India Circuit Breakers and Switches Market Size, Share, Trends and Forecast by Product Type, Voltage Rating, Distribution Channel, Application, and Region, 2026-2034

India Circuit Breakers and Switches Market Size, Share, Trends & Forecast (2026-2034)

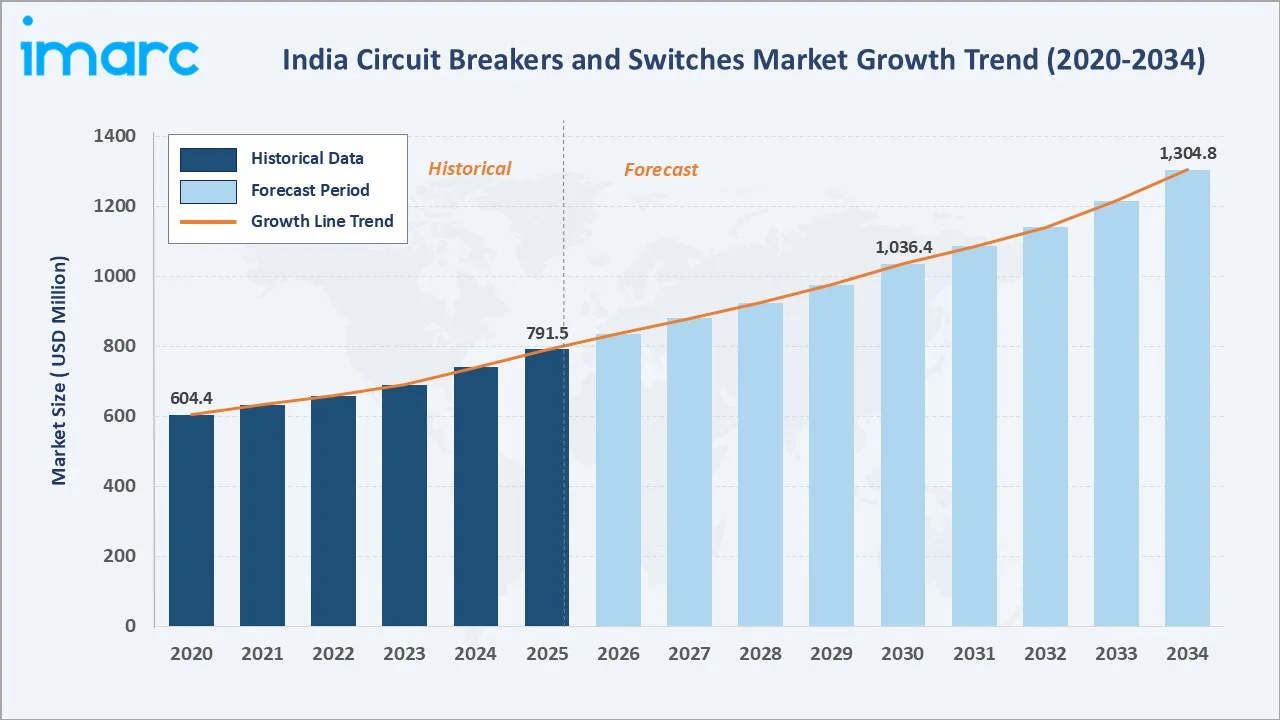

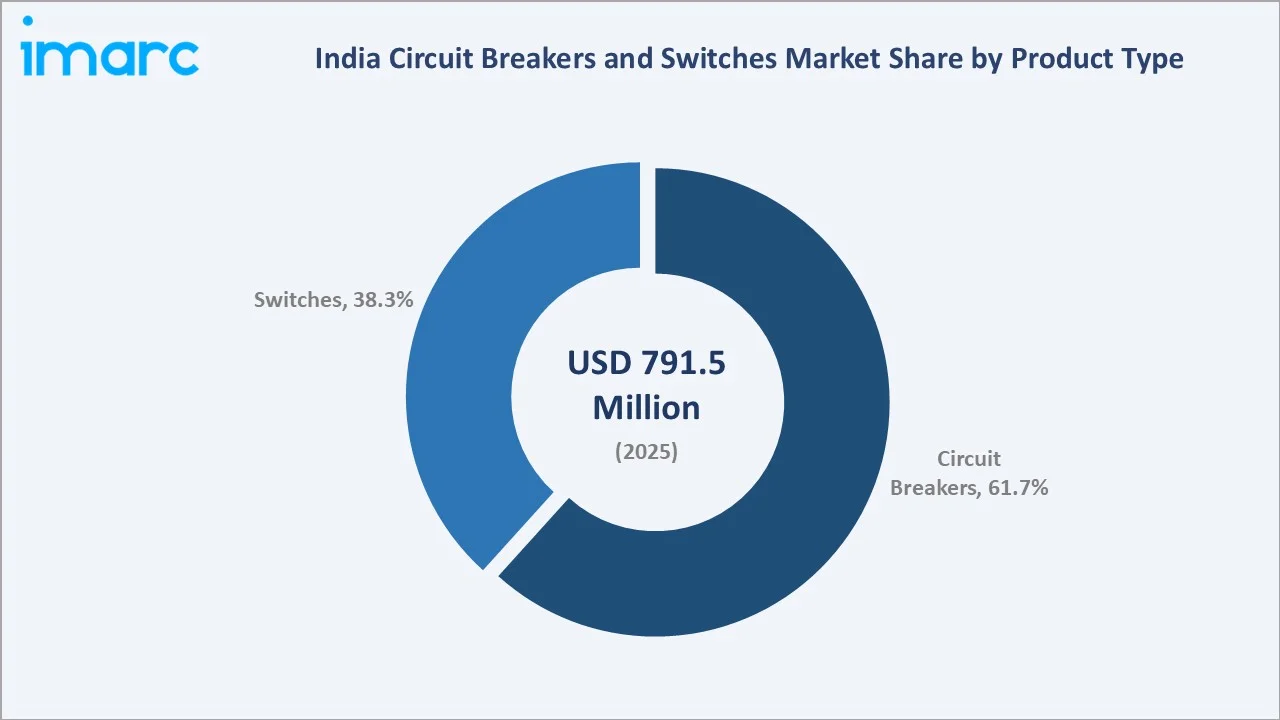

The India circuit breakers and switches market size reached USD 791.5 Million in 2025 and is projected to reach USD 1,304.8 Million by 2034, exhibiting a CAGR of 5.54% during 2026-2034. Expanding electricity demand, infrastructure investment, and renewable energy integration are the primary forces propelling market growth.

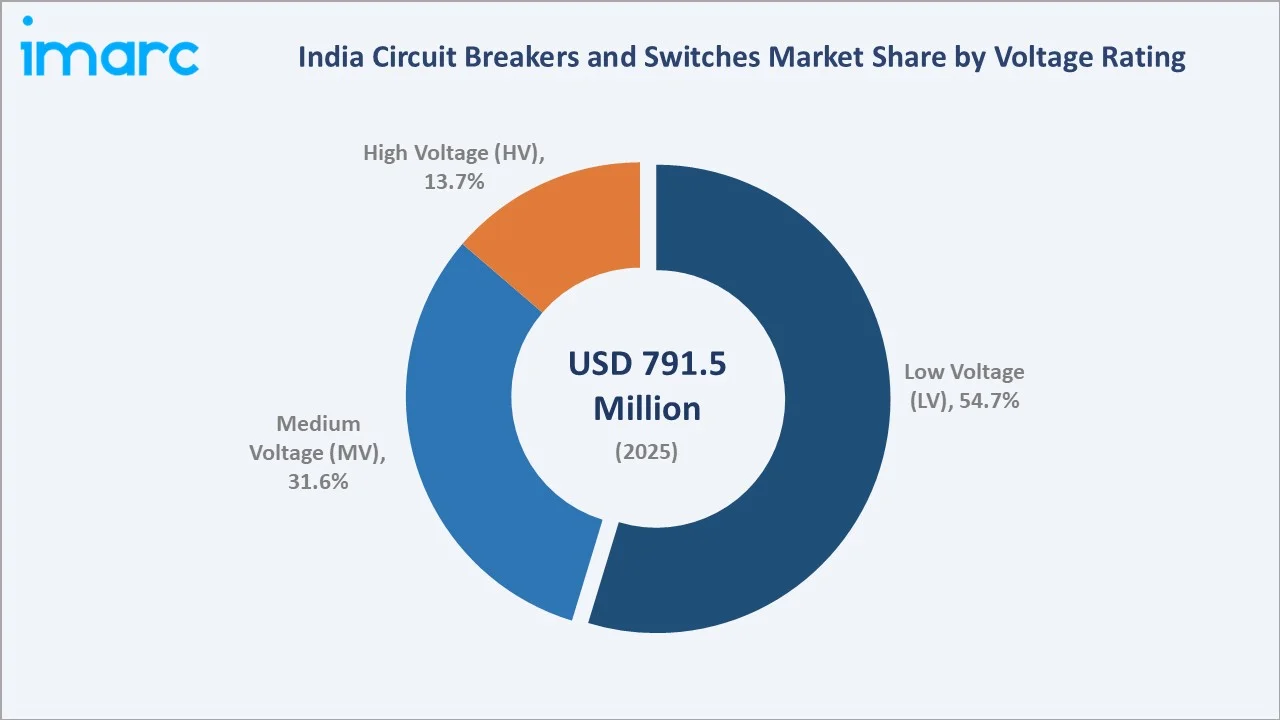

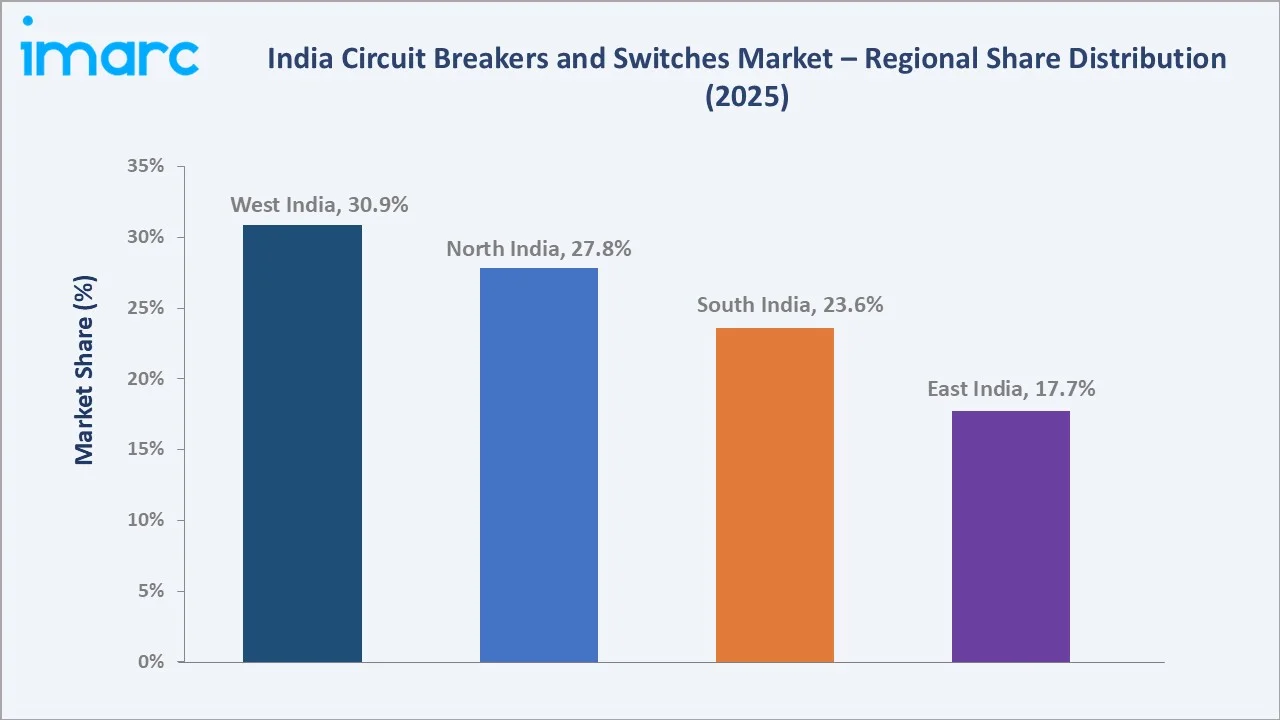

Circuit Breakers lead product-type segmentation at 61.7% in 2025, driven by grid modernisation and industrial safety standards. Within circuit breakers, Low Voltage (LV) commands a 54.7% share. West India dominates the regional landscape at 30.9%, underpinned by strong industrial and commercial activity.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 791.5 Million |

|

Forecast Market Size (2034) |

USD 1,304.8 Million |

|

CAGR (2026-2034) |

5.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Product Type |

Circuit Breakers (61.7% share, 2025) |

|

Leading Voltage Rating |

Low Voltage – LV (54.7% share, 2025) |

|

Leading Region |

West India (30.9% share, 2025) |

The India circuit breakers and switches market growth from 2020 through 2034 reflects consistent demand driven by power sector expansion, electrification initiatives, and industrial automation. The forecast to USD 1,304.8 Million by 2034 captures accelerating grid investment, renewable energy adoption, and growing electrical safety requirements across residential, commercial, and industrial segments in India.

To get more information on this market, Request Sample

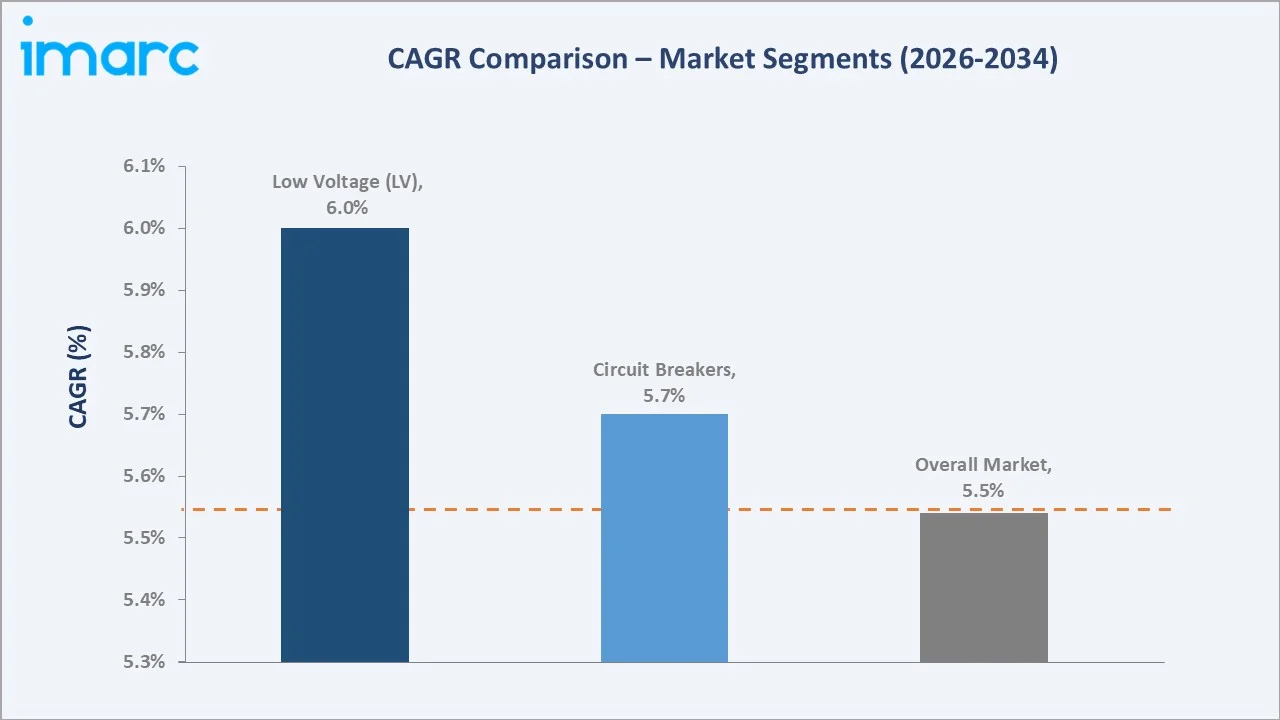

The CAGR trajectories across key product-type and voltage rating highlight Low Voltage (LV) circuit breakers at approximately 6.0% CAGR and circuit breakers overall at approximately 5.7% CAGR as the fastest-growing categories within the India circuit breakers and switches market through 2034.

Executive Summary

The India circuit breakers and switches market is on a sustained growth trajectory from USD 791.5 Million in 2025 to USD 1,304.8 Million by 2034. The market encompasses low, medium, and high-voltage circuit breakers and diverse switch types deployed across industrial, infrastructure, commercial, and residential sectors nationwide.

Circuit Breakers lead at 61.7% in 2025, driven by expanding grid networks, industrial safety compliance, and growing power distribution needs. Switches (38.3%) capture demand from smart automation, residential wiring, and load management across India’s rapidly urbanising landscape.

Within circuit breakers, Low Voltage (LV) commands 54.7% share in 2025, supported by residential electrification, commercial buildings, and light industrial applications. Medium Voltage (MV) holds 31.6%, while High Voltage (HV) accounts for 13.7%, driven by grid transmission infrastructure.

West India dominates at 30.9% in 2025, supported by Maharashtra and Gujarat’s industrial base. North India follows at 27.8%, South India at 23.6%, and East India at 17.7%, with the latter poised for accelerating growth driven by government electrification programmes.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Circuit Breakers – 61.7% share (2025) |

|

Leading Voltage Rating |

Low Voltage (LV) – 54.7% share (2025) |

|

Leading Region |

West India – 30.9% share (2025) |

|

Second Largest Region |

North India – 27.8% share (2025) |

|

Top Companies |

ABB, Siemens, Schneider Electric, Bharat Heavy Electricals Limited |

- Circuit Breakers: Circuit Breakers at 61.7% dominate because industrial plants, power distribution networks, and commercial buildings require reliable fault protection. Continuous demand for electrical safety, coupled with government grid upgrades, sustains capital investment in circuit breaker procurement across India.

- Low Voltage (LV): Low Voltage (LV) at 54.7% commands the voltage rating segment because residential electrification, commercial complexes, and light manufacturing facilities require widespread LV protection solutions. Rapid urbanisation and housing expansion are driving sustained LV circuit breaker deployment nationwide.

- West India: West India’s 30.9% regional dominance reflects Maharashtra and Gujarat’s unparalleled industrial and commercial electricity consumption. Strong manufacturing activity, port infrastructure, and large-scale real estate development are sustaining capital investment in circuit breakers and switches across the western corridor.

India Circuit Breakers and Switches Market Overview

The India circuit breakers and switches market encompasses low, medium, and high-voltage circuit breakers, plus isolators, load break switches, and smart switching devices serving industrial, infrastructure, commercial, and residential sectors. Market structure integrates equipment manufacturers, component suppliers, distributors, system integrators, and regulatory bodies ensuring electrical safety compliance.

The ecosystem integrates global and domestic equipment manufacturers, raw material and component suppliers, technology developers, regulatory agencies (BIS, CEA), power utilities, industrial end-users, and distribution partners serving diverse end-user segments across the Indian electrical infrastructure landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

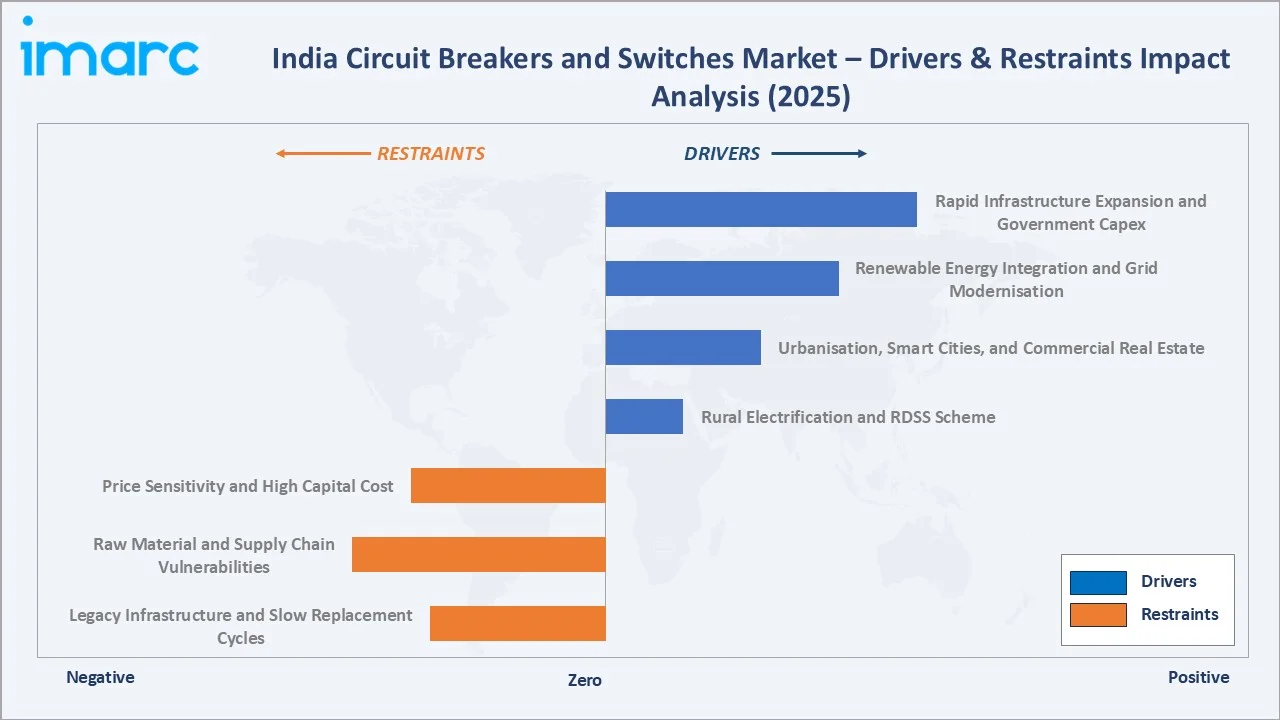

Market Drivers

- Rapid Infrastructure Expansion and Government Capex: Government infrastructure programmes including the National Infrastructure Pipeline and smart city missions are creating large-scale demand for circuit breakers and switches. Massive investments in power transmission, distribution upgrades, and electrification of underserved regions are directly stimulating procurement across all voltage categories.

- Renewable Energy Integration and Grid Modernisation: India’s renewable energy capacity expansion targets, including 500 GW of non-fossil energy by 2030, necessitate substantial investment in grid-compatible circuit breakers and switching equipment. Solar and wind plant connections require specialised protection devices supporting the growing renewable energy-linked electrical infrastructure.

- Urbanisation, Smart Cities, and Commercial Real Estate: Ongoing urbanisation, housing construction, and expansion of data centres, hospitals, and commercial buildings are driving sustained demand for low and medium-voltage circuit breakers. Smart city projects and commercial real estate development are accelerating electrical infrastructure investment across India’s urban clusters.

- Rural Electrification and RDSS Scheme Implementation: National electrification programmes including the Saubhagya scheme and Revamped Distribution Sector Scheme (RDSS) are expanding the addressable market for low-voltage circuit breakers and switches. Universal household electrification goals and rural distribution network upgrades are generating sustained procurement demand across state utilities.

Market Restraints

- Price Sensitivity and High Capital Cost: Premium circuit breakers and advanced switching equipment involve high upfront costs, limiting adoption among smaller industrial buyers and rural cooperatives. Price sensitivity in competitive procurement processes, particularly for public utility tenders, exerts margin pressure on manufacturers and constrains market penetration in cost-constrained segments.

- Raw Material and Supply Chain Vulnerabilities: Circuit breaker and switchgear manufacturing depends on steel, copper, and specialty electrical components, with supply chain disruptions increasing lead times and raising input costs. Global raw material volatility, import dependency for advanced components, and logistics constraints are creating procurement and production challenges for domestic manufacturers.

- Legacy Infrastructure and Slow Replacement Cycles: Many older industrial facilities and legacy residential installations rely on outdated electrical infrastructure that does not meet modern safety standards. Replacement cycles are slow due to cost and operational continuity concerns, limiting premium circuit breaker penetration in the installed base.

Market Opportunities

- Electric Vehicle Infrastructure and Energy Storage: India’s ambitious electric vehicle (EV) ecosystem expansion is creating demand for EV-compatible charging infrastructure switches and circuit protection devices. Grid integration of EV charging stations, battery storage systems, and distributed energy resources is generating a rapidly growing addressable market for specialised switching equipment manufacturers.

- Smart Grid and Digital Switchgear Adoption: Government mandates and utility procurement preferences for digital, IoT-enabled smart circuit breakers and switches are creating growth opportunities for technology-advanced manufacturers. Smart metering, predictive fault monitoring, and remote switching capabilities are gaining adoption in new grid investments and industrial automation deployments.

Market Challenges

- Regulatory Compliance and Certification Complexity: India’s electrical equipment sector is governed by Bureau of Indian Standards (BIS) certifications, Central Electricity Authority (CEA) regulations, and utility-specific procurement standards. Evolving regulatory frameworks and state-level variation in compliance requirements increase the cost and timeline for product qualification across diverse distribution channels.

- Intense Competitive Pressure from Global and Local Players: Indian manufacturers compete intensively with multinational players holding stronger technology and brand credentials, while also facing low-cost competition from imports. Balancing quality, compliance, and competitive pricing remains a persistent challenge across the LV and MV segments for both domestic and international manufacturers.

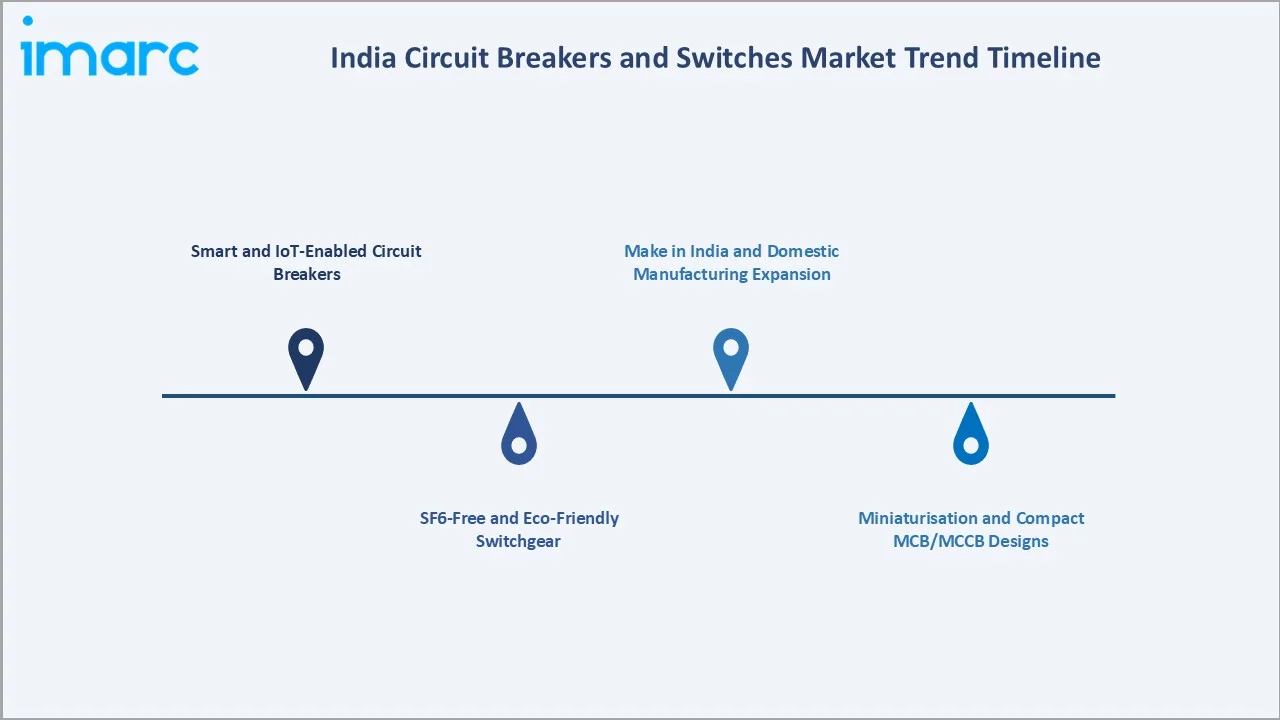

Emerging Market Trends

1. Smart and IoT-Enabled Circuit Breakers

Advanced IoT connectivity, remote monitoring, and automated fault detection are transforming circuit breaker capabilities in India. Smart circuit breakers with real-time diagnostics and predictive maintenance are gaining adoption in industrial facilities, data centres, and infrastructure projects prioritising operational efficiency and unplanned downtime reduction.

2. SF6-Free and Eco-Friendly Switchgear

Environmental concerns and international regulatory trends are driving Indian utilities and industrial buyers toward SF6-free and vacuum-based switchgear. Leading manufacturers are investing in alternative insulation technologies, positioning eco-friendly products for infrastructure tenders aligned with India’s sustainability and net-zero commitment goals.

3. Miniaturisation and Compact MCB/MCCB Designs

Growing demand for space-efficient electrical panels in urban residential projects and data centres is accelerating miniaturised MCB and MCCB development. Compact designs combining multi-pole protection and surge suppression in reduced footprints are increasingly specified in smart building electrical designs across Indian metro markets.

4. Make in India and Domestic Manufacturing Expansion

Government Production-Linked Incentive (PLI) schemes and Make in India policies are encouraging multinational and domestic manufacturers to expand local switchgear and circuit breaker production. Growing domestic manufacturing capacity is improving supply chain resilience, reducing import dependence, and enhancing competitiveness in government utility procurement tenders.

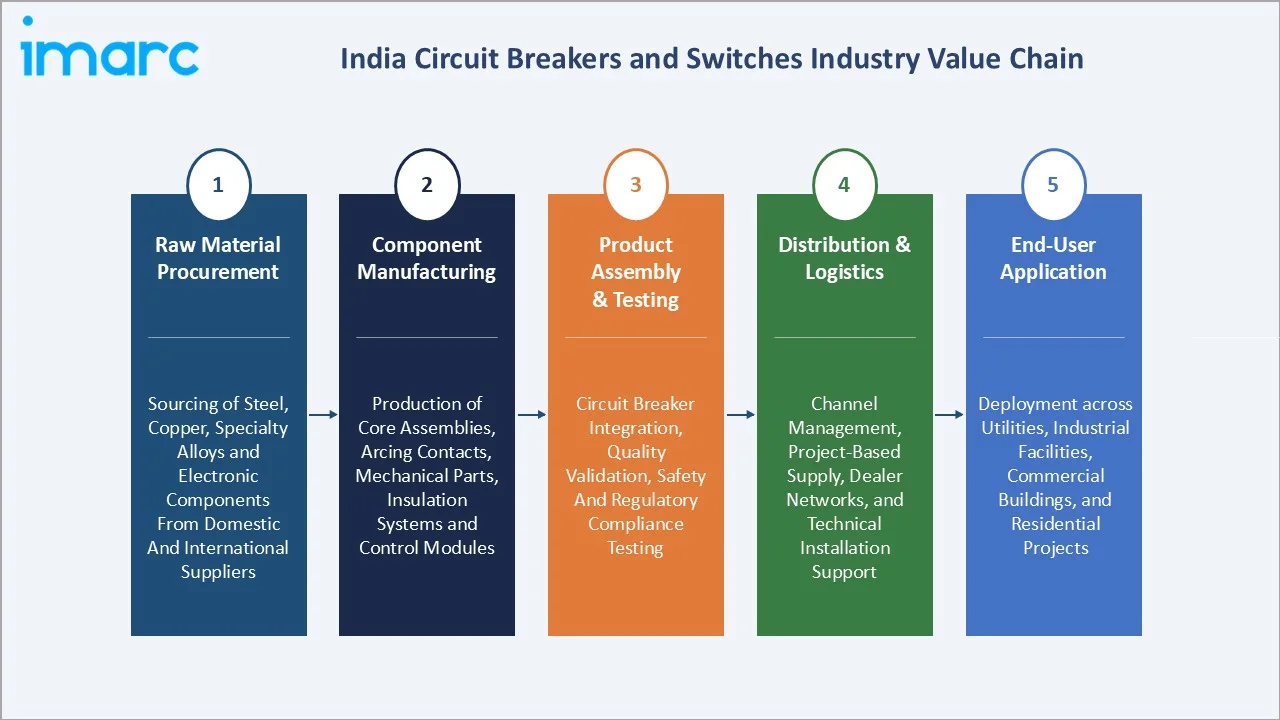

Industry Value Chain Analysis

The India circuit breakers and switches value chain spans five integrated stages from raw material sourcing through end-user installation. Equipment manufacturers capture primary value through product engineering and certification, while distribution networks and after-sales service generate recurring revenue streams supporting long-term customer relationships.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of key raw materials and electrical components from domestic and international suppliers |

|

Component Manufacturing |

Production of core assemblies, mechanical parts, insulation systems, and electronic control modules |

|

Product Assembly & Testing |

Circuit breaker and switch integration, regulatory certification, quality validation, and compliance testing |

|

Distribution & Logistics |

Channel management, project-based supply, dealer networks, and technical installation support |

|

End-User Application |

Deployment across utilities, industrial facilities, commercial buildings, and residential projects |

Product assembly and certification stages capture the highest value in the circuit breaker value chain, requiring engineering expertise, regulatory compliance capability, and sophisticated quality systems. After-sales service, spare parts, and preventive maintenance represent growing recurring revenue streams strengthening long-term customer retention for leading manufacturers.

Technology Landscape in the India Circuit Breakers and Switches Industry

Vacuum Circuit Breaker (VCB) Technology Advancement

Vacuum interrupter technology is gaining rapid adoption in medium-voltage applications due to superior arc extinction, minimal maintenance requirements, and extended service life. Advanced VCB designs are displacing older oil and air-blast circuit breakers across Indian utilities, industrial facilities, and renewable energy substations.

Digital and AI-Enabled Protection Relays

Integration of microprocessor-based and AI-enabled protection relays with circuit breakers is improving fault selectivity, reducing nuisance tripping, and enabling predictive maintenance. Smart relays with IEC 61850 communication protocols are being specified in new grid projects and industrial substation upgrades throughout India.

Solid-State and Hybrid Switching Technology

Solid-state switches and hybrid circuit breakers combining mechanical and electronic switching are emerging for high-frequency and high-speed fault interruption requirements. These technologies are finding application in data centre power distribution, EV charging infrastructure, and next generation microgrid projects across India.

Gas-Insulated Switchgear (GIS) Expansion

Gas-insulated switchgear adoption is growing in space-constrained urban substations and high-voltage transmission applications. GIS systems offer compact footprint, reduced maintenance cycles, and improved reliability in challenging environments, making them increasingly preferred for metro rail, airport, and high-density urban power distribution projects.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Circuit Breakers |

61.7% |

2025 |

|

Voltage Rating |

Low Voltage (LV) |

54.7% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West India |

30.9% |

2025 |

By Product Type

Circuit Breakers command a 61.7% majority share in 2025 owing to their essential role in fault protection, grid stability, and industrial safety across India’s expanding power infrastructure. Large-scale government investments in power transmission and distribution, combined with stringent electrical safety standards, are sustaining strong procurement of circuit breakers across all voltage categories.

To access detailed market analysis, Request Sample

Switches (38.3%) encompass isolators, load break switches, transfer switches, and smart switches supporting grid management, load balancing, and automated switching in power networks and industrial applications. Growing industrial automation, smart building adoption, and expansion of renewable energy farms are driving diversified switch procurement across India.

By Voltage Rating

Low Voltage (LV) voltage rating dominates at 54.7% in 2025, driven by the massive residential construction boom, commercial real estate growth, and light industrial expansion across Indian cities. MCBs, MCCBs, and ACBs are extensively deployed in buildings, factories, and infrastructure facilities, supported by ongoing housing electrification and smart city programmes.

Medium Voltage (MV) voltage rating hold 31.6%, serving industrial plants, substations, and renewable energy installations requiring 1 kV–36 kV protection. High Voltage (HV) at 13.7% is driven by transmission infrastructure, HVDC projects, and large power plant switchyards underpinning India’s national grid modernisation agenda.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Factors |

|

West India |

30.9% |

The region benefits from a strong industrial base, active commercial real estate investment, and robust power distribution infrastructure development. |

|

North India |

27.8% |

Rapid urban expansion, large-scale government infrastructure projects, and growing data centre development are key demand drivers in this region. |

|

South India |

23.6% |

Expanding manufacturing and technology sectors, coupled with renewable energy-linked grid investments, are driving circuit breaker and switch procurement. |

|

East India |

17.7% |

Government rural electrification programmes, expanding industrial zones, and infrastructure investment are supporting steady market growth in this region. |

West India’s 30.9% market dominance in 2025 is driven by Maharashtra and Gujarat’s concentration of large industrial facilities, power distribution investments, and major infrastructure projects. The region’s robust manufacturing sector, expanding ports, and active commercial real estate pipeline are sustaining strong circuit breaker and switch procurement from utilities and private developers.

North India, at 27.8% in 2025, is anchored by Delhi-NCR’s rapid urban expansion and government-led infrastructure corridor investments. South India at 23.6% maintains strong demand through IT parks and grid investment supporting renewable energy integration. East India at 17.7% is positioned for above-average growth driven by government electrification initiatives and industrial zone development.

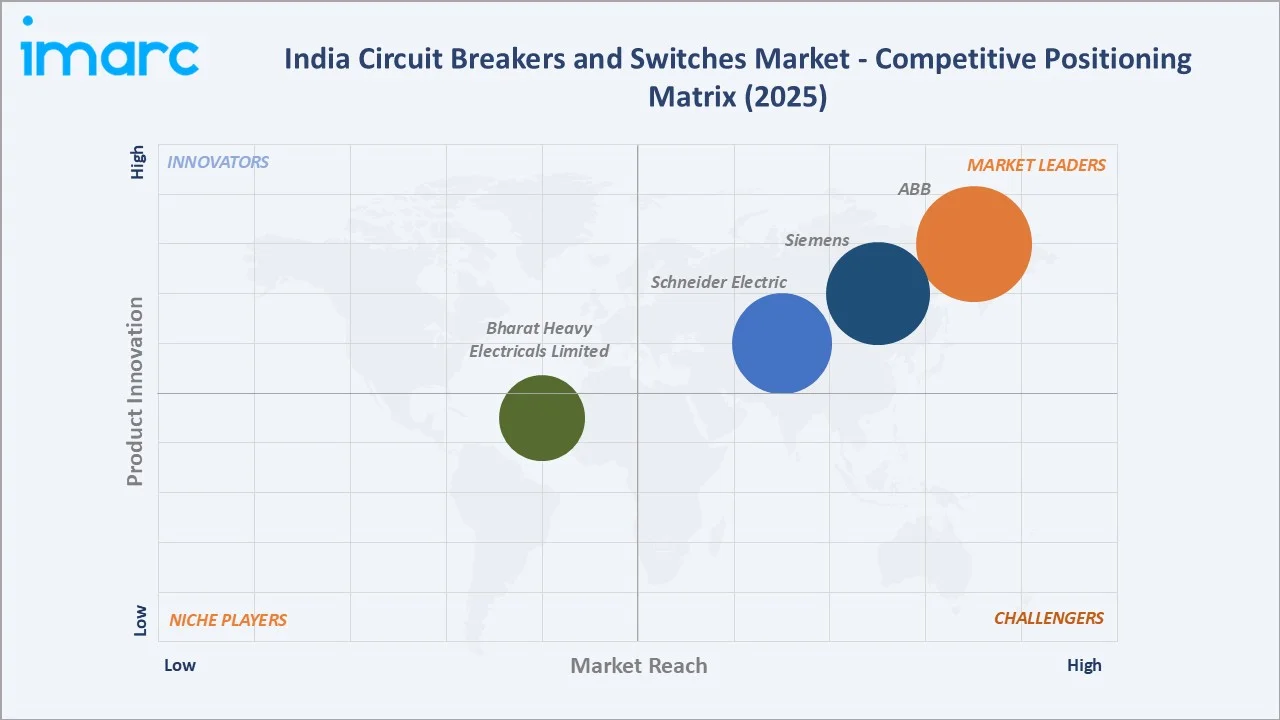

Competitive Landscape

The India circuit breakers and switches market is moderately concentrated, with global majors and established domestic players collectively commanding significant market shares. International manufacturers leverage technological expertise, certification capabilities, and service networks, while domestic leaders leverage local manufacturing, distribution reach, and government procurement relationships.

|

Company Name |

Key Products / Operations |

Market Position |

Strategic Focus |

|

ABB |

Emax 3, Emax 2, Tmax XT, Tmax T, Ekip UP, Manual operated switch fuses, Manual transfer switches, Manual operated bypass switches |

Leader |

Advancing digital switchgear; expanding SF6-free product portfolio for Indian utilities |

|

Siemens |

Sinova (retail MCBs/RCCBs), 3VA (MCCBs), SENTRON series |

Leader |

Promoting smart grid solutions; scaling local manufacturing under Make in India |

|

Schneider Electric |

Miniature circuit breaker, Residual Current Circuit Breaker, AvatarON, Clipsal X, Livia, Miluz Lara |

Leader |

Expanding EcoStruxure digital infrastructure; targeting renewable energy grid projects |

|

Bharat Heavy Electricals Limited |

Outdoor Vacuum Circuit Breakers |

Established |

Government utility partner; expanding GIS and smart grid equipment manufacturing |

Key players include ABB, Siemens, Schneider Electric, Bharat Heavy Electricals Limited, and others.

Key Company Profiles

ABB

ABB is a leading electrification and automation technology company offering comprehensive circuit breaker and switchgear solutions across low, medium, and high-voltage applications for Indian utilities, industries, and infrastructure projects.

- Product Portfolio: Emax 3, Emax 2, Tmax XT, Tmax T, Ekip UP, Manual operated switch fuses, Manual transfer switches, Manual operated bypass switches

- Strategic Focus: ABB is executing a dual strategy of expanding smart digital circuit breaker capabilities through its ABB Ability platform while advancing SF6-free switchgear solutions for Indian utility tenders. The company is investing in local manufacturing and deepening service coverage in Tier-2 and Tier-3 industrial cities.

Siemens

Siemens is a global engineering leader providing electrification, automation, and digitalisation solutions across India, offering a comprehensive range of circuit breakers, switchgear, and protection equipment for power, industrial, and infrastructure sectors.

- Product Portfolio: Sinova (retail MCBs/RCCBs), 3VA (MCCBs), SENTRON series

- Strategic Focus: Siemens India is focused on advancing smart switchgear integration with SCADA and energy management platforms, scaling local manufacturing under Make in India incentives, and deepening its presence in renewable energy substation and industrial automation projects.

Schneider Electric

Schneider Electric is a multinational leader in energy management and automation specialising in intelligent switchgear, circuit protection, and power distribution solutions for buildings, industry, data centres, and grid infrastructure across India.

- Product Portfolio: Miniature circuit breaker, Residual Current Circuit Breaker, AvatarON, Clipsal X, Livia, Miluz Lara

- Strategic Focus: Schneider Electric India is focused on expanding its EcoStruxure digital infrastructure framework across industrial, buildings, and grid segments, targeting renewable energy project developers and smart city infrastructure programmes, while advancing SF6-free switchgear to meet sustainability mandates.

Market Concentration Analysis

The India circuit breakers and switches market is moderately concentrated, with multinational leaders ABB, Siemens, and Schneider Electric holding significant shares through advanced technology portfolios, broad distribution, and strong utility relationships.

At the voltage segment level, the LV circuit breaker category is most competitive, with numerous domestic MCB and MCCB manufacturers competing alongside multinationals. MV and HV segments are more concentrated, with global OEMs and BHEL dominating government utility tenders through technical certification, project delivery capability, and established track records.

Investment & Growth Opportunities

Fastest-Growing Segments

Low Voltage (LV) circuit breakers represent the highest-growth segment through 2034 at approximately 6.0% CAGR, capturing rising demand from residential electrification, commercial construction, and industrial automation. Smart switches and IoT-enabled circuit breakers are positioned as the fastest-growing product innovation category within the India market.

Emerging Markets

East India and Tier-2/Tier-3 cities across all regions are emerging as significant investment frontiers. Government RDSS investments, industrial corridor development, and accelerating rural electrification are driving circuit breaker and switch procurement in traditionally underpenetrated geographies, creating new distribution and manufacturing opportunities.

Venture & Investment Trends

Private equity and strategic investors are increasing capital allocation to Indian switchgear manufacturers, smart grid technology firms, and digital protection system developers. Government PLI incentives for electrical equipment manufacturing are catalysing capacity expansion investments from both domestic players and multinational companies committing to local production.

Future Market Outlook (2026-2034)

The India circuit breakers and switches market is forecast to expand from USD 791.5 Million in 2025 to USD 1,304.8 Million by 2034 at a CAGR of 5.54%, driven by power sector investment, renewable energy integration, and sustained urbanisation across India’s rapidly growing economy through the forecast horizon.

Three structural forces will shape the market through 2034: power grid modernisation and the Revamped Distribution Sector Scheme will sustain demand for LV and MV circuit breakers; renewable energy capacity expansion will drive specialised switching equipment procurement; and industrial automation and smart building adoption will accelerate demand for intelligent, connected switchgear across all market segments.

Research Methodology

Primary Research

Primary research encompassed structured interviews with circuit breaker and switch manufacturers, power utility procurement managers, electrical contractors, and regulatory compliance specialists. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the India circuit breakers and switches market.

Secondary Research

Key secondary sources include Bureau of Indian Standards (BIS) certification databases, Central Electricity Authority (CEA) annual reports, Ministry of Power publications, industry association reports, company annual reports, trade publications, and market intelligence databases covering the Indian electrical equipment sector.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating India power sector investment plans, grid capacity data, housing construction statistics, and regional economic growth projections. Scenario modelling encompassed base, optimistic, and conservative cases through the 2034 horizon.

India Circuit Breakers and Switches Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Voltage Ratings Covered | Low Voltage (Up to 1 kV), Medium Voltage (1 kV–36 kV), High Voltage (Above 36 kV) |

| Distribution Channels Covered | Direct Sales, Retail Distributors, Online Platforms |

| Applications Covered | Residential, Commercial, Industrial, Utilities |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | ABB, Siemens, Schneider Electric, Bharat Heavy Electricals Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India circuit breakers and switches market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India circuit breakers and switches market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India circuit breakers and switches industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Circuit Breakers and Switches Market Report

The India circuit breakers and switches market reached USD 791.5 Million in 2025, reflecting sustained demand driven by power sector expansion, infrastructure investment, government electrification programmes, and growing industrial and commercial electricity consumption across India.

The market is projected to reach USD 1,304.8 Million by 2034, growing at a CAGR of 5.54% during 2026-2034, driven by renewable energy integration, smart grid investment, urbanisation, industrial automation, and the Revamped Distribution Sector Scheme (RDSS) implementation.

Circuit Breakers lead the market with a 61.7% share in 2025, driven by grid protection requirements, industrial safety standards, and large-scale power infrastructure investment. This segment is expected to maintain its leadership through 2034 as India’s electricity demand continues to grow.

Low Voltage (LV) circuit breakers command the largest share at 54.7% in 2025. Rising residential construction, commercial real estate growth, and light industrial expansion are sustaining LV circuit breaker deployment, with MCBs and MCCBs extensively specified across India’s rapidly urbanising markets.

West India dominates with a 30.9% share in 2025, underpinned by Maharashtra and Gujarat’s strong industrial base, port infrastructure, commercial real estate activity, and power distribution investments. The region is expected to maintain its leadership through the 2034 forecast horizon.

Key market drivers include rapid infrastructure expansion under the National Infrastructure Pipeline, renewable energy integration and grid modernisation, rural electrification through RDSS, urbanisation and smart city programmes, and growing demand for electrical safety solutions across residential, commercial, and industrial sectors.

Major challenges include price sensitivity limiting adoption among smaller buyers, raw material and supply chain vulnerabilities, slow replacement cycles in legacy installations, stringent regulatory compliance requirements, and intense competitive pressure from global multinationals and low-cost imports.

Leading companies include ABB, Siemens, Schneider Electric, Bharat Heavy Electricals Limited, and others.

Key emerging technologies include IoT-enabled smart circuit breakers with remote monitoring, SF6-free and vacuum-based eco-friendly switchgear, solid-state and hybrid switching for EV and energy storage applications, digital protection relays with AI-based fault prediction, and Gas-Insulated Switchgear (GIS) for compact urban substation deployment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)