India Connected Car Market Size, Share, Trends and Forecast by Technology, Connectivity Solutions, Service, End Market, and Region, 2026-2034

India Connected Car Market Summary:

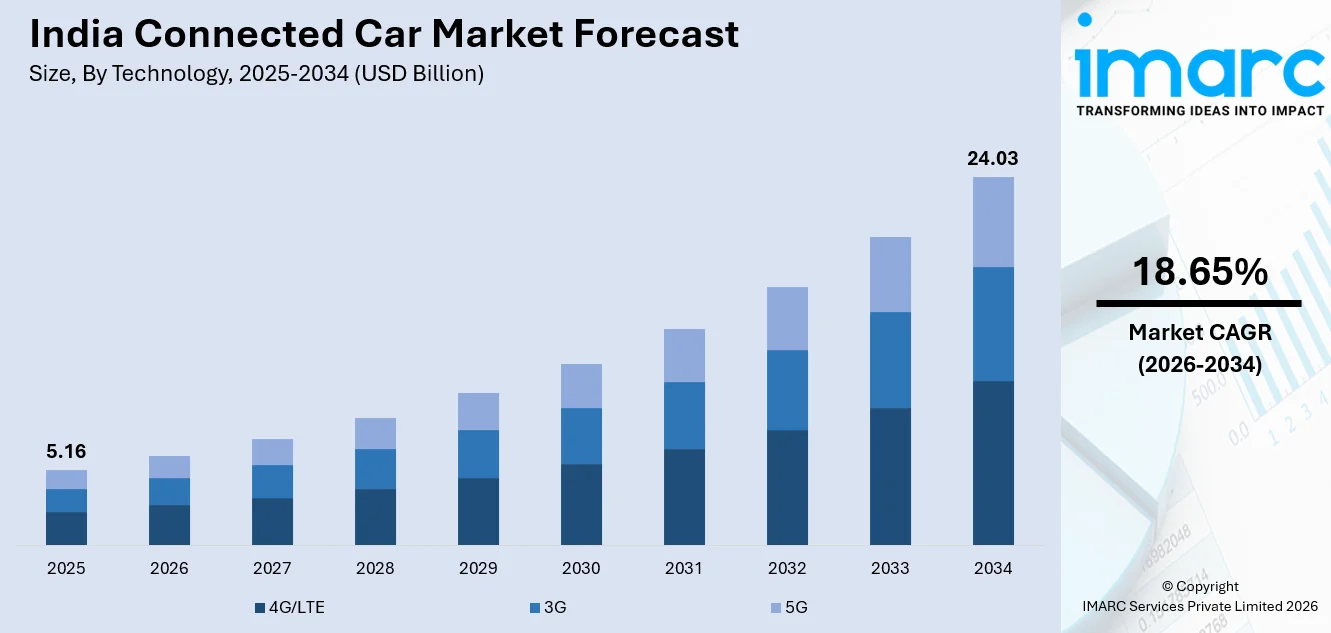

The India connected car market size was valued at USD 5.16 Billion in 2025 and is projected to reach USD 24.03 Billion by 2034, growing at a compound annual growth rate of 18.65% from 2026-2034.

The India connected car market is witnessing tremendous growth as manufacturers continue to incorporate advanced telematics, real-time navigation, smart infotainment systems, and other features as their offerings in the lineup of cars. Growing consumer interest in digital experiences, further supplemented by improved connectivity options with the proliferation of high-speed internet access and favorable government safety regulations, is driving growth momentum in the India connected car market. In addition, improvements in features like vehicle-to-everything communication, over-the-air updates, and even artificial intelligence-assisted safety features continue to change the driving experience, creating a new emerging India connected car market share.

Key Takeaways and Insights:

- By Technology: 4G/LTE dominates the market with a share of 51% in 2025, driven by widespread network availability, affordable data plans, and strong OEM adoption of LTE-enabled telematics modules across passenger and commercial vehicle segments.

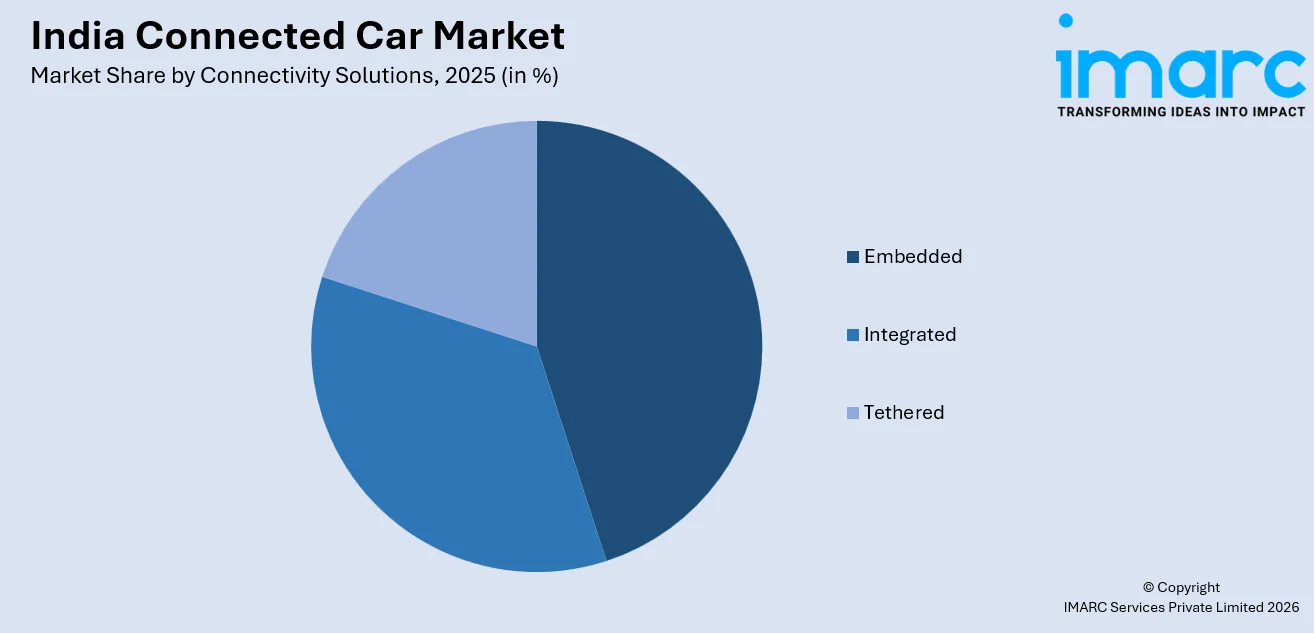

- By Connectivity Solutions: Embedded leads the market with a share of 40% in 2025, owing to its ability to deliver uninterrupted in-vehicle services, real-time diagnostics, and seamless over-the-air updates without reliance on external smartphone tethering.

- By Service: Driver assistance holds the largest share of 25% in 2025, reflecting growing consumer emphasis on road safety, advanced driver-assistance system integration, and regulatory mandates promoting active safety technologies in new vehicles.

- By End Market: Original Equipment Manufacturers (OEMs) account for the largest share of 78% in 2025, as automakers increasingly embed connected technologies at the factory level to differentiate their offerings and deliver integrated digital experiences.

- By Region: North India leads the market with a share of 30% in 2025, supported by the concentration of automobile manufacturing clusters, large consumer base, high urbanization, and robust telecommunications infrastructure across key metropolitan areas.

- Key Players: The India connected car market is highly competitive, with leading automakers expanding connected feature offerings, investing in telematics partnerships, enhancing in-vehicle digital ecosystems, and forming strategic alliances with technology and telecommunications providers to strengthen market share.

To get more information on this market Request Sample

The India connected car market is fast-paced, with automakers, technology providers, and telecommunications firms coming together to deliver smarter and more connected mobility solutions. For example, in January 2026, Kia India announced that it has surpassed 500,000 connected vehicles on Indian roads, supported by its Kia Connect 2.0 platform and Connected Car Navigation Cockpit (ccNC), underscoring strong consumer uptake of connected features in the country. A vital driver in this process is the country's rapidly expanding high-speed wireless network infrastructure, laying a friendly environment for the deployment of real-time vehicle services and data-intensive connected features. Telematics and vehicle safety regulatory mandates accelerate the integration of connectivity into new vehicle platforms. Increased consumer expectations for digital in-car experiences, growth in adoption of embedded communication modules, and an increase in subscription-based connected services foster a more dynamic and innovation-driven connected car ecosystem across the nation.

India Connected Car Market Trends:

Rising Integration of AI-Powered In-Vehicle Digital Experiences

Indian automakers are increasingly embedding artificial intelligence into vehicle infotainment and cockpit systems to deliver personalized and intuitive digital experiences. In July 2025, Indian automotive component maker Spark Minda announced a strategic partnership with Qualcomm Technologies to co‑develop next‑generation smart cockpit systems powered by Qualcomm’s Snapdragon Cockpit Platform, enabling richer multimedia, AI‑driven interfaces, and seamless cloud connectivity for software‑defined vehicles in India. Voice-enabled assistants, smart navigation, predictive maintenance alerts, and context-aware recommendations are becoming standard across mid-range and premium vehicle segments. This trend reflects a broader shift toward software-defined vehicles where the in-cabin experience mirrors the sophistication of personal smart devices, thereby accelerating the India connected car market growth.

Expansion of Over-the-Air Software Update Capabilities

Over-the-air update technology is transforming how automakers deliver new features, security patches, and performance enhancements to vehicles without requiring physical service visits. For instance, in November 2025, Kia India became the first carmaker in the country to introduce a “Plant Remote OTA” update system, enabling connected vehicles to receive the latest software remotely at the manufacturing stage so customers get fully updated, ready‑to‑drive cars from day one. OEMs are adopting OTA platforms to reduce maintenance costs, enhance customer satisfaction, and create post-sale revenue streams through subscription-based feature activation. This capability is increasingly influencing purchase decisions among tech-savvy consumers seeking future-proof vehicles.

Growing Adoption of Vehicle-to-Everything Communication

Vehicle-to-everything communication is gaining traction in India as smart city initiatives and intelligent transportation infrastructure expand across major urban corridors. In December 2025, the Indian government began developing a Connected Commercial Vehicle (CCV) protocol to enable standardized V2X communication between vehicles and road infrastructure, aiming to improve interoperability, traffic management, and real-time safety alerts across highways and urban transport networks. Technologies enabling vehicles to communicate with surrounding infrastructure, cloud platforms, and other road users are enhancing traffic efficiency, reducing congestion, and improving overall road safety. This trend is reinforcing the shift toward a fully connected and intelligent mobility ecosystem.

Market Outlook 2026-2034:

India's connected car market is poised for robust advancement, supported by expanding telecommunications infrastructure, accelerating regulatory mandates, and rising consumer demand for digitally enriched driving experiences. The growing integration of embedded telematics, AI-powered voice assistants, and over-the-air update capabilities is reshaping how consumers interact with their vehicles. Increasing investments in vehicle-to-everything communication and smart mobility ecosystems are further strengthening the market landscape. As automakers deepen partnerships with technology and connectivity providers, the sector is expected to witness sustained innovation, broader feature accessibility, and stronger adoption across diverse vehicle segments nationwide. The market generated a revenue of USD 5.16 Billion in 2025 and is projected to reach a revenue of USD 24.03 Billion by 2034, growing at a compound annual growth rate of 18.65% from 2026-2034.

India Connected Car Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Technology |

4G/LTE |

51% |

|

Connectivity Solutions |

Embedded |

40% |

|

Service |

Driver Assistance |

25% |

|

End Market |

Original Equipment Manufacturer (OEMs) |

78% |

|

Region |

North India |

30% |

Technology Insights:

- 3G

- 4G/LTE

- 5G

The 4G/LTE dominates with a market share of 51% of the total India connected car market in 2025.

Currently, the prevalent segment of the connected car market in India is the 4G/LTE technology segment due to the robust presence of the network in the region, which allows for real-time connectivity solutions with the help of telematics services and infotainment systems. The robust presence of the network allows car manufacturers to incorporate cellular circuits in cars of both lower as well as higher segments, ensuring the connectivity needs of those devices with the help of the available network backbones in the region.

The demand for smooth digital services while driving is further supporting the growth and development of this technology segment, which has already captured the driving scene in India with a strong hold. The auto industry is witnessing exciting times with the introduction of cutting-edge communication technologies which enable real-time traffic updates, cloud-based voice assistants, and predictive maintenance updates, thereby enabling customers with enhanced driving convenience and safety. Telecom operators are also rolling out specialized auto plans which help reduce costs associated with such plans, thus encouraging the adoption of these technologies through the availability of cheaper plans.

Connectivity Solutions Insights:

Access the comprehensive market breakdown Request Sample

- Integrated

- Embedded

- Tethered

The embedded leads with a share of 40% of the total India connected car market in 2025.

Embedded connectivity solutions account for the highest market share within the India connected car market due to the increasing interest of automakers to embed dedicated comms modules directly onto their vehicle architecture. This facilitates seamless connectivity to always-on services, aiding the provision of real-time telematics, emergency calls, remote management, and updating without reliance on the user’s own device to enable these capabilities. The embedded route also increases data security and provides OEMs with potential to generate recurrent revenue after the sale of the vehicle.

The growth of embedded connectivity is being fueled by the increased need for the automaker to exert greater control over the digital experience within the vehicle, as well as the need to engage consumers throughout the product life cycle. For instance, embedded modules guarantee performance across varying conditions of usage and facilitate software upgrades that improve the functional capabilities of the vehicle. Moreover, these embedded systems help support features of the vehicle, which include real-time vehicle health, location-based features, and infotainment personalization. Consequently, embedded connectivity has become one of the principal features of innovation in vehicle development.

Service Insights:

- Driver Assistance

- Safety

- Entertainment

- Vehicle Management

- Mobility Management

- Others

The driver assistance dominates with a market share of 25% of the total India connected car market in 2025.

The driver assistance services segment is found to dominate the India connected car market, as road safety, as well as accident avoidance, is becoming a major priority for consumers as well as the government. In February 2026, Mahindra & Mahindra announced that it has selected Mobileye’s SuperVision and Surround ADAS platforms for at least six upcoming vehicle models, with production planned from 2027, signaling a major expansion of advanced driver assistance capabilities across its future portfolio. Connected driver assistance services, including adaptive cruise control, lane departure warning, collision avoidance, as well as traffic-aware routing, offer the potential to become the norm on new vehicles. The advent of the domestic safety ratings, as well as the awareness of advanced safety technologies, have prompted car manufacturers to make available numerous forms of connected driver assistance services across various segments.

The expanding reach of driver assistance services can be further substantiated by the fact that car manufacturers have started to incorporate intelligent sensor fusion technology into their vehicle systems. In this way, real-time data processing can greatly assist in creating safety features for vehicles. Moreover, by being able to connect the driver assistance services with telematics systems, manufacturers have started to improve their vehicle safety systems by constantly analyzing the data of different scenarios. As awareness of active safety systems continues to emerge among the people of India, connected driver assistance services will strengthen in the country as well.

End Market Insights:

- Original Equipment Manufacturer (OEMs)

- Aftermarket

The original equipment manufacturer (OEMs) leads with a share of 78% of the total India connected car market in 2025.

The OEM segment has the maximum market share among the India connected car market. Over time, car manufacturers are using connected technologies to create seamless integrated digital experiences. The standard connected car experience is much more reliable in terms of integration, robustness, and better security compared to after-market connectivity solutions. Car maker companies are using connected technologies to reach out to end-users of their cars in a direct manner. Communication through mobile apps is therefore acting as a factor that differentiates one manufacturer from another.

Such a trend towards more emphasis on factory-installed connectivity is further supported by the need for automakers to build long-term digital engagement with consumers past the point of the original purchase. Many automakers are building their own connected platforms that offer consumers direct engagement capabilities such as vehicle diagnostics, real-time performance tracking, and predictive maintenance scheduling, all within a manufacturer-supported network. Such efforts enable automakers to garner valuable information that helps build product development and customer engagement strategies. In a competitive environment seeking excellence across all automotive segments, building the brand on connected offerings is a necessity.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India exhibits a clear dominance with a 30% share of the total India connected car market in 2025.

North India leads the connected car market, supported by the presence of key automobile manufacturing and sales clusters, a large and tech-savvy consumer base, and well-established telecommunications infrastructure across major metropolitan areas. The region benefits from high urbanization rates and strong demand for premium and feature-rich vehicles, encouraging automakers to prioritize connected technology deployment. Additionally, the concentration of corporate fleet operations and ride-hailing platforms in northern cities drives commercial adoption of telematics and connected vehicle management solutions, further strengthening the region's dominant market position.

The region's leadership is further reinforced by robust consumer purchasing power and a growing preference for vehicles equipped with advanced digital features and seamless connectivity capabilities. Automakers are strategically launching their latest connected vehicle models in northern metropolitan markets to capitalize on early adopter demand and strong brand awareness. The availability of dense high-speed wireless network coverage across key urban corridors enables reliable delivery of real-time navigation, remote diagnostics, and in-vehicle entertainment services. As smart city initiatives and intelligent transportation projects gain momentum across northern states, the region is expected to maintain its leading position in connected car adoption.

Market Dynamics:

Growth Drivers:

Why is the India Connected Car Market Growing?

Expanding High-Speed Wireless Network Infrastructure

India’s rapidly expanding telecommunications network infrastructure is creating a strong foundation for connected car adoption across the country. In November 2024, Ericsson reported that India is among the world’s fastest-growing 5G markets, with nationwide 5G population coverage expected to surpass 95% by 2027, supporting real-time connected vehicle services. The widespread rollout of high-speed wireless connectivity across urban, semi-urban, and emerging tier-two and tier-three cities is enabling automakers to deliver reliable real-time services including navigation, telematics, and infotainment to a broader consumer base. Network providers are actively collaborating with automotive manufacturers to develop tailored connectivity solutions that ensure uninterrupted data transfer for in-vehicle applications. The growing availability of affordable high-speed data plans is reducing barriers to connected service subscriptions, making advanced vehicle connectivity accessible to a wider demographic. As network density and coverage continue to improve, automakers are incorporating increasingly sophisticated connected features, reinforcing the expansion of the connected car ecosystem.

Rising Consumer Demand for Smart In-Vehicle Experiences

India’s growing middle class and tech-savvy consumer base are driving demand for vehicles that offer seamless digital integration and personalized in-cabin experiences. Today’s car buyers increasingly expect smartphones-like convenience within their vehicles, including real-time navigation, voice-controlled assistants, streaming entertainment, and remote vehicle management through dedicated mobile applications. Reinforcing this industry shift, Maruti Suzuki announced an investment in a connected mobility intelligence startup in 2025 to strengthen its capabilities in connected vehicle data, AI-driven insights, and customer experience innovation. Automakers are responding by equipping even mid-range and economy vehicles with advanced connectivity features that were previously exclusive to premium segments. The shift in consumer expectations from basic transportation to connected and intelligent mobility is encouraging manufacturers to invest heavily in telematics and digital cockpit technologies. This evolving demand pattern is accelerating the penetration of connected features across all vehicle categories and price segments in the Indian market.

Supportive Government Regulations and Safety Mandates

Regulatory initiatives by the Indian government are playing a pivotal role in accelerating connected car technology adoption across the automotive industry. Safety mandates requiring telematics-based tracking systems in commercial vehicles, along with the introduction of domestic vehicle safety assessment programs, are compelling automakers to integrate connected features as standard equipment. Strengthening the digital mobility ecosystem, the Ministry of Road Transport and Highways (MoRTH) launched a new National Transport Repository (NTR) data-sharing policy in 2025, enabling secure, standardized access to vehicle, FASTag, and transport datasets to support intelligent transport systems, real-time monitoring, and data-driven mobility solutions. Standards around emergency calling capabilities, real-time vehicle tracking, and satellite-based positioning are embedding connectivity into the regulatory framework for new vehicle approvals. Government-led initiatives promoting intelligent transportation systems and smart city development are further strengthening the infrastructure required for connected mobility. These regulatory measures are creating a predictable demand environment that allows both global and domestic technology suppliers to invest in localized connected car solutions with confidence.

Market Restraints:

What Challenges the India Connected Car Market is Facing?

Inconsistent Network Coverage in Rural and Semi-Urban Areas

Despite significant progress in expanding wireless network infrastructure, large portions of rural and semi-urban India continue to experience unreliable or limited high-speed connectivity. This inconsistency undermines the performance of real-time connected services such as navigation, telematics, and emergency calling, creating a fragmented user experience. The connectivity gap between metropolitan centers and smaller towns discourages broader adoption and limits the market’s penetration potential beyond major urban corridors.

Data Privacy and Cybersecurity Concerns

As connected vehicles generate and transmit increasing volumes of personal and location data, concerns around data privacy, unauthorized access, and cybersecurity threats are intensifying among consumers and regulators. The absence of a comprehensive automotive-specific data protection framework creates uncertainty around how vehicle-generated information is collected, stored, and shared. These concerns can erode consumer trust and slow adoption rates, particularly among privacy-conscious buyers who remain cautious about embracing always-on vehicle connectivity.

High Cost of Advanced Connected Technologies

The integration of sophisticated connected systems including embedded communication modules, advanced sensors, and cloud-based platforms adds significant cost to vehicle production. For price-sensitive segments that constitute a substantial portion of the Indian automotive market, these additional costs create affordability barriers. Many budget-conscious consumers are unwilling to pay a premium for connected features, particularly when subscription-based services add ongoing expenses beyond the initial vehicle purchase price.

Competitive Landscape:

The India connected car market is becoming increasingly competitive as automakers, technology providers, and telecommunications companies intensify their efforts to capture market share in the rapidly evolving connected mobility space. Vehicle manufacturers are differentiating their offerings by embedding advanced telematics, AI-powered voice assistants, and digital cockpit solutions across multiple vehicle segments. Strategic partnerships between automakers and network service providers are enabling seamless in-vehicle connectivity, while collaborations with software developers are enhancing in-car application ecosystems. Competition is also driven by the growing emphasis on subscription-based connected services that generate post-sale revenue streams. The aftermarket segment is witnessing increasing activity as third-party providers introduce retrofit connectivity solutions targeting existing vehicle owners. Market players are continuously refining their strategies to balance feature richness with affordability, aiming to address the diverse needs of India’s broad consumer base while strengthening their competitive positioning.

Recent Developments:

- In October 2025, HARMAN invested ₹345 crore to expand its Pune automotive electronics plant, enhancing production of infotainment, telematics, and connected car modules. The expansion aims to strengthen India’s position in connected and sustainable mobility, supporting OEMs with advanced in‑vehicle technologies.

India Connected Car Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | 3G, 4G/LTE, 5G |

| Connectivity Solutions Covered | Integrated, Embedded, Tethered |

| Services Covered | Driver Assistance, Safety, Entertainment, Vehicle Management, Mobility Management, Others |

| End Markets Covered | Original Equipment Manufacturer (OEMs), Aftermarket |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Connected Car Market Report

The India connected car market size was valued at USD 5.16 Billion in 2025.

The India connected car market is expected to grow at a compound annual growth rate of 18.65% from 2026-2034 to reach USD 24.03 Billion by 2034.

4G/LTE, holding the largest revenue share of 51%, remains the dominant connectivity technology in India’s connected car market, enabling reliable real-time telematics, infotainment, and driver assistance services across urban and semi-urban vehicle segments.

Key factors driving the India connected car market include expanding high-speed wireless network coverage, rising consumer demand for smart in-vehicle experiences, supportive government safety mandates, growing OEM investments in embedded connectivity, and advancements in telematics and AI-powered vehicle technologies.

Major challenges include inconsistent network coverage in rural areas, data privacy and cybersecurity concerns, high costs of advanced connected technologies, limited consumer awareness in price-sensitive segments, supply chain constraints for electronic components, and the absence of standardized automotive data protection frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade