India Cryptocurrency Market Size, Share, Trends and Forecast by Type, Component, Process, Application, and Region, 2026-2034

India Cryptocurrency Market Size, Share, Trends & Forecast (2026-2034)

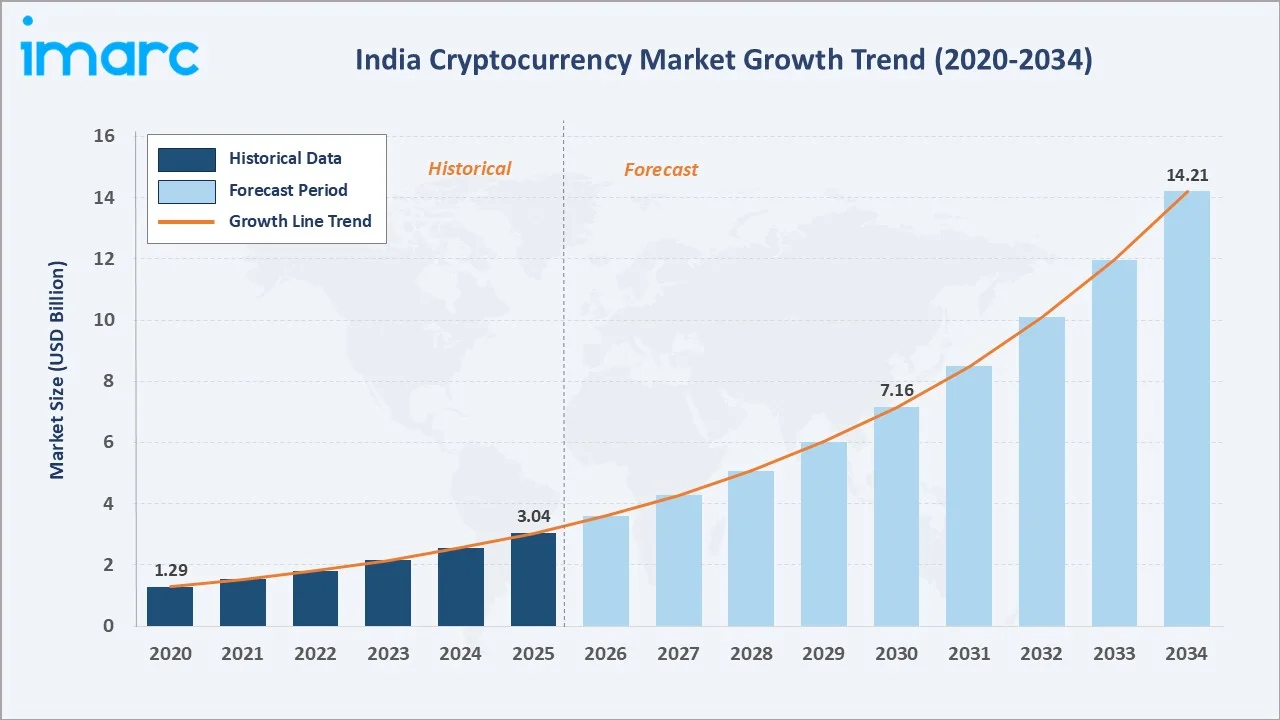

The India cryptocurrency market reached USD 3.04 Billion in 2025 and is projected to reach USD 14.21 Billion by 2034, growing at a CAGR of 18.66% during 2026-2034. India ranks first globally in crypto adoption (Chainalysis 2025), with rising retail engagement, a maturing FIU-IND-registered exchange ecosystem, and accelerating Web3 and DeFi innovation, collectively shaping market trajectory.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.04 Billion |

|

Forecast Market Size (2034) |

USD 14.21 Billion |

|

CAGR (2026-2034) |

18.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West & Central India (34.6% share, 2025) |

|

Fastest Growing Region |

South India |

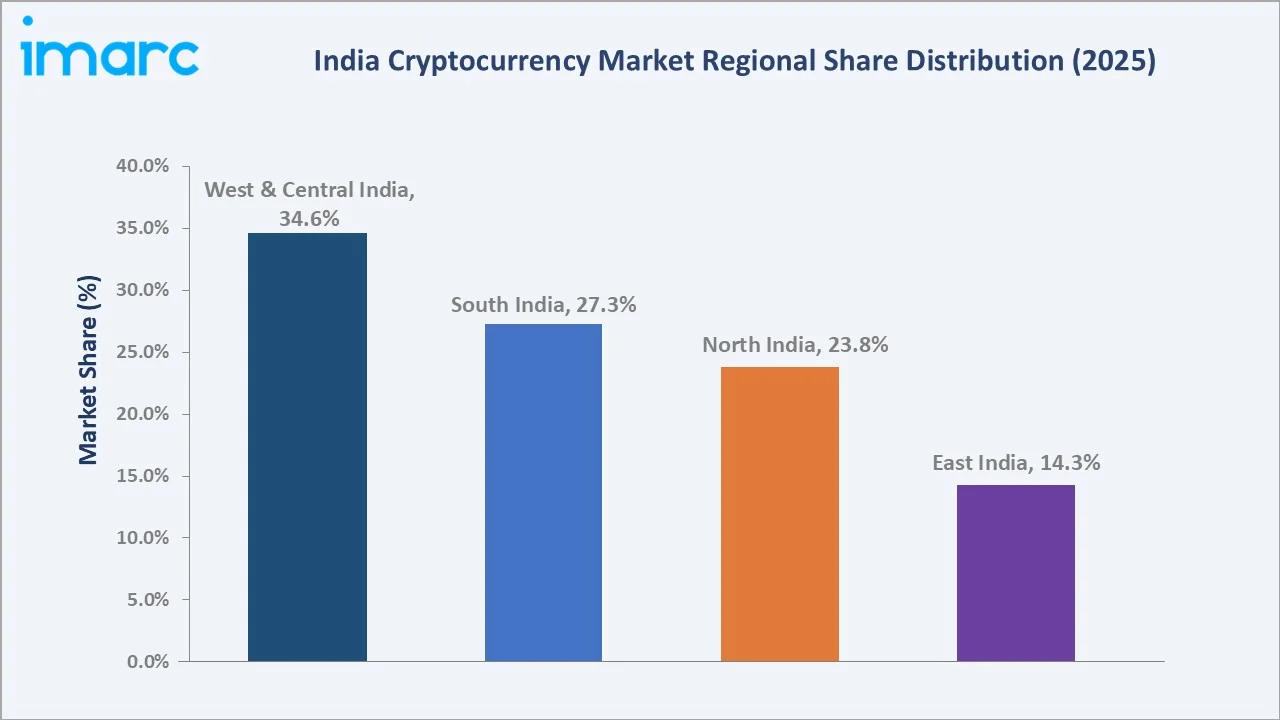

West & Central India dominates with a 34.6% share in 2025, anchored by Maharashtra, Gujarat, and Madhya Pradesh, where India’s leading exchanges and Web3 startups are headquartered. Software components lead at 56.07% of total market value, supported by exchange platforms, wallet protocols, and DeFi applications. Transaction processes represent 52.13% of activity, reflecting heavy retail engagement in trading, remittances, and payments over speculative mining.

To get more information on this market, Request Sample

With approximately 119 million crypto users and judicial recognition of cryptocurrencies as property by the Madras High Court, India is transitioning from regulatory ambiguity into a structured Virtual Digital Asset (VDA) market.

Executive Summary

India’s cryptocurrency market is on a sustained high-growth trajectory, propelled by the country’s top-ranked retail crypto adoption, deepening engagement of Tier-2 and Tier-3 cities, and a maturing compliance framework that filters reliable platforms from unregulated operators. The market reached USD 3.04 Billion in 2025 and is projected to reach USD 14.21 Billion by 2034, supported by smartphone-led onboarding, UPI-INR rails, and Web3 product innovation.

West & Central India leads regionally with a 34.6% share in 2025, followed by South India at 27.3%, reflecting concentrations of fintech ecosystem players, IT-services-led HNI investors, and emerging Web3 startup hubs in Bengaluru and Hyderabad. Software components dominate at 56.07%, while transaction-based activity represents 52.13% of segmented value.

Key activities in 2025 included Madras High Court’s recognition of cryptocurrencies as property in October 2025, FIU-IND’s enforcement actions against 25 offshore non-compliant platforms, the introduction of 18% GST on exchange services from July 2025, and India’s announcement to adopt the OECD Crypto-Asset Reporting Framework (CARF) by April 2027.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Component) |

Software – 56.07% (2025) |

|

Largest Segment (Process) |

Transaction – 52.13% (2025) |

|

Leading Region |

West & Central India – 34.6% share (2025) |

|

Fastest Growing Region |

South India (Web3 hub, IT-services-led HNI base) |

|

Top Companies |

Neblio Technologies Private Limited, Bitkuber Investments Private Limited, ZebPay, Mudrex Inc., and WazirX |

Key Analytical Observations:

- Software components account for 56.07% of the India cryptocurrency market in 2025, driven by exchange platforms, wallet applications, smart-contract protocols, and growing DeFi participation.

- Transaction processes lead the segmentation at 52.13% (2025), reflecting India’s strong retail trading orientation and rising use of crypto for cross-border remittances.

- West & Central India holds 34.6% of the total market in 2025, anchored by Mumbai’s fintech hub, Gujarat’s digital-payments density, and emerging blockchain clusters across the region.

- India ranks number one globally in the Chainalysis 2025 Crypto Adoption Index, topping every category, including retail, centralized finance, and decentralized finance use.

- As per the FIU-IND FY 2024–25 Annual Report, a total of 49 VDA service providers were registered, with total penalties of INR 2.8 billion imposed during the year on non-compliant entities, formalizing the regulated participant base.

India Cryptocurrency Market Overview

A cryptocurrency is a digital or virtual asset that uses cryptography for security and operates on decentralized blockchain networks. In India, cryptocurrencies are formally classified as Virtual Digital Assets (VDAs) under the Income Tax Act and are regulated through a multi-agency framework spanning the Financial Intelligence Unit (FIU-IND) under PMLA, the Central Board of Direct Taxes (CBDT) for taxation, and judicial precedent including the 2020 Supreme Court ruling that overturned RBI banking restrictions and the 2025 Madras High Court ruling recognizing crypto as property.

.webp)

Macroeconomic drivers include India’s approximately 1.12 billion active cellular mobile connections in early 2025, representing about 76.6% of the total population, a digitally native 18–35 demographic cohort, and the rapid expansion of UPI-linked fiat onboarding. While the 30% flat tax on gains and 1% TDS impose compliance burdens, they have simultaneously crystallized the legitimate participant base around FIU-IND-registered domestic exchanges, supporting transparent market growth toward the projected USD 14.21 Billion by 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

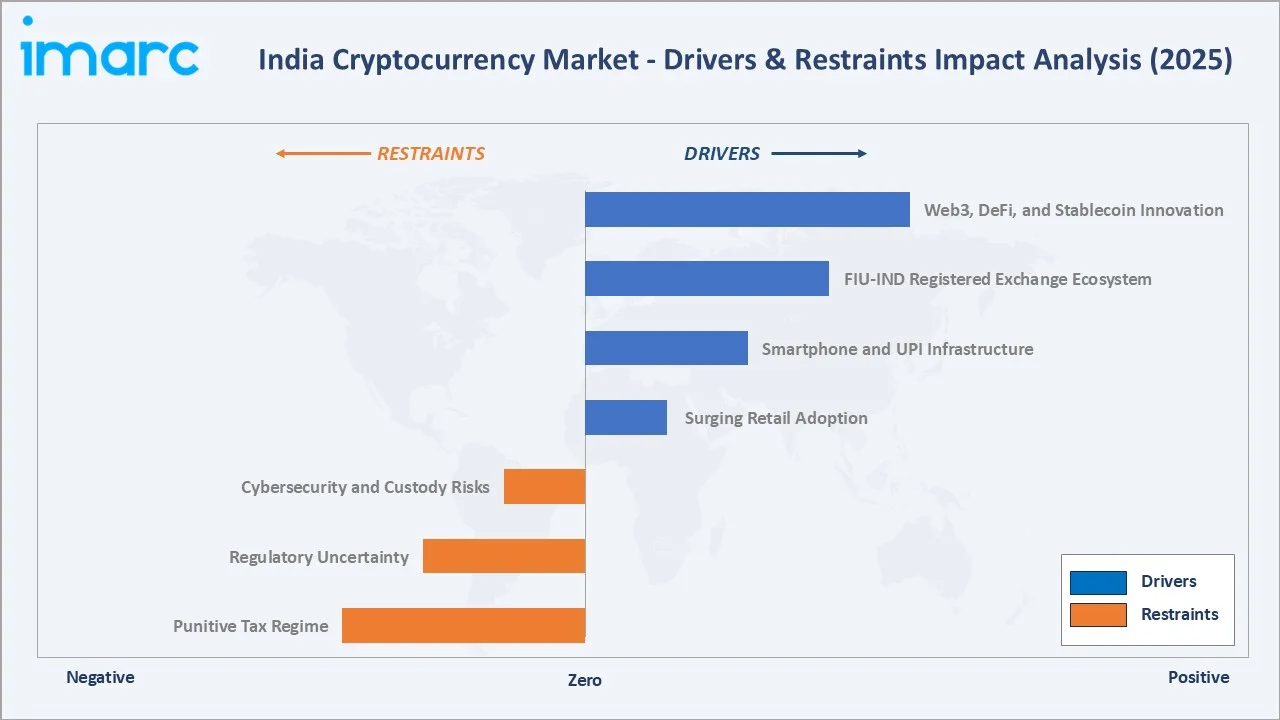

Market Drivers

- Surging Retail Adoption: India ranks number one globally in the Chainalysis 2025 Crypto Adoption Index, with approximately 119 million users and topping all categories, including retail, CeFi, and DeFi engagement, evidencing structural demand far beyond speculation.

- Smartphone and UPI Infrastructure: With around 806 million internet users at the beginning of 2025, with penetration reaching approximately 55.3% of the population, India has the digital backbone for mass onboarding. UPI-linked INR-to-VDA conversion and standardized eKYC have reduced friction across leading exchanges such as CoinDCX, CoinSwitch, and ZebPay.

- FIU-IND Registered Exchange Ecosystem: 49 Virtual Asset Service Providers are FIU-IND registered as of 2025, with mandatory PMLA reporting, Travel Rule compliance, and BitGo-grade custody, formalizing trust and reducing counterparty risk for retail and institutional investors.

- Web3, DeFi, and Stablecoin Innovation: Indian developers are emerging as a leading global cohort in DeFi protocol contributions, while stablecoins such as USDT and USDC are gaining adoption for cross-border remittances under the Liberalized Remittance Scheme cap of USD 250,000 per person per annum.

Market Restraints

- Punitive Tax Regime: A flat 30% tax on VDA gains, 1% TDS on transfers above INR 10,000, 4% cess, and 18% GST on exchange services introduced in July 2025 collectively impose one of the world’s heaviest crypto tax burdens, suppressing high-frequency trading and pushing some volumes offshore.

- Regulatory Uncertainty: The absence of a comprehensive standalone law and a dedicated regulatory body, with oversight currently distributed across RBI, SEBI, FIU-IND, and CBDT, creates strategic ambiguity for institutional participants and product developers seeking long-term clarity.

- Cybersecurity and Custody Risks: The July 2024 WazirX hack, in which exceeding USD 230 million in user assets were stolen, underscored persistent custody and security risks. Loss set-off and carry-forward are not permitted under Indian tax rules, amplifying investor exposure to such events.

Market Opportunities

- Tokenized Real-World Assets (RWAs): Tokenization of real estate, commodities, and government bonds presents a multi-billion-dollar opportunity. RBI’s Digital Rupee pilot and the Reserve Bank Innovation Hub are creating regulatory sandboxes that complement RWA development.

- Crypto-Linked Remittances: Stablecoin-based remittances offer 1% transfer costs versus 5–7% for traditional channels, addressing India’s position as the world’s largest remittance recipient (over USD 125 billion annually).

- Web3 Developer Economy: Indian developers contribute disproportionately to global Web3 talent, with over 50 fintech startups offering crypto-based lending, staking, and yield products, and major payment processors such as Razorpay and PayU enabling crypto purchases through their apps.

Market Challenges

- Loss Set-Off Restrictions: Losses from VDA trades cannot be set off against any other income or carried forward, increasing investor exposure during volatile cycles and discouraging long-term portfolio building.

- Offshore Volume Migration: Despite FIU-IND enforcement actions against 25 offshore platforms in 2024–2025, a meaningful share of high-volume Indian trading activity continues to migrate to offshore platforms and decentralized exchanges, reducing visible onshore tax revenue.

Emerging Market Trends

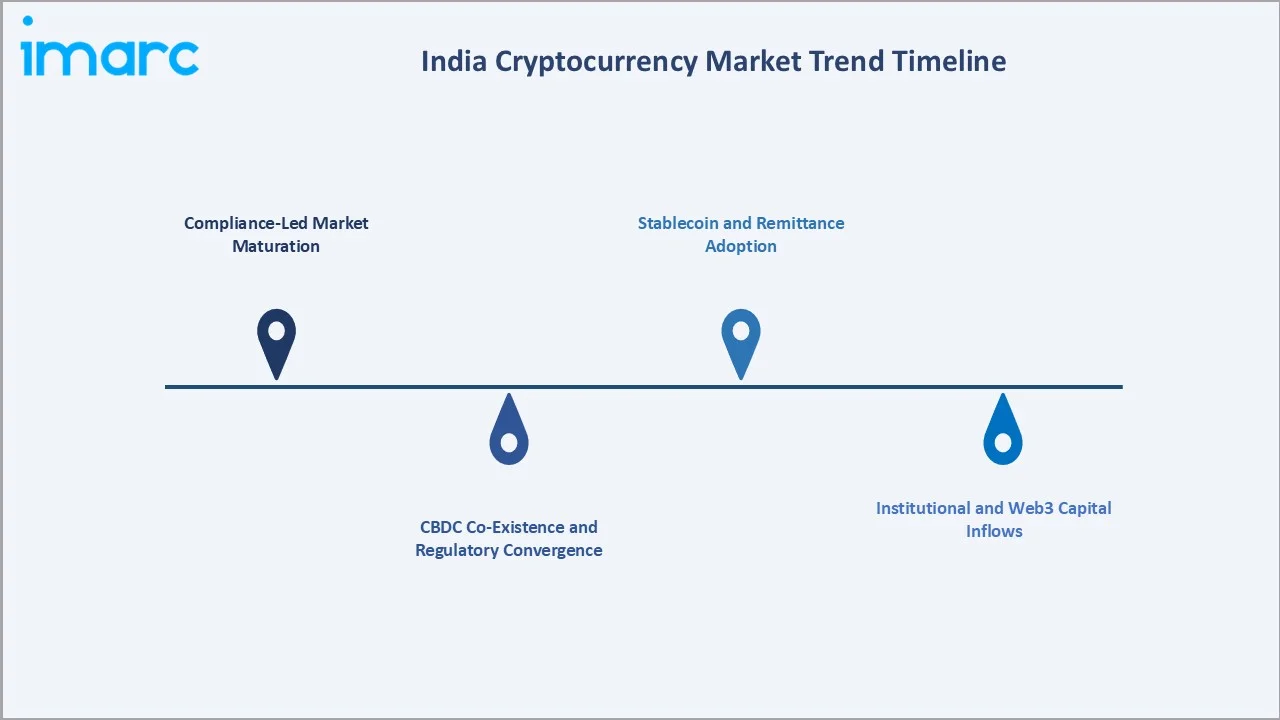

1. Compliance-Led Market Maturation

The FIU-IND classification of exchanges as PMLA-reporting entities since March 2023, the February 2025 VDA Income Tax Amendment Bill, and the August 2025 CBDT consultation paper on new VDA legislation collectively signal structured maturation. Mandatory Schedule VDA reporting in ITRs and the planned April 2027 OECD CARF implementation will further integrate India into the global regulated digital asset framework.

2. Stablecoin and Remittance Adoption

Stablecoins such as USDT and USDC are gaining traction in cross-border remittances, where they offer 1% transfer costs versus 5–7% for traditional channels. With India receiving over USD 125 billion annually in remittances, stablecoin pathways are reshaping low-value cross-border flows under the RBI’s Liberalized Remittance Scheme. Vendors and freelancers in cities like Ahmedabad, Varanasi, and Patna are integrating crypto-based receipt mechanisms into their workflows.

3. Institutional and Web3 Capital Inflows

Institutional engagement is rising through FIU-IND-registered platforms backed by global capital, including Coinbase’s investment in CoinDCX and Binance’s 2024 FIU-IND registration. Over 50 Indian crypto-fintech startups are offering lending, staking, and yield products, while payment processors such as Razorpay and PayU are integrating crypto purchase flows directly into mainstream consumer payments apps.

4. CBDC Co-Existence and Regulatory Convergence

The Reserve Bank of India’s Digital Rupee pilot, underway since 2022 across multiple banks and merchant categories, is increasingly seen as complementary rather than competitive to private VDAs. The proposed Crypto Assets Regulatory Authority (CARA) under the COINS Act, plus alignment with EU MiCA and OECD CARF frameworks, signals a convergent multi-rail digital payments environment by 2030.

Industry Value Chain Analysis

The India cryptocurrency industry value chain spans hardware infrastructure, software protocols, mining and validation, exchange platforms, custody and compliance, and end-user services. Each stage is anchored by specialized institutional and digital-native participants whose interactions determine product flow, security posture, and end-investor experience across the lifecycle.

|

Stage |

Key Players / Examples |

|

Hardware Providers |

ASIC manufacturers, GPU and high-performance computing suppliers, hardware wallet vendors, and mining rig assemblers |

|

Software & Protocol Layer |

Blockchain protocol developers, wallet application providers, smart-contract platforms, DeFi protocol builders, and node infrastructure operators |

|

Mining & Validation |

Mining pool operators, staking and validator node providers, energy supply partners, and proof-of-work and proof-of-stake infrastructure providers |

|

Exchanges & Trading Platforms |

FIU-IND-registered domestic exchanges, P2P platforms, derivatives exchanges, decentralized exchanges, and aggregator platforms |

|

Custodians & Compliance |

Institutional custodians, KYC/AML compliance providers, audit and proof-of-reserves attestors, and regulatory authorities |

|

End Users |

Retail investors, miners, merchants accepting crypto payments, corporate treasuries, remitters using stablecoin rails, and Web3 developers |

Technology Landscape in the India Cryptocurrency Industry

Layer-1 and Layer-2 Protocols

Indian developers contribute meaningfully to Ethereum, Polygon, Solana, and Avalanche ecosystems. Polygon, founded in India and now a global Layer-2 leader, exemplifies the country’s technical depth in scaling solutions, with adoption by major brands including Disney, Starbucks, and Reliance Jio.

Custody and Cold Storage Infrastructure

Industry leaders now store at least 95% of user assets in cold storage, offline hardware wallets that require physical access and multiple biometric authentications for access, employing multi-signature schemes, hardware security modules, and BitGo institutional custody. CoinDCX, ZebPay, and Mudrex publish regular proof-of-reserves disclosures aligned with global best practices.

AI-Driven Risk and Compliance

Exchanges deploy AI-led transaction monitoring for AML, market manipulation detection, and FATF Travel Rule compliance. Automated TDS deduction, real-time PMLA reporting, and Schedule VDA-aligned transaction tagging are now standard across the leading domestic platforms.

CBDC and Tokenization Pilots

The RBI Digital Rupee pilot has been extended across multiple banks for both wholesale and retail use cases. Parallel sandbox initiatives by NPCI, CBDT, and the Reserve Bank Innovation Hub are exploring tokenized deposits, asset-backed tokens, and government bond tokenization.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Bitcoin | 33.05% | 2025 |

| Component | Software | 56.07% | 2025 |

| Process | Transaction | 52.13% | 2025 |

| Application | Trading | 45.06% | 2025 |

| Region | West & Central India | 34.6% | 2025 |

By Component

Software components lead the component segment with a 56.07% share in 2025. The software stack encompasses centralized exchange platforms, hot and cold wallet applications, smart-contract development frameworks, decentralized exchange protocols, AML/KYC compliance modules, and DeFi yield products that have become increasingly mainstream.

.webp)

To access detailed market analysis, Request Sample

Hardware components hold the remaining 43.93%, comprising ASIC mining rigs, high-performance GPUs used for proof-of-work mining, hardware wallets such as Ledger and Trezor for cold custody, and specialized server infrastructure for staking nodes and validator operations. Hardware demand is concentrated in industrial mining facilities and HNI cold-storage deployments.

By Process

Transaction processes lead the process segment at 52.13% of the India cryptocurrency market in 2025, reflecting the predominance of retail trading, peer-to-peer transfers, and stablecoin-based remittances over speculative mining activity. UPI-INR onboarding, mandatory 1% TDS deduction at the transaction level, and standardized KYC have institutionalized transaction-led participation.

.webp)

Mining processes represent 47.87%, encompassing proof-of-work mining (predominantly Bitcoin and Litecoin), proof-of-stake validation for Ethereum and other PoS chains, and energy-linked operations. Mining is taxed as business income with energy-usage regulations applying state-by-state, and India’s renewable energy expansion is creating opportunities for green-mining initiatives.

Regional Market Insights

West & Central India leads with a 34.6% share in 2025, anchored by Maharashtra, Gujarat, and Madhya Pradesh. Mumbai hosts the headquarters of leading exchanges, including ZebPay, while Pune and Ahmedabad are emerging Web3 development hubs. The region also benefits from the highest density of digital-payments infrastructure, the deepest HNI investor base, and pioneering crypto-pay merchant adoption among small businesses.

South India follows at 27.3%, driven by Bengaluru, Hyderabad, and Chennai. Bengaluru is home to CoinDCX, CoinSwitch, and Unocoin, plus a substantial cohort of Web3 developers and DeFi protocol contributors. Hyderabad and Chennai support a fast-expanding base of IT-services-led HNI investors who are increasingly diversifying into crypto.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

34.6% |

Concentration of leading domestic crypto exchanges, asset managers, and brokerage operations, and the highest density of digital-payments users and HNI investor base in the country |

|

South India |

27.3% |

Bengaluru is positioned as the country's leading hub for crypto exchange operations and Web3/DeFi developer talent, and a large IT-services workforce driving HNI participation. |

|

North India |

23.8% |

Delhi NCR's digitally engaged retail investor base and broad demographic mix, and the second-largest tier-2 city inflow contributor after the western region |

|

East India |

14.3% |

Kolkata serves as the primary regional hub for both institutional and retail activity, and smartphone-led onboarding and stablecoin remittance use cases are driving incremental adoption. |

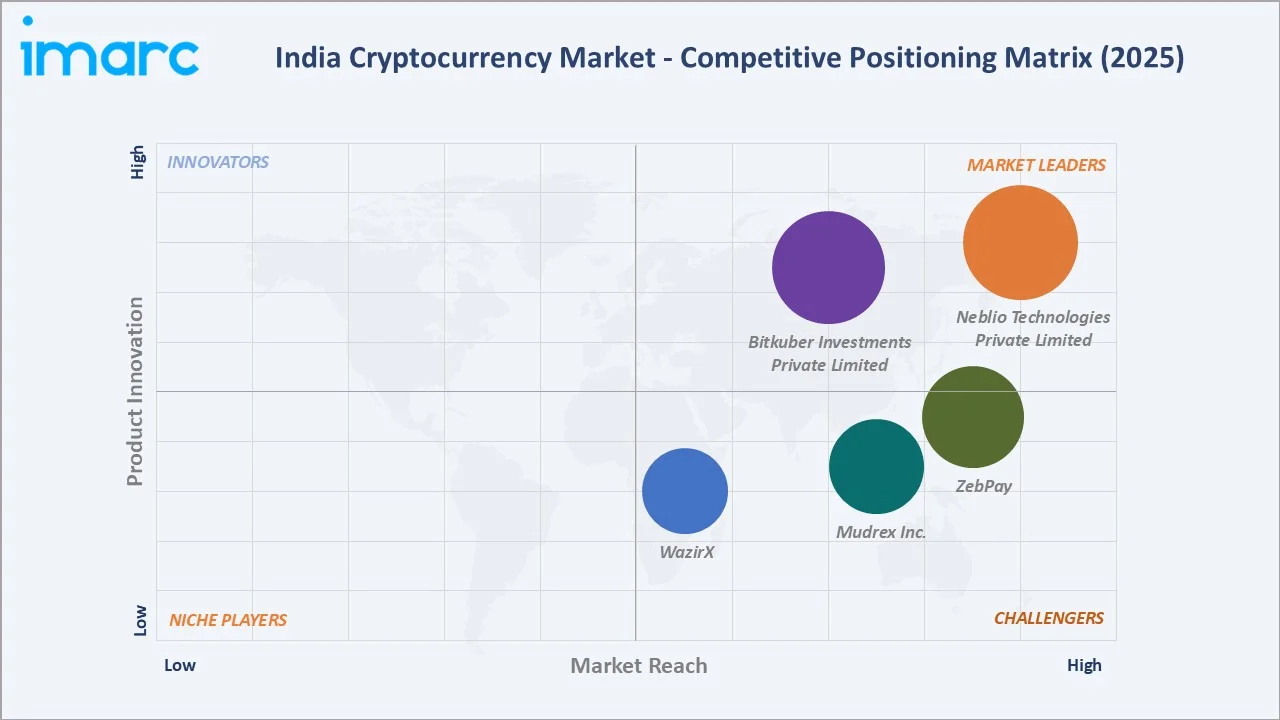

Competitive Landscape

The India cryptocurrency market exhibits a moderately fragmented structure dominated by FIU-IND-registered domestic exchanges. CoinDCX, CoinSwitch, ZebPay, and Mudrex anchor the high-trust retail segment, supported by 95%+ cold-storage custody, BitGo insurance, and proof-of-reserves disclosures.

|

Company |

Brand / Platform/Programs |

Market Position |

Core Strength |

|

Neblio Technologies Private Limited |

CoinDCX, DCX Learn CoinDCX Pro |

Market Leader |

India's first crypto unicorn; 20M+ users; spot, futures, margin, staking |

|

Bitkuber Investments Private Limited |

CoinSwitch, CoinSwitch Pro |

Market Leader |

20M+ registered users; aggregated liquidity model; simplified beginner interface |

|

ZebPay |

ZebPay |

Strong Challenger |

98% cold-storage custody; ZebPay Earn fixed returns; Lightning Network Bitcoin support |

|

Mudrex Inc. |

Mudrex, Coin Sets |

Strong Challenger |

Investment-led platform; Coin Sets thematic baskets; goal-based passive crypto investing |

|

WazirX |

WazirX, WRX Coin |

Challenger |

Relaunched October 2025 post-restructuring; BitGo custody; trust rebuild via post-relaunch fee incentives. |

Delta Exchange leads in derivatives. WazirX, despite its July 2024 hack, retained its FIU-IND license and relaunched with restructured custody in October 2025. Strategic alliances with global institutional players such as Coinbase and BitGo are deepening the credibility and product depth of the leading platforms.

Key Company Profiles

Neblio Technologies Private Limited

Neblio Technologies Private Limited operates CoinDCX, which is India’s first crypto unicorn and one of the most widely used FIU-IND-registered exchanges. The platform serves over 20 million users.

- Service Portfolio: Spot trading, futures, margin trading, staking, lending, DCX Learn educational platform; supports 1,000+ cryptocurrencies.

- Recent Development: CoinDCX’s 2025 Annual Report highlights that India’s crypto ecosystem is scaling rapidly, with over 2 crore (20+ million) users on the platform (+25% YoY) and total spot trading volume reaching INR 51,333 crore, alongside ~35% growth in institutional participation, reflecting increasing market depth.

- Strategic Focus: Beginner-friendly onboarding via UPI; INR 100 minimum investment; institutional-grade custody and proof-of-reserves disclosures.

Bitkuber Investments Private Limited

Bitkuber Investments Private Limited’s CoinSwitch, founded in 2017 and based in Bengaluru, has evolved from a crypto aggregator into a full-fledged FIU-IND-registered exchange with over 25 million registered users, one of the largest user bases among Indian crypto platforms.

- Service Portfolio: Spot and futures trading, simplified beginner interface, CoinSwitch Pro for advanced users, API, and OTC trading.

- Recent Development: In June 2025, CoinSwitch introduced crypto options trading, allowing users to trade derivatives with 24/7 access, aligning crypto markets with global, round-the-clock trading dynamics.

- Strategic Focus: Aggregated liquidity for competitive pricing; mobile-first user experience.

ZebPay

ZebPay, launched in 2014, is one of India’s oldest crypto exchanges, recognized for its conservative custody model with 98% of funds in cold storage and a strong long-term-investor user base.

- Service Portfolio: Spot trading, ZebPay Earn fixed returns, Lightning Network Bitcoin support, membership-based fee model.

- Recent Development: In August 2024, ZebPay launched Crypto-INR perpetual futures on its mobile app, enabling users to trade major cryptocurrencies like Bitcoin, Ethereum, Solana, and XRP directly using INR.

- Strategic Focus: Security-first positioning, regulated international operations, decade-long track record of compliance.

Market Concentration Analysis

The India cryptocurrency market is moderately concentrated. The top 5 FIU-IND-registered exchanges (CoinDCX, CoinSwitch, ZebPay, Mudrex, and Binance India) collectively account for an estimated 70–75% of compliant onshore trading volumes in 2025.

WazirX, Unocoin, Bitbns, and Delta Exchange contribute the bulk of the remainder, with smaller specialty platforms such as Giottus filling niche segments. Consolidation pressure is rising as compliance, custody, and FIU-IND licensing requirements raise entry barriers, while strategic backing from global players (Coinbase in CoinDCX, BitGo as custodian for multiple platforms) is reshaping the competitive frontier.

Investment & Growth Opportunities

Fastest Growing Segments

Stablecoin-based remittances (estimated CAGR ~25%), DeFi protocols and Web3 yield products (~22%), and tokenized real-world assets (~28%) represent the highest-growth investment vectors through 2034. Software-led offerings, including custody-as-a-service, compliance APIs, and Layer-2 scaling infrastructure, are projected to outpace hardware demand as Indian users gravitate toward wallet-based, exchange-mediated participation.

Emerging Market Expansion

India's USD 125 billion+ annual remittance market represents a major addressable opportunity for stablecoin corridors, where USDT and USDC rails offer transfer costs of ~1% versus 5–7% for traditional channels. Tier-2 and Tier-3 city expansion through vernacular onboarding, UPI integration, and crypto-literacy initiatives such as CoinDCX's Bitcoin Chai Cafe (January 2025) is unlocking the next 100 million users beyond metro hubs.

Venture and Institutional Investment Trends

Strategic capital is flowing into India's crypto ecosystem through global partnerships and institutional infrastructure. Coinbase's strategic backing of CoinDCX, BitGo custody integration across multiple FIU-IND-registered platforms, and Binance India's 2024 FIU-IND re-registration collectively signal deepening institutional engagement.

Future Market Outlook (2026-2034)

India’s cryptocurrency market is positioned for sustained, high-magnitude growth. From a base of USD 3.04 Billion in 2025, the market is projected to reach USD 14.21 Billion by 2034, expanding at a CAGR of 18.66%.

Three structural macro-themes will shape the trajectory: regulatory clarity through the proposed Crypto Assets Regulatory Authority (CARA) and OECD CARF implementation by April 2027; deepening institutional engagement through FIU-IND-licensed platforms backed by global capital; and Web3 product innovation across stablecoins, DeFi, and tokenized real-world assets. Platforms that combine compliance leadership, robust custody, and Tier-2 distribution depth will be best positioned to capture share in a maturing VDA ecosystem.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 110 industry participants in 2024–2025, including FIU-IND-registered exchange executives, custody and security providers, regulatory experts, Web3 startup founders, miners, and retail investors across all four Indian regions.

Secondary Research

Secondary research included Chainalysis Global Crypto Adoption Index, FIU-IND notifications, CBDT and Ministry of Finance circulars, AMFI-style industry reports for VDAs, exchange annual disclosures, and trade publications. Over 200 sources were triangulated for market sizing and segmentation.

Forecasting Models

Market size estimations apply a hybrid top-down and bottom-up approach, combining global crypto market trajectories, India-specific user adoption rates, exchange trading volume pipelines, regulatory compliance milestones, and tax-elasticity scenarios. The base-case CAGR of 18.66% reflects consensus across regulatory milestones, retail adoption projections, and observed flows in compliant onshore platforms.

India Cryptocurrency Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Bitcoin, Ethereum, Bitcoin Cash, Ripple, Litecoin, Dashcoin, Others |

| Components Covered | Hardware, Software |

| Processs Covered | Mining, Transaction |

| Applications Covered | Trading, Remittance, Payment, Others |

| Regions Covered | South India, North India, West & Central India, East India |

| Companies Covered | Neblio Technologies Private Limited, Bitkuber Investments Private Limited, ZebPay, Mudrex Inc., WazirX, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Cryptocurrency Market Report

The India cryptocurrency market reached USD 3.04 Billion in 2025 and is projected to reach USD 14.21 Billion by 2034.

The market is expected to grow at a CAGR of 18.66% during the forecast period 2026-2034, supported by top-ranked retail adoption, regulatory formalization, and Web3 product innovation.

West & Central India leads with a 34.6% share in 2025, anchored by Mumbai, Pune, Ahmedabad, and Surat, which together host the densest fintech and Web3 startup ecosystem.

Software components dominate the segment at 56.07% in 2025, reflecting the strength of exchange platforms, wallet protocols, smart-contract frameworks, and DeFi applications.

Transaction processes lead the segment at 52.13% in 2025, driven by retail trading, P2P transfers, and stablecoin-based remittances over speculative mining activity.

Key players include Neblio Technologies Private Limited, Bitkuber Investments Private Limited, ZebPay, Mudrex Inc., and WazirX.

Regulation formalizes the legitimate participant base. FIU-IND registration, mandatory PMLA reporting, the 30% flat tax with 1% TDS, 18% GST on exchange services from July 2025, and the planned April 2027 OECD CARF implementation collectively are crystallizing onshore trust around compliant platforms.

Key challenges include the punitive flat 30% tax with 1% TDS and 18% GST burden, no loss set-off provision, regulatory uncertainty pending CARA-led legislation, cybersecurity risks evidenced by the 2024 WazirX hack, and offshore volume migration.

Major opportunities lie in tokenized real-world assets, stablecoin-based remittances, DeFi yield products, custody-as-a-service offerings, FIU-IND-licensed exchange acquisitions, and Tier-2 city retail expansion via vernacular onboarding and UPI integration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)