India Compact Wheel Loaders Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

India Compact Wheel Loaders Market Summary:

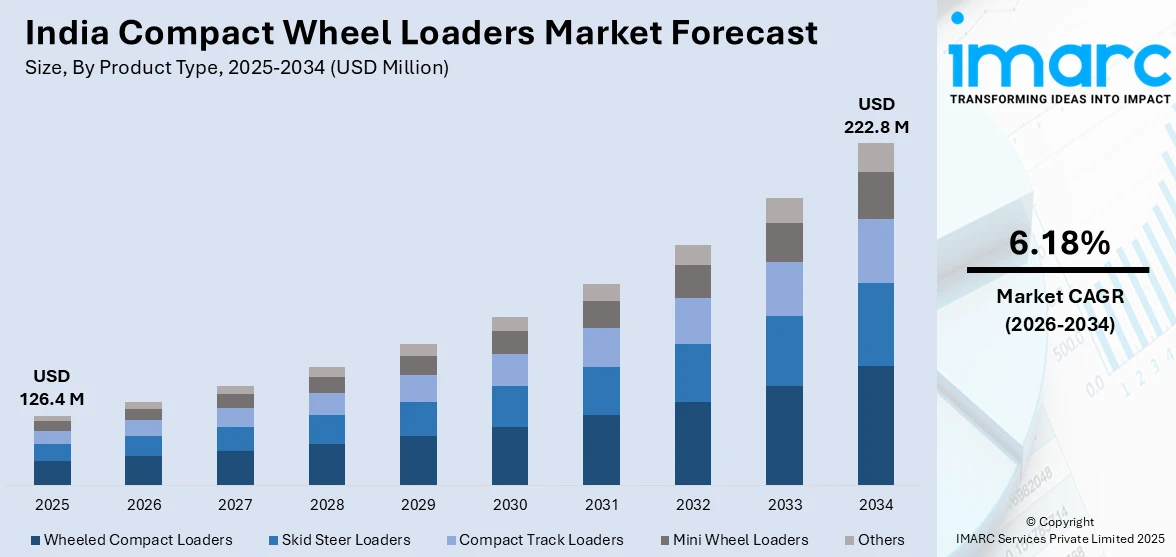

The India compact wheel loaders market size was valued at USD 126.4 Million in 2025 and is projected to reach USD 222.8 Million by 2034, growing at a compound annual growth rate of 6.18% from 2026-2034.

The India compact wheel loaders market is witnessing robust expansion driven by accelerating infrastructure development initiatives and rapid urbanization across the country. Government programs, including the National Infrastructure Pipeline and PM Gati Shakti are creating sustained demand for versatile earthmoving equipment. Growing mechanization in construction, agriculture, and material handling sectors is strengthening market adoption. Advancements in fuel-efficient engines, telematics integration, and emission-compliant technologies are reshaping equipment preferences, positioning compact wheel loaders as essential machinery for diverse applications across the India compact wheel loaders market share.

Key Takeaways and Insights:

- By Product Type: Wheeled compact loaders dominates the market with a share of 41.7% in 2025, supported by excellent maneuverability, higher mobility, and broad adaptability across urban environments and construction-related tasks.

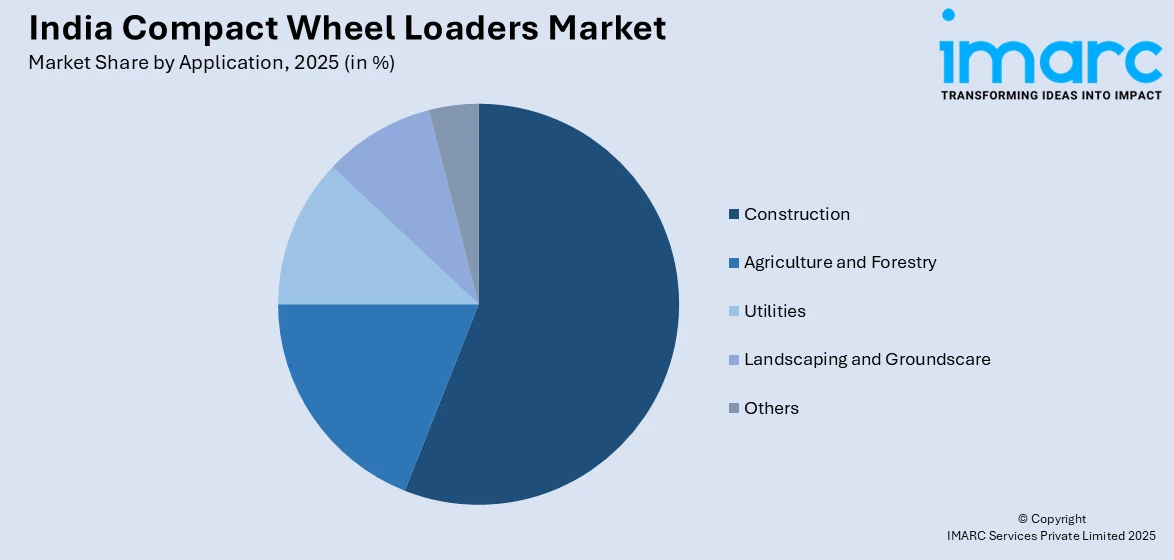

- By Application: Construction leads the market with a share of 56.2% in 2025, driven by massive infrastructure investments under Bharatmala Pariyojana and Smart Cities Mission initiatives.

- By Region: West India represents the largest segment with a market share of 35.4% in 2025, propelled by extensive industrial corridors, port expansions, and urban infrastructure projects in Maharashtra and Gujarat.

- Key Players: The India compact wheel loaders market exhibits moderate competitive intensity, with established multinational manufacturers competing alongside domestic players. Companies are focusing on product innovation, localized manufacturing, emission-compliant technologies, and expanded dealer networks to strengthen market positioning and capture emerging opportunities across diverse application segments.

To get more information on this market Request Sample

The India compact wheel loaders market is advancing rapidly as the construction equipment industry continues its growth trajectory. India's position as the world's third-largest construction equipment market, producing over 1.35 lakh units annually, reflects the sector's expanding significance. The market benefits from government initiatives that have catalyzed equipment demand across infrastructure, mining, and agricultural sectors. At Bauma Conexpo India 2024, Union Minister Nitin Gadkari highlighted plans to increase domestic production to 2.5 lakh units by 2030, underscoring the government's commitment to equipment manufacturing growth. The convergence of urbanization trends, mechanization requirements, and supportive policy frameworks is creating sustained momentum for compact wheel loaders, with manufacturers introducing CEV Stage V-compliant models featuring advanced telematics and fuel-efficient technologies to meet evolving regulatory standards and customer expectations.

India Compact Wheel Loaders Market Trends:

Technological Integration and Telematics Adoption

Advanced telematics systems, IoT sensors, and digital fleet management technologies are increasingly being integrated into compact wheel loaders to enhance operational efficiency and enable predictive maintenance capabilities. Manufacturers are investing in smart hydraulics and automation features that reduce operator fatigue while improving precision in material handling operations. At Bauma Conexpo India 2024, Caterpillar introduced its Cat Product Link telematics system, providing real-time data for efficient fleet management, exemplifying the industry's commitment to supporting India compact wheel loaders market growth through digital transformation.

Shift Toward Emission-Compliant Equipment

The introduction of stricter emission norms in India is prompting manufacturers to develop cleaner, more fuel-efficient compact wheel loaders with improved environmental performance. Equipment makers are focusing on advanced engine technologies that comply with regulations while maintaining operational productivity. This shift reflects the industry’s proactive approach to sustainability, emphasizing the importance of eco-friendly construction practices. As a result, compact wheel loaders are being designed to balance regulatory compliance, efficiency, and performance, supporting both environmental goals and the growing demand for versatile, high-performing machinery in the construction sector.

Expansion of Equipment Rental Services

Equipment rental and leasing services are rapidly expanding across India as small and medium enterprises increasingly favor flexible, pay-as-you-use access to modern machinery over large upfront investments. This model allows contractors, particularly in Tier 2 and Tier 3 cities, to access advanced compact wheel loader technologies without heavy capital expenditure. By catering to project-based demand fluctuations and limited financing options, rental and leasing services are broadening market reach, enabling more operators to utilize modern, efficient machinery and supporting the adoption of versatile construction equipment across diverse urban and semi-urban infrastructure projects.

Market Outlook 2026-2034:

The India compact wheel loaders market outlook remains strongly positive, supported by sustained government infrastructure investments and expanding construction activity across residential, commercial, and industrial segments. The India construction equipment market size was valued at USD 15.37 Billion in 2025 and is projected to reach USD 29.50 Billion by 2034, growing at a compound annual growth rate of 7.52% from 2026-2034, with compact equipment categories capturing increasing market share. India’s Union Budget has emphasized substantial capital expenditure on infrastructure, ensuring sustained demand for construction equipment and supporting growth in machinery adoption across the sector. The market generated a revenue of USD 126.4 Million in 2025 and is projected to reach a revenue of USD 222.8 Million by 2034, growing at a compound annual growth rate of 6.18% from 2026-2034.

India Compact Wheel Loaders Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Wheeled Compact Loaders |

41.7% |

|

Application |

Construction |

56.2% |

|

Region |

West India |

35.4% |

Product Type Insights:

- Skid Steer Loaders

- Compact Track Loaders

- Wheeled Compact Loaders

- Mini Wheel Loaders

- Others

Wheeled compact loaders dominate with a market share of 41.7% of the total India compact wheel loaders market in 2025.

Wheeled compact loaders have established dominance in the Indian market owing to their superior versatility, faster travel speeds, and excellent performance across diverse terrain conditions. These machines offer an optimal balance between power output and fuel efficiency, making them highly suitable for construction, landscaping, and urban infrastructure applications where mobility and quick repositioning are essential. The segment benefits from lower maintenance requirements compared to tracked alternatives and better adaptability to paved surfaces common in urban construction environments.

The preference for wheeled configurations reflects operational requirements of Indian construction sites, where equipment frequently moves between different work areas. Manufacturers are responding with enhanced models featuring advanced hydraulic systems, improved operator cabins, and telematics integration. For instance, Caterpillar's Hindustan brand offers wheel loaders specifically designed for Indian operating conditions, while global players continue introducing localized variants that meet both performance expectations and regulatory compliance requirements in this leading market segment.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Agriculture and Forestry

- Utilities

- Landscaping and Groundscare

- Others

Construction leads with a share of 56.2% of the total India compact wheel loaders market in 2025.

Construction activities are the primary driver of demand for compact wheel loaders in India, fueled by extensive government infrastructure development and rapid urbanization. These versatile machines are increasingly used across transport, energy, and urban projects, performing essential functions such as site preparation, material handling, and excavation. The growing focus on residential, commercial, and large-scale infrastructure development is reinforcing the adoption of compact loaders, highlighting their importance in improving operational efficiency, productivity, and flexibility on construction sites throughout the country.

The construction segment’s leading role is strengthened by major infrastructure initiatives focusing on road networks, urban development, and industrial corridors. These projects demand compact equipment that can operate efficiently in confined spaces while delivering high productivity. Growing contractor preference for mechanization is further driving adoption, as it helps accelerate project timelines, reduce reliance on manual labor, and enhance operational efficiency across diverse construction activities, making compact machinery an essential component of modern infrastructure development.

Regional Insights:

- North India

- South India

- East India

- West India

West India represent the largest share with 35.4% of the total India compact wheel loaders market in 2025.

West India has emerged as the leading regional market for compact wheel loaders, driven by extensive industrial development, port infrastructure expansion, and urban transformation projects concentrated in Maharashtra and Gujarat. The region benefits from major initiatives including the Mumbai Coastal Road Project with a budget of INR 14,000 crore, Gujarat's GIFT City development, and the Dholera Special Investment Region. The Delhi-Mumbai Industrial Corridor, extending through Gujarat and Maharashtra, is generating substantial equipment demand for industrial zone construction and logistics infrastructure development.

Maharashtra and Gujarat are key hubs of India’s construction activity, with rapid development occurring across Tier 2 and Tier 3 cities. Industrial and logistics infrastructure projects, along with port modernization initiatives, are driving consistent demand for compact earthmoving equipment. These developments highlight the region’s robust investment momentum and growing need for versatile machinery capable of supporting diverse construction and logistics operations. As a result, West India is emerging as a dynamic market for modern, efficient construction equipment, particularly compact wheel loaders and other small-scale earthmoving solutions.

Market Dynamics:

Growth Drivers:

Why is the India Compact Wheel Loaders Market Growing?

Government Infrastructure Development Initiatives

The Indian government’s extensive focus on infrastructure development is the key driver of growth for the compact wheel loaders market. Large-scale projects across transport, energy, and urban development sectors are fueling demand for versatile construction machinery, creating significant opportunities for compact wheel loaders and supporting their widespread adoption across diverse infrastructure initiatives. The Union Budget 2025-26 allocated INR 11.21 lakh crore for infrastructure capital expenditure, representing 3.1% of GDP and ensuring sustained equipment procurement. Flagship programs including Bharatmala Pariyojana, which has already constructed 19,826 km of the planned 34,800 km highway network, and PM Gati Shakti integrating 16 ministries for coordinated development are generating consistent demand. These initiatives create substantial opportunities for compact wheel loader deployment across road construction, site preparation, and material handling applications.

Rapid Urbanization and Construction Activity Expansion

India’s rapid urbanization is creating steady demand for construction equipment as cities expand and modern infrastructure takes shape. By 2036, around 600 million people, about two-fifths of the population, are expected to live in urban areas, compared with just under one-third in 2011. Cities and towns are also projected to generate close to 70 percent of the country’s economic output. Growing urban populations are driving increased residential and commercial construction, particularly multi-storey housing and mixed-use developments. Urban renewal programs focused on transport systems, housing, and municipal upgrades are further intensifying construction activity. These projects favor compact and versatile machinery that can operate efficiently in space-constrained city environments. As a result, demand for compact construction equipment continues to strengthen, supported by ongoing urban development and the need for faster, more efficient project execution.

Agricultural Mechanization and Rural Development

Rising mechanization in agriculture and rural areas is widening the use of compact wheel loaders beyond conventional construction activities. These machines are increasingly deployed for material handling in farming operations, dairy facilities, and village-level infrastructure projects. Rural housing programs and connectivity initiatives are supporting equipment adoption in regions that previously relied on manual labor. At the same time, focused development efforts in underserved and remote areas are improving access to modern machinery. Together, agricultural mechanization and rural infrastructure expansion are diversifying applications and extending the compact wheel loader market’s geographic footprint.

Market Restraints:

What Challenges the India Compact Wheel Loaders Market is Facing?

High Initial Acquisition Costs

Compact wheel loaders have a high initial capital investment cost that poses a major challenge to small and medium contractors who have limited capital capacity. Although the operational benefits are a reason to invest during the equipment lifecycle, several potential buyers will struggle to secure suitable financing plans, especially in Tier 2 and Tier 3 cities, where the banking infrastructure and equipment financing are yet to be developed.

Limited Skilled Operator Availability

The lack of skilled equipment operators who can work effectively at a high level could limit the potential of the market growth. The construction industry is still experiencing workforce issues, even though manufacturers provide training on how to operate the equipment. The complexity of equipment grows due to the presence of telematics and automation, and it demands more competencies of the operators, which are not always present in numerous regional markets.

Service and Maintenance Infrastructure Gaps

Inadequate service networks and spare parts availability in remote and semi-urban regions create operational challenges for equipment owners. Extended downtime for repairs affects project timelines and equipment utilization rates. While major manufacturers are expanding dealer networks, service infrastructure coverage in Northeast India and other emerging demand regions remains limited, constraining adoption in these high-growth areas.

Competitive Landscape:

The India compact wheel loaders market exhibits moderate competitive intensity, characterized by established multinational equipment manufacturers competing alongside domestic players and regional manufacturers. Market leaders are differentiating through product innovation, localized manufacturing capabilities, emission-compliant technologies, and expanded service networks. Strategic focus areas include developing India-specific models tailored to local operating conditions, establishing robust dealer support infrastructure, and introducing flexible financing solutions. Competition intensifies as companies invest in telematics integration, operator comfort enhancements, and fuel efficiency improvements. The market structure supports both premium and value-oriented positioning strategies, with aftermarket services and parts availability becoming increasingly important competitive factors.

Recent Developments:

- December 2024: Bobcat launched the B900 Ultra CEV Stage V Backhoe Loader at Bauma CONEXPO India 2024, designed to provide enhanced power, efficiency, and reliability for construction and mining operations in the Indian market.

- June 2024: CASE Construction Equipment launched its indigenously manufactured SR130B Skid Steer Loader from its Pithampur, Madhya Pradesh facility, marking the company's first made-in-India SSL featuring a 49 hp BS3-compliant Perkins engine and 590 kg rated operating capacity for the domestic market.

India Compact Wheel Loaders Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Skid Steer Loaders, Compact Track Loaders, Wheeled Compact Loaders, Mini Wheel Loaders, Others |

|

Applications Covered |

Construction, Agriculture and Forestry, Utilities, Landscaping and Groundscare, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Compact Wheel Loaders Market Report

The India compact wheel loaders market size was valued at USD 126.4 Million in 2025.

The India compact wheel loaders market is expected to grow at a compound annual growth rate of 6.18% from 2026-2034 to reach USD 222.8 Million by 2034.

Wheeled compact loaders, representing the largest revenue share of 41.7% in 2025, dominate the India compact wheel loaders market owing to superior maneuverability, faster travel speeds, and versatility across construction, landscaping, and urban infrastructure applications requiring equipment mobility.

Key factors driving the India compact wheel loaders market include government infrastructure development initiatives under the National Infrastructure Pipeline, rapid urbanization driving construction equipment demand, agricultural mechanization expansion, emission-compliant technology adoption, and growing equipment rental services accessibility.

Major challenges include high initial acquisition costs limiting SME adoption, shortage of skilled equipment operators, inadequate service and maintenance infrastructure in remote regions, financing accessibility constraints, and equipment downtime affecting project schedules.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)