India Cloud Gaming Market Size, Share, Trends and Forecast by Type, Device, Gamer Type, and Region, 2026-2034

India Cloud Gaming Market Summary:

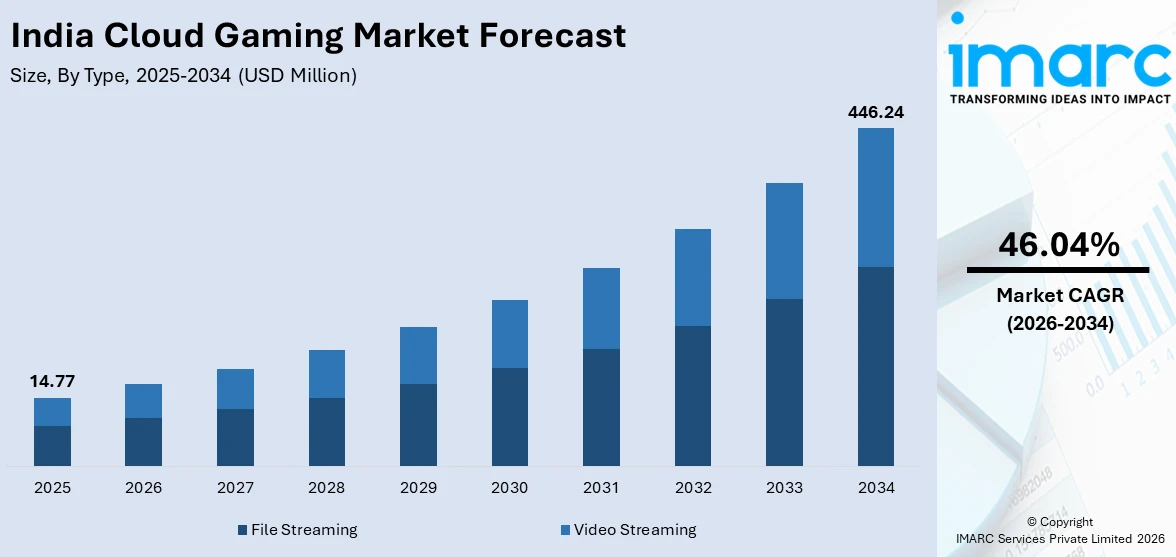

The India cloud gaming market size was valued at USD 14.77 Million in 2025 and is projected to reach USD 446.24 Million by 2034, growing at a compound annual growth rate of 46.04% from 2026-2034.

The India cloud gaming market is gaining strong momentum as the country's rapidly expanding digital infrastructure and growing gaming culture drive widespread adoption of cloud-based gaming solutions. Increasing internet connectivity, rising smartphone penetration, and the proliferation of affordable data plans are enabling seamless access to high-quality gaming experiences without dedicated hardware, positioning India as a key growth hub for India cloud gaming market share.

Key Takeaways and Insights:

- By Type: File streaming dominates the market with a share of 44% in 2025, owing to its ability to deliver high-fidelity gaming experiences with reduced latency and broader title compatibility across diverse device categories and network environments.

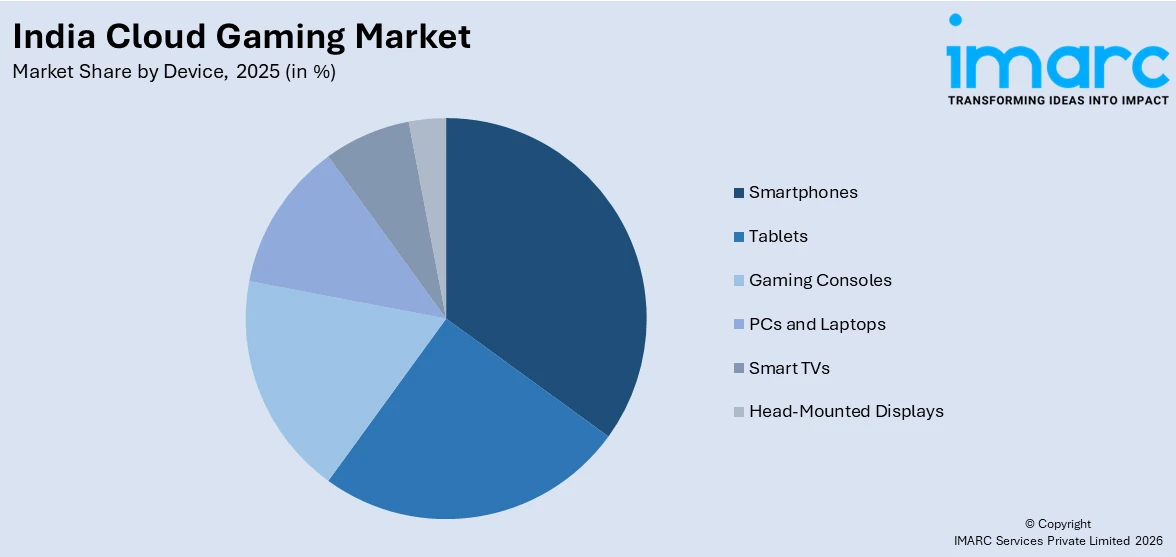

- By Device: Smartphones lead the market with a share of 30% in 2025, driven by widespread affordable handset adoption, extensive mobile internet coverage, and the strong preference for on-the-go gaming among young demographics.

- By Gamer Type: Casual gamers hold the biggest share at 48% in 2025, reflecting the appeal of accessible, easy-to-play cloud gaming titles that attract a broad demographic including first-time and occasional players across diverse age groups.

- By Region: North India is the largest region with 28% share in 2025, supported by robust digital infrastructure, high population density, and the concentration of technology-savvy consumers in major metropolitan clusters.

- Key Players: Leading players in the India cloud gaming market are strengthening their positions by expanding platform capabilities, forging telecom partnerships, enhancing content libraries, and investing in regional data center infrastructure to improve service delivery and broaden consumer accessibility.

To get more information on this market Request Sample

The India cloud gaming market is advancing as a burgeoning gaming population, infrastructure modernization, and evolving consumer preferences converge to reshape the interactive entertainment landscape. The country's expanding fifth-generation network coverage, which reached 365 Million subscribers by mid-2025 with availability across nearly all districts, provides the low-latency backbone essential for responsive cloud gaming delivery. Simultaneously, the proliferation of affordable smartphones and competitively priced data plans are eliminating traditional hardware barriers, enabling millions of first-time gamers across tier-two and tier-three cities to access premium gaming content. The increasing convergence of telecom operators and gaming platform providers is creating bundled service offerings that enhance accessibility and affordability. Additionally, the rise of vernacular content and regional-language interfaces is broadening the addressable audience beyond English-speaking urban centers. As data center capacity expands across key metropolitan regions and edge computing infrastructure matures, the India cloud gaming market is well-positioned for sustained growth driven by technology democratization and rising digital engagement.

India Cloud Gaming Market Trends:

Accelerated Fifth-Generation Network Deployment Fueling Cloud Gaming Accessibility

India's rapid rollout of fifth-generation wireless infrastructure is fundamentally transforming cloud gaming accessibility by delivering the ultra-low latency and high bandwidth required for seamless game streaming. The nationwide expansion of next-generation network coverage across urban and semi-urban districts is enabling real-time game rendering on remote servers with minimal input delay. This connectivity revolution is eliminating the dependency on high-end local hardware, allowing gamers across diverse geographies to access console-quality experiences through standard internet-connected devices, thereby accelerating India cloud gaming market growth.

Rise of Mobile-First Cloud Gaming Experiences

The dominance of mobile devices as the primary gaming platform in India is driving the evolution of cloud gaming services optimized for smartphone and tablet interfaces. With the majority of gamers accessing entertainment through mobile screens, platform providers are designing touch-friendly interfaces, adaptive streaming quality, and data-efficient delivery protocols. This mobile-first approach is particularly significant in a market where affordable handsets serve as the primary computing device for a substantial proportion of the population, enabling widespread adoption without additional hardware investment.

Telecom-Gaming Platform Convergence and Bundled Service Models

The increasing convergence between telecommunications operators and cloud gaming providers is creating integrated service ecosystems that bundle gaming subscriptions with data connectivity packages. This partnership model enables seamless onboarding of subscribers by embedding gaming access within existing telecom plans, reducing friction for first-time cloud gaming users. The convergence trend is accelerating market penetration by leveraging established distribution networks and billing relationships to introduce cloud gaming to mainstream consumer audiences beyond dedicated gaming enthusiasts across metropolitan and regional markets.

Market Outlook 2026-2034:

The India cloud gaming market is poised for transformative growth during 2026-2034 as the convergence of advanced telecommunications infrastructure, expanding data center capacity, and evolving consumer preferences creates a robust foundation for sustained market expansion. The increasing penetration of fifth-generation wireless networks across urban and semi-urban regions is enabling low-latency game streaming that rivals locally installed experiences. The market generated a revenue of USD 14.77 Million in 2025 and is projected to reach a revenue of USD 446.24 Million by 2034, growing at a compound annual growth rate of 46.04% from 2026-2034. Affordable subscription models and telecom-bundled gaming services are accelerating adoption among price-conscious consumers, while the proliferation of capable smartphones at accessible price points continues to expand the addressable market. As edge computing infrastructure matures and content libraries diversify with vernacular and regional offerings, cloud gaming is set to redefine interactive entertainment accessibility across India.

India Cloud Gaming Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

File Streaming |

44% |

|

Device |

Smartphones |

30% |

|

Gamer Type |

Casual Gamers |

48% |

|

Region |

North India |

28% |

Type Insights:

- File Streaming

- Video Streaming

File streaming dominates with a market share of 44% of the total India cloud gaming market in 2025.

File streaming has established its commanding position through a delivery model that installs and executes game files on remote cloud servers rather than streaming continuous video feeds to end-user devices. This approach substantially reduces real-time bandwidth consumption during active gameplay, offering near-native performance with minimal input latency that closely replicates the locally installed gaming experience. The technology is especially well-suited to India's heterogeneous network environment where connection speeds fluctuate across geographic regions and service providers. The country's strong mobile data consumption patterns, which rank significantly above the global average, provide a robust foundation for sustained file streaming adoption.

The file streaming segment is further strengthened by its compatibility with expansive game libraries that include both premium and independent titles, providing gamers access to a vast selection of games without local storage constraints on their personal devices. This model appeals particularly to users with mid-range and entry-level devices that lack the processing power and storage capacity for locally installed high-fidelity games. The growing deployment of edge computing infrastructure across major metropolitan regions is reducing server-to-user distances and enhancing file streaming responsiveness across metropolitan and tier-two city networks.

Device Insights:

Access the comprehensive market breakdown Request Sample

- Smartphones

- Tablets

- Gaming Consoles

- PCs and Laptops

- Smart TVs

- Head-Mounted Displays

Smartphones lead with a share of 30% of the total India cloud gaming market in 2025.

Smartphones command the India cloud gaming market by device, driven by the massive scale of mobile device ownership across the country that creates an enormous addressable base for mobile cloud gaming services. India ranks among the largest smartphone markets globally, with widespread handset adoption enabling extensive access to cloud gaming platforms through existing personal devices. The broad availability of capable Android devices at affordable price points has significantly lowered the hardware barrier for cloud gaming entry, enabling first-time gamers in both metropolitan and semi-urban areas to access premium gaming content through their existing handsets.

The smartphone segment's strength is further reinforced by India's mobile-first internet consumption pattern, where the majority of digital activities including gaming occur on handheld devices. Mobile gaming recorded approximately 8.45 Billion game installs during the fiscal year 2024-25, confirming the country's position as the largest mobile gaming market by downloads globally. Cloud gaming services optimized for smartphone interfaces are capitalizing on this behavioral preference by offering touch-friendly controls, adaptive streaming quality based on network conditions, and data-efficient delivery protocols that align with the connectivity and device capabilities prevalent among Indian gaming audiences across tier-one through tier-three cities.

Gamer Type Insights:

- Casual Gamers

- Avid Gamers

- Lifestyle Gamers

Casual gamers hold the largest share at 48% of the total India cloud gaming market in 2025.

Casual gamers represent the dominant gamer segment in the India cloud gaming market, reflecting the broad appeal of accessible and easy-to-learn gaming experiences among a diverse demographic that spans multiple age groups and geographic regions. The casual gaming category encompasses titles characterized by simple mechanics, short session durations, and social sharing features that attract first-time and intermittent players. Cloud gaming amplifies this segment's reach by eliminating hardware requirements, allowing casual gamers to access a wide variety of titles instantly through their connected devices. The younger demographic cohort serves as a particularly strong driver, with casual formats functioning as their primary entry point into gaming.

The casual gaming segment benefits from strong cultural drivers including family-oriented co-play experiences, viral social media integration, and the increasing availability of vernacular-language game interfaces that broaden participation beyond English-speaking urban populations. Casual and hyper-casual titles collectively account for the leading share within India's broader gaming market, underscoring their commercial significance within the interactive entertainment ecosystem. Cloud delivery particularly enhances casual gaming adoption by offering instant play without downloads or installations, aligning with the spontaneous and time-constrained usage patterns characteristic of this gamer segment across tier-one through tier-three Indian cities.

Regional Insights:

- North India

- South India

- East India

- West India

North India is the largest region with 28% share of the total India cloud gaming market in 2025.

North India leads the India cloud gaming market, anchored by the dense digital infrastructure of the Delhi National Capital Region and surrounding metropolitan corridors. The region benefits from exceptionally high telecommunications density, with the Delhi service area recording tele-density exceeding 278.24% as of 2024, reflecting extensive network coverage that supports bandwidth-intensive cloud gaming applications. Rapid data center expansion in locations such as Noida and Gurgaon is enhancing cloud gaming service delivery and reducing latency across northern metropolitan clusters.

The concentration of technology enterprises, software development hubs, and digital services companies within the region has fostered a highly connected consumer base with strong affinity for interactive digital entertainment. Additionally, the presence of major educational institutions and a large youth population across states such as Uttar Pradesh, Haryana, and Punjab contributes to a digitally engaged demographic that drives demand for cloud-based gaming solutions. The region's well-established broadband connectivity, coupled with ongoing investments in fiber optic networks and edge computing infrastructure, continues to strengthen its position as the primary revenue-generating geography within the India cloud gaming market.

Market Dynamics:

Growth Drivers:

Why is the India Cloud Gaming Market Growing?

Expanding Digital Infrastructure and Data Center Capacity

India's cloud gaming market is benefiting significantly from the country's accelerating investments in digital infrastructure and data center development. The establishment of hyperscale and edge data center facilities across major metropolitan regions is creating the computing backbone necessary for delivering responsive cloud gaming experiences with minimal latency. Government initiatives promoting digital transformation and smart city development are catalyzing infrastructure modernization, including the deployment of fiber optic networks, edge computing nodes, and content delivery systems that collectively improve gaming service quality. The expanding data center footprint across multiple cities is reducing the geographic distance between gamers and game servers, which directly translates into lower latency and smoother streaming performance. Furthermore, the increasing availability of high-speed fixed broadband connections complementing mobile networks is creating a multi-access environment where gamers can transition seamlessly between devices and connection types. The ongoing infrastructure buildout is particularly impactful in enabling cloud gaming adoption beyond traditional metropolitan centers, extending premium gaming accessibility to tier-two and tier-three cities where dedicated gaming hardware ownership remains limited but digital connectivity is rapidly improving.

Growing Youth Demographics and Rising Disposable Incomes

India's favorable demographic profile, characterized by a predominantly young population with increasing purchasing power, is creating fertile ground for cloud gaming market expansion. The country's large youth cohort demonstrates strong affinity for digital entertainment and interactive media, with gaming emerging as a preferred leisure activity across urban and semi-urban regions. Rising disposable incomes among the middle class are enabling greater spending on digital entertainment subscriptions and in-game purchases, while the aspirational desire for premium gaming experiences drives demand for cloud-based alternatives to expensive hardware. The cultural normalization of gaming as mainstream entertainment, supported by the growing popularity of esports tournaments and competitive gaming communities, is further expanding the addressable audience beyond traditional demographics. Additionally, the increasing participation of female gamers and older age groups is broadening the market beyond traditional core gaming segments. The combination of a young, digitally native population and improving economic conditions creates a virtuous cycle where growing consumer demand attracts platform investment, which in turn enhances service quality and further stimulates adoption across diverse socioeconomic segments throughout the country.

Affordable Access Models and Subscription-Based Gaming Services

The proliferation of competitively priced subscription models and freemium cloud gaming services is democratizing access to premium gaming content across India's diverse consumer landscape. Cloud gaming inherently eliminates the substantial upfront investment traditionally required for high-performance gaming hardware, making console-quality experiences accessible through devices that most Indian consumers already own. The availability of flexible pricing tiers, including free-to-play options with optional premium upgrades, aligns well with the price-sensitive nature of the Indian consumer market while providing clear monetization pathways for service providers. Telecom operators are further enhancing affordability by bundling cloud gaming subscriptions with mobile data plans, creating compelling value propositions that reduce the incremental cost of gaming access for subscribers. The subscription model also enables ongoing content refreshment, with regularly updated game libraries maintaining user engagement without requiring additional hardware investments. This accessibility-driven approach is particularly effective in penetrating tier-two and tier-three cities where consumers seek affordable entertainment alternatives and where cloud gaming's hardware-agnostic delivery model offers a compelling value proposition compared to traditional gaming platforms.

Market Restraints:

What Challenges the India Cloud Gaming Market is Facing?

Persistent Latency and Network Inconsistencies

Despite the expansion of next-generation wireless networks, cloud gaming in India continues to face challenges related to latency and connection inconsistencies, particularly outside major metropolitan centers. Many users in semi-urban and rural areas experience variable network speeds and intermittent connectivity that directly impact gaming performance, causing input lag and visual quality degradation. The uneven distribution of high-speed fiber broadband infrastructure and limited edge computing deployment in smaller cities restrict the seamless cloud gaming experience that consumers expect, creating a significant barrier to broader market penetration.

Device Thermal and Performance Limitations

While affordable smartphones have expanded gaming accessibility, many entry-level and mid-range devices in India face thermal throttling and performance limitations during extended cloud gaming sessions. Sustained high-bandwidth streaming generates significant heat in mobile devices, leading to frame drops, reduced visual quality, and forced session interruptions. The prevalence of budget handsets with limited cooling mechanisms and processing capacity constrains the quality and duration of cloud gaming experiences, creating a gap between service capability and device readiness across much of the consumer base.

Complex Regulatory and Taxation Environment

The Indian gaming industry faces a multifaceted regulatory landscape that creates uncertainty for cloud gaming operators and potentially increases consumer costs. The application of steep goods and services tax rates on gaming transactions, combined with evolving compliance requirements around anti-money laundering checks and player verification processes, increases operational overhead for platform providers. These regulatory complexities, coupled with platform service fees that further reduce margins, may slow investment in cloud gaming infrastructure expansion and limit the range of affordable service offerings available to consumers across different regions.

Competitive Landscape:

The India cloud gaming market features an evolving competitive landscape characterized by the convergence of global technology companies, domestic telecom operators, and specialized cloud gaming providers. Market participants are differentiating through infrastructure investments, content library expansion, and strategic partnerships that enhance service delivery and geographic reach. The competitive dynamics are shaped by the entry of established international gaming platforms alongside homegrown solutions developed by telecommunications providers leveraging existing subscriber networks. Companies are focusing on reducing latency through localized data center deployments, improving content accessibility through vernacular language support, and enhancing affordability through bundled subscription models integrated with mobile data plans. Strategic alliances between cloud infrastructure providers, game publishers, and telecom operators are emerging as a defining competitive strategy, enabling platform providers to offer comprehensive gaming ecosystems. The market structure is gradually consolidating as scale becomes critical for managing infrastructure costs, while simultaneously creating opportunities for niche players targeting specific segments such as casual gaming or regional language content delivery across diverse geographic markets.

India Cloud Gaming Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | File Streaming, Video Streaming |

| Devices Covered | Smartphones, Tablets, Gaming Consoles, PCs and Laptops, Smart TVs, Head-Mounted Displays |

| Gamer Types Covered | Casual Gamers, Avid Gamers, Lifestyle Gamers |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Cloud Gaming Market Report

The India cloud gaming market size was valued at USD 14.77 Million in 2025.

The India cloud gaming market is expected to grow at a compound annual growth rate of 46.04% from 2026-2034 to reach USD 446.24 Million by 2034.

File streaming, holding the largest revenue share of 44%, leads the India cloud gaming market through bandwidth-efficient game delivery technology that enables near-native performance across diverse network environments and device categories.

Key factors driving the India cloud gaming market include expanding fifth-generation network coverage, growing smartphone penetration, rising youth demographics, affordable subscription models, increasing data center investments, and telecom-gaming platform convergence.

Major challenges include persistent network latency in semi-urban and rural areas, device thermal and performance limitations during extended sessions, complex regulatory and taxation frameworks, limited edge computing infrastructure, and uneven broadband penetration across regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade