India Coffee Machine Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End User, and Region, 2026-2034

India Coffee Machine Market Size & Forecast 2026-2034

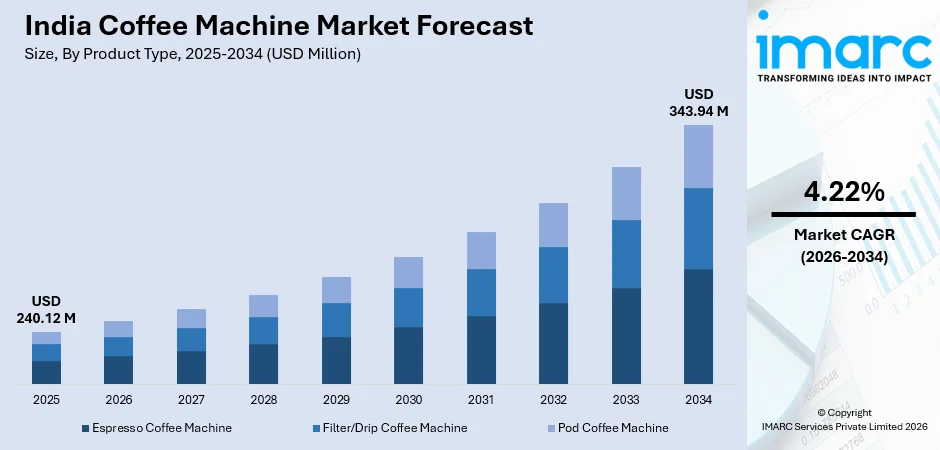

India coffee machine market size, valued at USD 240.12 Million in 2025, is projected to reach USD 343.94 Million by 2034, growing at a CAGR of 4.22% from 2026-2034, fueled by the rapid expansion of café culture, rising urban disposable incomes, and a growing preference for premium at-home brewing. According to the Coffee Board of India, domestic production reached approximately 363.500 metric tons in 2024-25, underscoring deepening consumer engagement with the beverage. These dynamics continue to widen the India coffee machine market share.

To get more information on this market Request Sample

India Coffee Machine Industry Analysis — Key Insights

- Espresso coffee machine owns 51.0% of the product type segment in 2025 - both café chains and home barista enthusiasts have converged on espresso as the defining format, with new entrants like WMF and Franke validating strong commercial demand.

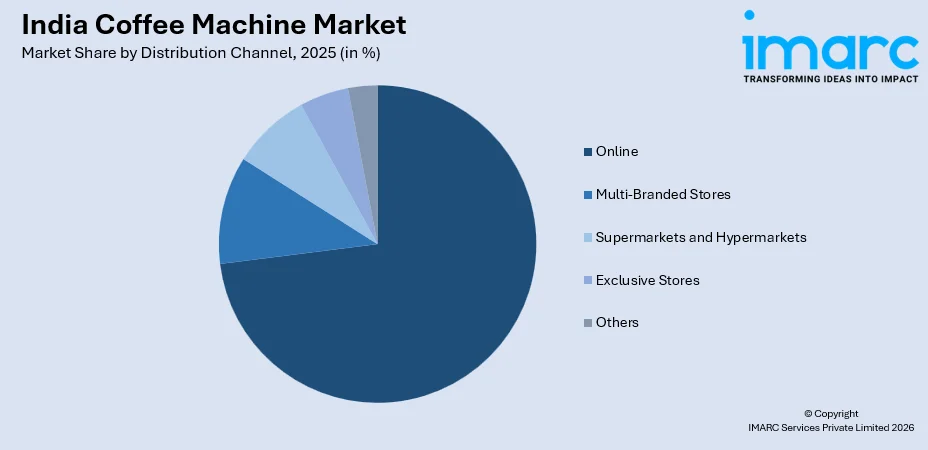

- Online channels hold 62.0% of distribution channel in 2025 - e-commerce has outpaced all physical retail formats combined. Nespresso’s India e-commerce channels launch in 2024 underscores how decisively the procurement channel has shifted.

- Food service dominates 73.0% of end user in 2025 - café chain proliferation and HoReCa investments are structurally dominant; residential and office segments remain secondary in comparison.

- West India leads at 30.0% of regional share in 2025 - Maharashtra and Gujarat’s commercial infrastructure and cosmopolitan consumer base keep the west ahead, though the margin suggests competitively distributed demand across all four regions.

India Coffee Machine Market Trends and Dynamic 2026

Market Trends

Premiumization and craft coffee culture are driving high-end espresso machine demand

Premiumization and the rise of craft coffee culture are significantly boosting demand for high-end coffee machines in India. Urban consumers, specialty cafés, and boutique coffee chains are increasingly investing in advanced espresso and bean-to-cup machines to deliver barista-style beverages, supporting the market growth across residential and commercial segments.

Smart connectivity and IoT integration are transforming the brewing experience

Tech-savvy consumers are propelling demand for app-enabled, Wi-Fi-connected machines offering programmable settings and remote brewing operations. Data from Redseer report showed smart device penetration is expected to increase from 8-10% in 2023 to 25-28% by 2028, establishing fertile conditions for smart appliance integration, including intelligent coffee equipment, a development that is actively reshaping India coffee machine market trends.

- Health-Oriented and Low-Caffeine Options: Growing consumer awareness around caffeine intake is spurring demand for machines that support decaf, cold brew, and low-extraction brewing formats.

- Sustainability Focus in Equipment Design: Indian buyers are increasingly favoring energy-efficient and recyclable-compatible machines as environmental awareness rises among urban consumers.

- Compact and Portable Machine Formats: Urban apartment culture and limited kitchen space are driving demand for smaller-format espresso and pod machines suitable for home use.

- Barista-Style Automation in Commercial Settings: Café chains are prioritizing super-automatic equipment that delivers consistency without skilled barista labor, in response to staffing challenges and operational efficiency demands.

Growth Drivers

Rapid café chain expansion is creating sustained commercial machine demand

India’s branded coffee shop market grew 12.7% in a single year to reach 5,339 outlets, according to Project Café India 2025, adding 600 new locations and representing enormous incremental equipment procurement. Third Wave Coffee and Café Buddy’s Espresso are each adding 56 new outlets, bringing their total store counts to 172 and 145 locations, respectively. This structural expansion is a primary engine of market growth in the food service segment.

Rising disposable incomes are enabling premium appliance investment

The increasing disposable income in India is motivating customers to spend on premium home appliances like coffee machines. Urban households and young professionals are increasingly using espresso and bean-to-cup machines to prepare coffee drinks like those consumed in coffee houses, thus contributing to the growth of India coffee machine market.

Online retail expansion is democratizing coffee machine accessibility

The growth in online retail platforms is significantly contributing to the accessibility of coffee machines in India. E-commerce platforms and online websites are allowing customers in Tier 2 and Tier 3 cities to purchase a variety of coffee machines, thus contributing to the growth of India coffee machine market.

- Urbanization and Lifestyle Aspiration: Growing urban middle-class populations increasingly associate premium coffee machines with modern lifestyle aspirations, driving both aspirational and functional purchases.

- Office and Corporate Sector Expansion: The return-to-office trend and workplace wellness initiatives have accelerated corporate procurement of bean-to-cup and fully automatic machines across India’s commercial real estate sector.

- Youth Demographics and Cultural Shift: Millennials and Gen Z, constituting a growing share of India’s consumer base, are transitioning from tea to coffee, creating lasting structural demand for home and commercial coffee machines.

- Tourism and Hospitality Infrastructure Growth: Expanding hotel inventory, airport cafés, and food courts are creating new procurement channels for professional coffee equipment.

Market Restraints

High import duties and complex certification requirements: India’s mandatory Bureau of Indian Standards certification for imported coffee equipment creates prolonged entry barriers for international brands. Complex multi-tier regulatory processes, coupled with high tariff structures, restrict the range of premium imported machines available, limiting consumer choice and dampening competitive pricing in premium categories.

Fragmented after-sales service infrastructure: Technical support and genuine spare parts for advanced espresso machines remain scarce in non-metro markets. Consumers and small café operators in Tier 2 and Tier 3 cities are often deterred from investing in high-performance equipment due to uncertainty about maintenance support, creating a bottleneck for deeper market penetration.

Cultural preference for tea and price sensitivity in broader markets: India’s deeply entrenched tea-drinking tradition creates a persistent cultural barrier to coffee machine adoption beyond urban centers. Consumer reluctance to invest in premium appliances for non-habitual use, combined with price sensitivity across semi-urban and rural segments, limits the addressable market to concentrated metro and affluent suburban clusters.

India Coffee Machine Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Espresso Coffee Machine | 51.0% | 2025 |

| Distribution Channel | Online | 62.0% | 2025 |

| End User | Food Service | 73.0% | 2025 |

| Region | West India | 30.0% | 2025 |

Product Type Insights

Espresso Coffee Machine - 51.0% market share (2025) | Leading Product Type

The dominant position of espresso coffee machines reflects the product’s essential role in India’s rapidly expanding café and hospitality sector. As branded café chains such as Third Wave Coffee, Tata Starbucks, and Barista continue to scale nationally, they consistently specify commercial espresso equipment as their primary brewing platform. In November 2024, Kaapi Machines unveiled the Carimali GLOW, a durable and affordable espresso machine specifically designed for small to medium-sized coffee businesses, addressing the growing demand from India’s tier-II café operators.

|

Segment Breakdown Espresso Coffee Machine (51.0%) · Filter/Drip Coffee Machine · Pod Coffee Machine |

Distribution Channel Insights

Access the comprehensive market breakdown Request Sample

Online - 62.0% market share (2025) | Leading Distribution Channel

The commanding share of the online channel reflects India’s rapid e-commerce expansion and the growing consumer preference for researching and purchasing appliances through digital platforms. Major e-commerce marketplaces, including Amazon India and Flipkart, offer extensive catalogues, competitive pricing, customer reviews, and convenient delivery, making them the default purchase channels for both residential and small business buyers.

|

Segment Breakdown Online (62.0%) · Multi-Branded Stores · Supermarkets and Hypermarkets · Exclusive Stores · Others |

End User Insights

Food Service - 73.0% market share (2025) | Leading End User

The dominant share of the food service segment reflects the structural role of India’s branded café, quick-service restaurant, and hospitality industries as the primary buyers of commercial coffee machines. In March 2025, UK-based Pret A Manger opened its first-ever global full-service dine-in store in Pune’s Phoenix Mall of the Millennium, further reinforcing the food service sector’s appetite for world-class coffee machine infrastructure as international chains accelerate their India entry.

|

Segment Breakdown Food Service (73.0%) · Residential · Offices · Institutional · Others |

Regional Insights

West India - 30.0% market share (2025) | Leading Region

West India’s leading market position is anchored by Mumbai’s status as India’s most concentrated commercial café hub and Maharashtra’s large base of corporate offices, hospitality businesses, and premium residential buyers. Third Wave Coffee, which opened its 200th café milestone location in Chembur, Mumbai, in December 2025, highlights the region’s critical importance in national café chain expansion strategies.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

30.0%

|

|

Key States

|

Maharashtra, Gujarat, Goa, Rajasthan |

|

Major Growth Drivers

|

Premium hospitality demand, commercial real estate expansion, youth-driven café culture |

|

Outlook

|

Regional market leader, sustained premium demand |

|

Regional Breakdown West India (30.0%) · North India · South India · East India |

North India:

North India, anchored by Delhi NCR, is India’s second-largest branded coffee market and a key focus area for national café chain expansion. Tata Starbucks’ strategy of opening a new store every three days targets North Indian markets significantly, while brands such as Kopi Kenangan launched their first India store at Pacific Mall, Tagore Garden, Delhi in April 2025.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Delhi, Uttar Pradesh, Haryana, Punjab, Himachal Pradesh |

|

Major Growth Drivers

|

Café chain proliferation, corporate office expansion, millennial coffee adoption |

|

Outlook

|

Fastest-growing café chain market in India |

South India:

South India carries a distinct position in the market, combining the traditional filter coffee culture of Tamil Nadu and Karnataka with the specialty café movements centered in Bengaluru. Third Wave Coffee’s roots are in Bengaluru, and the city remains India’s leading specialty coffee destination. South India’s blended demand for both traditional filter machines and premium espresso equipment makes it a unique dual-category growth zone.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Karnataka, Tamil Nadu, Kerala, Andhra Pradesh, Telangana |

|

Major Growth Drivers

|

Deep-rooted coffee culture, specialty café proliferation, strong HoReCa infrastructure |

|

Outlook

|

Highest organic coffee machine adoption nationally |

East India:

East India is an emerging market for coffee machine growth, historically dominated by tea culture but gradually responding to the café expansion driven by urban centers in Kolkata and Bhubaneswar. National café chains are beginning to extend footprints into East Indian metros, creating initial commercial machine demand.

|

Metric

|

Details

|

|---|---|

|

Key States

|

West Bengal, Odisha, Bihar, Jharkhand, Assam |

|

Major Growth Drivers

|

Youth demographics, urban café openings, online retail penetration |

|

Outlook

|

Emerging market with strong long-term potential |

Market Outlook 2026-2034

What is the future outlook of the India Coffee Machine market?

The India Coffee Machine market is expected to sustain steady revenue growth through 2034.

The growth in café chains, increasing disposable income, and penetration of coffee culture in India will sustain to support the espresso machines, pod machines, and filter machines segments. The food service segment will continue to be a key driver for commercial machine sales, while the online segment will help tap a larger consumer base for these machines. Smart machines will be a key driver for growth in this segment, making the India coffee machine market outlook positive during the forecast period.

India Coffee Machine Market — Leading Key Players

India coffee machine market features a competitive mix of global appliance majors and domestic kitchen equipment brands. International companies hold premium positioning through advanced technology, brand recognition, and dedicated channel investments, while domestic players compete on pricing, service network depth, and segment-specific product adaptation. Key strategies include new product launches aligned with India’s café culture, e-commerce channel investments, and partnerships with specialized distributors such as Kaapi Machines.

| Company | Leading Brands | Highlights |

|---|---|---|

| Philips India Limited | Philips Saeco | Launched three Philips Saeco models for home and office use; strong distribution across organized retail and e-commerce platforms |

| Nestle India Limited (Nespresso) | Nespresso Original, Nespresso Professional | Launched Nespresso in India in 2024; works with approximately 2,000 Indian coffee farmers through its AAA Sustainable Quality Program since 2011; direct-to-consumer model |

| Bosch and Siemens Home Appliances Group (BSH) | Bosch VeroSeries, Siemens EQ Series | Premium fully automatic machines for home and office; strong online presence across e-commerce channels; Wi-Fi connectivity available in top-tier models |

Some of the existing key players in the market are De’Longhi India Private Limited, Morphy Richards (Groupe SEB India), Bajaj Electricals Limited, Wonderchef Home Appliances Pvt. Ltd., Kaapi Machines India Pvt Ltd, etc.

Latest Development & News

- In September 2025, DIT’O introduced India’s first self-cleaning filter coffee machine, combining IoT controls and hygiene-focused automation for the hospitality segment. The device integrates smart connectivity with automated cleaning cycles, addressing maintenance concerns that have traditionally deterred institutional buyers. Its commercial launch reflects growing domestic product development ambition within India’s coffee equipment manufacturing space.

- In March 2025, Swiss manufacturer Franke Coffee Systems made its India market debut at AAHAR 2025, the International Food and Hospitality Fair in New Delhi. The company showcased its full A-line range, including the award-winning A300, S700, A600, and A800 models, designed for hotels, restaurants, and commercial coffee programs. Franke leveraged support from sister company Franke Faber India for local distribution and long-term customer service.

India Coffee Machine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Filter/Drip Coffee Machine, Espresso Coffee Machine, Pod Coffee Machine |

| Distribution Channels Covered | Multi-Branded Stores, Supermarkets and Hypermarkets, Online, Exclusive Stores, Others |

| End Users Covered | Food Service, Residential, Offices, Institutional, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Philips India Limited, Nestle India Limited (Nespresso), Bosch and Siemens Home Appliances Group (BSH) |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India coffee machine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India coffee machine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India coffee machine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Coffee Machine Market Report

The India Coffee Machine market was valued at USD 240.12 Million in 2025.

The India Coffee Machine market is anticipated to reach a value of USD 343.94 Million by 2034.

The espresso coffee machine segment dominates the market with a share of 51.0%, driven by robust demand from café chains, specialty coffee shops, and home barista enthusiasts seeking professional-grade experiences.

The online distribution channel dominates the market with a share of 62.0%, driven by the rapid expansion of e-commerce platforms, wider product availability, competitive pricing, and increasing consumer preference for convenient home delivery.

The food service segment commands the market with a share of 73.0%, supported by the rapid expansion of branded café chains, upscale restaurant growth, and rising corporate coffee programs in India’s major commercial centers.

West India currently leads the India Coffee Machine market, accounting for a share of 30.0%. Maharashtra’s premium hospitality ecosystem, Mumbai’s density of high-end cafés, and Gujarat’s growing tourism and commercial sector are the primary drivers of regional market leadership.

Some of the major players in the India Coffee Machine market include Philips India Limited, Nestle India Limited (Nespresso), De’Longhi India Private Limited, Bosch and Siemens Home Appliances Group (BSH), Morphy Richards (Groupe SEB India), Bajaj Electricals Limited, Wonderchef Home Appliances Pvt. Ltd., Kaapi Machines India Pvt Ltd, etc.

Growing demand for bean-to-cup and pod machines from Tier 2 city consumers reflects a broader shift toward convenience-led brewing. The integration of mobile app controls and programmable settings into mid-range machines is emerging as a standard feature expectation among urban buyers, blurring the line between home and professional brewing.

The proliferation of coffee subscription models and direct-to-consumer pod ecosystems introduced by global brands is widening the consumer base for machine ownership. Corporate wellness initiatives and the normalization of in-office premium coffee programs are additionally spurring bulk machine procurement across India’s expanding commercial real estate sector.

High acquisition costs for premium international machines remain a barrier for cost-sensitive consumers in smaller cities. Limited consumer education about maintenance and machine types creates hesitancy at the point of purchase, while competition from traditional South Indian filter coffee, deeply embedded in regional culture, continues to restrict adoption in non-metro markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)