India Construction Equipment Market Size, Share, Trends and Forecast by Solution Type, Equipment Type, Type, Application, Industry, and Region, 2026-2034

India Construction Equipment Market Size, Share, Trends & Forecast (2026-2034)

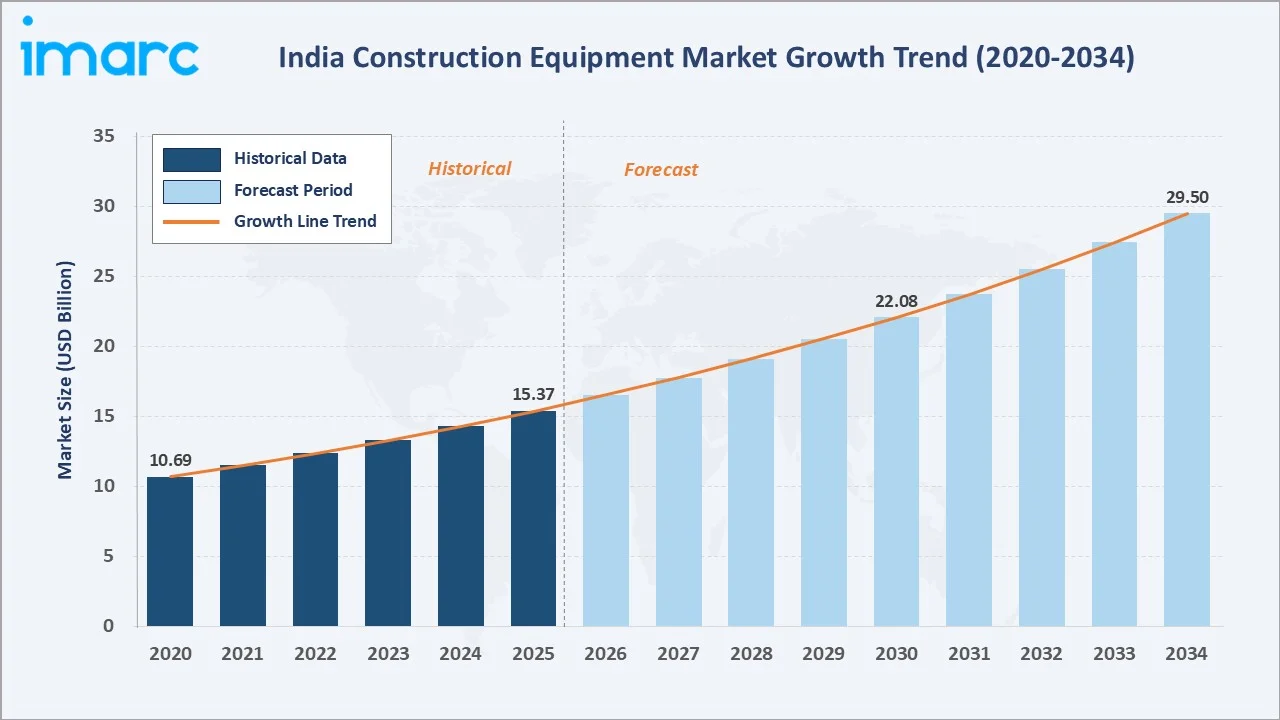

The India construction equipment market size reached USD 15.37 Billion in 2025 and is projected to reach USD 29.50 Billion by 2034, exhibiting a CAGR of 7.52% during 2026-2034. India's accelerating infrastructure pipeline - spanning highways, metro rail, smart cities, and affordable housing - continues to drive robust demand for heavy and compact machinery.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.37 Billion |

|

Forecast Market Size (2034) |

USD 29.50 Billion |

|

CAGR (2026-2034) |

7.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North India (30.0%) |

|

Fastest Growing Region |

West & Central India |

The chart below illustrates the market growth trend from 2020 through 2034, clearly distinguishing the historical base from the forward-looking forecast.

To get more information on this market, Request Sample

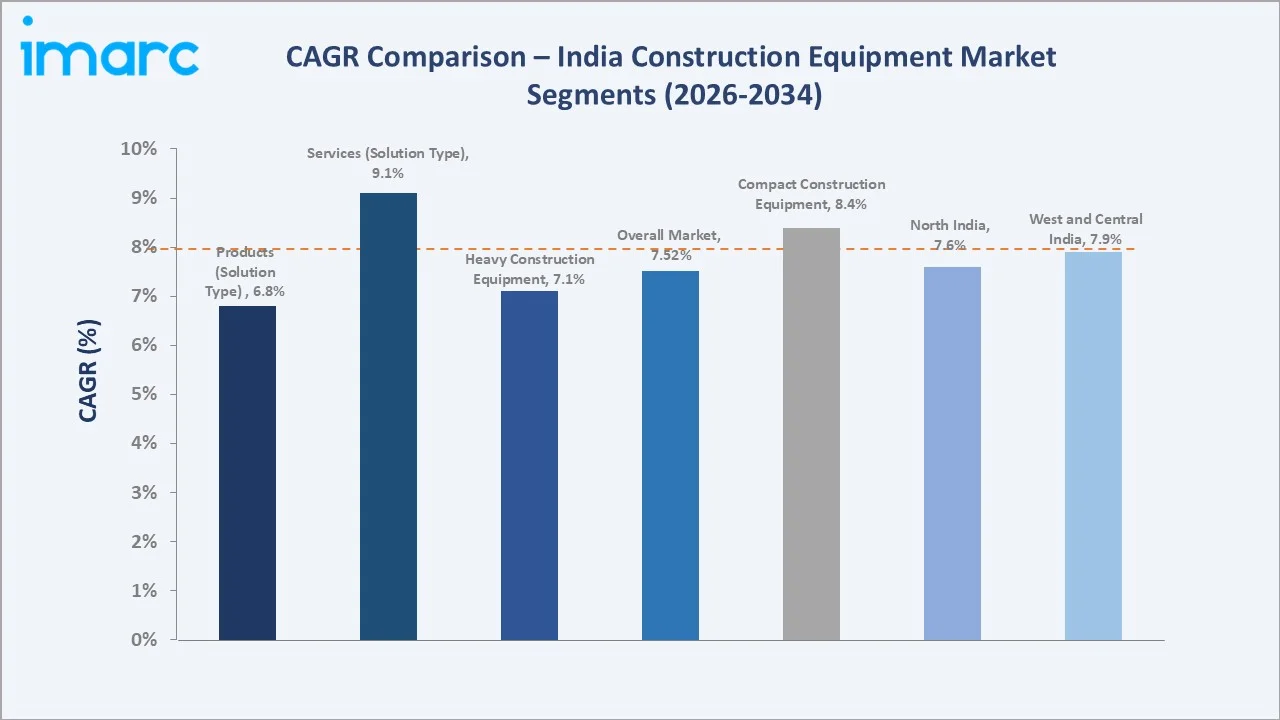

The CAGR comparison chart below benchmarks segment-level growth rates against the overall market rate of 7.52%, highlighting the fastest-growing sub-markets.

Executive Summary

India's construction equipment sector has grown steadily from USD 10.69 Billion in 2020 to USD 15.37 Billion in 2025, at a historical CAGR of approximately 7.5%. This growth trajectory reflects India's rising capital expenditure on infrastructure - with the Union Budget 2024-25 allocating INR 11.11 Trillion (USD 133 Billion) for infrastructure development. Rapid urbanisation, the expansion of expressways, and increased port and logistics investments are key catalysts sustaining demand across equipment categories.

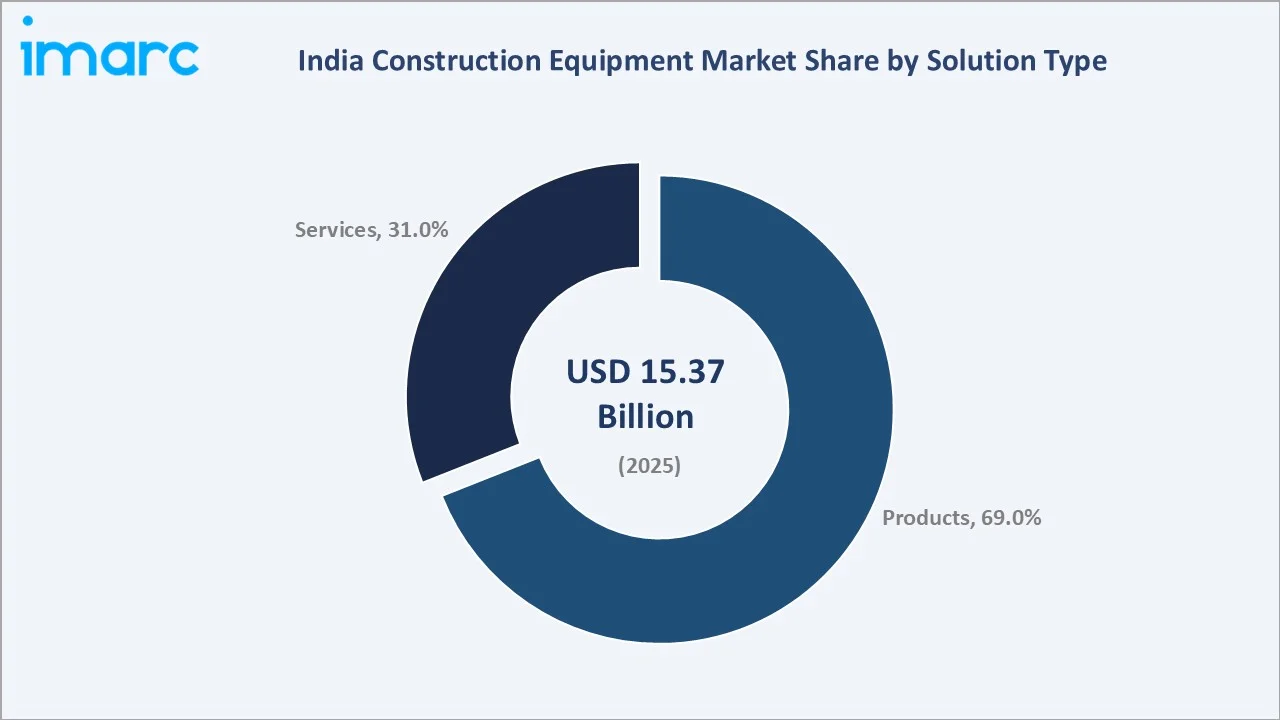

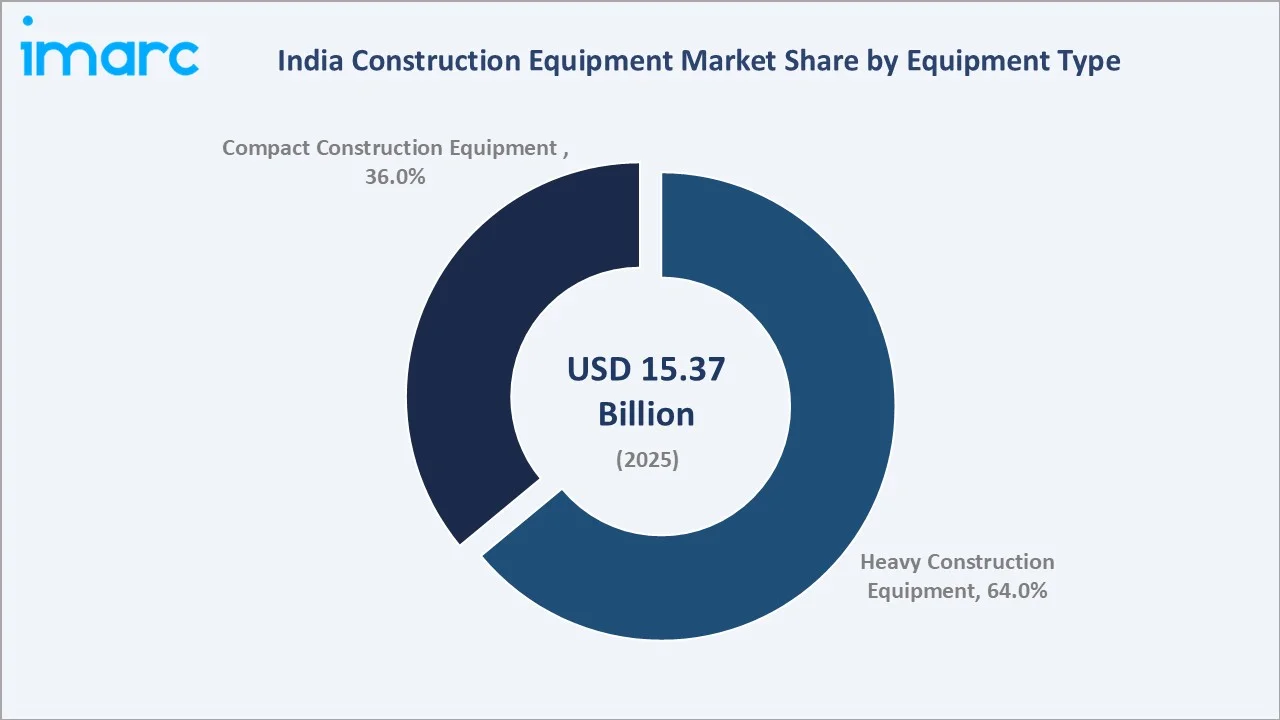

The Products segment holds a dominant 69% share of the market in 2025, supported by rising equipment procurement by contractors, government agencies, and mining companies. The Services segment (31% share) is gaining traction as fleet-management and maintenance-as-a-service models proliferate, particularly among medium-sized contractors. Among equipment types, Heavy Construction Equipment leads with a 64% revenue share, driven by the scale requirements of highway and metro projects.

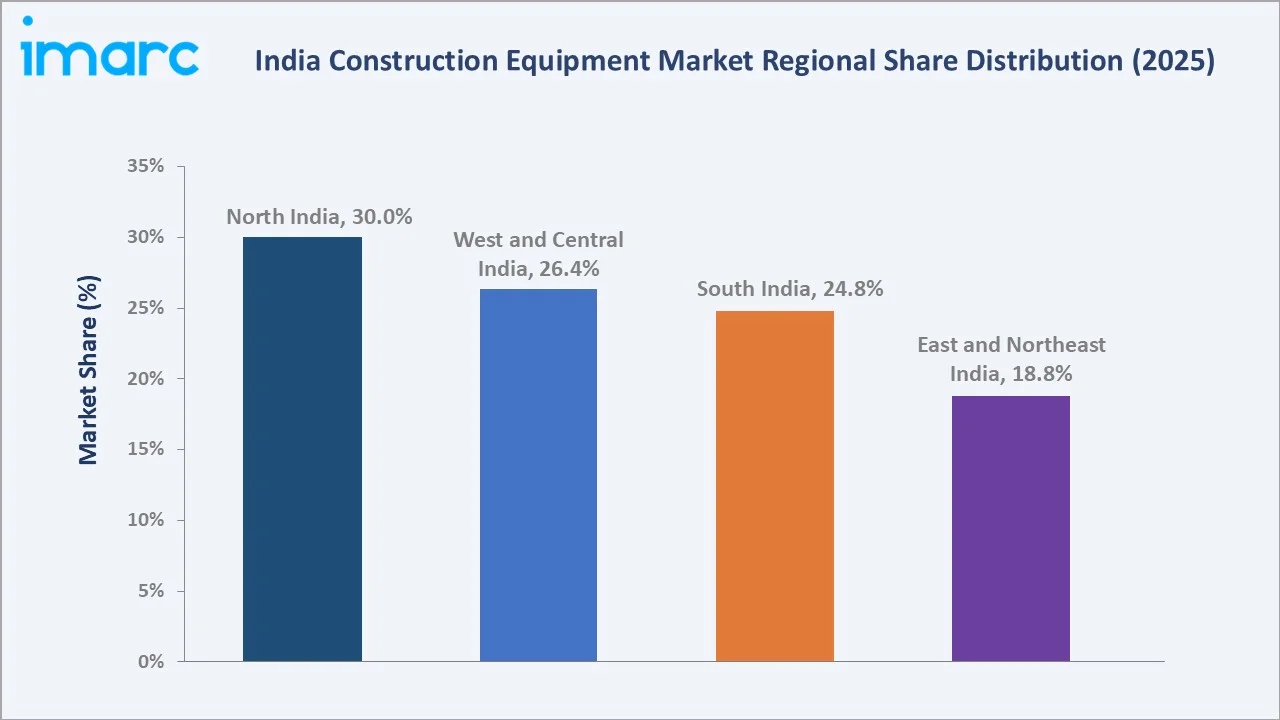

Regionally, North India commands 30.0% of market revenue - underpinned by Delhi-NCR real estate activity, NHAI highway projects, and industrial corridor development. West & Central India (26.4%) and South India (24.8%) follow, supported by IT corridor construction and port-expansion projects respectively. The market is projected to reach USD 22.08 Billion by 2030 and USD 29.50 Billion by 2034, reflecting the structural tailwinds embedded in India's long-term infrastructure ambitions.

|

Insight |

Data Point |

|

Largest Solution Type |

Products – 69% share (2025) |

|

Largest Equipment Type |

Heavy Construction Equipment – 64% share (2025) |

|

Leading Region |

North India – 30.0% revenue share (2025) |

|

Fastest Growing Region |

West & Central India |

|

Market Size 2025 |

USD 15.37 Billion |

|

Market Size 2034 (Forecast) |

USD 29.50 Billion |

|

CAGR 2026-2034 |

7.52% |

|

Top Companies |

JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery, AB Volvo, Escorts Kubota Limited, CNH Industrial N.V., MCE, Action Construction Equipment Ltd. |

|

Key Opportunities |

Infrastructure push under national programs, Rental and leasing growth |

Key Analytical Observations Supporting the Above Data:

- Products dominate solution-type segmentation with a 69% revenue share in 2025, driven by direct equipment purchases by large contractors, government bodies, and mining firms across India.

- Heavy Construction Equipment leads equipment-type segmentation at 64% share in 2025, supported by the sheer scale of highway, metro, and dam construction projects under government-funded programmes.

- North India holds the largest regional share at 30.0% of total revenue in 2025, reflecting high construction density in Delhi-NCR, Punjab, and Haryana, particularly for residential and expressway projects.

- The overall market CAGR of 7.52% (2034) reflects India's structural infrastructure spending trajectory, positioning the country as one of the fastest-growing construction equipment markets globally.

- JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery remain market leaders, with JCB commanding an estimated 45%+ share in the backhoe loader and excavator segments as of 2025.

- The market is expected to nearly double from USD 15.37 Billion (2025) to USD 29.50 Billion (2034), generating significant investment opportunities in equipment financing, telematics, and after-sales services.

India Construction Equipment Market Overview

Construction equipment encompasses machinery used for earthmoving, material handling, lifting, paving, and concrete operations across civil infrastructure, real estate, mining, and industrial projects. In India, the ecosystem spans domestic manufacturers, multinational OEMs, component suppliers, rental-fleet operators, and after-sales service providers. The sector is deeply linked to macroeconomic variables including government capex, housing starts, foreign direct investment in manufacturing, and commodity prices. India's push towards a USD 5 Trillion economy by 2028-29, coupled with an infrastructure investment target exceeding INR 143 Trillion over 2024-2030, establishes a robust long-term demand foundation for the sector.

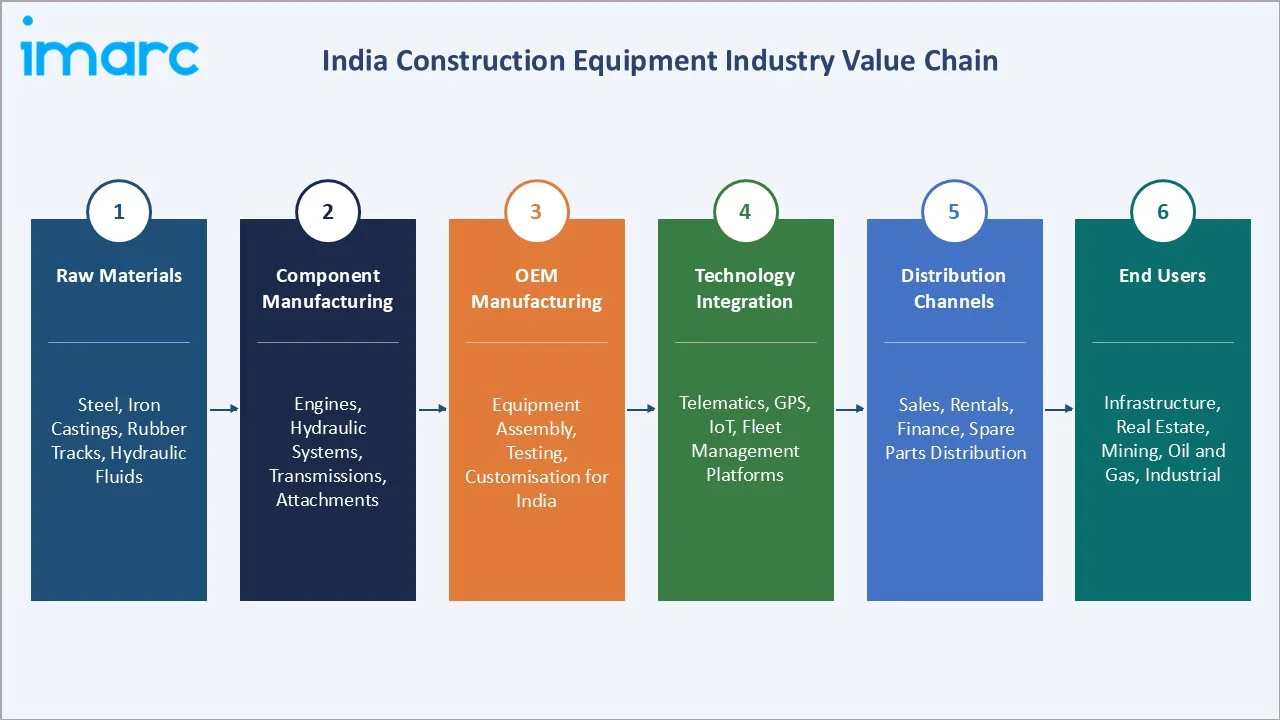

The industry ecosystem diagram below maps the end-to-end value network, from raw material suppliers and component manufacturers through to OEMs, distribution channels, and end users.

Market Dynamics

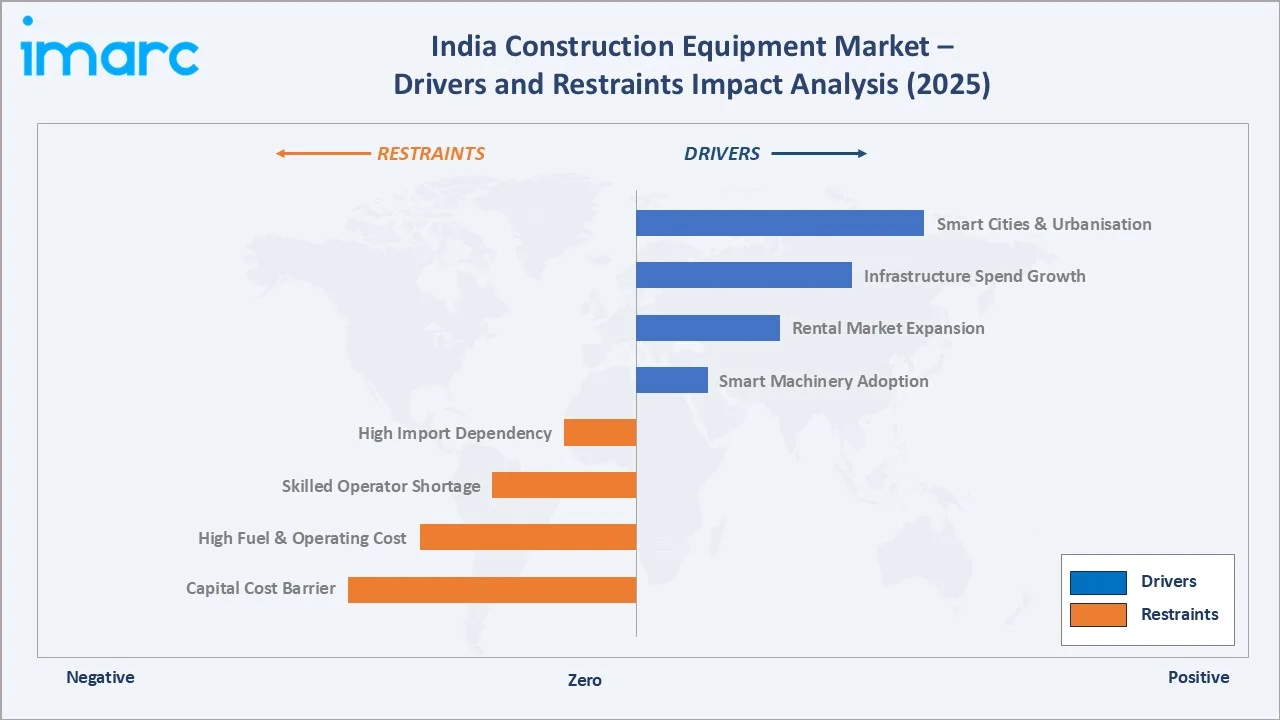

The dual-panel chart below compares the relative impact weights of the primary drivers and restraints shaping the India construction equipment market in 2025.

To evaluate market opportunities, Request Sample

Market Drivers

- Government Infrastructure Spending: The Union Budget 2024-25 earmarked INR 11.11 Trillion for capital investment. This directly funds road, metro, airport, and waterway projects, boosting demand for excavators, compactors, and material-handling equipment.

- Smart Cities & Urbanisation: Government-led urban transformation initiatives such as the Smart Cities Mission and AMRUT 2.0 (upgrades across 500+ cities) are significantly boosting infrastructure development. These large-scale programs, along with strong momentum in premium housing—where luxury residential demand saw over 30% year-on-year growth—are driving substantial demand for construction equipment across urban India, particularly for applications such as earthmoving, concrete handling, and material lifting.

- Rental Market Expansion: The growing preference for equipment rental over ownership is emerging as a key driver in the India construction equipment market. Rental models reduce upfront capital investment and provide flexibility to contractors, especially small and mid-sized players, enabling access to a wide range of machinery on demand.

- Smart Machinery Adoption: The increasing adoption of smart and connected construction equipment is emerging as a key growth driver in the India construction equipment market. Technologies such as telematics, GPS-based machine control, and AI-enabled diagnostics are enhancing equipment productivity, reducing downtime, and enabling predictive maintenance.

Market Restraints

- High Capital Cost: Construction equipment carries a high unit cost (backhoe loaders USD 20,000-40,000; large excavators USD 150,000+), limiting adoption among small contractors without financing access.

- Skilled Operator Shortage: The sector is experiencing a shortage of trained equipment operators, which is limiting equipment utilisation rates across project sites.

- High Import Dependency for Components: Advanced hydraulic systems, high-performance engines, and precision control electronics remain largely import-dependent, exposing margins to currency volatility.

- High Fuel & Operating Costs: Rising fuel prices and increasing maintenance expenses elevate the total cost of ownership, discouraging equipment usage and impacting profitability, particularly for small and cost-sensitive contractors.

Market Opportunities

- Electric & Hybrid Equipment: Government support for sustainable construction practices and incentives for electric mobility are creating early opportunities for electric compact equipment, with the segment expected to register strong double-digit growth through 2034.

- Telematics & IoT Integration: Real-time equipment monitoring can reduce downtime by up to 30%, while OEMs integrating telematics are strengthening their position in fleet management contracts through improved operational efficiency and data-driven control.

Market Challenges

- Fragmented Distribution: India’s contractor ecosystem remains highly fragmented, with a large base of registered contractors relying on informal equipment sourcing channels, thereby creating challenges for organized market penetration.

- BS-VI Emission Compliance Transition: The transition to BS-VI-equivalent off-road emission norms is increasing engine costs by 8–15%, which is impacting demand elasticity, especially in price-sensitive segments such as small construction equipment.

- Raw Material Price Volatility: Volatility in steel and iron ore prices—key raw materials for equipment manufacturing—has increased input cost pressures for OEMs, leading to margin compression and tighter cost management across the industry.

Emerging Market Trends

The timeline below maps the sequential emergence of key market trends across the 2020-2034 period, from rental-model adoption to the anticipated autonomous equipment pilots.

1. Electrification of Construction Fleets

Major OEMs such as J C Bamford Excavators Ltd, AB Volvo, and CNH Industrial N.V. have introduced electric variants of mini excavators and compact loaders. In India, pilot deployments have also been carried out across smart city projects in Pune and Bengaluru. The electric equipment segment is expected to witness strong long-term growth in the country, driven by sustainability initiatives and urban infrastructure development.

2. Telematics and Connected Equipment Platforms

J C Bamford Excavators Ltd’s LiveLink platform and BEML Limited’s remote diagnostics systems are collectively enabling real-time monitoring of a large machine fleet in India. These systems provide GPS tracking, fuel efficiency insights, and predictive maintenance alerts, helping reduce total cost of ownership across the equipment lifecycle.

3. Rental-as-a-Service (RaaS) Model

The Rental-as-a-Service (RaaS) model is helping to formalize the previously fragmented equipment rental market by shifting users away from ownership toward flexible, service-based access. Under this model, contractors can rent machinery as needed rather than investing in heavy upfront capital purchases.

4. BS-VI Off-Road Emission Norms

India is advancing towards BS-VI-equivalent emission standards for off-road equipment (Construction Equipment Vehicles - CEV V norms). Compliance deadlines are expected between 2026-2028, requiring OEMs to invest heavily in engine technology upgrades - an investment cycle that will refresh existing fleets and stimulate replacement demand.

5. AI-Enabled Predictive Maintenance

Artificial intelligence applications in construction equipment diagnostics are emerging as a key trend in the industry. AI-enabled maintenance systems are being used to optimize service scheduling, detect early signs of equipment faults, and reduce unplanned breakdowns, thereby improving overall machine reliability and operational efficiency.

Industry Value Chain Analysis

The detailed value chain table below maps the key participants and primary activities at each stage:

|

Stage |

Key Activities |

|

Raw Materials |

Steel, Iron Castings, Rubber Tracks, Hydraulic Fluids |

|

Component Manufacturing |

Engines, Hydraulic Systems, Transmissions, Attachments |

|

OEM Manufacturing |

Equipment Assembly, Testing, Customisation for Indian Conditions |

|

Technology Integration |

Telematics, GPS, IoT, Fleet Management Platforms |

|

Distribution Channels |

Sales, Rentals, Finance, Spare Parts Distribution |

|

End Users |

Infrastructure, Real Estate, Mining, Oil & Gas, Industrial |

The India construction equipment value chain integrates raw material suppliers, engine and component manufacturers, multinational and domestic OEMs, technology integrators, and a broad distribution network. Understanding this chain helps identify margin pools, supply-chain risks, and partnership opportunities.

Technology Landscape in the India Construction Equipment Industry

Engine & Emission Technology

India is transitioning construction equipment engines toward CEV Stage V emission standards, which require advanced after-treatment systems such as particulate filters and selective catalytic reduction technologies. This regulatory shift is driving significant investment in cleaner and more efficient powertrain development across the industry, with OEMs focusing on compliance-ready engine architectures.

Telematics & IoT Connectivity

The adoption of telematics in construction equipment has expanded significantly in India, with a large number of machines now connected to digital monitoring platforms compared to earlier years. Fleet management systems are increasingly being used to track equipment utilization, fuel efficiency, idle time, and operational compliance such as geo-fencing.

Electric & Hybrid Drivetrains

The electric construction equipment market in India remains nascent but fast-moving. JCB's 19C-1E electric mini-excavator and AB Volvo's ECR25 Electric have been demonstrated at major Indian construction expos. Battery-electric options are most viable for compact equipment (sub-5-tonne) in urban environments, where emission restrictions and noise ordinances are tightening.

Automation & Semi-Autonomous Systems

Machine-control systems based on GPS and laser-guided technologies are increasingly being used in large infrastructure projects such as highways and dams. These systems significantly improve grading precision and reduce reliance on manual intervention, leading to higher accuracy and faster execution.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Solution Type |

Products |

69.0% |

2025 |

|

Equipment Types |

Heavy Construction Equipment |

64.0% |

2025 |

|

Type |

Excavator |

30.0% |

2025 |

|

Applications |

Excavation and Mining |

28.0% |

2025 |

|

Industry |

Construction and Infrastructure |

45.0% |

2025 |

|

Region |

North India |

30.0% |

2025 |

By Solution Type

To access detailed market analysis, Request Sample

Products (69% share, 2025): The Products sub-segment - comprising outright sale of excavators, loaders, cranes, dozers, forklifts, and other equipment - dominates the market owing to large-scale procurement by state and central government agencies, mining companies, and tier-1 EPC contractors. Direct ownership models remain preferred for large, continuous-use applications. The sub-segment is projected to grow at ~6.8% CAGR through 2034.

The pie chart below illustrates the 2025 revenue split between Products and Services sub-segments:

By Equipment Type

Heavy Construction Equipment (64% share, 2025): Heavy equipment - including large excavators (20+ tonnes), wheeled loaders, motor graders, and large cranes - dominates demand. India’s road and expressway construction programme is the primary consumption driver. This sub-segment grows at approximately 7.1% CAGR through 2034, supported by sustained government capex.

The following chart visualises the equipment-type market share distribution for 2025:

Regional Market Insights

India's four regional clusters exhibit distinct demand drivers, infrastructure profiles, and regulatory dynamics. North India's dominance is expected to be maintained through 2034, though West & Central India is emerging as the fastest-growing region on the back of Maharashtra's infrastructure pipeline and the growing Central India mining belt.

|

Region |

Share (2025) |

Key Drivers |

|

North India |

30.0% |

NHAI highways, Delhi-NCR real estate, industrial corridors, DMIC |

|

West & Central India |

26.4% |

Mumbai infra, Pune IT corridors, Madhya Pradesh mining, port expansion |

|

South India |

24.8% |

Bengaluru metro, Chennai port, Hyderabad IT parks, AP Greenfield capital |

|

East & Northeast India |

18.8% |

Coal and iron-ore mining, NE India highway connectivity missions, Kolkata infra |

The regional share distribution chart below provides a visual comparison of the four regions' 2025 revenue contributions:

North India (30.0%)

North India leads with the highest revenue share, anchored by Delhi-NCR's sustained real estate construction and NHAI's expressway development programme in UP, Haryana, and Rajasthan. The Dedicated Freight Corridor (DFC) and Delhi-Mumbai Industrial Corridor have sustained equipment demand well above national averages since 2022.

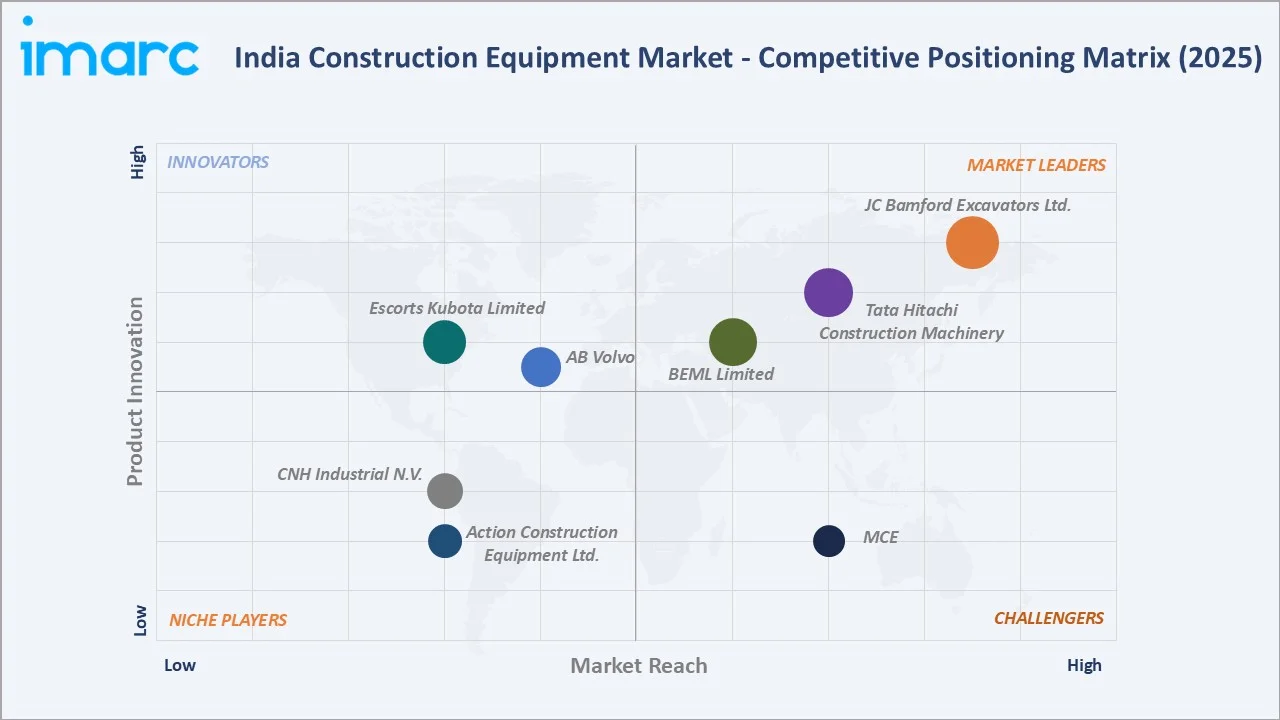

Competitive Landscape

The India construction equipment market exhibits a moderately consolidated structure, with JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery, AB Volvo. The competitive landscape is characterised by the co-existence of global OEM subsidiaries, domestic manufacturers, and specialist players serving niche applications.

|

Company Name |

Brand / Product Line |

Market Position |

Key Strength |

|

JC Bamford Excavators Ltd. |

JCB |

Leader |

Largest market share; backhoe & excavator dominance |

|

BEML Limited |

BEML / BH Series |

Leader |

Defence & mining equipment; strong PSU relationships |

|

Tata Hitachi Construction Machinery |

ZAXIS |

Leader |

Hydraulic excavators; local manufacturing advantage |

|

AB Volvo |

EC / L Series |

Challenger |

Premium segment; emission-compliant technology |

|

Escorts Kubota Limited |

Digmax |

Challenger |

Compact equipment & agricultural-infra crossover |

|

CNH Industrial N.V. |

Case |

Emerging |

Backhoe loaders; compact equipment growth |

|

MCE |

EarthMaster / Loader |

Emerging |

Backhoe loaders; rural & semi-urban penetration |

|

Action Construction Equipment Ltd. |

ACE |

Specialist |

Cranes & material handling; tier-2 city focus |

The competitive positioning matrix below maps key players on two axes - market presence (geographic reach) and product innovation capability - illustrating the leadership cluster and emerging challenger positions.

Key Company Profiles

J C Bamford Excavators Ltd

J C Bamford Excavators Ltd is a leading British multinational manufacturer of construction, agricultural, and industrial equipment, headquartered in Rocester, Staffordshire, UK. Founded in 1945 by Joseph Cyril Bamford, and has evolved into one of the world’s largest construction equipment manufacturers.

- Product Portfolio: Backhoe loaders, tracked & wheeled excavators, skid-steer loaders, compactors, telehandlers, and the EV range.

- Recent Developments: In 2025, J C Bamford Excavators Ltd launched its largest-ever 52-tonne excavator at the EXCON 2025 in Bengaluru, marking its entry into the heavy excavator segment. The launch was part of a broader showcase of over 10 new machines and digital solutions aimed at both domestic and export market.

- Strategic Focus: Localization of components, premium product positioning, and electrification roadmap for the Indian market by 2027.

BEML Limited

BEML Limited (formerly Bharat Earth Movers Limited) is a leading Indian public sector enterprise headquartered in Bengaluru. Established in 1964, the company plays a strategic role in supporting India’s core sectors, including defense, mining, construction, rail, and infrastructure.

- Product Portfolio: Dump trucks, mining dozers, motor graders, the BE series hydraulic excavators, pipe layers, and metro rail cars.

- Recent Developments: In 2026, BEML Limited introduced India’s first indigenously developed 35-ton electric dump truck, marking a significant step toward sustainable construction and mining equipment. The heavy-duty machine is designed for zero-emission operations and high energy efficiency, replacing conventional diesel-powered dumpers in mining and infrastructure applications.

- Strategic Focus: Self-reliance in defence-grade equipment, metro and rail expansion, and international market entry in Africa and Southeast Asia.

Tata Hitachi Construction Machinery

Tata Hitachi Construction Machinery is a leading construction equipment manufacturer in India, headquartered in Bengaluru. The company has strong domestic market presence with advanced Japanese engineering capabilities.

- Product Portfolio: ZAXIS series hydraulic excavators (mini to large), wheeled excavators, and soil compactors. The ZAXIS GI series is specifically designed for Indian ground conditions.

- Recent Developments: In 2025, Tata Hitachi Construction Machinery Company Pvt Ltd launched the Shinrai Prime CEV 5 backhoe loader, designed to meet the latest emission norms while enhancing performance and fuel efficiency. The new model features a CEV Stage V-compliant engine with advanced after-treatment systems, delivering improved power, lower emissions, and optimized operating costs.

- Strategic Focus: Hydraulic excavator segment leadership, Indian-condition product localisation, and digital after-sales transformation.

Market Concentration Analysis

Top-5 Market Share: The top-5 players - JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery, AB Volvo, Escorts Kubota Limited - collectively account for approximately 55-60% of total market revenue in 2025.

Fragmentation Level: The market is moderately fragmented, with over 25 active domestic and multinational players competing across diverse equipment categories. leading to intense competition, pricing pressures, and differentiated strategies based on product specialization, regional reach, and after-sales service capabilities.

Consolidation Trends: The market is witnessing gradual consolidation through strategic JVs, technology partnerships, and distributor acquisitions. Tata and Hitachi Construction Machinery joint venture and JCB's capacity expansion illustrate the trend towards scale building. Private equity interest in organised rental fleet companies (Quippo, Opifex‑Synergy) signals a consolidation wave in the services sub-segment, which could reshape the competitive dynamics of the overall market through 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

- Compact Construction Equipment (CAGR ~8.4%, 2026-2034): Urbanisation and urban utility projects create sustained demand for mini excavators and compact loaders - an increasingly attractive segment for both OEM investment and rental fleet building.

- Services Segment (CAGR ~9.1%): After-sales services, telematics subscriptions, and rental-as-a-service models offer recurring, high-margin revenue streams. Organised service networks remain underpenetrated beyond tier-1 cities.

- Electric Construction Equipment: Currently a nascent segment, it is expected to witness strong growth over the coming years, driven by government incentives, tightening urban emission norms, and OEM-led electrification strategies.

Emerging Market Opportunities

- Northeast India Infrastructure: Infrastructure development initiatives under the Act East Policy are accelerating connectivity projects in Northeast India, driving strong growth in construction equipment demand across a historically underserved region.

- Mining Sector Modernisation: Expansion in coal production and ongoing mineral block auctions are driving increased demand for heavy equipment such as dump trucks, surface miners, and hydraulic excavators, supporting the modernization of mining operations across India.

- Data Centre & Industrial Warehousing Construction: The surge in data centre investments and warehousing expansion by e-commerce players is generating a new demand pool for crane and material-handling equipment.

Venture & PE Investment Trends

- Private equity interest in India’s equipment rental sector has strengthened in recent years, with leading investors actively deploying capital to scale organized rental platforms, improve fleet quality, and expand regional presence.

- Equipment financing NBFCs such as Srei Equipment Finance (under restructuring) and competitors like L&T Finance are scaling equipment loan disbursals as construction activity accelerates.

- Fintech-driven digital equipment financing solutions are emerging as a key enabler in the market, offering flexible models such as zero-cost EMI and co-lending.

Future Market Outlook (2026-2034)

Growth Projections: The India construction equipment market is forecast to grow from USD 15.37 Billion in 2025 to USD 29.50 Billion by 2034, at a CAGR of 7.52%. Key milestones include USD 22.08 Billion by 2030. This trajectory assumes sustained government infrastructure spending, continued urbanisation at 1.5-2% annually, and stable commodity price environments.

Technological Disruptions: Three technology shifts are expected to meaningfully reshape market structure through 2034. First, battery-electric equipment will transition from niche to mainstream in compact categories by 2030.

Second, AI-driven predictive maintenance and semi-autonomous machine control will become standard features in new equipment sales by 2028-2030, redefining total cost of ownership models.

Third, the transition to stricter emission standards (CEV Stage V equivalent) is expected to drive a substantial replacement cycle, as a significant portion of the existing equipment fleet will need to be upgraded or replaced to meet new regulatory requirements over the coming years.

Industry Transformation: The industry is gradually shifting from a product-centric sales model toward a hybrid products-and-services approach, with services expected to account for a larger share of overall revenues over the long term.

Rental adoption is expected to rise significantly over the long term, reflecting a structural shift toward asset-light business models in the construction ecosystem.

Research Methodology

Primary Research

Primary data collection involved structured interviews and surveys with 150+ stakeholders across the value chain, including OEM executives, equipment dealers, fleet operators, construction contractors, government procurement officials, and financial institutions. Field interviews were conducted across 12 Indian states during 2024-2025. Primary research accounts for approximately 40% of total data inputs.

Secondary Research

Secondary sources encompass government publications (Ministry of Road Transport, Ministry of Mines, NITI Aayog), industry association reports (CII, CIDC), company annual reports and investor presentations, patent databases, trade publications, and customs-import-export data. CMIE and Bloomberg Terminal data were used for macroeconomic context.

Forecasting Models

A proprietary hybrid bottom-up/top-down forecasting model was applied. The bottom-up approach aggregates segment-level demand (by equipment type, solution type, and region) from primary field data. The top-down approach cross-validates against government infrastructure spending projections, GDP growth forecasts, and historical equipment penetration ratios.

India Construction Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solution Types Covered | Products, Services |

| Equipment Types Covered | Heavy Construction Equipment, Compact Construction Equipment |

| Types Covered | Loader, Cranes, Forklift, Excavator, Dozers, Others |

| Applications Covered | Excavation and Mining, Lifting and Material Handling, Earth Moving, Transportation, Others |

| Industries Covered | Oil and Gas, Construction and Infrastructure, Manufacturing, Mining, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery, AB Volvo, Escorts Kubota Limited, CNH Industrial N.V., MCE, Action Construction Equipment Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Construction Equipment Market Report

The India construction equipment market reached USD 15.37 Billion in 2025, driven by strong government infrastructure spending and urbanisation.

The market is projected to grow at a CAGR of 7.52% during 2026-2034, reaching USD 29.50 Billion by 2034.

The India construction equipment market is projected to reach USD 29.50 Billion by 2034, up from USD 15.37 Billion in 2025.

The Products segment dominates with a 69% revenue share in 2025, covering direct equipment sales of excavators, loaders, and cranes.

Heavy construction equipment leads with a 64% revenue share in 2025, driven by highway and metro rail construction projects.

North India dominates with a 30.0% revenue share in 2025, underpinned by NHAI expressways, Delhi-NCR real estate, and industrial corridors.

JC Bamford Excavators Ltd., BEML Limited, Tata Hitachi Construction Machinery, AB Volvo, Escorts Kubota Limited, CNH Industrial N.V., MCE, and Action Construction Equipment Ltd. are among the leading players.

Major drivers include government infrastructure capex of INR 11.11 Trillion (2024-25), urbanisation, real estate growth, and mining expansion.

Key trends include electric equipment adoption, telematics integration, rental market formalisation, and BS-VI emission compliance.

The India construction equipment market was valued at USD 10.69 Billion in 2020, establishing the historical baseline for the study.

The India construction equipment market is projected to reach USD 22.08 Billion by 2030, reflecting consistent 7.52% CAGR growth.

Key opportunities include compact electric equipment, organised rental services, northeast India infrastructure, and data centre construction.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)