India Dental Implants Market Size, Share, Trends and Forecast by Material, Product, End Use, and Region, 2026-2034

India Dental Implants Market Summary:

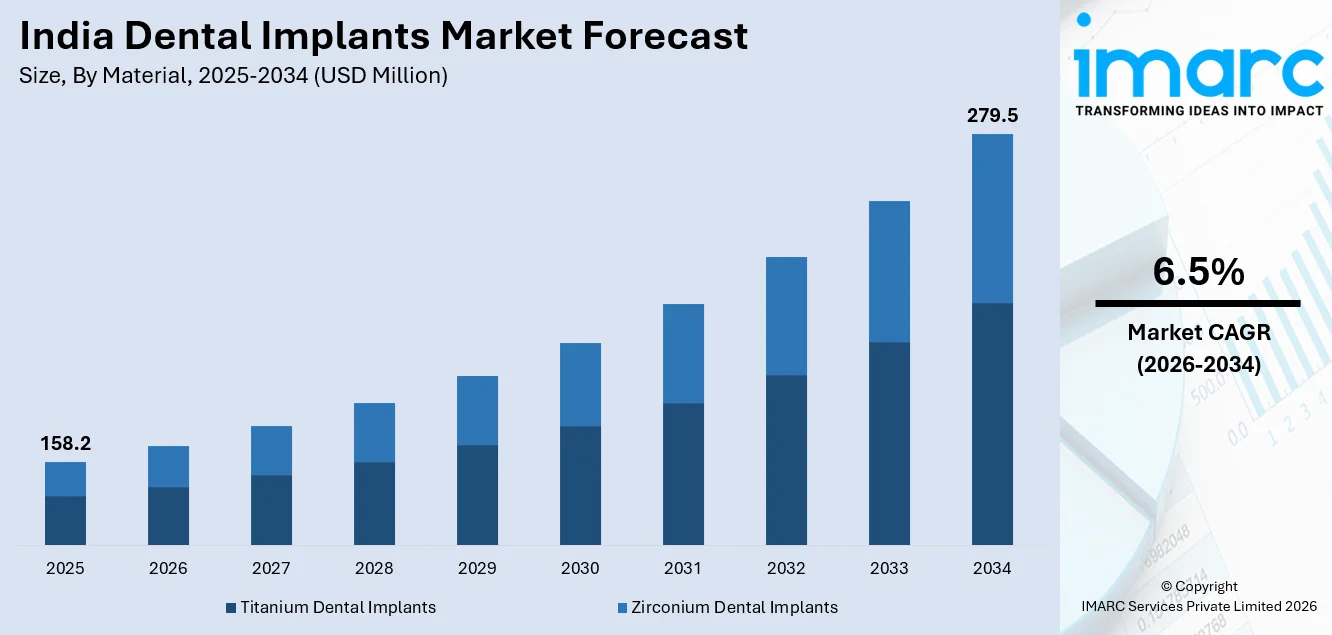

The India dental implants market size was valued at USD 158.2 Million in 2025 and is projected to reach USD 279.5 Million by 2034, growing at a compound annual growth rate of 6.5% from 2026-2034.

The Indian dental implants market is growing steadily, driven by increased awareness of oral health, rising levels of disposable income, and the growing geriatric population, which is experiencing an increase in restorative dental requirements. The India dental implants market share is being strengthened by the latest advancements in dental implants technology, developments in dental infrastructure, and the success of dental tourism in the country. Increased acceptance of cosmetic dental procedures is widening the support base for the dental implants market in India.

Key Takeaways and Insights:

- By Material: Titanium dental implants dominate the market with a share of 70% in 2025, driven by their superior biocompatibility, proven osseointegration performance, and wide clinical adoption across dental practices throughout the country.

- By Product: Endosteal implants lead the market with a share of 64% in 2025, owing to their versatility, high success rates, and suitability for the majority of patients requiring single or multiple tooth replacement solutions.

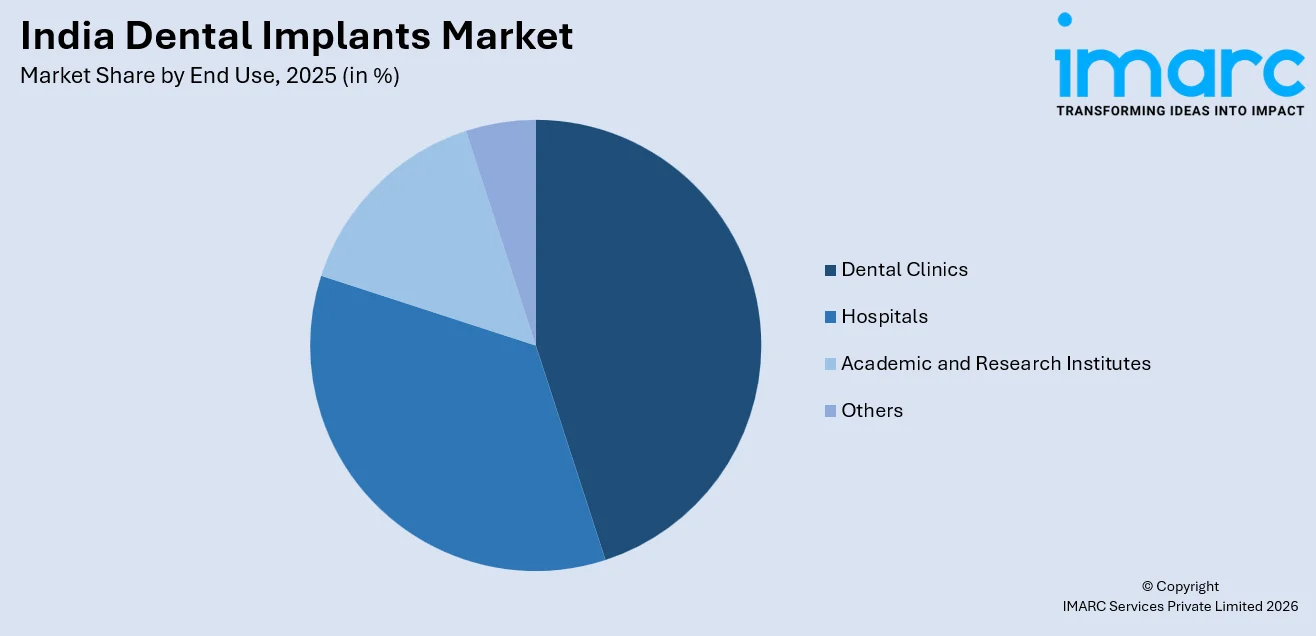

- By End Use: Dental clinics hold the largest share of 45% in 2025, reflecting patient preference for specialized, cost-effective, and personalized dental care in a focused clinical environment.

- Key Players: The India dental implants market features a competitive mix of global multinational corporations and regional manufacturers offering diverse implant solutions across premium and non-premium segments, catering to India's broad and price-sensitive patient base.

To get more information on this market Request Sample

India's dental implants market is positioned for sustained long-term growth, underpinned by several converging structural forces. A rapidly aging population coupled with a high prevalence of tooth loss and periodontal disease creates substantial and recurring demand for implant-based restorative treatments. Rising disposable incomes have made dental procedures increasingly accessible to urban and semi-urban populations who previously relied on conventional prosthetics. In September 2025, Osstem Implant expanded its clinical education and training initiatives in India, with over 10,466 Indian dentists trained through its implant education programs and 1,249 completing courses in 2024 alone. These programs strengthen clinical expertise and improve access to modern implant treatments nationwide. The country's growing recognition as a destination for affordable, high-quality dental tourism is also amplifying patient volumes. Moreover, expanding dental education programs are producing a larger pool of skilled practitioners, broadening geographic penetration into tier-2 and tier-3 cities. These dynamics collectively reinforce the India dental implants market share position within Asia-Pacific.

India Dental Implants Market Trends:

Rising Adoption of Digital Dentistry Solutions

Digital dentistry is reshaping implant planning and placement practices across India. Computer-aided design and manufacturing tools, combined with three-dimensional imaging technologies, allow clinicians to achieve greater precision during implant positioning and surgical execution. This transition is further reinforced by recent industry developments. In November 2025, Dentalkart launched the Waldent BLZ IntraVue 900 AI intraoral scanner in India, enabling real-time, high-precision digital impressions and seamless CAD/CAM integration for implant planning and restorative workflows. The technology improves scanning accuracy, enhances workflow efficiency, and supports broader adoption of digital implant procedures across modern dental clinics. These advancements minimize procedural errors, reduce chair time, and enhance overall patient outcomes. Growing practitioner familiarity with digital workflows is accelerating adoption across both urban specialty centers and expanding mid-tier dental practices nationwide.

Growing Preference for Minimally Invasive Implant Procedures

Indian patients and clinicians are increasingly favoring minimally invasive implant approaches that limit surgical trauma and support faster post-operative recovery. Techniques such as flapless implant placement and computer-guided surgery enable targeted interventions with minimal disruption to surrounding tissues. In December 2025, Dr. Agravat Dental Clinic in Gujarat launched an AI-enhanced implant program integrating digital 3D planning and flapless, sutureless surgery, improving precision and patient comfort while supporting faster healing. This shift reflects evolving patient expectations prioritizing comfort alongside clinical efficacy. Greater awareness of these refined techniques is widening the appeal of implant therapy across diverse age groups and income segments throughout India.

Expansion of Dental Tourism Fueling Premium Demand

India is increasingly emerging as a preferred dental tourism destination, attracting international patients seeking high-quality implant procedures at significantly lower costs compared to developed markets. This steady inflow of global patients is encouraging dental clinics to upgrade clinical infrastructure, integrate advanced implant technologies, and adopt recognized implant systems. Additionally, providers are enhancing service quality, patient experience, and clinical specialization to align with international standards. Tourism-driven demand is also stimulating investment in equipment and training, creating a reinforcing cycle of quality improvement, competitiveness, and sustained growth across India’s dental implant market.

Market Outlook 2026-2034:

The Indian dental implants market is expected to witness steady growth over the next decade, driven by favorable demographic factors, continued development of healthcare infrastructure, and increasing patient awareness about restorative dental options. Digital dentistry is expected to enter the mainstream, and the price of implants is likely to moderate as local manufacturing capacity increases. The increasing middle class, improved government support for oral health, an expanding dental workforce, and acceptance of cosmetic dentistry are expected to drive the market. The market generated a revenue of USD 158.2 Million in 2025 and is projected to reach a revenue of USD 279.5 Million by 2034, growing at a compound annual growth rate of 6.5% from 2026-2034.

India Dental Implants Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Material |

Titanium Dental Implants |

70% |

|

Product |

Endosteal Implants |

64% |

|

End Use |

Dental Clinics |

45% |

Material Insights:

- Titanium Dental Implants

- Zirconium Dental Implants

The titanium dental implants dominates with a market share of 70% of the total India dental implants market in 2025.

Titanium dental implants currently have a dominant market in India due to their outstanding biocompatibility and capacity to integrate perfectly with the jawbone through osseointegration. The material's ability to integrate with the jawbone ensures long-term stability and makes titanium the material of choice for dental implants among dental professionals. The material's high tensile strength, resistance to corrosion, and long-standing clinical success over several decades makes it the material of choice among dental professionals due to its ability to provide long-term stability.

The cost-effectiveness of titanium compared to other materials also contributes to its dominance in the dental market in India. The ability to manufacture titanium dental implant components locally has improved, making the material more affordable. Grade 4 and Grade 5 titanium alloys are currently the most preferred due to their optimal strength and weight ratio. Increased patient awareness about the material's strength, low maintenance costs, and long lifespan continues to fuel demand for the material in the Indian dental market.

Product Insights:

- Endosteal Implants

- Subperiosteal Implants

- Transosteal Implants

- Intramucosal Implants

The endosteal implants leads with a share of 64% of the total India dental implants market in 2025.

Endosteal implants represent the most widely adopted implant type across Indian dental practices due to their versatility and superior clinical outcomes. Inserted directly into the jawbone, these implants provide a stable foundation for crowns, bridges, and dentures, accommodating a broad range of patient anatomies. In October 2024, Straumann Group reported strong implantology demand across Asia-Pacific, including India, highlighting rising adoption of its advanced implant systems and digital solutions among dental professionals in the region. Their adaptability to single-tooth replacement as well as more complex full-arch rehabilitation makes them suitable for the majority of implant candidates presenting in clinical settings throughout the country.

The fact that endosteal implant systems are available in the market across different price ranges has made them accessible to both the high-end and budget-conscious patient groups in India. Improvements in surface treatment technologies have ensured faster and more successful osseointegration, thus solidifying their preference in clinical practice. The training facilities for endosteal implant placement are well developed in Indian dental education, thus ensuring a skilled workforce to provide consistent quality results.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Dental Clinics

- Academic and Research Institutes

- Others

The dental clinics dominates with a market share of 45% of the total India dental implants market in 2025.

Dental clinics act as the point of care for implant procedures in India, providing specialized care in a dedicated setting designed for patient comfort and convenience. The lower operational expenses of dental clinics compared to hospitals enable dentists to offer competitive pricing, which suits the cost-conscious patient base in India. The personalized care approach in dental clinics, with shorter appointment intervals and direct interaction between dentists and patients, promotes better acceptance rates for elective care like implants.

The sudden spurt in the number of multi-specialty and single-specialty dental clinics in Indian metros and tier-2 cities is increasing access to implant care. Specialized implant care centers have become important volume contributors, integrating advanced diagnostic tools with skilled implant surgeons. Dental chains and franchises are transforming the dental clinic scenario by standardizing care approaches and enhancing patient trust. Such shifts in the landscape enable sustained volume expansion in the dental clinics market across geographies.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India represents a significant contributor to the dental implants market, anchored by major urban centers including Delhi, Chandigarh, and Lucknow. Rising dental awareness among urban populations, a high concentration of qualified dental professionals, and increasing disposable incomes are driving procedural volumes. Expanding private dental clinic networks and growing patient acceptance of implant-based restorative treatments are collectively supporting steady market growth across this densely populated region.

West and Central India contribute substantially to the national dental implants market, with Mumbai, Pune, and Ahmedabad serving as key commercial and healthcare hubs. Strong private healthcare infrastructure, a growing affluent middle class, and active dental tourism activity underpin robust demand. Rising cosmetic dentistry awareness and increasing penetration of organized dental clinic chains across this region are further accelerating implant procedure adoption among diverse patient demographics.

South India commands a prominent position in the dental implants market, supported by a well-developed healthcare ecosystem, high oral health awareness, and a strong concentration of skilled dental professionals. Cities including Chennai, Bengaluru, and Hyderabad drive significant implant volumes. The region's established reputation in medical and dental tourism, combined with growing demand for premium cosmetic and restorative dental treatments, consistently reinforces South India's leading market contribution nationally.

East India presents an emerging and increasingly relevant opportunity within the dental implants landscape, with Kolkata and Bhubaneswar serving as primary growth centers. Rising urbanization, improving healthcare investments, and expanding organized dental practice networks are gradually unlocking the region's considerable patient base. Growing awareness of oral health and restorative treatment options, supported by increasing disposable incomes among urban populations, is steadily elevating implant procedure adoption across this developing regional market.

Market Dynamics:

Growth Drivers:

Why is the India Dental Implants Market Growing?

Rising Prevalence of Dental Disorders and Tooth Loss

India grapples with a significant burden of dental disorders, including widespread dental caries, periodontal disease, and tooth loss linked to poor dietary habits and limited access to preventive oral care. According to the World Health Organization Global Oral Health Status Report 2022, oral diseases affect nearly 3.5 billion people worldwide, with untreated dental caries in permanent teeth being the most common condition, underscoring the scale of the challenge faced by countries such as India. These conditions create a substantial and persistent pool of potential implant recipients, particularly among the aging population experiencing progressive tooth loss. As awareness of the long-term health consequences of untreated tooth loss grows, more patients are transitioning from conventional dentures and bridges toward permanent, implant-based restorative solutions. Dentists are actively educating patients about the functional and aesthetic advantages of implants, including jawbone preservation and improved quality of life, which is steadily expanding the addressable patient population and reinforcing demand throughout the country.

Expanding Dental Tourism and Cost Competitiveness

India's emergence as a globally recognized dental tourism destination is providing significant impetus to the implants market. The country's ability to offer internationally comparable quality at a fraction of the cost prevalent in Western markets makes it an attractive choice for overseas patients seeking full-arch restorations, single-tooth replacements, and implant-supported prosthetics. This cost competitiveness stems from lower operational overheads, affordable labor, and growing domestic implant manufacturing capacity. In February 2026, Dental Roots expanded its advanced implant services in South Delhi by integrating fully guided surgical workflows using 3D Cone Beam Computed Tomography (CBCT) and digital planning technologies, enabling sub-millimeter precision and improving clinical outcomes for implant procedures. This upgrade highlights how Indian clinics are adopting globally aligned digital implant systems to attract domestic and international patients. The tourism-driven demand not only boosts implant volumes but also creates incentives for broader infrastructure development, benefiting the domestic patient base and reinforcing India's position in the regional dental care ecosystem.

Government Initiatives and Oral Health Policy Support

Government-led initiatives focused on strengthening oral healthcare infrastructure and improving public awareness are contributing meaningfully to market growth. Policies promoting domestic manufacturing of medical devices, including dental implants, are stimulating local production capacity and reducing import dependency. In September 2025, India’s first Dental Technology Innovation Hub was inaugurated at the Maulana Azad Institute of Dental Sciences through collaboration between the Department of Science and Technology and the Indian Council of Medical Research to support indigenous dental technology innovation and reduce reliance on imported dental products. National oral health programs aimed at screening, prevention, and treatment are improving population-level awareness of dental disease, encouraging more individuals to seek professional intervention including restorative procedures. The establishment of dental facilities in government hospitals and community health centers is improving access in previously underserved rural and semi-urban areas. Regulatory frameworks supporting quality standards for dental implant products are building patient and practitioner confidence, creating a conducive environment for sustained market development and responsible adoption of advanced implant solutions.

Market Restraints:

What Challenges the India Dental Implants Market is Facing?

High Procedural Costs Relative to Affordability

Despite declining costs, dental implant procedures remain beyond the financial reach of a large segment of India's population. The comprehensive nature of the treatment, encompassing multiple visits, diagnostic imaging, surgical fees, and prosthetic components, results in cumulative expenses that deter cost-sensitive patients. Limited insurance coverage for dental implants further compounds affordability barriers, restricting adoption primarily to upper- and middle-income urban populations and leaving vast rural and lower-income demographics underserved.

Inadequate Dental Healthcare Infrastructure in Rural Areas

India's dental healthcare infrastructure remains unevenly distributed, with a pronounced concentration of qualified implantologists and advanced equipment in metropolitan and tier-1 cities. Rural and tier-3 regions face significant shortages of trained dental surgeons, sterilization facilities, and post-operative care services necessary for successful implant outcomes. This geographic disparity limits market penetration, creating structural barriers to achieving broad-based demand growth despite considerable untapped patient populations residing in underserved areas across the country.

Limited Awareness and Patient Misconceptions

A substantial proportion of India's dental patients remain unaware of implant-based solutions or hold misconceptions regarding procedural complexity, pain, and recovery duration. Cultural preferences for conventional dentures and bridges, reinforced by cost perceptions and inadequate clinician communication, suppress treatment conversion rates. Overcoming these informational gaps requires sustained patient education efforts by dental professionals and public health organizations, which remain inconsistent in reach and frequency across urban and rural healthcare delivery settings.

Competitive Landscape:

India's dental implants market features a dynamic and increasingly competitive landscape, characterized by the simultaneous presence of established multinational corporations and an expanding cohort of domestic manufacturers. Global players maintain strong positions through recognized brand equity, advanced research and development capabilities, and extensive distribution networks that ensure product availability across metropolitan dental practices. Domestic manufacturers are gaining meaningful ground by offering cost-effective alternatives that meet clinical performance standards, making implant therapy accessible to a broader patient base. The market is further shaped by active distributor networks and dealer partnerships that facilitate last-mile product delivery to practitioners nationwide. Product differentiation strategies, encompassing surface treatment innovations, customizable prosthetic options, and enhanced implant geometries, are key competitive levers. Increasing collaboration between implant manufacturers and dental educational institutions is also strengthening practitioner familiarity and loyalty, reinforcing competitive positioning across premium, mid-range, and economy market segments.

Recent Developments:

- In February 2026, Osstem Implant expanded its digital dentistry footprint in India by distributing advanced intraoral scanners such as the Medit i900 Mobility and digital surgery kits like OneGuide and OneCAS. These solutions improve implant precision, streamline digital workflows, and enhance clinical efficiency, supporting India’s rapidly expanding implant adoption.

India Dental Implants Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Titanium Dental Implants, Zirconium Dental Implants |

| Products Covered | Endosteal Implants, Subperiosteal Implants, Transosteal Implants, Intramucosal Implants |

| End Uses Covered | Hospitals, Dental Clinics, Academic and Research Institutes, Others |

| Regions Covered | North India, West and Central India, East India, South India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Dental Implants Market Research Report and Industry Forecast Report

The India dental implants market size was valued at USD 158.2 Million in 2025.

The India dental implants market is expected to grow at a compound annual growth rate of 6.5% from 2026-2034 to reach USD 279.5 Million by 2034.

Titanium dental implants held the largest market share of 70%, owing to their superior biocompatibility, proven osseointegration performance, and established long-term clinical track record across diverse dental applications.

Key factors driving the India dental implants market include rising prevalence of dental disorders and tooth loss, growing dental tourism, government oral health policy support, increasing disposable incomes, expanding dental infrastructure, and the growing adoption of advanced digital dentistry technologies nationwide.

Major challenges include high procedural costs limiting affordability for large population segments, inadequate dental healthcare infrastructure in rural and semi-urban areas, limited insurance coverage for implant procedures, and insufficient patient awareness and persistent misconceptions about implant treatments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)