India Copper Pipes and Tubes Market Size, Share, Trends and Forecast by Finish Type, Outer Diameter, End-User, and Region, 2026-2034

India Copper Pipes and Tubes Market Summary:

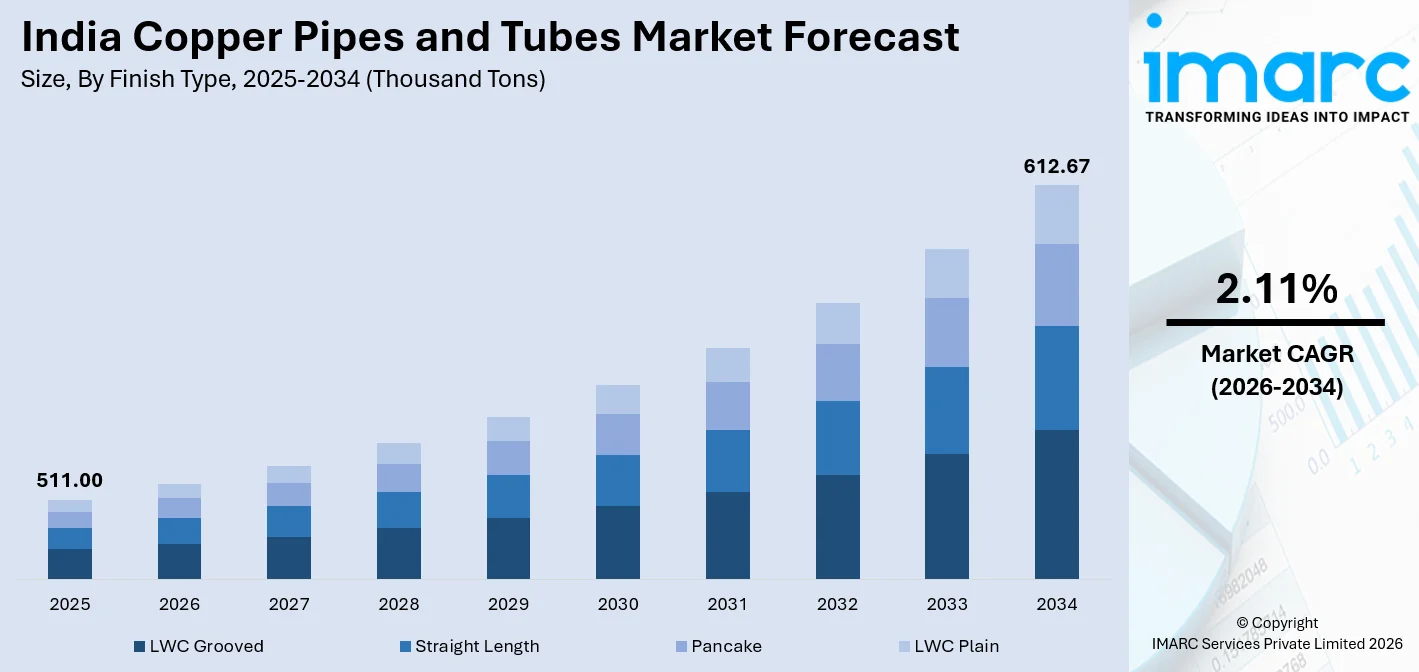

The India copper pipes and tubes market size reached 511.00 Thousand Tons in 2025 and is projected to reach 612.67 Thousand Tons by 2034, growing at a compound annual growth rate of 2.11% from 2026-2034.

The India copper pipes and tubes market is experiencing consistent growth underpinned by rapid urbanization, expanding HVAC adoption, and large-scale infrastructure development. Government initiatives, such as the Smart Cities Mission and PM Awas Yojana, are accelerating construction activity, while rising demand in industrial heat exchange and plumbing applications is reinforcing broader market growth. The superior thermal conductivity, corrosion resistance, and recyclability of copper continue to drive its preference across residential, commercial, and industrial applications, strengthening the India copper pipes and tubes market share.

Key Takeaways and Insights:

- By Finish Type: LWC grooved represents the largest segment with a market share of 38.5% in 2025, driven by its superior compatibility with HVAC refrigeration systems and widespread adoption in split air conditioning units across residential and commercial installations.

- By Outer Diameter: 3/8, ½, 5/8 inch dominates the market with a share of 45.5% in 2025, owing to widespread adoption in air conditioning and refrigeration systems where these standard dimensions are the most widely specified by original equipment manufacturers.

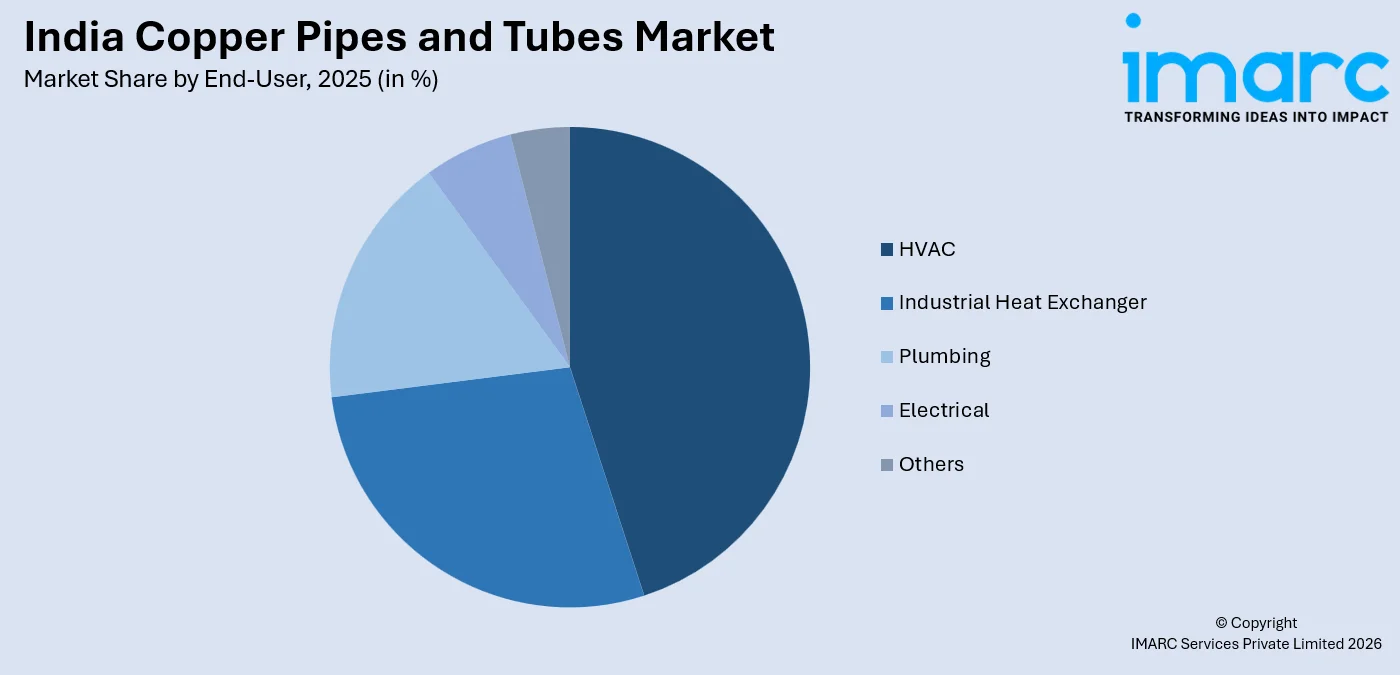

- By End-User: HVAC leads the market with a share of 41.5% in 2025, reflecting the rapid expansion of air conditioning and refrigeration systems across India’s residential, commercial, and industrial sectors driven by rising incomes and urbanization.

- By Region: West India represents the largest segment with a market share of 30.5% in 2025, supported by a strong concentration of industrial manufacturing hubs, a thriving commercial real estate sector, and robust HVAC adoption across Maharashtra and Gujarat.

- Key Players: The India copper pipes and tubes market is moderately competitive, with established domestic manufacturers and vertically integrated metals conglomerates competing on product quality, production capacity, and supply chain efficiency to capture growing sectoral demand.

To get more information on this market Request Sample

The India copper pipes and tubes market is advancing, driven by a convergence of urbanization, industrial expansion, and government-led infrastructure initiatives. This need is reinforced by demographic trends, as World Bank data indicates that approximately 36.87% of India’s total population resided in urban areas in 2024, reflecting a steady migration toward cities and the resulting demand for housing, utilities, and urban services. The growing construction of residential complexes, commercial facilities, healthcare institutions, and public infrastructure is increasing the need for durable plumbing, water distribution, and cooling systems where copper pipes and tubes are widely utilized. Industrial growth across manufacturing, engineering, and processing sectors is also contributing to the demand for copper tubing in thermal management and fluid transfer systems. Furthermore, the rising adoption of air-conditioning and refrigeration systems in buildings and industrial environments is contributing to the market growth. Together, these trends are strengthening the requirement for high-performance piping materials capable of delivering long service life and reliable operation across multiple infrastructure and industrial applications in India.

India Copper Pipes and Tubes Market Trends:

Rise of Building and Construction Activity

The steady expansion of residential, commercial, and institutional construction across India is strengthening demand for copper pipes and tubes used in plumbing, water distribution, and building services infrastructure. Copper is widely selected for these systems due to its durability, corrosion resistance, and ability to support long service life in concealed piping installations. Rising urbanization, increasing housing demand, redevelopment of older properties, and the construction of premium real estate projects are expanding the scope for high-quality piping materials. Reflecting this trend, Shapoorji Pallonji Real Estate launched the VANAHA Verdant residential development in Pune in 2025, covering about 5 acres with nearly 10 lakh square feet of saleable area and an estimated revenue potential of around INR 8 billion. Such large-scale projects reinforce demand for reliable plumbing and piping materials, supporting the continued adoption of copper pipes and tubes in modern building infrastructure.

Expansion of Domestic Copper Production Capacity

A key factor driving the India copper pipes and tubes market is the expansion of domestic copper production capacity, which improves raw material availability for downstream manufacturers. Higher local copper output supports a more reliable supply base for producers of pipes and tubes used in construction, HVAC, plumbing, and industrial applications. It also helps reduce dependence on imported refined copper, which can lower supply-side risks and support faster capacity planning by manufacturers. This trend is evident from Adani Group starting the first phase of its USD 1.2 billion Mundra copper plant in 2024, adding 0.5 million tons per year of refined copper capacity, with the full project targeted at 1 million tons annually by FY29.

Growing Focus on Copper Recycling and Resource Efficiency

The rising focus on copper recycling and resource efficiency, which helps expand domestic metal availability, is contributing to the market growth. Recycling creates an additional source of copper feedstock and supports long-term supply stability for downstream product makers, including tube manufacturers serving cooling, refrigeration, and industrial systems. This also aligns with the need to reduce reliance on imported raw materials and improve value recovery from scrap. Evidence of this trend can be seen in Hindalco Industries’ 2024 announcement of INR 2,450 Crore investment in Gujarat, including India’s first copper and e-waste recycling plant at Dahej, designed to process 300 to 350 kilotons of scrap annually. The company also planned to expand its copper smelting capacity in Dahej and set up a copper tube manufacturing unit in Vadodara for air-conditioning and refrigeration systems.

Market Outlook 2026-2034:

The India copper pipes and tubes market demonstrates notable growth potential throughout the forecast period, supported by rising construction activity, infrastructure development, and increasing demand from the HVAC and plumbing sectors. Copper pipes are widely used in residential and commercial buildings due to their durability, corrosion resistance, and high thermal conductivity. Expanding urbanization, growth in air conditioning installations, and government investments in housing and smart city projects are further expected to drive steady demand for copper piping systems across India. The market size was estimated at 511.00 Thousand Tons in 2025 and is expected to reach 612.67 Thousand Tons by 2034, reflecting a compound annual growth rate of 2.11% over the forecast period 2026-2034.

India Copper Pipes and Tubes Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Finish Type |

LWC Grooved |

38.5% |

|

Outer Diameter |

3/8, ½, 5/8 Inch |

45.5% |

|

End-User |

HVAC |

41.5% |

|

Region |

West India |

30.5% |

Finish Type Insights:

- LWC Grooved

- Straight Length

- Pancake

- LWC Plain

The LWC grooved exhibits a clear dominance with a 38.5% share of the total India copper pipes and tubes market in 2025.

LWC grooved dominates the market driven by its superior performance in thermal management applications. LWC grooved copper tube contains an internal spiral groove structure that increases the internal surface area available for heat transfer. This design significantly improves thermal exchange efficiency in refrigeration and air conditioning systems. HVAC manufacturers widely prefer LWC grooved tube as it allows better cooling performance while reducing the overall material requirement. Its ability to support compact system designs and maintain stable performance under varying temperature and pressure conditions makes it a standard component in residential and commercial HVAC equipment.

The dominance of LWC grooved tube is closely associated with the rapid growth of India’s air conditioning and refrigeration industry. India’s HVAC market is projected to grow at a CAGR of 14.89% during 2026–2034, according to IMARC Group. This expansion is driving consistent demand from equipment manufacturers that rely on high-efficiency copper tubing for refrigerant circulation. As urban households, offices, and commercial facilities increase adoption of air conditioning systems, OEMs are prioritizing energy-efficient components. LWC grooved tube supports improved system efficiency and compact designs, which makes it the preferred material for modern HVAC equipment, strengthening its leading position in the copper pipes and tubes market.

Outer Diameter Insights:

- 3/8, ½, 5/8 Inch

- 3/4, 7/8, 1 Inch

- Above 1 Inch

The 3/8, ½, 5/8 inch leads with a share of 45.5% of the total India copper pipes and tubes market in 2025.

3/8, ½, and 5/8 inch represents the largest segment because of their extensive use in air conditioning, refrigeration, and residential plumbing systems. These sizes are widely preferred in split air conditioners, refrigerators, and cooling units where compact tubing is required for efficient refrigerant flow. HVAC manufacturers and installers commonly select these diameters as they provide suitable pressure handling, heat transfer efficiency, and easy installation within compact mechanical systems. The rapid expansion of residential housing, commercial buildings, and office spaces across India is increasing installation of air conditioning units, which directly supports rising demand for copper tubes in these specific outer diameter categories.

The growing user demand for cooling appliances and rising adoption of HVAC systems in residential and commercial buildings are strengthening the dominance of these copper tube sizes. Air conditioner manufacturers typically use 3/8 and 5/8 inch copper tubes as standard piping configurations for refrigerant circulation between indoor and outdoor units. These sizes also support efficient thermal conductivity and durability, which are essential for long-term refrigeration performance. Increasing construction of shopping malls, hospitals, hotels, and office complexes is driving higher installation of centralized and split cooling systems. Furthermore, expanding cold storage, food processing, and refrigeration infrastructure across India continues to generate steady demand for these copper pipe diameters.

End-User Insights:

Access the comprehensive market breakdown Request Sample

- HVAC

- Industrial Heat Exchanger

- Plumbing

- Electrical

- Others

HVAC dominates with a share of 41.5% of the total India copper pipes and tubes market in 2025.

HVAC holds the biggest market share owing to the essential role copper plays in refrigeration and heat exchange systems. Copper pipes and tubes are widely used in air conditioners, refrigeration units, and ventilation equipment because of their high thermal conductivity, corrosion resistance, and ability to withstand varying pressure and temperature conditions. These properties enable efficient refrigerant circulation through condenser coils, evaporators, and heat exchangers. HVAC manufacturers also prefer copper for its flexibility and ease of fabrication into complex circuit designs required for modern cooling equipment used in residential, commercial, and industrial installations across India.

The dominance of the HVAC segment is further supported by the rapid expansion of India’s air conditioning market and rising urban housing construction. The PM Awas Yojana Urban 2.0 has committed ₹10 Lakh Crore to address housing needs for 1 crore urban families, according to data released by the government in 2024. This large-scale housing development is expected to generate substantial downstream demand for HVAC systems that utilize copper pipes in their cooling circuits. As newly constructed affordable and mid-income housing units increasingly incorporate air conditioning installations, demand for copper tubes within HVAC applications is projected to expand steadily.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 30.5% share of the total India copper pipes and tubes market in 2025.

West India leads the market due to strong industrial development, rapid urban infrastructure expansion, and high demand from construction and HVAC sectors. Major states, including Maharashtra and Gujarat, host large manufacturing clusters, commercial projects, and residential developments that require copper piping systems for plumbing, refrigeration, and air conditioning applications. The region’s well-established industrial base also supports strong demand from automotive, chemical, and engineering industries where copper tubes are widely used in heat exchangers and cooling systems. In addition, the presence of major ports and logistics networks supports efficient supply of raw materials and distribution of finished copper pipe products.

The growing urbanization and rising investments in real estate and commercial infrastructure across West India are strengthening the demand for copper pipes and tubes used in plumbing and HVAC systems. Large cities continue to witness expansion of residential and institutional buildings requiring durable piping materials. Reflecting this momentum, ANAROCK launched a Project Management & Engineering Services vertical in 2026, managing over 40 million sq. ft. of projects across India with more than 500 professionals. Such organized project development activity supports the adoption of reliable construction materials, reinforcing the demand for copper pipes and tubes in large-scale building infrastructure across the region.

Market Dynamics:

Growth Drivers:

Why is the India Copper Pipes and Tubes Market Growing?

Capacity Addition by Downstream Manufacturers

The India copper pipes and tubes market is driven by capacity addition by downstream manufacturers, as companies expand production to address rising application demand. New tube manufacturing lines help increase domestic output, widen product availability, and support demand from end-use sectors, such as air-conditioning, refrigeration, and engineering. This trend shows that manufacturers are seeing enough market potential to invest in dedicated tube production rather than limiting themselves to other copper product categories. A clear example is Ram Ratna Wires approving INR 200 Crore investment in 2024 to expand its Bhiwadi plant with a new copper tube manufacturing line focused on DHP copper tubes and related products, with production expected from Q2 FY2024-25.

Shift Toward Quality, Safety, and Lifecycle Efficiency

A growing emphasis on product quality, installation safety, and lifecycle cost efficiency is shaping purchasing decisions in favor of copper pipes and tubes. Buyers are increasingly evaluating materials not only on initial cost but also on durability, maintenance needs, resistance to failure, and long-term operational performance. Copper performs well in environments where product integrity and consistent service life are essential. This makes it attractive for projects that seek to reduce repair frequency and improve system dependability over time. As consultants, builders, and facility operators adopt more performance-driven procurement standards, the market is seeing stronger acceptance of copper-based piping and tubing solutions.

Industrial Growth and Process Infrastructure Development

Industrial expansion across manufacturing, engineering, chemicals, and process industries is supporting the use of copper pipes and tubes in fluid transfer, heat exchange, and equipment systems. Copper products are favored where precision, conductivity, strength, and dependable performance under demanding operating conditions are required. New plant installations, modernization of existing facilities, and capacity expansion programs are increasing the need for efficient tubing solutions in industrial infrastructure. Demand is also linked to machinery, fabricated systems, and thermal management applications where copper offers technical advantages. As industrial activity becomes more sophisticated and quality standards become stricter, the market for copper pipes and tubes is gaining a stronger base.

Market Restraints:

What Challenges the India Copper Pipes and Tubes Market is Facing?

Volatility in Global Copper Prices Impacting Production Costs

International copper prices are subject to significant fluctuations driven by geopolitical tensions, supply chain disruptions, and demand dynamics from major consuming economies, such as China. For Indian copper pipe and tube manufacturers, raw material price swings create margin pressure and complicate long-term procurement planning. Elevated copper prices directly inflate production costs and can dampen end-user demand, particularly in cost-sensitive plumbing and construction segments where buyers may defer purchases during extended price upswings.

Competition from Alternative Piping Materials in Price-Sensitive Segments

Copper pipes and tubes face higher competition from CPVC, PVC, and cross-linked polyethylene alternatives in plumbing and certain industrial applications. These synthetic materials offer lower upfront material costs and are easier to handle during installation. As price-sensitive contractors and developers increasingly evaluate total system cost, substitution risk from polymer-based piping becomes more pronounced, particularly in affordable housing and low-budget commercial construction segments where copper’s premium pricing is less easily accommodated.

Structural Import Dependency for Copper Concentrates

India currently relies heavily on imported copper concentrates, with domestic ore reserves meeting only a fraction of refinery requirements. This structural import dependency exposes the market to currency fluctuation risks and global supply chain disruptions. Periods of elevated import costs or constrained concentrate availability can limit domestic smelter output, reduce the availability of competitively priced refined copper cathodes, and ultimately narrow margins for downstream copper pipe and tube manufacturers across the value chain.

Competitive Landscape:

The India copper pipes and tubes market features a moderately concentrated competitive structure, with a handful of integrated metals conglomerates anchoring supply at scale while a broader base of regional manufacturers caters to specific application segments and geographic markets. Market participants are increasingly differentiating on product precision, energy efficiency, and compliance with international refrigeration standards, particularly in the HVAC segment that demands consistently high-quality inner-grooved tubes. Domestic raw material security is becoming a key competitive variable, with vertically integrated players enjoying cost and supply advantages as India’s copper smelting capacity expands. The competitive intensity is expected to increase over the forecast period as new entrants commission copper tube manufacturing capacity and partnerships between domestic smelters and international tube manufacturers reshape the supply chain. Players are also expanding geographic distribution networks to capture demand from Tier-II and Tier-III cities.

Recent Developments:

- October 2025: BIS Chennai organized a “Manak Manthan” stakeholder discussion on the draft revised Indian standard for wrought copper tubes used in refrigeration and air-conditioning. The session brought together manufacturers, industry bodies, labs, and academia to review proposed changes to IS 10773 and gather industry feedback on quality, safety, energy efficiency, and sustainability. The initiative was aimed at making Indian standards more relevant to industry needs while supporting reliable, efficient, and globally competitive copper tube manufacturing.

- July 2025: Adani Enterprises partnered with MetTube to build its copper tubes business through a 50:50 ownership structure across Kutch Copper Tubes Ltd. and MetTube Copper India Pvt. Ltd. The tie-up aimed to boost domestic copper tube manufacturing for HVAC, refrigeration, plumbing, and other fast-growing sectors, while cutting India’s reliance on imports. The partnership combined Adani’s copper infrastructure in Mundra with MetTube’s global manufacturing expertise to support local production, energy efficiency, and green infrastructure growth.

India Copper Pipes and Tubes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Finish Types Covered | LWC Grooved, Straight Length, Pancake, LWC Plain |

| Outer Diameters Covered | 3/8, 1/2, 5/8 Inch, 3/4, 7/8, 1 Inch, Above 1 Inch |

| End-Users Covered | HVAC, Industrial Heat Exchanger, Plumbing, Electrical, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Copper Pipes and Tubes Market Report

The India copper pipes and tubes market reached a volume of 511.00 Thousand Tons in 2025.

The India copper pipes and tubes market is expected to grow at a compound annual growth rate of 2.11% during 2026-2034 to reach 612.67 Thousand Tons by 2034.

LWC grooved holds the largest share of 38.5% in 2025, driven by its superior thermal transfer efficiency and widespread adoption in HVAC and refrigeration systems as the preferred inner-grooved tube format for air conditioning OEMs.

Key factors driving the India copper pipes and tubes market include the expanding residential and commercial construction, which increases the demand for durable plumbing and water distribution materials. Reflecting this trend, Shapoorji Pallonji Real Estate launched the VANAHA Verdant residential project in Pune in 2025, covering nearly 10 lakh sq. ft. of saleable area.

Major challenges include volatility in global copper prices affecting raw material costs, competition from alternative piping materials, such as CPVC and cross-linked polyethylene, in price-sensitive segments, and structural import dependency for copper concentrates exposing the market to supply chain and currency risks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)