India Cyber Insurance Market Size, Share, Trends and Forecast by Component, Insurance Type, Organization Size, End-Use Industry, and Region, 2026-2034

India Cyber Insurance Market Summary:

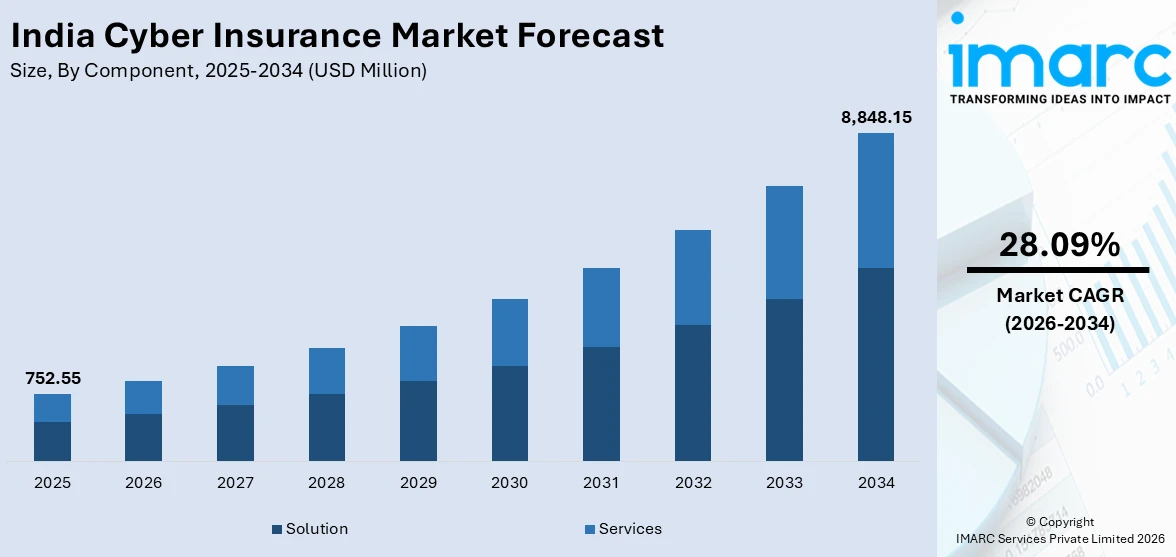

The India cyber insurance market size was valued at USD 752.55 Million in 2025 and is projected to reach USD 8,848.15 Million by 2034, growing at a compound annual growth rate of 28.09% from 2026-2034.

The India cyber insurance market is gaining strong traction, driven by escalating cyber threats, stricter data protection regulations, and the rapid digitalization of businesses across sectors. The growing adoption of cloud platforms, fintech solutions, and digital payment infrastructure is broadening attack surfaces and intensifying risk exposure. Proactive risk management awareness, evolving regulatory mandates, and expanding enterprise cybersecurity investments are creating a supportive environment for market growth.

Key Takeaways and Insights:

- By Component: Solution dominates the market with a share of 62.3% in 2025, owing to its comprehensive capabilities in automated risk assessment, policy administration, and real-time threat intelligence, enabling organizations to manage cyber risks within a unified and adaptive framework.

- By Insurance Type: Stand-alone leads the market with a share of 65.2% in 2025, driven by increasing demand for dedicated, purpose-built policies offering broader coverage and flexible customization for specific cyber risks compared to packaged alternatives.

- By Organization Size: Large enterprises prevail the market with a share of 68.4% in 2025, reflecting their greater exposure to cyber threats, extensive data assets, complex IT infrastructure, and the need for high-value, comprehensive coverage against financial and reputational losses.

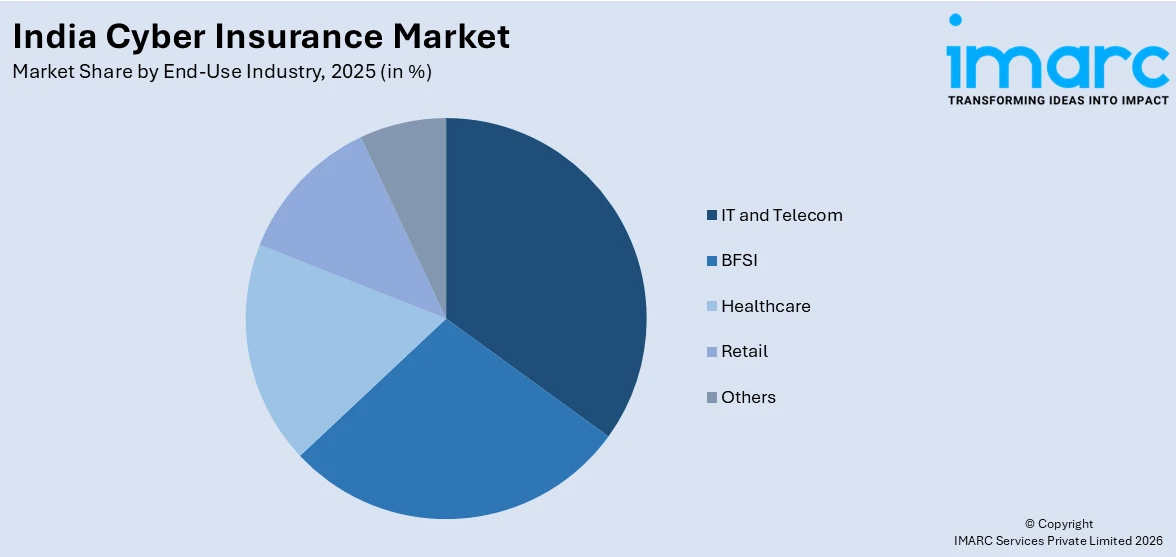

- By End-Use Industry: IT and telecom represent the largest segment with a market share of 32.5% in 2025, driven by the sector's extensive digital infrastructure, vast data repositories, high-value client relationships, and significant vulnerability to sophisticated cyberattacks and data breaches.

- By Region: South India comprises the largest region with 34.2% share in 2025, propelled by the high concentration of IT and technology companies in Bengaluru and Hyderabad, making it the most digitally intensive and cyber risk-exposed geographic zone in the country.

- Key Players: Key players in the India cyber insurance market drive growth by developing innovative policy structures, expanding digital distribution channels, and strengthening partnerships with cybersecurity firms. Their focus on customized coverage, competitive pricing, and enhanced incident response services ensures broad enterprise adoption across diverse industries.

To get more information on this market Request Sample

The India cyber insurance market is evolving rapidly, as organizations across sectors prioritize proactive digital risk management strategies. The convergence of increased cyberattack frequency, regulatory mandates, and digital transformation has elevated cybersecurity from an operational concern to a strategic imperative. According to the Computer Emergency Response Team of India, the country recorded over 2.04 Million cybersecurity incidents in 2024, highlighting the urgency for businesses to hedge financial and reputational exposure through insurance. The market encompasses a wide range of offerings, including coverage for data breach response, ransomware recovery, business interruption, and third-party liability. Enterprises and individuals are increasingly recognizing that cybersecurity investments alone are insufficient to address the full spectrum of digital risk, reinforcing the critical role of insurance in comprehensive risk management.

India Cyber Insurance Market Trends:

Rising Integration of Artificial Intelligence (AI) in Cyber Insurance Underwriting

The integration of AI into cyber insurance underwriting is transforming how insurers assess and price digital risks in India. AI-powered tools enable dynamic risk profiling by analyzing telemetry data from clients' IT environments, including endpoint security posture, patching cadence, and user behavior patterns. Insurers use machine learning (ML) to refine loss models and offer tiered pricing based on real-time security performance. As per IMARC Group, the India ML market size reached USD 1,013.3 Million in 2024. This data-driven approach improves underwriting accuracy, reduces moral hazard, and creates incentives for businesses to maintain stronger cyber hygiene, ultimately supporting the market growth.

Strengthening Regulatory Landscape Driving Policy Adoption

India's regulatory environment is increasingly mandating robust cybersecurity frameworks, directly stimulating demand for cyber insurance. The Digital Personal Data Protection Rules, 2025, notified in November 2025 by the Ministry of Electronics and Information Technology, established enforceable compliance obligations, including mandatory breach notifications, defined security safeguards, and penalties reaching up to INR 250 Crore for non-compliance. These regulatory requirements are compelling organizations across sectors to acquire cyber insurance as a financial safeguard against potential penalties, breach notification costs, and legal liabilities arising from data protection failures.

Growing Demand for Specialized Coverage Among IT and Telecom Enterprises

India's rapidly expanding IT services and telecom sector is emerging as a primary driver of specialized cyber insurance adoption. The sector's extensive digital infrastructure, dependence on third-party vendors, and large client data repositories create substantial exposure to ransomware, data breaches, and business interruption incidents. Cyber insurance is being integrated into enterprise risk management frameworks, helping organizations mitigate financial losses, ensure operational continuity, and strengthen stakeholder confidence in an evolving threat landscape.

Market Outlook 2026-2034:

The India cyber insurance market is on a strong growth trajectory, underpinned by the intersection of escalating digital threats, expanding regulatory obligations, and heightened corporate awareness of cyber risk. The increasing reliance of Indian enterprises on cloud platforms, digital payment systems, and remote work infrastructure is continuously widening the attack surface, elevating financial exposure across sectors. The market generated a revenue of USD 752.55 Million in 2025 and is projected to reach a revenue of USD 8,848.15 Million by 2034, growing at a compound annual growth rate of 28.09% from 2026-2034. The deployment of advanced policy structures covering ransomware recovery, legal liabilities, third-party vendor breaches, and regulatory penalties is expected to expand total addressable market potential significantly.

India Cyber Insurance Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Solution |

62.3% |

|

Insurance Type |

Stand-alone |

65.2% |

|

Organization Size |

Large Enterprises |

68.4% |

|

End-Use Industry |

IT and Telecom |

32.5% |

|

Region |

South India |

34.2% |

Component Insights:

- Solution

- Services

Solution dominates with a market share of 62.3% of the total India cyber insurance market in 2025.

Solution prevails the market, as solution-based cyber insurance integrates advanced risk assessment tools, automated policy management platforms, and real-time threat analytics into cohesive coverage frameworks. These solutions provide organizations with continuous monitoring capabilities and predictive incident modeling, enabling more accurate financial risk quantification. India reported approximately 370 Million malware attacks in 2024, underscoring the scale of digital threats that solution-centric policies are designed to address. The breadth of solution offerings, spanning endpoint protection, identity governance, and cloud security orchestration, ensures broad enterprise applicability, making them the preferred choice for risk managers seeking comprehensive and adaptive coverage.

Solution-driven cyber insurance policies offer unparalleled flexibility in coverage customization, enabling enterprises to tailor protection against specific threat vectors relevant to their industry and operational environment. Unlike bundled offerings, stand-alone solution packages allow organizations to add modular protections, such as ransomware response, third-party vendor risk coverage, and forensic investigation support, without the limitations of pre-packaged terms. This adaptability is particularly valuable in sectors characterized by high data sensitivity and frequent regulatory changes, where evolving risks demand continuous policy reassessment and adjustment to ensure adequate financial protection against new and emerging cyber threats.

Insurance Type Insights:

- Packaged

- Stand-alone

Stand-alone leads with a share of 65.2% of the total India cyber insurance market in 2025.

Stand-alone dominates the market, owing to its comprehensive coverage structure specifically designed to address evolving cyber risks, including ransomware attacks, data breaches, and business interruption losses. The ability to customize coverage limits, select specific incident response services, and integrate forensic support as part of the policy structure makes standalone products particularly attractive to enterprises managing significant digital assets and complex IT environments. This flexibility also enables organizations to align coverage with their unique risk exposure and regulatory obligations.

Stand-alone cyber insurance policies are gaining preference as organizations develop a more sophisticated understanding of their specific cyber risk profiles. Unlike packaged alternatives that bundle cyber coverage alongside other lines, such as commercial general liability or property insurance, standalone policies are designed exclusively around digital risk, enabling insurers to apply specialized underwriting expertise and provide targeted claims support. This specialization results in more refined coverage terms, clearer policy language, and faster incident response, making stand-alone products the preferred option for enterprises prioritizing clarity, depth of coverage, and efficient claims management in the event of a cyber incident.

Organization Size Insights:

- Small and Medium Enterprises

- Large Enterprises

Large enterprises exhibit a clear dominance with a 68.4% share of the total India cyber insurance market in 2025.

Large enterprises, with their complex IT ecosystems, extensive data repositories, and higher regulatory scrutiny, face disproportionately elevated exposure to ransomware, advanced persistent threats, and supply chain breaches. India's cybersecurity budget was nearly doubled from INR 400 Crore in 2023 to INR 759 Crore in 2024, reflecting government recognition of escalating cyber risks and setting a strong precedent for enterprise-level investments in security and risk mitigation. Comprehensive cyber insurance is a critical component of enterprise risk governance, enabling financial recovery from incidents that could otherwise result in catastrophic operational and reputational damage.

Large enterprises are increasingly integrating cyber insurance into their broader enterprise risk management frameworks as part of board-level governance strategies. The scale and interdependency of large-scale IT infrastructures, the extensive use of third-party vendors, and the critical nature of the data they handle demand high-value policy structures covering business interruption, regulatory investigation costs, crisis communications, and forensic services. As compliance obligations under the Digital Personal Data Protection Act expand, large enterprises are reassessing coverage adequacy and upgrading existing policies to ensure alignment with stricter data protection standards and evolving regulatory expectations.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- BFSI

- Healthcare

- IT and Telecom

- Retail

- Others

IT and telecom represent the leading segment with a 32.5% share of the total India cyber insurance market in 2025.

IT and telecom firms manage vast repositories of customer data, operate interconnected network infrastructure, and serve clients across critical industries, making them highly attractive targets for ransomware, data exfiltration, and denial-of-service attacks. India's IT job demand reached 1.8 Million roles in 2025, a 16% increase from 2024, reflecting the sector's rapid expansion and growing data management responsibilities that amplify cyber risk exposure. The sector's high operational dependency on digital continuity means that even brief service disruptions can result in significant financial losses, reinforcing strong demand for comprehensive cyber insurance coverage.

The IT and telecom sector's reliance on complex third-party ecosystems, cloud platforms, and global delivery models creates multidimensional cyber risk exposure that extends well beyond internal network perimeters. Software developers, managed service providers, and telecom operators face unique threats related to software supply chain vulnerabilities and customer data privacy obligations. Cyber insurance policies tailored to IT and telecom firms typically cover professional liability for technology errors, data breach notification costs, regulatory investigation expenses, and reputational management services, reflecting the breadth of coverage needed to adequately protect enterprises in this sector.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

South India prevails with a market share of 34.2% of the total India cyber insurance market in 2025.

South India leads the market, owing to its strong concentration of IT and technology-driven enterprises across key hubs, such as Bengaluru, Hyderabad, and Chennai. The region houses a dense cluster of IT companies, Global Capability Centers, and digital services firms, generating substantial demand for specialized cyber insurance to protect against data breaches, operational disruptions, and contractual liabilities arising from complex client relationships and cross-border data flows. This concentration also drives higher awareness of evolving cyber threats among enterprises.

In addition to its focus on IT services, South India's cyber insurance market is bolstered by the robust presence of financial technology firms, healthcare technology platforms, and e-commerce companies that collectively handle substantial amounts of sensitive financial and personal data. Businesses in Bengaluru, Hyderabad, and Chennai are actively working to comply with national data protection laws, demonstrating a high level of regional regulatory awareness. South India is the nation's most developed and commercially active cyber insurance market, due to its proactive compliance culture and large company investment in digital infrastructure.

Market Dynamics:

Growth Drivers:

Why is the India Cyber Insurance Market Growing?

Escalating Frequency and Sophistication of Cyberattacks

The India cyber insurance market is experiencing strong demand as organizations grapple with an increasingly hostile threat landscape characterized by rising attack frequency, greater complexity, and expanding financial consequences. The proliferation of ransomware, phishing campaigns, and advanced persistent threats has elevated the risk profile of businesses across all sectors, compelling risk managers to evaluate insurance as a critical financial safety net alongside technical cybersecurity controls. The financial exposure associated with these incidents is substantial. Recovery costs, legal fees, customer notification expenses, and regulatory penalties can collectively reach tens of crores for mid-sized enterprises. The evolving nature of attack methodologies, including AI-assisted phishing, deepfake fraud, and supply chain infiltration, is making it increasingly difficult for organizations to rely solely on preventive cybersecurity measures. Cyber insurance provides the financial resilience needed to absorb these costs, enabling business continuity while facilitating rapid incident response. This structural demand driver is expected to sustain strong market momentum throughout the forecast period.

Expanding Data Protection Regulatory Framework

India's data protection regulatory environment has undergone a fundamental transformation, creating substantial compliance-driven demand for cyber insurance. Organizations classified as Data Fiduciaries are required to implement mandatory breach notification procedures, secure data processing safeguards, and time-bound grievance resolution mechanisms. The Securities and Exchange Board of India introduced new cybersecurity regulations in August 2024, requiring all regulated financial entities to establish Security Operations Centers. These layered regulatory obligations spanning multiple sectors are fundamentally altering corporate risk management strategies, positioning cyber insurance as an essential compliance tool rather than a discretionary expense. As penalties for non-compliance and data breaches become more stringent, organizations are increasingly seeking financial protection against regulatory fines and legal liabilities. Insurers are also aligning policy structures with evolving legal frameworks, offering coverage extensions tailored to compliance risks. This shift is accelerating policy adoption across both large enterprises and mid-sized firms navigating complex regulatory landscapes.

Rapid Digital Transformation and Cloud Adoption Across Industries

India's accelerating digital transformation is generating systemic cyber risk exposure across previously low-risk industries, creating new addressable markets for cyber insurance providers. The widespread adoption of cloud computing, digital payment systems, e-commerce platforms, and internet of things infrastructure has dramatically expanded the attack surface for businesses of all sizes. Industries traditionally reliant on physical operations, including manufacturing, retail, and logistics, are managing large volumes of sensitive customer and operational data, increasing their vulnerability to cyberattacks. Healthcare organizations are digitizing patient records and adopting telemedicine platforms, while financial institutions are expanding digital lending, mobile banking, and payment gateway operations. Each of these transitions creates new insurance needs, from data breach coverage to operational continuity protection. The convergence of digital transformation and rising cyber threat sophistication is creating a powerful structural demand driver that is expected to sustain strong double-digit growth in the cyber insurance market throughout the forecast period.

Market Restraints:

What Challenges the India Cyber Insurance Market is Facing?

Limited Cybersecurity Maturity Among Small and Medium Enterprises (SMEs)

Despite growing cyber threats, a significant portion of Indian SMEs lack the foundational cybersecurity infrastructure required to qualify for comprehensive cyber insurance coverage. Insurers typically require minimum security controls, including firewalls, multi-factor authentication, and endpoint protection, as preconditions for policy issuance. Without these baseline measures, SMEs face higher premiums or outright rejection of coverage applications. This maturity gap not only limits market penetration but also leaves a large segment of India's business community without financial protection against cyber incidents, constraining overall market growth.

High Premium Costs and Affordability Constraints

The cost of cyber insurance premiums in India remains a significant barrier to widespread adoption, particularly among price-sensitive small businesses and mid-market enterprises. Premium calculations are influenced by the complexity of an organization's IT environment, historical incident frequency, and coverage breadth, resulting in prices that may be prohibitive for organizations with limited risk management budgets. Additionally, businesses that have experienced prior cyber incidents often face sharp premium increases upon renewal, further constraining their ability to maintain continuous coverage and creating persistent gaps in market penetration among smaller organizations.

Shortage of Specialized Cyber Insurance Expertise and Actuarial Talent

India faces a structural deficit in specialized cyber underwriting professionals and actuarial experts capable of accurately modeling digital risk. This talent gap results in pricing inefficiencies, limited product innovation, and challenges in developing coverage structures that adequately reflect India's unique threat environment and regulatory landscape. As a result, insurers often rely on global risk models that may not fully capture localized threat patterns and sector-specific vulnerabilities. This dependence limits underwriting precision and slows the development of tailored cyber insurance solutions suited to the Indian market.

Competitive Landscape:

The India cyber insurance market features a competitive blend of established general insurance companies and emerging specialist providers, each competing to capture share in a rapidly expanding segment. Leading insurers are differentiating through product innovation, expanding their policy structures to include advanced incident response services, forensic investigation support, and reputational damage management alongside traditional coverage. Technology partnerships with cybersecurity firms enable insurers to offer value-added risk assessment tools and proactive threat monitoring as part of integrated coverage packages. Distribution strategies are evolving, with digital platforms and Insurtech solutions facilitating broader market reach, particularly among SMEs that historically relied on traditional broker channels. Reinsurance arrangements are supporting capacity expansion, enabling domestic insurers to underwrite higher-value policies for large enterprises.

India Cyber Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| Insurance Types Covered | Packaged, Stand-alone |

| Organization Sizes Covered | Small and Medium-sized Enterprises (SMEs), Large Enterprises, |

| End Use Industries Covered | BFSI, Healthcare, IT and Telecom, Retail, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Cyber Insurance Market Report

The India cyber insurance market size was valued at USD 752.55 Million in 2025.

The India cyber insurance market is expected to grow at a compound annual growth rate of 28.09% from 2026-2034 to reach USD 8,848.15 Million by 2034.

Solution dominated the market with a share of 62.3%, owing to its comprehensive risk assessment capabilities, automated policy management tools, and ability to integrate real-time threat intelligence into cohesive coverage frameworks for organizations across sectors.

Key factors driving the India cyber insurance market include escalating cyber threat frequency, mandatory data protection regulations, rapid digital transformation, cloud adoption, growing enterprise risk awareness, and expanding digital payment infrastructure across industries.

Major challenges include limited cybersecurity maturity among SMEs, high premium costs, shortage of specialized cyber underwriting expertise, evolving and sophisticated threat landscapes, low market penetration in tier-two and tier-three cities, and limited awareness about cyber insurance coverage benefits.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade