers seeking subscription-based pricing and managed firmware updates.

Make in India Policy Accelerating Domestic Surveillance Manufacturing

India's regulatory environment is catalyzing a structural shift towards domestically produced surveillance equipment, with the government's Make in India initiative significantly altering the competitive landscape. Manufacturers are establishing local production facilities, investing in firmware design and hardware engineering capabilities, and pursuing Bureau of Indian Standards certifications to qualify for government procurement programs. This policy-driven manufacturing surge is reducing dependence on imported surveillance components and creating a new generation of cybersecurity-compliant, India-designed cameras.

Market Outlook 2026-2034:

The India CCTV market is poised for sustained and robust expansion throughout the forecast period, underpinned by widespread government deployment programs, accelerating digitalization of security infrastructure, and growing private sector investment in intelligent surveillance solutions. The rapid proliferation of AI-enabled cameras, deepening penetration of IP-based platforms in tier-2 and tier-3 cities, and ongoing implementation of Smart Cities Mission surveillance networks are expected to sustain momentum across all end user verticals. The market generated a revenue of USD 5.0 Billion in 2025 and is projected to reach a revenue of USD 24.1 Billion by 2034, growing at a compound annual growth rate of 18.32% from 2026-2034. Rising urbanization, infrastructure investments in transportation and airports, and heightened border security requirements will further support demand.

India CCTV Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

IP Cameras (excluding PTZ) |

58.4% |

|

End User Vertical |

Government |

35.2% |

|

Region |

North India |

32.6% |

Type Insights:

- Analog Cameras

- IP Cameras (excluding PTZ)

- PTZ Cameras

IP cameras (excluding PTZ) dominate the market with a market share of 58.4% of the total India CCTV market in 2025.

IP cameras (excluding PTZ) have taken the lead in the India CCTV industry, due to their strong compatibility with AI-driven video analytics platforms, excellent image resolution, and remote accessibility. IP cameras can be seamlessly integrated with cloud storage, edge computing modules, and centralized command-and-control systems since they transmit data over conventional network infrastructure, unlike their analog counterparts. They are especially appealing for large-scale government and corporate deployments due to their scalability.

Growing use cases in government, transportation, and industrial sectors that require high-resolution, adjustable surveillance over large regions are driving IP camera adoption. IP cameras are the go-to option for forward-thinking security deployments because of sophisticated capabilities like Power-over-Ethernet connectivity, night vision with infrared imaging, and embedded GPU processors for on-device object detection. As certified IP camera models from conforming manufacturers are gradually replacing imported alternatives, the government's drive for domestically produced surveillance equipment has expedited the changeover. They are positioned as the cornerstone of India's developing surveillance ecosystem due to their capacity to provide actionable, data-rich security intelligence.

End User Vertical Insights:

Access the comprehensive market breakdown Request Sample

- Government

- Industrial

- BFSI

- Transportation Vertical

- Others

Government leads with a share of 35.2% of the total India CCTV market in 2025.

The government segment maintains a dominant position in the India CCTV market, underpinned by sustained national and state-level investment in public safety infrastructure, border security, and smart city surveillance mandates. Major procurement programs, including the Safe City Project, the Smart Cities Mission, and the Nirbhaya Fund-backed security initiatives, have collectively driven large-scale camera deployments across police stations, public transport hubs, and urban intersections. Delhi alone had more than 2.4 Lakh CCTV cameras installed by the government by December 2023, exemplifying the scale of public sector commitment to comprehensive urban surveillance.

The government vertical's dominance also extends to critical infrastructure protection, with surveillance systems deployed at airports, railway networks, border checkpoints, and government buildings. The increasing integration of AI-powered facial recognition within government-managed surveillance networks is enhancing law enforcement capabilities, enabling faster identification of suspects and monitoring of high-risk individuals. In North India, AI-enabled cameras deployed under the Delhi Safe City Project have proven instrumental in solving criminal cases and enabling real-time threat monitoring.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents the leading segment with a 32.6% share of the total India CCTV market in 2025.

North India commands the largest share of the India CCTV market, driven by the concentration of major metropolitan areas, including Delhi-NCR, Lucknow, Chandigarh, and Jaipur, where government-led surveillance investments have been most intensive. The region has been at the forefront of smart city and safe city surveillance deployments, with extensive camera networks integrated into command-and-control infrastructure for traffic management, crime prevention, and public safety. As part of the Smart Cities Mission, Uttar Pradesh announced in January 2024 the installation of a network of 100,000 CCTV cameras, highlighting the region's commanding scale of deployment.

Beyond government deployments, North India's market is fueled by the region's dense industrial corridors, major transportation infrastructure, including airports, metro systems, and interstate highways, and a rapidly growing commercial real estate sector. Cities, such as Chandigarh, Noida, and Gurugram, have implemented sophisticated AI-enabled traffic enforcement and perimeter security systems, creating strong demand for advanced IP cameras and video analytics software. The proliferation of e-commerce fulfillment centers, logistics parks, and data centers across NCR further intensifies the requirement for robust, scalable surveillance solutions integrated with smart access control systems.

Market Dynamics:

Growth Drivers:

Why is the India CCTV Market Growing?

Government-Led Smart City and Safe City Surveillance Programs

The Indian government's concerted push to modernize urban safety infrastructure through Smart City and Safe City programs represents one of the most powerful catalysts for CCTV market growth. Under the Smart Cities Mission, authorities have prioritized the installation of integrated surveillance networks that seamlessly connect cameras with centralized command-and-control centers capable of managing traffic, public order, and emergency response in real time. These systems go beyond traditional reactive monitoring to enable predictive city management, where analytics engines identify patterns and alert law enforcement proactively. Border security requirements along India's extensive land and maritime boundaries have also driven large-scale surveillance deployments, with modern IP cameras and thermal imaging systems providing round-the-clock monitoring of sensitive perimeters. Additionally, state governments across Uttar Pradesh, Punjab, Haryana, and Maharashtra have independently launched public surveillance expansion projects that complement national programs, broadening the geographic and sectoral footprint of government-driven CCTV adoption.

Rapid Urbanization and Rising Public Safety Concerns

India's accelerating pace of urbanization is fundamentally reshaping the demand landscape for CCTV systems, as expanding urban populations create intensifying pressure on public safety infrastructure. As cities grow in size and density, the incidence of property crime, traffic violations, and unauthorized access in commercial and residential spaces increases, prompting local governments and private entities to invest proactively in deterrent and investigative surveillance tools. The forecasts for 2025 suggested around 227,120 property crimes happening across the country, marking a 2% rise from the 222,666 incidents recorded in 2023. Urban development programs have led to the construction of thousands of kilometers of smart roads equipped with embedded surveillance and traffic management infrastructure, generating recurring demand for network-connected cameras. The expansion of metro rail networks, national highway corridors, and international airport facilities across the country has similarly catalyzed large-scale CCTV deployments, as operators and government agencies require robust surveillance coverage of critical transportation infrastructure. Residential real estate developers are increasingly incorporating CCTV systems as standard features in gated communities, apartment complexes, and integrated townships, driven by buyer demand for enhanced security amenities.

Technological Advancements in AI, Internet of Things (IoT), and Cybersecurity Standards

The convergence of AI, the IoT, and advanced cybersecurity standards is fundamentally expanding the functional capabilities and commercial appeal of CCTV systems across India. As per IMARC Group, the India IoT market size was valued at USD 1.50 Billion in 2025. AI-powered video analytics platforms enable cameras to perform sophisticated functions beyond passive recording, including real-time facial recognition, behavioral anomaly detection, crowd density estimation, and license plate recognition, making surveillance systems increasingly valuable across law enforcement, retail analytics, and industrial safety applications. The integration of IoT connectivity allows cameras to function as intelligent nodes within broader smart city ecosystems, sharing data with traffic management systems, emergency response platforms, and utility monitoring networks in real time. Edge computing advancements have further enhanced the utility of IP cameras by enabling on-device data processing, significantly reducing bandwidth requirements and response latency for time-sensitive security applications.

Market Restraints:

What Challenges the India CCTV Market is Facing?

High Initial Installation and Infrastructure Costs

The deployment of comprehensive CCTV surveillance systems, particularly those incorporating AI analytics, cloud connectivity, and high-resolution IP cameras, requires substantial upfront investment in hardware, network infrastructure, and installation services. For smaller municipalities, tier-2 cities, and private sector organizations operating under constrained capital budgets, these costs represent a significant barrier to adoption. The recurring expenses associated with annual maintenance contracts, firmware updates, and cybersecurity compliance assessments further compound the total cost of ownership, discouraging adoption among cost-sensitive buyers and limiting the pace of market penetration in underserved regions.

Privacy Concerns and Regulatory Compliance Challenges

The widespread deployment of CCTV systems, particularly those enabled with facial recognition and behavioral analytics capabilities, has generated growing public concern over surveillance overreach, data privacy, and civil liberties. India's Digital Personal Data Protection Act introduces new compliance obligations for CCTV operators regarding the collection, storage, and use of video footage, increasing legal and operational complexity for both government agencies and private sector entities. Non-compliance with data protection regulations risks significant reputational and legal consequences, creating uncertainty and slowing adoption among privacy-sensitive buyers across regulated industries.

Supply Chain Disruption and Cybersecurity Certification Bottlenecks

India's stringent STQC cybersecurity certification mandate, while essential for ensuring the security of the national surveillance infrastructure, has created significant supply chain disruption and market uncertainty. The limited number of accredited testing laboratories capable of processing certification applications has resulted in a bottleneck that constrains the availability of certified CCTV products, particularly affecting smaller manufacturers and foreign brands. Import dependencies on overseas components for critical camera hardware further expose the market to geopolitical disruptions, tariff changes, and supply chain vulnerabilities that can delay project timelines and increase procurement costs.

Competitive Landscape:

The India CCTV market is characterized by moderate to high competitive intensity, with a mix of domestic manufacturers and global brands competing across various price segments and technology tiers. International brands are accelerating their localization strategies to retain market access under the Make in India policy framework. Competition is increasingly centered on AI integration, cybersecurity compliance, product certifications, and the breadth of after-sales service networks. Additionally, pricing strategies, channel partnerships, and government procurement opportunities play a crucial role in shaping competitive positioning. Vendors are also investing in cloud-based surveillance solutions and smart city projects to capture emerging demand across urban infrastructure and enterprise security applications.

Recent Developments:

- In June 2025, Honeywell launched its first-ever locally designed and manufactured CCTV camera portfolio in India, the 50 Series, developed at its global development center in Bengaluru in collaboration with VVDN Technologies. The cameras achieved Class 1 certification under the Make in India policy and were designed to meet India's growing demand for intelligent, high-quality, and cybersecurity-compliant surveillance systems.

India CCTV Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Analog Cameras, IP Cameras (excluding PTZ), PTZ Cameras |

| End User Verticals Covered | Government, Industrial, BFSI, Transportation Vertical, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India CCTV Market Report

The India CCTV market size was valued at USD 5.0 Billion in 2025.

The India CCTV market is expected to grow at a compound annual growth rate of 18.32% from 2026-2034 to reach USD 24.1 Billion by 2034.

IP cameras (excluding PTZ) dominated the market with a share of 58.4%, owing to their superior image quality, network scalability, and compatibility with AI-driven video analytics platforms across diverse end-user verticals.

Key factors driving the India CCTV market include government smart city and safe city programs, rising urbanization and public safety concerns, growing integration of AI in surveillance systems, and favorable regulatory frameworks promoting domestic manufacturing.

Major challenges include high upfront installation costs, privacy and data protection compliance requirements under the Digital Personal Data Protection Act, supply chain disruptions caused by STQC certification bottlenecks, and cybersecurity vulnerabilities in legacy surveillance equipment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)