India CDMO Market Size, Share, Trends and Forecast by Service Type, Product Type, Scale of Operation, Therapeutic Area, and Region, 2026-2034

India CDMO Market Summary:

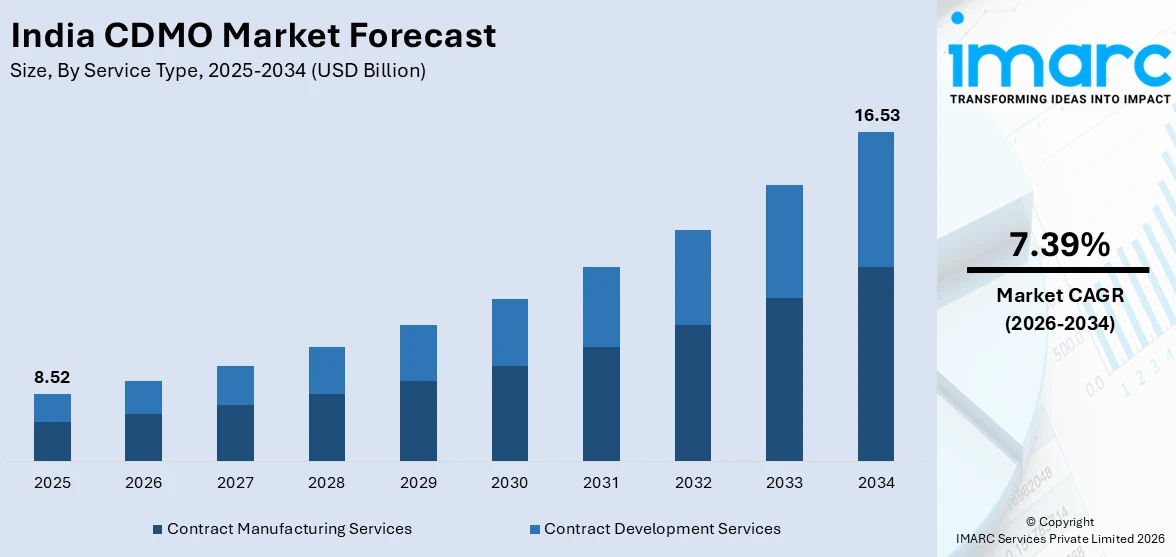

The India CDMO market size was valued at USD 8.52 Billion in 2025 and is projected to reach USD 16.53 Billion by 2034, growing at a compound annual growth rate of 7.39% from 2026-2034.

India's CDMO market is experiencing robust expansion driven by increasing pharmaceutical outsourcing, a well-established generics manufacturing base, and growing global demand for cost-effective drug development solutions. Rising investments in biopharmaceutical capabilities, a skilled scientific workforce, and strong regulatory alignment with international standards are propelling market growth. These factors collectively position India as a premier destination for end-to-end pharmaceutical contract services, augmenting the India CDMO market share.

Key Takeaways and Insights:

- By Service Type: Contract manufacturing services dominate the market with a share of 53.8% in 2025, owing to its strong demand for active pharmaceutical ingredient production, finished dosage form manufacturing, and biologics outsourcing. Rising cost-efficiency imperatives and global capacity expansion initiatives are fueling the continued dominance.

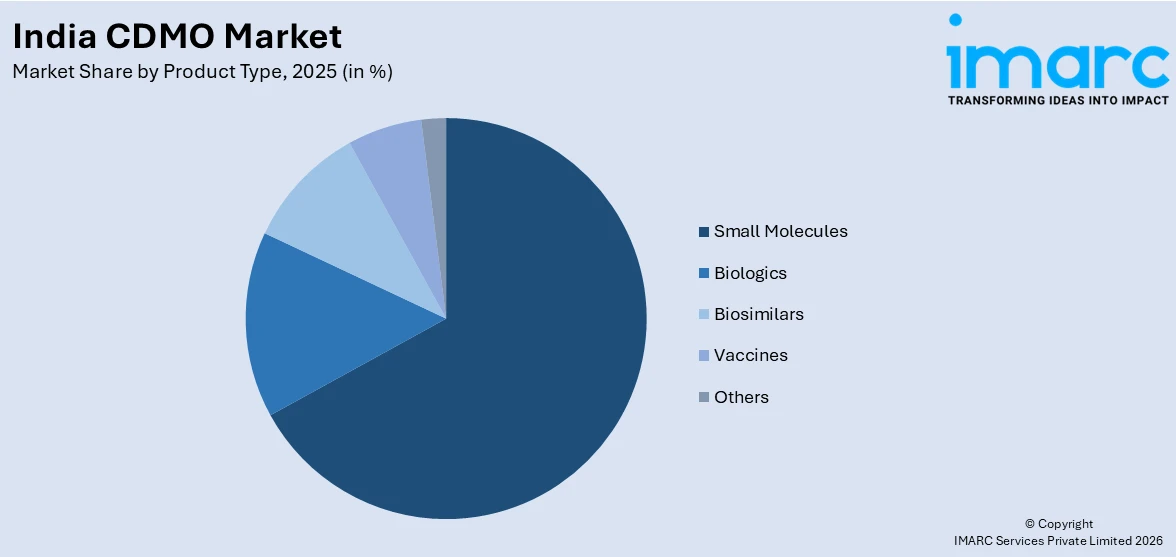

- By Product Type: Small molecules exhibit a clear dominance in the market with 67.2% share in 2025, reflecting the robust foundation in generics and complex molecule synthesis, supported by cost-competitive manufacturing capabilities and broad therapeutic area coverage across the CDMO landscape.

- By Scale of Operation: Commercial scale represents the leading segment with a 70.2% share in 2025, driven by the high-volume production requirements for generic drugs, APIs, and formulations serving pharmaceutical companies across international markets in North America, Europe, and beyond.

- By Therapeutic Area: Oncology dominates the market with a share of 33.2% in 2025, owing to the escalating global cancer burden, rising demand for complex oncology biologics and targeted therapies, and Indian CDMOs' advanced manufacturing capabilities in cytotoxic and immunotherapy compounds.

- By Region: West India holds the largest region with 29.8% share in 2025, driven by the concentration of pharmaceutical manufacturing clusters in Maharashtra and Gujarat, robust industrial infrastructure, and proximity to major export logistics corridors serving international markets.

- Key Players: Key players drive the India CDMO market through capacity expansions, strategic acquisitions, and end-to-end service integration. Their investments in advanced biomanufacturing, regulatory compliance, and global partnerships strengthen competitive positioning and accelerate sustainable market growth.

To get more information on this market Request Sample

The India CDMO market is undergoing a significant transformation driven by increasing pharmaceutical outsourcing, evolving global supply chain strategies, and rising investments in advanced manufacturing technologies. Government initiatives, including the Production-Linked Incentive (PLI) scheme for pharmaceuticals and active pharmaceutical ingredients, are actively encouraging domestic capacity expansion and attracting substantial foreign direct investment into India's life sciences manufacturing sector. India's approximately 650 USFDA-approved manufacturing facilities, representing a quarter of all such plants outside the United States, underscore its regulatory credibility and adherence to stringent international quality standards. Rising demand from North American and European markets, combined with geopolitical supply chain diversification trends, is driving pharmaceutical companies to increasingly partner with Indian CDMOs for comprehensive drug development and commercial-scale manufacturing solutions.

India CDMO Market Trends:

Rising Demand for Biologics and Biosimilars Manufacturing

The India CDMO market is witnessing strong momentum from the growing global demand for biologics and biosimilars. As biologic drugs face patent expirations, pharmaceutical companies are increasingly seeking cost-effective biosimilar production partners, and Indian CDMOs are well-positioned to capitalize on this shift. Investments in mammalian and microbial expression systems, single-use bioreactors, and bioprocess optimization are elevating India's biopharmaceutical manufacturing standards. The push toward affordable biologics is forging strategic partnerships between global innovators and Indian manufacturers, reinforcing the country's emerging role as a key biologics outsourcing hub and driving sustained market expansion through the forecast period.

Adoption of End-to-End Outsourcing Models

Global pharmaceutical companies are transitioning toward comprehensive outsourcing strategies, partnering with CDMOs capable of managing the full product lifecycle, from drug discovery and formulation development through clinical trials to commercial manufacturing. This trend is reshaping market dynamics in India, where leading CDMOs are expanding service portfolios to include high-potency API production, complex generics, sterile injectables, and regulatory support. The shift toward integrated outsourcing reduces time-to-market, enhances supply chain efficiency, and lowers development costs, making Indian CDMOs increasingly attractive to both multinational and emerging pharmaceutical companies seeking streamlined, scalable development partnerships.

Digital Transformation and AI Integration in Manufacturing

Digital technologies are transforming pharmaceutical contract manufacturing operations across India. CDMOs are increasingly deploying artificial intelligence-driven drug discovery platforms, predictive analytics, real-time IoT monitoring, and blockchain-enabled supply chain traceability to improve production efficiency and regulatory compliance. Automated quality control systems and process analytical technologies are reducing manufacturing variability and accelerating batch release timelines. These digital capabilities are enabling CDMOs to offer faster, more reliable services aligned with the evolving expectations of global pharmaceutical clients. The integration of smart manufacturing principles is positioning Indian CDMOs as technologically advanced partners capable of addressing the complex requirements of next-generation drug development programs.

Market Outlook 2026-2034:

The India CDMO market is poised for sustained growth during the forecast period, underpinned by the country's expanding pharmaceutical manufacturing infrastructure, growing global outsourcing demand, and increasing investments in advanced biopharmaceutical capabilities. The accelerating shift among global pharmaceutical companies toward asset-light models and cost-efficient drug development strategies is creating substantial opportunities for Indian CDMOs to expand their international client base. Government-backed programs, including production-linked incentives and regulatory harmonization efforts, continue to attract both domestic and foreign investment into the sector. Rising demand for specialty therapeutics, oncology drugs, and novel biologics is further expanding the scope of services required from contract manufacturers. As India's CDMO sector continues to evolve toward higher-value services, the market is expected to attract increased global partnerships and accelerate capacity additions across both small molecule and biologics manufacturing segments throughout the forecast period. The market generated a revenue of USD 8.52 Billion in 2025 and is projected to reach a revenue of USD 16.53 Billion by 2034, growing at a compound annual growth rate of 7.39% from 2026-2034.

India CDMO Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Service Type |

Contract Manufacturing Services |

53.8% |

|

Product Type |

Small Molecules |

67.2% |

|

Scale of Operation |

Commercial Scale |

70.2% |

|

Therapeutic Area |

Oncology |

33.2% |

|

Region |

West India |

29.8% |

Service Type Insights:

- Contract Development Services

- Preclinical Development

- Clinical Development

- Analytical and Bioanalytical Services

- Contract Manufacturing Services

- Active Pharmaceutical Ingredients (API) Manufacturing

- Finished Dosage Forms (FDF) Manufacturing

- Biologics Manufacturing

- Packaging

Contract manufacturing services dominate with a market share of 53.8% of the total India CDMO market in 2025.

Contract manufacturing services holds the dominant position in the India CDMO market, underpinned by the country's strong legacy in generic drug production and its well-established pharmaceutical manufacturing ecosystem. India's ability to deliver high-quality, cost-competitive manufacturing across diverse therapeutic categories has made it a preferred destination for global pharmaceutical outsourcing. Increasing demand for complex generics, high-potency APIs, and sterile injectables is driving sustained growth in this segment.

The segment's continued dominance is reinforced by India's extensive network of internationally accredited manufacturing facilities that comply with current good manufacturing practices recognized by major global regulatory agencies. Indian CDMOs in this segment are investing in advanced manufacturing infrastructure, including biologics production lines, high-potency compound containment facilities, and next-generation packaging capabilities. These capacity expansions, combined with a growing portfolio of global pharmaceutical partnerships and a robust pipeline of complex drug molecules entering commercial production, are further solidifying contract manufacturing services as the cornerstone of India's CDMO market.

Product Type Insights:

Access the comprehensive market breakdown Request Sample

- Small Molecules

- Biologics

- Biosimilars

- Vaccines

- Others

Small molecules exhibit a clear dominance in the market with 67.2% share of the total India CDMO market in 2025.

Small molecules dominate the India CDMO market, representing the foundation of India's pharmaceutical manufacturing industry and its position as the world's largest producer of generic drugs. India's proficiency in chemical synthesis, process chemistry, and scale-up manufacturing for small molecule APIs and formulations has created a robust ecosystem of contract development and manufacturing capabilities. The extensive patent expiry pipeline for branded blockbuster drugs continues to generate strong demand for small molecule generic manufacturing, enabling Indian CDMOs to expand their product portfolios and strengthen their global market footprint efficiently and competitively.

The continued dominance of small molecules is further driven by the deep integration of Indian CDMOs into global pharmaceutical supply chains, where they serve as critical suppliers for complex generics, cardiovascular drugs, oncology molecules, and anti-infective agents. Research and development investments in improved synthesis routes, green chemistry practices, and continuous manufacturing technologies are enhancing the competitiveness of Indian small molecule manufacturers. As global pharmaceutical companies seek to reduce development costs and accelerate time-to-market, India's small molecule expertise positions it as an indispensable manufacturing partner within the broader global CDMO ecosystem.

Scale of Operation Insights:

- Commercial Scale

- Clinical Scale

Commercial scale represents the leading segment with a 70.2% share of the total India CDMO market in 2025.

Commercial scale operations represent the most substantial segment within the India CDMO market, reflecting the high-volume production requirements of global pharmaceutical companies seeking cost-effective manufacturing partnerships. The segment's dominance is driven by India's capacity to deliver large-batch manufacturing of APIs, generics, and formulations meeting international quality standards. Significant investments in commercial-scale manufacturing infrastructure, including dedicated multipurpose production lines and high-containment manufacturing suites, are enabling Indian CDMOs to expand their capacity and serve a growing base of international pharmaceutical partners seeking reliable, compliant commercial manufacturing solutions.

The sustained prominence of commercial scale operations is reinforced by rising global demand for generic drugs and biosimilars, where India's manufacturing efficiency and cost advantages provide a compelling value proposition. Indian CDMOs operating at commercial scale benefit from economies of scale, optimized process parameters, and established supply chain networks that reduce per-unit production costs substantially. Strategic investments in automation, process analytical technology, and real-time quality monitoring are further improving throughput and compliance in commercial manufacturing environments, supporting the segment's continued leadership through the forecast period.

Therapeutic Area Insights:

- Oncology

- Cardiovascular Diseases

- Infectious Diseases

- Central Nervous System (CNS) Disorders

- Others

Oncology dominates with a market share of 33.2% of the total India CDMO market in 2025.

Oncology represents the most significant therapeutic area within the India CDMO market, reflecting the escalating global cancer burden and the increasing complexity of cancer treatment modalities. India's CDMO sector has developed robust capabilities in manufacturing oncology drugs, including cytotoxic APIs, targeted therapy molecules, and monoclonal antibody-based biologics. The demand for affordable generic oncology drugs in regulated markets, combined with the growing pipeline of novel targeted therapies requiring specialized manufacturing, has positioned Indian CDMOs as critical partners for global oncology drug development and commercialization programs across diverse markets.

The oncology segment continues to strengthen due to increasing focus on specialized manufacturing capabilities designed to handle complex and high-potency compounds. Pharmaceutical manufacturers and CDMOs in India are expanding their oncology-focused production capabilities to support a wide range of therapies, including monoclonal antibodies, peptide-based treatments, and targeted small molecule therapies. This growing emphasis on oncology is also encouraging the development of advanced manufacturing infrastructure and technical expertise, positioning oncology as a key focus area within India's pharmaceutical manufacturing and contract development landscape.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the largest region with 29.8% share of the total India CDMO market in 2025.

West India is currently in the lead in the India CDMO industry, driven by the pharmaceutical manufacturing clusters located in Maharashtra and Gujarat. The region has highly conducive conditions for CDMO operations due to its well-developed industrial base, access to major ports for easier export logistics, and access to a large talent pool of scientifically qualified personnel. Mumbai, Pune, and Ahmedabad are major pharmaceutical clusters with a high number of formulation and API manufacturing sites catering to international markets and contributing to a large share of pharmaceutical exports from India.

The region has a strong base for CDMO operations with investments in advanced technology, biologics manufacturing sites, and compliant infrastructure. West India has access to well-developed financial systems to support pharmaceutical investments and access to a large number of contract research organizations to complement CDMO operations. The region has strong government support for industrial development in Gujarat and Maharashtra, including pharmaceutical parks and special economic zones. West India is likely to remain the largest segment in the India CDMO industry during the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India CDMO Market Growing?

Cost-Competitive Manufacturing and Skilled Scientific Workforce

India's CDMO sector benefits significantly from its structural cost advantages, which position Indian manufacturers as highly attractive outsourcing partners for global pharmaceutical companies seeking to optimize development and production expenditures. Manufacturing costs in India are substantially lower than in Western countries and approximately 20% below those of Chinese competitors, enabling Indian CDMOs to offer globally competitive pricing without compromising quality or regulatory compliance standards. This cost efficiency extends across the full pharmaceutical manufacturing value chain, encompassing raw material sourcing, labor, utilities, and regulatory compliance activities. India's large and continuously expanding pool of highly trained scientists, chemists, and pharmaceutical engineers further enhances this competitive advantage. The country produces a substantial number of qualified science and engineering graduates each year, providing CDMOs with access to specialized talent in medicinal chemistry, process development, bioanalytical sciences, and regulatory affairs. This combination of cost competitiveness and scientific expertise has made India a first-choice outsourcing destination for generic manufacturers, biotech companies, and large multinational pharmaceutical corporations seeking to reduce costs while maintaining high standards of quality and innovation in drug development and manufacturing operations.

Rising Global Outsourcing and Supply Chain Diversification

The global pharmaceutical industry is undergoing a fundamental structural shift toward increased outsourcing, driven by the rising complexity of drug development, escalating R&D costs, and the need for operational flexibility. Major pharmaceutical companies are increasingly adopting asset-light business models, focusing internal resources on drug discovery and commercialization while delegating development and manufacturing functions to specialized CDMOs. This strategic reorientation is generating substantial demand for contract manufacturing services, and Indian CDMOs are well-positioned to capture a significant share of this expanding market. Simultaneously, geopolitical factors, including trade tensions and supply chain disruptions, have prompted global pharmaceutical companies to diversify their manufacturing footprints away from concentrated single-source dependencies. India has emerged as a preferred alternative for pharmaceutical companies seeking to de-risk their supply chains. A 2025 Boston Consulting Group report highlighted that some Indian CDMOs witnessed a surge of approximately 50% in requests for proposals in 2024 as global companies actively sought manufacturing alternatives, underscoring the scale of opportunity created by global supply chain realignment trends and India's growing stature as a preferred pharmaceutical manufacturing partner.

Supportive Government Policies and Regulatory Alignment

India's pharmaceutical sector has benefited substantially from a proactive government policy framework designed to strengthen domestic manufacturing capabilities and attract global pharmaceutical investment. The Production-Linked Incentive (PLI) scheme for pharmaceuticals and active pharmaceutical ingredients represents a landmark government initiative that provides financial incentives to domestic manufacturers for achieving defined production targets, encouraging investment in advanced manufacturing technologies and bulk drug production infrastructure. These incentive programs have stimulated meaningful capacity expansion and technology upgrades across the CDMO ecosystem. India's regulatory alignment with major international agencies, including the USFDA and EMA, further enhances its attractiveness as a manufacturing partner for global pharmaceutical companies. India operates one of the world's largest networks of USFDA-approved manufacturing facilities outside the United States, reflecting decades of investment in quality systems, manufacturing process controls, and regulatory compliance capabilities. This regulatory credibility is a critical decision-making factor for multinational pharmaceutical companies selecting manufacturing partners for products destined for regulated markets in North America, Europe, and other established pharmaceutical markets worldwide.

Market Restraints:

What Challenges the India CDMO Market is Facing?

Complex Regulatory Compliance Requirements

Meeting the stringent and continuously evolving regulatory requirements of multiple international markets presents a significant operational challenge for Indian CDMOs. Navigating the distinct quality standards, documentation requirements, and inspection protocols of agencies such as the USFDA, EMA, Health Canada, and others simultaneously demands substantial investment in quality management systems, compliance infrastructure, and dedicated regulatory affairs expertise. Regulatory inspections, Warning Letters, and import alerts pose serious risks to business continuity and client retention, and the cost and time required to achieve and maintain international regulatory credentials can constrain the growth capacity of smaller CDMO operators in the market.

Infrastructure and Technology Gaps in Advanced Therapeutics

Despite India's strong position in small molecule manufacturing, a technology and infrastructure gap persists in advanced therapeutic modalities, including cell and gene therapies, antibody-drug conjugates, and RNA-based therapeutics. The highly specialized equipment, containment systems, and manufacturing environments required for these emerging drug classes demand significant capital investment that many Indian CDMOs have not yet deployed at scale. This capability gap limits the ability of Indian players to fully capitalize on the growing global demand for next-generation biopharmaceutical contract manufacturing services and may restrict market competitiveness in higher-value service categories during the forecast period.

Intellectual Property and Data Security Concerns

Intellectual property protection remains a persistent concern for global pharmaceutical companies considering outsourcing development and manufacturing activities to Indian CDMOs. The pharmaceutical industry relies heavily on proprietary formulation know-how, synthesis processes, and clinical data that must be carefully protected when transferred to third-party contractors. While India's legal framework for intellectual property protection has strengthened progressively, concerns about data security, trade secret protection, and the potential for unauthorized technology transfer continue to influence risk assessments conducted by potential client companies. These concerns can extend due diligence processes, complicate contractual negotiations, and limit the depth of technology transfer that international clients are willing to undertake.

Competitive Landscape:

The Indian market for CDMOs is a dynamic and changing competitive landscape, where existing contract manufacturers are looking to increase their scope of services and reach in order to secure a greater share of the global market for pharmaceutical outsourcing services. The market comprises a wide array of large integrated contract manufacturers with full-service capabilities and specialized service providers with a focus on specific therapeutic areas and manufacturing technologies. Strategic transactions, global alliances, and expansion are changing the competitive landscape of the market, as leading players are investing in state-of-the-art technology for the manufacture of biologics, antibody-drug conjugates, and sterile injectables. Qualifications and certifications from major international regulatory agencies and technology differentiation are the major factors that influence competition in the market. As global pharmaceutical companies look for a consolidated supplier base and strategic long-term alliances, contract manufacturers with the capabilities of providing full-service development through commercialization services with robust quality management systems are gaining significant competitive advantages.

Recent Developments:

- In February 2025, Granules India announced the acquisition of Swiss CDMO Senn Chemicals AG for CHF 20 Million (approximately INR 192.5 Crore), marking its strategic entry into the peptide therapeutics and CDMO sectors. The acquisition provided Granules with access to specialized expertise in Liquid-Phase Peptide Synthesis (LPPS) and Solid-Phase Peptide Synthesis (SPPS), along with a well-established customer base across the pharmaceutical and theragnostic industries and a strong regulatory presence in Europe.

- In December 2024, Akums Drugs and Pharmaceuticals Limited announced a strategic partnership with a global pharmaceutical company to serve as a CDMO, manufacturing and supplying oral liquid formulations for the European market under a Euro 200 Million contract set to commence in 2027. The partnership underscores India's growing role as a preferred CDMO destination for European pharmaceutical companies seeking cost-effective and high-quality manufacturing solutions.

India CDMO Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered |

|

| Types Covered | Small Molecules, Biologics, Biosimilars, Vaccines, Others |

| Scale of Operations Covered | Commercial Scale, Clinical Scale |

| Therapeutic Areas Covered | Oncology, Cardiovascular Diseases, Infectious Diseases, Central Nervous System (CNS) Disorders, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India CDMO Market Report

The India CDMO market size was valued at USD 8.52 Billion in 2025.

The India CDMO market is expected to grow at a compound annual growth rate of 7.39% from 2026-2034 to reach USD 16.53 Billion by 2034.

Contract manufacturing services dominated the market with a share of 53.8%, driven by India's established API production capabilities, cost-competitive manufacturing ecosystem, and rising global demand for finished dosage forms and biologics outsourcing.

Key factors driving the India CDMO market include increasing pharmaceutical outsourcing by global companies, India's cost-competitive manufacturing advantages, strong regulatory compliance credentials, expanding biologics capabilities, and supportive government incentive programs such as the Production-Linked Incentive (PLI) scheme.

Major challenges include complex international regulatory compliance requirements, infrastructure and technology gaps in advanced biologics manufacturing, intellectual property protection concerns, intense global competition from established CDMO hubs, and high capital investment requirements for specialized facilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)