India Construction Market Size, Share, Trends and Forecast by End Use Sector, Type of Contractor, Type of Construction, and Region, 2026-2034

India Construction Market Summary:

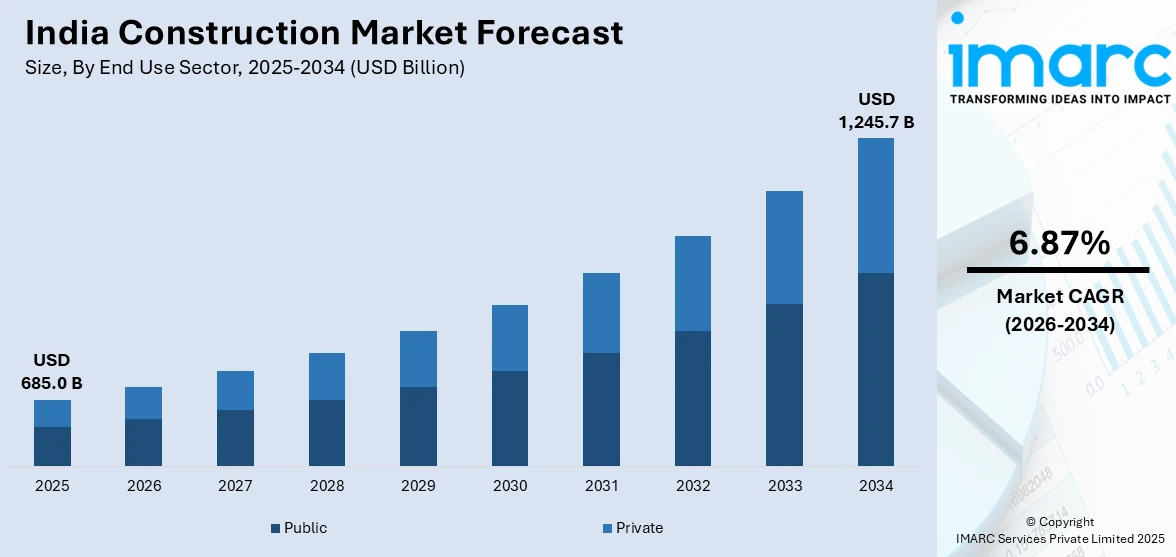

The India construction market size was valued at USD 685.0 Billion in 2025 and is projected to reach USD 1,245.7 Billion by 2034, growing at a compound annual growth rate of 6.87% from 2026-2034.

The India construction market is experiencing robust growth driven by unprecedented government capital expenditure on infrastructure development, rapid urbanization fueling the demand for residential and commercial spaces, and transformative policy initiatives aimed at modernizing the built environment. Rising investments in transportation networks, smart city projects, renewable energy installations, and industrial corridors are reshaping the construction landscape. Increasing adoption of advanced construction technologies, sustainable building practices, and public-private partnership (PPP) frameworks is further contributing to the India construction market share.

Key Takeaways and Insights:

- By End Use Sector: Public dominates the market with a share of 56.8% in 2025, driven by the government’s massive infrastructure spending programs, large-scale transportation and urban development projects, and sustained capital expenditure allocations.

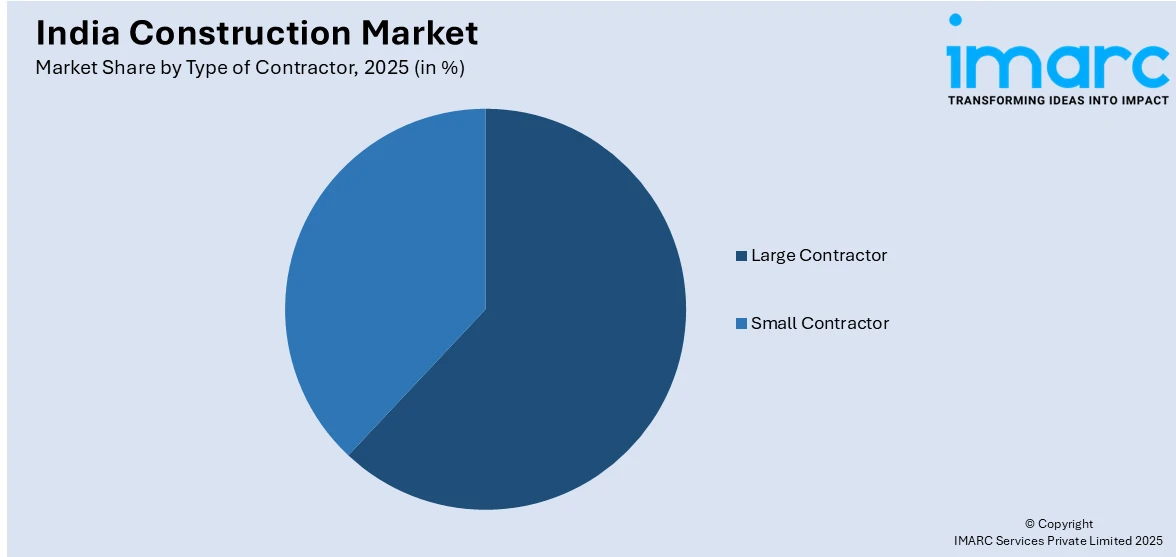

- By Type of Contractor: Large contractor represents the largest segment with a market share of 62.4% in 2025, owing to its capacity to execute complex mega-infrastructure projects, access to diversified funding sources, and strong order books.

- By Type of Construction: Buildings construction leads the market with a share of 44.9% in 2025, propelled by increasing housing demand from rapid urbanization, expanding commercial real estate requirements, and government affordable housing initiatives.

- By Region: West India dominates the market with a share of 31.6% in 2025. This dominance is because of Maharashtra and Gujarat serving as major economic hubs with concentrated industrial, commercial, and residential construction activity.

- Key Players: The India construction market exhibits highly competitive intensity, with diversified engineering conglomerates competing alongside specialized infrastructure developers, regional contractors, and emerging construction technology firms across public and private project segments.

To get more information on this market Request Sample

The India construction market is being driven by sustained infrastructure investment, rapid urbanization, industrial expansion, and rising private sector participation. Large-scale government spending on highways, metro rail systems, airports, ports, and regional connectivity projects continues to generate a strong pipeline of public works, supporting contractors and allied industries, such as cement, steel, and equipment manufacturing. Furthermore, increasing migration to cities is catalyzing the demand for housing, commercial offices, retail centers, and integrated townships. Growth in manufacturing, logistics, and digital infrastructure, including industrial corridors, warehouses, and data centers, is further strengthening construction activity. The market is also benefiting from technology adoption, such as prefabrication and modular building methods, which improve efficiency and delivery timelines. Investor interest in sustainable developments is accelerating renewable energy-related construction, reflected in 2026 when NTPC Green Energy Limited and GAIL approved a 50:50 joint venture to develop renewable energy projects nationwide, reinforcing clean energy infrastructure growth.

India Construction Market Trends:

Technology Adoption and Modern Construction Practices

The adoption of advanced construction technologies is transforming project execution in India by improving efficiency, quality, and delivery timelines. Practices, such as building information modeling, prefabrication, modular construction, and automation, are enabling faster completion of large infrastructure and real estate developments. This shift is exemplified by EPACK Prefab’s achievement in 2024, when it constructed a 151,000 sq ft structure in Mambattu, Andhra Pradesh, in just 150 hours using prefabrication and pre-engineered building technology, earning recognition from the Golden Book of World Records. As demand grows for rapid and high-standard delivery, technology-driven construction continues to expand sector capacity.

Public Infrastructure Investment

Sustained public expenditure on infrastructure continues to be a primary driver of construction growth in India, with major investments directed toward highways, railways, airports, ports, and urban transit systems. Multi-year capital expenditure programs provide contractors and engineering firms with long-term project visibility and execution stability. This momentum was evident in 2024 when Afcons Infrastructure received a ₹1,007 crore Letter of Acceptance for Package BH-05 of the Bhopal Metro Rail Project, involving an elevated viaduct and 13 metro stations to be completed within 36 months. Such large-scale public projects strengthen core infrastructure while supporting allied industries and employment generation.

Rising Investment in Sustainable Mixed-Use Real Estate

The growing investor interest in sustainable and integrated real estate developments is emerging as a key factor influencing the construction market in India. Mixed-use projects that combine residential, commercial, and retail spaces are increasingly preferred due to their efficient land use, higher asset value, and alignment with modern urban living requirements. The emphasis on green building standards further strengthens the demand for environmentally compliant construction practices. This trend is reflected in 2025 when Peerless General Finance and Investment Co Ltd announced its entry into real estate through Trayam, a ₹500 crore IGBC Gold pre-certified mixed-use project in New Town, Kolkata, scheduled for completion by 2029.

Market Outlook 2026-2034:

The India construction market demonstrates strong revenue growth potential throughout the forecast period, underpinned by irreversible urbanization trends, sustained government infrastructure spending, and expanding private sector investment. The market generated a revenue of USD 685.0 Billion in 2025 and is projected to reach a revenue of USD 1,245.7 Billion by 2034, growing at a compound annual growth rate of 6.87% from 2026-2034. Revenue expansion will be driven by accelerating highway, railway, and metro rail construction programs, rising demand for residential housing across metropolitan and tier-two cities, and growing investments in renewable energy infrastructure and industrial manufacturing corridors that collectively reinforce long-term construction sector momentum.

India Construction Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

End Use Sector |

Public |

56.8% |

|

Type of Contractor |

Large Contractor |

62.4% |

|

Type of Construction |

Buildings Construction |

44.9% |

|

Regional |

West India |

31.6% |

End Use Sector Insights:

- Public

- Private

Public dominates with a market share of 56.8% of the total India construction market in 2025.

Public holds the biggest share in the market due to extensive government investment in infrastructure and social development projects. Significant allocations toward roads, railways, airports, and metro systems sustain construction activity nationwide, while spending on schools, hospitals, and administrative facilities expands institutional development. National initiatives promoting urban mobility and regional connectivity further reinforce the demand. This commitment is evident in 2025, when Andhra Pradesh confirmed that construction of the Visakhapatnam Metro Rail Project will commence by October, adopting a double-decker model to strengthen urban transit infrastructure.

Another factor supporting public sector dominance is the long-term policy commitment to infrastructure modernization and economic growth. Government agencies commission large scale projects that require substantial budgets and multi-year execution timelines. Public works often involve strategic national priorities, attracting private contractors through public private collaborations. The emphasis on improving transportation networks, water supply systems, and affordable housing enhances construction volumes. With continuous capital expenditure in key sectors, the public segment remains the largest contributor to India’s overall construction activity.

Type of Contractor Insights:

Access the comprehensive market breakdown Request Sample

- Large Contractor

- Small Contractor

Large contractor exhibits a clear dominance with a 62.4% share of the total India construction market in 2025.

Large contractor leads the market owing to its ability to manage complex, high value projects across infrastructure, commercial, and residential sectors. This segment possesses strong financial capacity, advanced technical expertise, and access to modern equipment, enabling it to execute large scale developments efficiently. It is often preferred for government tenders and major private projects because of its proven track record and compliance standards. Its wide operational reach allows it to handle multiple projects simultaneously across regions.

Another reason for the dominance of large contractor is the growing demand for integrated project delivery and timely completion in India’s fast expanding construction sector. Large contractor benefits from established supply chains, skilled workforce availability, and partnerships with global technology providers. It can adopt advanced construction methods, improve quality control, and reduce execution risks. Its scale also enables better negotiation power with suppliers and subcontractors, lowering overall costs. As India increases investment in infrastructure and urban development, large contractor continues to secure the majority share of major construction opportunities.

Type of Construction Insights:

- Buildings Construction

- Heavy and Civil Engineering Construction

- Specialty Trade Contractors

- Land Planning and Development

Buildings construction leads with a market share of 44.9% of the total India construction market in 2025.

Buildings construction dominates the market because of rapid urbanization and the rising demand for residential and commercial spaces. Expanding city populations create ongoing requirements for housing, apartments, and integrated townships, while rising business activity supports growth in offices, retail centers, and hospitality developments. This trend is reinforced by steady private investment alongside government initiatives promoting affordable housing. Market momentum is reflected in 2026 with AGI Infra Limited’s launch of Urbana Square in Jalandhar, Punjab, comprising 142 commercial shops and 218 office spaces, totaling 360 units.

Another key factor behind its dominance is the increasing focus on modern urban development and real estate growth. Buildings projects are typically larger in volume and more frequent compared to specialized infrastructure works, ensuring consistent market activity. Developers invest heavily in new launches to address housing shortages and changing individual preferences. Advancements in construction technology and materials also improve efficiency and project delivery. With rising disposable incomes and stronger demand for quality living and working spaces, buildings construction continues to hold the largest share in India construction sector.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 31.6% share of the total India construction market in 2025.

West India represents the largest segment driven by its strong urbanization, industrial expansion, and large-scale infrastructure development. Major metropolitan areas drive continuous demand for residential, commercial, and mixed-use projects. The region attracts significant domestic and foreign investment, supporting real estate growth and public infrastructure upgrades. Ports, industrial corridors, and logistics hubs further stimulate construction activity. Rapid population growth in urban centers sustains housing demand, while ongoing modernization initiatives contribute to steady project pipelines across sectors.

West India’s strong position in the construction market is further supported by the concentration of major financial institutions and corporate headquarters, which consistently drive the demand for commercial real estate and business infrastructure. Regional growth is further reinforced through government-backed investments in highways, metro rail systems, and industrial development zones. This momentum was highlighted in 2025 when Prime Minister of India launched infrastructure projects worth INR 318.5 Billion in Maharashtra, focused on aviation, airport expansion, and connectivity improvements. Such large-scale public works continue to strengthen West India’s role as a leading construction hub.

Market Dynamics:

Growth Drivers:

Why is the India Construction Market Growing?

Expansion of Renewable Energy and Energy Infrastructure

India’s shift toward cleaner energy sources continues to accelerate construction activity across solar parks, wind farms, transmission corridors, and energy storage systems, each requiring significant civil works, structural foundations, and grid integration infrastructure. The scale of renewable capacity expansion demands coordinated development of substations, high-voltage transmission lines, and distribution upgrades to ensure reliable evacuation of power. In 2025, this momentum was reinforced when infrastructure projects worth ₹1.2 trillion were launched in Rajasthan, including the 4×700 MW Mahi Banswara Atomic Power Project valued at about ₹42,000 crore and the 925 MW Nokh Solar Park, alongside major solar-plus-storage developments, strengthening demand across generation and transmission segments.

Growth of Logistics, Warehousing, and Supply Chain Infrastructure

The rapid expansion of e-commerce is catalyzing the demand for modern logistics and warehousing infrastructure across India. Developers are increasingly investing in large-format distribution centers, cold storage facilities, and integrated logistics parks located near major consumption and manufacturing hubs. This demand is reinforced by the scale of digital commerce growth, with India’s e-commerce industry valued at INR 10,82,875 Crore in 2024 and projected to reach INR 29,88,735 Crore by 2030, reflecting a compound annual growth rate of 15%. As supply chains prioritize speed, efficiency, and organized storage, construction activity remains concentrated around industrial clusters and key transportation corridors.

Development of Smart Cities and Urban Infrastructure Programs

Urban development programs centered on technology-enabled governance and improved civic infrastructure are generating sustained construction activity across Indian cities. Projects involving integrated command centers, upgraded public transport networks, advanced waste management systems, and digital utilities require extensive civil, structural, and engineering coordination. This momentum is reflected in the 2025 announcement by the Karnataka government to develop the Greater Bengaluru Integrated Township near Bidadi, an 8,400-acre AI-powered city expected to function as Bengaluru’s second central business district within three years. Such large-scale smart urban developments, combining intelligent infrastructure with mixed-use planning, continue to expand construction pipelines in metropolitan and emerging urban regions.

Market Restraints:

What Challenges the India Construction Market is Facing?

Rising Raw Material Costs and Supply Chain Volatility Constraining Project Economics

Escalating prices of key construction inputs, including cement, steel, and bitumen, continue to exert significant pressure on project margins and contractor profitability. Cement costs remain elevated above pre-pandemic baselines, while steel prices fluctuate with global commodity cycles, creating uncertainty in project budgeting and bid pricing. Long-gestation infrastructure projects are particularly vulnerable to unexpected material cost spikes, compelling contractors to adopt price-escalation clauses and commodity hedging strategies that add complexity to project financial management.

Persistent Skilled Labor Shortages Limiting Construction Execution Capacity

The construction industry faces a substantial workforce gap, with shortages of trained workers for specialized tasks, including prefabricated component installation, digital construction tools operation, and advanced engineering techniques. The shortage of skilled labor in specialized trades constrains project execution timelines and quality assurance. Bridging this gap through vocational training and workforce development remains essential for sustaining construction output growth.

Regulatory Delays and Land Acquisition Challenges Impeding Project Timelines

Complex regulatory approval processes, multi-layered environmental clearance requirements, and protracted land acquisition procedures continue to hamper timely project execution across the construction sector. Inconsistent building codes and permit timelines across states create operational friction for contractors working on multi-state infrastructure programs. Streamlining approval mechanisms and harmonizing state-level regulations remain critical priorities for reducing project delays and cost overruns.

Competitive Landscape:

The India construction market exhibits a highly competitive landscape characterized by the presence of large diversified engineering and construction conglomerates competing alongside mid-sized regional contractors and emerging specialty firms across multiple project segments. Market dynamics reflect strategic positioning spanning integrated engineering procurement and construction offerings, turnkey project delivery capabilities, and technology-driven construction solutions. The competitive environment is increasingly shaped by digital transformation initiatives, sustainability certifications, and the ability to secure large-scale government contracts through hybrid annuity models and PPP frameworks. Leading players are expanding their order books through strategic diversification into renewable energy, metro rail, highway, and industrial construction verticals, while simultaneously investing in prefabrication, building information modeling, and modular construction capabilities to enhance execution efficiency and differentiate their service offerings in an increasingly technology-driven marketplace.

Recent Developments:

- November 2025: DLF announced plans to launch multiple luxury and ultra-premium housing projects across India over the next 18 months. Developments were planned in Goa, Mumbai, Gurugram, and Panchkula, including new phases of Privana and The Westpark. The Goa project was expected to launch in Q3 FY26, with others rolling out in FY27.

- October 2025: Larsen & Toubro’s Buildings & Factories business announced it had won major orders for large-scale construction projects in India. One key contract involves building a 5.9 million sq ft IT Park in Bengaluru for a reputed MNC, designed with LEED Platinum sustainability standards. L&T also secured another major order for a mixed-use development project in Mumbai with a 45-month execution timeline.

India Construction Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

End Use Sectors Covered |

Private, Public |

|

Type of Contractors Covered |

Large Contractor, Small Contractor |

|

Type of Constructions Covered |

Buildings Construction, Heavy and Civil Engineering Construction, Specialty Trade Contractors, Land Planning and Development |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Construction Market Report

The India construction market size was valued at USD 685.0 Billion in 2025.

The India construction market is expected to grow at a compound annual growth rate of 6.87% from 2026-2034 to reach USD 1,245.7 Billion by 2034.

Public dominates the India construction market with a share of 56.8% in 2025, driven by record government capital expenditure allocations for highways, railways, metro systems, and urban development projects.

Key factors driving the India construction market include the growing investor interest in sustainable mixed-use developments that integrate residential, retail, and office spaces to enhance land utilization and asset value. This is evident in 2025 with Peerless launching Trayam, a ?500 crore IGBC Gold project in Kolkata.

Major challenges include rising raw material costs and commodity price volatility, persistent skilled labor shortages constraining execution capacity, complex regulatory approval processes, land acquisition delays, inconsistent building codes across states, and supply chain disruptions affecting project timelines and profitability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)