India Courier, Express and Parcel (CEP) Market Size, Share, Trends and Forecast by Service Type, Destination, Type, End Use Sector, and Region, 2026-2034

Market Overview:

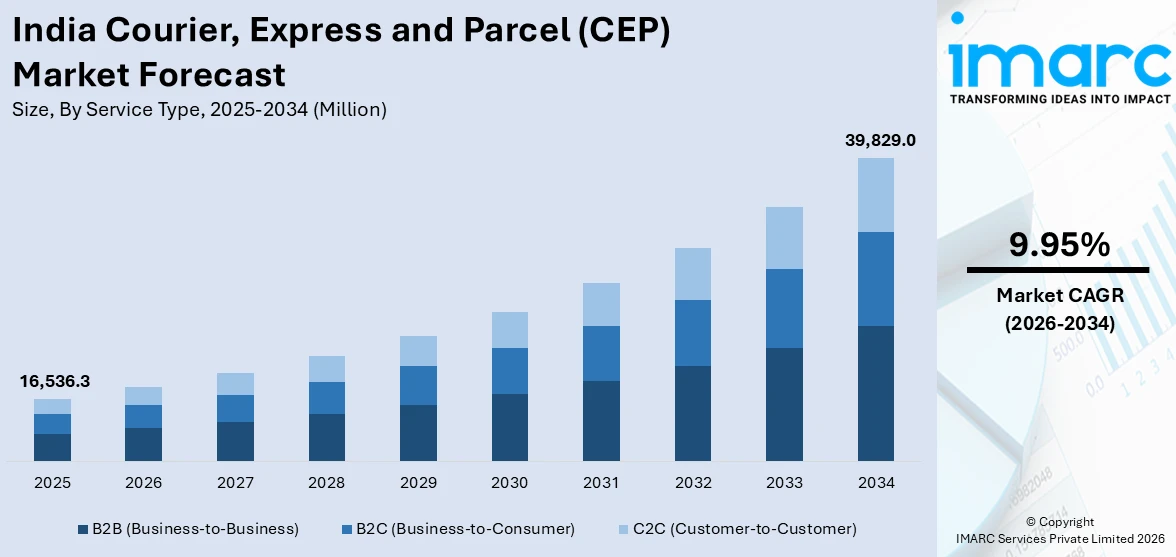

The India courier, express and parcel (CEP) market size reached USD 16,536.3 Million in 2025. The market is projected to reach USD 39,829.0 Million by 2034, exhibiting a growth rate (CAGR) of 9.95% during 2026-2034. The market growth is driven by the surge in e-commerce activity, rising demand for same-day/next-day deliveries, government support for logistics infrastructure, and the integration of advanced technologies like real-time tracking and automated sorting systems.

Market Insights:

- The regional segmentation includes North India, West and Central India, South India, and East and Northeast India.

- The market is segmented by service type into B2B (business-to-business), B2C (business-to-consumer), and C2C (customer-to-customer).

- Based on destination, the market is divided into domestic and international.

- The type segmentation includes air, ship, subway, and road.

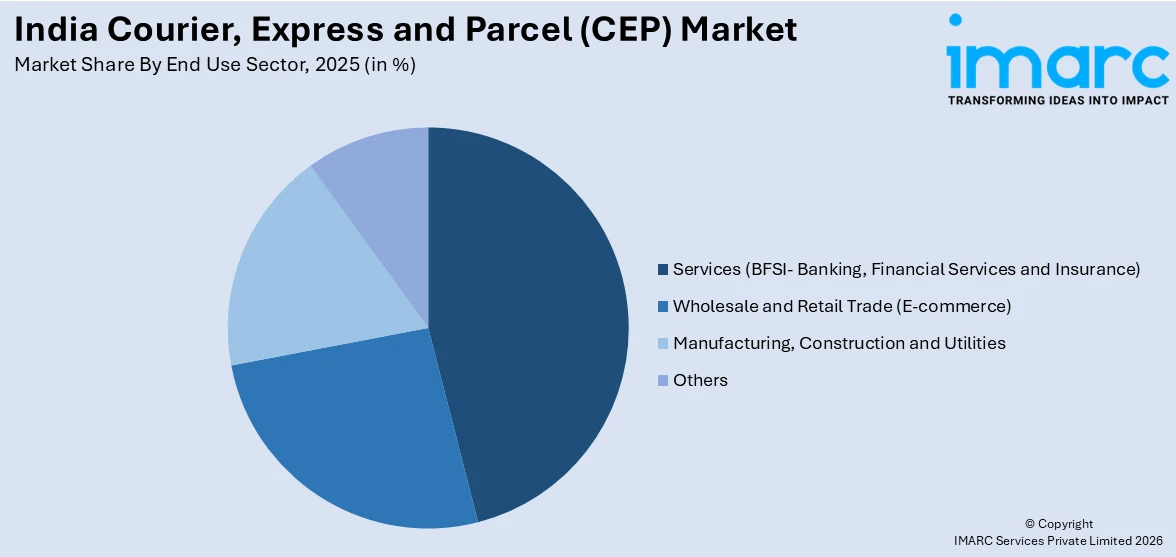

- The end use sectors include services (BFSI- Banking, Financial Services and Insurance), wholesale and retail trade (e-commerce), manufacturing, construction and utilities, and others.

Market Size and Forecast:

- 2025 Market Size: USD 16,536.3 Million

- 2034 Projected Market Size: USD 39,829.0 Million

- CAGR (2026–2034): 9.95%

Courier, express, and parcel (CEP) services constitute a specialized sector within the logistics industry that focuses on the swift and efficient delivery of packages, documents, and parcels. These services emphasize speed and reliability in transporting shipments from one location to another. Couriers, the primary carriers in CEP, are responsible for the secure and timely delivery of items, often catering to urgent or time-sensitive requirements. Express services prioritize quick transit times, employing streamlined processes and networks to expedite deliveries. Parcel services handle the transportation of packages, catering to both business and individual needs. The CEP industry has evolved significantly with technological advancements, employing tracking systems, advanced route optimization, and automation to enhance overall efficiency and customer satisfaction in the fast-paced world of logistics.

To get more information on this market Request Sample

The courier, express, and parcel (CEP) market in India is experiencing unprecedented growth, primarily driven by the regional surge in e-commerce activities. Evidently, with the increasing prevalence of online shopping, the demand for efficient and swift delivery services has become paramount. Consequently, companies within the CEP sector are harnessing advanced technology to enhance their operational capabilities, ensuring timely deliveries and customer satisfaction. Moreover, the ongoing digital transformation and the adoption of e-commerce platforms are major catalysts propelling the CEP market forward. This transformation has not only altered consumer behavior but has also intensified the need for reliable logistics services. Furthermore, the growing significance of same-day and next-day deliveries in the competitive market landscape acts as a significant driver. The race to meet consumer expectations for rapid and convenient shipping options has spurred innovation and investments in last-mile delivery solutions. Consequently, CEP companies are investing in cutting-edge technologies such as drones and autonomous vehicles to revolutionize their delivery mechanisms, making them more agile and responsive to the evolving demands of the modern consumer. In essence, the CEP market in India is thriving on a dynamic interplay of technological advancements, changing consumer preferences, and the evolving landscape of regional commerce.

India Courier, Express and Parcel (CEP) Market Trends:

Growth Drivers, Technology Adoption, and Sustainable Delivery

The demand for express delivery is growing significantly due to hyperlocal services, rapid grocery, and pharma logistics. Companies like Delhivery and Blinkit are experimenting with 2-hour delivery formats, pushing traditional CEP players to enhance their turnaround capabilities. Same-day and next-day delivery expectations from both urban consumers and businesses are pushing the market toward speed-focused services. In parallel, a surge in intercity personal parcel movement, gig-commerce (home businesses), and corporate document logistics is expanding use cases. Technology is playing a central role in improving efficiency and reducing risk. AI and machine learning are increasingly used for loss prediction, route optimization, and demand forecasting, while IoT-based parcel tracking and smart sorting hubs are reducing manual errors. Companies such as DTDC, Shadowfax, and ZEVO are piloting drone deliveries and integrating EVs into their last-mile fleets, aligning with sustainability goals. Green delivery initiatives, carbon efficiency benchmarks, and the push for cleaner urban logistics are now part of the business model, not just branding. With growing awareness of ESG metrics and fuel cost pressure, fleet electrification and micro-fulfillment center expansion are set to define the next wave of CEP transformation, therefore aiding the India courier, express and parcel (CEP) market growth. The intersection of rapid delivery expectations, regulatory tailwinds, and technological maturity is reshaping how parcels move across the country.

Challenges, Opportunities, and Government Support in the CEP Market

As per the India courier, express and parcel (CEP) market analysis, the market is rapidly expanding but not without complications. High operational costs, fragmented logistics networks in remote regions, and last-mile delivery inefficiencies continue to pose major challenges, especially for smaller players. Delays due to urban traffic congestion, inconsistent pin-code mapping, and reliance on manual processes affect delivery accuracy and increase return rates. However, the opportunities are equally significant. Tier II and III cities are becoming high-growth zones for B2C and C2C shipments, creating demand for reliable logistics partners. The rise of D2C brands and influencer-led commerce also presents new segments for hyperlocal and express deliveries, thereby expanding the India courier, express and parcel (CEP) market share. Government support has become more structured with the rollout of the National Logistics Policy, which focuses on digitization, standardization, and integrated logistics networks. Modernization of regional airports and expansion of cargo terminals are aimed at improving air express logistics, a key segment for time-sensitive CEP operations. Schemes supporting EV adoption and Make in India logistics startups are also indirectly benefiting CEP firms. Infrastructure projects like Bharatmala and Gati Shakti are enhancing road connectivity, reducing turnaround times, and supporting regional courier expansion. These policy efforts, if sustained, can ease some of the long-standing bottlenecks in network reliability and intermodal transport.

India Courier, Express and Parcel (CEP) Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on service type, destination, type, and end use sector.

Service Type Insights:

- B2B (Business-to-Business)

- B2C (Business-to-Consumer)

- C2C (Customer-to-Customer)

The report has provided a detailed breakup and analysis of the market based on the service type. This includes B2B (business-to-business), B2C (business-to-consumer), and C2C (customer-to-customer).

Destination Insights:

- Domestic

- International

A detailed breakup and analysis of the market based on the destination have also been provided in the report. This includes domestic and international.

Type Insights:

- Air

- Ship

- Subway

- Road

The report has provided a detailed breakup and analysis of the market based on the type. This includes air, ship, subway, and road.

End Use Sector Insights:

Access the comprehensive market breakdown Request Sample

- Services (BFSI- Banking, Financial Services and Insurance)

- Wholesale and Retail Trade (E-commerce)

- Manufacturing, Construction and Utilities

- Others

A detailed breakup and analysis of the market based on the end use sector have also been provided in the report. This includes services (BFSI- banking, financial services and insurance), wholesale and retail trade (e-commerce), manufacturing, construction and utilities, and others.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, West and Central India, South India, and East and Northeast India.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Latest News and Developments:

- July 2025: Zoomcar expanded its Home Delivery service to 14 Indian cities, using both flexible host tools and partnerships with third-party driver platforms to improve fulfillment, convenience, and booking reliability. Already accounting for 12% of total bookings, the service is expected to double its share as coverage increases, supporting over 40,000 cars and 10 million users nationwide, and enhance last-mile delivery and customer experience.

- May 2025: Uber launched Courier XL in India, enabling on-demand delivery of large shipments up to 750 kilograms using three- and four-wheeler carriers, initially available in Delhi NCR and Mumbai with expansion plans underway. Uber Courier’s package delivery volume grew by over 50% year-on-year in 2024, reaching 25 cities and more than 5 million users, with the average delivery distance at 11 km and longer trips recorded in Delhi NCR (14 km) and Mumbai (12 km).

- May 2025: The Express Industry Council of India (EICI) released a white paper recommending measures for the seamless integration of the Express Cargo Clearance System (ECCS) into India’s upcoming Customs Integrated System (CIS), aiming to retain the speed and operational agility needed for express cargo. The white paper highlights system architecture, real-time updates, and continued industry engagement as essential for strengthening India’s CEP market competitiveness.

- April 2025: Daakia.com launched its AI-based courier booking platform in India, backed by partnerships with India Post and leading private logistics providers, aiming to deliver parcel services to every PIN code within six months. The platform will leverage over 300,000 channel partners nationwide, with plans to double this network, offering MSMEs and individuals affordable rates, multiple delivery options, and real-time tracking.

- February 2025: DTDC entered the quick delivery space with the launch of 2-4 hour and same-day delivery options. To support this move, the company opened its first dark store in Bengaluru, aimed at improving hyperlocal fulfilment and last-mile operations. This setup is tailored for D2C brands and social commerce sellers, with plans to roll out similar services across India to enhance delivery speed for both businesses and end consumers.

India Courier, Express and Parcel (CEP) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered | B2B (Business-to-Business), B2C (Business-to-Consumer), C2C (Customer-to-Customer) |

| Destinations Covered | Domestic, International |

| Types Covered | Air, Ship, Subway, Road |

| End Use Sectors Covered | Services (BFSI- Banking, Financial Services and Insurance), Wholesale and Retail Trade (E-commerce), Manufacturing, Construction and Utilities, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India courier, express and parcel (CEP) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India courier, express and parcel (CEP) market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India courier, express and parcel (CEP) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)