India Continuous Glucose Monitoring Devices Market Size, Share, Trends and Forecast by Component, and Region, 2026-2034

India Continuous Glucose Monitoring Devices Market Size, Share, Trends & Forecast (2026-2034)

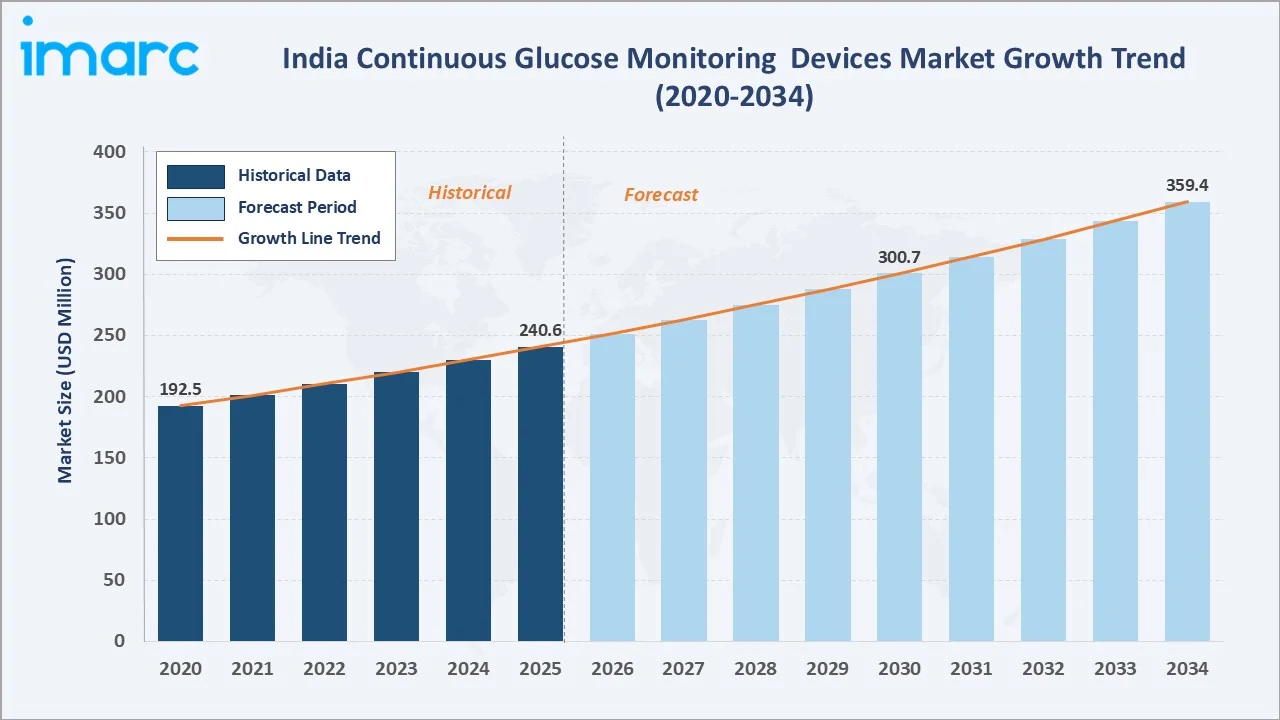

The India continuous glucose monitoring (CGM) devices market reached USD 240.6 Million in 2025 and is projected to reach USD 359.4 Million by 2034, growing at a CAGR of 4.56% during 2026-2034. The market is driven by India’s rapidly expanding diabetic population, technological advancements in CGM sensors, government digital health initiatives, and growing awareness of continuous glucose monitoring as a superior alternative to periodic finger-prick testing.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 240.6 Million |

| Forecast Market Size (2034) | USD 359.4 Million |

| CAGR (2026-2034) | 4.56% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

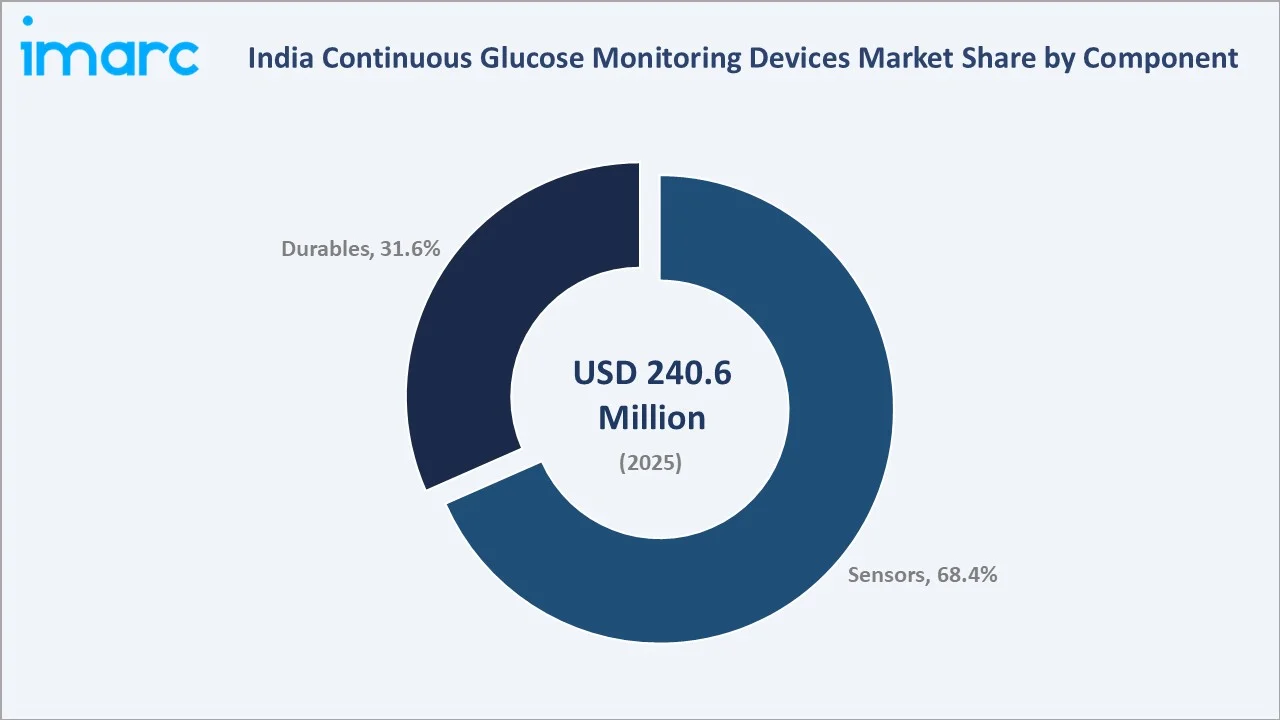

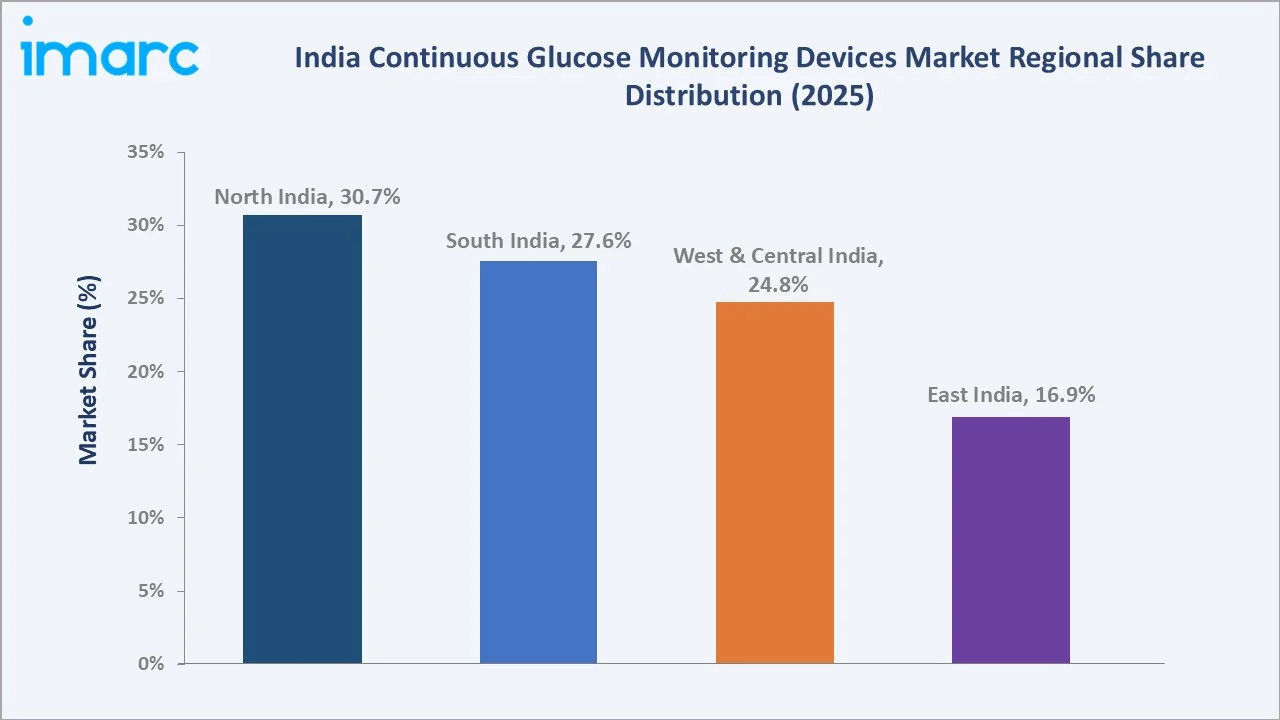

Sensors account for the dominant 68.4% share in 2025, reflecting the need for frequent replacement in CGM systems. North India’s 30.7% regional leadership reflects Delhi-NCR’s diabetes specialist hospital concentration and urban-affluent demographics.

To get more information on this market, Request Sample

The market grew from USD 192.5 Million in 2020 to USD 240.6 Million in 2025 at a steady 4.56% CAGR, driven by rising Type 2 diabetes prevalence, CGM technology improvements, and increasing affordability. The forecast to USD 359.4 Million by 2034 is reinforced by Abbott’s FreeStyle Libre expansion, domestic sensor manufacturing, and digital health integration under the Ayushman Bharat Digital Mission (ABDM).

Executive Summary

India’s CGM devices market is on a sustained growth trajectory, expanding from USD 192.5 Million in 2020 to a projected USD 359.4 Million by 2034 at a 4.56% CAGR. According to the International Diabetes Federation (2024), India currently has more than 101 million adults living with diabetes, making it the second-largest diabetic population after China. Rising Type 2 diabetes prevalence, worsening sedentary lifestyles, and increasing obesity rates are generating persistent demand for advanced glucose monitoring solutions.

Sensors command 68.4% of component revenue in 2025, driven by the recurring consumption model inherent in CGM systems. Users replace sensors every 7 to 15 days, depending on the product. Durables (receivers and transmitters) at 31.6% represent the one-time hardware investment in receivers and transmitters. North India leads regionally at 30.7%, anchored by Delhi-NCR’s private hospital density and high-income urban demographics with greater willingness to pay for premium health monitoring devices.

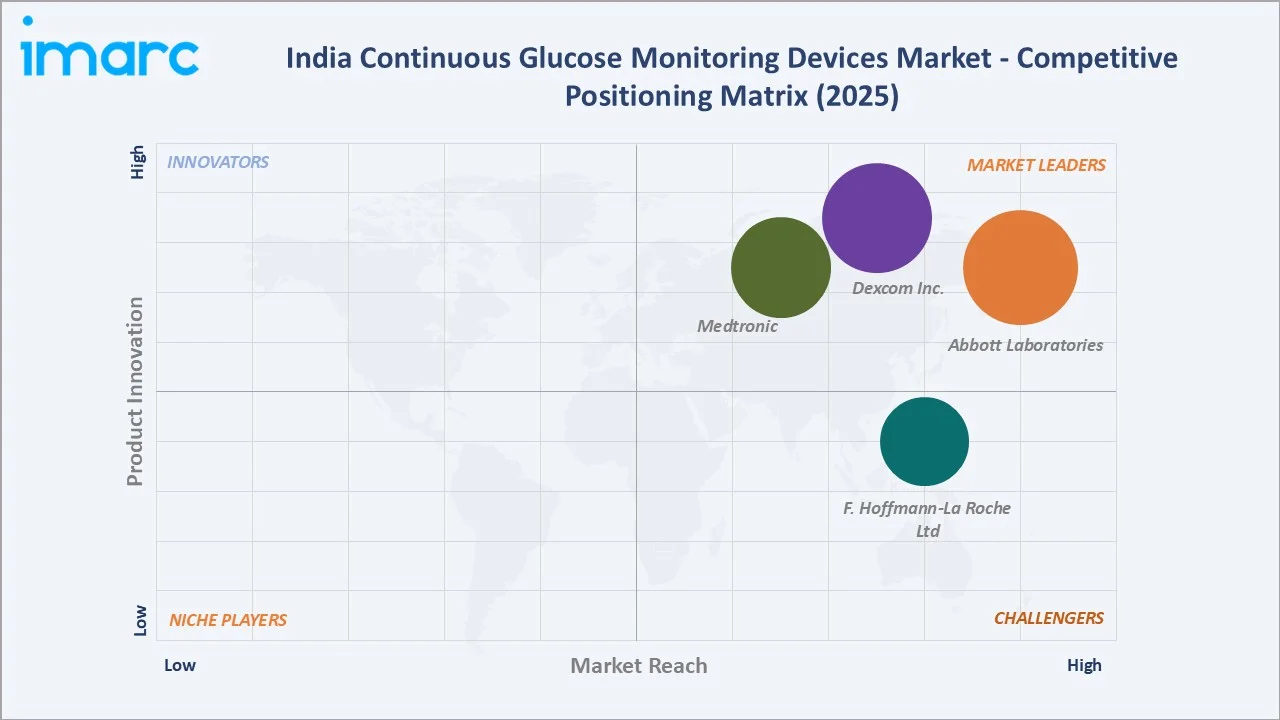

Key players, including Abbott Laboratories, Dexcom, Inc., Medtronic, and F. Hoffmann-La Roche Ltd, are intensifying their India market presence through local pricing strategies, e-commerce distribution, and co-marketing with diabetes clinics. Abbott’s August 2025 launch of FreeStyle Libre 2 Plus in India, offering minute-by-minute real-time monitoring, and Tracky’s June 2025 launch of India’s first Bluetooth-enabled Continuous Glucose Monitor (CGM), signal accelerating product innovation across the market.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Component | Sensors – 68.4% share (2025) |

| Second Largest Component | Durables (Receivers & Transmitters) – 31.6% share (2025) |

| Fastest Growing Component | Sensors – ~4.9% CAGR (2026-2034) |

| Leading Region | North India – 30.7% share (2025) |

| Second Largest Region | South India – 27.6% share (2025) |

| Top Companies | Abbott Laboratories, Dexcom, Inc., Medtronic, F. Hoffmann-La Roche Ltd |

Key Analytical Observations:

- Sensors at 68.4% (2025) dominate component revenue because CGM systems require sensor replacement every 7–15 days, creating a high-frequency recurring purchase cycle. India’s growing base of active CGM users directly amplifies sensor consumption volumes, making sensors the primary revenue driver through the forecast period.

- North India’s 30.7% (2025) regional share reflects Delhi-NCR’s concentration of endocrinology and diabetes specialty hospitals, the high-income urban demographics with greater product affordability, and strong e-commerce penetration enabling direct-to-consumer CGM sales across Punjab, UP, and Haryana.

- Durables at 31.6% (2025) represent the hardware ecosystem, receivers, transmitters, and smartphone-compatible readers, which enable CGM functionality. As more CGM systems shift toward smartphone-only display models without dedicated receivers, costs are declining, improving affordability for first-time users in price-sensitive Indian markets.

- The 4.56% CAGR through 2034 reflects a measured growth trajectory constrained by product affordability challenges. At USD 3,500–5,000 per year for premium CGM systems, penetration beyond India’s top-income quintile remains limited. Government reimbursement expansion and local manufacturing under Make in India are the primary catalysts expected to accelerate adoption after 2027.

- South India at 27.6% (2025) is the second-largest regional market, driven by Tamil Nadu and Karnataka’s strong private healthcare infrastructure, high diabetes prevalence in urban South Indian populations, and the biotech corridor in Bengaluru and Hyderabad facilitating distribution partnerships.

India Continuous Glucose Monitoring Devices Market Overview

Continuous glucose monitoring (CGM) devices are wearable medical systems that measure glucose levels in interstitial fluid every 1–15 minutes, providing real-time and retrospective glucose data to patients and clinicians via dedicated receivers or smartphone applications. CGM systems consist of a subcutaneous sensor, a transmitter (in real-time CGM), and a display device, together enabling uninterrupted glucose trend analysis and hypoglycemia/hyperglycemia alerts.

India’s CGM ecosystem is evolving rapidly, shaped by the world’s second-largest diabetic population, accelerating digital health infrastructure under ABDM, and government manufacturing incentives. The market is transitioning from a premium niche to broader adoption as product prices decline through local manufacturing initiatives. India’s Make in India program and the PLI scheme for medical devices are encouraging domestic sensor production, with Tracky’s June 2025 Bluetooth-enabled CGM launch marking a significant milestone in domestic CGM manufacturing capability.

Market Dynamics

To evaluate market opportunities, Request Sample

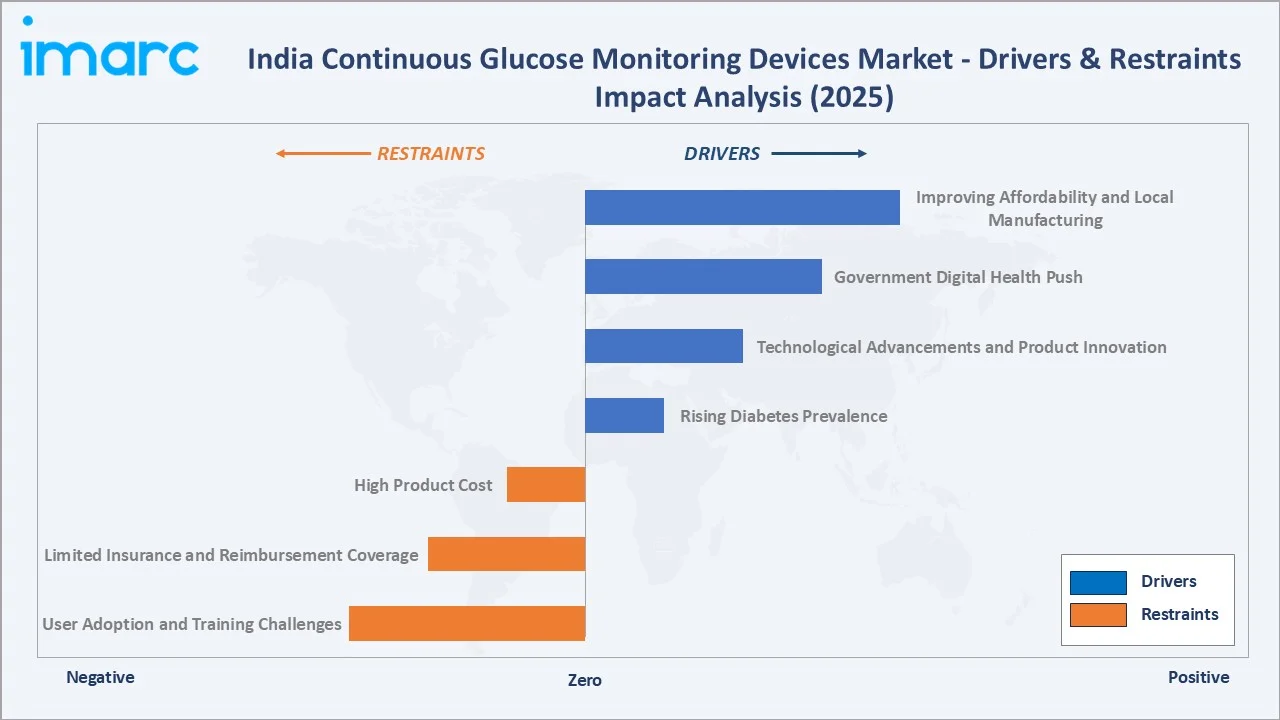

Market Drivers

- Rising Diabetes Prevalence: According to the International Diabetes Federation (2024), India currently has more than 101 million adults living with diabetes. The IDF further projects this to reach 134 million by 2045. This escalating disease burden creates persistent structural demand for continuous monitoring solutions that provide better glycemic control than periodic testing.

- Technological Advancements and Product Innovation: Long-wear sensors, factory-calibrated systems eliminating finger-prick calibration, AI-driven glucose trend analytics, and Bluetooth smartphone integration have dramatically improved CGM usability. Abbott’s FreeStyle Libre 2 Plus, launched in India in August 2025, offers real-time minute-by-minute glucose data with optional alarms, raising the clinical standard for India’s CGM market.

- Government Digital Health Push: The Ayushman Bharat Digital Mission (ABDM) is creating a framework for CGM integration with electronic health records and telemedicine platforms, opening new institutional procurement channels beyond the current private-pay user base.

- Improving Affordability and Local Manufacturing: Domestic manufacturing under Make in India and PLI is reducing CGM costs. E-commerce through Flipkart Health+ and Amazon India has improved Tier-2 city accessibility. Corporate wellness programs are increasingly procuring CGM for pre-diabetic employee populations.

Market Restraints

- High Product Cost: Premium CGM systems cost USD 3,500–5,000 annually per patient, limiting adoption to India’s high-income urban segments. Even flash glucose monitoring costs approximately USD 300–400 per year, which remains prohibitive for the majority of India’s 101 million diabetic patients who rely on government healthcare facilities.

- Limited Insurance and Reimbursement Coverage: CGM devices are not covered under most Indian health insurance policies or government healthcare programs, including Ayushman Bharat PM-JAY. This absence of reimbursement suppresses adoption among the middle and lower-income diabetic population, where CGM clinical benefits are potentially highest for patients with poor glycemic control.

- User Adoption and Training Challenges: Successful CGM use requires patient education on sensor insertion, data interpretation, and alert management. Limited diabetes educator capacity in Tier-2 and Tier-3 cities creates an adoption barrier. Skin irritation and sensor adhesion issues in India’s hot and humid climate conditions also contribute to device discontinuation rates.

Market Opportunities

- Closed-Loop Insulin Delivery Integration: Hybrid closed-loop systems, which combine CGM sensors with automated insulin pumps, represent the highest-value opportunity in India’s diabetes care market. As insulin pump adoption grows, each pump user generates ongoing CGM sensor consumption. Medtronic’s Guardian CGM paired with the MiniMed 780G pump system is currently the primary closed-loop offering in India.

- Non-Invasive and Implantable CGM Innovation: Senseonics’ Eversense implantable CGM and non-invasive CGM prototypes using spectroscopic techniques represent the next frontier. If non-invasive CGM achieves clinical accuracy validation, India’s cost sensitivity and needle aversion will make it a high-adoption market, significantly expanding the addressable patient population.

Market Challenges

- Regulatory and Quality Standards: CDSCO Class C medical device certification requires demonstration of clinical accuracy. Stringent quality standards and the need for India-specific clinical validation data create a significant barrier for new domestic CGM manufacturers seeking to enter the market.

- Sensor Performance in Tropical Conditions: India’s high ambient temperature, humidity, and physical activity patterns create specific CGM calibration and adhesive challenges. Sensor drift and premature detachment in humid conditions remain a persistent technical challenge for global CGM manufacturers seeking broader India market adoption.

Emerging Market Trends

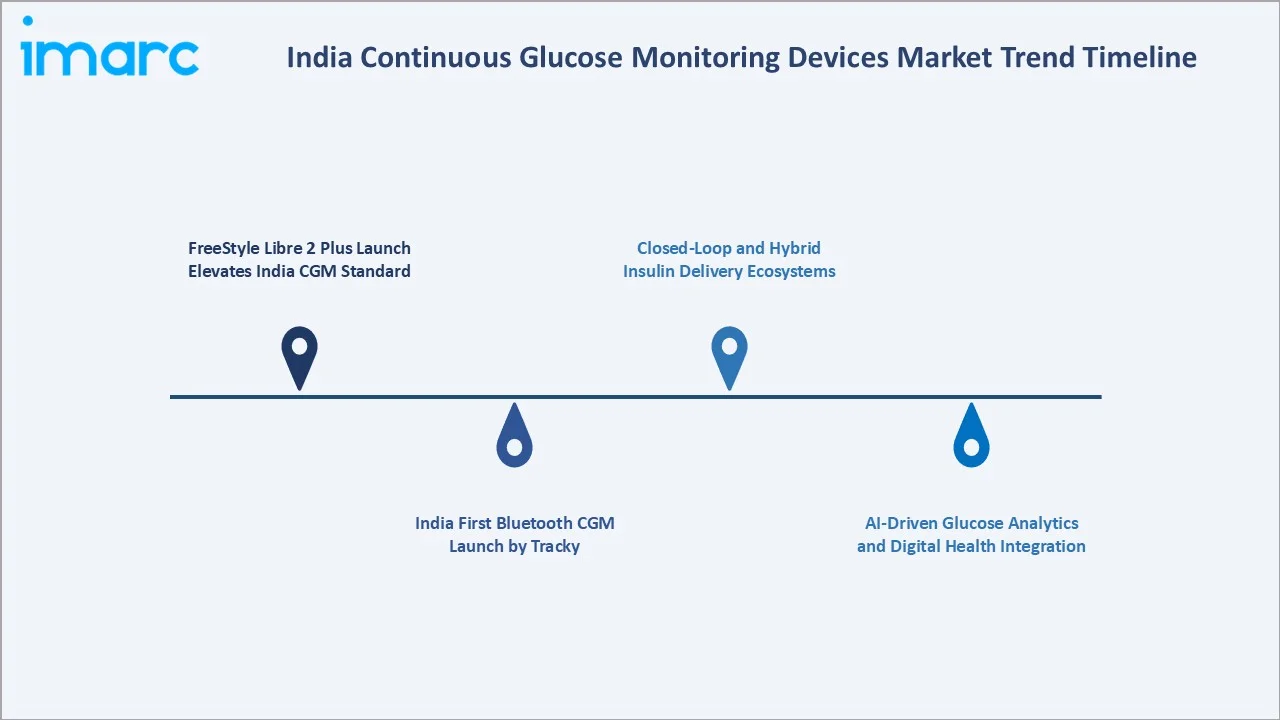

1. FreeStyle Libre 2 Plus Launch Elevates India’s CGM Standard

In August 2025, Abbott launched the FreeStyle Libre 2 Plus in India, offering real-time minute-by-minute glucose monitoring with optional high and low glucose alarms via a 14-day wear sensor. This upgrade from the FreeStyle Libre’s scan-to-see model to continuous real-time reading directly addresses India’s growing demand for proactive diabetes management, particularly among Type 1 patients and those with brittle diabetes.

2. India’s First Bluetooth CGM Launch by Tracky

In June 2025, Tracky launched India’s first Bluetooth-enabled CGM device, enabling scan-free real-time glucose tracking via a mobile application without a dedicated receiver. This domestic innovation targets India’s growing middle-income diabetic population seeking affordable, smartphone-integrated monitoring and marks a pivotal step in building India’s domestic CGM manufacturing capability.

3. AI-Driven Glucose Analytics and Digital Health Integration

CGM platforms are incorporating AI-powered glucose prediction engines forecasting trends 30–60 minutes ahead, enabling proactive meal and insulin adjustments. Integration with India’s ABDM health ID allows CGM data to flow into patient health records, enabling remote endocrinologist care for Tier-2 city patients.

4. Closed-Loop and Hybrid Insulin Delivery Ecosystems

Automated insulin delivery systems combining CGM sensors with smart insulin pumps are gaining clinical traction at India’s leading diabetes centers. Medtronic’s MiniMed 780G system, launched in India in March 2022, pairs the Guardian 4 CGM sensor with an automated pump for Type 1 diabetes management, representing the highest-value CGM application in the Indian market.

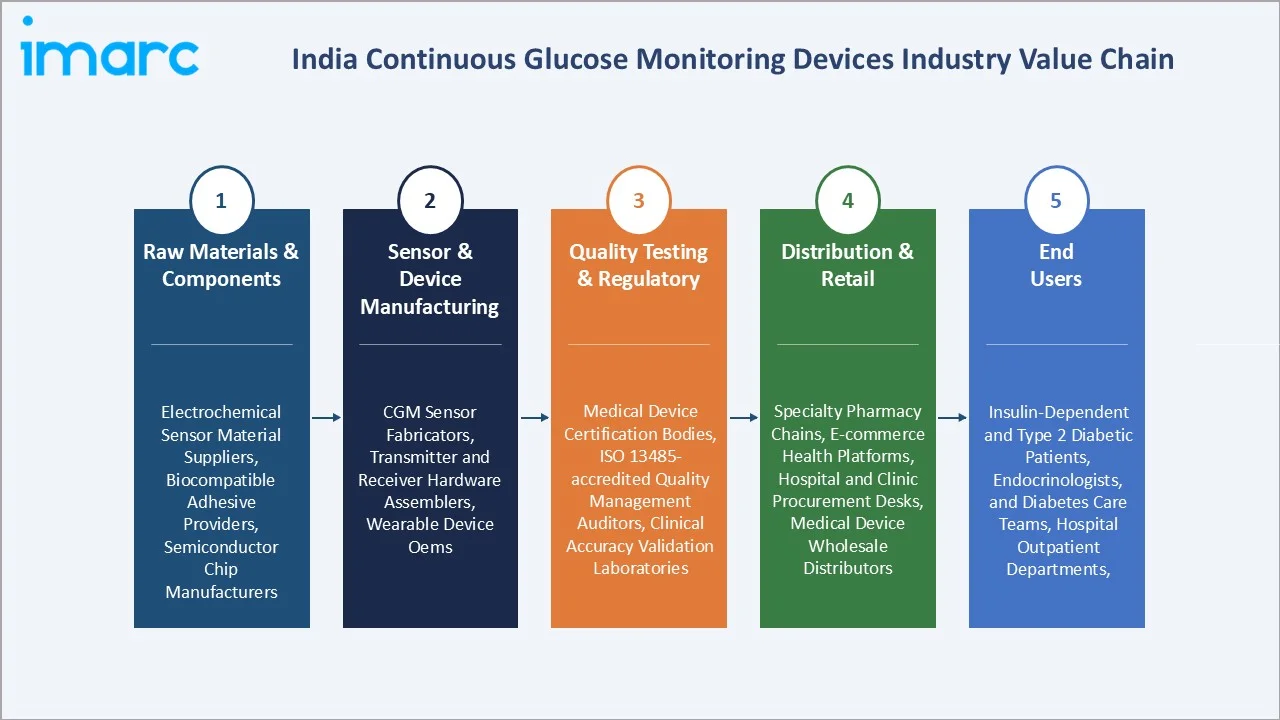

Industry Value Chain Analysis

| Stage | Key Players / Examples |

|---|---|

| Raw Materials & Components | Electrochemical sensor material suppliers, biocompatible adhesive providers, semiconductor chip manufacturers |

| Sensor & Device Manufacturing | CGM sensor fabricators, transmitter and receiver hardware assemblers, wearable device OEMs |

| Quality Testing & Regulatory | Medical device certification bodies, ISO 13485-accredited quality management auditors, clinical accuracy validation laboratories |

| Distribution & Retail | Specialty pharmacy chains, e-commerce health platforms, hospital and clinic procurement desks, medical device wholesale distributors |

| End Users | Insulin-dependent and Type 2 diabetic patients, endocrinologists and diabetes care teams, hospital outpatient departments |

Technology Landscape in the India CGM Devices Industry

Electrochemical Sensor Technology

Current CGM sensors use glucose oxidase-based electrochemical detection to measure interstitial fluid glucose every 1–15 minutes. Abbott’s FreeStyle Libre 2 Plus uses a 14-day factory-calibrated sensor with no finger-prick calibration required, while Dexcom G7’s 10-day sensor achieves a mean absolute relative difference (MARD) of 8.2%, the highest accuracy in the CGM category. Sensor miniaturization has reduced insertion discomfort and improved wearability for India’s hot and humid climate conditions.

Wireless Connectivity and Smartphone Integration

Bluetooth Low Energy (BLE) connectivity enables CGM sensors to transmit glucose readings directly to iOS and Android smartphones, eliminating dedicated receivers in next-generation devices. Abbott’s NFC-based scan architecture represents a dominant connectivity paradigm in India’s CGM market. Integration with Apple Health, Google Fit, and Indian digital health apps enables seamless health data aggregation for holistic diabetes management.

Non-Invasive and Implantable Sensor Innovation

Senseonics’ Eversense E3 implantable CGM system, offering 180-day continuous monitoring from a subcutaneous fluorescence-based sensor, represents the long-wear frontier currently in clinical evaluation for India entry. Non-invasive CGM technologies using near-infrared spectroscopy, electromagnetic sensing, and microneedle arrays are in advanced development stages globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Component | Sensors | 68.4% |

2025 |

| Region | North India | 30.7% |

2025 |

By Component

Sensors dominate the market at 68.4% in 2025. The sensors segment comprises the subcutaneous glucose-detecting elements that require replacement every 7 to 15 days, creating the recurring revenue backbone of the CGM market. India’s growing installed base of active CGM users directly multiplies sensor consumption. Abbott’s 14-day FreeStyle Libre sensor and Dexcom’s 10-day G7 sensor represent the two dominant product formats in India’s sensor market, with Abbott commanding significantly higher volume through its lower price point.

To access detailed market analysis, Request Sample

Durables (receivers and transmitters) at 31.6% encompass the hardware ecosystem enabling CGM functionality. Dedicated receivers are increasingly being replaced by smartphone apps in newer models, reducing costs for patients. The durable segment is projected to grow at approximately 3.9% CAGR through 2034, as software-enabled displays gradually replace dedicated hardware.

Regional Market Insights

North India leads the India CGM devices market with a 30.7% share in 2025. Delhi-NCR hosts India’s highest concentration of endocrinology centers, diabetes specialty hospitals, and high-income urban populations with both the ability and awareness to use CGM devices. Strong e-commerce penetration across North India’s urban belt facilitates direct-to-consumer CGM procurement, further amplifying regional demand.

South India, at 27.6%, is the second-largest and a rapidly growing market, underpinned by Tamil Nadu’s exceptionally high urban diabetes prevalence and Karnataka’s strong tech-savvy consumer base receptive to digital health devices.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| North India | 30.7% | Delhi-NCR endocrinology hub, high-income urban demographics, strong e-commerce CGM adoption, dense diabetes clinic network |

| South India | 27.6% | High diabetes prevalence in Tamil Nadu and Andhra Pradesh, strong private hospital networks, biotech corridor in Bengaluru and Hyderabad |

| West and Central India | 24.8% | Mumbai’s corporate wellness adoption, Maharashtra and Gujarat pharmaceutical industry synergies, growing Pune and Ahmedabad diabetes specialty infrastructure |

| East India | 16.9% | Expanding healthcare infrastructure in Kolkata, rising diabetes awareness, government healthcare programs increasing access in West Bengal and Odisha |

West and Central India, at 24.8%, benefit from Mumbai’s corporate wellness CGM procurement and Gujarat’s growing medical device distribution network. East India at 16.9% is the fastest-growing region on a CAGR basis as government healthcare investment accelerates.

Competitive Landscape

India’s CGM devices market is moderately concentrated, with Abbott Laboratories and Dexcom, Inc. collectively dominating CGM sensor revenue through their established FreeStyle Libre and G7 platforms, respectively. Medtronic holds leadership in the insulin pump-integrated CGM segment.

| Company | Product Brand | Market Position | Core Strength |

|---|---|---|---|

| Abbott Laboratories | FreeStyle Libre, Libre 2 Plus, FreeStyle Optium Neo, FreeStyle Optium Strips, LibreView cloud data management platform, LibreLinkUp | Market Leader | One of India’s largest CGM market shares, affordable flash CGM, 14-day factory-calibrated sensor, strong pharmacy distribution |

| Dexcom, Inc. | Dexcom G7 and G7 15 Day, Dexcom G6, Dexcom ONE+, and Stelo biosensor | Market Leader | Highest sensor accuracy, direct Bluetooth-to-phone connectivity, preferred by Type 1 patients and closed-loop users |

| Medtronic | MiniMed 780G, Guardian 4 | Co-Leader | Insulin pump-integrated CGM leadership, closed-loop automation for Type 1 diabetes, strong hospital channel presence |

| F. Hoffmann-La Roche Ltd | Accu-Chek SmartGuide, mySugr | Strong Challenger | Established blood glucose brand equity, Roche Care ecosystem integration, strong pharmacy distribution network |

The market is experiencing increasing competition from Indian domestic entrants, including Tracky, targeting the price-sensitive mass market with Bluetooth-enabled CGM solutions.

Key Company Profiles

Abbott Laboratories

Abbott Laboratories is the global and Indian market leader in flash and continuous glucose monitoring through its FreeStyle Libre platform. Abbott Diabetes Care India Pvt. Ltd. distributes CGM products to major hospital chains and direct-to-consumer e-commerce.

- Product Portfolio: FreeStyle Libre 2 Plus, FreeStyle Libre, FreeStyle Optium Neo, FreeStyle Optium Strips, LibreView cloud data management platform, and LibreLinkUp.

- Recent Developments: In August 2025, Abbott Laboratories launched the FreeStyle Libre 2 Plus sensor in India, offering automatic glucose readings every minute on compatible smartphones with optional high and low glucose alarms.

- Strategic Focus: Broad India penetration through affordable pricing; FreeStyle Libre 2 Plus expansion across endocrinology clinics; LibreView integration with ABDM health ID for remote monitoring; partnership with Indian telemedicine platforms.

Dexcom, Inc.

Dexcom, Inc. is the global leader in real-time CGM accuracy and technology innovation. Dexcom India Pvt. Ltd. targets India’s premium CGM segment, including Type 1 diabetes patients, those on insulin pump therapy, and high-compliance Type 2 users seeking best-in-class glucose management.

- Product Portfolio: Dexcom G7 and G7 15 Day, Dexcom G6, Dexcom ONE+, and Stelo biosensor.

- Recent Developments: Dexcom, Inc. reaffirmed its full-year revenue forecast of USD 5.16–5.25 billion after reporting quarterly revenue of USD 1.19 billion, up 15% year-on-year and slightly above analyst estimates. The performance was supported by strong demand for the continuous glucose monitor and broader rollout of its G7 15-Day sensor.

- Strategic Focus: Premium CGM market leadership in India’s Type 1 and insulin-dependent Type 2 segment; closed-loop insulin delivery system integrations with Tandem Diabetes and Medtronic; Clarity platform analytics for remote endocrinologist care.

Market Concentration Analysis

India’s CGM devices market is moderately concentrated. Abbott Laboratories and Dexcom, Inc. collectively account for an estimated 70–75% of premium real-time CGM and flash glucose monitoring revenue in 2025. Medtronic holds approximately 15–20% of the insulin pump-integrated CGM segment.

Market concentration is expected to moderate progressively as domestic CGM manufacturers scale production under Make in India incentives and introduce CDSCO-certified CGM products in the USD 50–100 per month price range. Insurance policy evolution to include CGM coverage, a policy change advocated by the RSSDI (Research Society for the Study of Diabetes in India), would be the single largest structural driver of market democratization through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Sensors (~4.9% CAGR), AI-integrated CGM platforms, closed-loop insulin delivery ecosystems, and OTC CGM for pre-diabetic populations represent the highest-value investment vectors through 2034. The OTC pre-diabetic monitoring segment, targeting India’s 136 million pre-diabetic adults, represents an incremental multi-hundred-million-dollar opportunity currently unaddressed by any India-specific CGM product.

Emerging Market Expansion

Tier-2 and Tier-3 cities represent the largest under-penetrated geography. Rising smartphone penetration, expanding pharmacy chains (PharmEasy, Netmeds), and telehealth platforms (Apollo 24/7, Practo) are creating digital distribution pathways for CGM devices in cities previously limited to periodic blood glucose monitoring.

Venture and Institutional Investment Trends

- Indian healthtech startups developing CGM-integrated diabetes platforms raised USD 120+ Million in 2023–2025. BeatO (diabetes management with CGM integration) received Series C funding, while Sugar.fit and HealthifyMe have embedded CGM trial programs within their diabetes care platforms.

- Abbott’s India-specific FreeStyle Libre pricing strategy has created a template for global CGM companies to capture India’s middle-income market through tiered pricing. Replicating this approach across sensor subscription models could accelerate CGM adoption among the 20–30 million cost-sensitive insulin-dependent Type 2 patients.

Future Market Outlook (2026-2034)

India’s CGM devices market will expand from USD 240.6 Million in 2025 to USD 359.4 Million by 2034 at a 4.56% CAGR, adding USD 118.8 Million in incremental revenue. The sensor segment will continue to dominate, driven by the recurring replacement model and rising active CGM user base. Affordable domestic CGM products, government insurance expansion, and AI analytics integration are the three catalysts most likely to accelerate growth above the baseline trajectory.

By 2034, non-invasive CGM technology could disrupt the market by eliminating the skin penetration barrier. India’s young, smartphone-native diabetic population and 136 million pre-diabetic adults position it as one of the highest-potential CGM markets in Asia for the 2026–2034 forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including endocrinologists, diabetes educators, hospital procurement managers, CGM device distributor representatives, CDSCO regulatory consultants, and digital health platform operators across Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad.

Secondary Research

Secondary research covered CDSCO device registration databases, ICMR National Diabetes and Diabetic Retinopathy Survey, IDF Diabetes Atlas 10th Edition, company annual reports and investor presentations, SEBI filings for listed companies, RSSDI clinical guidelines, and publications including Diabetologia, Journal of Diabetes Science and Technology, and Express Healthcare.

Forecasting Models

Market size estimations used bottom-up and top-down approaches, incorporating diabetes prevalence projections, CGM adoption rate modeling by income quintile, sensor replacement cycle economics, and import-export data analysis. A base CAGR of 4.56% reflects consensus validated against CDSCO device registration growth trends and IMARC’s primary expert panel inputs through 2034.

India Continuous Glucose Monitoring Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Sensors, Durables (Receivers and Transmitters) |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Abbott Laboratories, Dexcom Inc., Medtronic, F. Hoffmann-La Roche Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India continuous glucose monitoring devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India continuous glucose monitoring devices market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India continuous glucose monitoring devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Continuous Glucose Monitoring Devices Market Report

The market reached USD 240.6 Million in 2025 and is forecast to reach USD 359.4 Million by 2034 at a 4.56% CAGR during 2026-2034.

Sensors dominate with a 68.4% share in 2025, driven by the recurring 7–15 day replacement cycle that makes sensors the primary recurring revenue driver in CGM systems.

North India leads at 30.7% in 2025, anchored by Delhi-NCR’s concentration of diabetes specialty hospitals and high-income urban demographics with greater CGM adoption propensity.

Key players include Abbott Laboratories, Dexcom, Inc., Medtronic, and F. Hoffmann-La Roche Ltd.

Rising diabetes prevalence, technological advancements, government digital health initiatives (ABDM), improving affordability through local manufacturing, and growing awareness of CGM benefits over periodic finger-prick testing.

High product cost, absence of insurance reimbursement, limited diabetes educator access in Tier-2 cities, and sensor performance challenges in India’s hot and humid climate conditions.

OTC CGM for India’s 136 million pre-diabetic population, AI-integrated glucose analytics platforms, closed-loop insulin delivery ecosystems, and affordable domestic sensor manufacturing under Make in India incentives.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade