India Data Center Market Size, Share, Trends and Forecast by Application, Type, Component, Size, and Region, 2026-2034

India Data Center Market Size, Share, Trends & Forecast (2026-2034)

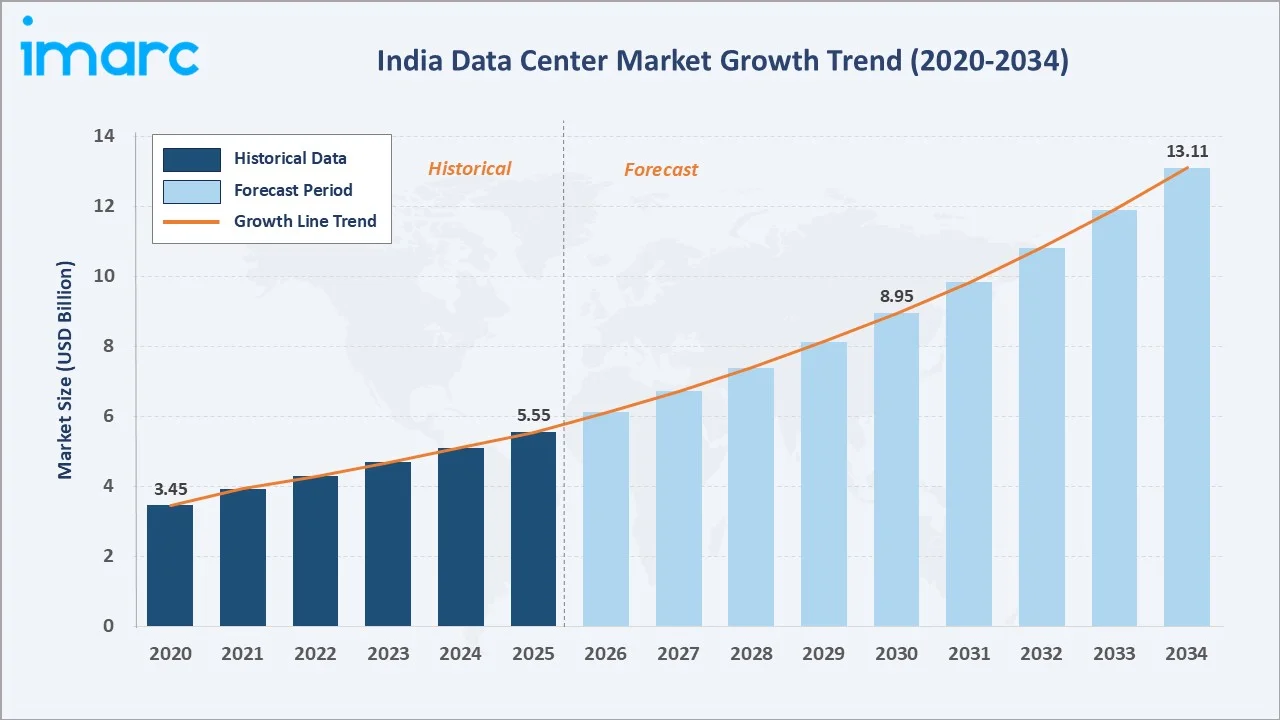

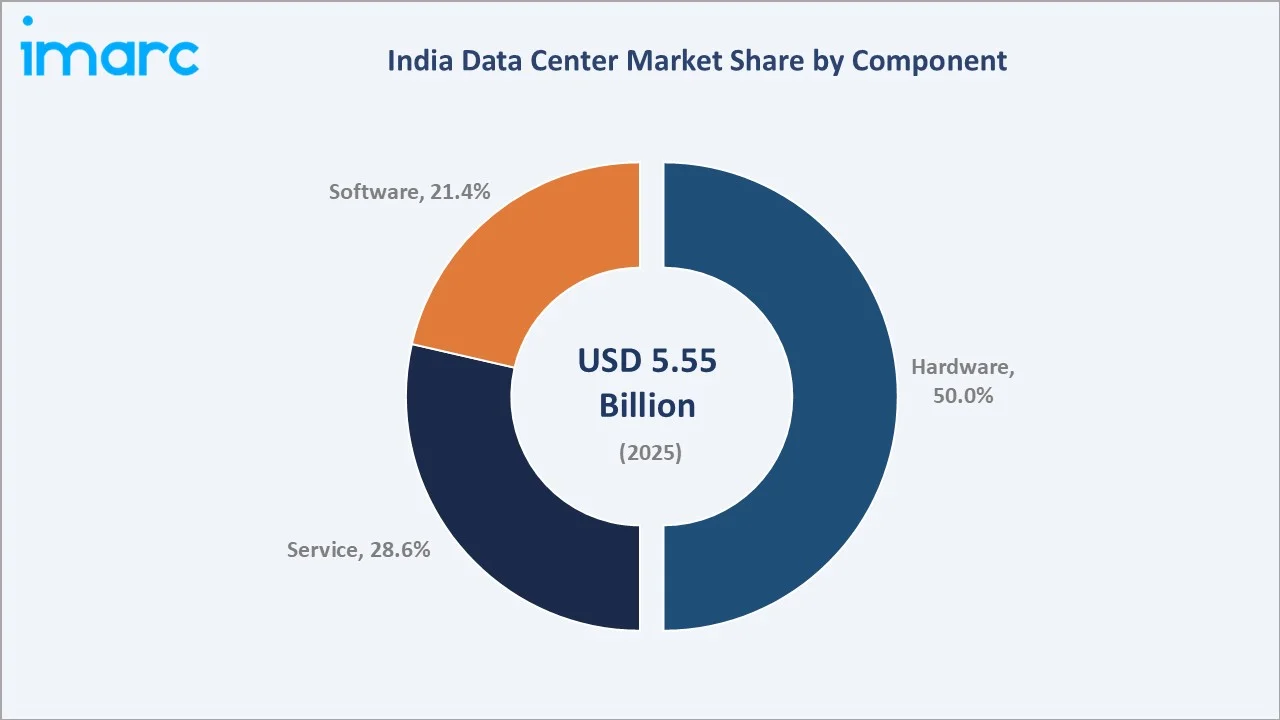

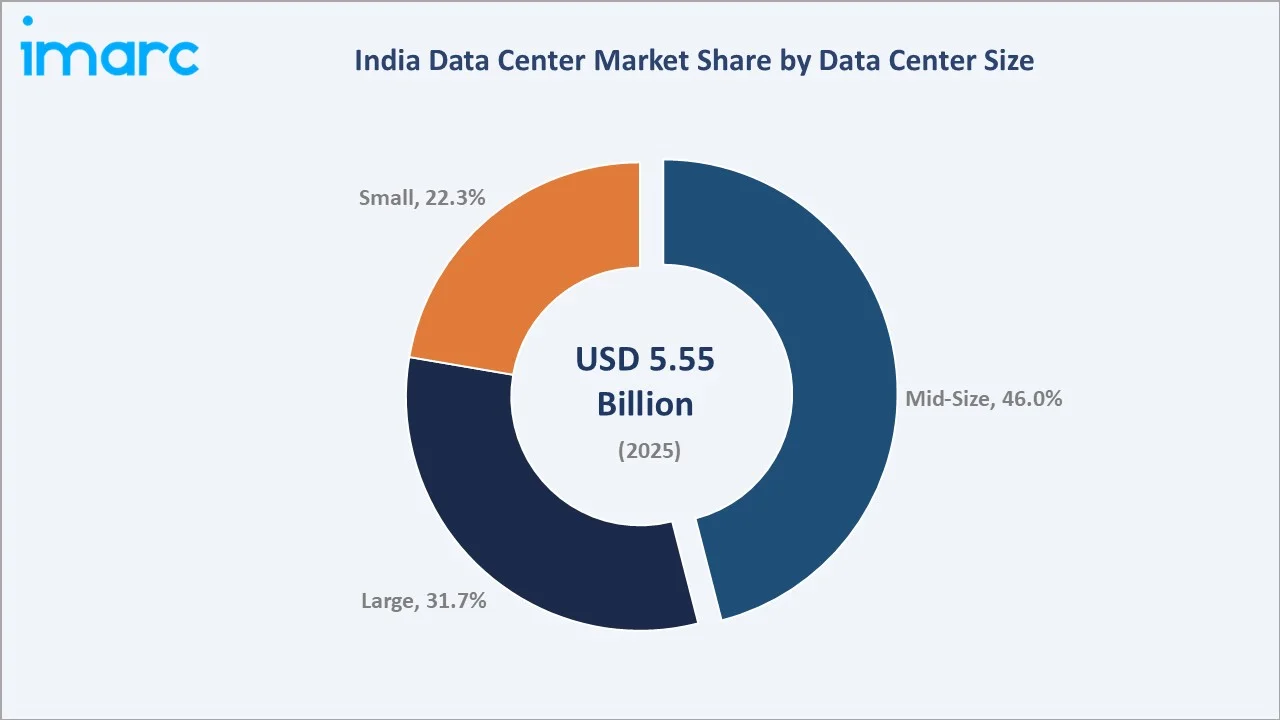

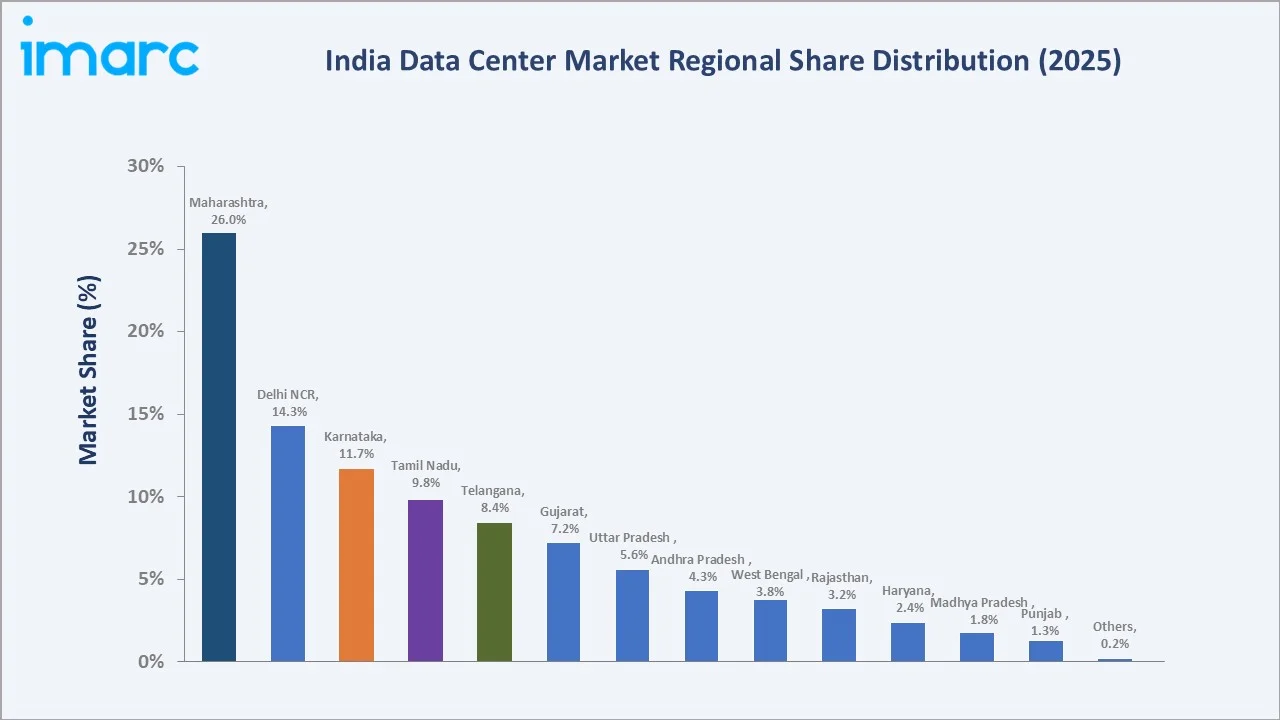

The India data center market size was valued at USD 5.55 Billion in 2025 and is projected to reach USD 13.11 Billion by 2034, exhibiting a CAGR of 10.01% during the forecast period 2026-2034. Rapid digital transformation across enterprises, surging cloud adoption, and escalating AI/ML workload requirements are the primary catalysts driving this growth. Data localisation mandates under India’s Digital Personal Data Protection Act (DPDPA) 2023, combined with government digital infrastructure initiatives such as BharatNet and Smart Cities Mission, are further accelerating data center investment. Hardware leads the component segment with a 50.0% share in 2025, while Mid-Size Data Centers dominate the size segment at 46.0%. Maharashtra commands the largest regional share at 26.0%, anchored by Mumbai’s position as India’s premier financial and digital connectivity hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.55 Billion |

|

Forecast Market Size (2034) |

USD 13.11 Billion |

|

CAGR (2026-2034) |

10.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Maharashtra (26.0% share, 2025) |

|

Fastest Growing Region |

Telangana & Uttar Pradesh |

|

Leading Component Segment |

Hardware (50.0%, 2025) |

|

Leading Size Segment |

Mid-Size Data Center (46.0%, 2025) |

The India data center market growth trajectory from 2020 through 2034 reflects a consistent historical expansion base, transitioning into a sustained forecast growth curve powered by enterprise cloud adoption, AI infrastructure investments, and government-mandated data localisation across regulated sectors, including BFSI, healthcare, and telecommunications.

To get more information on this market, Request Sample

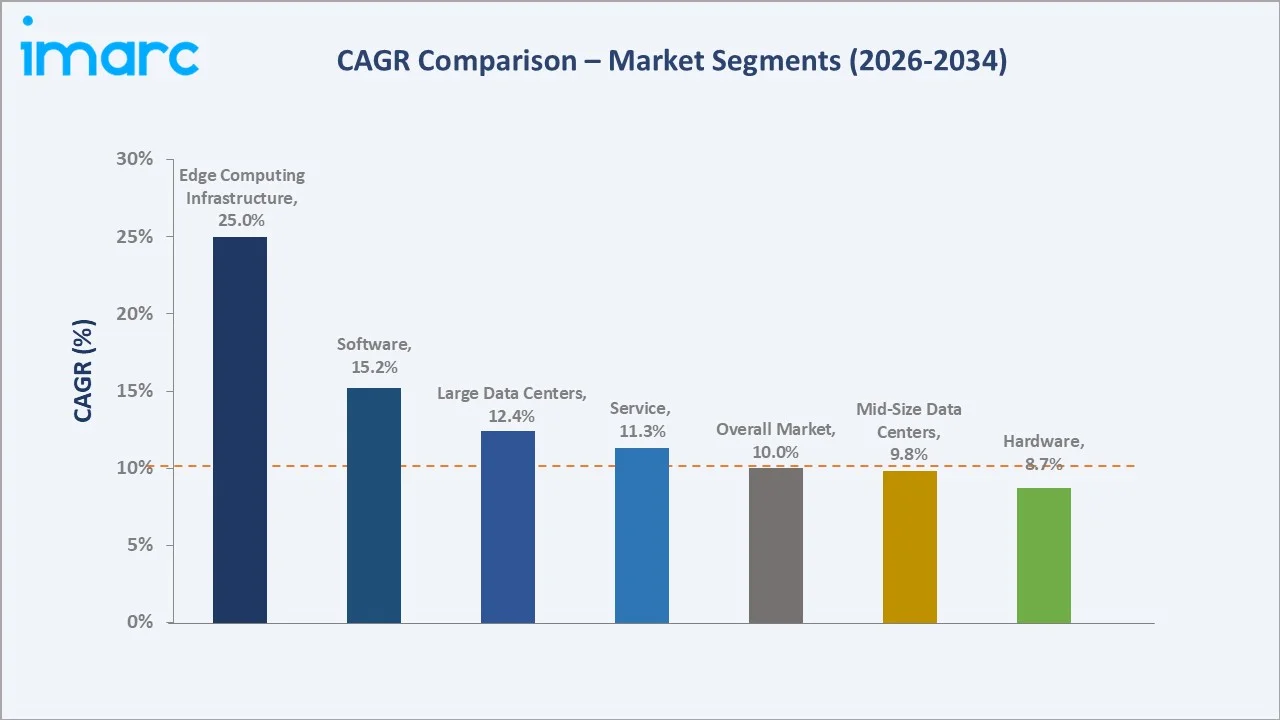

Segment-level CAGR comparisons highlight Edge Computing Infrastructure and Software/AI Management platforms as the two fastest-growing technology sub-categories within the India data center industry analysis through 2034, while the overall market sustains a steady 10.01% CAGR throughout the forecast horizon.

Executive Summary

The India data center industry is undergoing a structural transformation, evolving from a cost-efficient hosting destination into a strategically critical digital infrastructure ecosystem. Valued at USD 5.55 Billion in 2025, the market is on course to reach USD 13.11 Billion by 2034 at a 10.01% CAGR.

Hardware accounts for the dominant component share at 50.0% in 2025, anchored by large-scale capital expenditure on servers, GPU clusters, storage arrays, and cooling infrastructure. The service segment at 28.6% benefits from enterprise preference for outsourced colocation and managed services that reduce capital risk and improve uptime guarantees. Software tools – DCIM platforms, virtualisation middleware, and cybersecurity suites – hold a 21.4% share and are the fastest-growing category, driven by AI-embedded operational analytics and ESG reporting requirements.

Maharashtra continues to lead India’s regional landscape with a 26.0% share in 2025, supported by Mumbai’s 14+ submarine cable systems and its status as the country’s financial capital. Delhi NCR at 14.3% benefits from government digital services demand and corporate headquarters concentration, while Karnataka at 11.7% is propelled by Bengaluru’s world-class technology ecosystem. Tamil Nadu (9.8%), Telangana (8.4%), and Gujarat (7.2%) collectively represent a diversifying second tier of regional markets, reshaping India’s geographic data center footprint through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component Segment |

Hardware – 50.0% share (2025) |

|

Second Component Segment |

Service – 28.6% share (2025) |

|

Leading Size Segment |

Mid-Size Data Center – 46.0% share (2025) |

|

Leading Region |

Maharashtra – 26.0% share (2025) |

|

Second Region |

Delhi NCR – 14.3% share (2025) |

|

Top Companies |

Adani Group, Equinix Inc., Bharti Enterprises, Sify Technologies, CtrlS Datacenters Ltd. |

|

Market Opportunity |

AI-ready hyperscale campuses & Tier-II city edge infrastructure |

Key Analytical Observations Supporting the Above Data:

- Hardware’s 50.0% dominance in 2025 reflects intensive capital expenditure on GPU-dense servers, NVMe storage arrays, and liquid-cooled rack infrastructure required for high-performance AI computing environments.

- Mid-Size Data Centers at 46.0% represent the sweet spot for India’s growing enterprise segment, offering scalability without the complexity and capex burden of hyperscale campuses, typically ranging from 500 to 2,000 server racks.

- Software, while at 21.4% share in 2025, is the fastest-growing component category, with AI-powered DCIM platforms, predictive maintenance systems, and automated workload orchestration tools recording double-digit annual growth.

- Maharashtra’s 26.0% share in 2025 is structurally anchored by Mumbai’s 14+ submarine cable landings, government-designated data center zones, and the concentration of India’s financial services sector requiring high-frequency, low-latency data processing.

- India’s DPDPA 2023 and RBI payment data localisation mandates are creating structural, policy-driven demand for sovereign data infrastructure across regulated sectors, particularly BFSI and healthcare.

India Data Center Market Overview

A data center is a centralized facility housing compute, storage, and networking infrastructure that underpins IT operations, cloud services, and digital delivery. India’s ecosystem includes hyperscale campuses, colocation facilities, enterprise-owned data centers, edge nodes, and government infrastructure, supporting applications across telecom, BFSI, healthcare, e-commerce, media, and public digital platforms.

Growth is driven by sustained economic expansion, rapid MSME digitization, and large-scale government initiatives in connectivity, digital services, and AI. The ecosystem operates across five layers: hardware supply, core infrastructure, software platforms, connectivity, and end-user service delivery. Rising data generation continues to necessitate significant capacity expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

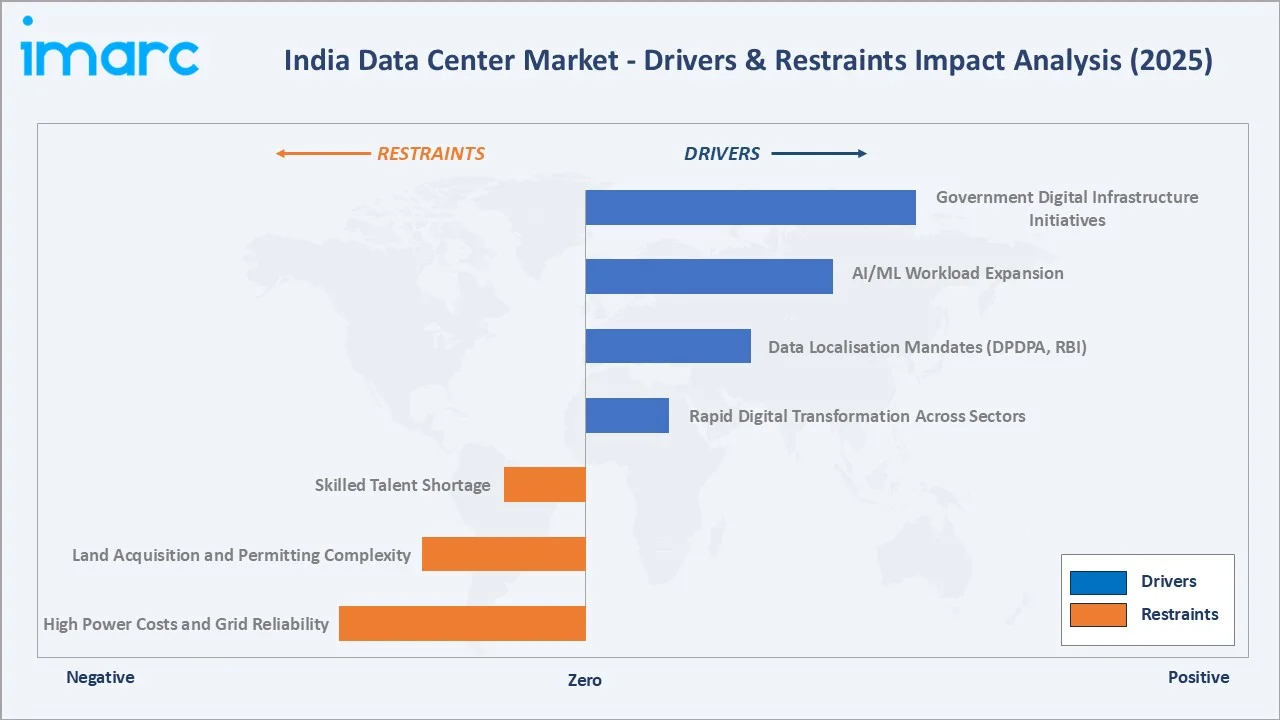

Market Drivers

- Rapid Digital Transformation Across Sectors: Rapid cloud adoption across BFSI, healthcare, retail, and manufacturing is accelerating data generation and driving sustained demand for colocation and hyperscale infrastructure. India’s large and expanding internet user base reinforces this growth trajectory.

- Data Localisation Mandates: Regulatory frameworks such as the Digital Personal Data Protection Act (DPDPA) and RBI guidelines are mandating domestic data storage, creating structural demand across financial services, healthcare, and government sectors.

- AI/ML Workload Expansion: Expansion of AI use cases—including large language models, real-time analytics, and computer vision—is driving high-density compute requirements and large-scale investments in GPU-enabled data centers.

- Government Digital Infrastructure Initiatives: National programs in connectivity, smart infrastructure, and AI are accelerating demand for distributed data center capacity beyond primary metro markets.

Market Restraints

- High Power Costs and Grid Reliability: Energy remains the largest operating expense, with inconsistent grid reliability increasing dependence on backup systems and raising the total cost of ownership.

- Land Acquisition and Permitting Complexity: Limited availability of suitable land with reliable power access near key hubs, coupled with lengthy approval timelines, delays project execution.

- Skilled Talent Shortage: Shortage of skilled professionals in data center operations, networking, and cybersecurity continues to drive higher staffing costs.

Market Opportunities

- Tier-II City Expansion: Emerging cities are gaining traction due to lower land costs, improving infrastructure, and supportive state policies, enabling geographic diversification.

- Green Data Center Development: Growing enterprise focus on sustainability is driving demand for renewable-powered facilities, enabling premium pricing and long-term cost efficiencies.

- Edge Computing Infrastructure Build-out: Rising adoption of 5G, IoT, and latency-sensitive applications is creating strong demand for distributed edge data center networks.

Market Challenges

- Cybersecurity and Regulatory Compliance: Increasing regulatory requirements and stricter incident reporting norms are driving continuous investment in security infrastructure.

- Cooling Technology Transition: Shift toward advanced cooling solutions for high-density AI workloads requires significant capital and operational adaptation.

- State-Level Policy Fragmentation: Variability in state-level regulations on power, land, and approvals adds complexity and execution risk for multi-location deployments.

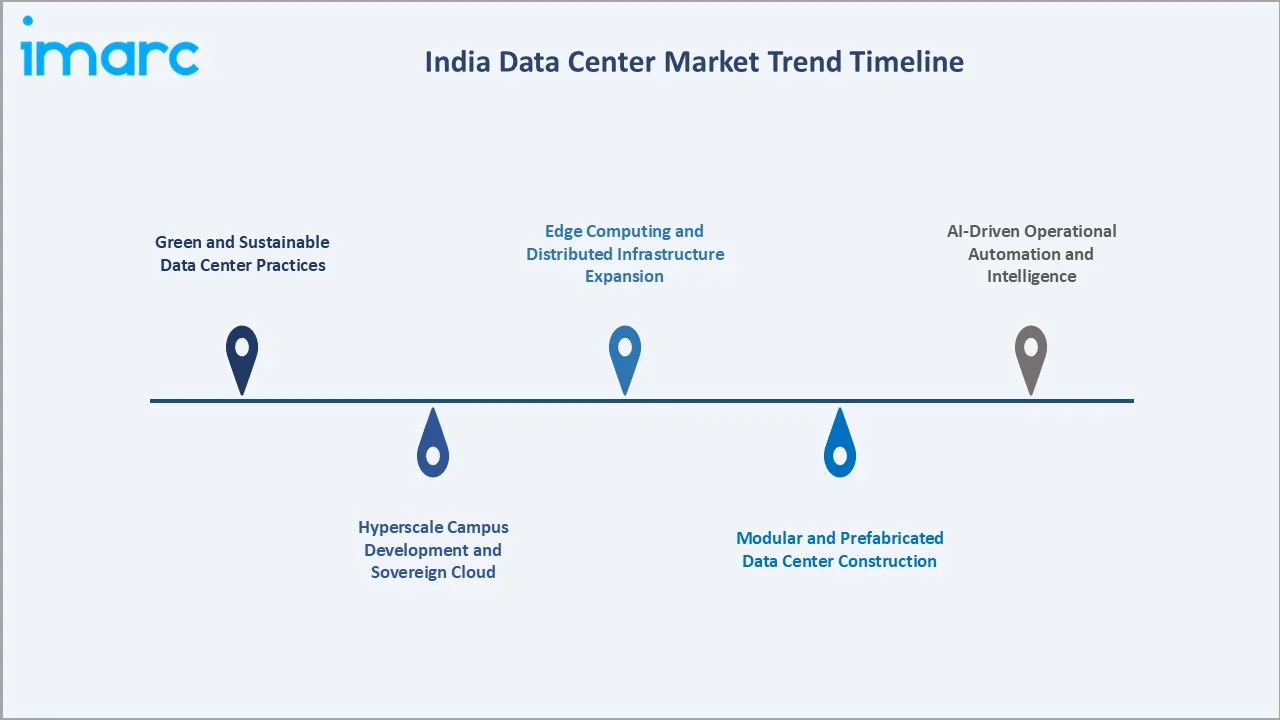

Emerging Market Trends

1. Green and Sustainable Data Center Practices

Sustainability is evolving into a core economic driver, with operators prioritising energy efficiency and decarbonisation. Advanced cooling technologies—including liquid, free-air, and adiabatic systems—are enabling lower PUE levels, while renewable energy integration is improving cost predictability and ESG positioning. Large-scale captive renewable deployments highlight the commercial viability of green data center operations.

2. Edge Computing and Distributed Infrastructure Expansion

The expansion of 5G and IoT ecosystems is accelerating investment in edge infrastructure. Operators are deploying smaller, distributed facilities in non-metro locations to support low-latency, real-time applications such as industrial automation, telemedicine, and smart city systems.

3. AI-Driven Operational Automation and Intelligence

AI and machine learning are transforming data center management through predictive maintenance, intelligent workload allocation, and real-time thermal optimisation. These capabilities are improving uptime, reducing energy consumption, and enhancing operational efficiency, emerging as key competitive differentiators.

4. Hyperscale Campus Development and Sovereign Cloud Infrastructure

Global cloud providers are investing in large-scale, India-based infrastructure to support data sovereignty requirements and rising enterprise cloud adoption. These hyperscale developments are driving ecosystem growth, including power infrastructure upgrades, land development, and talent concentration in key regions.

5. Modular and Prefabricated Data Center Construction

Prefabricated modular data centers are gaining traction due to faster deployment timelines and scalability. Off-site manufacturing of standardised modules enables phased capacity expansion, reduces execution risk, and aligns capital deployment more closely with demand growth.

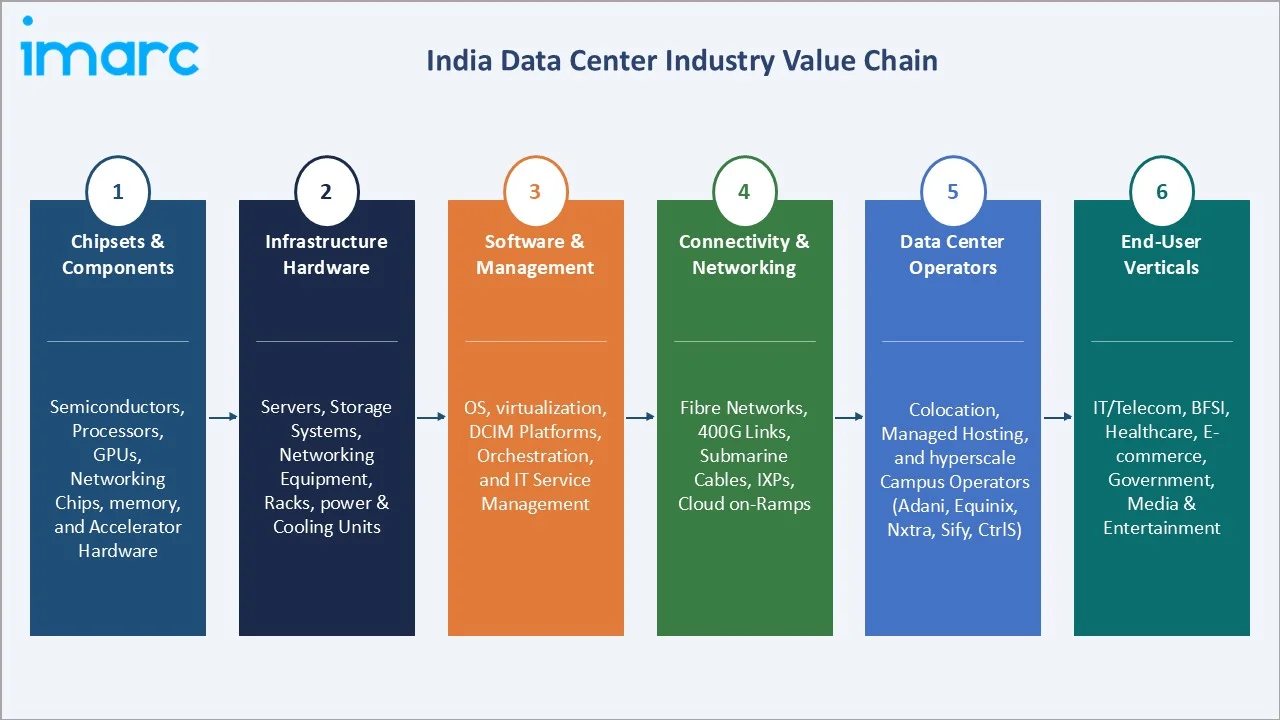

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Chipsets & Components |

The foundational layer of the data center ecosystem encompasses the design and manufacture of semiconductors, processors, GPUs, and networking chips. |

|

Infrastructure Hardware |

Covers the physical build-out of data centers — servers, storage systems, networking equipment, racks, and power/cooling units. |

|

Software & Management |

Includes the operating systems, virtualization platforms, DCIM (Data Center Infrastructure Management) tools, and IT service management solutions that orchestrate, monitor, and optimize data center operations. |

|

Data Center Operators |

Companies that own, build, and operate physical data center facilities, offering colocation, managed hosting, or hyperscale services to enterprise and cloud clients. |

|

End-User Verticals |

IT/Telecom, BFSI, Healthcare, E-commerce, Government |

Data center operators occupy the highest visible strategic position in India’s market, integrating upstream hardware, software, and connectivity inputs into end-to-end infrastructure services for enterprise tenants. However, this position faces competitive pressure from two directions: global hyperscalers internalising more infrastructure operations within their owned campuses, and enterprise customers adopting hybrid multicloud architectures that distribute workloads across multiple operator and public cloud environments simultaneously.

Technology Landscape in the India Data Center Industry

Power Infrastructure: UPS, Generators, and Renewable Integration

Indian data centers are built on N+1 or 2N redundancy architectures to deliver carrier-grade uptime. Core systems include UPS, diesel generators, and automatic transfer switches. The technology stack is evolving toward lithium-ion battery storage and integrated renewable energy solutions, improving space efficiency, lifecycle performance, and energy cost stability while supporting decarbonisation goals.

Cooling Architecture: Air, Liquid, and Immersion Technologies

Rising rack densities—driven by AI and high-performance computing—are accelerating the shift beyond traditional air-based cooling. Operators are deploying containment systems, rear-door heat exchangers, and direct liquid cooling, with early adoption of immersion cooling in high-density environments. These technologies significantly enhance thermal efficiency and reduce overall energy consumption.

Connectivity and Network Architecture: Fibre, 400G, and Cloud On-Ramps

Data center networks are transitioning to high-capacity, spine-leaf architectures to support bandwidth-intensive workloads. Carrier-neutral facilities are integrating Internet exchange points and enabling direct cloud connectivity, reducing latency and improving performance for enterprise and cloud workloads.

Security Architecture: Physical and Cyber Convergence

Security frameworks are increasingly integrated across physical and digital layers. Facilities deploy biometric access controls, continuous surveillance, and controlled entry systems alongside advanced cybersecurity measures such as zero-trust access, threat mitigation, and centralized monitoring platforms, ensuring compliance and operational resilience.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

IT and Telecom |

47.0% |

2025 |

|

Type |

Colocation Data Centers |

61.0% |

2025 |

|

Component |

Hardware |

50.0% |

2025 |

|

Sizes |

Mid-Size Data Center |

46.0% |

2025 |

|

Region |

Maharashtra |

26.0% |

2025 |

By Component

Hardware dominates due to high capex in servers, GPU clusters, storage, networking, and cooling systems. The shift to AI-driven workloads is sharply increasing spend, with rack densities rising from 8–12 kW to 40–80 kW, requiring significantly higher investment in power and cooling infrastructure. Ongoing hyperscaler investments in India are further accelerating hardware demand.

To access detailed market analysis, Request Sample

The Service segment at 28.6% is anchored by the colocation sub-category, capturing over 61% of overall market revenue from data center types in 2025. Enterprise preference for outsourced infrastructure management – converting fixed capex to variable opex – is sustaining strong colocation demand. Software, the fastest-growing segment at 21.4%, is propelled by AI-embedded DCIM tools, predictive failure analytics, and automated compliance reporting that collectively enable 20–25% operational efficiency gains versus manual management approaches.

By Size

Data centers in India are classified into Small (below 5,000 sq. ft.), Mid-Size (5,000–50,000 sq. ft.), and Large (above 50,000 sq. ft.) facility categories. Mid-Size data centers dominate with a 46.0% share in 2025, while Large facilities account for 31.7%, and Small data centers represent 22.3%.

Mid-Size Data Centers command the dominant position by offering enterprises an ideal combination of scalability, operational manageability, and cost efficiency. Facilities in this tier typically support 500–2,000 server racks and benefit from modular expansion capabilities aligned with phased IT budget cycles. Their 18–24 month deployment timelines versus 36+ months for hyperscale campuses make them particularly attractive for operators seeking to rapidly respond to demand signals. Large Data Centers anchored in Maharashtra, Karnataka, and Delhi NCR are primarily operated by hyperscale cloud providers and major telecom carriers, with committed investment pipelines driving the highest absolute growth through 2034. Small Data Centers at 22.3% serve edge computing and enterprise branch requirements, with deployment increasingly concentrated in Tier-II cities as part of 5G-enabled distributed computing strategies.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Maharashtra |

26.0% |

Mumbai connectivity hub, submarine cable landings, and the financial sector demand |

|

Delhi NCR |

14.3% |

Government IT demand, enterprise headquarters, and BFSI concentration |

|

Karnataka |

11.7% |

Bengaluru technology cluster, startup ecosystem, IT/ITeS anchor tenants |

|

Tamil Nadu |

9.8% |

Chennai port connectivity, automotive & manufacturing digitisation |

|

Telangana |

8.4% |

HITEC City pharma/tech demand, government e-services, renewable energy |

|

Gujarat |

7.2% |

GIFT City fintech zone, industrial digitalisation, port logistics data |

|

Uttar Pradesh |

5.6% |

Government digital services, a rapidly expanding internet user base |

|

Andhra Pradesh |

4.3% |

APSDC incentives, renewable energy availability, and coastal connectivity |

|

West Bengal |

3.8% |

Kolkata, the eastern gateway, BFSI digitisation, e-government services |

|

Rajasthan |

3.2% |

Solar energy surplus, data center policy incentives, and smart city projects |

|

Haryana |

2.4% |

NCR proximity, logistics sector digitisation, and manufacturing data needs |

|

Madhya Pradesh |

1.8% |

Central India connectivity node, government cloud requirements |

|

Punjab |

1.3% |

Agriculture tech, cross-border trade data, and retail digitisation |

|

Others |

0.2% |

Emerging micro-markets in the North-East and Hill States |

Maharashtra commands a 26.0% share of India’s data center market in 2025, the country’s dominant data center geography. Mumbai’s structural advantages are multi-dimensional: 14+ international submarine cable landings establish it as the primary internet gateway, government-designated data center zones offer streamlined clearances, and the concentration of India’s financial services, media, and technology sectors provides a deep anchor tenant base.

Delhi NCR commands a 14.3% share, benefitting from proximity to central government IT departments, a dense financial services ecosystem, and the largest corporate headquarters concentration outside Mumbai. Noida and Greater Noida corridors have emerged as preferred data center development zones, offering competitive real estate pricing and dedicated power feeder availability. The region is anchored by strong demand from government digital missions, including the National e-Governance Plan and the Ministry of Electronics and IT’s cloud adoption mandates for central government departments.

Karnataka at 11.7% derives its market position from Bengaluru’s globally recognised technology ecosystem, home to over 5,000 technology companies and more than 600 MNC R&D centres. Tamil Nadu (9.8%) and Telangana (8.4%) represent the fastest-growing secondary markets, each benefiting from proactive state investment incentive frameworks and improving power infrastructure that are positioning them to capture a greater share of new capacity additions through 2034.

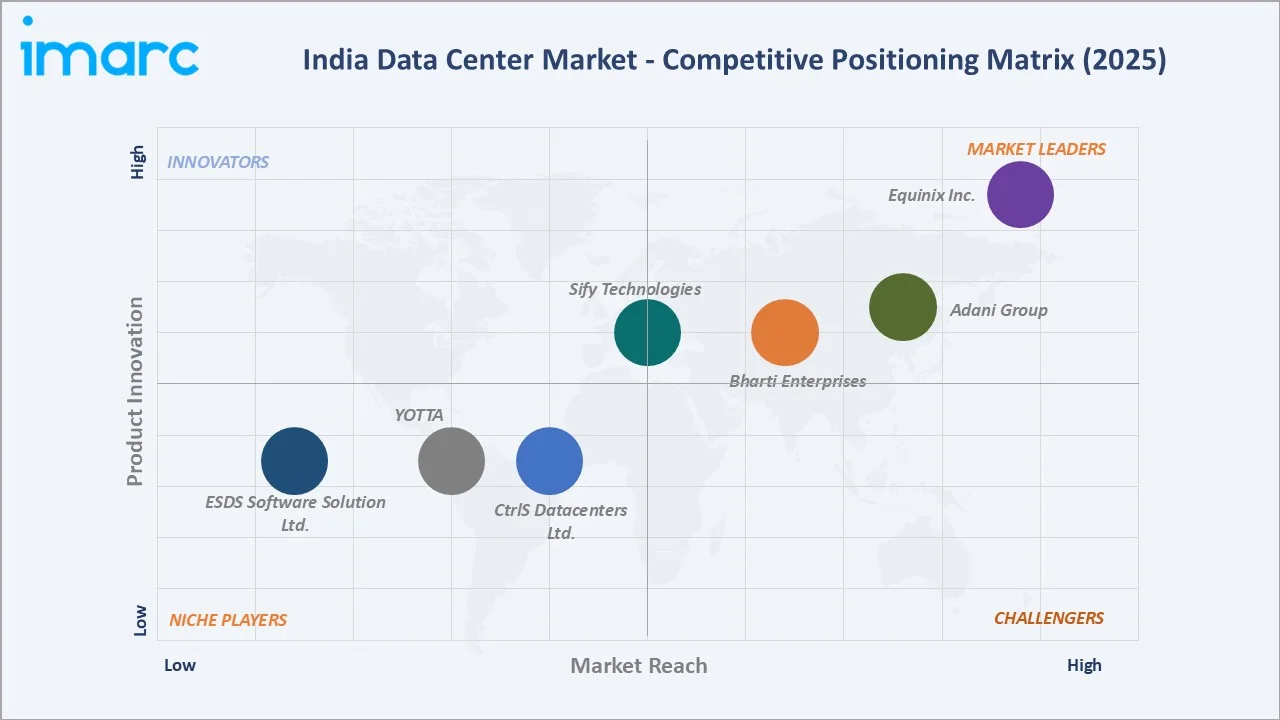

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Adani Group |

AdaniConneX |

Leader |

Hyperscale pipeline, renewable energy, 8-city footprint |

|

Equinix Inc. |

IBX Centers |

Leader |

Carrier-neutral, global interconnection, Mumbai IBX |

|

Bharti Enterprises |

Nxtra |

Leader |

Pan-India 11+120 edge centers, strong enterprise base |

|

Sify Technologies |

Sify Data Centers |

Leader |

USD 5B AI expansion plan, 10+ campus locations |

|

CtrlS Datacenters Ltd. |

CtrlS |

Challenger |

Tier IV certified, BFSI/Govt focus, 3 Hyperscale Parks |

|

YOTTA |

Yotta NM1 |

Challenger |

9,000-rack NM1 campus, modular hyperscale design |

|

ESDS Software Solution Ltd. |

ESDS |

Emerging |

Sovereign cloud emphasis, NxtGen platform, SME focus |

The India data center competitive landscape is characterised by a moderately fragmented structure at the mid-market colocation tier, with growing concentration among hyperscale-capable operators. The top five operators – Adani Group, Equinix Inc., Bharti Enterprises, Sify Technologies, CtrlS Datacenters Ltd.– collectively account for approximately 55–60% of total installed IT capacity in 2025.

Key Company Profiles

Adani Group

Adani Group is establishing itself as India’s largest hyperscale data center developer through its AdaniConneX joint venture, targeting 1 GW+ of IT capacity across 8 Indian cities.

- Product & Platform Portfolio: Hyperscale campuses in Mumbai, Chennai, Hyderabad, Noida, Pune, Bengaluru, Kolkata, and Ahmedabad; 100% renewable energy commitment via group-owned solar and wind projects; dedicated 220 kV power substations for hyperscale tenants.

- Recent Developments: In February 2021, Adani Enterprises and EdgeConneX announced the establishment of a 50:50 joint venture.

- Strategic Focus: Adani’s strategy targets hyperscale cloud providers requiring sovereign Indian data infrastructure, leveraging the group’s integrated industrial capabilities to offer turnkey campus solutions from land development through power delivery and network connectivity at total costs structurally below international operators.

Equinix Inc.

Equinix is a carrier-neutral data center and interconnection services, operating 260+ IBX data centers across 72 cities globally.

- Product & Platform Portfolio: IBX campuses MB1–MB5 in Mumbai; Equinix Fabric for cloud on-ramp services; Equinix Metal for bare-metal infrastructure; Internet Exchange at Mumbai for peer-to-peer routing optimisation across India’s digital economy.

- Recent Developments: In November 2024, Equinix partnered with CleanMax to develop a 33 MW captive solar and wind power project in Maharashtra, providing renewable energy to decarbonise its Mumbai data centers. The company also announced expansion plans for MB6 in Navi Mumbai, adding 5 MW of colocation capacity.

- Strategic Focus: Equinix’s India strategy centres on interconnection density – building the richest ecosystem of cloud providers, content networks, and enterprise tenants at its Mumbai campus to create network effects that reduce switching costs and sustain premium pricing for colocation and connectivity services.

Sify Technologies

Sify Technologies is India’s largest domestic data center and IT services company, operating campuses across Mumbai, Chennai, Noida, Bengaluru, Hyderabad, Kolkata, Pune, and Nagpur.

- Product & Platform Portfolio: 10+ campus data centers; Sify Cloud (public, private, and hybrid); managed security services; enterprise network services; AI inference data center programme targeting 20 secondary cities, including Jaipur, Lucknow, Kochi, and Indore.

- Recent Developments: In January 2025, Sify announced its USD 5 billion investment programme to establish AI inference data centers across secondary cities, positioning the company to capture enterprise AI computing demand outside primary metro markets where real estate and power costs are structurally lower.

- Strategic Focus: Sify’s strategy differentiates through geographic breadth and service integration – combining data center colocation, managed IT services, cloud, and network connectivity into integrated enterprise outsourcing contracts that provide higher revenue per customer and stronger switching barriers than colocation-only competitors.

Market Concentration Analysis

The India data center market exhibits a dual-tier concentration structure. At the premium hyperscale and carrier-neutral tier, the top five operators – Adani Group, Equinix Inc., Bharti Enterprises, Sify Technologies, CtrlS Datacenters Ltd. – collectively account for approximately 55–60% of total installed IT capacity in 2025, reflecting the capital barriers required for multi-hundred-megawatt campus development that limit market entry at this tier.

Simultaneously, the mid-market colocation segment remains notably fragmented, with over 30 active operators competing for enterprise and SME tenants in primary and secondary metro markets. This fragmentation creates conditions for consolidation activity through 2034 – smaller regional operators lacking the capital for AI-ready infrastructure upgrades, renewable energy procurement, and certification maintenance are likely M&A targets for larger platform operators seeking to extend geographic coverage without greenfield development lead times.

Investment & Growth Opportunities

Fastest-Growing Segments

Edge computing infrastructure is emerging as the fastest-growing segment, driven by 5G rollout and increasing IoT adoption requiring low-latency processing. This is followed by rapid growth in AI/ML infrastructure, where demand for GPU-dense environments is rising as enterprises scale generative AI and real-time analytics use cases. In parallel, software and management platforms are expanding steadily, supported by the adoption of AI-enabled DCIM tools and automation solutions that enhance operational efficiency.

Emerging Market Expansion

Tier-II cities represent a major greenfield opportunity, offering lower land costs, improved power infrastructure, and strong policy support from state governments. These locations are increasingly attracting data center investments as operators diversify beyond primary metros. At the same time, green data centers powered by renewable energy are gaining traction, enabling premium pricing and aligning with enterprise sustainability goals, particularly among global tenants.

Venture & Private Investment Trends

The sector continues to attract strong private equity and strategic investment, particularly in hyperscale and colocation platforms through joint ventures and long-term infrastructure partnerships. In addition, capital is increasingly flowing into adjacent ecosystem layers such as AI infrastructure software, edge computing platforms, and cybersecurity solutions, reflecting a broader shift toward integrated digital infrastructure investment.

Future Market Outlook (2026-2034)

The India data center market is projected to sustain robust double-digit growth through 2034, expanding from USD 5.55 Billion in 2025 to USD 13.11 Billion by 2034 at a CAGR of 10.01% – representing a near-tripling of market value underpinned by converging structural forces that are unlikely to reverse over the forecast horizon.

Three technology discontinuities are most likely to reshape India’s data center landscape through 2034. First, AI infrastructure mainstreaming will drive a wholesale upgrade cycle for high-density GPU rack installations, liquid cooling infrastructure, and AI-optimised network fabrics across the installed base. This infrastructure refresh represents a multi-billion-dollar capex opportunity for hardware vendors, EPC contractors, and facility operators. Second, sovereign cloud mandates from regulated sectors will drive a material increase in dedicated, compliance-certified facility capacity, creating a structurally different demand category with higher barriers to entry, longer contract terms, and premium pricing.

By 2034, India’s data center market is forecast to feature a more concentrated competitive landscape of 10–12 platform-scale operators. Installed IT power capacity nationally is projected to exceed 3 GW by 2030 and approach 5 GW by 2034, positioning India as one of the top five global data center markets by capacity – a structural shift driven by the irreversible digitalisation of the world’s most populous nation.

Research Methodology

Primary Research

Primary research included 50+ structured interviews conducted in 2024–2025 with data center operators, enterprise IT leaders, colocation providers, investors, regulators, and academic experts. Insights were used to validate market sizing, segmentation, technology adoption trends, and competitive positioning.

Secondary Research

Secondary sources included MeitY Data Centre Policy documents, TRAI telecom infrastructure reports, RBI digital payments data, ICRA India data center capacity analyses, JLL India real estate reports, company annual reports and investor presentations (Equinix, Nxtra Data, Sify Technologies, CTRLS), IDC India cloud market reports, Cushman & Wakefield India data center market reports, and trade publications including Data Center Dynamics, DQ India, and Network World India.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up forecasting methodologies. The bottom-up model aggregates capacity data from individual operators and facility development pipelines. The top-down model applies macroeconomic regression analysis incorporating GDP growth, internet penetration rates, cloud adoption indices, and FDI inflows into the technology sector. Scenario analysis incorporating base, optimistic, and conservative growth cases accounts for macroeconomic uncertainty, regulatory evolution, and supply-side constraints. All estimates underwent rigorous triangulation across primary research, secondary data sources, and expert panel validation.

India Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Middle East Tire Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Banking Financial Services & Insurance (BFSI), Government, IT and Telecom, Media, Retail, Manufacturing, Others |

| Types Covered | Enterprise Data Centers, Colocation Data Centers, Edge Data Centers, Hyperscale Data Centers |

| Components Covered | Hardware, Software, Service |

| Sizes Covered | Small Data Center, Mid-Size Data Center, Large Data Center |

| Regions Covered | Maharashtra, Tamil Nadu, Uttar Pradesh, Gujarat, Karnataka, West Bengal, Rajasthan, Andhra Pradesh, Telangana, Madhya Pradesh, Delhi NCR, Punjab, Haryana, Others |

| Companies Covered | Adani Group, Equinix Inc., Bharti Enterprises, Sify Technologies, CtrlS Datacenters Ltd., YOTTA, ESDS Software Solution Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Data Center Market Report

The India data center market was valued at USD 5.55 Billion in 2025, driven by rapid digital transformation, cloud adoption, and growing enterprise demand for data infrastructure across all major industry verticals.

The market is projected to reach USD 13.11 Billion by 2034, growing at a CAGR of 10.01% during 2026-2034, driven by AI infrastructure investment, data localisation mandates, and hyperscale campus development by global cloud providers.

Hardware leads with a 50.0% share in 2025.

Mid-Size Data Centers dominate with a 46.0% share in 2025.

Maharashtra leads with a 26.0% share in 2025.

Key drivers include digital transformation, cloud adoption, DPDPA 2023 data localisation mandates, AI/ML workload growth, and government digital infrastructure programs.

Leading operators include Adani Group, Equinix Inc., Bharti Enterprises, Sify Technologies, CtrlS Datacenters Ltd., YOTTA, and ESDS Software Solution Ltd.

Edge computing is expanding distributed processing capacity to serve 5G and IoT applications. India’s edge data center capacity is forecast to triple from 60–70 MW in 2024 to 200–210 MW by 2027 per ICRA, supporting smart manufacturing, telemedicine, and autonomous logistics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)