India Cement Board Market Size, Share, Trends and Forecast by Product Type, Application, End-User Industry, and Region, 2026-2034

India Cement Board Market Size, Share, Trends & Forecast (2026-2034)

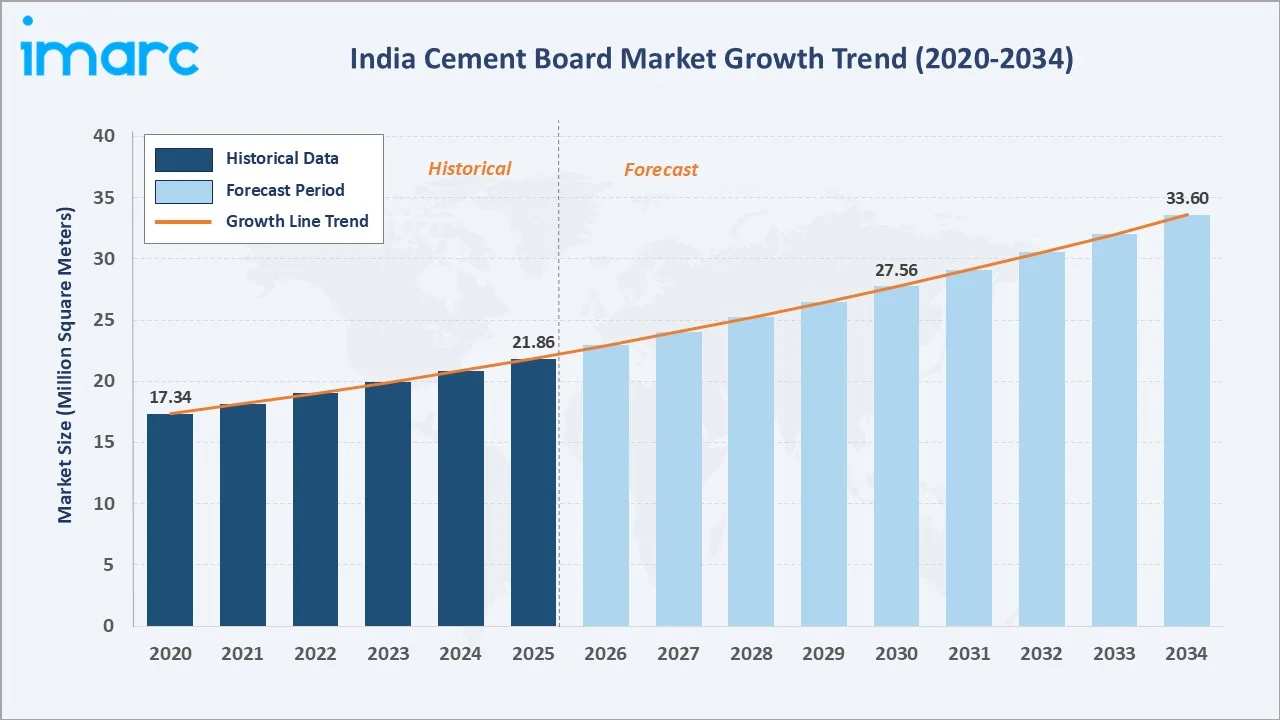

The India cement board market was valued at 21.86 Million Square Meters in 2025 and is projected to reach 33.60 Million Square Meters by 2034, exhibiting a CAGR of 4.75% during 2026-2034. India's expanding real estate sector, accelerating adoption of green and sustainable construction materials, and strong demand for fire-resistant and moisture-proof building panels are the primary forces driving market growth.

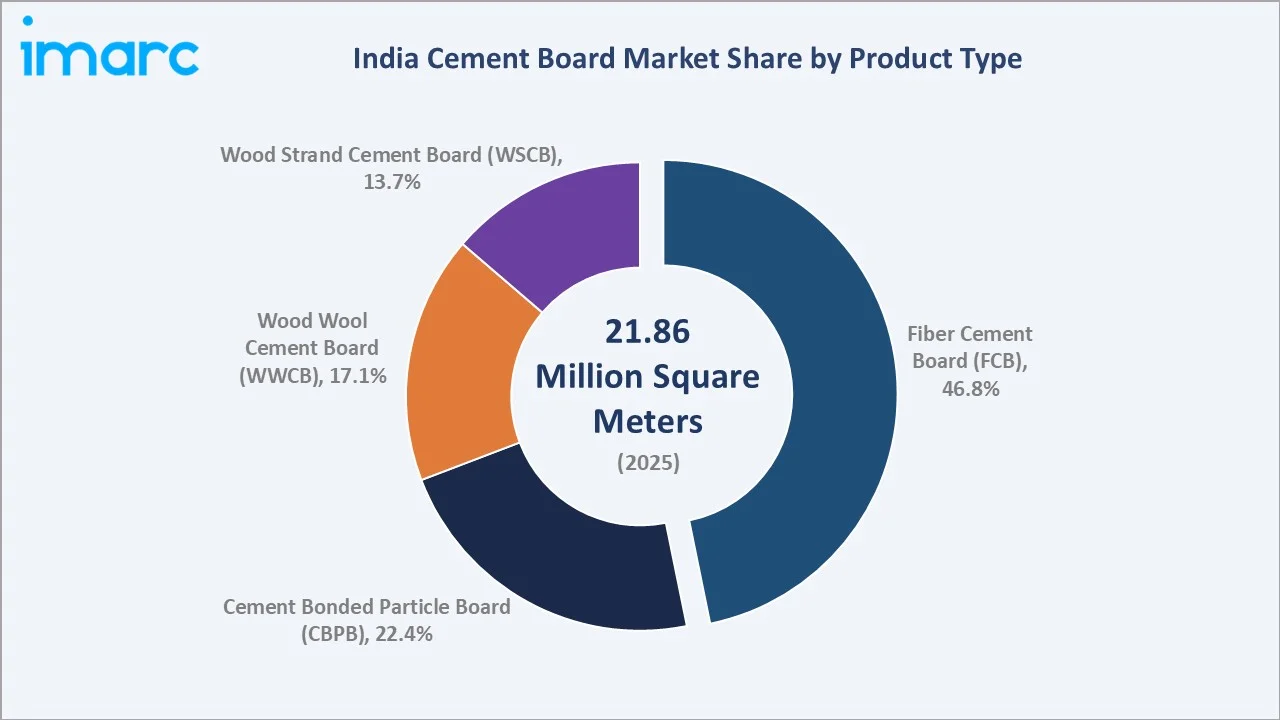

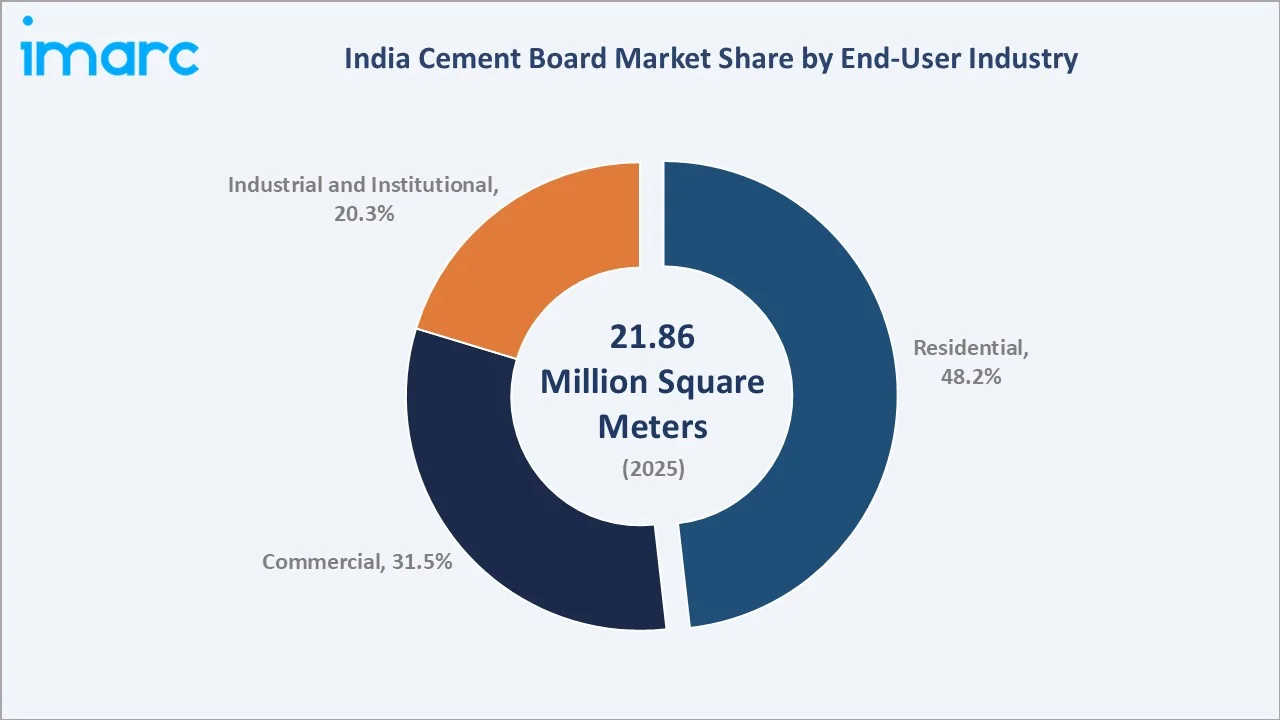

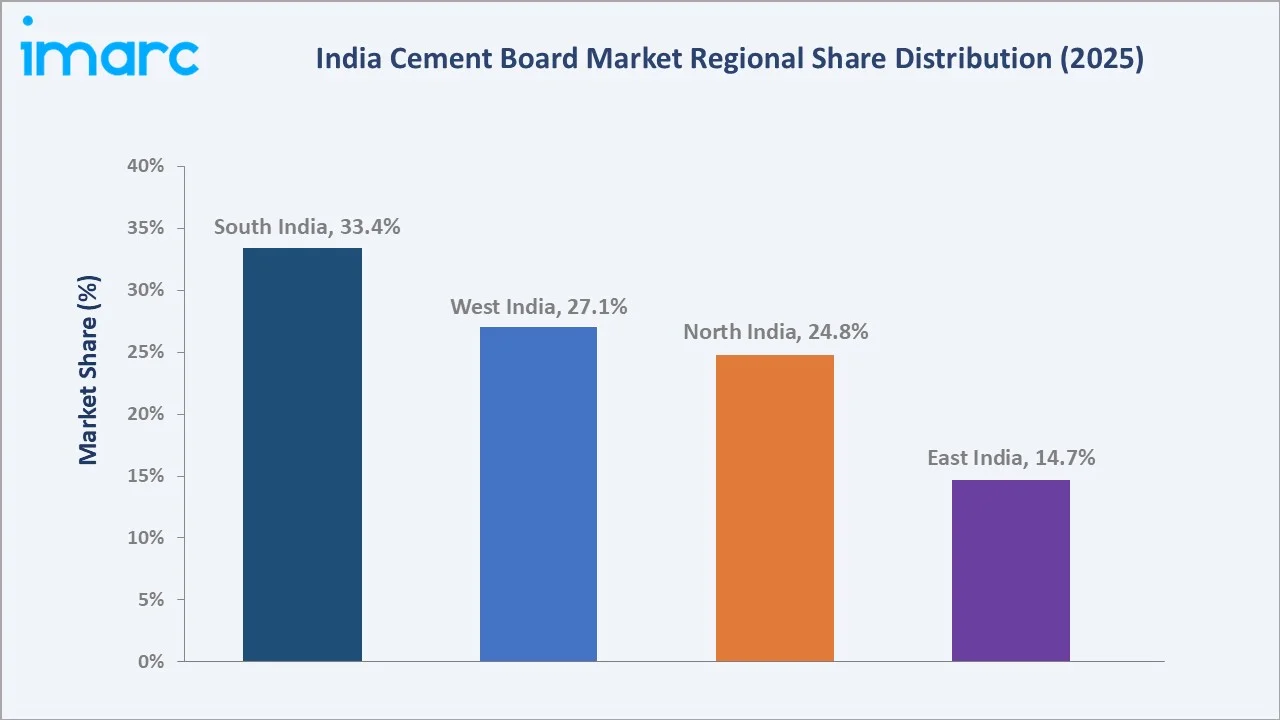

Fiber cement board (FCB) leads the product type segment at 46.8%, residential commands 48.2% end-user industry share, and South India dominates regional demand at 33.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

21.86 Million Square Meters |

|

Forecast Market Size (2034) |

33.60 Million Square Meters |

|

CAGR (2026-2034) |

4.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (33.4%, 2025) |

|

Second Largest Region |

West India (27.1%, 2025) |

|

Leading Product Type |

Fiber Cement Board (FCB) (46.8%, 2025) |

|

Leading End-User Industry |

Residential (48.2%, 2025) |

The India cement board market expanded from 17.34 Million Square Meters in 2020 to 21.86 Million Square Meters in 2025, driven by rising urban construction activity, rapid adoption of modular building techniques, and increasing substitution of traditional plywood and gypsum with cement-based panel solutions. Anchored at 27.56 Million Square Meters in 2030, the forecast to 33.60 Million Square Meters by 2034 is underpinned by green building norms, smart city projects, and growing commercial real estate investments across tier-2 and tier-3 Indian cities.

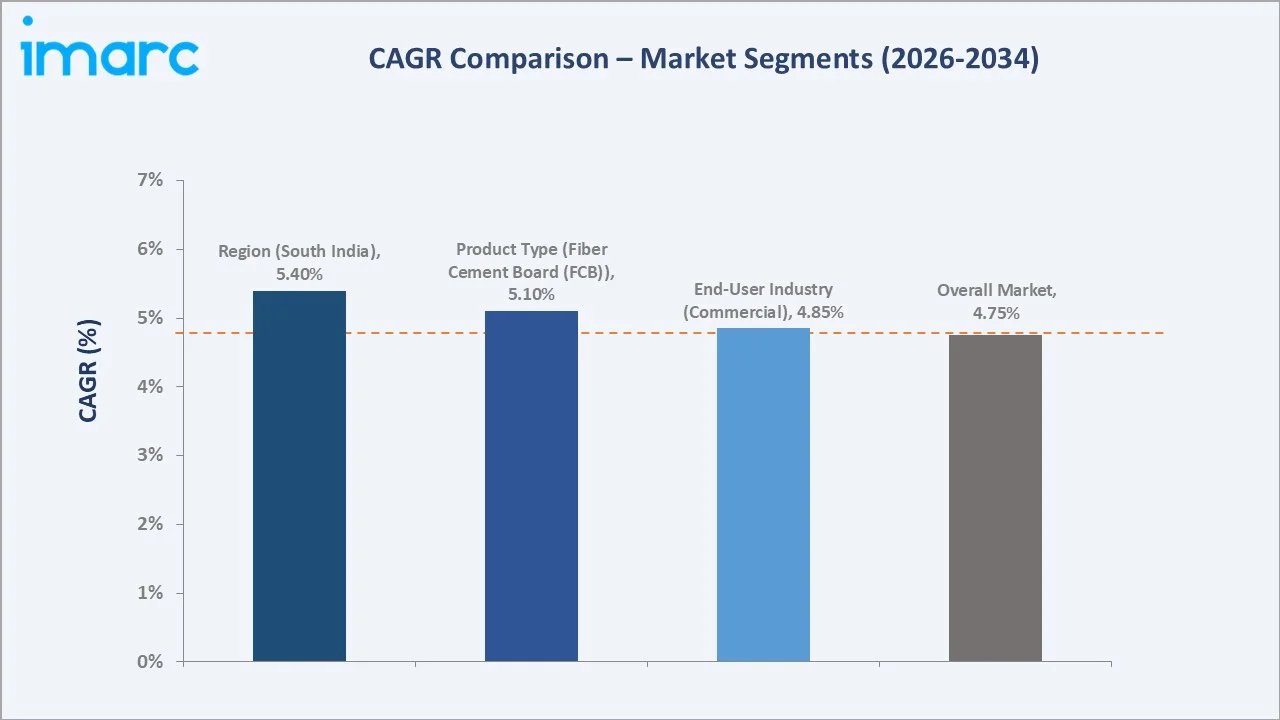

CAGR trajectories across product type and end-user industry sub-segments reveal that fiber cement board (FCB) and residential are expanding faster than the overall 4.75% market CAGR, driven by rising urbanization, affordable housing demand, and superior performance attributes in humid Indian climatic conditions.

Executive Summary

The India cement board market is on a steady growth trajectory from 17.34 Million Square Meters in 2020 to 33.60 Million Square Meters by 2034. The sector has transitioned from a niche construction alternative to a mainstream building material, adopted across residential, commercial, and industrial applications. Cement board's superior moisture resistance, fire retardancy, and dimensional stability over wood and gypsum-based panels have made it the preferred choice in humid, coastal, and high-fire-risk zones across India.

Fiber cement board (FCB) leads the product type segment at 46.8% share in 2025, supported by its lightweight nature, ease of installation, and widespread use in external cladding, facade systems, and partition walls. Residential commands 48.2% share of the end-user industry segment in 2025, reflecting the acceleration of affordable housing schemes and urban housing demand. Under the Pradhan Mantri Awaas Yojana–Gramin (PMAY-G), as of August 4, 2025, the Ministry set a total target of 4.12 Crore for states and Union Territories (UTs), of which 3.85 Crore houses were approved and over 2.82 Crore houses were finished. South India anchors 33.4% regional share, led by large-scale construction activity in Tamil Nadu, Karnataka, Andhra Pradesh, and Kerala.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Fiber Cement Board (FCB) – 46.8% share (2025) |

|

Second Largest Product Type |

Cement Bonded Particle Board (CBPB) – 22.4% share (2025) |

|

Leading End-User Industry |

Residential – 48.2% share (2025) |

|

Second Largest End-User Industry |

Commercial – 31.5% share (2025) |

|

Leading Region |

South India – 33.4% share (2025) |

|

Second Largest Region |

West India – 27.1% share (2025) |

|

Top Companies |

Everest Industries Limited, Visaka Industries Limited, CKA Birla Group, Etex Group, Sahyadri Industries Pvt. Ltd. |

Key Analytical Observations Expanding On The Data Above:

- Fiber cement board (FCB) at 46.8% dominates the product type segment, reflecting strong preference for its superior strength-to-weight ratio, dimensional stability, and suitability for both interior and exterior applications across India's diverse climatic zones.

- Cement bonded particle board (CBPB) at 22.4% holds the second-largest product type share, driven by its acoustic performance and growing adoption in industrial flooring, prefabricated housing modules, and commercial partition systems.

- Residential dominance at 48.2% reflects accelerating urban housing construction under central and state government schemes, rising middle-class homeownership aspirations, and the shift toward modular construction formats. As per IMARC Group, the India modular construction market size reached USD 3.2 Billion in 2025.

- Commercial at 31.5% represents growing adoption in office complexes, retail spaces, hotels, and healthcare facilities, where fire resistance and long-term durability are key material selection criteria.

- South India at 33.4% leads regional demand, anchored by Tamil Nadu, Karnataka, Andhra Pradesh, and Kerala, supported by high construction activity, humidity-driven demand for moisture-resistant materials, and the presence of major manufacturers.

India Cement Board Market Overview

A cement board is a flat-panel building material manufactured from a composite of Portland cement, silica, cellulose fiber, and fly ash, pressed and cured through high-temperature autoclaving or air-curing processes. It serves as a structural and non-structural panel for wall cladding, flooring underlay, facade systems, roofing, and partition walls across residential, commercial, and industrial construction applications.

The Indian ecosystem integrates raw material suppliers, board manufacturers, processing and fabrication units, logistics and distribution networks, retailers and building material dealers, and end-user construction companies. Macroeconomic factors, including urbanization rates, housing policy, construction sector GDP contribution, and building code standards, collectively shape near-term demand.

Market Dynamics

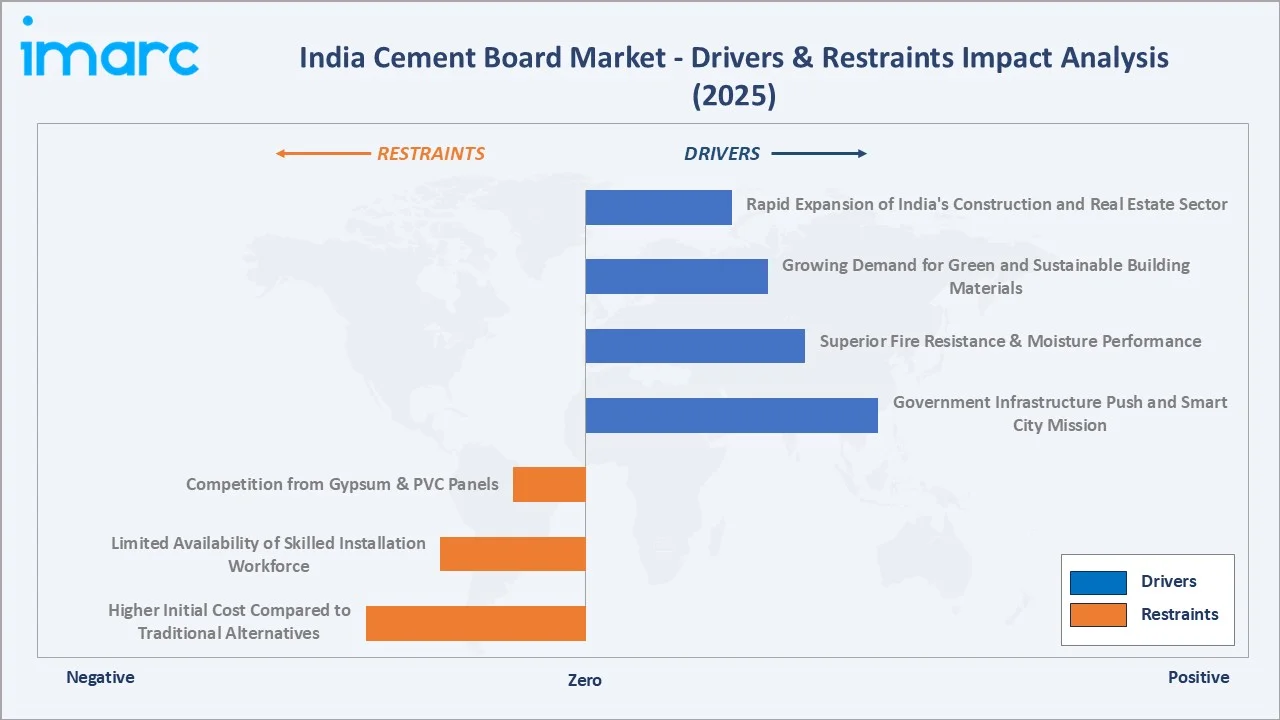

Market Drivers

- Rapid Expansion of India's Construction and Real Estate Sector: India's ongoing urbanization, estimated to drive 600 Million urban dwellers by 2031, is generating unprecedented construction activity across residential, commercial, and infrastructure segments. The resulting demand for scalable, cost-efficient, and high-performance building panel materials is a primary driver of cement board adoption across project categories.

- Growing Demand for Green and Sustainable Building Materials: India's adoption of GRIHA, IGBC, and BEE green building standards is accelerating the substitution of traditional wood, asbestos, and gypsum boards with cement-based panels. Cement boards contain no asbestos, have lower embodied carbon than concrete alternatives, and offer superior recyclability, aligning with ESG-driven procurement by institutional developers.

- Superior Fire Resistance and Moisture Performance: Cement boards are widely preferred in high-rise residential buildings, healthcare facilities, and public infrastructure projects due to their excellent fire-resistant properties and compliance with stringent building safety requirements. Their inherent moisture resistance also makes them well-suited for coastal and humid environments, supporting long-term durability and reduced maintenance needs.

- Government Infrastructure Push and Smart City Mission: Ongoing investments in urban development, transportation infrastructure, commercial complexes, and public facilities are creating sustained demand for durable and high-performance construction materials. Cement boards are increasingly being adopted across these projects due to their versatility, ease of installation, and ability to meet modern building performance standards.

Market Restraints

- Higher Initial Cost Compared to Traditional Alternatives: FCBs and CBPBs typically command a cost premium over standard gypsum boards and plywood panels on a per-square-meter basis. In price-sensitive residential markets, especially tier-3 cities and rural housing projects, this initial cost differential limits adoption and extends payback period calculations for contractors and developers.

- Limited Availability of Skilled Installation Workforce: Cement boards require specialized drilling, cutting, and fastening techniques distinct from those used with gypsum or plywood. The fragmented nature of India's construction workforce and limited vocational training for cement board installation creates quality control risks, project delays, and hesitance among small contractors to specify the material.

- Competition from Gypsum Boards and PVC Panel Substitutes: The India gypsum board market is a well-established segment with deep distribution, established installer bases, and lower material costs. For interior partition and false ceiling applications, gypsum boards remain the default specification in commercial projects, posing a structural competitive challenge for cement board in this application category.

Market Opportunities

- Industrial and Institutional Segment Growth: Expanding investments in logistics warehousing, healthcare infrastructure, and data center construction across India are creating new demand pools for cement boards in industrial roofing, interior wall linings, and mezzanine flooring. These segments require fire-rated, heavy-load-bearing panels with low maintenance profiles, where cement boards hold clear performance advantages.

- Export Potential to Southeast Asia and the Middle East: Indian cement board manufacturers, particularly FCB producers in South and West India, are well-positioned to supply construction markets in the UAE, Saudi Arabia, Vietnam, and Indonesia, where green building norms are tightening and import substitution is being actively sought by project developers.

Market Challenges

- Raw Material Price Volatility: Cement boards require Portland cement, fly ash, cellulose fibers, and silica as primary inputs. Fluctuations in cement prices, linked to coal and limestone costs, and volatility in cellulose fiber sourcing, can compress manufacturer margins and limit the ability to offer competitive pricing in tender-driven infrastructure projects.

- Fragmented Distribution and Low Brand Awareness in Tier-2 Markets: Unlike gypsum boards, cement boards lack deep dealer penetration in tier-2 and tier-3 Indian cities. Low product awareness among small contractors, insufficient demonstrator projects, and limited point-of-sale marketing constrain market penetration outside major metro and Tier-1 construction hubs.

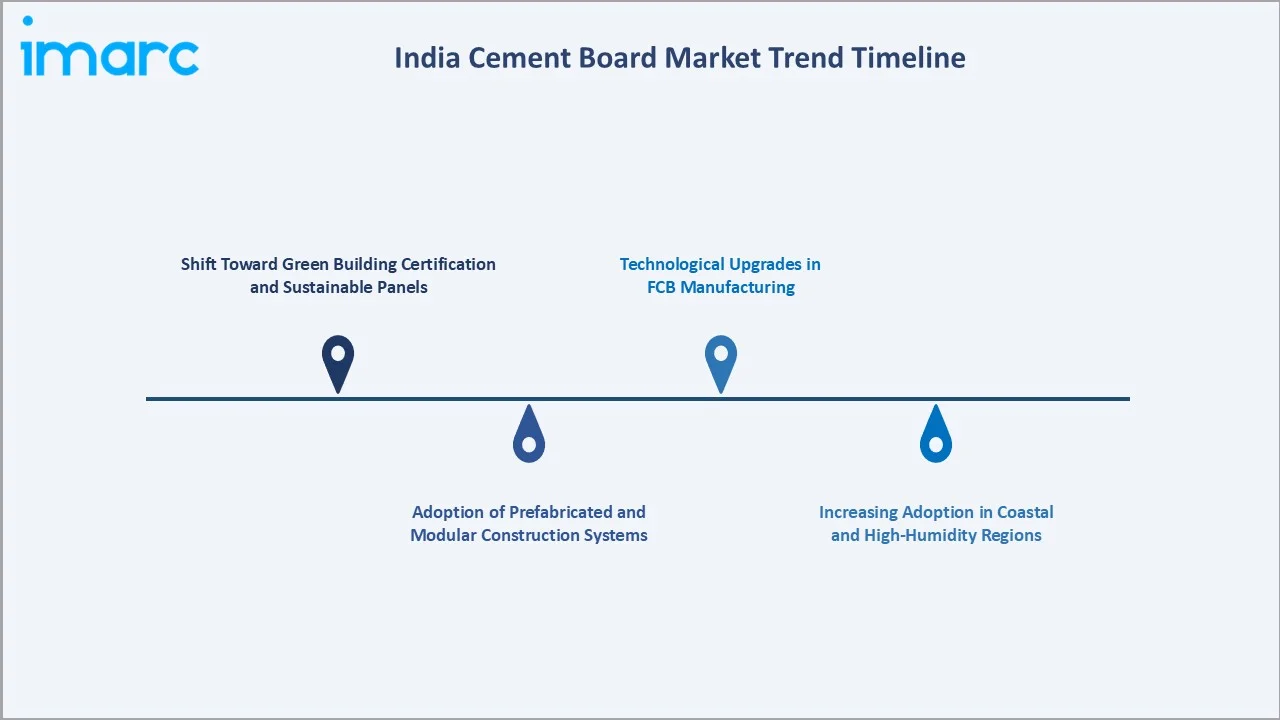

Emerging Market Trends

1. Shift Toward Green Building Certification and Sustainable Panels

The growing adoption of green building standards and sustainable construction practices is driving demand for non-asbestos, low-emission, and resource-efficient building materials. Cement boards are gaining preference in residential, commercial, and institutional projects due to their durability, fire resistance, moisture tolerance, and alignment with evolving sustainability and building-performance requirements.

2. Adoption of Prefabricated and Modular Construction Systems

India's construction industry is rapidly embracing prefabricated and modular building techniques to reduce on-site labor dependency and accelerate project timelines. Cement boards, particularly CBPB and wood strand cement board (WSCB) variants, are integral to panelized wall systems, modular bathroom pods, and light gauge steel frame structures.

3. Technological Upgrades in FCB Manufacturing

Indian FCB manufacturers are investing in Hatschek process upgrades, digital fiber blending controls, and advanced autoclaving technologies to improve board density, surface finish, and dimensional accuracy. These investments are enabling domestic producers to supply specification-grade boards meeting international standards, expanding their competitiveness in premium commercial and infrastructure projects.

4. Increasing Adoption in Coastal and High-Humidity Regions

Coastal states, including Kerala, Tamil Nadu, Goa, Andhra Pradesh, Maharashtra, and Gujarat, are recording above-average cement board adoption rates due to the material's inherent resistance to salt air corrosion, moisture ingress, and biological degradation. This climatic demand factor reinforces the structural leadership of South and West India in regional market share and is expected to drive higher per-capita consumption in these regions through 2034.

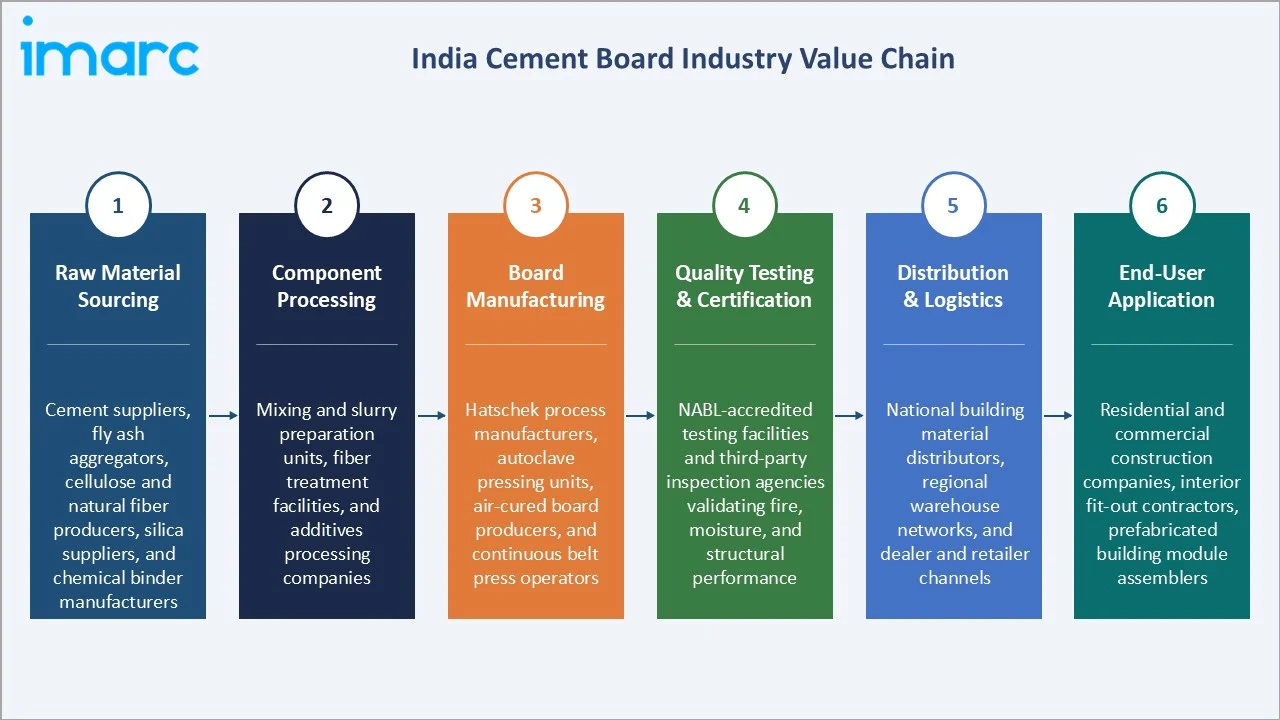

Industry Value Chain Analysis

The India cement board value chain spans six stages from raw material sourcing to end-user application and lifecycle maintenance. Board manufacturing, quality control, and distribution logistics capture the highest value-add, while raw material procurement and technology licensing increasingly determine competitive cost positioning among domestic producers.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Cement suppliers, fly ash aggregators, cellulose and natural fiber producers, silica suppliers, and chemical binder manufacturers providing inputs for board manufacturing |

|

Component Processing |

Mixing and slurry preparation units, fiber treatment facilities, and additives processing companies supporting board composition and quality standards |

|

Board Manufacturing |

Hatschek process manufacturers, autoclave pressing units, air-cured board producers, and continuous belt press operators producing FCB, CBPB, wood wool cement board (WWCB), and WSCB variants |

|

Quality Testing & Certification |

NABL-accredited testing facilities and third-party inspection agencies validating fire, moisture, and structural performance |

|

Distribution & Logistics |

National building material distributors, regional warehouse networks, dealer and retailer channels, and direct supply partners to large construction companies and contractors |

|

End-User Application |

Residential and commercial construction companies, interior fit-out contractors, prefabricated building module assemblers, and government project developers across housing, infrastructure, and industrial segments |

Vertically integrated manufacturers with in-house fiber sourcing and direct distribution networks are positioned to capture greater value than companies reliant on third-party manufacturing or narrow product portfolios limited to a single board variant.

Technology Landscape in the India Cement Board Industry

Hatschek Process and Advanced Manufacturing Automation

The Hatschek wet process remains the dominant FCB manufacturing technology in India, enabling high-volume, consistent panel production with controlled density and fiber distribution. Leading manufacturers are investing in digital process monitoring, automated slurry blending, and computer-controlled sheet forming to improve yield, reduce raw material waste, and achieve international density specifications for specification-grade commercial projects.

Cellulose Fiber and Synthetic Fiber Integration

Indian FCB producers are progressively integrating synthetic PVA fibers alongside traditional cellulose fibers to enhance tensile strength, crack resistance, and durability of boards under thermal cycling conditions. This fiber hybridization technology improves product performance in extreme climate zones and positions Indian-manufactured boards as competitive in specification markets.

Digital Quality Control and Non-Destructive Testing

Advanced manufacturers are deploying inline thickness gauges, surface defect detection cameras, and ultrasonic non-destructive testing systems on production lines to ensure consistent quality across high-volume runs. Real-time quality data analytics are reducing post-production rejection rates and supporting compliance with BIS and international certification requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Fiber Cement Board (FCB) |

46.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End-User Industry |

Residential |

48.2% |

2025 |

|

Region |

South India |

33.4% |

2025 |

By Product Type

Fiber cement board (FCB) commands a leading 46.8% share in 2025, driven by its versatility across external cladding, facade panels, wet area wall linings, roofing underlays, and internal partitions. Its lightweight nature relative to solid concrete panels makes FCB the standard specification for residential and commercial construction across India.

To access detailed market analysis, Request Sample

Cement bonded particle board (CBPB) holds a 22.4% share in 2025, valued for acoustic insulation, structural density, and suitability for industrial flooring and prefabricated housing panel systems.

By End-User Industry

Residential leads at 48.2% share in 2025, fueled by urban housing demand, government-backed affordable housing programs, and the increasing adoption of cement boards in bathroom walls, kitchen areas, external cladding, and roofing underlays.

Commercial at 31.5% reflects growing corporate campus, retail, hospitality, and healthcare construction. The segment benefits from increasing demand for fire-resistant, moisture-resistant, and low-maintenance building materials in modern commercial developments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

33.4% |

Large construction activity, humidity-driven material demand, presence of major manufacturers, coastal residential and commercial building expansion |

|

West India |

27.1% |

Strong commercial real estate in Maharashtra and Gujarat, rising infrastructure investment, growing industrial corridor construction, and port-led logistics facility development |

|

North India |

24.8% |

High urban population density, large-scale affordable housing projects, growing commercial construction in NCR and Punjab, and expanding retail and institutional segments |

|

East India |

14.7% |

Rising industrial activity, government-led urban infrastructure projects, and increasing construction in Odisha, West Bengal, and the northeast corridor |

South India at 33.4% in 2025 leads the regional landscape, anchored by Tamil Nadu, Karnataka, Andhra Pradesh, and Kerala. The region's high humidity, cyclone-prone coastal belt, and strong IT-driven commercial construction activity create consistent demand for moisture-resistant, high-performance cement board solutions.

West India at 27.1% is the second largest region. Robust commercial construction in Mumbai, Pune, Ahmedabad, and Surat, combined with major industrial corridor development under the Delhi-Mumbai Industrial Corridor (DMIC), is driving cement board adoption.

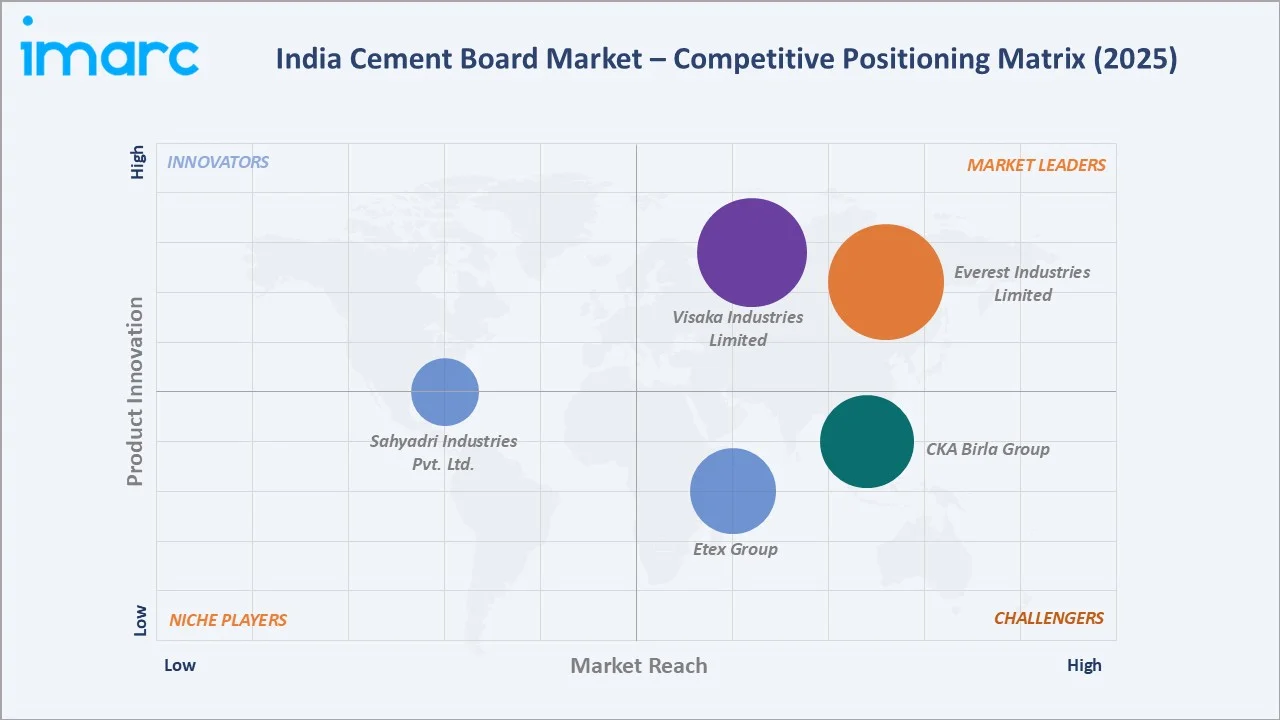

Competitive Landscape

The India cement board market is moderately fragmented, with established domestic manufacturers holding strong positions in regional distribution and product certification, while international players compete on product technology and specification quality. Market leadership is determined by product range breadth, manufacturing scale, BIS certification status, and presence in high-value commercial and infrastructure project categories.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Everest Industries Limited |

Everest Fiber Cement Board, SuperHD |

Leader |

Pan-India manufacturer with diversified cement board and steel building solutions portfolio |

|

Visaka Industries Limited |

Vnext (VBoards, VPanel) |

Leader |

India's leading FCB brand by volume with pan-India manufacturing and export presence |

|

CKA Birla Group |

BirlaNu Aerocon |

Challenger |

Diversified building materials company with strong roofing and panel solutions distributed across India |

|

Etex Group |

Cedral, EQUITONE, Eternit |

Challenger |

Expanding sustainable building solutions through product innovation, distribution growth, and stronger project specification capabilities |

|

Sahyadri Industries Pvt. Ltd. |

Ecopro |

Emerging |

Maharashtra-based FCB manufacturer serving residential and commercial construction across West and South India |

Key players include Everest Industries Limited, Visaka Industries Limited, CKA Birla Group, Etex Group, and Sahyadri Industries Pvt. Ltd., among others.

Key Company Profiles

Everest Industries Limited

Everest Industries Limited is an Indian building materials company engaged in the manufacture and trading of FCBs, roofing products, boards and panels, and pre-engineered steel buildings. The company serves residential, commercial, and industrial construction segments across India and exports to multiple international markets.

- Product Portfolio: Everest Fiber Cement Board for partition walls, wall linings, false ceilings, and internal applications; SuperHD high-density FCBs for exterior cladding, facade systems, and wet areas.

- Recent Developments: The company has continued to strengthen its building products portfolio through ongoing product enhancements, distribution network expansion, and increased focus on serving residential, commercial, and industrial construction projects across key markets.

- Strategic Focus: Expanding the FCB product range, growing commercial project specification, and scaling distribution across urban and semi-urban construction markets through strengthened dealer and contractor partnerships.

CKA Birla Group

CKA Birla Group is an Indian multinational conglomerate with a diversified presence across technology, automotive, home and building, and healthcare sectors. Its building materials operations are conducted through BirlaNu, the group's flagship building solutions company, which manufactures FCBs, roofing products, AAC blocks, wall panels, pipes and fittings, construction chemicals, and flooring solutions.

- Product Portfolio: BirlaNu Aerocon FCBs and sandwich wall panels for partition walls, cladding, and prefabricated building applications.

- Recent Developments: The company has been focusing on enhancing its building solutions portfolio through new product introductions, expanded channel engagement, and broader participation in construction projects, while reinforcing its position in the fiber cement and prefabricated building materials segment.

- Strategic Focus: Building an integrated home and building solutions platform, strengthening dealer and contractor networks across India, and growing fiber cement panel and board specification in residential, commercial, and infrastructure construction segments.

Etex Group

Etex Group is a Belgian multinational building materials company headquartered in Zaventem, Belgium. Founded in 1905, the company operates across several countries and manufactures fiber cement, plasterboard, fire protection, and insulation products.

- Product Portfolio: Cedral fiber cement weatherboard and slate cladding for residential facades and roofs; EQUITONE through-colored fiber cement facade panels for commercial and architectural projects; and Eternit fiber cement roofing and facade systems.

- Recent Developments: Etex Group has been expanding its product certification portfolio, growing specification partnerships with architects and contractors across global markets, and investing in sustainable manufacturing practices to reduce the carbon intensity of its fiber cement product range.

- Strategic Focus: Growing fiber cement facade and exterior cladding specification in commercial and premium residential construction markets, expanding sustainable product offerings, and strengthening distribution partnerships across Asia-Pacific and emerging construction markets.

Market Concentration Analysis

The India cement board market exhibits moderate concentration, with the top two domestic producers - Everest Industries Limited and Visaka Industries Limited - collectively accounting for the largest share of production capacity, BIS certifications, and commercial project specifications across the fiber cement board (FCB) and cement bonded particle board (CBPB) product type categories.

Barriers to entry include high capital expenditure for Hatschek process manufacturing lines, BIS and NABL certification requirements, the need for established dealer networks in tier-2 and tier-3 cities, and deep product knowledge for specification selling to architects and project consultants. These factors favor well-capitalized incumbents with established manufacturing footprints, certified product ranges, and multi-state distribution capabilities.

Consolidation trends are emerging as smaller regional manufacturers face margin pressure from rising raw material costs and increasing certification compliance requirements. Domestic manufacturers are expanding capacity to serve the high-volume affordable housing pipeline, while international players maintain premium specification positions in commercial facade and industrial board segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Wood strand cement board (WSCB) is expanding the fastest among product types, driven by growing adoption in light gauge steel frame construction, engineered timber hybrid buildings, and structural insulated panel systems for modular housing. Fiber cement board (FCB) remains the highest absolute-volume segment, growing at above-market rates in coastal high-rise facade and premium residential cladding applications.

Emerging Markets

West India is the fastest-growing region, anchored by Maharashtra and Gujarat's robust commercial and industrial construction pipelines. East India at 14.7% represents the most underpenetrated regional opportunity, with rising urban infrastructure investment, government-funded smart city projects, and growing industrial activity in West Bengal, Odisha, and Assam creating new addressable demand.

Venture & Investment Trends

Investment is concentrated in Hatschek process automation and capacity expansion by domestic FCB manufacturers, export infrastructure development to serve Southeast Asian and Middle Eastern markets, and technology licensing for new CBPB and WSCB production lines. Private equity interest is also visible in the building material distribution segment, with consolidation of regional dealer networks creating wider and more efficient go-to-market infrastructure.

Future Market Outlook (2026-2034)

The India cement board market is forecast to expand from 21.86 Million Square Meters in 2025 to 33.60 Million Square Meters by 2034 at a CAGR of 4.75%, adding approximately 11.74 Million Square Meters of incremental market volume over the forecast period.

Four forces will shape the market through 2034: continued urbanization and housing demand growth under PM Awas Yojana and smart city initiatives; tightening green building and fire safety standards under the revised National Building Code; technological advancement in FCB manufacturing enabling higher-performance, lower-cost products; and the accelerating adoption of prefabricated and modular construction methods where cement boards are structurally integral.

By 2034, fiber cement board (FCB) is expected to maintain segment leadership with an expanded share driven by facade and cladding applications in urban high-rise construction. The residential end-user industry segment is projected to sustain its dominant position as India's housing construction pipeline remains one of the world's largest. South India will retain regional leadership, while West India's share is expected to approach near-parity as commercial and industrial construction activity continues its structural expansion.

Research Methodology

Primary Research

Primary research included structured interviews with cement board manufacturers, construction project developers, building material dealers, interior design consultants, architects, and government housing scheme project managers. Insights from these engagements were used to validate market sizing, regional demand patterns, product preference trends, and competitive positioning across the India cement board value chain.

Secondary Research

Secondary research sources included BIS certification databases, Ministry of Housing and Urban Affairs reports on PM Awas Yojana, DGCI&S trade statistics for cement board imports and exports, company annual reports, investor presentations, press releases, and industry association publications from the Building Materials & Technology Promotion Council (BMTPC).

Forecasting Models

Market forecasts employed top-down and bottom-up modeling, combining total India construction sector output projections, cement board penetration rates by application, segment-level adoption curves, regional housing start data, and macroeconomic variables including GDP growth, urbanization rates, and fixed capital formation in construction. Scenario analysis addressed policy implementation pace, raw material cost trajectories, and competitive substitution from gypsum and PVC panel segments.

India Cement Board Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Square Meters |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Fiber Cement Board (FCB), Wood Wool Cement Board (WWCB), Wood Strand Cement Board (WSCB), Cement Bonded Particle Board (CBPB) |

| Applications Covered | Flooring, Exterior and Partition Walls, Roofing, Columns and Beams, Facades, Weatherboard, and Cladding, Acoustic and Thermal Insulation, Others |

| End-User Industries Covered | Residential, Commercial, Industrial and Institutional |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Everest Industries Limited, Visaka Industries Limited, CKA Birla Group, Etex Group, Sahyadri Industries Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India cement board market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India cement board market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India cement board industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Cement Board Market Report

The India cement board market was valued at 21.86 Million Square Meters in 2025, driven by expanding residential and commercial construction activity, rising demand for fire-resistant panels, and growing green building adoption.

The market is projected to grow at 4.75% CAGR from 2026 to 2034, reaching 33.60 Million Square Meters, supported by urbanization, affordable housing programs, and tightening building safety standards across India.

Fiber cement board (FCB) leads at 46.8% share in 2025, driven by its versatility, lightweight nature, and wide adoption in external cladding, wet area walls, and facade systems across residential and commercial projects.

Residential construction leads at 48.2% share in 2025, fueled by urban housing demand, government affordable housing programs, and growing preference for moisture-resistant and fire-safe panel materials.

South India commands 33.4% in 2025, led by high construction activity, coastal climate-driven demand, and the presence of major manufacturers in Tamil Nadu, Karnataka, and Andhra Pradesh.

Leading players include Everest Industries Limited, Visaka Industries Limited, CKA Birla Group, Etex Group, and Sahyadri Industries Pvt. Ltd., among others.

GRIHA and IGBC green building certifications encourage the use of non-asbestos, low-emission building materials, driving substitution of traditional plywood and gypsum with cement boards across specification-grade residential and commercial projects.

Key challenges include higher upfront material costs versus gypsum and plywood alternatives, limited skilled installer availability in tier-2 and tier-3 markets, and distribution gaps outside major metro and Tier-1 construction hubs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)