India Commercial Printing Market Size, Share, Trends and Forecast by Technology, Print Type, Application, and Region, 2026-2034

India Commercial Printing Market Size, Share, Trends & Forecast (2026-2034)

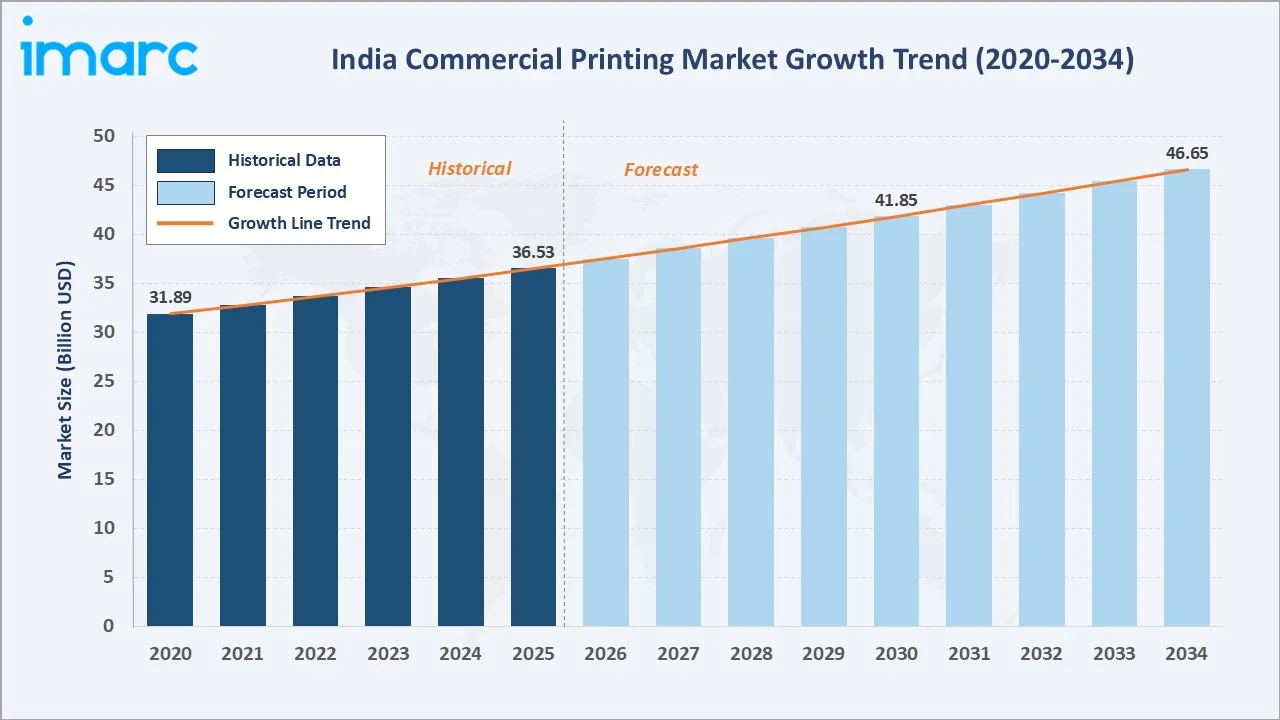

The India commercial printing market was valued at USD 36.53 Billion in 2025 and is projected to reach USD 46.65 Billion by 2034, exhibiting a CAGR of 2.76% during 2026-2034. Expanding e-commerce activity, rising brand promotion needs, surging FMCG consumption, and the adoption of advanced digital printing technologies are the primary drivers shaping the market growth. As per ITA, the India e-commerce industry is expected to hit USD 325 Billion by 2030, showing remarkable expansion.

Image leads the print type segment at 43.2%, packaging dominates the application segment at 43.8%, and South India commands 34.15% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 36.53 Billion |

|

Forecast Market Size (2034) |

USD 46.65 Billion |

|

CAGR (2026-2034) |

2.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

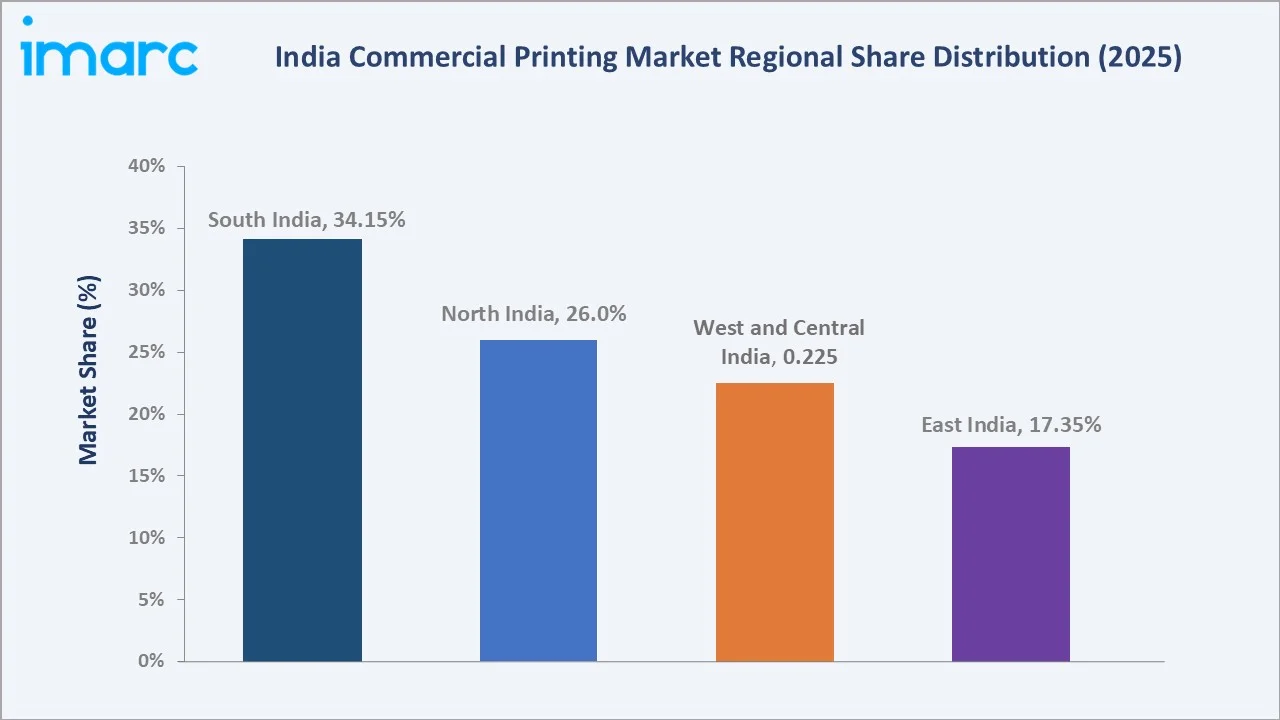

South India (34.15%, 2025) |

|

Fastest Growing Region |

East India (17.35%, 2025) |

|

Leading Print Type |

Image (43.2%, 2025) |

|

Leading Application |

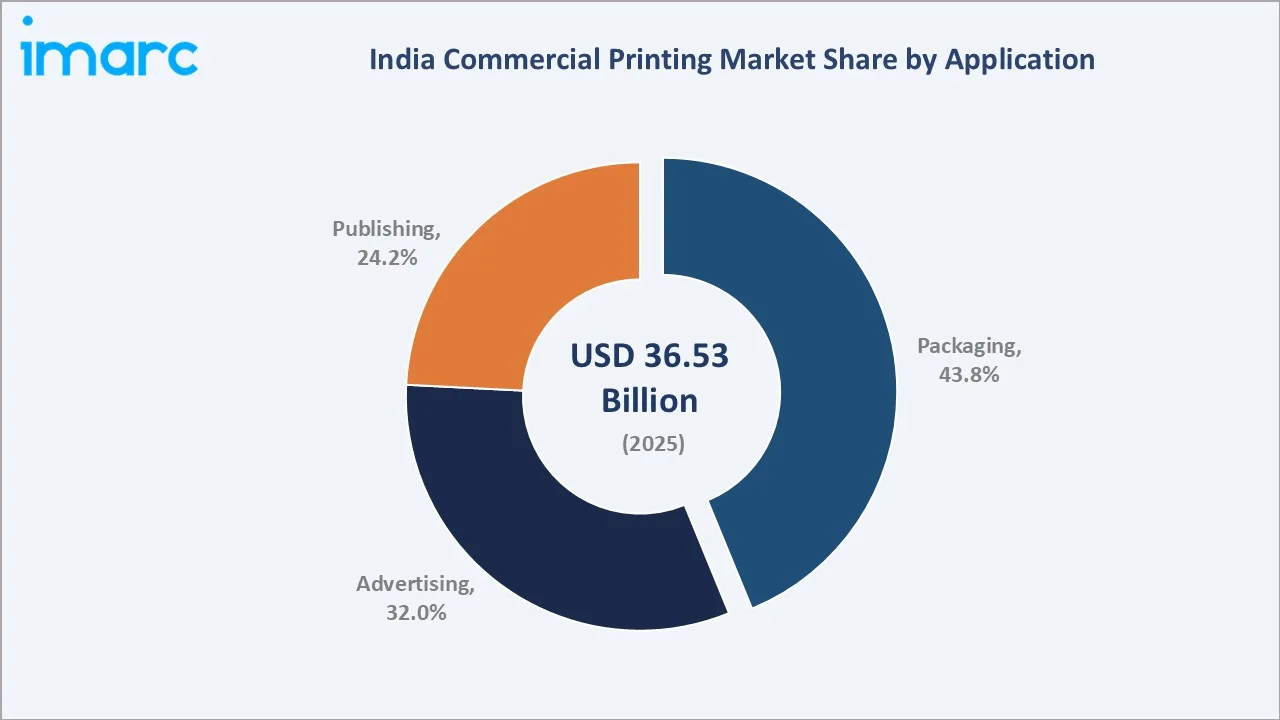

Packaging (43.8%, 2025) |

The India commercial printing market expanded from USD 31.89 Billion in 2020 to USD 36.53 Billion in 2025, driven by increasing packaging demand, growing advertising spend, and rising adoption of digital printing technology. Anchored at USD 41.85 Billion in 2030, the forecast to USD 46.65 Billion by 2034 is supported by expanding e-commerce, brand proliferation, and sustained investment in printing infrastructure.

To get more information on this market, Request Sample

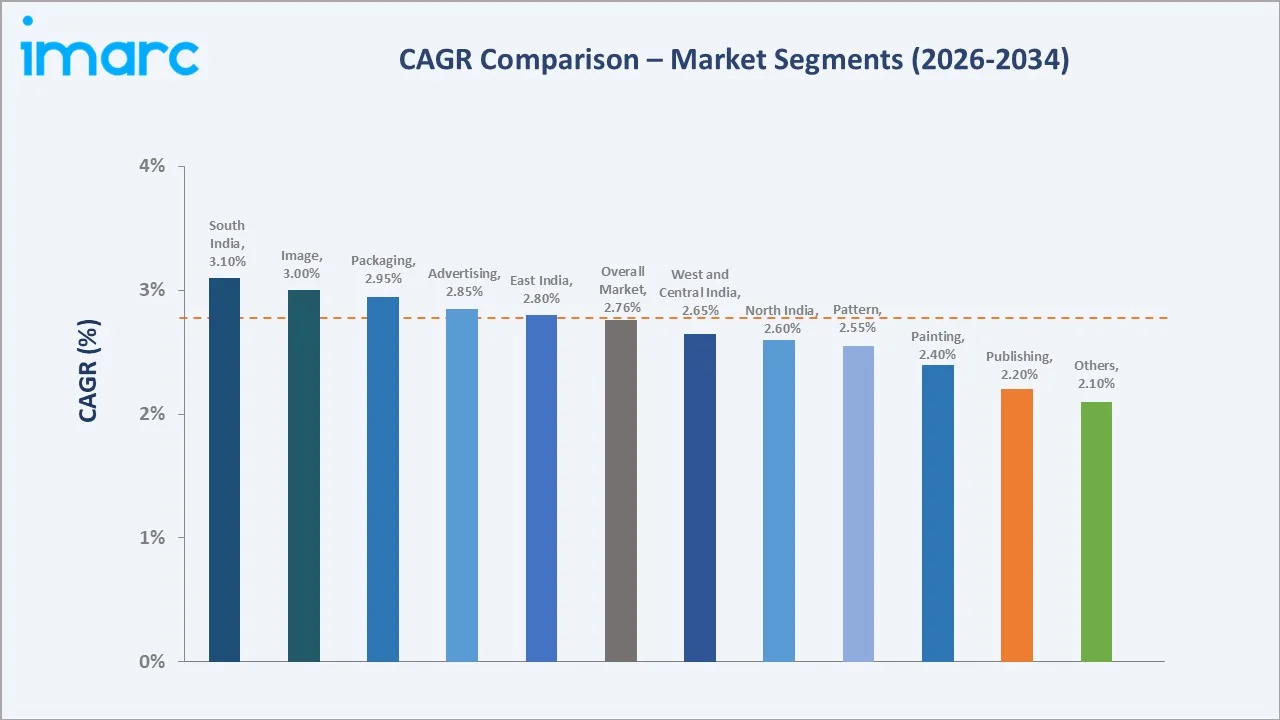

CAGR trajectories across print type, application, and regional sub-segments show image and South India expanding faster than the overall 2.76% market CAGR, driven by premium packaging requirements and robust industrial activity.

Executive Summary

The India commercial printing market is on a steady growth path from USD 31.89 Billion in 2020 to USD 46.65 Billion by 2034. Commercial printing has evolved from traditional offset-dominated operations to a technology-driven industry embracing digital presses, ultraviolet (UV) curing, and automated workflows. Rising consumer goods demand and the proliferation of organized retail are encouraging businesses to invest in high-quality printed marketing materials, packaging, and publications.

Image leads print type at 43.2% in 2025, supported by strong demand from FMCG packaging and advertising collateral. Packaging dominates the application segment at 43.8%, fueled by e-commerce expansion, food processing growth, and regulatory labeling requirements. South India commands 34.15%, driven by a strong industrial base in Tamil Nadu, Karnataka, and Telangana. In July 2025, Canon India launched the upgraded imagePRESS V1000 at Print Expo Chennai 2025, reinforcing the shift toward high-volume digital production printing.

Key Market Insights

|

Insight |

Data |

|

Leading Print Type |

Image - 43.2% share (2025) |

|

Second Print Type |

Pattern - 24.0% share (2025) |

|

Leading Application |

Packaging - 43.8% share (2025) |

|

Second Application |

Advertising - 32.0% share (2025) |

|

Leading Region |

South India - 34.15% share (2025) |

|

Fastest Growing Region |

East India - 17.35% share (2025) |

|

Top Companies |

UFlex Limited, ITC, Parksons Packaging Ltd., Repro India Limited |

Key Analytical Observations Expanding on the Data Above:

- Image dominance at 43.2% is driven by strong demand from FMCG brands, consumer goods packaging, and premium advertising materials requiring high-resolution visual reproduction.

- Pattern share at 24.0% is sustained by textile printing, decorative applications, and growing demand for customized surface printing across wallpapers and furnishing materials.

- Packaging leadership at 43.8% reflects the expanding food processing industry, rising e-commerce fulfillment requirements, and mandatory regulatory labeling across pharmaceuticals and consumer products. As per IMARC Group, the India food processing market size reached INR 33,052.5 Billion in 2025.

- Advertising at 32.0% continues to grow through corporate demand for brochures, point-of-sale materials, and out-of-home promotional collateral, supported by increasing marketing budgets across organized retail and real estate sectors.

- South India at 34.15% dominates owing to a well-established printing infrastructure in Chennai, Bengaluru, and Hyderabad, combined with proximity to major FMCG and pharmaceutical manufacturing hubs.

India Commercial Printing Market Overview

Commercial printing encompasses the production of printed materials for business and consumer use, including packaging labels, advertising brochures, corporate reports, books, magazines, and promotional collateral. Technologies deployed range from traditional offset lithography to advanced digital, flexographic, and gravure printing methods.

The industry ecosystem integrates paper and substrate suppliers, ink manufacturers, printing equipment vendors, pre-press service providers, commercial printers, finishing and binding specialists, and distribution networks. Together, these players enable seamless delivery from design conceptualization to final printed output across diverse applications.

Market Dynamics

To evaluate market opportunities, Request Sample

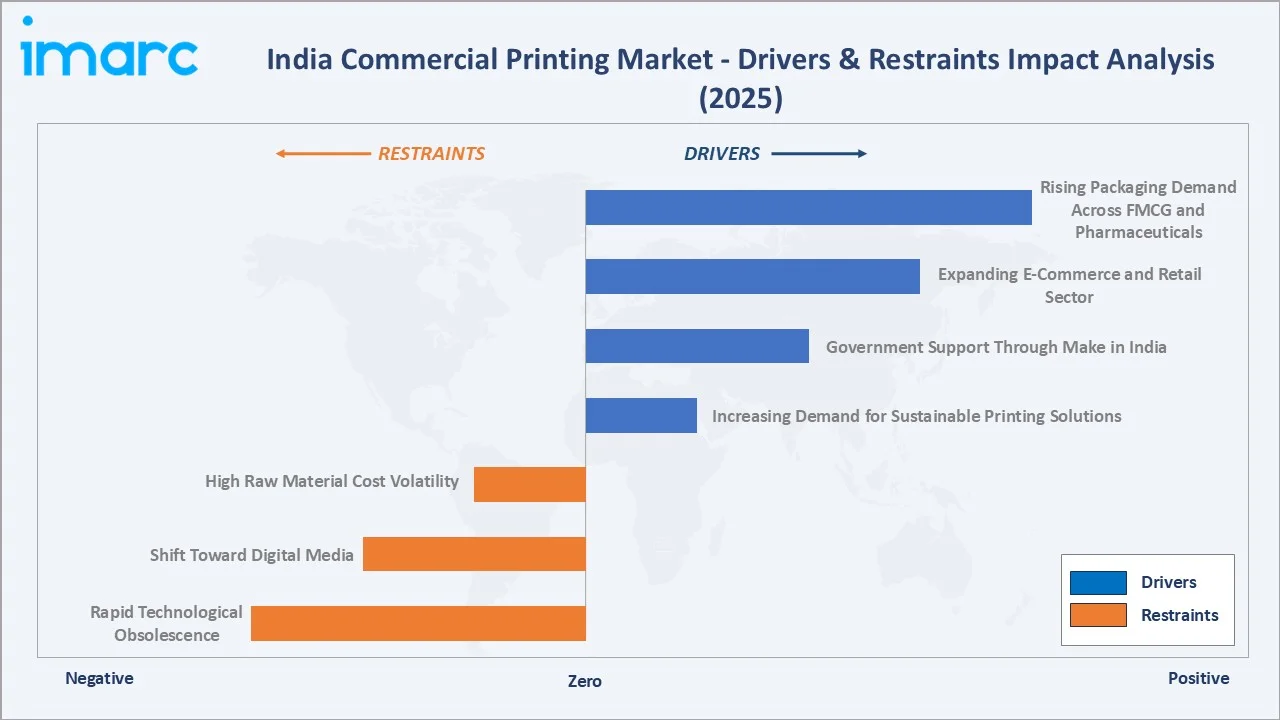

Market Drivers

- Rising Packaging Demand Across FMCG and Pharmaceuticals: The expanding food processing sector and growing pharmaceutical industry are generating sustained demand for high-quality packaging printing services. According to PIB, as of March 2026, the Indian pharmaceutical sector was positioned 3rd worldwide in volume and 11th in value, boasting over 3,000 firms and 10,500 production facilities. Major corporations are increasing collaborations with commercial printers to enhance product presentation.

- Expanding E-Commerce and Retail Sector: The rapid growth of online retail platforms is driving demand for branded packaging, shipping labels, and promotional inserts. Customized unboxing experiences are becoming a competitive differentiator for e-commerce brands.

- Government Support Through Make in India: The Indian government’s Make in India initiative is encouraging domestic manufacturing of printing machinery, inks, and packaging materials, supporting capacity expansion and reducing dependence on imports across the printing ecosystem.

- Increasing Demand for Sustainable Printing Solutions: Brands across packaging, publishing, and commercial advertising are increasingly adopting eco-friendly inks, recyclable substrates, and energy-efficient printing technologies to meet sustainability goals and evolving consumer expectations.

Market Restraints

- High Raw Material Cost Volatility: Fluctuations in paper, ink, and chemical substrate prices continue to compress margins for commercial printers. Import dependence for specialty substrates adds risk during currency fluctuations. Global pulp shortages cause longer lead times for raw material procurement.

- Shift Toward Digital Media: The rise of digital advertising and online media platforms continues to challenge traditional printing segments. Volume declines in magazines, newspapers, and office documents are placing structural pressure on publishing-focused printers.

- Rapid Technological Obsolescence: Continuous advancements in digital printing, automation, and smart packaging technologies are shortening equipment replacement cycles. Printing companies must invest regularly in upgraded machinery and software to remain competitive, increasing capital expenditure burdens.

Market Opportunities

- Digital Printing Adoption in SMEs: Affordable digital presses are enabling SMEs to access high-quality printing with shorter turnaround times, opening new market segments for personalized and on-demand printing services.

- Sustainable and Eco-Friendly Printing: Growing consumer and regulatory emphasis on sustainability is creating opportunities for printers adopting eco-friendly inks, recyclable substrates, and energy-efficient production processes.

Market Challenges

- Fragmented and Unorganized Market Structure: A large portion of the India commercial printing industry remains unorganized, with numerous small-scale operators competing primarily on price. This fragmentation limits quality standardization and technology adoption.

- Skilled Labor Shortage: The transition toward advanced digital printing, pre-press automation, and color management systems requires technically skilled operators, creating workforce gaps across the industry.

Emerging Market Trends

1. Rapid Adoption of Digital Printing Technology

Digital printing is gaining significant traction across India, driven by its ability to deliver faster turnaround times, lower minimum order quantities, and superior customization capabilities. This shift is reducing reliance on traditional offset methods for short-run commercial and packaging applications.

2. Integration of Automation and Artificial Intelligence (AI) in Print Workflows

Commercial printers are increasingly integrating automation, AI, and cloud-based print management solutions into their operations. These technologies enhance operational efficiency, reduce waste, and enable printers to offer value-added services, such as variable data printing and personalized marketing materials.

3. Growth of Sustainable Printing Practices

Environmental consciousness is reshaping printing practices across India. Adoption of soy-based inks, waterless printing technologies, and recyclable substrates is accelerating as brands and regulators continue to prioritize sustainable supply chains.

4. Convergence of Print and Digital Media

The boundary between print and digital is blurring as commercial printers develop hybrid business models. QR codes, augmented reality (AR) integrations on printed materials, and cross-media campaigns are creating new revenue streams for forward-looking print service providers.

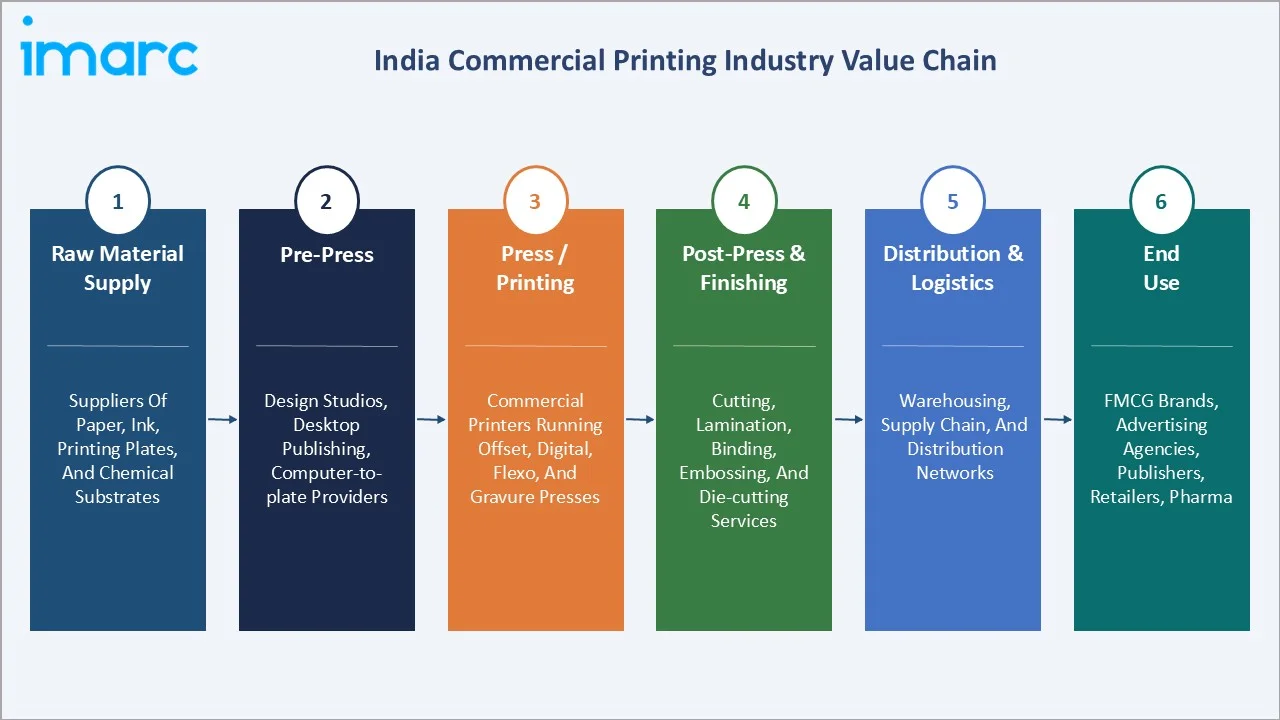

Industry Value Chain Analysis

The India commercial printing value chain spans six stages from raw material sourcing through end-use distribution. Pre-press and press operations capture the highest value-add, while distribution relationships and client account management generate downstream competitive advantages.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of paper, ink, printing plates, and chemical substrates supporting offset and digital printing production |

|

Pre-Press |

Design studios, desktop publishing firms, computer-to-plate service providers, and color management specialists |

|

Press / Printing |

Commercial printers operating offset, digital, flexographic, and gravure presses for packaging, advertising, and publishing applications |

|

Post-Press & Finishing |

Cutting, lamination, binding, embossing, and die-cutting service providers completing printed output |

|

Distribution & Logistics |

Warehousing, supply chain, and distribution networks delivering finished products to end-use clients |

|

End Use |

FMCG brands, advertising agencies, publishers, retailers, pharmaceutical companies, and e-commerce platforms |

Vertically integrated players, which operate multiple printing plants with full pre-press through post-press capabilities, achieve superior cost control and turnaround efficiency versus smaller single-process operators.

Technology Landscape in the India Commercial Printing Industry

Offset Printing Technology

Offset lithography remains the dominant technology for high-volume commercial printing in India, offering consistent quality and cost efficiency for long production runs. Modern computer-to-plate systems have streamlined pre-press workflows, reducing setup times and improving color accuracy across packaging and publication applications.

Digital Printing Advancement

High-speed inkjet and electrophotographic digital presses are transforming short-run and variable-data printing capabilities. These systems enable personalized marketing collateral, on-demand book printing, and rapid prototyping of packaging designs without traditional plate-making requirements.

Flexographic and Gravure Innovation

Flexographic printing continues to advance through HD plate technology and servo-driven press systems, improving registration accuracy for flexible packaging applications. Gravure printing retains its position for ultra-high-volume decorative and packaging runs requiring exceptional image consistency.

Smart Connectivity and Automation

Cloud-based print management platforms, IoT-enabled press monitoring, and AI-driven color matching systems are enabling real-time production optimization. These capabilities support predictive maintenance, automated job scheduling, and waste reduction across commercial printing operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

🔒 |

🔒 |

2025 |

|

Print Type |

Image |

43.2% |

2025 |

|

Application |

Packaging |

43.8% |

2025 |

|

Region |

South India |

34.15% |

2025 |

By Print Type

Image commands a 43.2% majority share in 2025, driven by strong demand from FMCG packaging, advertising collateral, and premium corporate communications. High-resolution image reproduction remains essential for brand differentiation across consumer-facing product categories.

To access detailed market analysis, Request Sample

Pattern at 24.0% in 2025 serves textile printing, wallpaper production, decorative laminates, and surface printing applications. Growing demand for customized interior décor and digitally printed textile designs continues to support segment expansion across residential and commercial applications.

By Application

Packaging dominates with 43.8% share in 2025, reflecting the central role of printed packaging in India’s expanding consumer goods, food processing, and pharmaceutical sectors. Regulatory labeling requirements and brand presentation standards continue to drive investment in high-quality packaging printing.

Advertising at 32.0% in 2025 is sustained by corporate marketing budgets, point-of-sale material production, and out-of-home promotional collateral. Brand owners are increasingly investing in high-quality visual printing and short-run customized campaigns to improve consumer engagement across retail and event marketing channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

34.15% |

Strong industrial base, established printing infrastructure, proximity to FMCG and pharmaceutical hubs, and robust IT-driven demand |

|

North India |

26.0% |

Large consumer market, presence of government and institutional printing demand, expanding retail sector, and growing advertising spend |

|

West and Central India |

22.5% |

Concentration of FMCG headquarters, strong pharmaceutical manufacturing, expanding organized retail, and well-developed logistics networks |

|

East India |

17.35% |

Developing industrial base, rising consumer demand, expanding education sector, and growing investment in printing infrastructure |

South India at 34.15% in 2025 leads the market, driven by a well-established printing and packaging ecosystem in Tamil Nadu, Karnataka, and Telangana. Chennai and Bengaluru serve as major commercial printing hubs with strong demand from the IT, FMCG, and pharmaceutical industries.

East India at 17.35% represents a high-growth opportunity as industrialization accelerates, education sector demand rises, and commercial printing infrastructure develops across Kolkata, Patna, and Bhubaneswar.

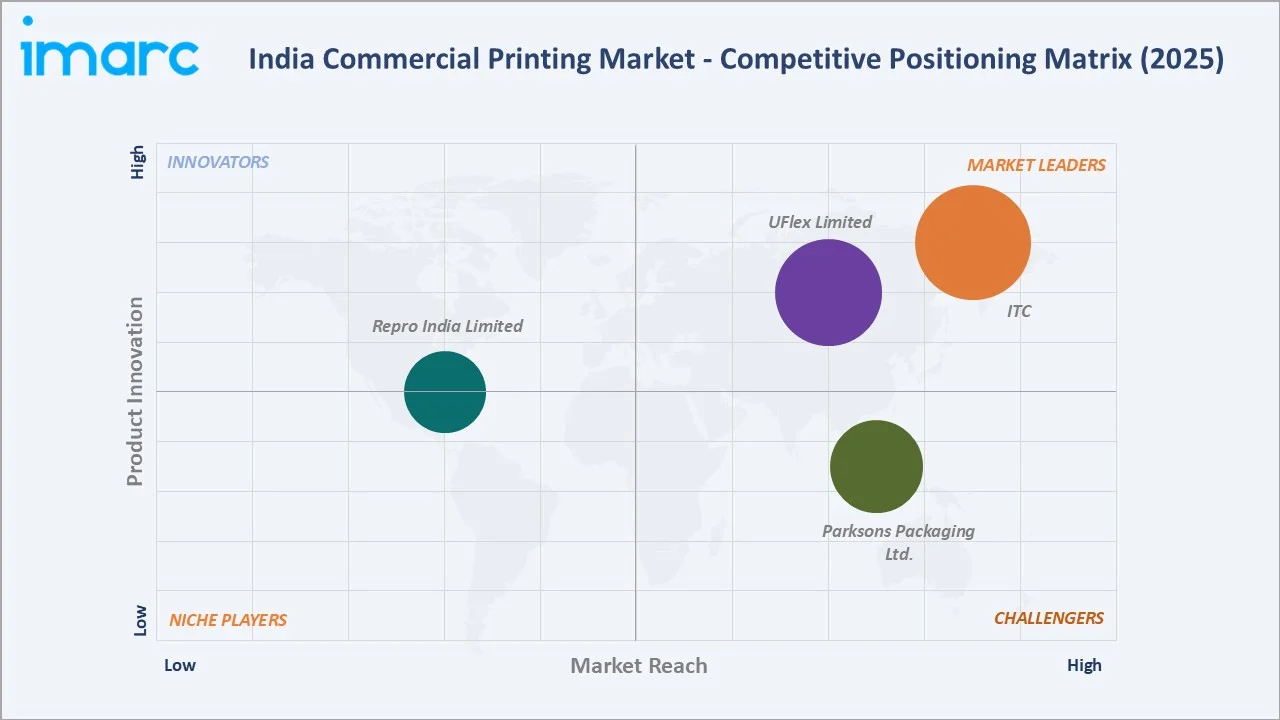

Competitive Landscape

The India commercial printing market is moderately fragmented, with established players dominating large-volume contracts while numerous regional and small-scale operators serve local demand. Technology adoption, client relationships, and diversified service offerings form the key competitive differentiators.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

UFlex Limited |

Flex Films |

Leader |

Leading integrated flexible packaging player; vertical integration; sustainable mono-material innovation; strong export base |

|

ITC |

ITC Packaging & Printing Business |

Leader |

Integrated packaging solutions; sustainable practices; strong FMCG linkage |

|

Parksons Packaging Ltd. |

Offset Printing, Flexography, Cold foil Printing |

Challenger |

Premium packaging and commercial printing; design innovation; multi-sector client base |

|

Repro India Limited |

Print on Demand (POD), Offset Book Printing Service |

Emerging |

Book printing and content solutions; digital production; export-oriented operations |

Key players include UFlex Limited, ITC, Parksons Packaging Ltd., and Repro India Limited, among others.

Key Company Profiles

UFlex Limited

UFlex Limited is India’s leading multinational flexible packaging and solutions company. Headquartered in Noida, the company operates across films, packaging, printing, holography, chemicals, engineering, and recycling verticals.

- Product Portfolio: Flex Films (BOPET, polyester films); holographic films and security solutions, printing inks and coatings; converting and packaging machinery.

- Recent Developments: The company has expanded its focus on sustainable packaging solutions by developing recyclable and mono-material substrates for FMCG and food packaging applications. The firm is also strengthening its domestic manufacturing and printing capabilities to address rising demand for high-quality flexible packaging solutions across India.

- Strategic Focus: Vertically integrated flexible packaging and printing operations; sustainable mono-material and recyclable substrate innovation; circular economy through PET and mixed-plastic recycling; export-led growth across global markets.

Parksons Packaging Ltd.

Parksons Packaging Ltd., founded in 1996, is one of India’s leading paper-based packaging companies, operating 12 manufacturing plants across the country. The company serves major FMCG, food and beverage, pharmaceutical, and retail brands with folding cartons, litho-laminated packaging, and high-quality printed packaging solutions across the Indian market.

- Product Portfolio: Folding cartons made from paperboard and plastic sheets; offset printing, flexography, cold foil printing, and embossing services; end-to-end packaging solutions from conceptualization to value-added final delivery.

- Recent Developments: The firm has continued to expand capacity and broaden its capabilities through technology investments and strategic acquisitions, including Fortuner Packaging in 2023.

- Strategic Focus: Premium folding-carton packaging; design and print innovation; diversified client base spanning FMCG, pharmaceuticals, food and beverage (F&B) items, home and personal care, and industrials.

ITC

ITC operates one of India’s most comprehensive packaging and printing divisions, ITC Packaging and Printing Business, leveraging its strong FMCG presence to drive integrated packaging solutions across food, personal care, and consumer product categories.

- Product Portfolio: Packaging solutions for food, personal care, and lifestyle products; printed cartons and labels; sustainable packaging materials.

- Recent Developments: ITC has strengthened its sustainable packaging initiatives, expanding the use of recyclable and biodegradable materials across its printing and packaging operations.

- Strategic Focus: Integrated packaging value chain leveraging FMCG scale, sustainability leadership, and advanced printing capabilities.

Market Concentration Analysis

The India commercial printing market is moderately fragmented, with the top five companies (UFlex Limited, ITC, Parksons Packaging Ltd., and Repro India Limited) estimated to hold approximately 15-20% of the total market revenue in 2025. The remaining market comprises thousands of small and medium-scale printers operating across regional clusters.

Barriers to entry in organized commercial printing include significant capital investment in modern presses, the need for skilled operators and color management expertise, and client relationship depth built over years of consistent service delivery.

Consolidation is gradually accelerating as larger players invest in digital capabilities, expand geographic reach, and acquire specialized printing operations. Scale advantages in procurement, technology adoption, and multi-location service delivery are reinforcing the competitive position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Image at 43.2% is the fastest-growing print type segment, supported by premium packaging and advertising demand. Packaging at 43.8% leads application growth, driven by e-commerce expansion and food processing sector requirements.

Emerging Markets

East India at 17.35% represents the highest-growth regional opportunity, with expanding industrialization, rising consumer demand, and growing investment in printing infrastructure across Kolkata, Patna, and Bhubaneswar.

Venture & Investment Trends

Investment is concentrated in digital press technology, automated finishing equipment, sustainable ink and substrate development, and cloud-based print management platforms. Venture capital interest is growing in print-tech startups offering on-demand printing, web-to-print platforms, and personalized packaging solutions.

Future Market Outlook (2026-2034)

The India commercial printing market is forecast to expand from USD 36.53 Billion in 2025 to USD 46.65 Billion by 2034 at a CAGR of 2.76%, adding roughly USD 10.12 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: continued packaging demand growth driven by FMCG and e-commerce; accelerating digital printing adoption across SMEs; sustainability-driven material innovation; and convergence of print with digital marketing technologies.

By 2034, digital printing is expected to capture a significantly larger share of commercial print volume, while offset lithography will retain dominance in high-volume packaging and publication runs. Automation and AI integration will redefine production efficiency across the value chain.

Research Methodology

Primary Research

Primary research included interviews with senior executives at leading commercial printers, packaging industry specialists, printing equipment distributors, and brand marketing managers, validating market sizing, regional demand patterns, and technology adoption trends.

Secondary Research

Secondary sources included industry association publications, government manufacturing statistics, trade show reports, company annual reports, investor presentations, and regulatory filings from listed printing and packaging companies.

Forecasting Models

Market forecasts used top-down and bottom-up models combining printing industry output data, packaging consumption trends, advertising expenditure growth, and technology adoption rates. Scenario analysis addressed raw material price variation and digital substitution impacts.

India Commercial Printing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Lithographic Printing, Digital Printing, Flexographic Printing, Screen Printing, Gravure Printing, Others |

| Print Types Covered | Image, Painting, Pattern, Others |

| Applications Covered | Packaging, Advertising, Publishing |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | UFlex Limited, ITC, Parksons Packaging Ltd., Repro India Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Commercial Printing Market Report

The market was valued at USD 36.53 Billion in 2025, driven by packaging demand, advertising growth, and rising adoption of digital printing technologies.

The market is projected to grow at a 2.76% CAGR from 2026 to 2034, reaching USD 46.65 Billion, supported by packaging expansion and technology modernization.

Image leads at 43.2% in 2025, driven by FMCG packaging and advertising collateral. Pattern at 24.0% follows through textile and decorative applications.

Packaging dominates at 43.8% in 2025, driven by food processing growth, e-commerce expansion, and regulatory labeling requirements across consumer products.

South India commands 34.15% in 2025, led by Chennai, Bengaluru, and Hyderabad, supported by strong industrial infrastructure and proximity to manufacturing hubs.

Leading players include UFlex Limited, ITC, Parksons Packaging Ltd., and Repro India Limited, among others.

Digital printing growth is driven by shorter turnaround times, lower minimum order quantities, customization capabilities, and declining equipment costs for commercial applications.

E-commerce expansion is driving demand for branded packaging, shipping labels, promotional inserts, and personalized unboxing materials across online retail platforms.

Sustainability is driving adoption of eco-friendly inks, recyclable substrates, waterless printing, and energy-efficient production as brands prioritize environmental responsibility.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)