India Compact Loaders Market Size, Share, Trends and Forecast by Application, Product Type, and Region, 2026-2034

India Compact Loaders Market Summary:

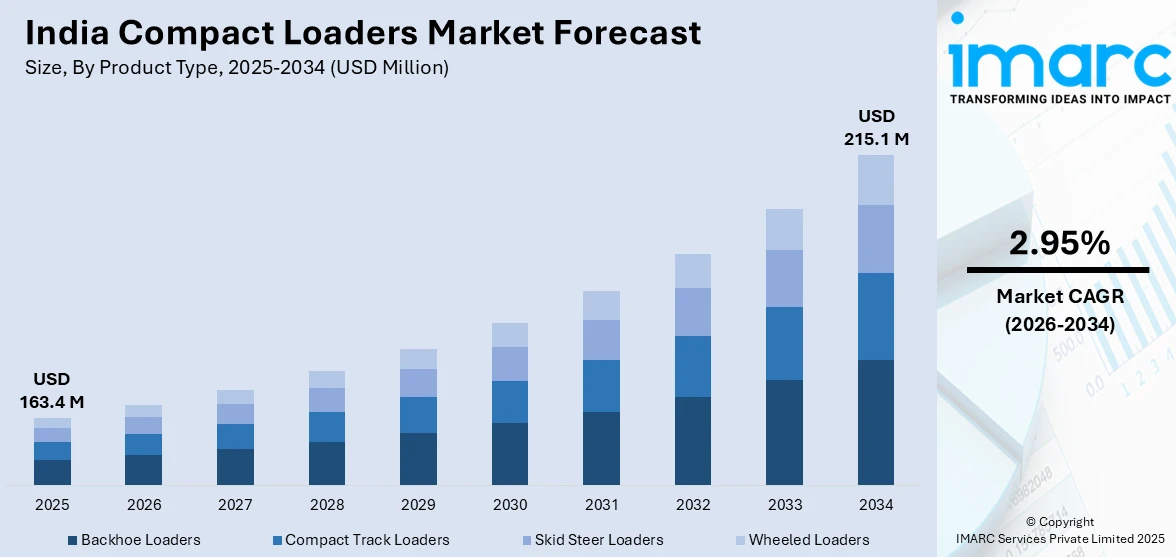

The India compact loaders market size was valued at USD 163.4 Million in 2025and is projected to reach USD 215.1 Million by 2034, growing at a compound annual growth rate of 2.95% from 2026-2034.

The India compact loaders market is experiencing robust expansion driven by accelerating infrastructure development, rapid urbanization, and growing construction activities across residential, commercial, and industrial sectors. The versatility of compact loaders in performing multiple tasks including excavation, material handling, and site preparation makes them indispensable in modern construction operations. Rising agricultural mechanization and industrial modernization initiatives are further propelling market demand.

Key Takeaways and Insights:

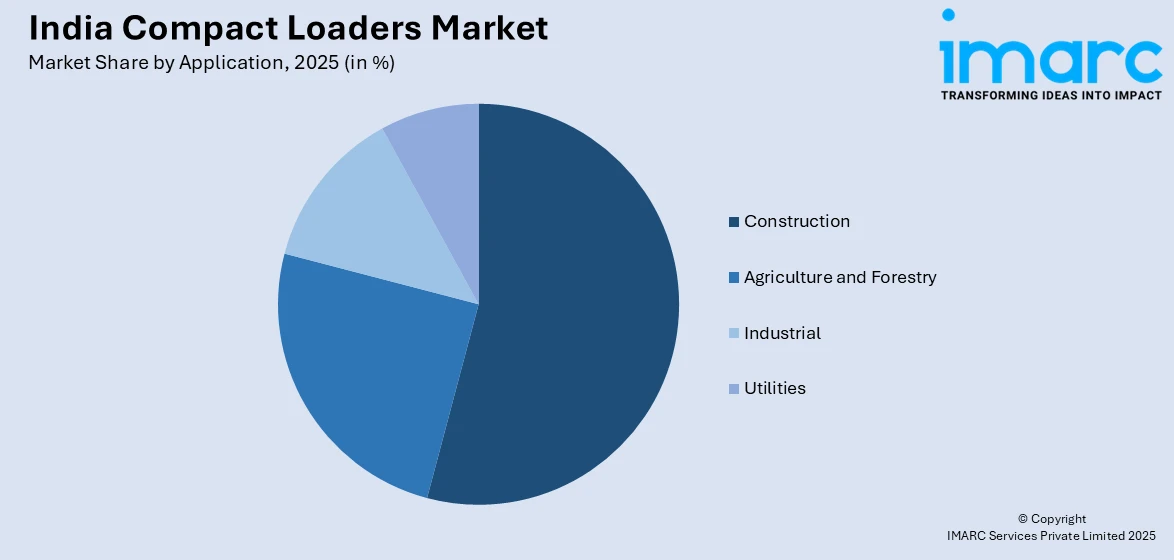

- By Application: Construction dominates the market with a share of 54.3% in 2025, owing to extensive infrastructure development projects including highways, railways, and urban development initiatives. The National Infrastructure Pipeline's sustained investment thrust, and smart city developments are accelerating construction equipment deployment across the nation.

- By Product Type: Backhoe loaders lead the market with a share of 38.6% in 2025, reflecting strong demand for versatile equipment capable of performing excavation, trenching, and material handling operations. Their multi-functionality and cost-effectiveness make them preferred choices for contractors across diverse construction applications.

- By Region: West India represents the largest region with 34.1% share in 2025, driven by Maharashtra and Gujarat's industrial corridors, port infrastructure expansions, and major urban development projects including the Mumbai Coastal Road and Gujarat International Finance Tec-City developments.

- Key Players: Key players drive the India compact loaders market by expanding manufacturing capacities, introducing technologically advanced equipment with enhanced fuel efficiency, and strengthening nationwide dealer networks. Strategic investments in after-sales services, operator training programs, and flexible financing solutions ensure consistent equipment availability and customer support across diverse market segments.

To get more information on this market Request Sample

The India compact loaders market is positioned for sustained growth as the country pursues ambitious infrastructure modernization under the PM Gati Shakti National Master Plan, a transformative initiative integrating multimodal connectivity across sixteen ministries with planned investments. This coordinated infrastructure approach is generating substantial demand for versatile construction equipment capable of operating efficiently across diverse applications including road construction, urban development, and industrial projects. The construction equipment industry witnessed significant expansion in recent fiscal years, with earthmoving equipment including backhoe loaders and excavators accounting for the majority of sales volumes. Government initiatives such as the Bharatmala Pariyojana highway development program, which continue to drive equipment demand. The market's growth trajectory is further supported by increasing mechanization in agriculture, expansion of rental and leasing services providing equipment access to small contractors, and the transition toward emission-compliant machinery meeting CEV Stage V standards. Regional development disparities present opportunities for market expansion as infrastructure investments increasingly target tier-two and tier-three cities alongside established metropolitan markets.

India Compact Loaders Market Trends:

Rising Adoption of Technologically Advanced Equipment

The India compact loaders market is witnessing increasing adoption of technologically advanced equipment featuring telematics, GPS tracking, and automated control systems that enhance operational efficiency and productivity. Manufacturers are integrating smart connectivity solutions enabling real-time machine monitoring, predictive maintenance alerts, and fleet management capabilities. These technological advancements reduce operational downtime, optimize fuel consumption, and improve overall equipment utilization, making advanced compact loaders increasingly attractive for contractors seeking competitive operational advantages in demanding project environments. In 2024, JCB India launched LiveLink 4.0, the next-generation telematics platform that enables machine users to make quick and informed decisions maximizing machine uptime, productivity, and profitability. The upgraded system renders advanced machine insights and analytics, with instant critical health and service alerts ensuring machines are always operational and warned of potential failures before they occur.

Growing Preference for Fuel-Efficient and Emission-Compliant Machinery

Environmental regulations and rising fuel costs are driving demand for fuel-efficient compact loaders meeting stringent emission standards. The transition to CEV Stage V emission norms is compelling manufacturers to develop cleaner, more efficient equipment while operators seek machinery that delivers lower operating costs and reduced environmental impact. This sustainability focus is accelerating innovation in engine technologies, with manufacturers achieving significant improvements in fuel efficiency while maintaining performance capabilities essential for demanding construction applications.

Expansion of Equipment Rental and Leasing Services

The rental and leasing segment is experiencing substantial growth as contractors increasingly prefer flexible equipment access over ownership, particularly for project-based requirements. This trend is democratizing access to modern compact loaders for small and medium enterprises previously constrained by high capital costs. Rental platforms offering pay-per-use models with comprehensive maintenance support are expanding nationwide, enabling contractors to deploy right-sized equipment for specific project requirements while avoiding the financial burden of equipment ownership and maintenance.

Market Outlook 2026-2034:

The India compact loaders market outlook remains positive through the forecast period, underpinned by sustained government infrastructure investments and expanding private sector participation in construction activities. The National Infrastructure Pipeline encompassing projects across transportation, energy, and urban development sectors continues providing robust demand foundations. Rising urbanization, estimated to reach substantial levels by decade-end, drives construction activity in residential and commercial segments. Agricultural mechanization initiatives supported by government subsidies expand equipment applications beyond traditional construction. The emergence of electric and hybrid compact loaders presents opportunities for manufacturers as environmental sustainability becomes increasingly prioritized across infrastructure development projects nationwide. The market generated a revenue of USD 163.4 Million in 2025 and is projected to reach a revenue of USD 215.1 Million by 2034, growing at a compound annual growth rate of 2.95% from 2026-2034.

India Compact Loaders Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Construction |

54.3% |

|

Product Type |

Backhoe Loaders |

38.6% |

|

Region |

West India |

34.1% |

Application Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Agriculture and Forestry

- Industrial

- Utilities

Construction dominates with a market share of 54.3% of the total India compact loaders market in 2025.

The construction segment commands the largest share of the India compact loaders market, driven by extensive infrastructure development across the country. The National Infrastructure Pipeline spanning transportation, energy, and urban development sectors creates sustained demand for versatile compact loading equipment. Major highway construction programs including Bharatmala Pariyojana, require substantial compact loader deployment for earthmoving, material handling, and site preparation operations. Smart city development initiatives across designated cities further strengthen construction equipment demand.

Urban construction activities including metro rail expansions, commercial complex development, and residential housing projects contribute significantly to segment growth. The government's allocation of INR 11.21 Lakh Crore for infrastructure capital expenditure in the Union Budget 2025-26 demonstrates continued commitment to construction sector expansion. Real estate development projected to reach substantial valuation by mid-century supports long-term equipment demand. Compact loaders' ability to operate efficiently in confined urban spaces while performing multiple functions including excavation, loading, and material transport makes them indispensable for modern construction project execution across diverse site conditions.

Product Type Insights:

- Compact Track Loaders

- Skid Steer Loaders

- Backhoe Loaders

- Wheeled Loaders

Backhoe loaders lead with a share of 38.6% of the total India compact loaders market in 2025.

Backhoe loaders maintain market leadership owing to their exceptional versatility in performing excavation, trenching, loading, and material handling operations with a single machine. This multi-functionality delivers significant cost advantages for contractors managing diverse project requirements without maintaining extensive equipment fleets. The India backhoe loaders market is expected to reach USD 944.45 Million by 2033, reflecting strong demand from construction, mining, and agricultural sectors. Rural infrastructure development under schemes like Pradhan Mantri Awas Yojana further accelerates backhoe loader adoption for housing and sanitation project execution across remote locations.

Manufacturers continue enhancing backhoe loader capabilities through technological innovations including improved fuel efficiency, enhanced operator comfort features, and advanced hydraulic systems delivering superior performance. The transition to CEV Stage V emission standards has driven equipment upgrades incorporating cleaner engine technologies. Comprehensive dealer networks ensure nationwide service availability and parts support, critical factors influencing purchase decisions. Flexible financing options and competitive pricing strategies by manufacturers make backhoe loaders accessible to contractors across various project scales, sustaining segment dominance throughout the forecast period.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 34.1% share of the total India compact loaders market in 2025.

West India commands market leadership driven by Maharashtra and Gujarat's robust construction activities encompassing industrial development, port infrastructure expansions, and major urban projects. The Delhi-Mumbai Industrial Corridor traversing both states generates sustained equipment demand for manufacturing facility construction and supporting infrastructure development. The Western Dedicated Freight Corridor connecting Dadri to Jawaharlal Nehru Port creates additional equipment requirements for railway infrastructure construction. Mumbai's urban transformation including the Coastal Road Project and metro expansions requires substantial compact loader deployment for excavation and material handling operations.

Gujarat's industrial investment initiatives including Gujarat International Finance Tec-City and Dholera Special Investment Region attract equipment demand for commercial and industrial construction projects. The region's developed dealer networks and service infrastructure ensure equipment availability and support. Port development activities at Jawaharlal Nehru Port and the upcoming Vadhavan Port project requiring investments of approximately INR 76,200 crore create sustained demand for earthmoving and material handling equipment throughout the forecast period. Maharashtra and Gujarat's economic significance ensures continued infrastructure investments supporting regional market dominance.

Market Dynamics:

Growth Drivers:

Why is the India Compact Loaders Market Growing?

Accelerating Infrastructure Development Under National Programs

The India compact loaders market is experiencing substantial growth propelled by extensive infrastructure development initiatives under comprehensive national programs. The PM Gati Shakti National Master Plan, a transformative multi-modal connectivity initiative, is generating unprecedented demand for construction equipment. This coordinated infrastructure approach encompasses highways, railways, ports, airports, and urban development projects requiring versatile compact loading equipment for diverse applications. The Bharatmala Pariyojana highway development program continues expanding the national highway network with substantial kilometer additions annually, requiring consistent equipment deployment. Smart city development initiatives across designated cities drive urban infrastructure construction including roads, utilities, and public spaces requiring compact equipment for efficient operations in constrained environments. The government's sustained capital expenditure commitment for infrastructure development ensures continued equipment demand throughout the forecast period.

Rising Urbanization and Real Estate Development Activities

Rapid urbanization transforming India's demographic landscape is driving substantial construction activity requiring compact loading equipment across residential, commercial, and mixed-use development projects. Urban population growth necessitates expanded housing infrastructure, commercial facilities, and supporting utilities driving construction equipment demand. The real estate sector's projected growth trajectory reaching substantial market valuations positions it as a key demand driver for compact loaders utilized in building construction, landscaping, and site development operations. Metro rail expansions across multiple cities require equipment for station construction, tunneling support operations, and surface infrastructure development. The Pradhan Mantri Awas Yojana housing initiative targeting construction of additional dwelling units accelerates affordable housing development requiring equipment deployment nationwide. Urban redevelopment projects including slum rehabilitation and infrastructure modernization create consistent equipment requirements as cities transform to accommodate growing populations and economic activities.

Expanding Agricultural Mechanization and Rural Infrastructure Development

Growing agricultural mechanization supported by government subsidies and financing schemes is expanding compact loader applications beyond traditional construction sectors. The Sub-Mission on Agricultural Mechanization providing subsidies on equipment purchases facilitates farmer and cooperative access to compact loading equipment for farm operations including material handling, land leveling, and infrastructure maintenance. Rural infrastructure development programs encompassing road connectivity, irrigation projects, and agricultural storage facilities require compact equipment capable of operating in diverse terrain conditions. Custom hiring centers established under government programs enable equipment sharing among small farmers, expanding market reach beyond direct equipment purchasers. The agriculture sector's modernization imperative addressing labor shortages and productivity requirements drives mechanized equipment adoption. Rural housing and sanitation projects under various government schemes create additional equipment demand in previously underserved market segments, diversifying the compact loaders market beyond urban construction applications.

Market Restraints:

What Challenges the India Compact Loaders Market is Facing?

Shortage of Skilled Equipment Operators and Maintenance Technicians

The India compact loaders market faces significant challenges from persistent shortages of skilled equipment operators and maintenance technicians limiting optimal equipment utilization. Industry estimates indicate requirement of substantial additional trained professionals to meet rising demand across construction trades. Inadequate vocational training infrastructure fails to produce sufficient qualified operators, while migration of skilled workers to overseas markets exacerbates domestic availability constraints. The shortage impacts project execution timelines, increases operational costs through suboptimal equipment handling, and potentially compromises safety standards on construction sites.

High Equipment Acquisition Costs and Financing Challenges

Elevated equipment acquisition costs present substantial barriers for small and medium contractors limiting market expansion potential. The transition to emission-compliant machinery meeting CEV Stage V standards has increased equipment prices as manufacturers incorporate advanced engine technologies and after-treatment systems. Small contractors and individual operators often lack access to affordable financing options enabling equipment purchases, constraining demand in potentially high-growth market segments. Interest rate environments and credit availability fluctuations impact equipment financing accessibility affecting purchase decisions and market growth trajectories.

Supply Chain Disruptions and Raw Material Price Volatility

Supply chain vulnerabilities and raw material price fluctuations impact equipment manufacturing costs and availability, creating market uncertainties. Steel price volatility directly affects construction equipment manufacturing expenses, potentially translating to higher equipment prices that moderate demand growth. Component sourcing challenges, particularly for specialized parts and electronic systems, can delay equipment production and delivery schedules. These supply-side constraints create pricing pressures and delivery uncertainties affecting contractor procurement planning and equipment deployment schedules.

Competitive Landscape:

The India compact loaders market features intense competition among established domestic manufacturers and international equipment providers vying for market share across diverse application segments. Market participants compete through product innovation, pricing strategies, dealer network expansion, and after-sales service quality differentiation. Manufacturers are investing in local production capabilities aligned with Make in India initiatives, enhancing competitive positioning through reduced costs and improved delivery responsiveness. Strategic partnerships between domestic and international companies facilitate technology transfers and market access expansion. Companies are increasingly emphasizing digital integration, telematics capabilities, and operator comfort features to differentiate offerings. The competitive landscape is evolving as manufacturers respond to emission regulation transitions and customer demands for fuel-efficient, technologically advanced equipment delivering superior operational economics.

Recent Developments:

- In December 2025, JCB India launched its largest-ever made-in-India 52-tonne excavator at EXCON 2025 along with enhanced backhoe loaders including the 3DX Super and 4DX models, demonstrating continued investment in manufacturing capabilities and product portfolio expansion for domestic and export markets.

- In December 2025, Kubota launched its BLX75K Backhoe Loader at EXCON 2025 in Bengaluru, expanding its construction equipment portfolio for the Indian market with advanced features designed for enhanced productivity and operator comfort.

- In December 2024, Action Construction Equipment Ltd announced the launch of the AX124 BS-V (CE-V) backhoe loader at Bauma CONEXPO INDIA 2024, featuring a 74 HP engine delivering improved fuel efficiency and compliance with latest emission standards.

India Compact Loaders Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Applications Covered |

Construction, Agriculture and Forestry, Industrial, Utilities |

|

Product Types Covered |

Compact Track Loaders, Skid Steer Loaders, Backhoe Loaders, Wheeled Loaders |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Compact Loaders Market Report

The India compact loaders market size was valued at USD 163.4 Million in 2025.

The India compact loaders market is expected to grow at a compound annual growth rate of 2.95% from 2026-2034 to reach USD 215.1 Million by 2034.

Construction dominated the market with a share of 54.3%, driven by extensive infrastructure development programs, highway construction initiatives, and urban development projects creating sustained demand for versatile compact loading equipment.

Key factors driving the India compact loaders market include accelerating infrastructure development under PM Gati Shakti initiatives, rising urbanization driving real estate construction, expanding agricultural mechanization, and growing equipment rental services improving market accessibility.

Major challenges include shortage of skilled equipment operators, high equipment acquisition costs limiting small contractor access, supply chain disruptions affecting component availability, rising raw material prices, and financing constraints for equipment purchases in underserved market segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)