India Clean Technology Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Clean Technology Market Summary:

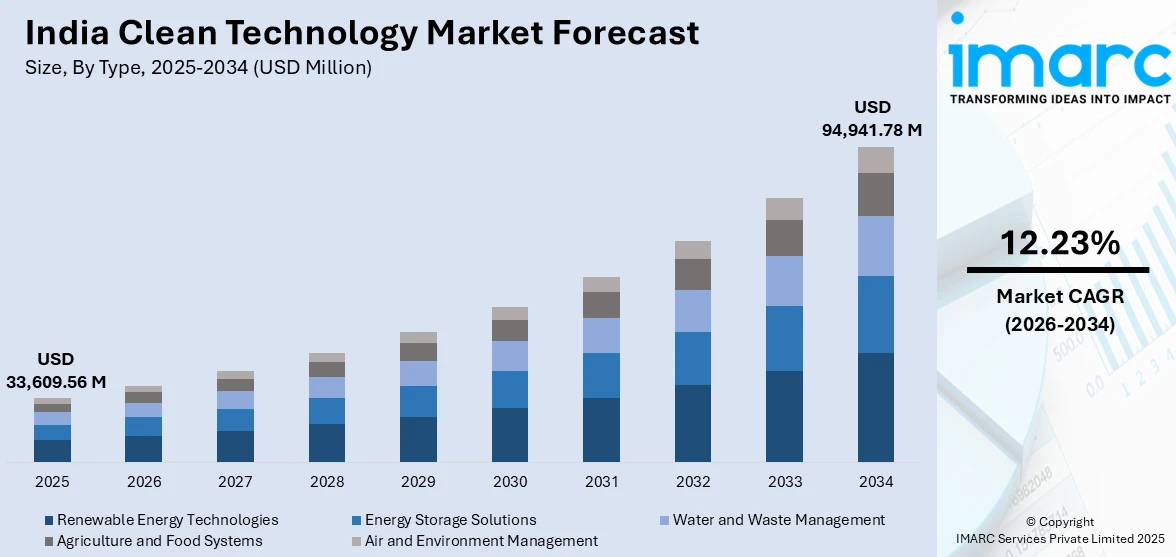

The India clean technology market size was valued at USD 33,609.56 Million in 2025 and is projected to reach USD 94,941.78 Million by 2034, growing at a compound annual growth rate of 12.23% from 2026-2034.

India's clean technology market is experiencing transformative growth driven by ambitious government renewable energy targets, accelerating industrial decarbonization initiatives, and substantial domestic and foreign investments in sustainable infrastructure. India’s commitment to expanding non-fossil fuel energy capacity and achieving net-zero emissions is accelerating the adoption of renewable energy, energy storage, and advanced water and waste management solutions across residential, commercial, and industrial sectors. These efforts are strengthening India’s position as a global leader in clean technology innovation and market growth.

Key Takeaways and Insights:

- By Type: Renewable energy technologies dominate the market with a share of 68.0% in 2025, driven by aggressive solar and wind capacity additions under the 500 GW non-fossil target, supported by policy incentives including Production Linked Incentive schemes for domestic solar module manufacturing and viability gap funding for hybrid renewable projects.

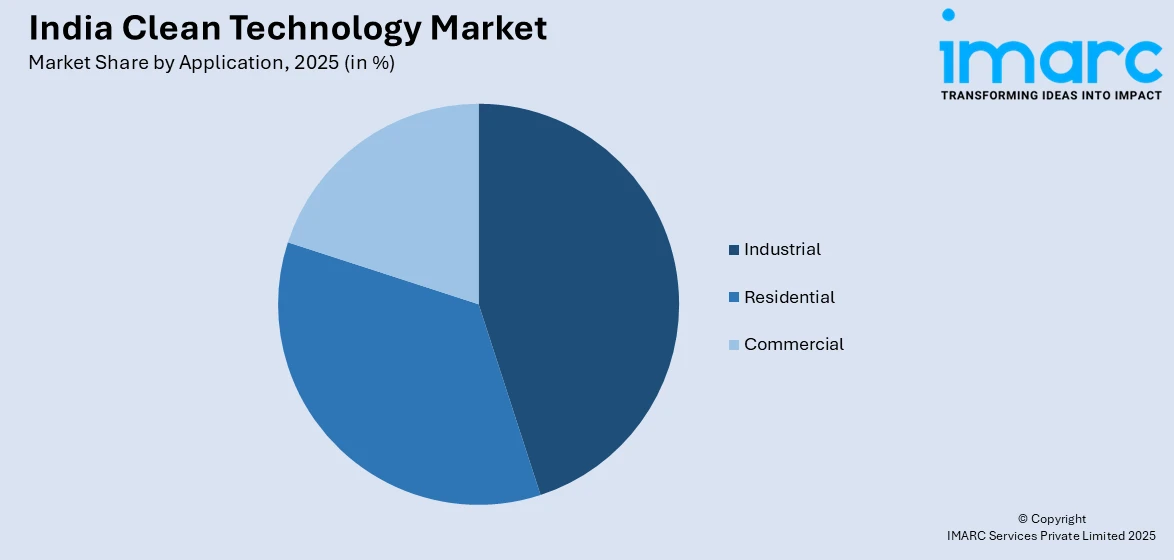

- By Application: Industrial leads the market with a share of 33.2% in 2025, as manufacturing facilities adopt clean technologies to meet corporate sustainability goals, comply with environmental regulations, and leverage cost savings from renewable power procurement and energy efficiency improvements.

- By Region: South India dominates the market in 2025, driven by strong renewable policies, rich solar and wind resources, rising power demand, industrial growth, and increasing investment in sustainable energy solutions.

- Key Players: The India clean technology market exhibits a moderately fragmented competitive landscape, with established energy conglomerates, specialized renewable developers, and emerging technology providers competing across segments. Market participants are pursuing vertical integration strategies, strategic partnerships, and capacity expansion to capture growing demand across utility-scale and distributed clean energy solutions.

To get more information on this market Request Sample

India's clean technology sector is undergoing an unprecedented transformation as the nation accelerates its energy transition journey. The government's comprehensive policy framework, including the National Green Hydrogen Mission with an outlay of Rs. 19,744 crore and the PM Surya Ghar Muft Bijli Yojana targeting one crore rooftop solar installations, is catalyzing market expansion across all segments. For instance, in FY 2024-25, India achieved a record renewable energy capacity addition of 29.52 GW, bringing total installed capacity to 220.10 GW, while solar module manufacturing capacity nearly doubled from 38 GW to 74 GW within a single year. The convergence of declining technology costs, particularly in solar photovoltaic systems and lithium-ion batteries, with strengthening regulatory mandates is creating favorable conditions for sustained market growth through the forecast period. Additionally, rising private-sector investments, expanding domestic manufacturing ecosystems, and increasing corporate commitments to decarbonization are further reinforcing India’s position as one of the fastest-growing clean technology markets globally.

India Clean Technology Market Trends:

Rapid Scale-Up of Solar and Wind Energy Infrastructure

India is witnessing unprecedented growth in utility-scale renewable energy infrastructure as developers commission mega solar parks and wind farms across resource-rich states. The solar segment recorded 23.83 GW capacity additions in FY 2024-25 alone, representing a significant increase over prior years, while wind capacity reached 51.5 GW. For instance, in September 2025, the Khavda Renewable Energy Park in Gujarat, spanning 538 square kilometers, is operational with over 8 GW capacity and is positioned to become the world's largest renewable energy facility upon completion by 2029, demonstrating India's capability to execute large-scale clean energy projects.

Battery Energy Storage System Deployment Acceleration

Grid-scale battery energy storage is becoming an essential pillar of India’s clean technology ecosystem as rising renewable energy integration increases the need for flexible and reliable grid management solutions. Energy storage systems are increasingly being adopted to support grid stability, balance supply and demand, and enhance the reliability of intermittent renewable sources. Improving project economics and growing policy support are encouraging wider deployment of large-scale battery installations, strengthening their role in enabling a resilient and efficient low-carbon power system. For instance, in the first quarter of 2025 alone, eleven standalone energy storage tenders totaling 6.125 GW were issued, exceeding entire 2024 issuance volumes, supported by the Viability Gap Funding scheme offering up to 30% capital cost subsidy for qualifying projects.

Green Hydrogen Ecosystem Development

The National Green Hydrogen Mission is accelerating India's transition toward hydrogen-based industrial decarbonization, targeting production of five million tonnes of green hydrogen by 2030. The government has allocated 3,000 MW electrolyser manufacturing capacity and approved 8.6 lakh tonnes per annum of green hydrogen production under initial program tranches. For instance, industrial clusters in Odisha, Gujarat, and Andhra Pradesh are emerging as green hydrogen hubs, with integrated infrastructure development including high-voltage substations and advanced water treatment facilities to support electrolyser operations.

Market Outlook 2026-2034:

The India clean technology market is set for strong growth as the country advances its transition toward non-fossil energy sources. Achieving long-term capacity expansion goals is driving sustained investment across renewable power generation, energy storage solutions, and grid modernization. Strong backing from public sector financial institutions is reinforcing investor confidence and enabling large-scale project development. This institutional support, combined with supportive policies and rising private sector participation, is creating a stable and attractive environment for clean technology adoption, positioning the market for continued expansion over the forecast period. The market generated a revenue of USD 33,609.56 Million in 2025 and is projected to reach a revenue of USD 94,941.78 Million by 2034, growing at a compound annual growth rate of 12.23% from 2026-2034.

India Clean Technology Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Renewable Energy Technologies |

68.0% |

|

Application |

Industrial |

33.2% |

Type Insights:

- Renewable Energy Technologies

- Energy Storage Solutions

- Water and Waste Management

- Agriculture and Food Systems

- Air and Environment Management

Renewable energy technologies dominate with a market share of 68.0% of the total India clean technology market in 2025.

Renewable energy technologies encompass solar photovoltaic systems, wind power installations, hydroelectric generation, and biomass-based power solutions that collectively form the foundation of India's clean technology sector. The segment's dominance reflects the government's sustained focus on achieving 500 GW of non-fossil fuel capacity by 2030, supported by comprehensive policy frameworks including the National Solar Mission, wind power development programs, and renewable purchase obligations mandating minimum clean energy procurement by distribution utilities.

Solar power has emerged as the primary growth driver within this segment, with installed capacity reaching 105.65 GW by March 2025, positioning India as the world's third-largest solar energy producer. India’s clean technology manufacturing base has strengthened significantly, with rapid expansion in domestic solar module production reducing reliance on imports and improving supply chain resilience. At the same time, wind energy development has gained momentum, supported by favorable geographic conditions and supportive policy measures. Growing investments in both onshore and emerging offshore wind projects are reinforcing the role of wind power as a key contributor to the country’s renewable energy mix.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

Industrial leads with a share of 33.2% of the total India clean technology market in 2025.

Industrial applications represent the largest demand segment for clean technologies as manufacturing facilities, heavy industries, and processing plants accelerate their sustainability transformations. Corporate sustainability commitments, environmental compliance requirements, and economic benefits from renewable power procurement are driving widespread adoption of clean energy solutions across India's industrial landscape, particularly in energy-intensive sectors including steel, cement, chemicals, and textiles.

The industrial segment benefits from favorable commercial and industrial renewable energy procurement policies, allowing direct power purchase agreements with renewable generators. For instance, major industrial conglomerates are establishing dedicated renewable energy portfolios to power manufacturing operations, with companies like ArcelorMittal partnering with renewable developers for round-the-clock clean power supply. The Green Steel Mission launched in December 2024 and emerging green hydrogen applications in steel and fertilizer production are expected to further accelerate industrial clean technology adoption through the forecast period.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates the total India clean technology market in 2025.

South India is a major driver of the clean technology market due to its abundant solar and wind resources, particularly in states with strong natural potential and established renewable corridors. Well-developed transmission infrastructure and early adoption of renewable energy policies have enabled large-scale deployment of solar and wind projects. Industrial demand for clean power and the presence of renewable energy parks further support capacity expansion, making the region a hub for utility-scale and distributed clean energy solutions.

The region benefits from a growing clean technology manufacturing ecosystem, including solar modules, wind components, and energy storage systems. Supportive state-level policies, investment incentives, and skilled labor availability have encouraged domestic manufacturing and technology innovation. In addition, strong private sector participation and increasing corporate commitments to renewable energy procurement are accelerating adoption. These factors collectively position South India as a key growth engine for India’s clean technology market.

Market Dynamics:

Growth Drivers:

Why is the India Clean Technology Market Growing?

Comprehensive Government Policy Support and Renewable Energy Targets

India's clean technology market is experiencing accelerated growth driven by comprehensive government policy frameworks targeting ambitious renewable energy and sustainability objectives. The nation's commitment to achieving 500 GW of non-fossil fuel-based electricity capacity by 2030, coupled with net-zero emissions by 2070, provides a clear directional mandate for market expansion. Policy instruments including the Production Linked Incentive scheme for high-efficiency solar modules with an allocation of Rs. 19,500 crore, waiver of inter-state transmission charges for renewable energy, and Renewable Purchase Obligations mandating minimum clean energy procurement, are creating favorable conditions for investment. For instance, India achieved 51% of total installed power capacity from non-fossil fuel sources by September 2025, reaching this milestone five years ahead of its Paris Agreement commitment, demonstrating effective policy implementation.

Declining Technology Costs and Improving Economic Competitiveness

Falling costs across key clean technology segments are improving economic viability and accelerating adoption across multiple sectors. Declining prices of solar photovoltaic systems have made renewable power generation increasingly competitive, while lower battery costs are enhancing the feasibility of energy storage for grid and commercial use. Improved project economics are also evident in large-scale energy storage deployment, supporting wider integration of renewables. As a result, clean energy solutions are increasingly offering cost advantages over conventional power sources, encouraging adoption by industrial and commercial users beyond regulatory requirements.

Surging Investment Flows and Corporate Sustainability Commitments

The India clean technology market is benefiting from unprecedented investment flows from both domestic and international sources, complemented by strengthening corporate sustainability commitments driving clean energy procurement. Foreign direct investment in renewable energy has grown substantially, reaching approximately 8% of total FDI inflows in FY 2024-25 compared to just 1% in FY 2020-21, while public sector financial institutions have deployed around Rs. 2.68 trillion for renewable energy projects in FY 2024-25 alone. Growing corporate commitments to renewable energy procurement and carbon reduction goals are driving strong growth in the commercial and industrial segment. Large companies are increasingly entering long-term power procurement arrangements to secure clean and reliable energy supplies. At the same time, major investments in large-scale renewable projects across multiple regions are strengthening generation capacity and supporting corporate sustainability strategies, reinforcing the role of private sector participation in expanding India’s clean technology market.

Market Restraints:

What Challenges the India Clean Technology Market is Facing?

Grid Infrastructure and Transmission Capacity Constraints

The development of Indian renewable energy is increasing faster than the development of transmission infrastructure, which leads to grid overload and constriction in the ability to evacuate renewable-abundant states. Poor transmission corridors between states and the capacity of substations are leading to the curtailment of renewable generation, as well as the postponement of commissioning of projects, as developers await grid connection clearance. The mismatch of timelines of the renewable capacity additions with the extended time it takes to build the transmission lines continues to challenge the development of the market.

High Capital Investment Requirements and Financing Challenges

Clean technology projects involve huge initial capital investments, which pose a problem in financing, especially for emerging technologies and small market players. High borrowing costs relative to global standards increase project development expenses, while longer development cycles for capital-intensive clean technology solutions may not align with conventional venture capital return expectations. These financing constraints can limit market expansion beyond well-capitalized corporate developers.

Supply Chain Dependencies and Domestic Manufacturing Gaps

Despite progress in domestic manufacturing, India's clean technology sector maintains significant import dependencies for critical components including advanced battery cells, specialized semiconductors, and certain renewable energy equipment. Supply chain vulnerabilities, including raw material availability and geopolitical factors affecting component sourcing, can impact project costs and execution timelines. First-generation domestic manufacturing facilities may operate at lower cost efficiencies compared to established international suppliers until achieving production scale.

Competitive Landscape:

The India clean technology market exhibits a moderately fragmented competitive structure with large integrated energy conglomerates, specialized renewable energy developers, and emerging technology providers competing across market segments. Major players are pursuing vertical integration strategies encompassing equipment manufacturing, project development, and power generation to capture value across the clean energy chain. The market demonstrates increasing consolidation as established players acquire capacity and technology capabilities. Strategic partnerships between domestic developers and international technology providers are expanding, enabling access to advanced solutions and project financing. Competition is intensifying in emerging segments including battery energy storage and green hydrogen, with new entrants positioning for growth opportunities created by supportive policy frameworks and expanding market demand.

Recent Developments:

- November 2025: ReNew Energy Global announced an investment of Rs. 60,000 crore (approximately USD 6.7 billion) in Andhra Pradesh to establish multiple green energy projects, including solar plants, wind facilities, and battery energy storage systems, marking one of the largest single-state clean energy investment commitments in India.

- September 2025: Adani Group announced plans to invest USD 21 billion in India's renewable energy sector, with Adani Green Energy Limited targeting renewable capacity expansion to 50 GW by FY 2030 through solar, wind, and hybrid power projects across multiple states.

- February 2025: Emmvee Group, a Bengaluru-based solar photovoltaic panel manufacturer, announced an investment of Rs. 15,000 crore (approximately USD 1.7 billion) to establish a new manufacturing facility in Bengaluru, expected to create 10,000 jobs and strengthen domestic solar module supply chains.

India Clean Technology Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Renewable Energy Technologies, Energy Storage Solutions, Water and Waste Management, Agriculture and Food Systems, Air and Environment Management |

|

Applications Covered |

Residential, Commercial, Industrial |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Clean Technology Market Report

The India clean technology market size was valued at USD 33,609.56 Million in 2025.

The India clean technology market is expected to grow at a compound annual growth rate of 12.23% from 2026-2034 to reach USD 94,941.78 Million by 2034.

Renewable energy technologies dominated the India clean technology market with a share of 68.0% in 2025, driven by aggressive solar and wind capacity additions under the government's 500 GW non-fossil target, supported by policy incentives and Production Linked Incentive schemes.

Key factors driving the India clean technology market include comprehensive government policy support with ambitious renewable energy targets, declining technology costs improving economic competitiveness, surging investment flows from domestic and international sources, and strengthening corporate sustainability commitments driving clean energy adoption.

Major challenges include grid infrastructure and transmission capacity constraints limiting renewable energy evacuation, high capital investment requirements creating financing barriers particularly for emerging technologies, supply chain dependencies on imported critical components, and regulatory uncertainties affecting project planning and execution timelines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)