India Coconut Water and Fortified Water Market Size, Share, Trends and Forecast by Organized and Unorganized, Pack Type, Pack Size, Distribution Channel, and Region, 2026-2034

India Coconut Water and Fortified Water Market Summary:

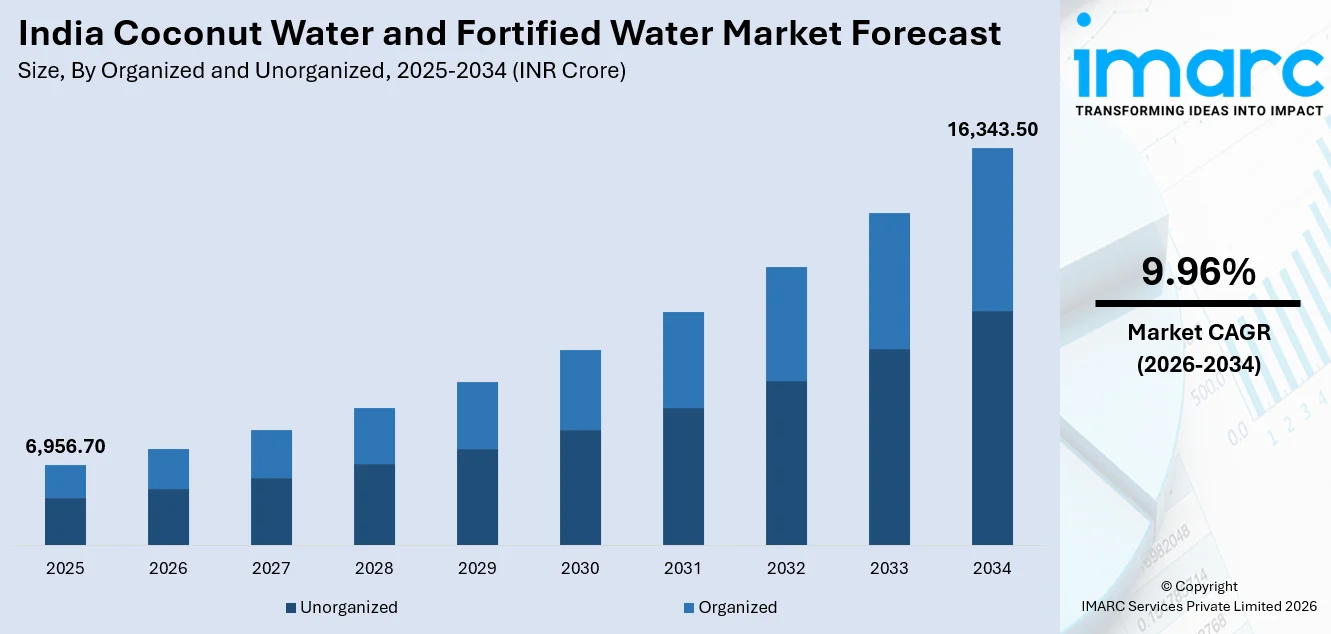

The India coconut water and fortified water market size was valued at INR 6,956.70 Crore in 2025 and is projected to reach INR 16,343.50 Crore by 2034, growing at a compound annual growth rate of 9.96% from 2026-2034.

The market is driven by increasing health consciousness among Indian consumers, growing preference for natural and low-calorie hydration alternatives, and rising demand for packaged ready-to-drink beverages. Expanding retail infrastructure, the proliferation of quick-service restaurants and cafes, and the adoption of organic and clean-label product variants are further accelerating market expansion. Additionally, favorable government initiatives promoting healthier lifestyle choices and abundant domestic coconut availability are contributing to the sustained growth of the India coconut water and fortified water market share.

Key Takeaways and Insights:

- By Organized and Unorganized: Unorganized dominates the market with a share of 60% in 2025, driven by the widespread presence of street vendors and local sellers offering fresh, affordable coconut water.

- By Pack Type: Bottles lead the market with a share of 72% in 2025, owing to consumer preference for convenient, portable, and resealable packaging formats ensuring product freshness and extended shelf life.

- By Pack Size: 200 ML represents the largest segment with a market share of 48% in 2025, driven by affordability and single-serve convenience, making them ideal for impulse and on-the-go consumption.

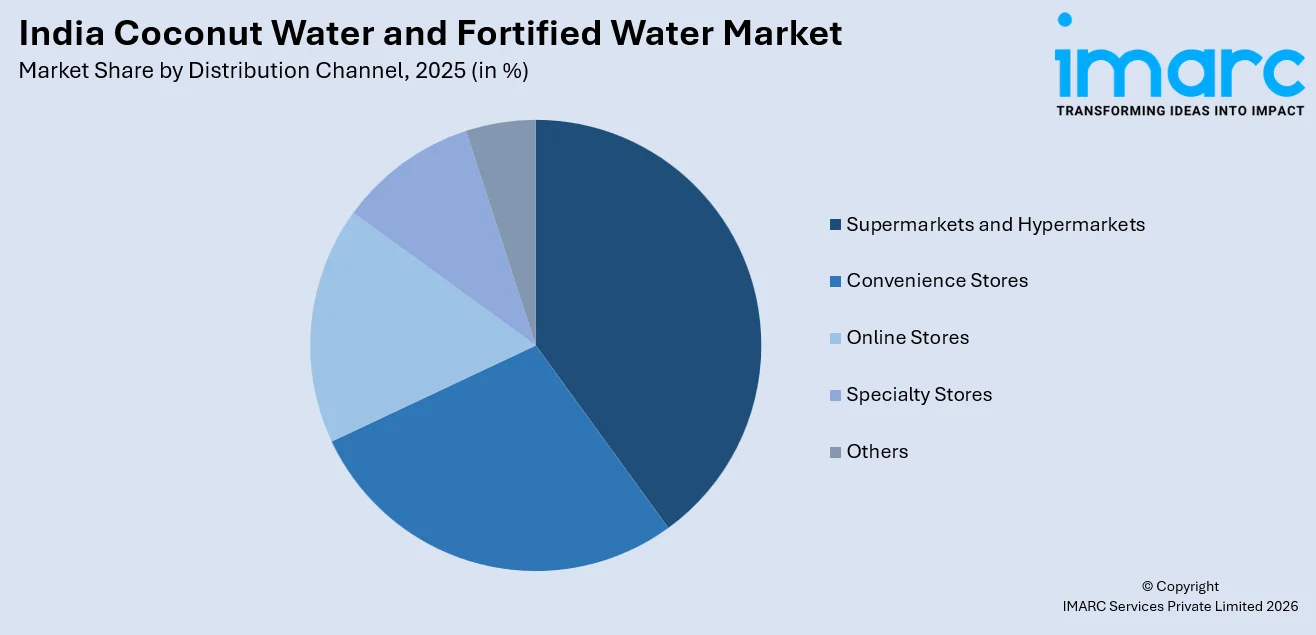

- By Distribution Channel: Supermarkets and hypermarkets dominate the market with a share of 40% in 2025, owing to wide product assortment, organized shelf displays, and the growing footprint of modern retail chains.

- Key Players: The market exhibits a fragmented competitive landscape, with established beverage corporations and emerging regional players competing across segments, focusing on product innovation, organic offerings, sustainable packaging, and broader distribution expansion. Some of the key players operating in the market include Agricoles Naturel Foods, Dabur India Limited, Hector Beverages Pvt. Ltd., Jain Agro Food Products Pvt. Ltd., Madhura Agro Process Pvt. Ltd., Manpasand Beverages Limited, Nature’s First India Pvt. Ltd., Nilgai Foods Pvt. Ltd., Pure Tropic, RAW Pressery, Sakthi Coco Products, Coca-Cola India, FDC Private Limited, G7 Beverages, NourishCo Beverages Limited and Pepsico India.

To get more information on this market Request Sample

The India coconut water and fortified water market is witnessing robust expansion fueled by a convergence of health, lifestyle, and demographic factors. Rising consumer awareness about the nutritional benefits of natural hydration alternatives, including electrolyte replenishment and antioxidant properties, is reshaping beverage preferences across the country. Urbanization and increasingly hectic lifestyles are driving demand for convenient, packaged ready-to-drink beverages that align with wellness-oriented consumption habits. In August 2025, the Ministry of Food Processing Industries (MoFPI) announced that over 1.44 lakh food processing projects were approved under the PMFME scheme, supporting value-added beverage segments including coconut-based processing units across India. The growing popularity of cafe culture, quick-service restaurants, and fitness-oriented lifestyles is further propelling market demand. Additionally, expanding organized retail infrastructure and the rapid proliferation of e-commerce platforms are enhancing product accessibility across urban and rural markets.

India Coconut Water and Fortified Water Market Trends:

Shift Toward Clean-Label and Organic Beverage Formulations

Indian consumers are increasingly gravitating toward clean-label beverages free from artificial additives, preservatives, and synthetic sweeteners. This preference is driving manufacturers to reformulate coconut water and fortified water products with transparent ingredient lists and organic certifications. The demand for naturally sourced, minimally processed beverages is particularly strong among urban millennials and health-conscious demographics who prioritize ingredient authenticity. As per sources, ITC Limited expanded its healthy beverage portfolio through the launch of B Natural Tender Coconut Water made with no added sugar or artificial flavors, reinforcing industry movement toward clean-label hydration products in India. This trend is further reinforced by the growing influence of wellness-oriented social media content and nutritionist-led advocacy promoting natural hydration as a cornerstone of preventive health management.

Emergence of Functional and Fortified Hydration Solutions

The market is witnessing a notable trend toward functional beverages enriched with vitamins, minerals, amino acids, and bioactive botanicals offering targeted health benefits beyond basic hydration. Fortified water variants incorporating immunity-boosting ingredients, electrolyte-enhanced formulations, and plant-based nutrient blends are gaining traction among fitness enthusiasts and wellness-focused consumers. In February 2025, Coca-Cola India announced plans to introduce BodyArmor Lyte in India, an electrolyte hydration drink formulated with coconut water, reflecting growing industry focus on performance-oriented and functional hydration solutions. This evolution reflects a broader industry shift from conventional beverages to purpose-driven hydration solutions addressing specific nutritional needs, including post-workout recovery, cognitive performance support, and digestive health enhancement, thereby expanding the addressable consumer base significantly.

Expansion of Digital Commerce and Direct-to-Consumer Channels

The rapid growth of e-commerce platforms and direct-to-consumer distribution models is transforming the market landscape for coconut water and fortified water in India. Online retail channels are enabling brands to reach consumers in smaller cities where physical modern retail penetration remains limited. In July 2024, Yu Foods Co. announced that its newly launched 100% natural coconut water would be distributed through omni-channel networks including e-commerce and quick-commerce platforms, strengthening digital access to hydration beverages across India. Subscription-based delivery models and curated wellness bundles are enhancing consumer engagement and brand loyalty. The integration of digital marketing strategies, influencer collaborations, and targeted social media campaigns is further amplifying brand visibility and enabling both established and emerging players to compete effectively.

Market Outlook 2026-2034:

The India coconut water and fortified water market is poised for sustained growth over the forecast period, driven by rising health consciousness, expanding retail infrastructure, and increasing consumer preference for natural, functional beverages. Favorable demographic trends, including a young and urbanizing population with growing disposable incomes, are expected to sustain the upward trajectory. Continued product innovation, premiumization strategies, deepening digital distribution networks, and the growing adoption of organic and clean-label formulations are anticipated to further amplify the market potential through the forecast period. The market generated a revenue of INR 6,956.70 Crore in 2025 and is projected to reach a revenue of INR 16,343.50 Crore by 2034, growing at a compound annual growth rate of 9.96% from 2026-2034.

India Coconut Water and Fortified Water Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Organized and Unorganized |

Unorganized |

60% |

|

Pack Type |

Bottles |

72% |

|

Pack Size |

200 ML |

48% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

40% |

Organized and Unorganized Insights:

- Unorganized

- Organized

Unorganized dominates with a market share of 60% of the total India coconut water and fortified water market in 2025.

The unorganized commands the largest share of the India coconut water and fortified water market, reflecting the deeply entrenched presence of traditional vendors, street sellers, and local distributors across the country. Fresh coconut water sold through roadside stalls and informal retail outlets remains the preferred choice for a vast majority of Indian consumers, particularly in semi-urban and rural areas where affordability and accessibility take precedence over branded alternatives. The cultural association of fresh coconut water with natural purity further reinforces consumer loyalty toward unorganized channels.

The unorganized sector is flourishing due to the easy availability of tender coconuts in the coastal and southern regions of India, which is providing an uninterrupted supply chain to the vendors in the unorganized sector who lack the infrastructure to package and brand their products. This perception of consumers regarding the natural and organic nature of the product, along with its affordability, provides the much-needed boost to the unorganized sector to remain at the top of the distribution channels of the diverse consumers in the market.

Pack Type Insights:

- Bottles

- Tetra

- Others

Bottles lead with a share of 72% of the total India coconut water and fortified water market in 2025.

The bottles dominate the pack type category, driven by widespread consumer preference for durable, portable, and resealable packaging that ensures product integrity and convenience. Plastic and PET bottles remain the primary packaging format for both coconut water and fortified water products, favored for their lightweight nature, cost-effectiveness, and suitability for on-the-go consumption across diverse retail environments. In June 2024, Coca-Cola India expanded the use of 100% food-grade recycled PET (rPET) bottles across its beverage portfolio, reinforcing the industry’s continued reliance on bottle-based packaging while advancing sustainable hydration packaging formats.

Another advantage of bottles is the enhanced brand presence on store shelves, which helps the manufacturer take full advantage of eye-catching labeling, nutritional facts panel displays, and advertising copy that ultimately affects the end-purchase decision. The compatibility of bottle packaging with machine-based filling and sealing equipment also contributes to efficient production processes while maintaining quality assurance. Moreover, the increasing importance of recyclable and environmentally safe bottle materials is bringing this packaging type into alignment with the environmentally conscious end-consumer profile, thus solidifying its position as the leading packaging type in the India coconut water and fortified water market landscape.

Pack Size Insights:

- 200 ML

- 1000 ML

- 500 ML

- Others

200 ML exhibits a clear dominance with a 48% share of the total India coconut water and fortified water market in 2025.

200 ML leads the market, driven by strong consumer preference for affordable, single-serve portions that cater to impulse purchase behavior and on-the-go consumption patterns. This compact format is particularly popular among price-sensitive consumers, students, and working professionals seeking quick hydration solutions during commutes, office breaks, and outdoor activities. The affordability of smaller pack sizes enables broader market penetration, especially in semi-urban and rural areas where purchasing power considerations significantly influence buying decisions and consumption frequency among everyday consumers.

The dominance of the 200 ML is further supported by its widespread availability across diverse retail touchpoints, including convenience stores, railway stations, bus terminals, and street kiosks where single-serve beverages experience the highest demand. Manufacturers strategically price this format as an entry-level offering to attract first-time consumers and build brand familiarity before encouraging migration to larger pack sizes. The compact nature of this format also reduces packaging and logistics costs per unit, enabling brands to maintain competitive pricing while preserving healthy profit margins across distribution networks.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Specialty Stores

- Others

Supermarkets and hypermarkets lead with a market share of 40% of the total India coconut water and fortified water market in 2025.

Supermarkets and hypermarkets represent the leading distribution channel for coconut water and fortified water in India, owing to their extensive product assortment, organized merchandising, and ability to offer consumers a comprehensive comparison-shopping experience. These modern retail formats benefit from strategic store locations in high-footfall commercial areas, promotional offers, loyalty programs, and dedicated beverage aisles that enhance product visibility and drive purchase conversion among health-conscious consumers seeking trusted, branded hydration options across premium and value product categories.

The dominance of supermarkets and hypermarkets is further reinforced by their capacity to accommodate diverse brand portfolios, enabling consumers to evaluate multiple product variants based on pricing, packaging, nutritional profiles, and brand reputation within a single shopping visit. These retail outlets also serve as key platforms for new product launches, sampling campaigns, and seasonal promotional activities that generate consumer awareness and trial. The continued expansion of organized retail chains into tier-two and tier-three Indian cities is broadening the geographic reach of this distribution channel significantly.

Regional Insights:

- North India

- Delhi NCR

- Uttar Pradesh

- Haryana

- Rajasthan

- Punjab

- Others

- West and Central India

- Maharashtra

- Gujarat

- Madhya Pradesh

- Others

- East India

- West Bengal

- Bihar

- Orissa

- Jharkhand

- Others

- South India

- Tamil Nadu

- Karnataka

- Andhra Pradesh

- Others

North India represents the largest regional market for coconut water and fortified water, driven by growing health consciousness among urban consumers, expanding modern retail infrastructure across Delhi NCR and surrounding states, and rising demand for packaged ready-to-drink beverages. The region benefits from high disposable incomes, increasing fitness culture, and the proliferation of cafes and quick-service restaurants that prominently feature natural hydration beverages.

West and Central India hold a significant share in the market, supported by the strong presence of organized retail chains in Maharashtra and Gujarat, rising urban population density, and increasing consumer preference for convenient packaged beverages. The region benefits from well-established distribution networks, growing health awareness among metropolitan consumers, and expanding e-commerce penetration that enhances product accessibility across urban and semi-urban markets.

East India is an emerging market for coconut water and fortified water, driven by gradually increasing health awareness, expanding retail infrastructure, and rising disposable incomes across key states including West Bengal and Bihar. Growing urbanization, improving supply chain connectivity, and the entry of organized beverage brands into previously underserved markets are creating new growth opportunities and driving consumer adoption across the region.

South India plays a vital role in the market, benefiting from abundant domestic coconut production, deep-rooted cultural affinity for coconut-based beverages, and strong consumer familiarity with fresh coconut water. The region serves as a critical sourcing hub for raw materials while simultaneously experiencing rising demand for packaged and fortified variants among urban consumers seeking convenient, branded hydration alternatives across modern retail and online channels.

Market Dynamics:

Growth Drivers:

Why is the India Coconut Water and Fortified Water Market Growing?

Rising Prevalence of Lifestyle-Related Health Conditions

The growing incidence of lifestyle-related health conditions including obesity, diabetes, hypertension, and digestive disorders is prompting Indian consumers to adopt healthier dietary and hydration choices. Coconut water, naturally rich in electrolytes, potassium, and antioxidants, is increasingly recognized as a beneficial alternative to sugar-laden carbonated beverages and artificially flavored drinks. In May 2025, Dabur India Limited promoted its Réal Activ Coconut Water through a nationwide ‘Keep It Real’ campaign highlighting no-added-sugar hydration to encourage consumers to shift from high-sugar soft drinks toward natural beverage options. Health practitioners and wellness advocates are actively recommending coconut water and fortified beverages as part of preventive healthcare routines, driving sustained consumer demand across diverse age groups and income segments nationwide.

Abundant Domestic Coconut Production and Favorable Agricultural Ecosystem

India ranks among the leading coconut-producing nations globally, providing a strong agricultural foundation that supports consistent raw material availability for coconut water manufacturers. The extensive cultivation of coconut across southern and coastal states ensures a reliable supply chain that reduces dependency on imports and enables competitive pricing for domestic producers. As per sources, in February 2026, the Government of India introduced a Coconut Promotion Scheme under the Union Budget to replace aging coconut palms with high-yielding varieties, strengthening long-term raw material availability for processing industries and beverage manufacturers. Government initiatives promoting coconut farming, improving post-harvest processing infrastructure, and supporting smallholder farmers are further strengthening the upstream ecosystem, creating favorable conditions for sustained market expansion and product diversification.

Growing Influence of Fitness Culture and Active Lifestyle Adoption

The rapid proliferation of gymnasiums, yoga studios, sports academies, and marathon events across Indian cities is driving significant demand for natural post-workout hydration and recovery beverages. Coconut water is increasingly positioned as a preferred natural sports drink owing to its electrolyte-replenishing and rehydrating properties that appeal to fitness enthusiasts and active lifestyle consumers. In November 2025, Tata Consumer Products’ Tata Copper+ beverage was announced as the Official Hydration Partner for the Vizag Marathon 2025, highlighting the growing integration of functional hydration drinks within India’s expanding running and fitness ecosystem. The endorsement of coconut water by fitness trainers, athletes, and wellness influencers through social media platforms is further accelerating consumer adoption and normalizing its integration into daily fitness and nutrition routines.

Market Restraints:

What Challenges the India Coconut Water and Fortified Water Market is Facing?

Seasonal Supply Variability and Raw Material Constraints

Coconut water production is inherently dependent on seasonal harvesting cycles, creating supply chain inconsistencies and price volatility throughout the year. Geographic concentration of coconut plantations in select southern and coastal states further compounds logistical complexities for nationwide distribution, leading to intermittent product shortages and elevated procurement costs during off-peak harvest seasons affecting manufacturer profitability.

Inadequate Cold Chain Infrastructure Across Rural Markets

Coconut water is a perishable product requiring stringent cold chain management to preserve nutritional integrity and freshness. Inadequate refrigerated storage and transportation infrastructure, particularly across rural and semi-urban areas, poses significant challenges for maintaining product quality during distribution. This limitation restricts the geographic reach of brands and increases wastage-related losses across supply networks.

Intense Price Competition from Unorganized Market Participants

The dominance of unorganized vendors selling fresh coconut water at significantly lower price points creates substantial pricing pressure on organized branded players. Consumers in price-sensitive segments perceive freshly extracted coconut water as more authentic and affordable compared to packaged alternatives, making it challenging for branded manufacturers to successfully drive consumer migration toward packaged products.

Competitive Landscape:

The India coconut water and fortified water market features a highly fragmented competitive landscape characterized by a mix of large-scale organized beverage corporations and a vast network of regional and local players operating in the unorganized segment. Competition in the organized space is intensifying as brands focus on product differentiation through organic certifications, innovative flavoring, functional fortification, and sustainable packaging solutions. Strategic investments in marketing campaigns, celebrity endorsements, and digital engagement are becoming critical differentiators for market positioning. The growing trend of premiumization is prompting companies to develop value-added offerings targeting health-conscious urban consumers.

Some of the key players include:

- Agricoles Naturel Foods

- Dabur India Limited

- Hector Beverages Pvt. Ltd.

- Jain Agro Food Products Pvt. Ltd.

- Madhura Agro Process Pvt. Ltd.

- Manpasand Beverages Limited

- Nature’s First India Pvt. Ltd.

- Nilgai Foods Pvt. Ltd.

- Pure Tropic

- RAW Pressery

- Sakthi Coco Products

- Coca‑Cola India

- FDC Private Limited

- G7 Beverages

- NourishCo Beverages Limited

- PepsiCo India

Recent Developments:

- In February 2026, Ghodawat Consumer Limited launched TBH Coconut Water in India, made from fresh Tamil Nadu–sourced coconuts with no added sugar, concentrates, or artificial flavours. Packaged in PET bottles, the product marks the company’s entry into clean-label functional hydration beverages responding to rising demand for natural coconut water.

India Coconut Water and Fortified Water Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Crore, Million Liters |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Organised and Unorganised Covered | Unorganized, Organized |

| Pack Types Covered | Bottles, Tetra, Others |

| Pack Sizes Covered | 200 ML, 1000 ML, 500 ML, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Specialty Stores, Others |

| Region Covered | South India, North India, West and Central India, East India |

| States Covered | Delhi NCR, Uttar Pradesh, Haryana, Rajasthan, Punjab, Maharashtra, Gujrat, Madhya Pradesh, West Bengal, Bihar, Orissa, Jharkhand, Tamil Naidu, Karnataka, Andhra Pradesh |

| Companies Covered | Agricoles Naturel Foods, Dabur India Limited, Hector Beverages Pvt. Ltd., Jain Agro Food Products Pvt. Ltd., Madhura Agro Process Pvt. Ltd., Manpasand Beverages Limited, Nature’s First India Pvt. Ltd., Nilgai Foods Pvt. Ltd., Pure Tropic, RAW Pressery, Sakthi Coco Products, Coca-Cola India, FDC Private Limited, G7 Beverages, Hector Beverages Pvt. Ltd., NourishCo Beverages Limited and Pepsico India. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India coconut water and fortified water market size was valued at INR 6,956.70 Crore in 2025.

The India coconut water and fortified water market is expected to grow at a compound annual growth rate of 9.96% from 2026-2034 to reach INR 16,343.50 Crore by 2034.

Unorganized held the largest market share, accounting for approximately 60% of the total revenue, driven by the widespread presence of traditional coconut water vendors, street sellers, and local distributors across urban, semi-urban, and rural India.

Key factors driving the India coconut water and fortified water market include ising health consciousness among consumers, increasing preference for natural and functional hydration beverages, expanding retail and e-commerce distribution infrastructure, growing fitness culture, and the rising popularity of organic and clean-label product formulations.

Major challenges include seasonal supply variability in coconut harvesting, limited cold chain infrastructure in rural areas, intense price competition from the unorganized segment, short shelf life of natural coconut water products, high packaging and logistics costs, and consumer preference for fresh unpackaged coconut water over branded alternatives.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)