India Cosmetics Market Size, Share, Trends and Forecast by Product Type, Category, Gender, Distribution Channel, and Region, 2026-2034

India Cosmetics Market Size, Share, Trends & Forecast (2026-2034)

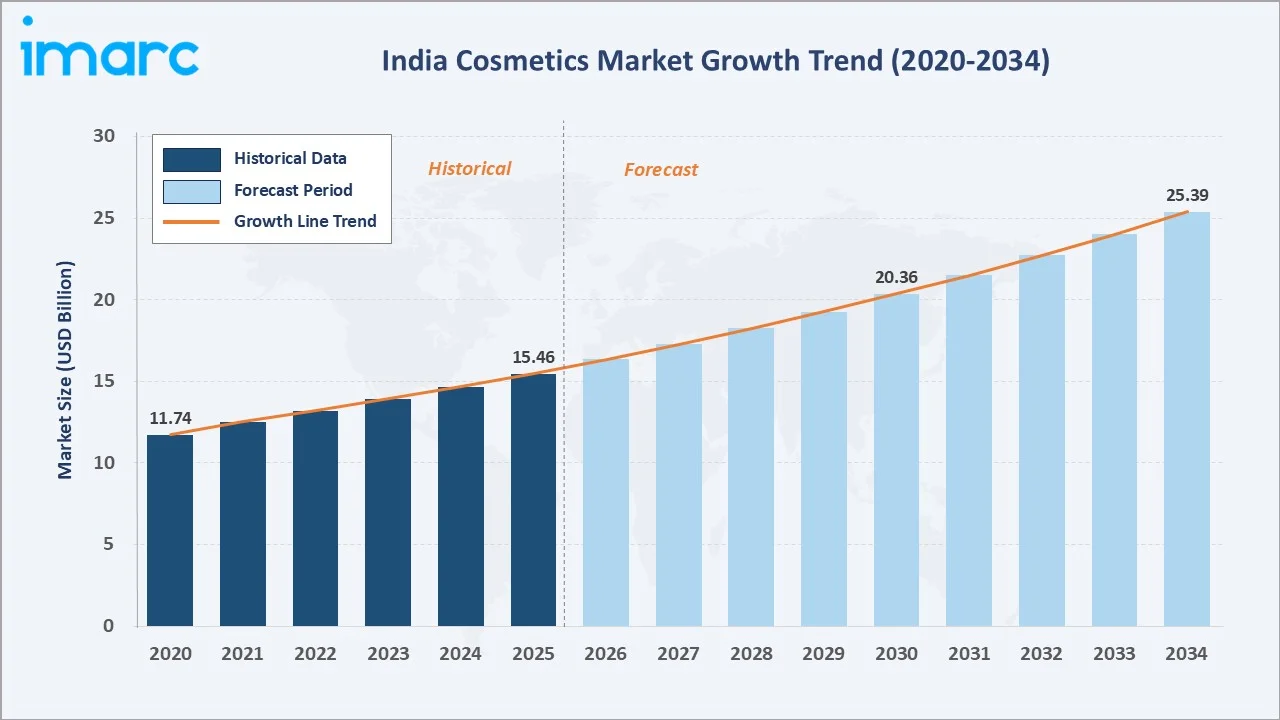

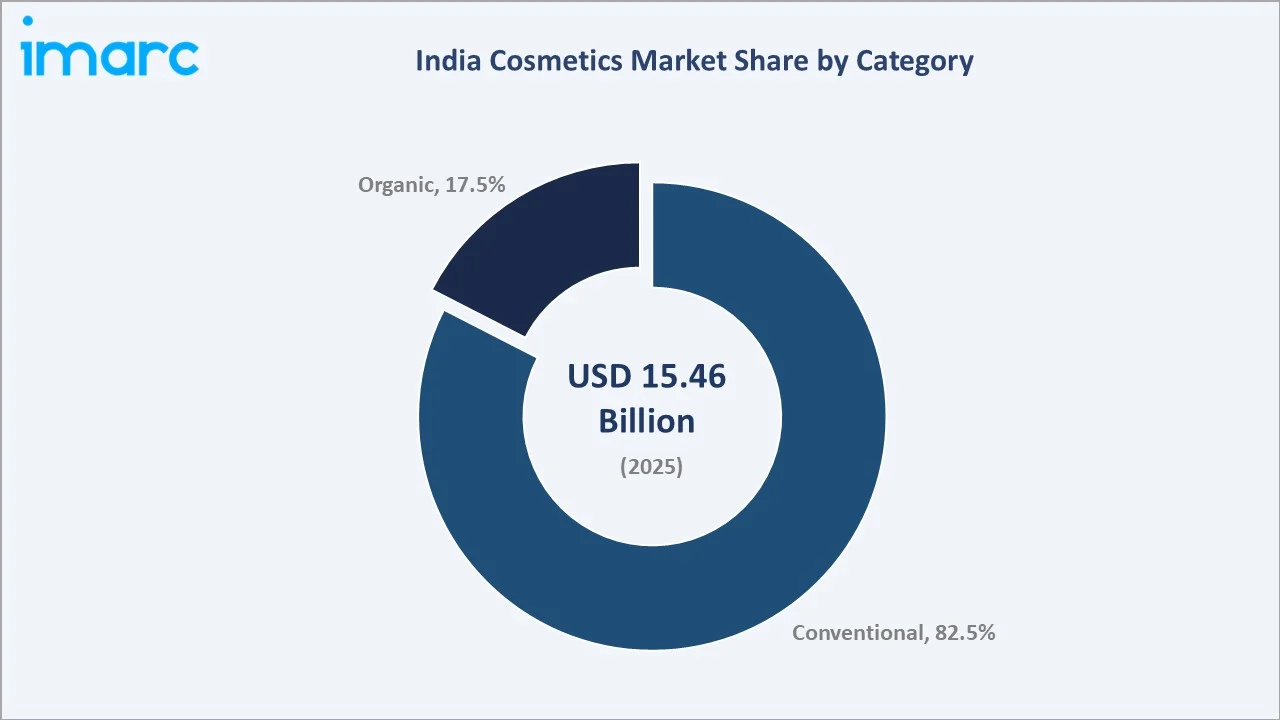

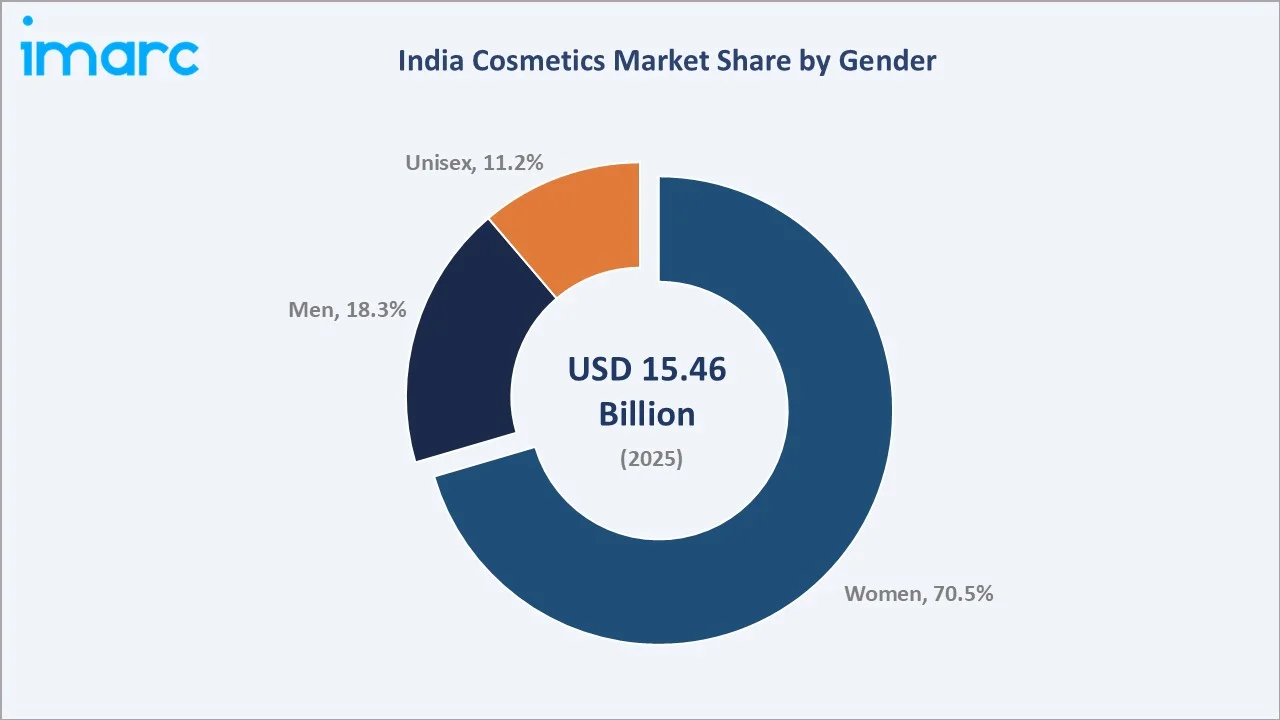

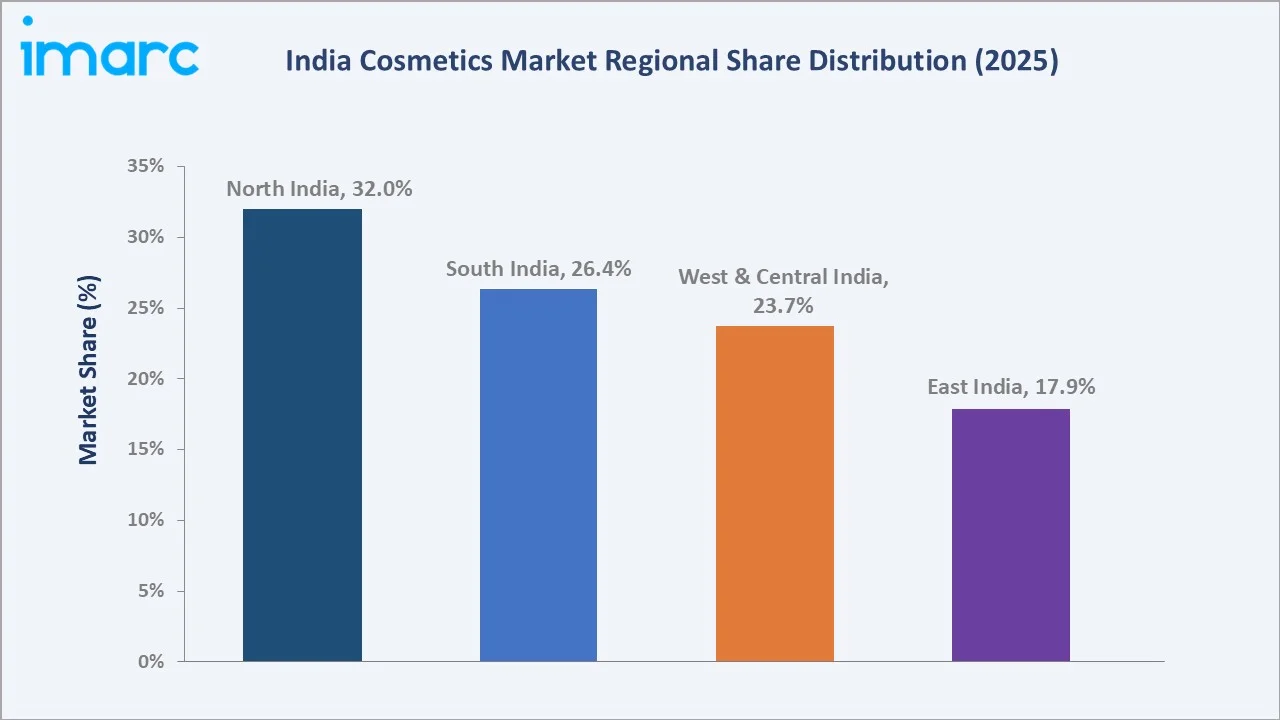

India cosmetics market size was valued at USD 15.46 Billion in 2025 and is projected to reach USD 25.39 Billion by 2034, exhibiting a CAGR of 5.66% during the forecast period 2026-2034. Rising disposable incomes, rapid urbanization, and growing beauty awareness among consumers across demographic segments are driving the India cosmetics market growth. Conventional products lead the category segment at 82.54% in 2025, while women dominate the gender segment at 70.46%. North India accounts for 32% of market revenue in 2025, the largest regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.46 Billion |

|

Forecast Market Size (2034) |

USD 25.39 Billion |

|

CAGR (2026-2034) |

5.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (32% share, 2025) |

|

Fastest Growing Region |

East India |

|

Leading Category |

Conventional (82.54%, 2025) |

|

Leading Gender Segment |

Women (70.46%, 2025) |

The India cosmetics market growth trajectory from 2020 through 2034 highlights a steady historical expansion base against a sustained forecast growth curve, powered by premiumization, e-commerce penetration, and expanding male grooming adoption.

To get more information on this market, Request Sample

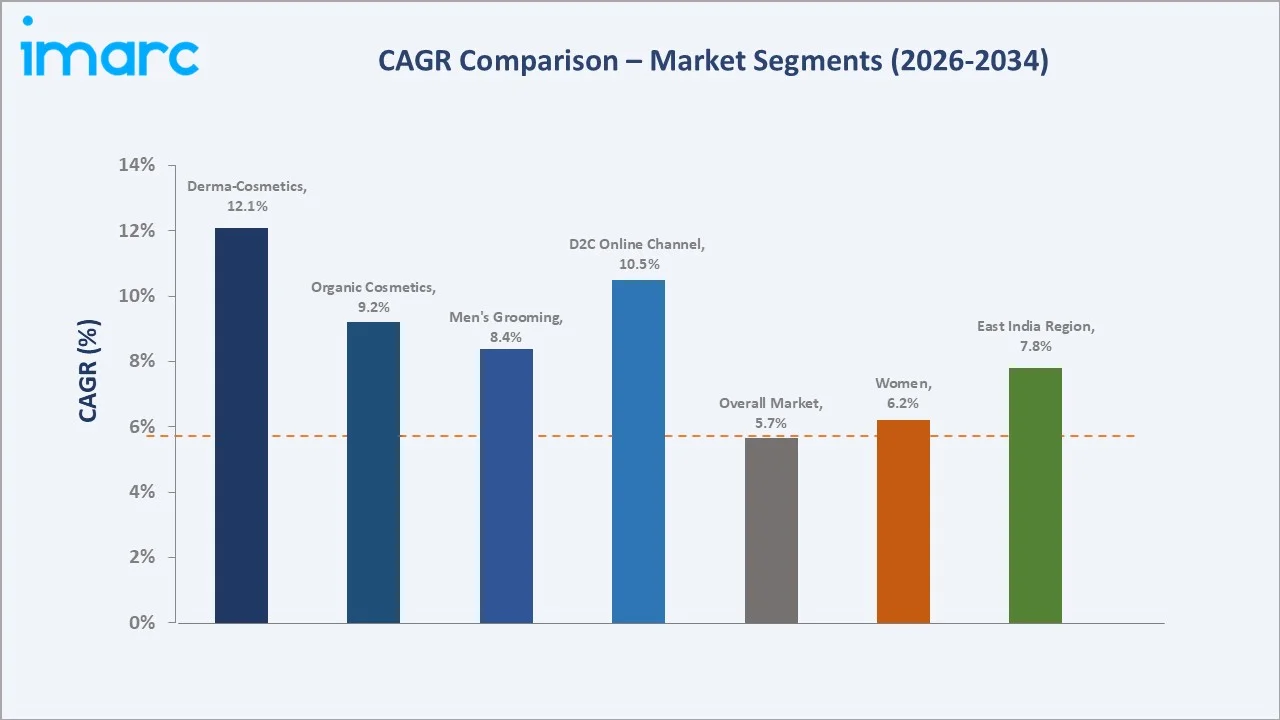

Segment-level CAGR comparisons highlighting organic cosmetics and men’s grooming as the two fastest-growing sub-categories within the India cosmetics market through 2034.

Executive Summary

India cosmetics market is undergoing a structural transformation fueled by demographic shifts, digital commerce proliferation, and evolving consumer attitudes toward personal care and grooming. Valued at USD 15.46 Billion in 2025, the market is projected to reach USD 25.39 Billion by 2034 at a CAGR of 5.66%.

Conventional cosmetics maintain market leadership with an 82.54% share in 2025, supported by a wide distribution reach and price accessibility across 9 million+ retail outlets. However, the organic segment at 17.46% is growing at an estimated 9.2% CAGR, approximately 1.6 times the overall market rate, propelled by consumer concerns around synthetic ingredient safety and rising interest in Ayurvedic and plant-based formulations. Female consumers contribute 70.46% of market revenue in 2025, while the men’s segment at 18.32% is the fastest-growing gender category, reflecting changing grooming norms among younger male demographics.

North India leads regional consumption at 32% in 2025, anchored by high urban density in Delhi NCR, Lucknow, and Chandigarh. Companies including Unilever, L’Oréal SA, Procter & Gamble, Emami Ltd., and Marico are intensifying their competitive presence through product innovation, premiumization, and digital-first strategies. The market outlook through 2034 is robust, reinforced by India’s position as one of the world’s top five fastest-growing beauty economies.

Key Market Insights

|

Insight |

Data |

|

Largest Category |

Conventional – 82.54% share (2025) |

|

Fastest Growing Category |

Organic – 17.46% share (2025); ~9.2% CAGR through 2034 |

|

Leading Gender Segment |

Women – 70.46% revenue share (2025) |

|

Fastest Growing Gender |

Men – 18.32% share (2025); ~8.4% CAGR through 2034 |

|

Leading Region |

North India – 32% revenue share (2025) |

|

Top Companies |

Unilever, L’Oréal SA, Procter & Gamble, Emami Ltd., Marico |

Key Analytical Observations Supporting the Above Data:

- Conventional cosmetics command 82.54% of the India market in 2025, driven by affordability, mass retail availability, and established brand familiarity across rural and semi-urban India, where over 60% of the population resides.

- The organic segment’s 17.46% share in 2025 understates its growth momentum; consumer searches for “paraben-free” and “natural” beauty products on e-commerce platforms.

- Women’s segment dominance at 70.46% is sustained by rising economic participation, with female workforce participation in urban India reaching 33% in 2024, significantly increasing beauty spending power.

- Men’s grooming at 18.32% is undergoing rapid formalization; brands such as Beardo, The Man Company, and Ustraa, alongside extensions from Garnier Men and Nivea Men, are expanding category penetration.

- North India’s 32% regional share reflects Metro and Tier-1 city infrastructure in the Delhi NCR belt, Uttar Pradesh, and Punjab, where modern trade and quick-commerce platforms are accelerating product accessibility.

- E-commerce now accounts for over 22% of total cosmetics sales in India in 2025, with platforms like Nykaa, Myntra Beauty, Amazon India, and Flipkart driving premiumization through curated brand stores.

India Cosmetics Market Overview

The India cosmetics market covers skin and sun care, hair care, color cosmetics, fragrances, deodorants, and oral care, spanning both mass and premium segments with participation from multinational FMCG players and domestic Ayurvedic brands.

The ecosystem is supported by a vast FMCG retail network of over 9 million outlets and rapidly expanding e-commerce channels. India’s strong demographic base—over 1.4 billion people with a median age of ~28—drives sustained demand for beauty and personal care products. Overall, growth is driven by favorable demographics, rising incomes, expanding retail access, and increasing preference for natural and Ayurvedic formulations.

Market Dynamics

To evaluate market opportunities, Request Sample

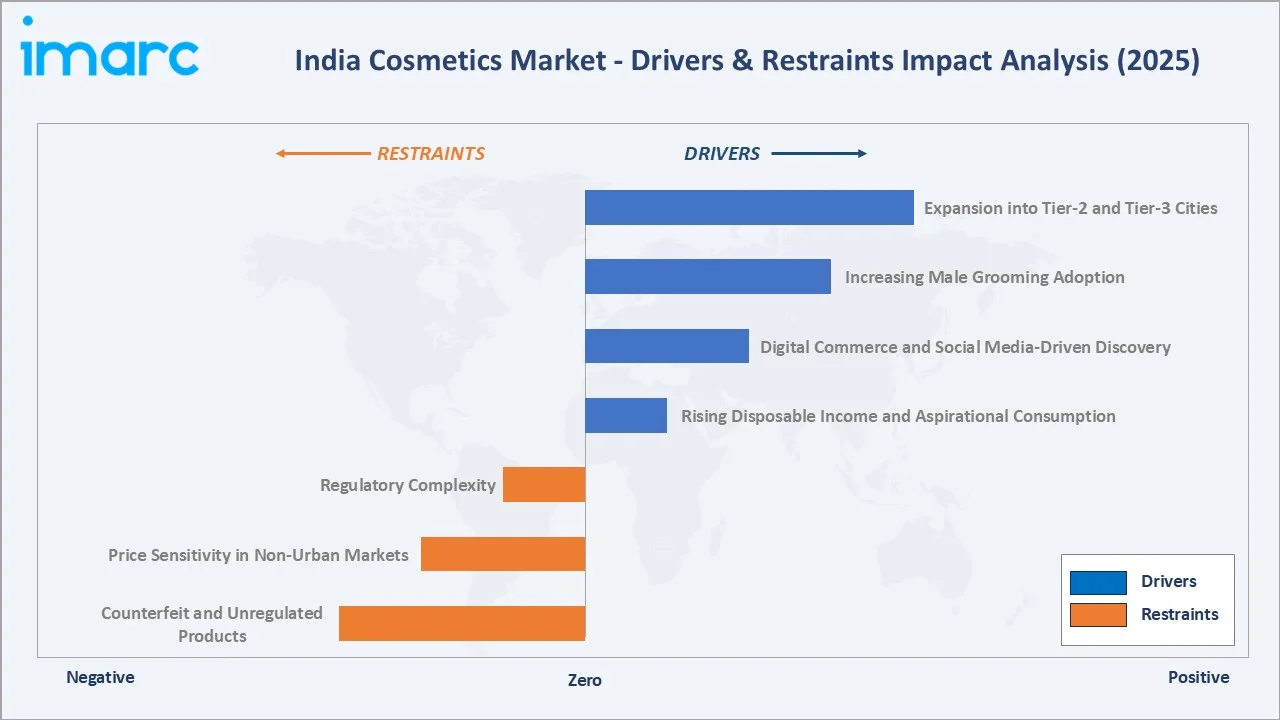

Market Drivers

- Rising Disposable Income and Aspirational Consumption: India’s per capita income grew to approximately USD 2,485 in 2024, with urban households allocating a growing share of discretionary spending to personal care. Beauty and grooming now rank among the top five consumer expenditure categories in urban India.

- Digital Commerce and Social Media-Driven Discovery: India has over 950 million internet users as of 2025. Beauty content accounts for approximately 18% of total social media engagement on Instagram and YouTube India. D2C brands leveraging influencer marketing achieve lower customer acquisition costs than traditional retail channels.

- Increasing Male Grooming Adoption: The male grooming segment grew at approximately 9.8% annually in 2023-2024. Products including face wash, moisturizers, beard care, and anti-dandruff solutions are driving incremental category volumes, with dedicated men’s brands proliferating rapidly.

- Expansion into Tier-2 and Tier-3 Cities: Organized beauty retail, including Nykaa stores, Reliance Trends beauty sections, and pharmacy-format beauty chains, is penetrating cities such as Kanpur, Coimbatore, Surat, and Bhopal, unlocking previously unaddressed consumer bases.

Market Restraints

- Counterfeit and Unregulated Products: The India cosmetics market faces a significant counterfeit challenge, with low-cost imitations sold through informal trade channels, suppressing premium brand revenues and raising consumer safety concerns.

- Price Sensitivity in Non-Urban Markets: Rural and semi-urban consumers remain highly price-sensitive, limiting premiumization penetration to urban-centric demographics and constraining average selling price expansion across the broader market.

- Regulatory Complexity: Divergent state-level interpretations of BIS and CDSCO guidelines create compliance inconsistencies, particularly for imported cosmetic formulations entering the Indian market.

Market Opportunities

- Ayurvedic and Organic Premiumization: The Ayurvedic cosmetics sub-segment, led by Forest Essentials, Kama Ayurveda, and Biotique. Organic formulations command 40-60% premium pricing above conventional equivalents.

- Men’s Grooming White Space: Penetration of specialized men’s skincare beyond shaving remains below 25% in Tier-2 markets, representing an underpenetrated USD 500-700 Million addressable opportunity by 2030.

- Personalization and Skin-Tech: AI-powered skin analysis tools deployed by L’Oreal (ModiFace), Nykaa, and mCaffeine are enabling personalized product recommendations, increasing basket size by 30-40% per consumer engagement.

Market Challenges

- Supply Chain and Raw Material Volatility: Rising crude oil prices affect petroleum-derived cosmetic ingredients, while supply disruptions in botanical raw materials impact natural cosmetics and manufacturers. Fragrance ingredient costs increased approximately 12-15% in 2023-2024.

- Intense Brand Fragmentation: The India cosmetics market hosts over 800 active brands, creating significant brand recall challenges and increasing marketing spend requirements for emerging players.

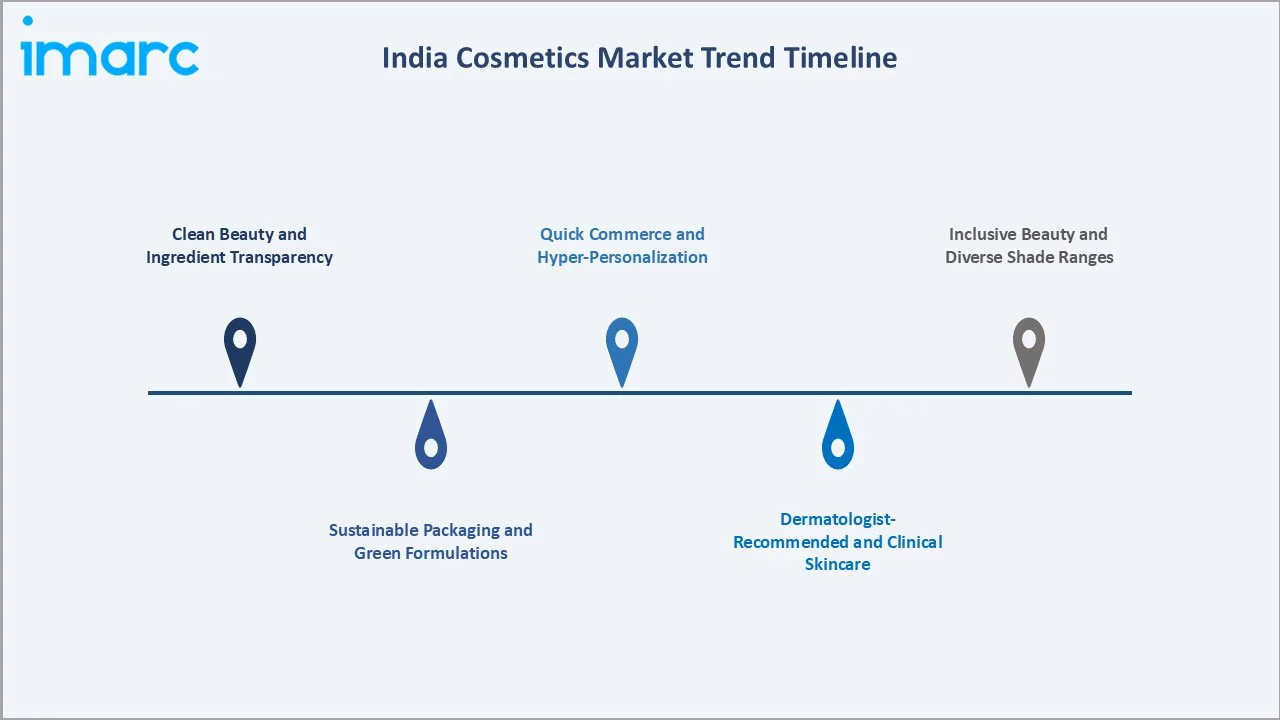

Emerging Market Trends

1. Clean Beauty and Ingredient Transparency

Consumer demand for transparent ingredient labeling and cruelty-free formulations is reshaping product development. Over 68% of urban female consumers reviewed ingredient lists before purchasing skincare in 2024. Brands are reformulating to eliminate parabens, sulfates, and microplastics, with clean beauty a defining premium differentiator.

2. Quick Commerce and Hyper-Personalization

10-minute delivery platforms, including Blinkit, Zepto, and Swiggy Instamart, are transforming beauty retail. Cosmetics now account for approximately 8-10% of quick commerce GMV in major metro cities, making same-day beauty delivery a baseline consumer expectation.

3. Inclusive Beauty and Diverse Shade Ranges

The inclusive beauty movement is influencing Indian market offerings. Domestic brands, including Sugar Cosmetics and Nykaa’s Kay Beauty, have launched foundation ranges with 20-40 shades, addressing India’s diverse skin tone spectrum and capturing previously underserved consumer segments.

4. Sustainable Packaging and Green Formulations

Regulatory and consumer pressure are driving the transition toward recyclable, refillable, and biodegradable packaging. Hindustan Unilever is committed to 100% recyclable plastic packaging for its beauty portfolio by 2025-2026. Refillable fragrance formats are gaining traction in the premium segment.

5. Dermatologist-Recommended and Clinical Skincare

The derma-cosmetics sub-segment is growing at an estimated 11-13% CAGR. Brands including Minimalist, Dot and Key, and dermatologist-backed platforms are positioning evidence-based formulations as superior alternatives, with clinical validation becoming a core marketing claim.

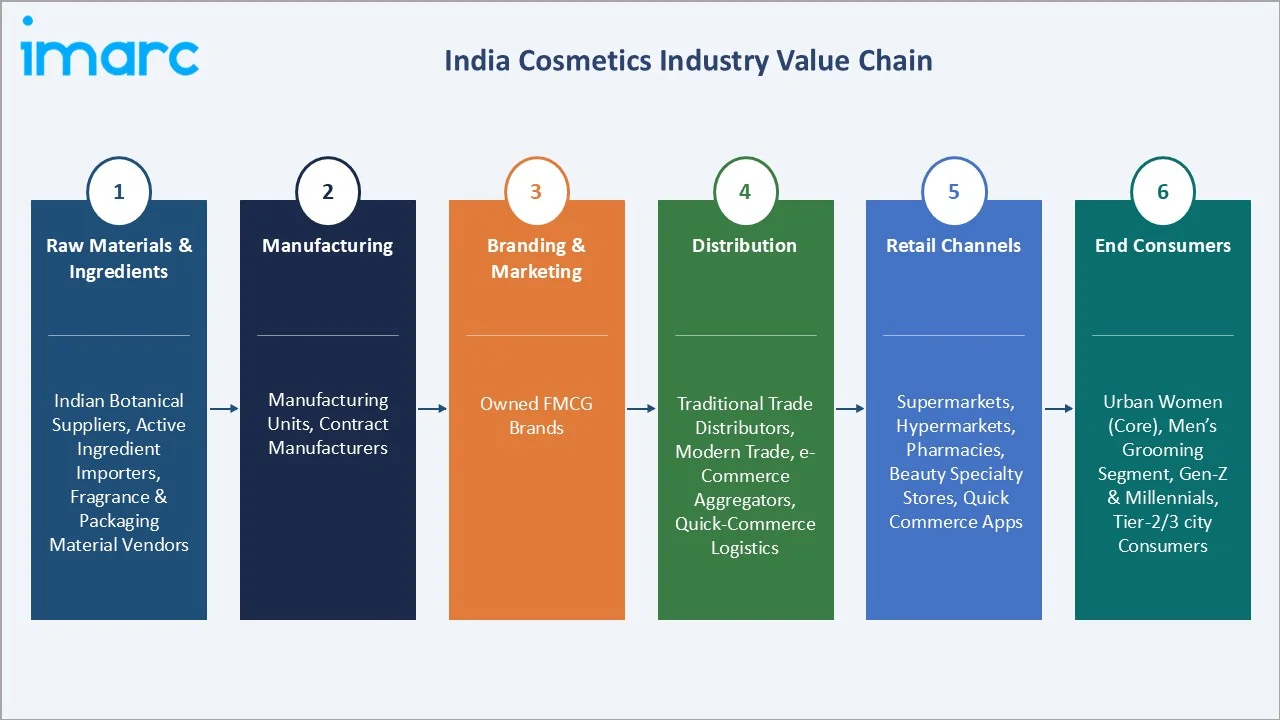

Industry Value Chain Analysis

The India cosmetics value chain spans six integrated stages from raw material sourcing through consumer point-of-purchase. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Activities |

|

Raw Materials & Ingredients |

Indian botanical suppliers |

|

Manufacturing |

HUL manufacturing units, Marico plants, contract manufacturers |

|

Branding & Marketing |

Owned brands, D2C brands |

|

Distribution |

Traditional trade distributors, modern trade, e-commerce |

|

Retail Channels |

Supermarkets/hypermarkets, pharmacies, beauty specialty stores, and quick commerce apps |

|

End Consumers |

Urban women (core), men’s grooming segment, Gen-Z and millennial demographics, Tier-2/3 city consumers |

Brand owners and FMCG manufacturers occupy the highest strategic value position in the India cosmetics value chain, integrating raw material sourcing, formulation innovation, and multi-channel distribution. However, this position is being challenged by D2C brands that bypass traditional distribution to reach consumers directly through digital channels.

Technology Landscape in the India Cosmetics Industry

Digital Commerce and AI-Powered Personalization

Technology is fundamentally reshaping how cosmetics are discovered, evaluated, and purchased in India. Nykaa’s AI-powered recommendation engine analyzes over 200 skin parameters to suggest personalized product regimens, driving a reported 35% increase in average order value. L’Oreal’s ModiFace AR try-on tool enables consumers to virtually test makeup shades before purchase, reducing product return rates.

Formulation Technology: Biotechnology and Active Ingredients

Cosmetic formulation technology is advancing rapidly in India, with biotech-derived active ingredients including hyaluronic acid, niacinamide, retinol, and peptides entering mass market price tiers. The Minimalist brand pioneered transparent high-concentration active ingredient formulations at accessible price points, triggering broad industry reformulation.

Sustainable and Green Chemistry Technologies

Green chemistry and sustainable ingredient sourcing are transitioning from a premium niche to a mainstream industry requirement. Waterless formulations, solid beauty bars, and concentrated refill formats are reducing packaging waste and logistics costs simultaneously. Patanjali Ayurved’s investment in standardized Ayurvedic extraction technology represents India’s contribution to global green cosmetics innovation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Skin and Sun Care Products |

43.73% |

2025 |

|

Category |

Conventional |

82.54% |

2025 |

|

Gender |

Women |

70.46% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

60.51% |

2025 |

|

Region |

North India |

32% |

2025 |

By Category

Conventional cosmetics command an 82.54% majority share in 2025, reflecting the market’s established reliance on widely available, affordably priced formulations distributed through mass retail channels. The conventional segment benefits from decades of brand equity investment by FMCG leaders, including Hindustan Unilever and Procter & Gamble, and from price positioning accessible to India’s broad consumer base.

To access detailed market analysis, Request Sample

Organic cosmetics at 17.46% in 2025 are growing at an estimated 9.2% CAGR through 2034. Consumer searches for “paraben-free” and “natural” beauty products on Indian e-commerce platforms increased over 45% year-on-year in 2024. Brands including Forest Essentials, Kama Ayurveda, Biotique, and The Body Shop India lead organic premiumization.

By Gender

Women command a 70.46% share in 2025, driven by deep-rooted beauty culture and expanding beauty consciousness across age groups. The female consumer base spans a broad portfolio from daily-use moisturizers and hair care to premium color cosmetics and anti-aging serums. Rising economic empowerment, with female workforce participation in urban India reaching 33% in 2024, is significantly expanding women’s beauty spending power.

Men at 18.32% represent the most dynamic growth opportunity in the India cosmetics market, with an estimated 8.4% CAGR through 2034. Indian men spent an estimated USD 1.1 Billion on personal care products in 2024, a figure projected to reach USD 2.3 Billion by 2030. Brands including Beardo, The Man Company, Ustraa, Garnier Men, and Nivea Men are driving category expansion. Unisex at 11.22% is expanding as brands such as Dove and Plum position products as gender-inclusive offerings.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Notable Markets |

|

North India |

32.0% |

High urban density, elevated disposable incomes, strong, organized, and quick-commerce retail |

Delhi NCR, Lucknow, Chandigarh, Jaipur |

|

South India |

26.4% |

Tech-hub workforce, premium beauty adoption, strong IT-sector income concentration |

Bengaluru, Hyderabad, Chennai, Kochi |

|

West & Central India |

23.7% |

Mumbai-led premium market, Tier-2 expansion, strong FMCG distribution infrastructure |

Mumbai, Pune, Ahmedabad, Nagpur |

|

East India |

17.9% |

Emerging market growth, increasing organized retail, and growing e-commerce penetration |

Kolkata, Bhubaneswar, Guwahati, Patna |

North India leads with a 32% revenue share in 2025. The region’s dominance reflects the highest urban density within India’s cosmetics-consuming demographics, concentrated in the Delhi NCR belt and surrounding major cities. Rapid quick-commerce penetration, with Blinkit and Zepto achieving 20-minute delivery across 50+ cities, is accelerating purchase frequency. Premium.

South India commands a 26.4% share, driven by tech-hub cities with high disposable income populations. Bengaluru and Hyderabad’s large IT workforce represents a premium beauty consumer base with strong online purchasing behavior. South Indian consumers demonstrate above-average affinity for skincare and herbal product categories, aligned with regional Ayurvedic traditions and cultural emphasis on personal care.

West and Central India account for 23.7%, led by Mumbai, which serves as India’s fashion and beauty capital and the headquarters of most major FMCG companies. East India at 17.9% is the fastest-developing regional market, with e-commerce growth in Odisha, Bihar, and Jharkhand unlocking previously inaccessible consumer bases, where beauty and personal care rank among the top three purchase categories.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Unilever |

Lakme, Pond’s |

Leader |

Distribution depth, portfolio breadth, rural reach |

|

L’Oréal SA |

Garnier, Maybelline |

Leader |

Premium positioning, R&D, multi-segment coverage |

|

Procter & Gamble |

Olay |

Leader |

Brand equity, consumer research, and modern trade leadership |

|

Emami Ltd. |

BoroPlus, Smart & Handsome |

Leader |

Ayurvedic heritage, rural penetration, mass market |

|

Marico |

Just Herbs, plix, kaya |

Challenger |

Hair care dominance, strong innovation pipeline |

|

FSN E-Commerce (Nykaa) |

Nykaa Cosmetics |

Challenger |

Digital-first, curated brand ecosystem, beauty retail |

|

Lotus Herbals Pvt. Ltd. |

Lotus Herbals, Lotus Make-up |

Emerging |

Herbal expertise, mid-premium positioning, SPF leadership |

The India cosmetics competitive landscape is highly fragmented, combining global FMCG leaders with strong domestic challengers and emerging D2C disruptors. Hindustan Unilever commands the broadest portfolio reach through iconic brands spanning skincare, hair care, and personal care. International players, including L’Oreal India and P&G India, are investing heavily in premiumization and R&D to capture the growing aspirational middle-class consumer segment.

Key Company Profiles

Unilever

Unilever is India’s FMCG company and the undisputed leader in the India cosmetics market. Its beauty and personal care division commands a portfolio spanning mass to premium tiers across skincare, hair care, and color cosmetics.

- Product Portfolio: Lakme (color cosmetics, skincare), Dove (personal care), Pond’s (skincare), TRESEMME (professional hair care), Vaseline (skincare), Indulekha (Ayurvedic hair care).

- Recent Developments: In June 2024, Unilever launched new tools that use AI capabilities to help consumers make personalised product choices.

- Strategic Focus: HUL is pursuing a premiumization strategy through the Lakme and Indulekha brands while maintaining mass market volume leadership with Dove and Pond’s. The company’s 3.5 million-outlet direct distribution network provides unmatched rural reach for new product launches.

L’Oréal SA

L’Oreal is the premium beauty market leader and India’s fastest-growing major cosmetics multinational. It operates across professional, consumer, and luxury beauty divisions with a strong focus on digital innovation and localized formulation development.

- Product Portfolio: L’Oreal Paris (hair color, skincare, cosmetics), Garnier (skin and hair care), Maybelline New York (color cosmetics), Kerastase (professional hair care), Giorgio Armani Beauty (luxury).

- Recent Developments: In February 2026, Nykaa signed an exclusive distribution agreement with L’Oréal India to manage all operations of luxury skincare brand Kiehl’s in India.

- Strategic Focus: L’Oreal India’s strategy centers on digital-first engagement through ModiFace AR try-on technology, e-commerce platform expansion, and localization of formulations for Indian skin types. The company targets doubling its India revenue by 2030.

Emami Ltd.

Emami is a leading Indian consumer goods company with a strong Ayurvedic and herbal heritage. Its cosmetics portfolio spans skincare, hair care, and men’s grooming with particularly strong rural distribution and mass market positioning.

- Product Portfolio: BoroPlus (antiseptic cream, skincare), Smart & Handsome (men’s skincare), Navratna (hair oil, cool talc), Zandu (Ayurvedic personal care), Kesh King (hair care).

- Recent Developments: In January 2025, Emami rebranded Fair & Handsome to ‘Smart & Handsome’, aligning the men’s grooming brand with evolved consumer sensibilities. The company expanded its international footprint across SAARC and African markets.

- Strategic Focus: Emami’s strategy focuses on Ayurvedic brand differentiation, rural market penetration through its 3 million+ distributor network, and men’s grooming category expansion. The company is investing in premium formulation upgrades for urban consumers.

Market Concentration Analysis

The India cosmetics market exhibits moderate concentration at the national level. The top five players, including Unilever, L’Oréal SA, Procter & Gamble, Emami Ltd., and Marico, collectively account for an estimated 38-44% of organized market revenue in 2025. However, the broader market remains fragmented with over 800 active brands competing across sub-categories.

A structural fragmentation dynamic is driven by the rapid proliferation of D2C brands since 2019-2020. Brands such as Minimalist, Dot and Key, mCaffeine, and SUGAR Cosmetics have each achieved strong revenue in annual revenue within 3-5 years of launch, demonstrating that the India cosmetics market remains highly accessible to new entrants with differentiated positioning.

Consolidation is emerging in the color cosmetics and men’s grooming sub-segments. Nykaa’s acquisition of the Dot & Key brand and Marico’s acquisition of Beardo represent the growing consolidation trend among D2C brand leaders, signaling the maturing of India’s direct-to-consumer cosmetics ecosystem.

Investment & Growth Opportunities

Fastest-Growing Segments

Organic and clean beauty is the highest-growth category at an estimated 9.2% CAGR through 2034. Brands with certified natural ingredient claims and cruelty-free positioning command premium pricing 40-60% above conventional equivalents. The men’s grooming segment at approximately 8.4% projected CAGR represents significant white space, particularly in face care, body care, and hair styling for male consumers in Tier-2 markets.

Emerging Market Expansion

Tier-2 and Tier-3 city beauty market expansion represents the largest volume growth opportunity through 2034. An estimated 280 million new beauty consumers in non-metro India are becoming accessible through expanding organized retail and e-commerce logistics. Derma-cosmetics and cosmeceuticals, growing at 11-13% CAGR, represent a premium segment with high margins and strong consumer loyalty driven by dermatologist recommendations.

Venture & Private Investment Trends

Venture and private equity investment in India's beauty and personal care D2C brands is expanding. Notable transactions include investments in Minimalist, mCaffeine, and Plum Goodness. Nykaa’s continued expansion and international strategic investors, including L’Oreal and Estee Lauder, are deepening India investments through joint ventures and acquisitions.

Future Market Outlook (2026-2034)

The India cosmetics market is projected to grow from USD 15.46 Billion in 2025 to USD 25.39 Billion by 2034 at a CAGR of 5.66%, representing a near-doubling of market value over nine years. This sustained growth trajectory is underpinned by favorable demographic trends, increasing beauty consciousness among younger consumer cohorts, and the structural shift of beauty spending from discretionary to essential expenditure across middle-class India.

Three transformative forces are expected to reshape the market structure through 2034. First, digital commerce will account for an estimated 35-40% of total cosmetics revenue by 2034, reshaping brand economics and reducing distribution barriers for new entrants. Second, the premiumization of the women’s segment and formalization of men’s grooming will sustain above-average growth in the USD 500+ price tier. Third, India’s Ayurvedic heritage is expected to gain international traction, positioning India as a net cosmetics exporter to Southeast Asia and the GCC markets by 2028-2030.

By 2034, the India cosmetics industry is forecast to have completed its transition from a distribution-led market dominated by FMCG giants to a diversified ecosystem where D2C brands, beauty tech platforms, and premium Ayurvedic labels each hold significant market share. The competitive landscape will be shaped by HUL’s multi-brand distribution empire, Nykaa’s digital beauty ecosystem, and international premium brands driving aspirational consumption among India’s rapidly expanding affluent consumer class.

Research Methodology

Primary Research

Primary research included over 50 structured interviews conducted during 2024-2025 with beauty industry stakeholders, including category managers at leading FMCG companies, independent pharmacists and beauty retail owners, female and male consumers across 8 Indian cities spanning all four regions, D2C brand founders, and institutional investors in India consumer brands. Primary insights validated market sizing, segmentation estimates, and regional consumption patterns.

Secondary Research

Secondary sources include Nielsen India FMCG retail audit data, Euromonitor International India Beauty and Personal Care report (2024), IBEF India Beauty and Wellness sector report, Ministry of MSME cosmetics and personal care industry data, FSSAI regulatory publications, company annual reports, and trade publications including Cosmetics Business, Personal Care Magazine, and Beauty Launchpad India.

Forecasting Models

Market size estimations used a combination of top-down and bottom-up methodologies, incorporating India’s GDP growth rate projections, urban household income growth, and per capita beauty spending benchmarks against comparable emerging markets, including Brazil, China, and Indonesia. Scenario analysis was performed for base, optimistic, and conservative forecast cases to account for macroeconomic uncertainty.

India Cosmetics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Skin and Sun Care Products, Hair Care Products, Deodorants and Fragrances, Makeup and Color Cosmetics, Others |

| Categories Covered | Conventional, Organic |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Pharmacies, Online Stores, Others |

| Regions Covered | South India, North India, West and Central India, East India |

| Companies Covered | Unilever, L’Oréal SA, Procter & Gamble, Emami Ltd., Marico, FSN E-Commerce (Nykaa), Lotus Herbals Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email |

Frequently Asked Questions About the India Cosmetics Market Report

The India cosmetics market was valued at USD 15.46 Billion in 2025, driven by rising disposable incomes, urbanization, and growing beauty awareness across demographic segments.

The market is projected to reach USD 25.39 Billion by 2034, growing at a CAGR of 5.66% during 2026-2034, driven by digital commerce, premiumization, and men’s grooming expansion.

Conventional cosmetics lead with an 82.54% share in 2025, supported by wide distribution, accessible pricing, and established brand familiarity across Indian consumer segments.

The organic cosmetics segment, holding 17.46% share in 2025, is growing at approximately 9.2% CAGR, driven by clean beauty trends, ingredient transparency demands, and Ayurvedic positioning.

Women account for 70.46% of India cosmetics market revenue in 2025, driven by economic empowerment, social media beauty influence, and comprehensive product adoption across categories.

Men’s grooming at 18.32% in 2025 is the fastest-growing gender segment, estimated at 8.4% CAGR through 2034, driven by changing grooming norms among Gen-Z and millennial male consumers.

North India leads with 32% of market revenue in 2025, anchored by high urban density, elevated disposable incomes, and strong organized and quick-commerce retail infrastructure.

Leading companies include Unilever, L’Oréal SA, Procter & Gamble, Emami Ltd., Marico, FSN E-Commerce (Nykaa), and Lotus Herbals Pvt Ltd.

E-commerce accounts for over 22% of total cosmetics sales in India in 2025, with Nykaa, Amazon, and Myntra Beauty driving premiumization and expanding access in Tier-2 and Tier-3 cities.

Rising consumer awareness of synthetic ingredient risks, Ayurvedic heritage, and premium willingness among urban consumers drive organic cosmetics, with Forest Essentials and Kama Ayurveda leading growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)