India Commercial Vehicle Market Size, Share, Trends and Forecast by Vehicle Body Type, Propulsion Type, and Region, 2026-2034

India Commercial Vehicle Market Size, Share, Trends & Forecast (2026-2034)

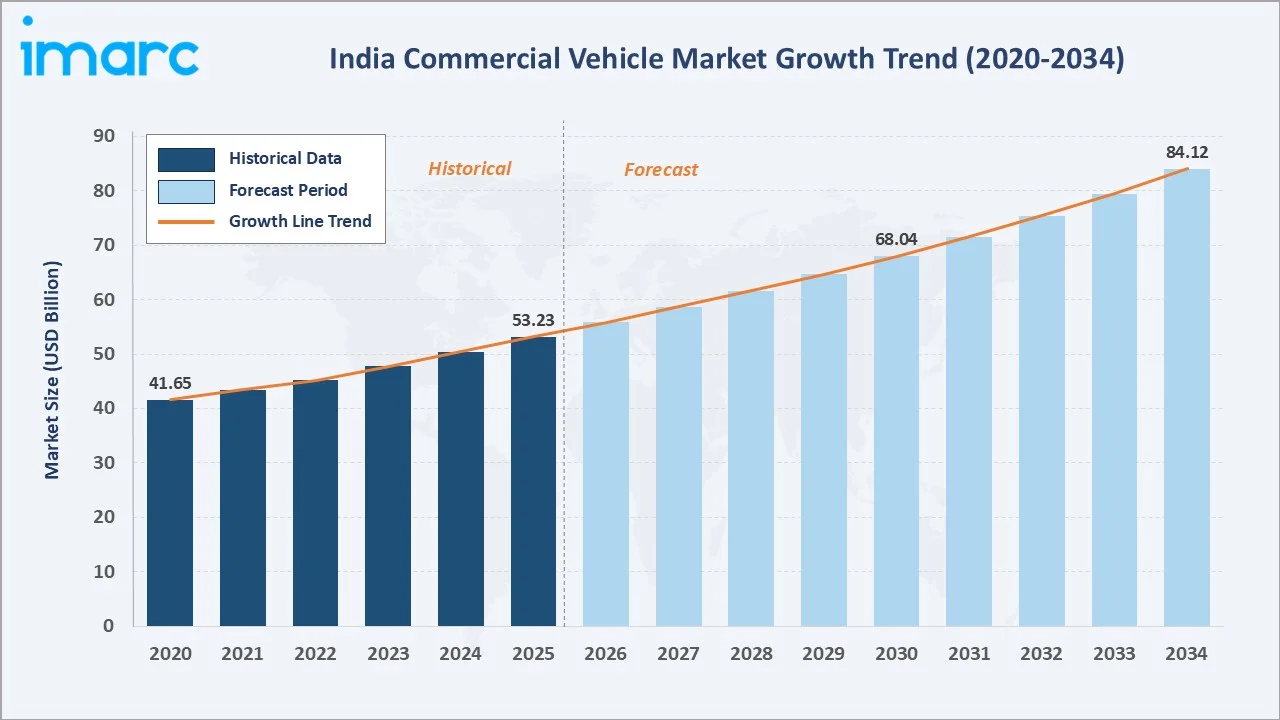

The India commercial vehicle market size reached USD 53.23 Billion in 2025 and is projected to reach USD 84.12 Billion by 2034, exhibiting a CAGR of 5.03% during 2026-2034. Government infrastructure investment, e-commerce-driven logistics growth, and accelerating fleet electrification are the primary forces shaping this market.

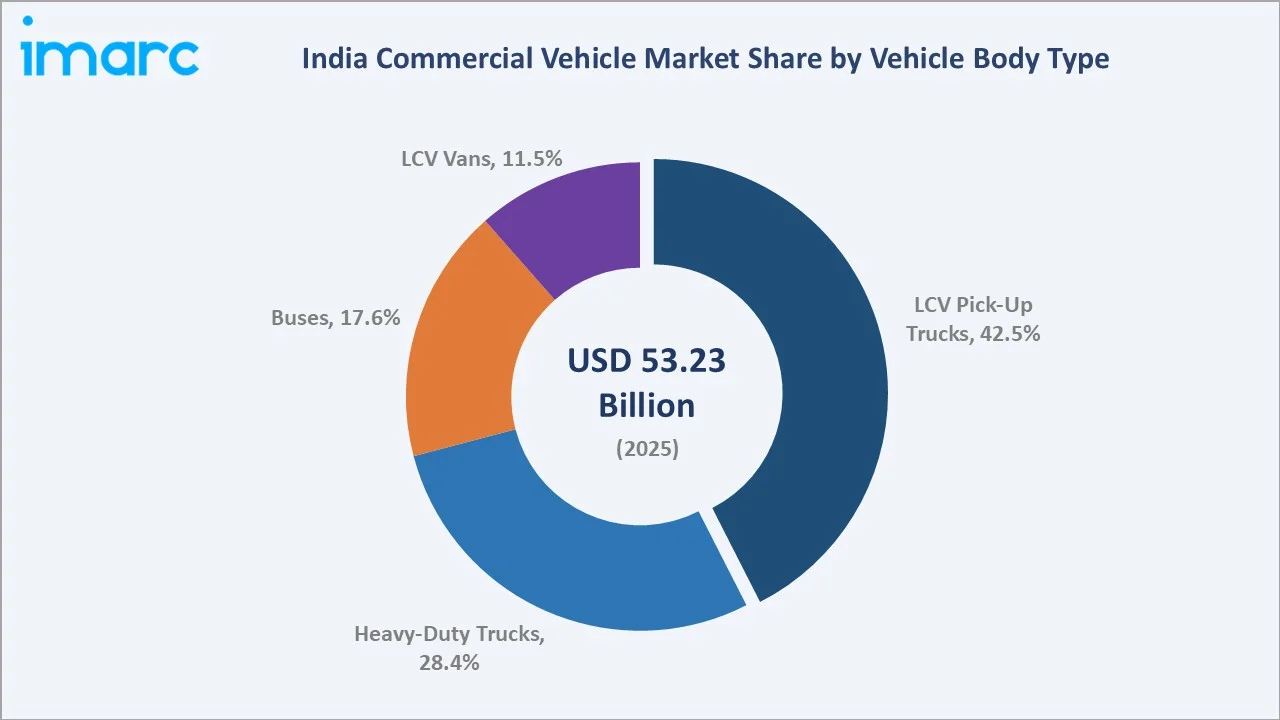

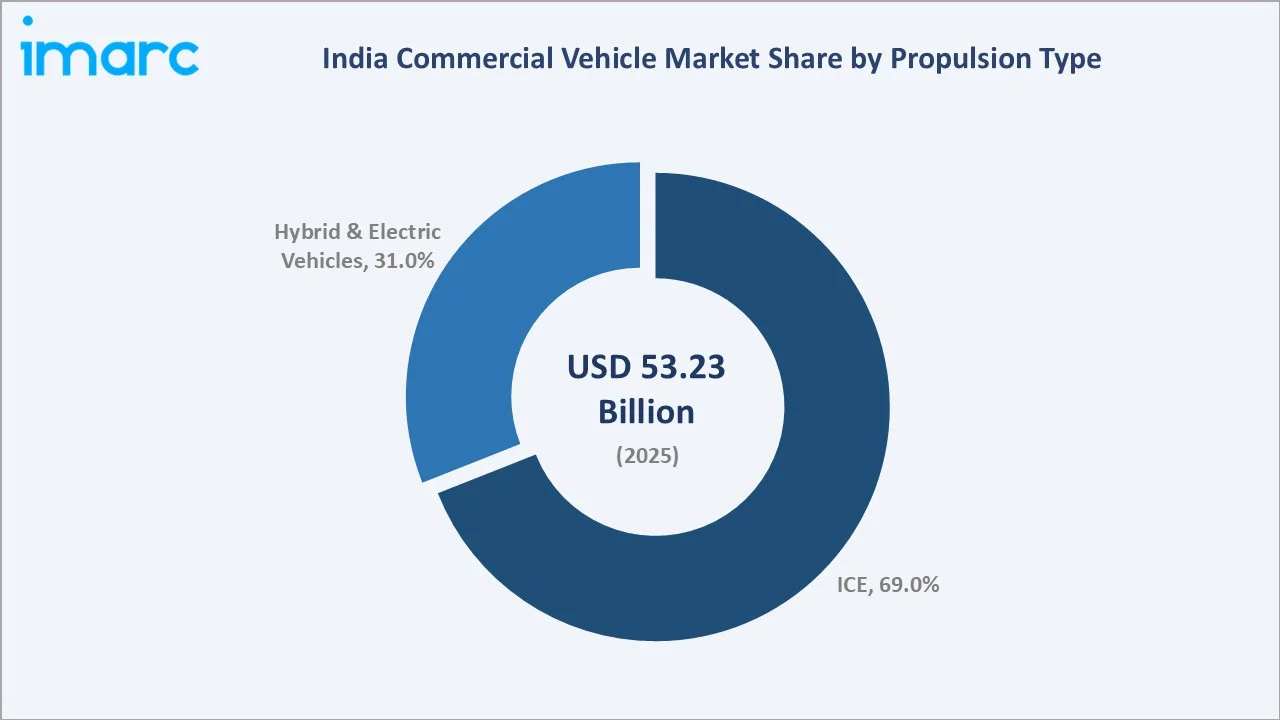

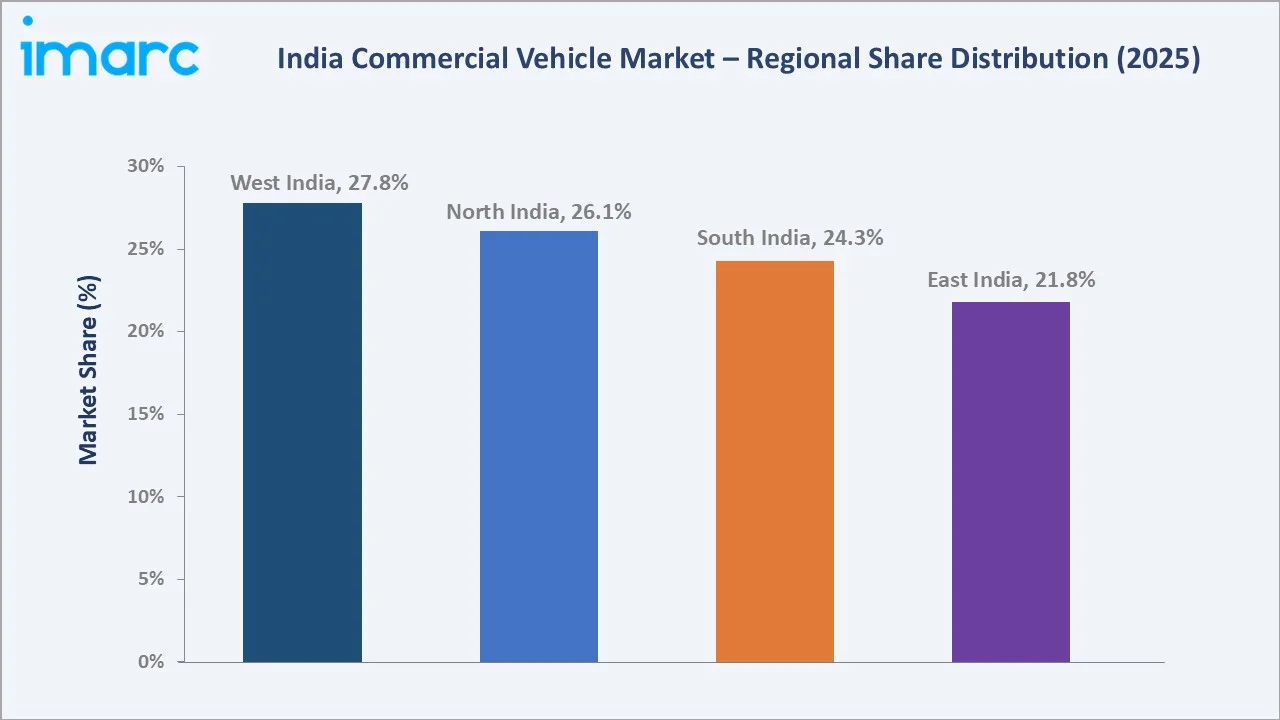

Light Commercial Pick-Up Trucks lead vehicle body type segmentation at 42.5% in 2025, driven by last-mile delivery expansion. ICE propulsion commands 69.0% share. West India dominates the regional landscape at 27.8%, underpinned by strong industrial output and port logistics infrastructure.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 53.23 Billion |

| Forecast Market Size (2034) | USD 84.12 Billion |

| CAGR (2026-2034) | 5.03% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Leading Vehicle Body Type | Light Commercial Pick-Up Trucks (42.5% share, 2025) |

| Leading Propulsion Type | ICE (69.0% share, 2025) |

| Leading Region | West India (27.8% share, 2025) |

The India commercial vehicle market growth from 2020 through 2034 reflects structural demand driven by infrastructure modernization, rising freight movement, and progressive electrification. The forecast to USD 84.12 Billion by 2034 captures sustained government investment, logistics sector formalization, and accelerating EV adoption.

To get more information on this market, Request Sample

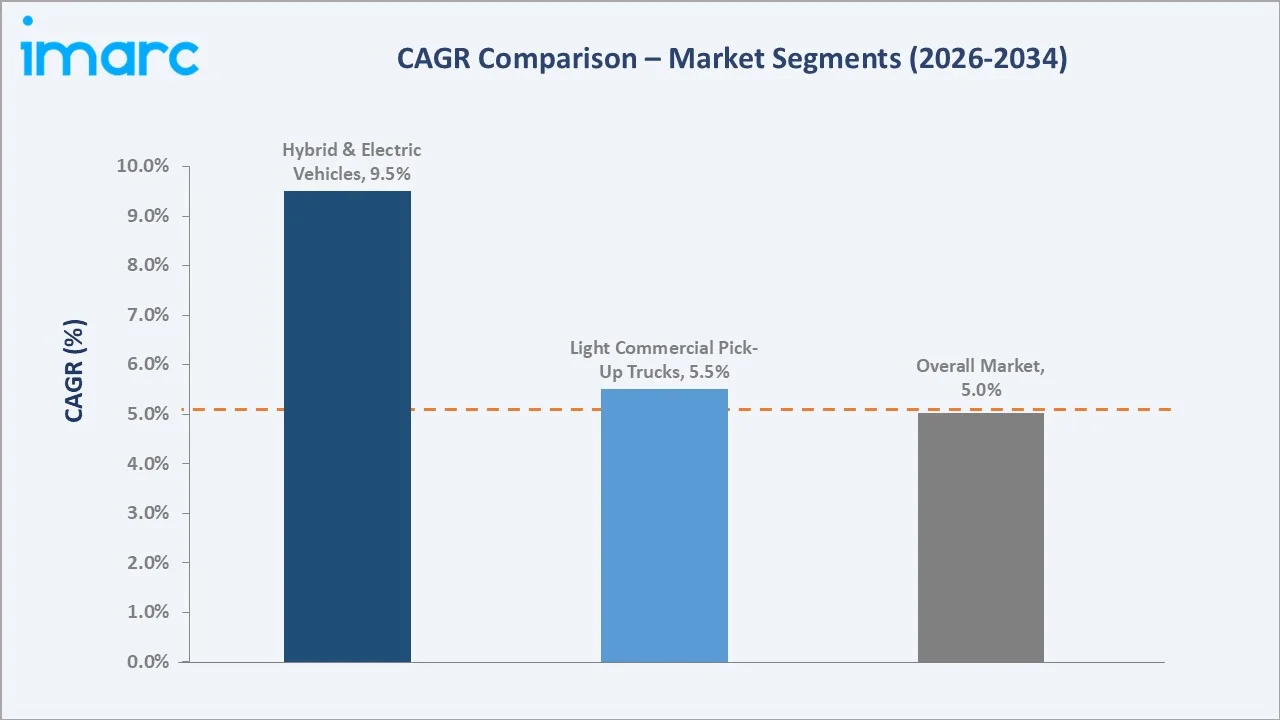

The CAGR trajectories across key vehicle body type and propulsion sub-segments highlight Hybrid and Electric Vehicles at approximately 9.50% CAGR and Light Commercial Pick-Up Trucks at approximately 5.50% CAGR as the fastest-growing categories within the India commercial vehicle market through 2034.

Executive Summary

The India commercial vehicle market is on a sustained growth trajectory from USD 53.23 Billion in 2025 to USD 84.12 Billion by 2034. The market encompasses light, medium, and heavy commercial vehicles deployed across freight logistics, passenger transport, construction, and e-commerce delivery applications throughout India.

Light Commercial Pick-Up Trucks lead at 42.5% in 2025, owing to their critical role in last-mile delivery, agricultural logistics, and urban freight. Heavy-Duty Commercial Trucks (28.4%) support large-scale industrial freight, mining, and construction operations across the national highway network.

ICE propulsion commands 69.0% share in 2025, underpinned by established diesel and CNG fueling infrastructure. Hybrid and Electric Vehicles (31.0%) are capturing accelerating demand, led by PM E-DRIVE policy support and rising fuel-cost pressures on fleet operators across urban and semi-urban markets.

West India dominates at 27.8% in 2025, supported by Maharashtra and Gujarat’s industrial base and port infrastructure. North India follows at 26.1%, South India at 24.3%, and East India at 21.8%, the latter driven by mining and natural resource logistics demand.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Vehicle Body Type | Light Commercial Pick-Up Trucks – 42.5% share (2025) |

| Leading Propulsion Type | ICE – 69.0% share (2025) |

| Leading Region | West India – 27.8% share (2025) |

| Second Largest Region | North India – 26.1% share (2025) |

| Top Companies | Tata Motors Limited, Mahindra & Mahindra Ltd, Eicher |

- Light Commercial Pick-Up Trucks at 42.5% dominate because rapid e-commerce expansion and urban-rural freight demand versatile, fuel-efficient trucks. Rising demand from agriculture, quick-commerce, and construction sectors sustains capital investment in pick-up truck procurement across all Indian geographies.

- ICE propulsion commands 69.0% share because diesel and CNG commercial vehicles benefit from established national refueling infrastructure, proven engine durability, and lower acquisition costs versus battery-electric alternatives for long-haul fleet operators.

- West India’s 27.8% regional dominance reflects Maharashtra and Gujarat’s unrivalled industrial output, port logistics activity, and freight corridor density. Major automotive manufacturing clusters and EXIM trade volumes sustain heavy-duty truck demand across the western region.

India Commercial Vehicle Market Overview

The India commercial vehicle market encompasses light commercial pick-up trucks, heavy-duty trucks, buses, and light commercial vans deployed across freight, passenger, and specialized applications. Market structure integrates OEM manufacturers, component suppliers, financing institutions, fleet operators, and regulatory bodies ensuring emission compliance and safety standards.

The ecosystem integrates domestic and global OEMs, component and ancillary manufacturers, financiers and NBFCs, fleet operators, logistics service providers, charging infrastructure developers, dealer networks, and regulatory agencies operating under the Ministry of Road Transport and Highways and SIAM framework.

Market Dynamics

To evaluate market opportunities, Request Sample

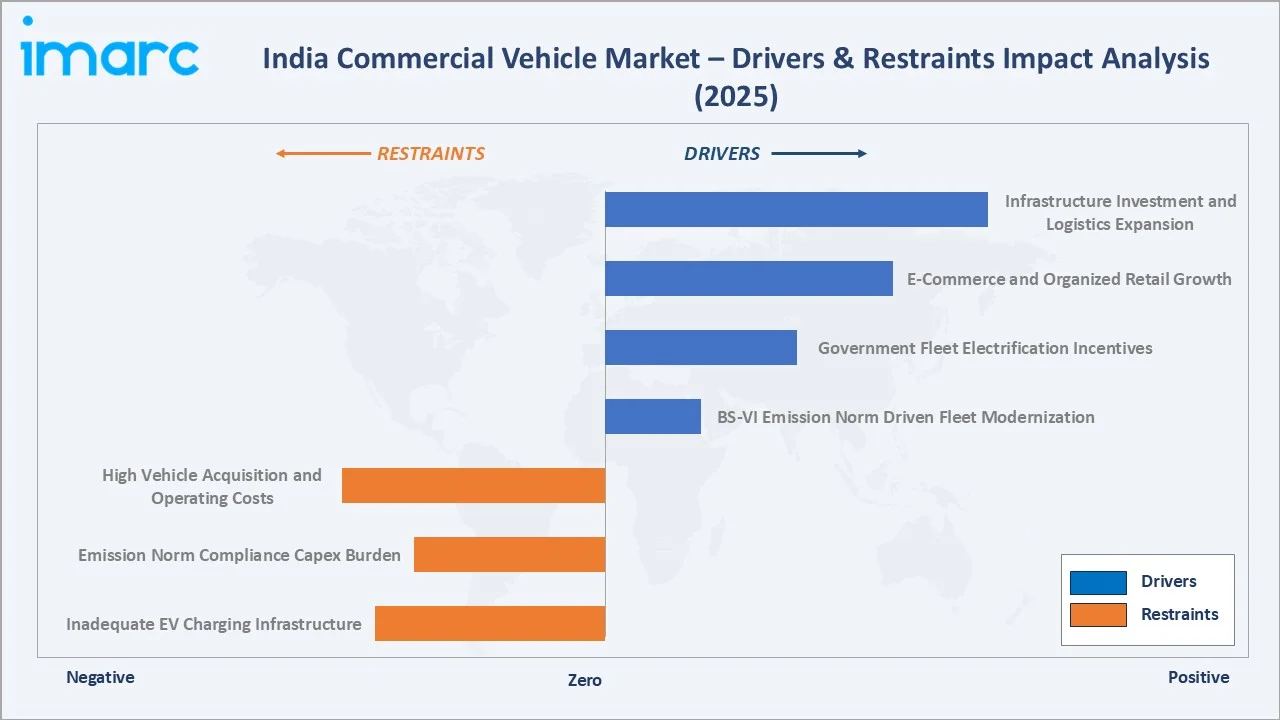

Market Drivers

- Infrastructure Investment and Logistics Expansion: Large-scale government initiatives including the Bharatmala highway corridor and Sagarmala port modernization are generating sustained demand for heavy-duty trucks. The National Industrial Corridor programme is catalyzing industrial freight movement and commercial vehicle procurement across India.

- E-Commerce and Organized Retail Growth: Rapid e-commerce platform expansion is fueling demand for light commercial pick-up trucks and vans across first- and last-mile delivery applications. Quick-commerce platforms operating on sub-hour delivery promises are driving compact urban delivery vehicle procurement nationwide.

- Government Fleet Electrification Incentives: PM E-DRIVE policy extensions, state EV subsidies, and preferential GST rates on electric commercial vehicles are accelerating electrification of bus and light commercial vehicle fleets. Intra-city electric bus deployment initiatives are generating large-volume procurement orders from state transport undertakings.

- BS-VI Emission Norm Driven Fleet Modernization: Stricter Bharat Stage VI emission standards have accelerated retirement of pre-compliant fleets and driven replacement demand for trucks, buses, and light commercial vehicles across both organized and unorganized fleet operator segments.

Market Restraints

- High Vehicle Acquisition and Operating Costs: Commercial vehicles represent significant capital investment for small and medium fleet operators. Rising finance costs, insurance premiums, and driver wages increase total cost of ownership, constraining fleet expansion among mid-tier logistics service providers and independent truck owners.

- Emission Norm Compliance Capex Burden: Transitioning from older BS-IV vehicles to BS-VI compliant commercial vehicles requires substantial investment, imposing financial strain on small fleet operators. Higher upfront vehicle costs and mandatory retrofitting requirements create short-term demand suppression in the price-sensitive segment.

- Inadequate EV Charging Infrastructure: Limited fast-charging infrastructure and inadequate battery swapping networks constrain electric commercial vehicle adoption beyond urban centers. Range anxiety, long charging times, and inconsistent grid reliability restrict fleet operator’s willingness to transition to electric vehicles at scale.

Market Opportunities

- Hydrogen Fuel Cell and CNG Commercial Vehicle Expansion: The government’s National Green Hydrogen Mission is creating opportunities for hydrogen ICE and fuel cell commercial vehicle development. CNG truck adoption is accelerating supported by expanding gas pipeline distribution networks across Tier-1 and Tier-2 city corridors.

- Cold Chain and Specialized Logistics Fleet Growth: India’s expanding pharmaceutical, food processing, and agri-export sectors are creating significant demand for refrigerated trucks and specialized commercial vehicles. Cold chain logistics investment represents a high-growth adjacent market for OEMs and bodybuilders.

Market Challenges

- Driver Shortage and Skilled Workforce Deficit: India’s commercial transport sector faces a severe shortage of trained and licensed commercial vehicle drivers, limiting fleet utilization rates. Attrition, aging driver demographics, and insufficient vocational training infrastructure constrain logistics capacity expansion despite growing vehicle procurement.

- Competitive Pressure from Rail and Multimodal Freight: Expanding rail freight capacity under the Dedicated Freight Corridor programme offers cost-competitive alternatives to road haulage for bulk commodity movement. Multimodal logistics platforms diverting cargo from road to rail create substitution pressure on heavy commercial vehicle demand.

Emerging Market Trends

1. Electric Vehicle Adoption and Fleet Electrification

Government incentives under PM E-DRIVE and state EV policies are accelerating electric bus and LCV procurement across India. Fleet operators are evaluating total cost of ownership benefits as battery costs decline, and OEMs are rapidly expanding electric model portfolios to capture early-mover advantage in this high-growth segment.

2. Telematics, IoT, and Connected Fleet Technology

Fleet management platforms integrating GPS tracking, driver behavior analytics, fuel monitoring, and predictive maintenance are becoming standard across organized fleet operators. AIS 140 mandates have accelerated telematics deployment, improving fleet efficiency and reducing operational costs across the sector.

3. CNG and Alternative Fuel Expansion

Expanding natural gas pipeline infrastructure and rising diesel prices are driving CNG commercial vehicle adoption beyond metro cities. OEMs are expanding CNG model availability across trucks and buses. LNG heavy trucks are gaining interest for long-haul freight corridors where CNG refueling infrastructure is insufficient.

4. ADAS and Safety Technology Integration

Advanced Driver Assistance Systems including automatic emergency braking, lane departure warning, and fatigue detection are being introduced in premium commercial vehicles. Regulatory mandates for ADAS in new commercial vehicles are accelerating technology adoption and improving road safety outcomes across Indian freight corridors.

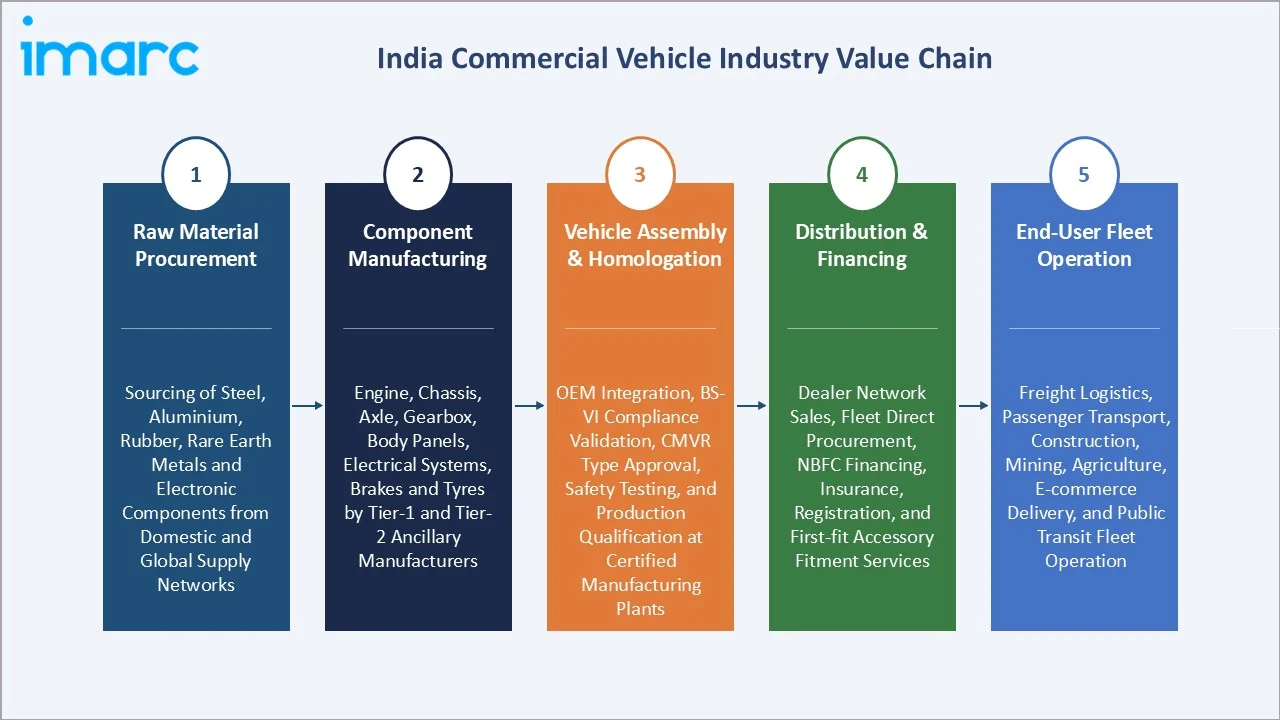

Industry Value Chain Analysis

The India commercial vehicle value chain spans five integrated stages from raw material procurement through end-user fleet operation. OEM assembly captures primary value through engineering integration, while financial services and aftersales networks generate recurring revenue supporting long-term customer relationships.

| Stage | Key Activities |

|---|---|

| Raw Material Procurement | Sourcing of steel, aluminium, rubber, glass, plastics, rare earth metals, and electronic components from domestic and global supply networks |

| Component Manufacturing | Engine, chassis, axle, gearbox, body panels, electrical systems, brakes, and tyres produced by Tier-1 and Tier-2 ancillary manufacturers |

| Vehicle Assembly & Homologation | OEM integration, BS-VI compliance validation, CMVR type approval, safety testing, and production qualification at certified manufacturing plants |

| Distribution & Financing | Dealer network sales, fleet direct procurement, NBFC financing, insurance, registration, and first-fit accessory fitment services |

| End-User Fleet Operation | Freight logistics, passenger transport, construction, mining, agriculture, e-commerce delivery, and public transit fleet operation |

Vehicle assembly and homologation stages capture the highest value in the India commercial vehicle chain, requiring specialized engineering expertise and BS-VI regulatory validation knowledge. Aftersales service, spare parts, and fleet management consulting represent growing recurring revenue streams improving long-term customer retention.

Technology Landscape in the India Commercial Vehicle Industry

Battery Electric Vehicle (BEV) Technology for Commercial Fleets

LFP battery chemistry is emerging as the preferred platform for electric commercial vehicles in India, offering lower cost, improved thermal stability, and longer cycle life. OEMs are developing dedicated BEV platforms for light commercial vans and city buses with ranges exceeding 250 km per charge to address fleet operator requirements.

Hydrogen Internal Combustion Engine (H-ICE) Technology

Hydrogen ICE technology is gaining traction as a near-term decarbonization pathway for heavy commercial vehicles where battery electric solutions face range limitations. Ashok Leyland and Tata Motors are actively developing H-ICE truck prototypes under national pilot programmes, targeting long-haul freight corridor applications.

Advanced Driver Assistance Systems (ADAS)

ADAS technologies including forward collision warning, automatic emergency braking, lane departure warning, and electronic stability control are being integrated into new commercial vehicle generations. Indian OEMs are collaborating with global technology partners to develop cost-appropriate ADAS solutions for price-sensitive markets.

Telematics and Vehicle Connectivity Platforms

AIS 140-compliant vehicle tracking units are now mandatory across Indian commercial vehicles. OEMs are building advanced telematics platforms offering real-time diagnostics, predictive maintenance alerts, driver scorecards, and fleet analytics to enable new logistics service models built on real-time freight visibility data.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Body Type | Light Commercial Pick-Up Trucks | 42.5% | 2025 |

| Propulsion Type | ICE | 69.0% | 2025 |

| Region | West India | 27.8% | 2025 |

By Vehicle Body Type

Light Commercial Pick-Up Trucks commanded a 42.5% majority share in 2025 owing to their essential role in last-mile delivery, agri-logistics, and urban freight movement. Rapidly expanding e-commerce platforms and quick-commerce operators are sustaining high procurement volumes of pick-up trucks across urban and peri-urban markets throughout India.

To access detailed market analysis, Request Sample

Heavy-Duty Commercial Trucks (28.4%) support large-scale freight, mining, and construction operations across India’s industrial corridors. Buses (17.6%) address public transport, school transport, and inter-city travel demand. Light Commercial Vans (11.5%) serve urban delivery, ambulance, and specialized payload applications nationally.

By Propulsion Type

ICE dominates at 69.0% in 2025, driven by established diesel and CNG fueling infrastructure and lower total acquisition costs for fleet operators. Proven reliability for long-distance freight, wide dealer service networks, and readily available driver expertise reinforce ICE vehicle preference across India’s commercial vehicle market.

Hybrid and Electric Vehicles (31.0%) are capturing accelerating demand, led by government subsidy support, PM E-DRIVE incentives, and growing fleet operator awareness of electric total cost of ownership benefits for intra-city operations. Electric bus and LCV adoption is advancing fastest in Maharashtra, Delhi, and Gujarat.

Regional Market Insights

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| West India | 27.8% | Robust industrial base, port logistics in Maharashtra and Gujarat, concentrated HCV freight movement |

| North India | 26.1% | Large agriculture and FMCG logistics demand, national highway freight, Delhi NCR e-commerce hub driving LCV demand |

| South India | 24.3% | IT and manufacturing sector logistics, port-led freight, growing automobile and electronics manufacturing demand |

| East India | 21.8% | Coal, iron ore, and mineral logistics driving HCV demand; improving highway connectivity accelerating market growth |

West India’s 27.8% market dominance in 2025 is driven by Maharashtra and Gujarat’s industrial output, port logistics activity, and freight corridor density. The Mumbai-Pune-Nashik manufacturing corridor generates sustained heavy commercial vehicle demand. Gujarat’s Kandla and Maharashtra’s JNPT port logistics sustain high freight vehicle utilization.

North India at 26.1% is anchored by the Delhi NCR logistics hub, Punjab and Haryana agricultural freight, and the Dedicated Freight Corridors. South India at 24.3% benefits from diversified manufacturing spanning automotive, electronics, and pharmaceuticals. East India at 21.8% is driven by mining and steel sector freight logistics with improving connectivity.

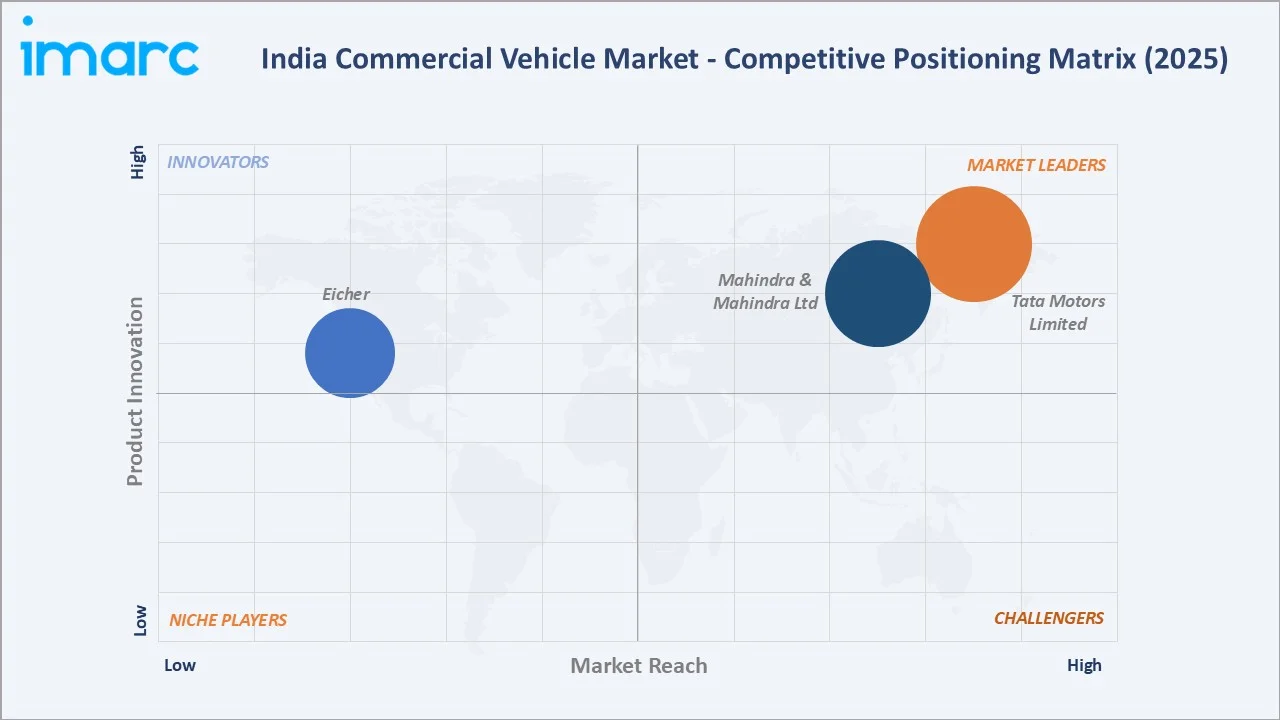

Competitive Landscape

The India commercial vehicle market is highly consolidated at the OEM level, with domestic leaders and global joint ventures collectively commanding dominant market shares. Leading manufacturers leverage product breadth, dealer network depth, financing partnerships, and brand trust to maintain competitive advantage across light, medium, and heavy vehicle segments.

| Company Name | Key Products / Operations | Market Position | Global Strategic Focus |

|---|---|---|---|

| Tata Motors Limited | Tata LPT, Tata Signa, Tata Prima, Tata Ultra, Tata Starbus, Tata Cityride, Tata Magic, Winger, Tata Ace, Tata Intra, Tata Yodha | Leader | Expanding EV portfolio; advancing ADAS and connected truck platforms |

| Mahindra & Mahindra Ltd | Bolero Pik-up, Bolero Camper, Veero, Maxx HD, Jayo, Furio, Cruzio, Blazo X | Leader | Leading EV pick-up truck segment; expanding LCV range; ADAS integration |

| Eicher | Eicher Pro Plus Series | Established | Expanding mid-segment trucks; building CNG and alternative fuel range |

Key players include Tata Motors Limited, Mahindra & Mahindra Ltd, Eicher, and others.

Key Company Profiles

Tata Motors Limited

Tata Motors Limited is India’s largest commercial vehicle manufacturer offering a comprehensive range of light, medium, and heavy commercial vehicles across goods and passenger applications. The portfolio spans urban delivery LCVs to heavy haulage trucks and electric buses.

- Product Portfolio: Tata LPT, Tata Signa, Tata Prima, Tata Ultra, Tata Starbus, Tata Cityride, Tata magic, Winger, Tata Ace, Tata Intra, Tata Yodha, and others.

- Recent Developments: In May 2024, Tata Motors expanded its electric commercial vehicle range with the launch of the Tata Ace EV 1000, a zero-emission mini truck targeting urban last-mile delivery operations with a 161 km range per charge, designed for dense metro logistics networks.

- Strategic Focus: Tata Motors is executing a dual-track strategy of sustaining ICE truck leadership while aggressively expanding its zero-emission commercial vehicle portfolio. The company is investing in connected truck telematics, fleet mobility solutions, and dedicated EV manufacturing infrastructure to consolidate market leadership through 2034.

Mahindra & Mahindra Ltd

Mahindra & Mahindra Ltd is a leading Indian commercial vehicle manufacturer with a dominant presence in the light commercial vehicle segment, particularly pick-up trucks and small commercial vehicles. The company’s commercial vehicle division is actively developing electric LCV platforms targeting the rapidly growing e-commerce delivery market.

- Product Portfolio: Bolero Pick-up, Bolero Camper, Veero, Maxx HD, Jayo, Furio, Cruzio, Blazo X, and others.

- Recent Developments: In September 2024, Mahindra & Mahindra launched the all-new Mahindra Veero, expanding its presence in India’s light commercial vehicle (LCV <3.5-tonne) segment. Built on Mahindra’s new Urban Prosper Platform (UPP), the Veero is designed to improve operating efficiency, payload capability, safety, and driver comfort for commercial users.

- Strategic Focus: Mahindra & Mahindra is investing heavily in expanding its LCV portfolio through new multi-fuel platform launches, while scaling its electric commercial vehicle range to capture growing e-commerce and last-mile delivery demand.

Market Concentration Analysis

The India commercial vehicle market is highly concentrated, with major players collectively holding the majority of domestic market share. The top three players benefit from extensive dealer networks, strong brand equity, captive financing arms, and deep aftermarket service infrastructure creating substantial barriers to new entrants.

Investment & Growth Opportunities

Fastest-Growing Segments

Hybrid and Electric Vehicles represents the highest-growth propulsion segment through 2034 at approximately 9.50% CAGR, capturing government incentive-driven demand for electric buses and urban delivery vehicles. Light Commercial Pick-Up Trucks lead vehicle body type growth at approximately 5.50% CAGR, driven by e-commerce logistics expansion nationally.

Emerging Markets

East India and Tier-2/Tier-3 city markets are emerging as high-growth frontiers. Improving road infrastructure under the Bharatmala programme, rising agricultural incomes, and expanding organized logistics penetration in secondary cities are generating incremental commercial vehicle demand with significant untapped volume growth potential.

Venture & Investment Trends

Private equity and strategic investors are increasing capital allocation to Indian electric commercial vehicle startups and fleet electrification platforms. Government Production-Linked Incentive schemes for automotive EV components and battery manufacturing are catalyzing private capital mobilization in the Indian commercial vehicle electrification value chain.

Future Market Outlook (2026-2034)

The India commercial vehicle market is forecast to expand from USD 53.23 Billion in 2025 to USD 84.12 Billion by 2034 at a CAGR of 5.03%, driven by infrastructure investment, logistics formalization, fleet electrification, and sustained freight demand growth across India’s expanding industrial corridors through the forecast horizon.

Three structural forces will shape the market through 2034: government infrastructure spending under Bharatmala, Sagarmala, and NIP will sustain heavy commercial vehicle procurement; e-commerce and organized retail expansion will drive LCV segment growth; and PM E-DRIVE plus state EV policies will accelerate commercial fleet electrification, rebalancing the propulsion mix toward hybrid and electric platforms by 2030.

Research Methodology

Primary Research

Primary research encompassed structured interviews with commercial vehicle OEM executives, fleet operators, logistics service providers, auto component manufacturers, and government transport officials. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the India commercial vehicle market.

Secondary Research

Key secondary sources include SIAM vehicle sales data, MoRTH transport statistics, CMVR regulatory publications, annual reports from leading OEMs, ACMA component industry reports, trade publications covering automotive and logistics sectors, and government scheme notifications covering PM E-DRIVE and BS-VI emission norms.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating vehicle registration data, freight index trends, infrastructure investment pipeline analysis, and fleet operator surveys. Scenario modelling encompassed base, optimistic, and conservative cases through the 2034 horizon.

India Commercial Vehicle Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Body Types Covered | Buses, Heavy-Duty Commercial Trucks, Light Commercial Pick-Up Trucks, Light Commercial Vans |

| Propulsion Types Covered |

|

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Tata Motors Limited, Mahindra & Mahindra Ltd, Eicher, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Commercial Vehicle Market Report

The India commercial vehicle market reached USD 53.23 Billion in 2025, reflecting sustained demand driven by large-scale infrastructure investment, e-commerce logistics growth, fleet modernization under BS-VI norms, and expanding industrial freight movement across the country.

The market is projected to reach USD 84.12 Billion by 2034, growing at a CAGR of 5.03% during 2026-2034, driven by infrastructure development, logistics formalization, fleet electrification, and sustained demand from industrial, agricultural, and e-commerce sectors.

Light Commercial Pick-Up Trucks lead the market with a 42.5% share in 2025, driven by e-commerce last-mile delivery demand, agricultural logistics, and urban freight applications. This segment is expected to maintain leadership through 2034.

ICE commands the largest propulsion share at 69.0% in 2025, underpinned by established fueling infrastructure and proven reliability. Hybrid and Electric Vehicles at 31.0% are the fastest-growing propulsion segment driven by government incentives and declining battery costs.

West India dominates with a 27.8% share in 2025, supported by Maharashtra and Gujarat’s industrial output, port logistics infrastructure, and concentrated HCV freight movement across major industrial corridors.

Key drivers include government infrastructure investment (Bharatmala, NIP), rapid e-commerce logistics growth, BS-VI fleet modernization demand, PM E-DRIVE fleet electrification incentives, and rising industrialization across manufacturing corridors nationwide.

Major challenges include high vehicle acquisition costs for small fleet operators, BS-VI compliance capex burden, inadequate EV charging infrastructure outside metros, skilled driver shortage, and competitive pressure from rail freight alternatives.

Leading companies include Tata Motors Limited, Mahindra & Mahindra Ltd, Eicher, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)